CEE Real Estate market outlook

16

CEE Real Estate market outlook | Mark Robinson February 2017

Transcript of CEE Real Estate market outlook

CEE Real Estate market outlook | Mark Robinson February 2017

Colliers International 20172

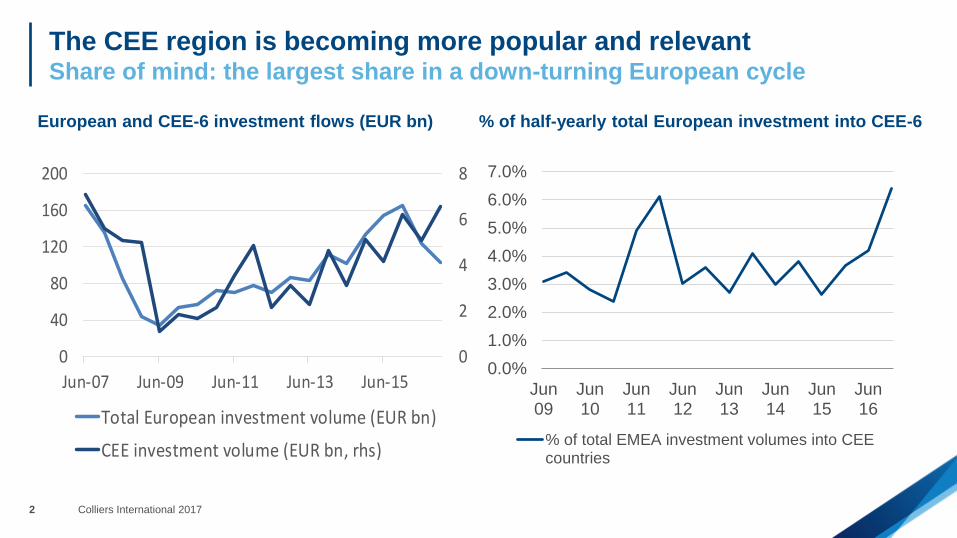

The CEE region is becoming more popular and relevantShare of mind: the largest share in a down-turning European cycle

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

Jun09

Jun10

Jun11

Jun12

Jun13

Jun14

Jun15

Jun16

% of total EMEA investment volumes into CEEcountries

% of half-yearly total European investment into CEE-6

0

2

4

6

8

0

40

80

120

160

200

Jun-07 Jun-09 Jun-11 Jun-13 Jun-15

Total European investment volume (EUR bn)

CEE investment volume (EUR bn, rhs)

European and CEE-6 investment flows (EUR bn)

Colliers International 20173

Investment state of play Hungary‘s investment volumes accelerating out of 2012-13 trough

4.7

3.8

1.7

0.87 0.850.26

0

1

2

3

4

5

Investment volumes into the region in 2016

(EUR bn)

Source: Real Capital Analytics, Colliers International, data as of 1 January 2017

1088

436

2103

755

364 305

660

122

361596 627

1687

0

500

1000

1500

2000

2500

Investment volumes in Hungary (EUR m)

Source: BRF, Colliers International

Colliers International 20174

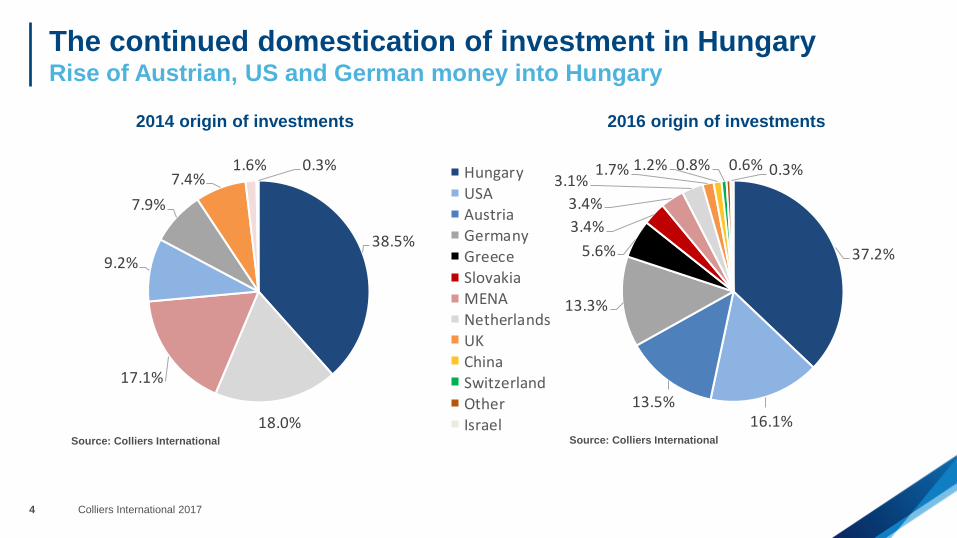

The continued domestication of investment in HungaryRise of Austrian, US and German money into Hungary

