CEA Mpstudy

480

Report of for Eleventh Plan (2007-12) The Working Group on Power Volume - II Main Report Government of India Ministry of Power New Delhi February 2007 lR;eso t;rs lR;eso t;rs

Transcript of CEA Mpstudy

Report of

for Eleventh Plan (2007-12)

The Working Group on Power

Volume - IIMain Report

Government of India

Ministry of Power

New DelhiFebruary 2007

lR;eso t;rslR;eso t;rs

Working Group on Power

for Eleventh Plan (2007-12)

Volume – II Main Report

Contents Working Group on Power for 11th Plan

Page 1 of Contents

CONTENTS

CHAPTER DESCRIPTION PAGE NO. PREFACE INTRODUCTION EXECUTIVE SUMMARY 1 - 69

Chapter 1 DEMAND FOR POWER AND GENERATION PLANNING

1 - 93

1.1 10th Plan Review 1.2 Target Capacity Addition during Tenth Plan

1.3 Actual Capacity Addition and Power Supply Position during 10th Plan (Till date)

1.4 Actual/ Likely Capacity Addition during Tenth Plan

1.5 Likely Installed Capacity at the end of 10th Plan i.e. as on 31.03.2007

1.6 Demand for Power 1.7 Approach to Selection of Projects for 11th Plan 1.8 Generation Planning Norms 1.9 Generation Expansion Planning 1.10 Twelfth Plan Perspective (2012-2017) 1.11 Medium Term Plan: 11th Plan (2007-12) 1.12 Long Term Plan: 12th Plan (2012-17) 1.13 New Initiatives 1.14 Captive Power Plants

1.15 Maximising Generation from Existing Plants and AGS&P

1.16 Energy Efficiency Improvement through Energy Audit

1.17 Accelerated Generation & Supply Programme (AGS&P) Scheme

1.18 Non Conventional Energy Sources

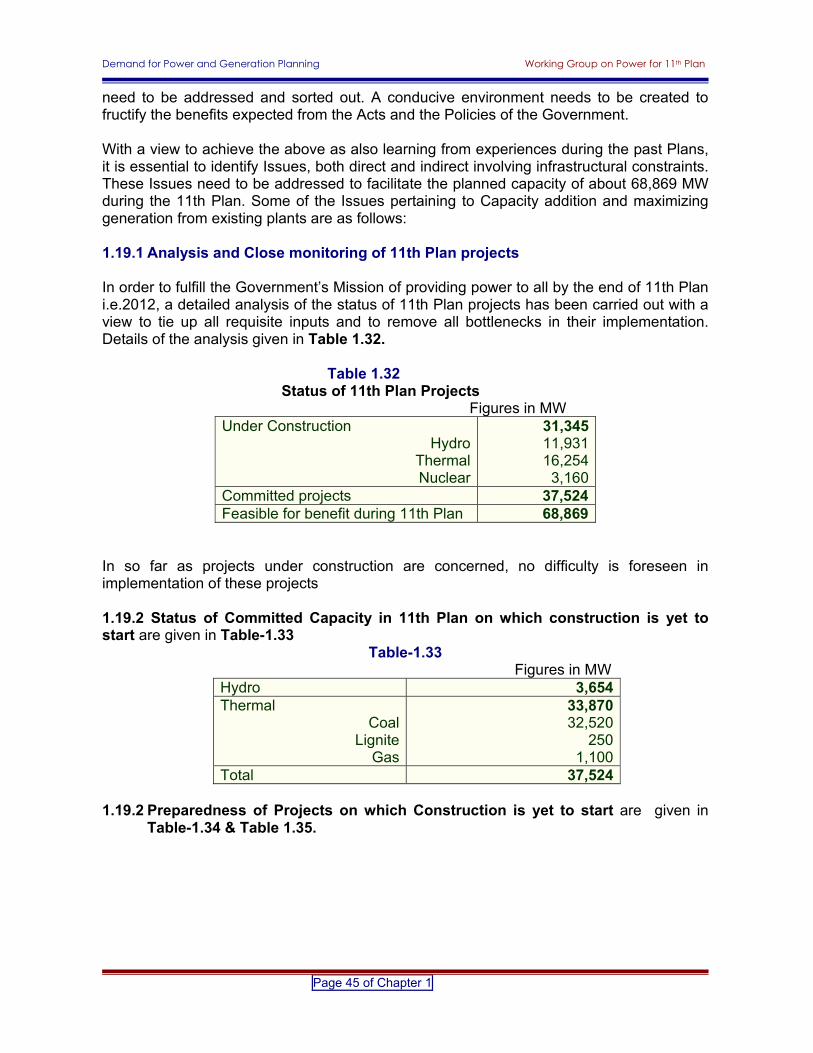

1.19 Issues to be Addressed and Strategy to be adopted for 11th Plan

1.20 Recommendation of the Group

Appendix-1.1: Summary of Capacity Addition Target of 41,110 MW during 10th Plan (Region Wise, Sector Wise and Status Wise)

Appendix-1.2 List of Projects Commissioned during 10th Plan upto 31.12.2006

Appendix-1.3 List of Units dropped from 10th Plan (41110 MW)

Appendix-1.4 List of the Thermal Projects slipping from 10th Plan (41,110 MW) and included in 11th Plan (As per 30,641 MW)

Contents Working Group on Power for 11th Plan

Page 2 of Contents

CHAPTER DESCRIPTION PAGE NO.

Appendix-1.5 List of the Hydro Projects slipping from 10th Plan (41,110 MW) and included in 11th Plan (As per 30,641 MW)

Appendix-1.6 Details of Best Effort Projects

Appendix-1.7 List of Projects Likely to slip to 11th Plan

Appendix-1.8 Capacity Addition programme for 11th Plan

Appendix-1.9 Year wise coal requirement for 11th Plan

Appendix-1.10 Shelf of 12th Plan projects

Appendix 1.11 Comparative Performance of Partnership in Excellence (PIE) Stations with NTPC as PIE Partner

Appendix 1.12 State Wise List of Hydro RM&U Projects Completed in the 10th Plan

Appendix 1.13 State Wise List of ongoing Hydro RM&U Projects Programmed For Completion In the 10th Plan

Appendix 1.14 State Wise List of ongoing Hydro RM&U Projects Programmed for Completion in the 11th Plan

Appendix 1.15 State Wise List of Hydro RM&U Projects Programmed for Completion in the 11th Plan but works of which are yet to be taken up for Implementation

Chapter 2 TRANSMISSION PLANNING AND NATIONAL GRID

1 - 66

2.1 Review of Transmission System during 10th Plan

2.2 National Grid 2.3 Eleventh Plan Programme 2.4 Technology Development

2.5 Transmission Requirements for Open Access and Trading

2.6 Power Exchange with Neighbouring Countries 2.7 Reliability Issues and Grid Operation

2.8 Fund Requirement during 11th Plan for

Transmission System Development and Related Schemes

Appendix-2.1: HVDC Transmission Bipole, Back-to-back and Monopole lines and terminal station – Existing at the end of 9th Plan and programme for 10th Plan 2002-07

Appendix-2.2: Transmission lines and sub-station at 765kV – Existing at the end of 9th Plan and programme for 10th Plan 2002-07

Contents Working Group on Power for 11th Plan

Page 3 of Contents

CHAPTER DESCRIPTION PAGE NO.

Appendix 2.3 List of major transmission schemes completed and programmed under the development plan of the Regional Grids and National Grid during the 10th Plan-Northern Region

Appendix 2.4 List of major transmission schemes completed and programmed under the development plan of the Regional Grids and National Grid during the 10th Plan-Western Region

Appendix 2.5 List of major transmission schemes completed and programmed under the development plan of the Regional Grids and National Grid during the 10th Plan-Southern Region

Appendix 2.6 List of major transmission schemes completed and programmed under the development plan of the Regional Grids and National Grid during the 10th Plan-Eastern Region

Appendix 2.7 List of major transmission schemes completed and programmed under the development plan of the Regional Grids and National Grid during the 10th Plan-Inter-Regional

Appendix-2.8: Inter-State Transmission Schemes For The 11th Plan

Appendix- 2.9: States’ Transmission Schemes for the 11th Plan Evacuation System for Generation Projects

