Cebit m krzyzanowski_atm_vs3

14

Warsaw as an emerging data center and connectivity hub in CEE Maciej Krzyżanowski, CEO ATM S.A.

-

Upload

alina-nedelcu -

Category

Documents

-

view

196 -

download

2

Transcript of Cebit m krzyzanowski_atm_vs3

Warsaw as an emerging data center

and connectivity hub in CEE

Maciej Krzyżanowski, CEO

ATM S.A.

Warsaw as an emerging data center

and connectivity hub in CEE

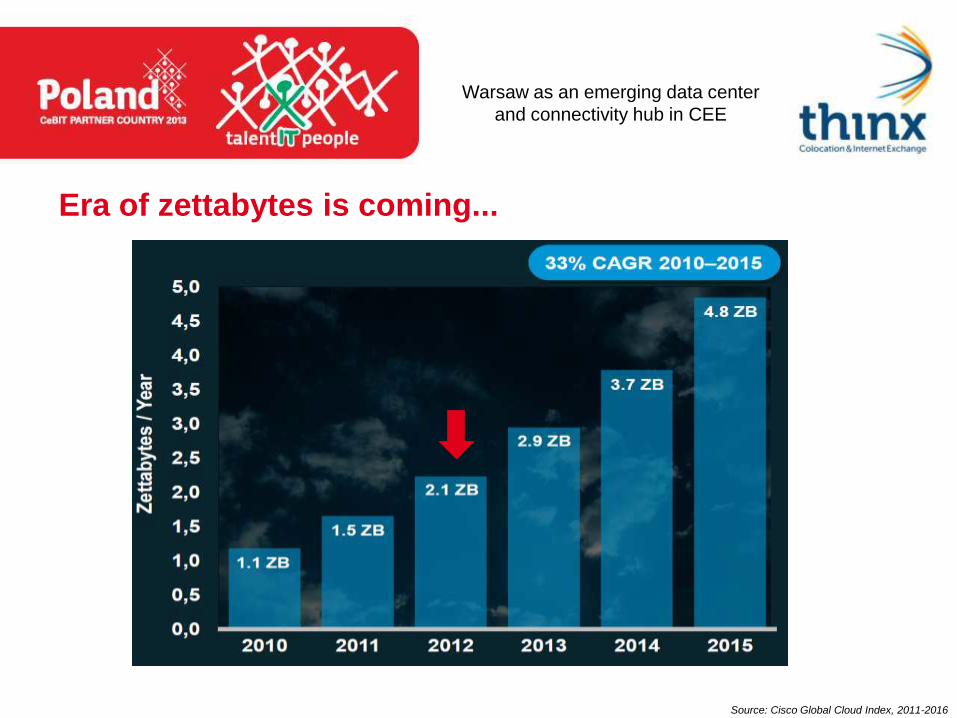

Era of zettabytes is coming...

Source: Cisco Global Cloud Index, 2011-2016

Warsaw as an emerging data center

and connectivity hub in CEE

How much is 4.8 zettabytes?

