Research Governance Toolkit The journey thus far Bill Karanatsios 20 May 2010.

Upload

trinhthuanCategory

view

214download

0

CELENT MODEL BANK 2015 PART 2: CASE STUDIES OF OMNICHANNEL BANKING

Bob Meara March 2015

This is an authorized reprint from a Celent report profiling Model Bank initiatives. This excerpt was prepared for Infosys, but the analysis has not been changed. For more information about the full report see www.celent.com.

CONTENTS

Case Studies in Omnichannel Banking ............................................................................... 1

Standard Bank of South Africa: Guided Sales Workbench ............................................. 1

Leveraging Celent’s Expertise ............................................................................................ 6

Support for Financial Institutions ..................................................................................... 6

Support for Vendors ........................................................................................................ 6

Related Celent Research .................................................................................................... 7

CASE STUDIES IN OMNICHANNEL BANKING

STANDARD BANK OF SOUTH AFRICA: GUIDED SALES WORKBENCH Established in 1862, Standard Bank of British South Africa has grown into Standard Bank Group, the largest African bank group by assets and earnings, with total assets of R1.5 trillion (US$183 billion) and approximately 49,000 employees. Standard Bank of South Africa, one of Standard Bank Group’s subsidiaries, is joined by Stanbic IBTC, Standard International Holdings, and Liberty Holdings. The bank now known as Standard Bank was formed in 1962 as a South African subsidiary of Standard Bank Group, under the name Standard Bank of South Africa. It operates in South Africa and 17 countries in sub-Saharan Africa, offering personal, business and commercial banking, corporate and investment banking, and wealth management services.

Table 1: Standard Bank of South Africa Snapshot

THROUGH 12/31/2014 STANDARD BANK OF SOUTH AFRICA

YEAR FOUNDED 1862

COMPANY SIZE 49,000 employees

US$162 billion assets

15.5 million personal banking clients in Africa

Countries: 20

HQ LOCATION Johannesburg, South Africa

CHANNEL COVERAGE 1,283 branches throughout 18 African countries

9,300 ATMs

Internet, mobile and call center

Source: Standard Bank of South Africa

Standard Bank transformed its sales force through deploying a comprehensive Guided Sales Workbench on mobile tablets alongside business process redesign without a rip-and-replace of legacy systems. It has done so supporting Personal and Private Banking lines of business, as well as Business Banking and Offshore. Prior to the rollout of the mobile sales force application, Standard Bank had no capability to support proactive acquisition of customers remotely.

Opportunity Many sub-Saharan markets in which Standard Bank operates are characterized by dense urban population centers separated by wide areas of low-income, rural, transportation-challenged populations (see Figure 1 on Page 2). These characteristics limit the effectiveness of retail branch and ATM network coverage beyond urban and suburban markets, while increasing the importance of remote sales operations.

Chapte

r: C

ase

Stu

die

s in O

mnic

hann

el B

ankin

g

2

Figure 1: Standard Bank Enjoys a Substantial Sub-Saharan Footprint

Source: Standard Bank of South Africa

Remote sales operations have been challenging, in part, because systems and workflow supporting selling and acquiring was historically paper based. Sales Agents had to hand-deliver documents to Head Office, Branch Fulfillment Centers, or Operations Processing Centers for fulfillment. The key challenges in this approach were:

1. The process relied heavily on the Sales Agent’s knowledge and experience with the various products available across multiple customer segments. This introduced a great deal of variability.

2. The lack of broad based proactive understanding of customer’s needs resulted in inconsistent cross-selling of products and higher selling costs.

3. Most compliance-related issues were noticed during fulfillment due to incomplete capture of information or lack of enforcement in the physical (paper-based) forms. This in turn resulted in multiple visits to the customer leading to poor customer experience, lower productivity, and higher turnaround time (TAT).