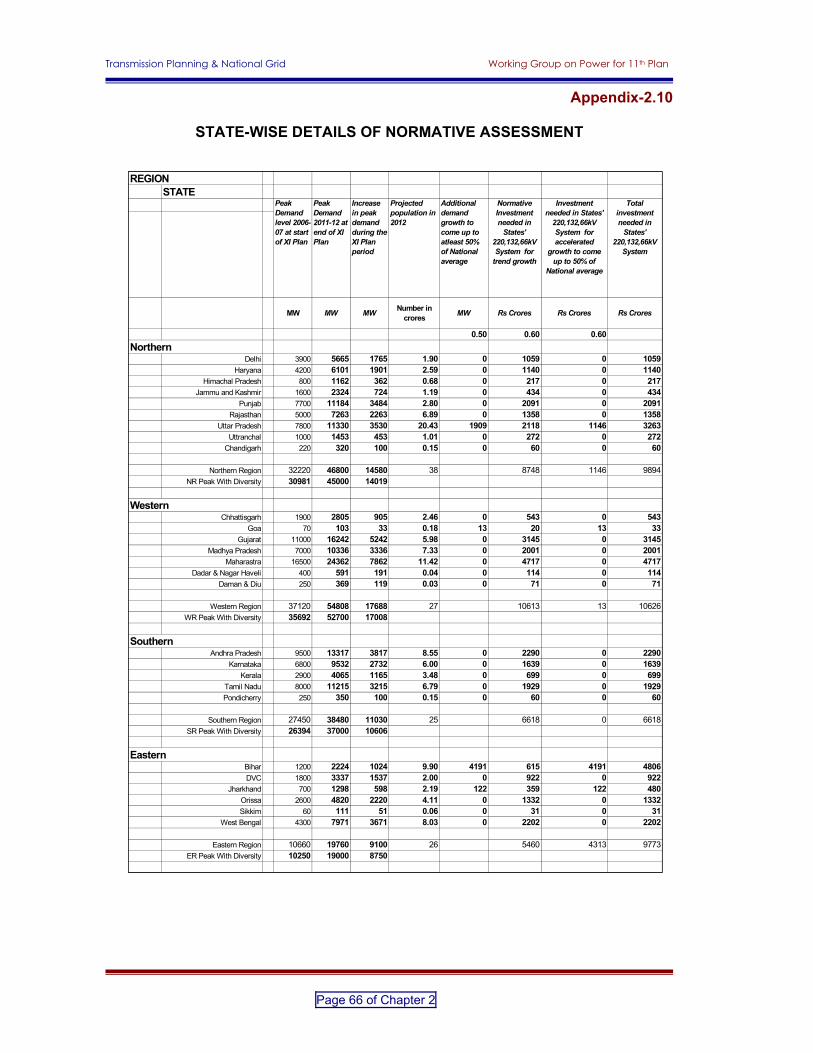

Appendix-2.10 State-Wise Details of Normative Assessment

Chapter 3 DISTRIBUTION INCLUDING VILLAGE AND HOUSHOLD ELECTRIFICATION

1 - 57

3.0 Overview 3.1 Key Issues in Electricity Distribution Sector 3.2 Distribution Reforms 3.3 New Legal and Policy Framework 3.4 Policy Initiatives 3.5 Distribution of Power in Urban Areas 3.6 Achievements Under APDRP

3.7 Distribution of Power in Rural Areas - Initiatives in 10th Plan

3.8 Development of Revenue Sustainability - Franchisees

3.9 Role of Panchayati Raj in Franchisee Development

3.10 Power Distribution in Rural Areas Through DDG

3.11 Short Term Strategies for DDG Schemes 3.12 Medium Term and Long Term Strategies 3.13 Cost to Serve/ Delivered Cost

Contents Working Group on Power for 11th Plan

Page 4 of Contents

CHAPTER DESCRIPTION PAGE NO. 3.14 Role of Stakeholders 3.15 Role of REC 3.16 Institutional and Financial Models 3.17 Special Focus Areas for 11th Plan 3.18 New Programmes/Schemes for 11th Plan

3.19 Agriculture Sector - Subsidies and Cross Subsidies

3.20 Water Energy Nexus 3.21 Open Access in Distribution 3.22 Multi-Year Tariff 3.23 Public Private Partnership

3.24 Impact of Power Sector Reforms – Success Stories

3.25 Best Practices 3.26 Requirement of Funds 3.27 Recommendations

Chapter 4 DEMAND SIDE MANAGEMENT AND ENERGY EFFICIENCY

1 - 14

4.0 Introduction 4.1 The Energy Conservation Act

4.2 Energy Saving –Target and Achievement of 10th Plan

4.3 Energy Conservation Strategy in the 11th Five-Year Plan

4.4 Policy Research for Accelerating Adoption of Energy Efficiency and DSM Programs

4.5 Budget Outlay for the 11th Plan 4.6 Recommendations Chapter 5 RESEARCH & DEVELOPMENT 1 - 21 5.0 Introduction 5.1 Overview of R&D 5.2 Technology Development in Power Sector

5.3 Identified Projects for 11th Plan by Central Utilities

5.4 R&D Project Provisions and Test Facilities for CPRI

5.5 Major Project Proposals for 11th Five Year Plan

5.6 Short Listed Short Term & Long Term Projects

5.7 R&D Funding 5.8 Intellectual Property Rights

5.9 Human Resource Development and Technical Competence Building

Chapter 6 DEVELOPMENT OF POWER SECTOR IN NORTH-EASTERN REGION

1 - 11

6.0 Introduction

Contents Working Group on Power for 11th Plan

Page 5 of Contents

CHAPTER DESCRIPTION PAGE NO. 6.1 Status at the beginning of 10th Plan

6.2 Review of Generation Capacity Addition Programme during 10th Plan

6.3 Reasons for Slow Pace of Project Execution

6.4 Power Demand & Supply Analysis of the Region

6.5 Generating Capacity Addition Programme in

North Eastern Region/ Sikkim during 11th Plan

6.6 Development of Transmission System in North Eastern Region

6.7 Evacuation of Power from Major Generation Projects in the North-Eastern Region along with Power from Projects coming up in Sikkim and Bhutan during the 11th Plan and early 12th Plan Period

6.8 Special Attention for Distribution in NE Region

6.9 Fund Requirement 6.10 Policy Initiatives and Recommendations Chapter 7 HUMAN RESOURCE DEVELOPMENT 1 - 25 7.0 Back Ground 7.1 Elements of HRD Planning 7.2 Assessment of Manpower 7.3 Training 7.4 Funding & Capital Outlay

Appendix 7.1: Training Load during 11th Plan for Technical Manpower (Includes Infrastructure) in Thousand-Man-Months (TMM)

Appendix 7.2: Training Load during 11th Plan for Non-Technical Manpower (Includes Infrastructure) in Thousand-Man-Months

Appendix 7.3: Training Load (Induction) during 12th Plan for Technical Manpower (Includes Infrastructure) in Thousand-Man-Months

Appendix 7.4: Training Load (Induction) during 12th Plan for Non-Technical Manpower (Includes Infrastructure) in Thousand-man-months

Chapter 8 LEGISLATIVE AND POLICY ISSUES 1 - 41 8.0 Back Ground

8.1 Implementation of Provisions of Act and Policies

8.2 Status of Implementation and Deviations of Integrated Energy Policy

8.3 National Electricity Policy - Deviations and Status of Implementation

8.4 Major Issues and Recommendations

Contents Working Group on Power for 11th Plan

Page 6 of Contents

CHAPTER DESCRIPTION PAGE NO. 8.5 Summary of Recommendations

Appendix 8.1: Fund Requirement for Training of Electricity Regulators and Staff

Appendix 8.2: Comments of Prayas Energy Group Appendix 8.3: Comments of IIT Kanpur Chapter 9 KEY INPUTS 1 - 49 9.1 Introduction 9.2 Coal & Lignite 9.3 Transportation of Coal: Available Infrastructure 9.4 Natural Gas 9.5 Key Input Materials 9.6 Generation Expansion Plan 9.7 Material Requirements for Generating Stations

9.8 Material Requirement for Power Transmission System Network

9.9 Material Requirement for Distribution System Network

9.10 Material Requirement for Power and Distribution Transformers

9.11 Other Materials for 11th & 12th Plan Projects

9.12 Total Requirement of Various Materials for

Capacity Addition Planned during 11th & 12th Plans

9.13 Availability / Supply of Key Materials 9.14 Constraints / Policy Support Required 9.15 Availability / Capability of Manufacturers 9.16 Construction Capability

9.17 Availability/Capability of Construction Agencies

9.18 Availability of Construction Equipment 9.19 Special Measures for Thermal Projects 9.20 Recommendations

Appendix 9.1: Port wise Projected Traffic and Capacity Estimation (2013-14)

Appendix 9.2: List of Construction Equipments to be Augmented for Hydro Projects

Appendix 9.3: Construction Equipment Availability vis a vis Augmentation required for adding 14000 MW / per yr.

Chapter 10 FINANCIAL ISSUES AND POWER SECTOR FINANCING

1 - 46

10.1 Financial Performance of Power Sector during 10th Plan

10.2 Fund Requirement for 11th Plan

10.3 Renovation and Modernization of Power Plants

10.4 Transmission Network

Contents Working Group on Power for 11th Plan

Page 7 of Contents

CHAPTER DESCRIPTION PAGE NO. 10.5 Distribution and Rural Electrification 10.6 Human Resource Development 10.7 Research and Technology Development 10.8 Demand Side Management 10.9 11th Plan Estimated Fund Requirement 10.10 Year Wise Fund Requirement 10.11 Sources of Funds 10.12 Estimated Funds Mobilization 10.13 Lenders’ Issues 10.14 Developers’ Concerns

10.15 Recommendations & Implementation Strategy

10.16 Implementation Mechanisms

Appendix 10.1: Detailed Outlay and Achievement for Funding 10th Plan - State Sector

Appendix 10.2: Approved Tenth Plan Outlay Internal and Extra Budgetary Resources Gross Budgetary Support

Appendix 10.3: Assumptions for Estimation of Cost of Generation Projects

Appendix 10.4: Projects Under Construction Appendix 10.5: Committed Projects

Appendix 10.6: Projects to be taken up in 11th Plan for Likely Benefit in 12th Plan

ACRONYMS

INTRODUCTION

The Working Group on Power was constituted by the Planning Commission vide its Office Order No.I-15/1/2005-P&E dated 20th April 2006 (copy enclosed at Appendix-A) to formulate the power programme for 11th Plan. Secretary (Power) was the Chairman of the Working Group and Member (Planning), CEA was the Member Secretary of the Working Group. The Composition and Terms of Reference of the Working Group for Eleventh Plan are given in Appendix-A. The first meeting of the Working Group was held on 19th May 2006 under the Chairmanship of Secretary (Power). It was decided to constitute 8 specialized Sub-Groups to go into the specific areas to cover comprehensively all the Terms of Reference of the Working Group. Subsequently, review meetings of the Working Group were held in MoP on a regular basis to assess the progress of the Sub-Groups from time to time. During the discussions, it emerged that it was essential to have a separate Sub-Group on “Human Resource Development” and accordingly Sub Group 9 was constituted. Details of the various Sub Groups are enclosed in Appendix- B The Sub-Groups discussed various issues regarding Demand, Generation, Transmission & Distribution Expansion Planning, Households & Rural Electrification, Demand Side Management & Energy Efficiency Issues, Research & Development, Manpower Planning & Training and Fund Requirement. A separate chapter has also been included on development of North Eastern Region as well as Policy Issues. A review of and measures for implementation of National Electricity Policy and Integrated Energy Policy have also been included in the Report. The report is based on 10th Plan likely capacity addition of 30,641 MW corresponding to which the 11th Plan capacity addition is 68,869 MW and 12th Plan capacity addition is 82,000 MW. Subsequent to the finalization of the Report, CEA had reviewed the likely capacity addition during the 10th Plan. This is now expected to be around 23,250 MW. The balance 10th Plan capacity would slip to 11th Plan in addition to 68,869 MW planned for 11th Plan. These changes have, however not been effected in the body of the Report. Various Sub-Groups submitted their Reports to the main Working Group. Based on the recommendations of these Sub-Groups the Report of the Working Group for 11th Plan has been formulated. It is in 2 Volumes- Volume I containing the Executive Summary of the Report and Volume II containing the main Chapters of the Report. The Executive Summary has also been made part of Volume II for the sake of completeness & ease of reference.