66.7 trillion hours of streaming music

at 160 kbps

4.8 trillion hours of online streaming

720p HD video

15.5 trillion hours of standard-definition

web conferencing

Warsaw as an emerging data center

and connectivity hub in CEE

Download speed across the regions

Source: Cisco Global Cloud Index, 2011-2016

Fixed download speed Mobile download speed

Warsaw as an emerging data center

and connectivity hub in CEE

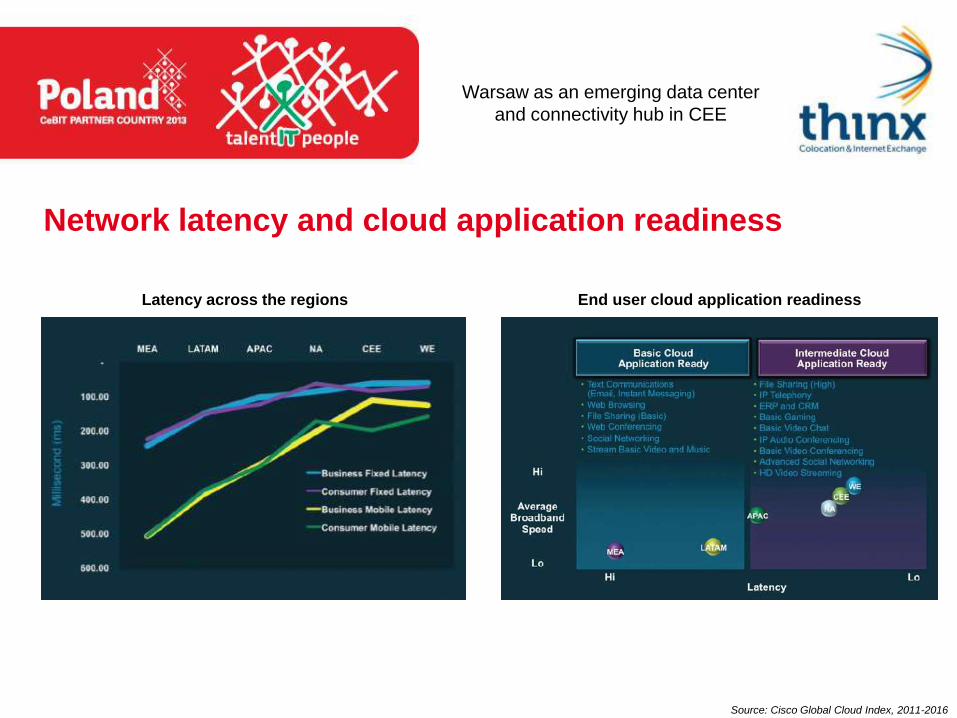

Network latency and cloud application readiness

Source: Cisco Global Cloud Index, 2011-2016

Latency across the regions End user cloud application readiness

Warsaw as an emerging data center

and connectivity hub in CEE

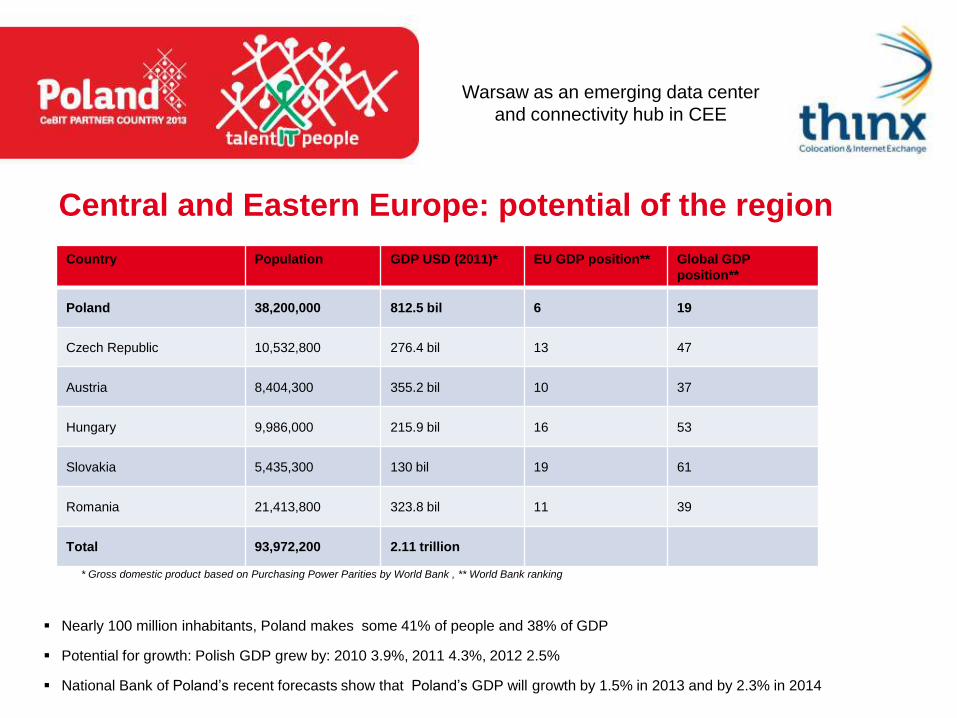

Central and Eastern Europe: potential of the region

Nearly 100 million inhabitants, Poland makes some 41% of people and 38% of GDP

Potential for growth: Polish GDP grew by: 2010 3.9%, 2011 4.3%, 2012 2.5%

National Bank of Poland’s recent forecasts show that Poland’s GDP will growth by 1.5% in 2013 and by 2.3% in 2014