Chapte

r: C

ase

Stu

die

s in O

mnic

hann

el B

ankin

g

3

With this opportunity, Standard Bank sought to be the first bank to roll out a mobile salesforce application in Africa. In so doing, it meant to equip its sales force with the right tools and support materials to engage customers professionally in order to maximize sales opportunities at first customer contact, improving sales results while providing a superior customer experience. Standard Bank’s secondary objectives were to minimize the administrative burden through automated data capture and improved compliance.

Sales & Service Enablement Standard Bank developed a framework designed to deliver a superior and consistent customer experience. Sales & Service Enablement is a strategic, ongoing process adopted by Standard Bank to equip customer-facing employees with the ability to consistently and systematically have valuable conversations with appropriate customer stakeholders at each stage of the customer’s problem-solving lifecycle in order to optimize the return of investment. The framework directs both the selling process (Figure 2) and the sales management process.

Figure 2: Standard Bank’s Sales & Service Enablement Framework

Source: Standard Bank of South Africa

The challenge was to equip Standard Bank’s mobile sales force with the tools necessary to deliver this objective.

Solution The Sales Force Enablement Application is a native iPad application developed using Objective C and Xcode IDE. Both Sales Agents and customers interact with the application and benefit from a guided sales process.

The Customer's private and confidential information captured during the guided sales process is stored securely in iPad's local SQLite Database. This information is encrypted using “AES 128 bit” algorithm and is purged once the completed application forms are sent for fulfillment, improving security.

Subversion (SVN) is used for configuration management during development. The installable file (ipa) is generated using Standard Bank's provisioning profile, and the final build is uploaded onto the Amazon Cloud for each country.

Using this solution, the remote sales force can complete all required documentation and necessary customer details, including electronic signatures, in a single meeting.

Chapte

r: C

ase

Stu

die

s in O

mnic

hann

el B

ankin

g

4

Application forms are then automatically compressed into PDF format and emailed for processing, with copies also emailed to the customer for record-keeping. This approach, while not technically elegant, allowed Standard Bank to roll out the application in quick fashion with minimal legacy system integration and without needing to rip-and-replace. This hastened the availability of the application and accelerated project payback.

