Celebrating our 30th Anniversary in 2017 · Anniversary in 2017 Putting people before profi t. I am...

7

Celebrating our 30th Anniversary in 2017 Putting people before profit

-

Upload

duongthuan -

Category

Documents

-

view

215 -

download

0

Transcript of Celebrating our 30th Anniversary in 2017 · Anniversary in 2017 Putting people before profi t. I am...

Celebrating our 30th Anniversary in 2017

Putting people before profi t

I am proud that Leeds Credit Union is celebrating its 30th Anniversary this year. Leeds Credit Union demonstrates that there is a clear credit union difference. We are different from high-cost lenders on the one hand, and shareholder-led interests of the big banks on the other, by truly putting our members first. We still hold a place of trust with our members and our mutual, educational and volunteer principles set credit unions apart.

From small beginnings 30 years ago, Leeds Credit Union has become a pioneer in its field. Over the years we have united with a number of other credit unions in Leeds to be one of the first to have a city-wide field of membership. More recently White Rose Credit Union merged with Leeds Credit Union so that we now cover Wakefield too. We now also extend across the Harrogate and Craven local authority areas.

Among a wide range of creative approaches, we have grasped the opportunities presented by the credit union Legislative Reform Order to extend our common bond. This has allowed us to develop key partnerships at a national as well as a local basis, and to enter enterprise lending.

I am extremely proud that we have a skilled and commercially minded Board and Senior Management team that has delivered on its promises consistently over the last eight years. This proven track record demonstrates a sound foundation on which to build, a foundation made all the stronger by our marvellous staff group, whose commitment is extraordinary.

This briefing summarises the achievements of Leeds Credit Union. More importantly it indicates our longer term strategy and vision to grow and become an even more significant financial social enterprise and community bank. We know we can do more to deliver ethical, locally-rooted services to support our members, in a way that only a credit union can deliver. Through growth we will also develop new employment opportunities across a range of skills.

Looking to the future, challenges will remain in providing vital loans and savings services, in helping those who struggle to repay loans with budgeting support and repayment plans, in keeping pace with the march of technology, and matching the speed of the competition. It is only by meeting these challenges head on that our credit union and our members will continue to prosper.

Isobel Mills CBE, President

Vision needs a practical application if it is to matter.

We benchmark our operational performance against other major credit unions. We pay close attention to key banking ratios such as the cost income ratio. We monitor innovation and developments wider than the credit union world alone.

At the member level we monitor the quality of service we provide; we have welcomed the independent reviews of our performance undertaken by partners.

Our operational goals are stretching. Our aspiration to be the best credit union in the UK is a challenge, though by these words we actually mean rather more. That is, what it will take for us to be an even more material financial services provider in the wider highly competitive environment.

We have tremendous partners. Our Local Authorities and Housing Association partners really care about Citizens and residents and their financial well-being. Our employer partners are dedicated in helping their employees to save. Together with activists, volunteers and straightforward enthusiasts they all play a fantastic part in the practical delivery of credit union services in the many communities that we serve.

Within our operation we have an ‘Achieving Excellence’ programme for every member of staff, our Investor in People accreditation has recently been reaffirmed and we are a Living Wage accredited employer.

In systems and processes we are constantly refining the tools we have and seeking new ways of working. In the current programme we have a range of exciting developments ranging from the mundane but important to the strategic.

All this means I am confident that Leeds Credit Union financial services for the benefit of our existing members and those who join in the future.

Chris Smyth, Chief Executive

Foreword Foreword

From small beginnings 30 years ago, Leeds Credit Union has become a pioneer in its field.

This briefing summarises the achievements of Leeds Credit Union. More importantly it indicates our longer term determination to grow and become an even more significant financial social enterprise and community bank.