New Delhi (V. S. VERMA) 15th Feb. 2007 Member (Planning) CEA and Member Secretary of the Working Group on Power

Appendix-A No.I-15/1/2005-P&E

GOVERNMENT OF INDIA PLANNING COMMISSION

(POWER & ENERGY DIVISION) ******

Yojana Bhawan Sansad Marg

New Delhi— 110001.

Dated: 20th April, 2006

ORDER

Subject: Constitution of a Working Group on Power for formulation of Eleventh Five Year Plan (2007-2012.

It has been decided to constitute a Working Group on Power in the context of preparation

of Eleventh Five Year Plan (2007-2012). The Composition and Terms of Reference of the Group will be as follows: A. Composition

Secretary, Ministry of Power - Chairman Members

1. Adviser (Energy), Planning Commission 2. Chairperson, Central Electricity Authority 3. Representative of Ministry of Non-Conventional Energy Sources 4. Representative of Department of Atomic Energy 5. Representative of Ministry of Coal 6. Representative of Ministry of Petroleum & Natural Gas 7. Representative of Ministry of Environment & Forests 8. Representative of Department of Science & Technology 9. Member (Planning), Central Electricity Authority— Member Secretary

PSUs 1. CMDs, NTPC/NHPC/PGCIL/PFC/REC 2. Chairmen, GRIDCO/APTRANSCO/MSEB/MPEB/TNEB/PSEB

Private Sector Representatives 1. Representative of Reliance Energy Company 2. Representative of Tata Electric Company 3. Representative of Torrent Electric Company

OTHERS 1. Shri Girish Sant, PRAYAS 2. Shri Navroj Dubash, NIPFP 3. Prof. Anoop Singh, lIT Kanpur

B. Terms of Reference

i) To review the Integrated Energy Policy Report and suggest measures to operationalise its recommendations during the Eleventh Plan Period.

ii) To review the status of various policies notified under the provisions of Electricity Act, 2003 and identify steps needed to realize the objectives of the Electricity Act, 2003.

iii) To recommend an industry structure that would enhance the number of players, promote competition, provide a consistent & transparent pricing regime and raise conversion, transmission, distribution & end use efficiency.

iv) To review the likely achievement during the Tenth Plan period in meeting targets set for Generation, Transmission, Distribution and Renovation & Modernisation R&M). An analysis of the reasons for shortfalls, if any, may be highlighted. v) To review the current status of captive generation in the country, highlight issues

facing this sub sector and make recommendations for enhancing/reducing captive generation during the Eleventh Plan period.

vi) To review the effectiveness of Eleventh Plan Schemes such as Accelerated Generation & Supply Programme (AG&SP), Accelerated Power Development & Reforms Programme (APDRP) and Rajiv Gandhi Grameen Vidyutikaran Yojana (RGGVY). To suggest modifications and/or give recommendations for scrapping these schemes or replacing them with alternative schemes to better address the desired objectives.

vii) To assess the State-wise/region-wise demand for power in terms of both peak and energy requirements.

viii) To recommend the optimal mix of additional generating capacity to be created during the Eleventh Plan period in terms of hydro, thermal (coal, gas, lignite and liquid fuel) and nuclear generation on the basis of relative economics of different fuels at different locations. The executing agency of the project i.e. State Sector, Central Sector or Private Sector should also be identified. A possible listing of the projects and their phasing for benefits during Eleventh Plan must be prepared. Advance action to be taken in the Eleventh Plan period for the Twelfth Plan projects may also be identified.

ix) To assess the potential for improving availability of power from existing power stations through Renovation & Modernisation/life extension.

x) To maximise benefit from the existing plants by improving their operational efficiency and capacity utilization, improvement and augmentation of Transmission and Distribution network and dealing effectively with the problem of Aggregate Technical & Commercial (AT&C) losses and theft of power.

xi) To review the on-going reform process undertaken by States in the power sector. xii) To assess if privatisation is an answer to address the ills of the Power Sector. xiii) To suggest energy conservation measures through Demand Side Management

(DSM) such as staggering of load, time of the day metering and pricing, reduction in the energy intensity of the large consumers etc.

xiv) To recommend the operational norms for thermal including Gas, Liquid fuel and nuclear generations.

xv) To develop a work plan to tackle problems in ash disposal, pollution and other environmental issues.

xvi) To make recommendations regarding S&T programme to be implemented in the Eleventh Plan period and the institutional arrangements necessary therefore.

xvii) To explore avenues for purchase of power from neighbouring countries through joint venture schemes.

xviii) To assess the investment requirement for the Eleventh Plan in the Power Sector. xix) To assess the infra-structural support such as transportation, port facilities, construction and manufacturing capabilities, roads etc. that would be required for implementation of the Eleventh and Twelfth five year Plans.

2. In order to assist the Working Group in its task, separate Sub-Groups on specific aspects

may be formed by the Working Group. These Sub-Groups will furnish their reports to the Working Group

3. The Chairman of the Working Group may co-opt experts as may be considered necessary.

4. The Working Group will submit its report to the Planning Commission latest by 30th September, 2006

5. Non-official members shall be entitled to payment of TA/DA by the Planning Commission as per SR 190(a). Official members will be entitled to payment of TAJDA by their respective Departments/Organizations, as per the rules of entitlement applicable to them.

6. The name(s) of the Representative(s) of various organizations, as per the above composition may be communicated to the Member-Secretary of the Working Group under intimation to Shri Surya P. Sethi, Adviser (Energy), Planning Commission.

7. Shri R.K. Kaul, Joint Adviser, Planning Commission, Room No.503, Yojana Bhavan, New Delhi-i 10 001 (Telephone No. 2309 6718), shall be the Nodal Officer for this Working Group and for any further query/correspondence may be made with him.

(K.K. Chhabra)

Under Secretary to the Government of India Chairman and Members (including Member-Secretary) of the Working Group. Copy for information to:

1. PSs to Deputy Chainman/ MOS(Planning)/ Members/ Member-Secretary, Planning Commission.

2. All Principal Advisers/ Advisers/JS(SP&Admn.) 3. Prime Minister’s Office, South Block, New Delhi. 4. Information Officer, Yojana Bhavan. 5. For general information in Yojana Bhavan through e-mail.

(K.K. Chhabra)

Under Secretary to the Government of India

Appendix-B

WORKING GROUP ON POWER FOR 11TH FIVE YEAR PLAN (2007-2012) – Details of Sub-Groups

SUB-GROUP 1- DEMAND PROJECTION AND GENERATION PLANNING. Shri Rakesh Nath-Chairperson, CEA- Chairman of Sub-Group Shri A.S. Bakshi-Chief Engineer (IRP) CEA - Member Secretary of Sub-Group SUB-GROUP 2- TRANSMISSION PLANNING INCLUDING NATIONAL GRID Shri V. Ramakrishna - Member (PS) CEA - Chairman of Sub-Group Shri A.K. Asthana, Chief Engineer (SP&PA), CEA - Member Secretary of Sub-Group Shri Jiwesh Nandan,Director (PTC & Trans), Ministry of Power - Member Secretary of Sub-Group SUB-GROUP 3- DISTRIBUTION INCLUDING VILLAGE & HOUSEHOLD ELECTRIFICATION Shri Anil Kr. Lakhina - Chairman , REC - Chairman of Sub-Group Ms Dharitri Panda, Director (RE), Min. of Power , Member Secretary of Sub-Group SUB-GROUP 4 - LEGISLATIVE AND POLICY ISSUES – FORMULATION, IMPLEMENTATION & FEEDBACK Shri Ajay Shankar Additional Secretary, Ministry of Power - Chairman of Sub-Group Shri Alok Kumar, Director (R&R), Ministry of Power - Member Secretary of Sub-Group SUB-GROUP 5 - DEMAND SIDE MANAGEMENT, ENERGY EFFICIENCY & ENERGY CONSERVATION Dr. Ajay Mathur- Director General, BEE - Chairman of Sub-Group Shri K.K.Chakarvarti Energy Economist BEE - Member Secretary of Sub-Group SUB-GROUP 6 - TECHNOLOGICAL ADVANCEMENT AND RESEARCH & DEVELOPMENT Shri A.K.Tripathi - Director General CPRI - Chairman of Sub-Group Dr. R.R. Sonde, Executive Director (R&D) NTPC- Member Secretary of Sub-Group

SUB-GROUP 7 - ISSUES CONCERNING KEY INPUTS

Shri T. Sankarlingam - CMD NTPC - Chairman of Sub-Group Shri S.Sheshadri-Chief Engineer (TPIA)CEA - Member Secretary of Sub-Group

SUB-GROUP 8 - FINANCIAL ISSUES Dr. V.K.Garg - CMD, PFC - Chairman of Sub-Group Sh. Mukul Modi,Asstt Vice President,SBI Capital Markets Limited- Member Secretary of Sub-Group SUB-GROUP 9 - HUMAN RESOURCE DEVELOPMENT AND CAPACITY BUILDING Shri U.N. Panjiar, Additional Secretary, Ministry of Power - Chairman of Sub-Group, Shri C.S.Malik , Principal Director, NPTI - Member Secretary of Sub-Group Chief Coordinator from MoP – Shri Sudhakar Shukla, Director, MoP

Executive Summary Working Group on Power-11th Plan (2007-12)

1

EXECUTIVE SUMMARY

1.0 DEMAND PROJECTION AND GENERATION PLANNING 1.1 TENTH PLAN REVIEW The capacity addition target of 41,110 MW comprising 14,393 MW hydro, 25,417 MW thermal and 1,300 MW nuclear was fixed for the 10th Plan. The sector wise, type wise summary of this capacity addition target is given in Table below.