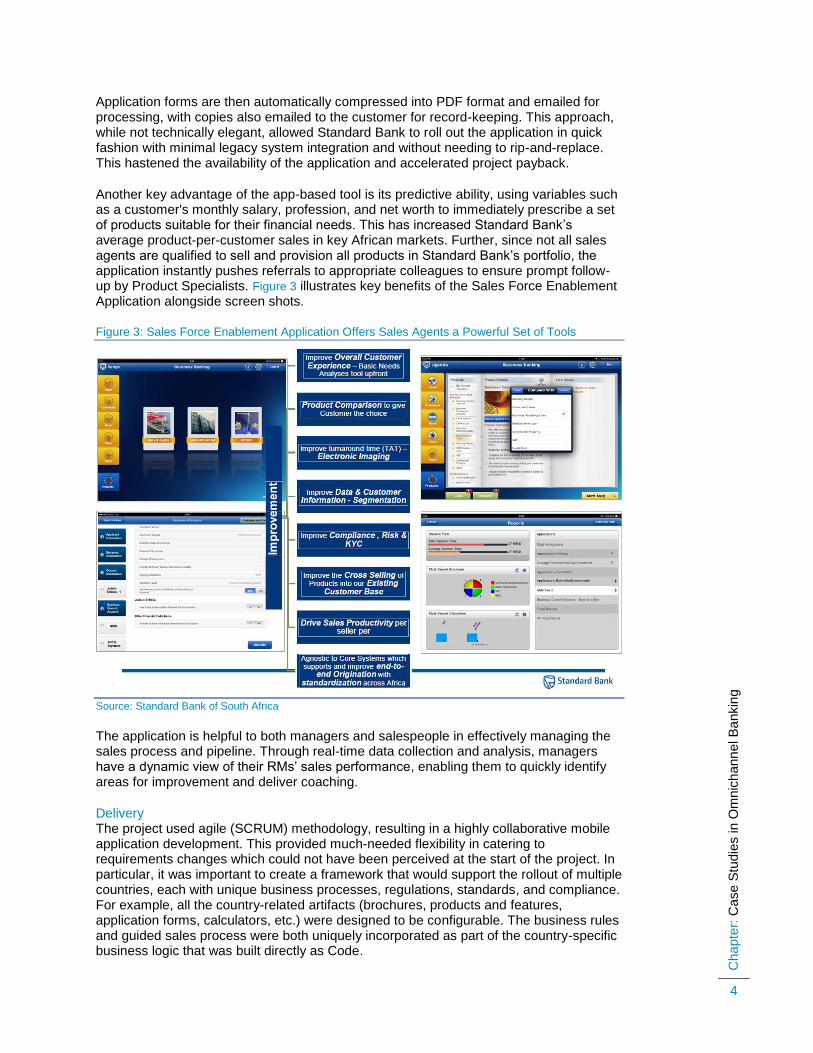

Another key advantage of the app-based tool is its predictive ability, using variables such as a customer's monthly salary, profession, and net worth to immediately prescribe a set of products suitable for their financial needs. This has increased Standard Bank’s average product-per-customer sales in key African markets. Further, since not all sales agents are qualified to sell and provision all products in Standard Bank’s portfolio, the application instantly pushes referrals to appropriate colleagues to ensure prompt follow-up by Product Specialists. Figure 3 illustrates key benefits of the Sales Force Enablement Application alongside screen shots.

Figure 3: Sales Force Enablement Application Offers Sales Agents a Powerful Set of Tools

Source: Standard Bank of South Africa

The application is helpful to both managers and salespeople in effectively managing the sales process and pipeline. Through real-time data collection and analysis, managers have a dynamic view of their RMs’ sales performance, enabling them to quickly identify areas for improvement and deliver coaching.

Delivery The project used agile (SCRUM) methodology, resulting in a highly collaborative mobile application development. This provided much-needed flexibility in catering to requirements changes which could not have been perceived at the start of the project. In particular, it was important to create a framework that would support the rollout of multiple countries, each with unique business processes, regulations, standards, and compliance. For example, all the country-related artifacts (brochures, products and features, application forms, calculators, etc.) were designed to be configurable. The business rules and guided sales process were both uniquely incorporated as part of the country-specific business logic that was built directly as Code.