Our values • Affordable credit

• Savings and thrift

• Care of members’ money

• Education

• Alleviation of poverty

Our highlights• Spectacular business turnaround

• Year on year growth

• Doing what we say – track record of achievement

• First class governance

• Exceeding regulatory ratios

• Successful integration of Wakefi eld Credit Union

• Winning new partners

Our challenges • Growth

• Awareness

• Old systems

• Pace of competition and speed of digital media developments in banking

Our products Savings• Instant Access Account

• High Balance Savings Account

• Young Savers Account

• Christmas Club Account

• Interactive website

Transactions • Pre-paid Visa Card

• Budget Account

• Online banking

Loans• Personal Loans from £250 to £20k

• Business Loans

£11mloans

9branches

£16mdeposits

50staff

36kmembers

£20massets

Channels

Telephone Mobile Online Post Branch

Key factsOur impact over the last 10 years

£265mcash issued viaour community

branches

110,000loans issued

£92mworth of loans

issued

£47minterest saved to the community*

Every £1 spent on financial

inclusion work

is worth £9for the

community**

Ourimpact in

the last10 years

alone

*The saving that credit union borrowers make when compared to the higher interest rate of a principal doorstep lender (some high-cost lenders’ interest rates are considerably higher) and assumes this saving has been achieved on 75% of the Credit Union’s lending.

**Research by Salford University for Leeds City Council 2009.

What makes us different? • Mutuality

• Member owned

• Community focused

• No shareholders with special privileges

• Educational aim

Our savings: • Straightforward and fair

Our Loans: • Affordable

• We will never add to unmanageable debt

• No hidden charges

Our aims by 2020 • Reach a wider audience – to be the

institution of choice for 5% of the Leeds and Wakefi eld population

• Increase dividend

• Build on fi nancial soundness so we can invest in delivering better services

• Increase choice in retail fi nancial services

Our vision: to be thebest community credit union in the UK Our members

Lancashire

North East

Midlands

E. Anglia

South West

South West SouthSouth East

Scotland

N. Ireland

Wales

Yorkshire

London

Leeds Credit Union currently has over

36,000 members located throughout the UK

GreenDeal

Schemes

ProjectInnovation

Centre

Wakefield

BusinessLending

Employment

Harrogate& Craven

Employer Savings

Schemes

Housing Solutions

Flexibility and Cap

ability

Products and Services

Pro

cess

and

Pla

tform

DevelopingKey

Partners

Developing the Core

LEEDS &WAKEFIELD

Social Return on

Investment

How we will get there

Leeds Credit Union 72.6%Co-op Bank 69%

Santander Bank 62%

Lloyds Bank 59%

Barclays Bank 58%

HSBC Bank 56%

Royal Bank of Scotland (RBS) 54%

Overall industry average 65%

Member satisfaction

Leeds Credit Union results from Affinity Sutton Group survey of members summer 2016.

Bank results from Which? survey December 2016.

Members also say:

83.5%are likely/very likely to recommend Leeds Credit Union

61.4%have already recommended the credit union

81.9%rated Leeds Credit Union service as good/very good

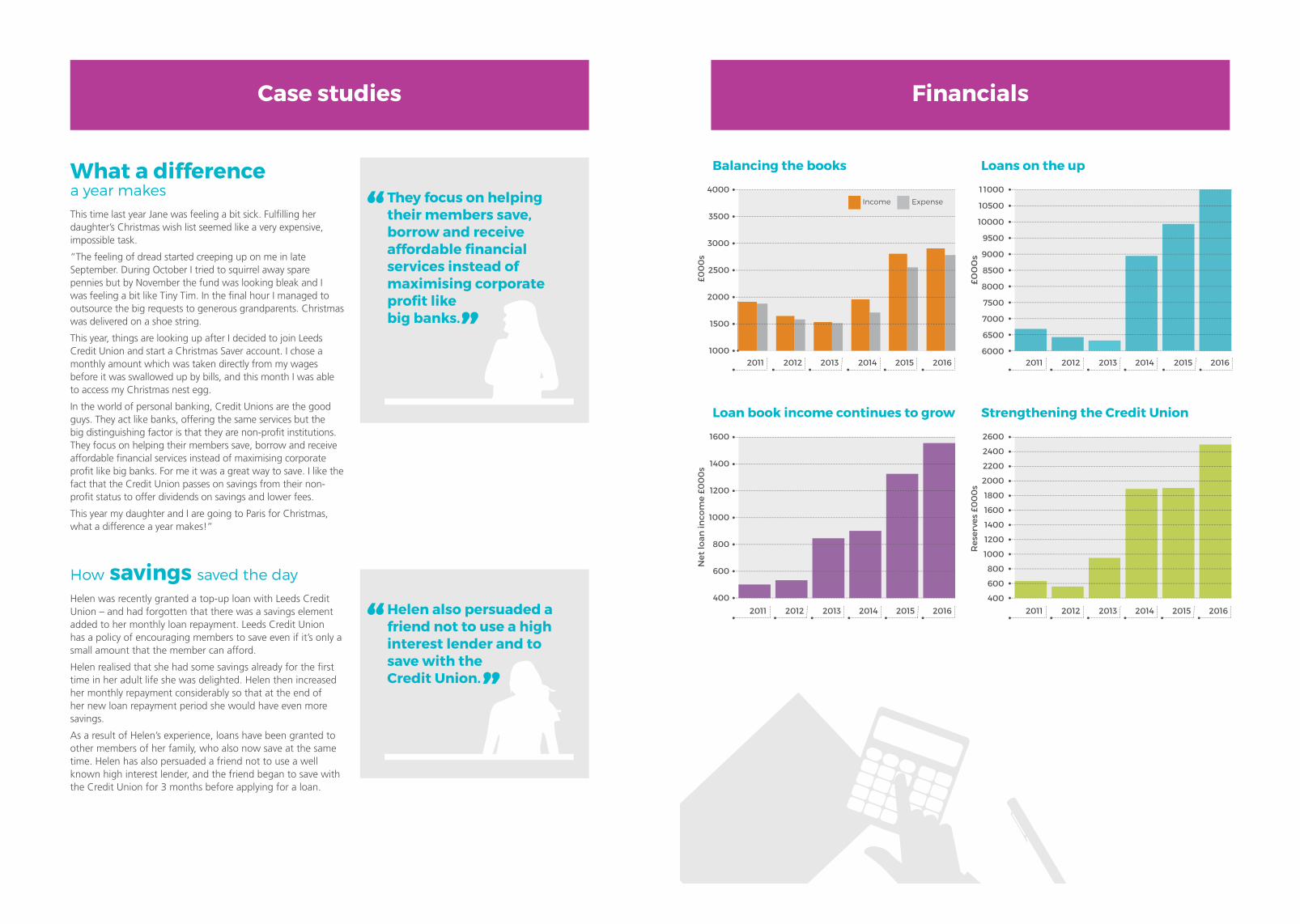

“ They focus on helping their members save, borrow and receive affordable fi nancial services instead of maximising corporate profi t like big banks.”

“ Helen also persuaded a friend not to use a high interest lender and to save with the Credit Union.”

What a differencea year makes This time last year Jane was feeling a bit sick. Fulfilling her daughter’s Christmas wish list seemed like a very expensive, impossible task.

“The feeling of dread started creeping up on me in late September. During October I tried to squirrel away spare pennies but by November the fund was looking bleak and I was feeling a bit like Tiny Tim. In the final hour I managed to outsource the big requests to generous grandparents. Christmas was delivered on a shoe string.

This year, things are looking up after I decided to join Leeds Credit Union and start a Christmas Saver account. I chose a monthly amount which was taken directly from my wages before it was swallowed up by bills, and this month I was able to access my Christmas nest egg.

In the world of personal banking, Credit Unions are the good guys. They act like banks, offering the same services but the big distinguishing factor is that they are non-profit institutions. They focus on helping their members save, borrow and receive affordable financial services instead of maximising corporate profit like big banks. For me it was a great way to save. I like the fact that the Credit Union passes on savings from their non-profit status to offer dividends on savings and lower fees.