10TH PLAN CAPACITY ADDITION TARGET-SECTOR WISE

(Figures in MW) SECTOR Hydro Thermal Nuclear Total (%)

CENTRAL 8,742 12,790 1,300 22,832 (55.5%) STATE 4,481 6,676 0 11,157 (27.2%) PRIVATE 1,170 5,951 0 7,121 (17.3%) TOTAL 14,393 25,417 1,300 41,110 (100%)

A moderate target was set for state and private sectors keeping in view the preparedness of various state power utilities and IPPs. 1.1.2 Actual Capacity Addition (till 31.12.2006) A capacity addition of 17,995 MW has been achieved during 10th Plan till 31/12/06. The total installed capacity as on 31/12/2006 was 1,27,753 MW comprising 33,642 MW hydro, 84,020 MW thermal including gas & diesel, 3,900 MW nuclear power plants and 6,191 MW from renewable energy sources including wind. (The sector– wise details of installed capacity are given in Table 1.4 in Chapter-1.) 1.1.3 Power supply position in 10th plan The year-wise actual power supply position during 2002-03, 2003-04, 2004-05 ,2005-06 and 2006-07(till Dec-06) of 10th plan is given in Table below

Executive Summary Working Group on Power-11th Plan (2007-12)

2

ACTUAL POWER SUPPLY POSITION (ALL INDIA BASIS)

Year Peak Energy Requir

ement (MW)

Availability (MW)

Shortage MW (%)

Requirement (MU)

Availability (MU)

Shortage MU (%)

2002-03 81492 71547 9945 (12.2%) 545983 497690 48093 (8.8%) 2003-04 84574 75066 9508 (11.2%) 559264 519398 39866 (7.1%) 2004-05 87906 77652 10254 (11.7%) 591373 548115 43258 (7.3%) 2005-06 93255 81792 11463 (12.3%) 631757 578819 52938 (8.4%) 2006-07 (upto Dec,06)

100466 86425 14041 (14.0%) 510223 465149 45074 (8.8%)

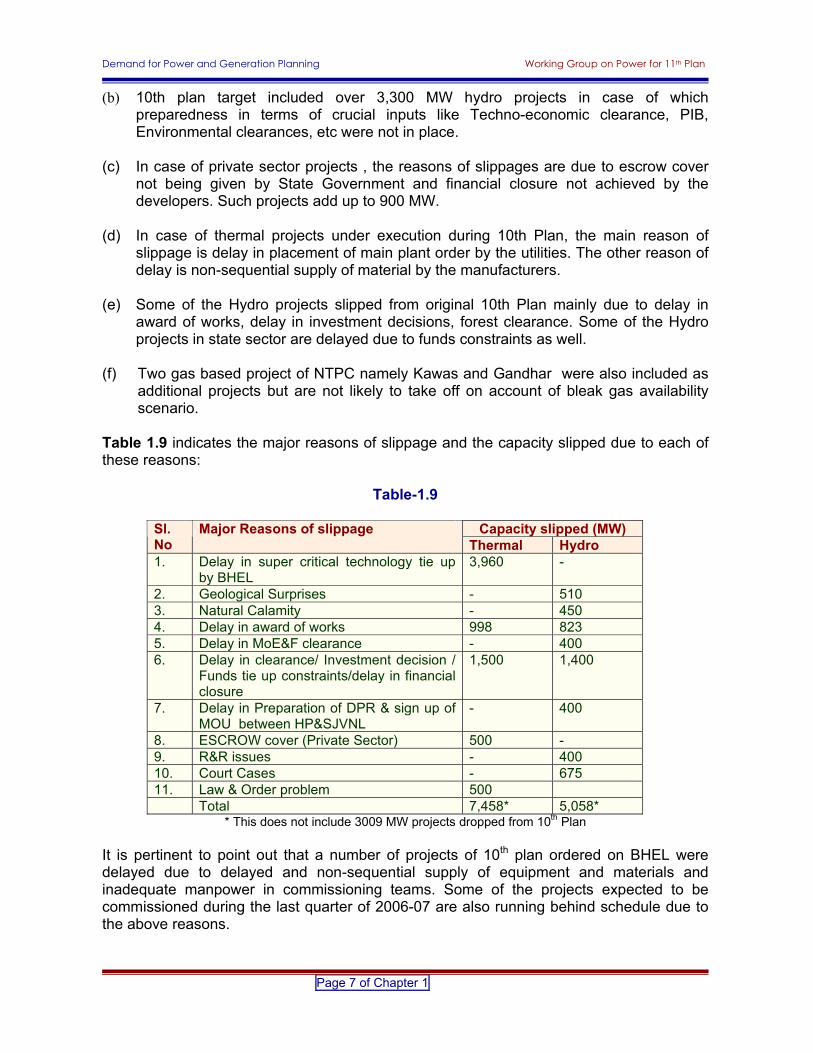

The likely achievement of capacity addition during the 10th Plan is expected to be 30,641 MW which includes 2,578 MW capacity of projects which have been included on best effort basis. Any slippage of these best efforts projects from 10th plan would be reckoned as additional capacity in 11th plan over and above being proposed in this document. In 8th & 9th plan, capacity addition of 16,423 MW and 19,119 MW respectively was achieved. Even though the capacity addition target of 10th plan could not be achieved, the actual capacity addition is expected to be much higher than the earlier five year plans. The reasons for the slippages during the 10th plan have been analysed to learn lessons for capacity addition planning for future plans. During the first year of 10th plan itself it became clear that a number of projects totalling to 3,009 MW in public and private sectors could not be taken up due to various reasons which included non availability of escrow cover by State Government to IPP projects and fund constraints. There was also delay in super critical technology tie-up by BHEL for six units of 660 MW to be taken up by NTPC which resulted in delay in tendering. Additional projects totalling to 5,008 MW capacity were identified for execution during 10th plan to make up for the projects which could not take off. However, a total capacity of 12,516 MW (excluding 3,009 MW projects which could not be taken up) is expected to slip to 11th Plan due to reasons mentioned against each, in the following table:

Executive Summary Working Group on Power-11th Plan (2007-12)

3

Capacity slipped (MW) Sl. No Major Reasons of slippage Thermal Hydro

1. Delay in super critical technology tie up by BHEL

3960 -

2. Geological Surprises - 510 3. Natural Calamities 450 4. Delay in award of works 998 823 5. Delay in MoE&F clearance - 400 6. Investment decision/ Funds tie up

constraints/ delay in financial closure 1500 1400

7. Delay in Preparation of DPR & signing of MOU with state govt.

- 400

8. ESCROW cover (Private Sector) 500 - 9. R&R issues - 400 10. Court Cases - 675 11. Law & Order problem 500

Total 7458 5058 (The details are given in Para 1.5 of Main Working Group Report)

It is pertinent to point out that a number of projects of 10th plan ordered on BHEL were delayed due to delayed and non-sequential supply of equipment and materials and inadequate manpower in commissioning teams. Some of the projects expected to be commissioned during the last quarter of 2006-07 are also running behind schedule due to the above reasons. 1.2 GROWTH IN ENERGY GENERATION 1.2.1 Growth in Generation During 10th Plan The growth in generation has been 3.2%, 5.1%, 5.2% and 5.2% during 2002-03, 03-04, 04-05 and 05-06 respectively. In the year 2006-07(upto Dec-2006) a growth rate of 7.5 % has been recorded. The Compounded Annual Growth Rate(CAGR)of generation during the 10th Plan period is expected to be about 5.1%. However, higher growth could have been achieved if adequate gas would have been available for the existing and new gas based plants commissioned during 10th plan. 1.2.2 Growth in Generation during 11th Plan As per the Integrated Energy Policy (IEP), issued by the Planning Commission, GDP growth rates of 8%-9% have been projected during the 11th Plan. Assuming a higher growth rate of 9% and assuming the higher elasticity projected by the IEP of around 1.0, electrical energy generation would be required to grow at 9% p.a. during the 11th plan period. Also generation has to be collectively met by utilities, captive plants and Non-conventional energy sources. No reliable plans

Executive Summary Working Group on Power-11th Plan (2007-12)

4

about captive power capacity expansion are available but based on indications available from the manufacturers for addition in captive capacity and present utilization of available capacity, the generation from captive plants is expected to increase from 78 BU to 131 BU per annum. Since the load factor of non-conventional energy sources is very low (about 20% on an average), even though the capacity projected by MNRE from these sources is about 23,500 MW by the end of 11th Plan, the expected generation would be only around 41 BU. The generation from these renewables however has not been taken into account for planning purposes. Based on these assumptions following scenario emerges:

(i) Likely energy Generation by utilities in 2006-07 663 BU (ii) Likely Energy Generation by captive plants in 2006-07 78 BU (iii) Total Likely Generation in 2006-07 741 BU (iv) Compounded Annual Growth Rate 9% (v) Required Energy Generation by 2011-12 @ 9% growth rate over 741 BU 1140 BU (vi) Less Estimated Energy Generation by captive plants in 2011-12 131 BU (vii) Total Estimated Generation Requirement from Utilities by 2011-12 1008 BU

However to meet the objectives of NEP to increase the per capita consumption to 1000 units by the year 2011-12, the requirement of generation works out to 1210 BU, assuming a population of 121 crores in 2011-12 as per projections of Census 2001. After excluding the generation from captive plants (131 BU) and that from renewables (41 BU), the requirement of generation from utilities works out to 1038 BU. This would require a generation growth rate of 9.5% p.a (CAGR)for utilities.