Chapte

r: C

ase

Stu

die

s in O

mnic

hann

el B

ankin

g

5

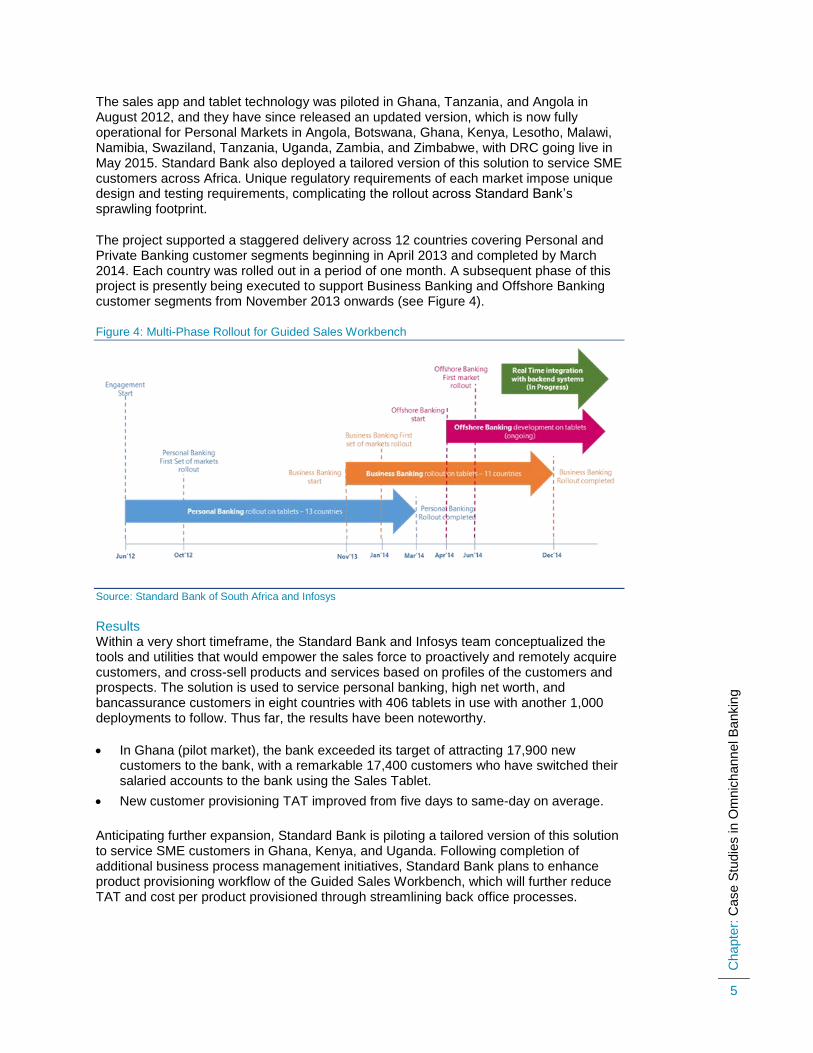

The sales app and tablet technology was piloted in Ghana, Tanzania, and Angola in August 2012, and they have since released an updated version, which is now fully operational for Personal Markets in Angola, Botswana, Ghana, Kenya, Lesotho, Malawi, Namibia, Swaziland, Tanzania, Uganda, Zambia, and Zimbabwe, with DRC going live in May 2015. Standard Bank also deployed a tailored version of this solution to service SME customers across Africa. Unique regulatory requirements of each market impose unique design and testing requirements, complicating the rollout across Standard Bank’s sprawling footprint.

The project supported a staggered delivery across 12 countries covering Personal and Private Banking customer segments beginning in April 2013 and completed by March 2014. Each country was rolled out in a period of one month. A subsequent phase of this project is presently being executed to support Business Banking and Offshore Banking customer segments from November 2013 onwards (see Figure 4).

Figure 4: Multi-Phase Rollout for Guided Sales Workbench

Source: Standard Bank of South Africa and Infosys

Results Within a very short timeframe, the Standard Bank and Infosys team conceptualized the tools and utilities that would empower the sales force to proactively and remotely acquire customers, and cross-sell products and services based on profiles of the customers and prospects. The solution is used to service personal banking, high net worth, and bancassurance customers in eight countries with 406 tablets in use with another 1,000 deployments to follow. Thus far, the results have been noteworthy.

In Ghana (pilot market), the bank exceeded its target of attracting 17,900 new customers to the bank, with a remarkable 17,400 customers who have switched their salaried accounts to the bank using the Sales Tablet.

New customer provisioning TAT improved from five days to same-day on average.

Anticipating further expansion, Standard Bank is piloting a tailored version of this solution to service SME customers in Ghana, Kenya, and Uganda. Following completion of additional business process management initiatives, Standard Bank plans to enhance product provisioning workflow of the Guided Sales Workbench, which will further reduce TAT and cost per product provisioned through streamlining back office processes.

Chapte

r: L

evera

gin

g C

ele

nt’s E

xpert

ise

6

LEVERAGING CELENT’S EXPERTISE

If you found this report valuable, you might consider engaging with Celent for custom analysis and research. Our collective experience and the knowledge we gained while working on this report can help you streamline the creation, refinement, or execution of your strategies.

SUPPORT FOR FINANCIAL INSTITUTIONS Typical projects we support include:

Vendor short listing and selection. We perform discovery specific to you and your business to better understand your unique needs. We then create and administer a custom RFI to selected vendors to assist you in making rapid and accurate vendor choices.