This year my daughter and I are going to Paris for Christmas, what a difference a year makes!”

How savings saved the day Helen was recently granted a top-up loan with Leeds Credit Union – and had forgotten that there was a savings element added to her monthly loan repayment. Leeds Credit Union has a policy of encouraging members to save even if it’s only a small amount that the member can afford.

Helen realised that she had some savings already for the first time in her adult life she was delighted. Helen then increased her monthly repayment considerably so that at the end of her new loan repayment period she would have even more savings.

As a result of Helen’s experience, loans have been granted to other members of her family, who also now save at the same time. Helen has also persuaded a friend not to use a well known high interest lender, and the friend began to save with the Credit Union for 3 months before applying for a loan.

Case studies Financials

Loan book income continues to grow

1400

1600

1200

1000

800

600

400

Net

loan

inco

me

£00

0s

2011 2012 2013 2014 2015 2016

2015 2016

£00

0s

2014

Loans on the up

6500

6000

7000

7500

8000

8500

9000

9500

10000

1 1000

10500

2011 2012 2013

Strengthening the Credit Union

2600

1800

2000

2200

2400

1200

1600

1000

1400

800

600

400

Res

erve

s £0

00

s

2011 2012 2013 2014 2015 2016

2014 2015 201620132011 2012

Balancing the books

3500

4000

3000

2500

2000

1500

1000

£00

0s

Income Expense

1997 We become a community credit union, opening our doors to everyone living or working in the local authority area. We now operate in 9 branches across Leeds, Wakefi eld, Harrogate and Craven with a number of additional information points across the district.

2007 Leeds City Credit Union wins the Social Enterprise of the Year Award at the annual awards event for Yorkshire and Humber. We gain Investor in People accreditation and become a living wage employer in 2016.

2012 We take advantage of new credit union powers which allow us to have multiple common bonds. We win the business of a number of corporate partners increasing our membership numbers.

2014 The fi rst Your Loan Shop opens in Leeds, giving us a high street presence to help combat high-interest lenders. White Rose Credit Union merges with Leeds City Credit Union extending our common bond into Wakefi eld and substantially increasing our membership.

2015Following the merger with White Rose we extend our common bond into North Yorkshire with Harrogate and Craven.

2016 We refi ne our visual identity, shorten our name to Leeds Credit Union and upgrade our online presence and back offi ce systems.

We launch an online system to support our free school savings club to raise the importance of saving. We now operate in 38 schools across the district.

2017 We celebrate our 30th year.

2016. 2014 The fi rst opens in Leeds, giving us a high street presence to help combat high-interest lenders. White Rose Credit Union merges with Leeds City Credit Union extending our common bond into Wakefi eld and substantially increasing our membership.

new credit union powers

multiple common bonds. 2015new credit union powers

August 1987 Originally operating from a broom cupboard in Leeds Civic Hall, the credit union began life as the Leeds City Council Employees Credit Union, offering savings and loans to local authority staff.

A brief history How you can help

By investing – for philanthropists, partners and businesses

By saving – by individuals

By encouraging others to save – by opening staff savings schemes

By partnering – in any way to use our services

By infl uencing – Government and others

By volunteering

By spreading the word – via journalists, commentators, Twitter and Facebook followers (fi nd us at @leedscredunion on Twitter and search Leeds Credit Union on Facebook)

By getting in touch today – to discuss any of these opportunities email us at [email protected]

Leeds Credit Union is on a journey. If you would like to take part in making Leeds Credit Union an even more signifi cant fi nancial social enterprise and community bank, offering a real alternative and additional choice on the high street, then here are some ways to be involved:

Leeds Credit Union, Westminster Buildings, 31 New York Street, Leeds LS2 7DTTel: 0113 242 [email protected]

www.leedscreditunion.co.uk

Putting people before profit

and

are trading names of Leeds City Credit Union Ltd.

Leeds City Credit Union Ltd is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority – firm reference number 213369. This information may be checked by visiting www.fca.org.uk or www.bankofengland.co.uk/pra.