1.2.3 Growth in generation During 12th Plan During the 12th Plan period, assuming a GDP growth rate of 9% per annum and elasticity 0.8 as compared to 1.0 during 11th plan mainly due to adoption of energy efficient technologies & other Energy Conservation and Demand Side Management measures being taken up during 11th Plan, electricity demand is likely to grow @ 7.2% p.a. Keeping this in view, the energy generation should increase to a level of 1470 BU by 2016-17 from a level of 1038 BU in 2011-12. However sensitivity analysis have been carried out assuming 8,9 & 10 % GDP growth rates & GDP-electricity elasticity of 0.9 & 0.8 respectively and the same is given in table below:

Executive Summary Working Group on Power-11th Plan (2007-12)

5

Generation Requirement for 2016-17

( As Per 8,9,10 % GDP Growth)

GDP Growth

GDP/ Electricity Elasticity

Electricity Generation Required

(BU) 0.8 1415 8 % 0.9 1470 0.8 1470 9 % 0.9 1532 0.8 1525 10 % 0.9 1597

1.3 APPROACH TO SELECTION OF PROJECTS FOR 11TH PLAN Keeping in view the lessons learnt from 10th plan while planning for capacity addition during 11th Plan, cautious approach have been adopted while choosing projects for commissioning in the 11th plan. It has been the endeavour to include only such projects as have high degree of certainty of implementation during 11th Plan. The approach adopted for selection of Hydro, Thermal and Nuclear projects have been as follows:

1.3.1 Hydro India is duly concerned about climate change and efforts are on to promote benign sources of energy. Hydro Power is one such source and is to be accorded priority also from the consideration of energy security. Irrespective of size and nature of hydro projects, whether ROR or Storage projects, these are all renewable technologies. However, execution of hydro projects requires thorough Survey and Investigation, preparation of DPR, development of infrastructure, EIA and other preparatory works, which are time consuming and require two to three years for their preparation. It would take about 5 years to execute a hydro project after the work is awarded for construction. Thus in order to achieve completion of a hydro project during 11th plan, the project should either be already under construction or execution should start at the beginning of the plan. The broad criteria adopted for selection of hydro projects for 11th plan are as under:

• Those hydro projects whose concurrence has been issued by CEA and

order for main civil works is likely to be placed by March 2007.

Executive Summary Working Group on Power-11th Plan (2007-12)

6

• Apart from the above, a few hydro projects of smaller capacity which are ROR type having surface power houses and where gestation period is expected to be less than 5 years have also been included. These projects would need to be rigorously followed up for completion during the 11th Plan.

Keeping in view the preparedness of various hydro projects, a capacity addition of 15, 585 MW is envisaged for 11th Plan. (The details of projects are given in Appendix 1.8- in Chapter-1 of main Working Group Report.) 1.3.2 Nuclear

Nuclear is environmentally benign source of energy and over a period of time, its proportion in total capacity should increase. Keeping in view the availability of fuel, a moderate capacity addition of 3,160 MW nuclear plants has been programmed during the 11th Plan by the Nuclear Power Corporation. All projects are presently under construction. However, in view of the recent developments in the Nuclear Sector, capacity addition in nuclear plants during 12th Plan is expected to be much higher.

(The details of projects are given in Appendix 1.8- in Chapter-1 of main Working Group Report.)

1.3.3 Thermal Gas

Although gas is relatively a clean fuel, at present there is uncertainty about the availability, period of availability and price of gas. Only 2,114 MW gas based capacity has been planned for 11th Plan where gas supply has already been tied up. This does not include NTPC’s gas based projects at Kawas and Gandhar, totalling to 2,600 MW, for which NTPC says that it has the gas supply contract but the matter is sub-judice. However more gas based projects could be taken up for construction as and when there is more clarity about availability and price of gas.

(The details of projects are given in Appendix 1.8- in Chapter-1 of main Working Group Report.)

Coal & Lignite based Thermal plants

Coal is expected to be main stay of power generation in the years to come. The following criteria have been adopted for identifying the coal and lignite based projects for inclusion in the 11th plan. • Such projects as have already been taken up for execution in the 10th

Plan period itself and are due for commissioning in the 11th Plan period. • Those thermal projects whose LOA has already been placed by the State

and Central Public Sector Corporations, other inputs also being in place.

Executive Summary Working Group on Power-11th Plan (2007-12)

7

• Those thermal projects whose LOA has already been placed and the financial closure achieved by private developers.

• Those thermal projects whose LOA is expected to be placed by 30th Sept, 2008 and commissioning is expected during the 11th Plan keeping in view the normal gestation period, the size of the plant & the type(green field/expansion).

After discussion with the various State Government and Central Generating Companies, thermal projects with total capacity of 46,635 MW of coal based and 1375 MW lignite based capacity have been identified for capacity addition during 11th plan. (The details of projects are given in Appendix 1.8- in Chapter-1 of main Working Group Report.) 1.4 CAPACITY ADDITION DURING 11TH PLAN (2007-12) Based on the preparedness of the projects, it was envisaged that a capacity of about 68,869 MW is feasible for addition during 11th plan period. The sector wise break-up of feasible capacity addition during 11th plan is given in Table below:

THERMAL BREAKUP SECTOR HYDRO TOTAL THERMAL

COAL LIGNITE GAS/LNG

NUCLEAR TOTAL (%)

CENTRAL 9685 23810 22060 1000 750 3160 36655 (53.2%)

STATE 2637 20352 19365 375 612 - 22989 (33.4%)

PRIVATE 3263 5962 5210 0 752 - 9225 (13.4%)

ALL-INDIA 15585 50124 46635 1375 2114 3160 68869 (100%)

In addition to above, thermal projects totalling to 11,545 MW have been identified as best effort projects. These projects would normally be commissioned in the beginning of 12th Plan but in case of any constraints in taking up of any of the projects included in 11th plan, some of these projects would be tried for commissioning during 11th Plan. Further, a capacity of 13,500 MW has been planned under renewable as per information given by MNRE. As can be seen from the above profile of capacity addition plan, central sector will play a lead role with capacity addition of more than half of the capacity addition target. There has been a good response from states on the need for

Executive Summary Working Group on Power-11th Plan (2007-12)

8

capacity addition to meet their growing demand and the states with IPPs, have been given target for achieving the balance capacity. The State owned capacity projected for the 11th Plan is 33.4 % of the total plan as compared to 27% likely during 10th Plan. Out of feasible capacity addition of 68,869 MW, projects totalling to 31,345 MW are already under construction and the balance projects totalling to 37,524 MW have been committed for implementation by the concerned generating companies during the 11th Plan. Details are furnished in the Table below:

THERMAL BREAKUP SECTOR HYDRO TOTAL

THERMAL COAL LIGNITE GAS/LNG

NUCLEAR TOTAL

Projects Under Construction 11931 16254 14115 1125 1014 3160 31345

Committed Projects 3654 33870 32520 250 1100 - 37524 *

Total 15585 50124 46635 1375 2114 3160 68869 (The details of projects are given in Appendix 1.8- in Chapter-1 of main Working Group Report.) * Note: Out of the projects totalling to 37,524 MW under committed category as given above, orders for Dadri Unit-6 (490 MW) & Mezia Ph-II (1000 MW) has been recently placed. The thermal capacity addition comprises of1 unit of 800 MW, 11 units of 660 MW, 53 units of 500/600 MW class, 49 units of 210/250/300 MW class, 7 units of 110/125 MW class. With the above capacity addition it would be possible to meet the projected energy requirement of 1038 BU (considering peak demand of 1,51,500 MW) for meeting per capita consumption of 1000 units at the end of 11th plan. With this capacity addition it would be feasible to achieve a generation growth rate of 9.5% p.a. (CAGR) 1.5 FUEL REQUIREMENT The requirement of various fuels for the thermal plants during the terminal year of the 11th Plan (2011-12) at normative generation parameters (PLFs and specific fuel consumption is summarised in the table below. This is based on a thermal capacity addition of 20,387MW and 50,124MW during the 10th and 11th Plan respectively.

Executive Summary Working Group on Power-11th Plan (2007-12)

9

Fuel Requirement (Tentative) during 2011-12

Fuel Requirement (2011-12) Coal* 545 MT

Lignite 33 MT

Gas/LNG** 89 MMSCMD

(The details of projects are given in Appendix 1.9- in Chapter-1 of main Working Group Report.)

* From domestic sources, total coal availability is expected to be 482 MT per annum by 2011-12. Accordingly, imported coal of the order of 40MT, equivalent to 63 MT of Indian coal, may have to be organised. This quantity may reduce provided production of domestic coal is increased. ** 89 MMSCMD of gas requirement at 90% PLF has been projected in 2011-12. At present, the availability of gas is of the order of 40 MMSCMD and therefore not sufficient to meet the requirement of even existing plants.