2014 origin of investments

Source: Colliers International

2016 origin of investments

Source: Colliers International

38.5%

18.0%

17.1%

9.2%

7.9%

7.4%1.6% 0.3%

37.2%

16.1%13.5%

13.3%

5.6%

3.4%

3.4%

3.1%1.7% 1.2% 0.8% 0.6% 0.3%Hungary

USAAustriaGermanyGreeceSlovakiaMENANetherlandsUKChinaSwitzerlandOtherIsrael

Colliers International 20175

Germany leads CEE – a steady ship, for nowLeading indicator of CEE economic sentiment with 4-month lag

German IFO Expectations survey and economic sentiment in CEE countries

Source: Bloomberg

70

80

90

100

110

120

German IFO Expectations subcomponent (lagged 4 months) CEE6 composite ESI sentiment indicator

Colliers International 20176

If CEE “is left alone”, future flows look promisingConsumers a leading indicator for likely investment volumes

Lagged composite consumer confidence versus investment volumes into CEE6

Source: Real Capital Analytics, Bloomberg, Colliers International

-48

-36

-24

-12

0

0

2

4

6

8

Jun-09 Jun-10 Jun-11 Jun-12 Jun-13 Jun-14 Jun-15 Jun-16 Jun-17 Jun-18

Investment into CEE6 real estate (EURbn)

EC composite consumer confidence for CE6 (18-month lagged, rhs)

?

Colliers International 20177

State of play with prime yields – still compressingQ4 2016 key sector capital city prime yields

Prime yields (compression vs Q3 2016 circled)

Source: Colliers International

4.85

6.50

5.25

6.50

7.50

9.00

6.25

8.25

6.50

7.75

9.00

11.00

5.00

6.25

5.255.75

7.00

8.50

0.00

2.00

4.00

6.00

8.00

10.00

12.00

Prague Budapest Warsaw Bratislava Bucharest Sofia

Office Industrial Retail TSC

Colliers International 20178

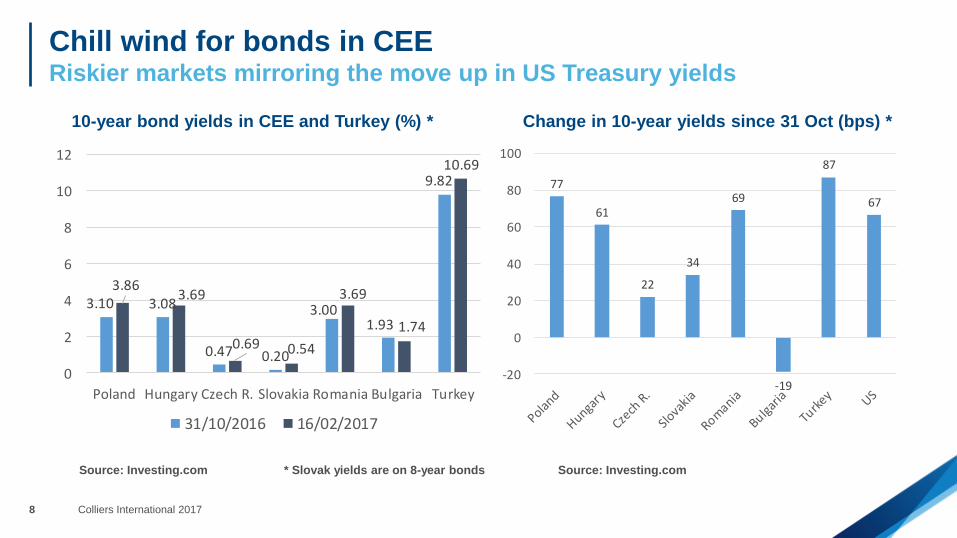

Chill wind for bonds in CEERiskier markets mirroring the move up in US Treasury yields

10-year bond yields in CEE and Turkey (%) * Change in 10-year yields since 31 Oct (bps) *