Business practice evaluations. We spend time evaluating your business processes. Based on our knowledge of the market, we identify potential process or technology constraints and provide clear insights that will help you implement industry best practices.

IT and business strategy creation. We collect perspectives from your executive team, your front line business and IT staff, and your customers. We then analyze your current position, institutional capabilities, and technology against your goals. If necessary, we help you reformulate your technology and business plans to address short-term and long-term needs.

SUPPORT FOR VENDORS We provide services that help you refine your product and service offerings. Examples include:

Product and service strategy evaluation. We help you assess your market position in terms of functionality, technology, and services. Our strategy workshops will help you target the right customers and map your offerings to their needs.

Market messaging and collateral review. Based on our extensive experience with your potential clients, we assess your marketing and sales materials—including your website and any collateral.

Chapte

r: R

ela

ted C

ele

nt R

esearc

h

7

RELATED CELENT RESEARCH

Celent Model Bank 2015: Part 1: Case Studies of Digital Banking March 2015

Celent Model Bank 2015: Part 3: Case Studies of Innovation and Emerging Technology March 2015

Celent Model Bank 2015: Part 4: Case Studies of Legacy & Ecosystem Transformation March 2015

Celent Model Bank 2015: Part 5: Case Studies of Payments Innovation March 2015

How One Bank Changed a Nation: A Case Study of Commercial Bank of Africa’s M-Shwari Initiative May 2014

Celent Model Bank 2014: Part 1: Case Studies of Digital and Omnichannel Banking April 2014

Celent Model Bank 2014: Part 2: Case Studies of Innovation and Emerging Technology April 2014

Celent Model Bank 2014: Part 3: Case Studies of Legacy & Ecosystem Transformation April 2014

Celent Model Bank 2014: Part 4: Case Studies of Payments Innovation April 2014

Celent Model Bank 2014: Part 5: Case Studies of Innovation in Cash Management April 2014

Celent Model Bank 2013: Case Studies of Effective Use of Technology in Banking February 2013

Celent Model Bank 2012: Case Studies of Effective Use of Technology in Banking June 2012

Celent Model Bank 2011: Case Studies of Effective Use of Technology in Banking May 2011

Celent Model Bank 2010: Case Studies of Effective Use of Technology in Banking May 2010

Celent Model Bank 2009: Case Studies of Effective Use of Technology in Banking May 2009

Celent Model Bank 2008: Case Studies of Effective Use of Technology in Banking March 2008

Chapte

r: R

ela

ted C

ele

nt R

esearc

h

8

Copyright Notice

Prepared by

Celent, a division of Oliver Wyman, Inc.

Copyright © 2015 Celent, a division of Oliver Wyman, Inc. All rights reserved. This report may not be reproduced, copied or redistributed, in whole or in part, in any form or by any means, without the written permission of Celent, a division of Oliver Wyman (“Celent”) and Celent accepts no liability whatsoever for the actions of third parties in this respect. Celent and any third party content providers whose content is included in this report are the sole copyright owners of the content in this report. Any third party content in this report has been included by Celent with the permission of the relevant content owner. Any use of this report by any third party is strictly prohibited without a license expressly granted by Celent. Any use of third party content included in this report is strictly prohibited without the express permission of the relevant content owner This report is not intended for general circulation, nor is it to be used, reproduced, copied, quoted or distributed by third parties for any purpose other than those that may be set forth herein without the prior written permission of Celent. Neither all nor any part of the contents of this report, or any opinions expressed herein, shall be disseminated to the public through advertising media, public relations, news media, sales media, mail, direct transmittal, or any other public means of communications, without the prior written consent of Celent. Any violation of Celent’s rights in this report will be enforced to the fullest extent of the law, including the pursuit of monetary damages and injunctive relief in the event of any breach of the foregoing restrictions.