1.6 INITIATIVES DURING 11TH PLAN 1.6.1 High Hydro Development 50,000 MW Hydro Initiative was launched in 2003 and Preliminary Feasibility Report (PFRS) of 162 projects totalling to 48,000 MW were prepared. Out of this 77 projects with total capacity of about 37000 MW for which first year tariff is expected to be less than Rs.2.50/unit were selected for execution. Hydro projects have longer gestation period and therefore there is a need to formulate a 10 year plan for hydro projects. In 11th plan a capacity addition of over 15,500 MW has been targeted keeping in view the present preparedness of these projects. Projects totalling to a capacity of 30,000 MW have been identified for 12th Plan on which necessary preparations have to be made from now onwards to ensure their commissioning during 12th Plan. Thus the effect of 50,000 MW initiative would be visible in 12th Plan period. Preparation of DPR and various clearances and approval etc for these projects are to be obtained during the first two years of 11th Plan. It is recommended that CEA should closely monitor the progress of preparedness of DPR of these projects and their further execution. 1.6.2 Initiatives in Thermal Power Development: Efforts were made to bring in highly efficient super critical technology in the country for thermal power plants and execution of six super critical units of 660 MW capacity each was taken up during the 10th Plan period. The first unit of 660 MW based on super critical technology is likely to be commissioned during the

Executive Summary Working Group on Power-11th Plan (2007-12)

10

first year of 11th Plan i.e. 2007-08. The 11th Plan feasible capacity addition of coal based plants includes 12 units based on super critical technology with a capacity of 8060 MW which is about 18% of total coal capacity planned for 11th Plan. More and more power projects based on super critical technology are under planning stage and they would yield benefit during the 12th Plan period. It is envisaged that more than 50-60% of capacity addition of thermal plants during 12th plan period would be based on super critical units. This would also help in reducing the Carbon dioxide emission from new coal fired capacity. 1.6.3 Ultra Mega Power Projects (UMPP): Ministry of Power in the year 2006 has launched an initiative of development of coal based ultra mega projects with a capacity of 4,000 MW each on tariff based competitive bidding. Ultra Mega Power projects are either pit head based projects having captive mine block or coastal projects based on imported coal. Sasan UMPP, a pithead plant in Chattisgarh based on domestic fuel and Mundra UMPP in Gujrat based on imported coal have already been awarded for execution to the respective developers. According to the bids submitted by these developers only one unit of 660 MW is expected to be commissioned during the 11th Plan and the remaining unit during 12th Plan. Other projects where considerable progress has been made are coastal projects in Andhra Pradesh and Tamil Nadu and a pit head based project in Jharkhand. Further the projects under consideration include pit head projects in Orissa and Chatisgarh and coastal projects in Maharashtra and Karnataka. 1.6.4 Nuclear Power Development: 11th Plan power programme includes 3160 MW of nuclear power plants all of which are under construction. Recently, agreement has been signed with USA in respect of nuclear co-operation which is expected to improve the supply of nuclear fuel for nuclear power plants. It is also expected that execution of nuclear projects will also be opened up to enable participation by other PSUs and private sector. The effect of this is likely to be visible in 12th Plan period. Nuclear Power Corporation of India has indicated a capacity addition of about 11,000 MW during 12th plan. In addition, NTPC have also expressed their intention to enter into the nuclear power arena and have proposed an addition of 2,000 MW during 12th plan period. 1.6.5 Merchant Power Plants: A merchant power plant does not have long term PPA for sale of its power and is generally developed on the balance sheet of developers. Government of India has reserved coal block with reserves of 3.2 Billion Tons of coal for allotment by Screening Committee of Ministry of coal for merchant and captive plants. About 10,000 MW capacity is expected to be developed through this initiative. This capacity has not been taken into account while working out the capacity required

Executive Summary Working Group on Power-11th Plan (2007-12)

11

in the 9.5% growth in generation scenario. Capacity addition through this route would further contribute to better economic growth, better reliability of power, more spinning reserve and above all would promote creation of competition in the electricity market. 1.6.6 Decentralised Distributed Generation (DDG): In some of the remote areas, it is not techno-economically feasible to extend the grid supply. For meeting the demand of such remote areas, it is proposed to set up some power plants based on local energy sources available. These are small hydro and non-conventional sources such as Bio-Mass, Wind, DG sets etc wherein other sources are not available. During the XI plan period a capacity addition of about 5,000 MW of capacity under DDG is envisaged. (Refer Para 3.1 of the Report)

1.7 CAPTIVE POWER PLANTS

The generation from captive power plants at the end of X plan (2006-07) is likely to be about 78 billion units. It is envisaged that during the XI plan period about 12,000 MW capacity power plants would be added to the system which will take care of the demand of the industry and also supply surplus power to the grid under Open Access arrangements which has been allowed as per the Electricity Supply Act, 2003.

It is envisaged that the generation from non utility captive power plants by the year 2011-12 may be of the order of 131 billion units which results into a CAGR of 10.5% p.a in captive generation. 1.8 12TH PLAN SCENARIO The requirement of installed capacity and capacity addition to meet the generation requirement during the 12th Plan period as discussed in Para 1.2.2 of this Report are given in Table below:

Capacity addition required during 12th plan (2012-17)

GDP

Growth GDP

/Electricity Elasticity

Electricity Generation

Required (BU)

Peak Demand

(MW)

Installed Capacity

(MW)

Capacity Addition Required During 12th

PLAN (MW) 0.8 1415 215700 280300 70800 8 % 0.9 1470 224600 291700 82200 0.8 1470 224600 291700 82200 9 % 0.9 1532 233300 303800 94300 0.8 1525 232300 302300 92800 10 % 0.9 1597 244000 317000 107500

Executive Summary Working Group on Power-11th Plan (2007-12)

12

It would be seen from the above table that under various growth scenarios, the capacity addition required during 12th plan would be in the range of 71,000 - 1,07,500 MW, based on normative parameters. The Working Group recommends a capacity addition of 82,200 MW for the 12th Plan based on Scenario of 9% GDP growth rate and an elasticity of 0.8%. During 12th plan about 30,000 MW capacity addition is likely to be based on hydro and about 11,000-13,000 MW will be nuclear based. The balance capacity addition of about 50,000 MW will be from thermal projects. A shelf of projects totalling over 1,50,000 MW has been identified & listed in main report.

1.9 RENOVATION & MODERNIZATION, LIFE EXTENSION AND PIE PROGRAMME

A Renovation and Modernisation (R&M) Programme for Thermal Power Stations was launched by the Government of India all over the country way back in September 1984 for completion during the Seventh Plan Period. This programme was successfully completed and intended benefits were achieved. In the subsequent 8th and 9th Plans, Renovation and Modernisation and Life Extension (LE) works were carried out on a number of older generating units which resulted in improvement in their performance and extension of their useful life. In the 10th plan life extension of 106 Nos of thermal units totalling to 10,413 MW was envisaged. However progress was not satisfactory due to high execution time & cost involved in LE works. The cost of LE was also not economically feasible considering the age of plants and there was reluctance from power plants to shut down their units for longer periods due to prevailing power shortages. In view of above a new initiatives called Partnership of Excellence was taken up. Under this programme generating companies who were performing well provide assistance in improving performance of non-performing units by following measures;

Phase-I: Toning up of O&M Practices Phase-II: Comprehensive Overhaul Phase-III: LE for those units were found techno-economically feasible.

Towards this initiative, CEA identified 22 power stations of 11 utilities, with a capacity of 7930.5 MW across the country. Out of these, 17 stations with an operating capacity of 5050 MW were entrusted to NTPC and one stations (280 MW) to TATA power. On remaining 4 stations the respective utilities are taking their own course of action. The plants entrusted to NTPC recorded an additional generation of power-3690 MUs- corresponding to an equivalent capacity addition

Executive Summary Working Group on Power-11th Plan (2007-12)

13

of 720 MW, considering national average PLF. Capacity addition of this order requires an investment of around Rs.3,000 crore at a Greenfield project. The phase-II of the programme, therefore, needs to be continued. Some additional units have also been identified for R&M and life extension. The decision for investment for R&M/LE will be based on cost benefit analysis. If not economically viable installation of new plants at existing sites, may be considered. (The details of R&M, LE & PIE programme and their status are given in Chapter-1,Para 1.15 of main Working Group Report) 1.10 NEW AND RENEWABLE ENERGY SOURCES The Ministry of New and Renewable Energy Sources (MNRE) have chalked out plan of adding 13,500 MW of renewable power in the country during 11th Plan period. This would make total installed capacity of these plants at 23,500 MW by the year 2011-12 which is detailed as below: Wind - 17000 MW Bio Mass - 3200 MW Small Hydro- 3300 MW Although installed capacity of the plants is high but on an average plant load factor of wind turbine plants is only of the order of 15-20% and as such this capacity can generate about 41 billion units at the maximum. 1.11 RECOMMENDATIONS

1. The Working Group recommends generation planning based on growth of

energy generation requirement of 9.5%. Keeping in view the above objectives and preparedness of various projects the Working Group recommends capacity addition of 68,869 MW during 11th Plan as per details given below:

THERMAL BREAKUP SECTOR HYDRO TOTAL

THERMAL COAL LIGNITE GAS/LNG

NUCLEAR TOTAL (%)

CENTRAL 9685 23810 22060 1000 750 3160 36655 (53.2%)

STATE 2637 20352 19365 375 612 - 22989 (33.4%)

PRIVATE 3263 5962 5210 0 752 - 9225 (13.4%)

ALL-INDIA 15585 50124 46635 1375 2114 3160 68869 (100%)

(Detail list is in Appendix-1.8 of main Working Group Report)

Executive Summary Working Group on Power-11th Plan (2007-12)

14

2. States are required to take an active role in the capacity addition programme by their own agencies & by private sector participation through tariff based competitive bidding route on the lines of developments of Ultra Mega Power Project. In the 11th plan addition of less than 50% of total capacity is targeted in states and private sector. It is recommended that in 12th Plan more than 50% capacity should come through initiative of the states.

3. Some of the states do not have resources for capacity addition in their states. Such states should tie up long term PPAs with surplus states/generation companies.

4. Manufacturing capacity of BHEL needs to be enhanced to meet the capacity addition programme envisaged in 11th & 12th Plans.

5. A 10 year plan for hydro development is to be pursued in view of higher gestation period. A hydro capacity of 30,000 MW has been identified for commissioning during 12th Plan. The survey and investigation, preparation of DPR, statutory clearances should be vigorously followed up right from now to enable their commission during 12th Plan. The CEA should closely monitor progress on these projects. .