Source: Investing.com * Slovak yields are on 8-year bonds Source: Investing.com

3.10 3.08

0.47 0.20

3.001.93

9.82

3.863.69

0.69 0.54

3.69

1.74

10.69

0

2

4

6

8

10

12

Poland Hungary Czech R. Slovakia Romania Bulgaria Turkey

31/10/2016 16/02/2017

77

61

22

34

69

-19

87

67

-20

0

20

40

60

80

100

Colliers International 20179

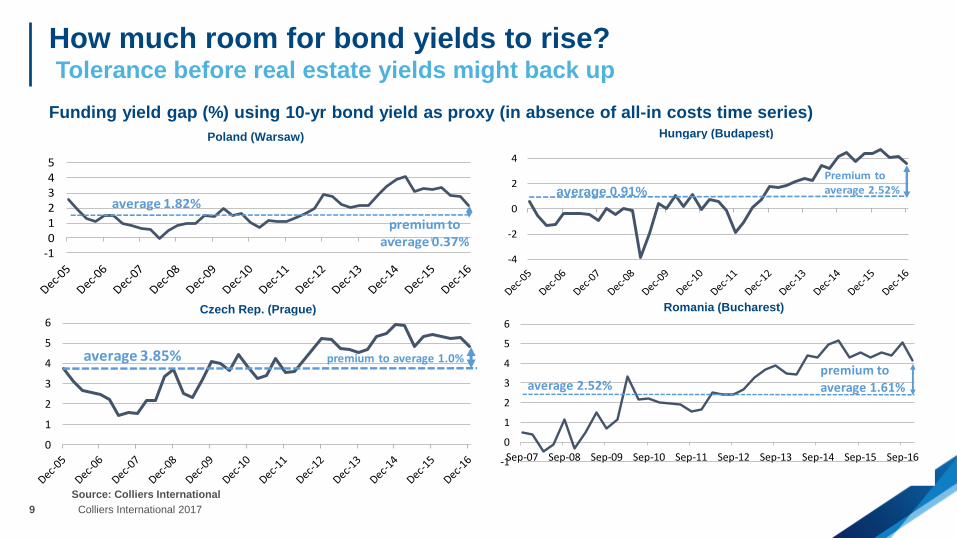

How much room for bond yields to rise?Tolerance before real estate yields might back up

Funding yield gap (%) using 10-yr bond yield as proxy (in absence of all-in costs time series)

Source: Colliers International

Czech Rep. (Prague)

Hungary (Budapest)

Romania (Bucharest)

Poland (Warsaw)

-4

-2

0

2

4

Premium to average 2.52%average 0.91%

-1012345

average 1.82%

premium to average 0.37%

0

1

2

3

4

5

6

average 3.85% premium to average 1.0%

-1

0

1

2

3

4

5

6

Sep-07 Sep-08 Sep-09 Sep-10 Sep-11 Sep-12 Sep-13 Sep-14 Sep-15 Sep-16

average 2.52%premium to average 1.61%

Colliers International 201710

Inputs to rents – Unemployment low, CPI risingTight labour markets and CPI picking up

Selected EU member unemployment rates (Nov 2016)

19.3%

11.7%10.2% 10.0% 9.4%

7.5%5.9% 5.7%

5.0% 4.9%4.1% 4.0%

0%

5%

10%

15%

20%

Source: Eurostat

Eurozone CPI and CEE-6 blended CPI (yoy, ave)

0.5%

-0.3% -0.2%

0.5%

2.2%

2.4%2.4%

1.5%

0.5%

0.2%

0.5%

2.5% 2.5%

2.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

2013 2014 2015 2016 2017E 2018E 2019ECEE-6 blended Eurozone

Boost to rents coming

Source: Oxford Economics, Colliers International

Colliers International 201711

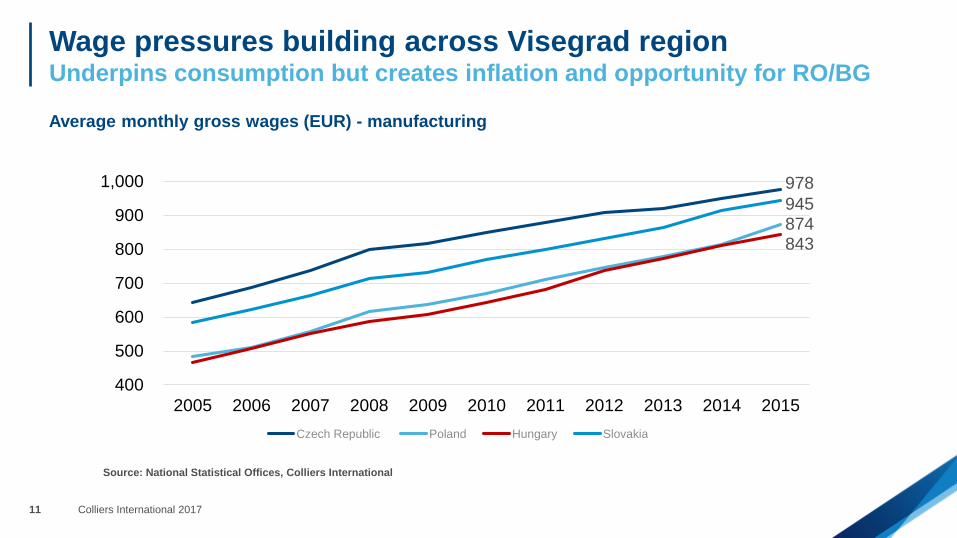

Wage pressures building across Visegrad regionUnderpins consumption but creates inflation and opportunity for RO/BG