This report is not a substitute for tailored professional advice on how a specific financial institution should execute its strategy. This report is not investment advice and should not be relied on for such advice or as a substitute for consultation with professional accountants, tax, legal or financial advisers. Celent has made every effort to use reliable, up-to-date and comprehensive information and analysis, but all information is provided without warranty of any kind, express or implied. Information furnished by others, upon which all or portions of this report are based, is believed to be reliable but has not been verified, and no warranty is given as to the accuracy of such information. Public information and industry and statistical data, are from sources we deem to be reliable; however, we make no representation as to the accuracy or completeness of such information and have accepted the information without further verification.

Celent disclaims any responsibility to update the information or conclusions in this report. Celent accepts no liability for any loss arising from any action taken or refrained from as a result of information contained in this report or any reports or sources of information referred to herein, or for any consequential, special or similar damages even if advised of the possibility of such damages.

There are no third party beneficiaries with respect to this report, and we accept no liability to any third party. The opinions expressed herein are valid only for the purpose stated herein and as of the date of this report.

No responsibility is taken for changes in market conditions or laws or regulations and no obligation is assumed to revise this report to reflect changes, events or conditions, which occur subsequent to the date hereof.

For more information please contact [email protected] or:

Bob Meara [email protected]

AMERICAS EUROPE ASIA

USA

200 Clarendon Street, 12th Floor Boston, MA 02116

Tel.: +1.617.262.3120 Fax: +1.617.262.3121

France

28, avenue Victor Hugo Paris Cedex 16 75783

Tel.: +33.1.73.04.46.20 Fax: +33.1.45.02.30.01

Japan

The Imperial Hotel Tower, 13th Floor 1-1-1 Uchisaiwai-cho Chiyoda-ku, Tokyo 100-0011

Tel: +81.3.3500.3023 Fax: +81.3.3500.3059

USA

1166 Avenue of the Americas New York, NY 10036

Tel.: +1.212.541.8100 Fax: +1.212.541.8957

United Kingdom

55 Baker Street London W1U 8EW

Tel.: +44.20.7333.8333 Fax: +44.20.7333.8334

China

Beijing Kerry Centre South Tower, 15th Floor 1 Guanghua Road Chaoyang, Beijing 100022

Tel: +86.10.8520.0350 Fax: +86.10.8520.0349

USA

Four Embarcadero Center, Suite 1100 San Francisco, CA 94111

Tel.: +1.415.743.7900 Fax: +1.415.743.7950

Italy

Galleria San Babila 4B Milan 20122

Tel.: +39.02.305.771 Fax: +39.02.303.040.44

China

Central Plaza, Level 26 18 Harbour Road, Wanchai Hong Kong

Tel.: +852.2982.1971 Fax: +852.2511.7540

Brazil

Av. Doutor Chucri Zaidan, 920 – 4º andar Market Place Tower I São Paulo SP 04578-903

Tel.: +55.11.5501.1100 Fax: +55.11.5501.1110

Canada

1981 McGill College Avenue Montréal, Québec H3A 3T5

Tel.: +1.514.499.0461

Spain

Paseo de la Castellana 216 Pl. 13 Madrid 28046

Tel.: +34.91.531.79.00 Fax: +34.91.531.79.09

Switzerland

Tessinerplatz 5 Zurich 8027

Tel.: +41.44.5533.333

Singapore

8 Marina View #09-07 Asia Square Tower 1 Singapore 018960

Tel.: +65.9168.3998 Fax: +65.6327.5406

South Korea

Youngpoong Building, 22nd Floor 33 Seorin-dong, Jongno-gu Seoul 110-752 Tel.: +82.10.3019.1417 Fax: +82.2.399.5534

![Amaranth Lessons Thus Far - EDHEC-Risk Institute · “Amaranth Lessons Thus Far” ... [Natural gas] traders … make complex wagers on gas at multiple points in the future, betting,](https://static.fdocuments.us/doc/165x107/5f0620077e708231d4166a7d/amaranth-lessons-thus-far-edhec-risk-institute-aoeamaranth-lessons-thus-fara.jpg)