6. The Working Group recommends continuation of PIE programme during 11th Plan also.

7. In addition to capacity addition programme, concerted efforts to continue in regard to:

- Development of captive power plants. - Maximising Generation from existing plants. - Energy Efficiency improvement through Energy Audit. - Better O & M practices. - RM&U/Partnership in Excellence (PIE) Programme. - Development of Non-Conventional Energy Sources.

8. Major recommendations for facilitating open access in distribution and

harnessing surplus captive generation in the country are as under:

Reasonable cross subsidy surcharge and other charges to provide some economic incentive to the generators to avail open access.

The SERCs should allow recovery of some portion of fixed cost in addition to the variable cost of captive generation. The captive generators may offer their surplus power on the basis of a firm schedule. Infirm power from CPP should also be considered for purchase.

There should be no penalty for reduction of contract demand by any industry having captive plant.

Executive Summary Working Group on Power-11th Plan (2007-12)

15

2.0 TRANSMISSION PLANNING INCLUDING NATIONAL GRID The transmission system facilities had earlier been planned on regional basis with provision of inter-regional link to transfer regional surplus power arising out of diversity in demand. The generation resources in the country are unevenly located, the hydro in the northern and north-eastern states and coal being mainly in the eastern part of the country. Development of strong National Grid has become necessity to ensure reliable supply of power to all. The planning & operation of the transmission system has thus shifted from regional to national level. Formation of a strong National Power Grid has been recognized as a flagship endeavour to steer the development of Power System on planned path leading to cost effective fulfilment of the objective of ‘Electricity to All’ at affordable prices. A strong All India Grid would enable exploitation of unevenly distributed generation resources in the country to their optimum potential by providing enhanced margins in inter-regional transmission system. These margins, together with open access in transmission, would facilitate increased trading in electricity leading to market determined generation dispatches thereby resulting in supply at reduced prices to the distribution utilities and ultimately to consumers benefit. 2.1 PROGRAMME OF DEVELOPMENT OF NATIONAL GRID As on today, the inter-regional transmission capacity of 11,450 MW is existing and inter-regional energy exchanges of more than 12 billion kWh in a year are taking place contributing to optimum utilization of generation capacity. The program is to achieve inter-regional capacity of 15750 MW by the end of 10th Plan and about 37,150 MW by the end of 11th Plan. Transmission systems within the regions to support the above inter-regional transmission capacity has been also planned. The plan for National Power Grid and the schemes have been identified. (Ref 2.2 of Main Working group Report) 2.2 North Eastern region, Sikkim and Bhutan have vast untapped hydro potential which is planned for development during 11th plan and beyond. A major component of this power will be utilised by deficit states in the northern and western region and for which reliable evacuation system is planned to be developed. The requirement of transmission system for evacuation of NER hydro power has been estimated corresponding to the capacity of hydro projects which may be feasible to develop say in the next about 20 years. This generation is estimated to be about 35000 MW in NER, about 8000 MW in Sikkim and about 15000 MW in Bhutan. Taking local development at accelerated pace resulting in demand within the NER, Sikkim and Bhutan to be in the range of 10000 – 12000 MW (presently it is about 1500 MW), the transmission requirement through the chicken neck works out to be of the order of 45000 MW. The total requirement including additional circuits for meeting the contingencies and reliability needs,

Executive Summary Working Group on Power-11th Plan (2007-12)

16

would work out to 7 or 8 numbers of 800 KV HVDC bi-pole lines and 4 or 5 numbers of 400kV double circuit lines – a total of 12 numbers of high capacity transmission corridors passing through the chicken neck. For this, RoW requirement would be about 1.5 Km in width considering minimum distance between adjacent towers to be such that fall of any tower does not affect the adjoining line. The first 800kV HVDC bi-pole line has been planned from a pooling substation at Biswanath Chariyali in North-eastern Region to Agra in Northern region. This is being programmed for commissioning matching with Subansiri Lower HEP in 2011-12. 2.3 ASSESSMENT OF TRANSMISSION CAPACITY REQUIREMENT The focus of transmission system development programme for the XI Plan is to provide adequate inter-regional and intra-regional transmission capacity so as to consolidate and strengthen the National Grid network towards a strong All India Grid. The inter-regional power exchange requirement has been assessed from possible scenarios of regional surpluses and deficit for the peak and off-peak conditions of winter, summer and monsoon months. Projections of deficit/surplus based on which transmission requirement has been assessed are given in Chapter-8 of this report. The projection based on programme of generation and anticipated demand aims at estimating the transmission requirement at the inter-regional level. Grid expansion plan evolved based on this projection would be able to cater to the needs of various feasible operating scenarios and also provide required margins to support market oriented power exchanges. (Ref Para 2.3 of main Working Group Report) 2.4 TRANSMISSION CAPACITY FOR TRADING The above method adopted for evolving the transmission system expansion plan provides sufficient transmission capacities which would have inherent margins for trading transactions. Transmission system implemented on the basis of the expansion plan evolved in this manner would enable trading across the regional boundaries towards optimal utilization of generation resources in the country for ultimate benefit of the consumer. As the system is evolved based on extreme dispatches, it would facilitate trading most of the time without congestion. Currently, trading is taking place through short-term bilateral contracts. With introduction of Power Exchange at National level, which is being envisaged to be in place in near future, trading would also take place through Power Exchange which would be day ahead contracts. All the short term as well as Power exchange transaction would need transmission capacity which would come out of the spare capacity inbuilt in the transmission system. The reliability and operational margins in the planned and implemented transmission system corresponding to the committed long-term transmission needs would provide the transmission capacity for trading of power. (Ref Para 2.5 of main Working Group Report)

Executive Summary Working Group on Power-11th Plan (2007-12)

17

2.5 TRANSMISSION CAPACITY MARGINS Transmission capacity through creation of additional transmission system could be provided based on long-term commitment for the transmission charges. It has been estimated that reliability and operation margins would be generally of the order of 25-30% of the transmission capacities required for meeting the firm transmission needs of the long-term open access. This level of redundancy would generally provided sufficient margins for trading needs. However, it should be noted that short-term open access (STOA) transactions operating on these margins, even if curtailable, cause reduction in the security level. Therefore, unless margins are increased by design, the system operator would have tendency to keep cushions by underestimating the operational margins. As such, and as the system security is of paramount importance, creation of increased margins by design becomes essential for accommodating STOA. (Ref para 2.5 of main Working Group Report) 2.6 TRANSMISSION PLANNING CRITERIA The network expansion has been planned to provide a reliable power system with sufficient redundancies for secure operation maintaining adequate margins at all times to maintain system parameters with in such limits that contingencies do not lead to loss of system integrity. The contingency criteria is based on ‘N-1’ in general and ‘N-2’ for large generating complexes and multi-line corridors. 2.7 TRANSMISSION SYSTEM FOR MERCHANT PLANTS Merchant plants would sell their power to customers who are not predetermined through Power exchange contracts. However, they are long term-user of the transmission system. The transmission system for the connectivity of the merchant plant as well as for meeting their transmission needs is required to be planned and built matching with the implementation of the merchant generation plant. Also, some of the generation plants have only a part of their generation capacity tied-up in long-term bi-lateral PPAs. When such plants seek long-term open access only for a part of their full generation capacity, they inherently also seek connectivity for the remaining capacity which would be available with them as a merchant plant capacity. As the transmission system in both the cases would be required to be planned and implemented corresponding to the full requirement, they are long-term beneficiary of the transmission system. For proper planning and implementation of transmission system, the merchant generators need to inform about region(s) in which they would generally sell their power, so that transmission system requirement for evacuation of their power and transmitting it to identified load centres could be assessed and any additional capacity required could be planned. As building the identified transmission schemes including obtaining necessary approvals by the identified transmission

Executive Summary Working Group on Power-11th Plan (2007-12)

18

company /companies would generally require almost same time as that for implementation generation projects, firming up of sellers and assessment of transmission requirement should be started at the earliest. (Ref para 2.5 of main Working Group Report) 2.8 TRANSMISSION SYSTEM UNDER STATE SECTOR A well planned and reliable transmission system at the National and Regional level would need to be complemented with development of matching transmission system at 220kV and 132kV and also the sub-transmission and distribution system so as to cater to the load growth and ensure proper utilisation of development in generation and transmission facilities for the ultimate goal of delivery of the services up to the end consumers in the country. Inadequate development of sub-transmission and distribution system facilities in the States of NER has been adversely affecting the reliability of power supply to the consumers and also hampering the load growth in the region. The transmission, sub-transmission and distribution systems of states require major strengthening/up-gradation. Transmission lines that are under outage require speedy restoration for bringing them into operation so that the states could avail their central sector shares as well as utilize their own generation without any constraint. Inadequacies in the transmission and distribution system had been on account of slow implementation of schemes due to various factors such as time consumed in E&F clearances, land acquisition, RoW constraints, fund limitation, organizational difficulties of state utilities, lack of vendor response due to locational factors, law and order, terrain specific difficulties, etc. Due to limited funding capabilities of state utilities, most of the required transmission projects are generally funded by NEC or by NLCPR under DONER and investment/funding approval of scheme so funded also takes additional time. All these issues need to be addressed to achieve the accelerated demand growth in NER. 2.9 ELEVENTH PLAN PROGRAMME 2.9.1 Evolving the Perspective Transmission System for XI Plan In transmission system development in the country, the focus of XI Plan programme is formation of the National Power Grid. A strong All India Grid would enable exploitation of unevenly distributed generation resources in the country to their optimum potential. The transmission capacity together with the margins provided for required redundancies as per planning criteria would provide a reliable transmission system. This would meet the firm transmission needs and with open access in transmission, would facilitate increased real time trading in electricity leading to market determined generation dispatches thereby resulting

Executive Summary Working Group on Power-11th Plan (2007-12)