Country Population GDP USD (2011)* EU GDP position** Global GDP

position**

Poland 38,200,000 812.5 bil 6 19

Czech Republic 10,532,800 276.4 bil 13 47

Austria 8,404,300 355.2 bil 10 37

Hungary 9,986,000 215.9 bil 16 53

Slovakia 5,435,300 130 bil 19 61

Romania 21,413,800 323.8 bil 11 39

Total 93,972,200 2.11 trillion

* Gross domestic product based on Purchasing Power Parities by World Bank , ** World Bank ranking

Warsaw as an emerging data center

and connectivity hub in CEE

Top 10 Internet countries in Europe

Source: Internet World Stats, www.internetworldstats.com, Miniwatts Marketing Group

Warsaw as an emerging data center

and connectivity hub in CEE

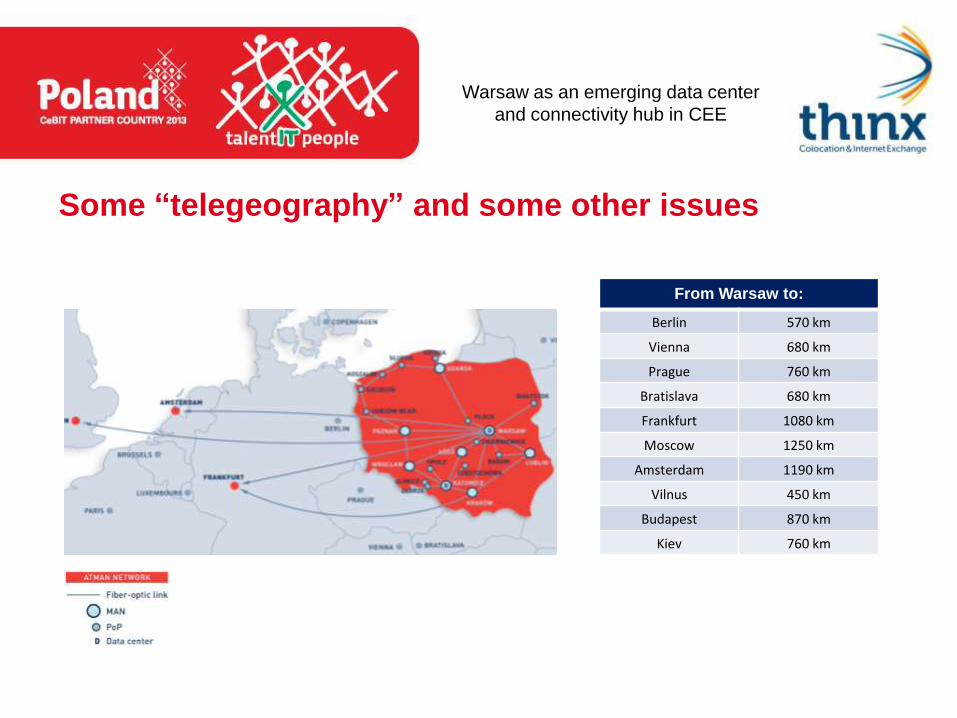

Some “telegeography” and some other issues

Poland – the shortest land route to the East: Baltic countries, Russia, Ukraine and further east

Warsaw centrally placed in the region

Highly skilled workforce, much lower salary costs

Warsaw as an emerging data center

and connectivity hub in CEE

Some “telegeography” and some other issues

From Warsaw to:

Berlin 570 km

Vienna 680 km

Prague 760 km

Bratislava 680 km

Frankfurt 1080 km

Moscow 1250 km

Amsterdam 1190 km

Vilnus 450 km

Budapest 870 km

Kiev 760 km

Warsaw as an emerging data center

and connectivity hub in CEE

Warsaw – the largest data center market in CEE

Warsaw24%

Moscow22%

Budapest17%

Prague15%

Bratislava10%

St. Petersburg 7%

Kiev5%

Top 4 markets sq m net % share in CEE

Warsaw 23,979 24%

Moscow 21,450 22%

Budapest 16,958 17%

Prague 15,063 15% Source: Tier1 Research, Eastern European Multi-Tenant

Data Center Market Assessment 2011

Warsaw as an emerging data center

and connectivity hub in CEE

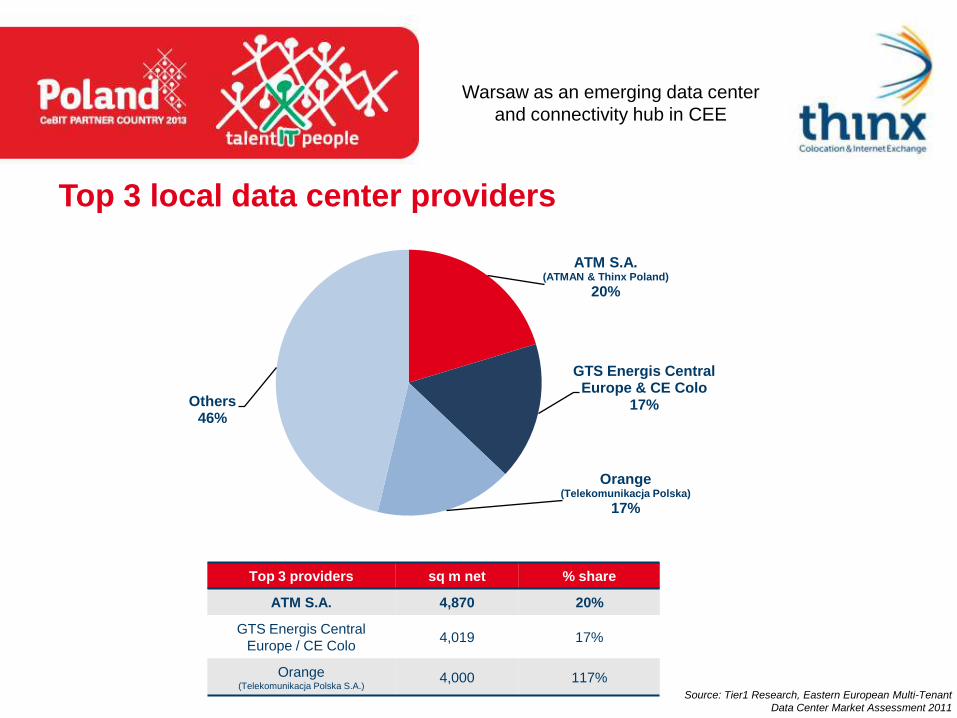

Top 3 local data center providers

ATM S.A.(ATMAN & Thinx Poland)

20%

GTS Energis Central Europe & CE Colo

17%

Orange (Telekomunikacja Polska)

17%

Others46%

Top 3 providers sq m net % share

ATM S.A. 4,870 20%

GTS Energis Central

Europe / CE Colo4,019 17%

Orange (Telekomunikacja Polska S.A.)

4,000 117%Source: Tier1 Research, Eastern European Multi-Tenant

Data Center Market Assessment 2011

Warsaw as an emerging data center

and connectivity hub in CEE

Pricing index

Competitive colocation offer for the Polish and CEE markets:

Colocation space at up to 30% less than the market price for data centers in Frankfurt, London, Moscow or Vienna

Racks starting at 350 euro MRC, energy below 0.1 euro per kWhSource: Tier1 Research, Eastern European Multi-Tenant

Data Center Market Assessment 2011

Warsaw as an emerging data center

and connectivity hub in CEE

Warsaw – data center and connectivity hub in CEE

Polish data center market is among the most dynamically developing ones in Europe

High domestic demand in Poland

Increasing external demand (colocation requests from across the globe)

Strategically located between Western and Eastern Europe

Competitive pricing: racks, power and connectivity to European tier 1 cities (like Frankfurt, London, Amsterdam)

High availability of resources: rack space and power

State-of-the-art colocation services: high quality and technical competence