Average monthly gross wages (EUR) - manufacturing

Source: National Statistical Offices, Colliers International

400

500

600

700

800

900

1,000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Czech Republic Poland Hungary Slovakia

978

945

843874

Colliers International 201712

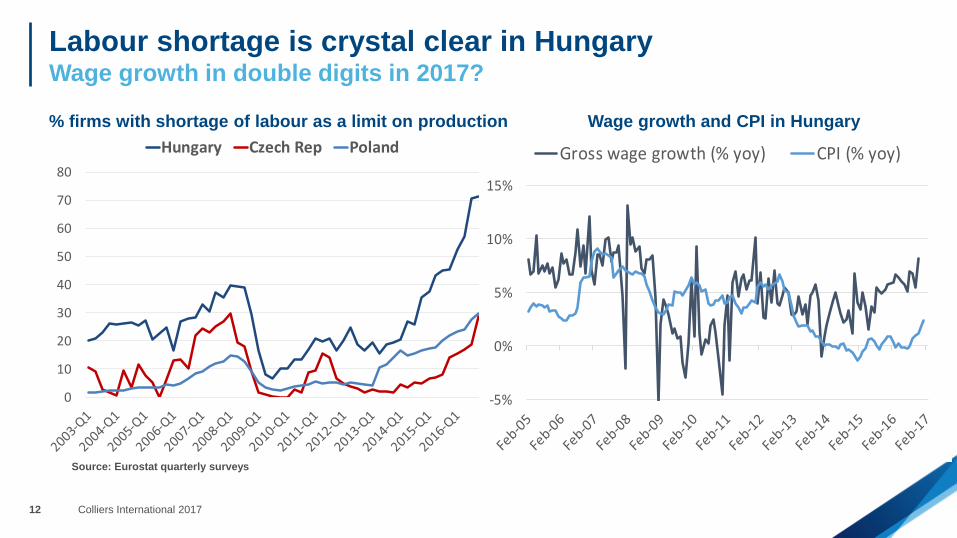

Labour shortage is crystal clear in HungaryWage growth in double digits in 2017?

% firms with shortage of labour as a limit on production

Source: Eurostat quarterly surveys

0

10

20

30

40

50

60

70

80

Hungary Czech Rep Poland

-5%

0%

5%

10%

15%

Gross wage growth (% yoy) CPI (% yoy)

Wage growth and CPI in Hungary

Colliers International 201713

Potential disrupter to CEE retail story in 2017Growth rates at 10%-20% in the region

% of people in 2015 shopping online in the last 12 months

Source: Factset

81%73%

65%

53% 50%45% 42%

37% 36%

26%18%

11%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Greater growth potential

Growth in e-commerce revenues

12% 12%13%

12%

17%

10%10% 10%

13%11%

16%

10%

0%

5%

10%

15%

20%

Bulgaria Czech Rep Hungary Poland Romania Slovakia

2015-16 growth 2016-17 growth

Source: Statista

Colliers International 201714

2017 outlookPositives and negatives

Negatives

• Continued momentum in consumption-led GDP growth

• Firming rents, especially in retail

• Wage growth positive for retail

• Fiscal expansion in most countries

• Inflation spike in EUR terms is not impossible to see (rent

linkage to CPI across the region)

• Appreciation of Czech Koruna as currency “cap” removed

• Effect of rate rises on CEE is not immediate

Positives

• Rates rising and risk of inflation spike and strong USD

• E-commerce risk for retail

• Wage growth negative for BPO/SSC and industrial

• EU funding reduces as punishment for populism or as

a result of EU political instability

• Taxation risk (the Trump-Brexit World)

• China debt instability spikes strong Developed Market

sentiment sending all risky asset prices tumbling

(including Emerging Markets)

• Trump unpredictability (trade wars?)

| Mark Robinson January 2017

THANK YOU

Colliers International 201716

Colliers International | Prague

Slovansky Dum

Na Prikope 859/22

Prague 1 11000

Czech Republic

TEL +420 226 536 618

Mark RobinsonCEE Research Specialist | Prague

+420 226 537 646