19

in supply at reduced prices to the distribution utilities and ultimately to the consumers. Development of National Grid has been necessitated by the large thermal generation potential in eastern part of the country and equally large hydro generation potential in north-eastern part. It has also been spurred by the opportunity provided by open access, variation in hydrology / hydro potential and diversity of load across the country. It is envisaged to add during the XI plan period new inter-regional capacities of 20700 MW at 220kV and above. This would increase the total inter-regional transmission capacity of National Power Grid at 220kV and above from 16450 MW of XI Plan beginning to 37150 MW by 2011-12. (Ref Para 2.3 of main Working Group Report) 2.9.2 Fund Requirement for Transmission System Development and

Related Schemes Total Fund requirement for transmission system development and related schemes has been estimated as following: Rs Crores

Inter State system 75000 Intra State system 65000 TOTAL 140000

(For details please refer to Para 2.8 of main Working Group Report) 2.10 TECHNOLOGY DEVELOPMENT

2.10.1 Adopting New Technologies In Transmission System New technologies would need to be adopted and implemented in a proactive manner to achieve the objective of optimum utilization of the available transmission assets as well as conservation of Right-of-Way, reducing transmission costs, reduction of losses etc. Some of the new technologies adopted/being adopted in its transmission system include:

• High capacity 6000MW +800kV HVDC system • 765kV AC Transmission System • Ultra High Voltage AC Transmission System(1000kV) • Application of Series Compensation • Flexible AC Transmission System (FACTS) • Upgradation/Uprating of transmission line • High temperature endurance conductor • Tall/Multi-circuit & Compact tower • High Surge Impedance Loading Line (HSIL)

Executive Summary Working Group on Power-11th Plan (2007-12)

20

• Remote operation of substation, substation automation and Gas Insulated substation (GIS)

• All Aluminum Alloy Conductors (AAAC) and Polymer/Composite Insulators.

• Development of disc insulators of 320kN & 420kN indigenously for both AC & HVDC applications, as import substitution.

• Indigenous development of semi-conducting glazed insulators (Offering better pollution performance)

• Introduced source/process inspection of equipment to ensure zero defect • Airborne Laser Terrain Mapping (ALTM) for detailed route survey • Thermo-vision scanning of the lines and sub-stations • Conditional monitoring of equipment • Preventive maintenance of Transformers using State-of-art Oil testing

laboratories set up by the company • Emergency Restoration System (ERS)

For modernization of transmission system through latest technology integration, two pronged strategies have been envisaged as under:

• Enhance capacity and reliability of existing systems. • Suitable technology for new systems keeping in view the long term

perspective

3.0 DISTRIBUTION INCLUDING VILLAGE & HOUSEHOLD

ELECTRIFICATION 3.1 OVERVIEW OF DISTRIBUTION SECTOR The electricity distribution section is the most daunting sector due to its interface with the public at large with different needs and expectations and varying degrees of capacity to pay. The distribution sector is the cutting edge and as the need to improve this sector was realized, in the 10th plan the emphasis was on steps to reduce the huge aggregate technical and commercial losses, control the theft & pilferage and rationalise the tariff structures. Investment was also made in the distribution sector and across the states reforms were taken up. Major schemes like Accelerated Power Development & Reform Program for urban areas and the Rajiv Gandhi Grameen Vidyutikaran Yojana was also initiated in the 10th plan which aimed at bringing in investment in urban areas and creating an electricity infrastructure in rural areas. There is however a pressing need to continue these efforts in the 11th plan so as to reduce the AT&C losses and to continue with the reforms in the distribution sector to provide an affordable, good quality and reliable power supply to the citizen of India, be it in urban or rural areas.

Executive Summary Working Group on Power-11th Plan (2007-12)

21

The distribution of power can be studied in two distinct components viz. ,

(i) Distribution of power in urban areas, and (ii) Distribution of power in rural areas.

(Refer Para 3.0 of main Working Group Report) 3.2 QUALITATIVE APPROACH 3.2.1 Distribution of power in urban areas The Accelerated Power Development & Reform Program (ARDRP) was aimed at bringing about improvement in the urban distribution sector by funding investment in the distribution network, and by incentivising the states who performed well in reducing losses. The Ministry of Power constituted a task force in 2006 under Shri P. Abraham which has recommended that APDRP may be continued with investment and incentive component beyond the 10th plan. However the conditions may be made more stringent and reform oriented. While broadly agreeing with recommendations of the Abraham Committee report, it is felt that APDRP needs to be continued in 11th plan with revised terms and conditions. The focus of the programme should be on establishment of base line data, which shall enable reduction of AT&C losses in major towns of the country through strengthening , upgradation of sub-transmission and distribution network and adoption of Information Technology in the areas of energy accounting & auditing and improvement in consumer services through establishment of Bijlee Sewa Kendras. The programme may focus on the town and cities covering all district headquarters and town with population of more than 50,000 and town with lesser population in special category sates . The investment and incentive components may be merged and funding may be in form of loan assistance with the provision of conversion of loan to incentives to the distribution companies on achieving specified milestones with regard of reforms and reduction of AT&C losses. There also needs to be a provision of incentive to the employees of the utilities. The loan assistance may be converted to grant (50 % for general category states and 90 % for special category states) and the loan should be from Central Sector with a moratorium of three years on interest and on repayment. The rate of interest may be as determined by Ministry of Finance from time to time. ADDRP assistance should be also available to private distribution companies as the ultimate beneficiary was the consumer. The loan / grant needs to be funded under Central sector through REC / PFC. 3.2.2 Distribution of power to rural areas RGGVY (Rajiv Gandhi Grameen Vidyutikaran Yojna) aims to achieve power for all by 2009 and in the long run accelerate rural development, adequate employment and eliminate poverty through irrigation, development of small scale industries, provision of health care and promotion of education and information

Executive Summary Working Group on Power-11th Plan (2007-12)

22

technology. RGGVY also aims at bridging the urban rural gap and provide reliable quality power supplies to rural areas. However, in order to bring about access to electricity to all rural households, there would be need to widen the electricity coverage to hamlets / habitations of the country. In case the funding of RGGVY becomes a constraint it is proposed that in the first phase all un-electrified villages and hamlets with more than 300 population are covered. Those hamlets with less then 300 populations may be excluded except those in hilly, forest, desert and tribal areas. The total cost of phase 1 is estimated at Rs. 24,000 crore. Phase 1 would be completed by 2009 and would reach electricity to all the un-electrified villages and about 3 lakh hamlets. The second phase would start from 2009 onwards and would reach electricity to the balance un-electrified hamlets and complete the task of providing access to all rural households by 2012 . Second phase is estimated around Rs. 16,000 crores. The two phases is estimated around at Rs. 40,000 crores . (Refer Para 3.7 of main Working Group Report) 3.2.3 Prioritization of RGGVY Maximum number of un-electrified villages exist in the under developed States. RGGVY programme should give top priority in the allocation of funds for these States. Second priority should be given for intensive electrification of such States where the household electrification is below the national average. Third priority should be on the intensive electrification for the remaining States. (Refer Para 3.7.2 of main Working Group Report) 3.2.4 Public Private Partnership through rural franchisees Management of rural infrastructure has to be based upon all inclusive growth model that involves rural set ups and provides the local Panchayat Raj institutions a supervisory function to ensure the durability and sustainability of electricity infrastructure. Franchisee system for management of rural distribution has been made mandatory under RGGVY to make the revenue model sustainable. RGGVY allows enterprising individuals, NGOs, private entrepreneurs, co-operatives, Panchayat Raj institutions to become franchisees. The franchisees system needs major push in 11th plan with initiatives for capacity building and financial support. (Refer Para 3.23 of main Working Group Report)

Executive Summary Working Group on Power-11th Plan (2007-12)

23

3.2.5 Financial support to Franchisees Not many people are coming forward for franchiseeship especially from remote rural areas where loads are small and sustainability difficult. As franchisees will be mainly rural entrepreneurs, they will have difficulties in raising small funds for their micro level projects to guarantee their performance or meet working capital requirements. No funds have been allocated under RGGVY for development of franchisees. It is necessary to develop institutions that extend micro credit to meet the franchise level financing needs. 3.2.6 Distribution of power in Rural Areas through Decentralized

Distributed Generation (DDG) Electricity Act, 2003 provides the requisite framework for accelerating electrification in rural areas with necessary empowerment. It permits operation of stand alone systems independent of the regulatory regime. Integrated Energy Policy 2006 has estimated the requirement of power at 8,00,000 MW by 2031. It implies that India must add 25000 MW or more every year for a quarter century. It is a colossal task and would require exploitation of all renewable and fossil resources. Secondly, the creation of huge rural village and block level electricity infrastructure will require immediate supply of power. Village level energy resources like biomass, hydro and solar energy will help to reduce the dependence on grid based thermal, gas nuclear and hydro power. India has a potential to generate 10-15000 MW of power from the available biomass. DDG based on this resource will meet the critical needs of parched villages asking for timely power. Cost of electricity should be based on cost to serve basis and DDG to be taken up on a mission mode. Viability gap funding may be adopted in case of grid interconnected schemes. Bio mass cultivation may be encouraged to support DDG and bio-fuel cultivation to be funded by Financial Institutions (FIs) / Banks. However, multifuel technologies may be encouraged. (Refer Para 3.10 of main Working Group Report) 3.2.7 Pilot Programmes on DDG The problem of providing power to rural areas would be critical when the infrastructure under RGGVY becomes ready but remains without the supply of power. To attract the entrepreneurs, REC may be encouraged to put up pilot projects in the selective rural areas to have a demonstrative effect. Such projects could be linked to the neighboring substations and incorporated as the long-term lease infrastructure under RGGVY on cheaper finance. DDG will go a long way to ameliorate the shortages of power in rural areas. Nationwide survey of available resources in each villages to be undertaken in fixed time frame through a nodal agency like REC. (Refer Para 3.10 of main Working Group Report)

Executive Summary Working Group on Power-11th Plan (2007-12)

24