CDP 2015 Climate Change 2015 Information Request 2015 Climate Change 2015 Information Request ......

57

CDP CDP 2015 Climate Change 2015 Information Request VESTEL ELEKTRONİK SANAYİ VE TİCARET A.Ş. Module: Introduction Page: Introduction CC0.1 Introduction Please give a general description and introduction to your organization. Operating in the fields of consumer electronics, white goods and information technologies with its more than 13,000 employees, Vestel Group of Companies (Vestel), which is the flagship of Zorlu Group, comprises of 29 companies, 13 of which are abroad. Vestel is one the largest consumer electronics and white goods producers in Turkey and Europe. The Company’s manufacturing facilities are located in Manisa, Turkey and Alexandrov, Russia. The Company enjoys economies of scale which results in productivity, efficiency, and cost advantages by undertaking the majority of its manufacturing within a single 600 thousand square meter area, namely Vestel City, the largest industrial complex in Europe. Vestel Elektronik was established in 1984 and is mainly engaged in production of televisions, set-top- boxes, display panels, touch screens, tablets,handphones, led lightings. The Company is among the leading ODMs ( Original Design Manufacturers ) in World Wide LCD TV market, as ranked #2 in Q4 2014, #2 in Q4 2013 in the European Market (#8 in 2011, #4 in 2012), while enjoys being one of the three major players in the domestic LCD TV market with its well-known Vestel brand. The strategic importance given to R&D has a key role in Vestel’s ability to reach the fast rate of gr owth and strong competitive position the Company enjoys today. Vestel has improved its superior production technology and design development capability continuously though its team of 900 engineering professionals employed in its R&D centers. The Company is attracting increasing attention with its modern consumer friendly and innovative products. Vestel designs its products and manufacturing processes to maximize productivity, while making a special effort to protect the nature and raise environmental awareness. Vestel places its “friendly technology” concept at the center of its brand culture, strengthening its innovative power with consumer and environmentally friendly products. Underlying Vestel’s unique, pioneering designs and innovative products is the Company’s mission to leave a habitable world for future generations while envisioning the technology of the future. Vestel continually strives to minimize all negative impacts on the environment with its new products and targets to increase its R&D investments toward the direction of sustainable innovation.By producing world-class quality products, Vestel was listed among the “Top 250 Consumer Products Companies list” in Deloitte’s “Global Powers of The Consumer Products Industry 2014” report. Vestel conducts its business processes in accordance with ISO 14001 Environment Management System (EMS), which is integrated with ISO 9001 Quality Management System (QMS) and adopted to Total Quality Approach,since 1998.Vestel also certified its Energy Management System with ISO50001 since 2012. Vestel also implements Total Productive Maintenance (TPM) and Supply Chain Excellence (SCM) methodologies for cost reduction,quality and process improvement while increasing its competitive edge day by day through its flexible production structure. CC0.2

Transcript of CDP 2015 Climate Change 2015 Information Request 2015 Climate Change 2015 Information Request ......

CDP CDP 2015 Climate Change 2015 Information Request

VESTEL ELEKTRONİK SANAYİ VE TİCARET A.Ş.

Module: Introduction

Page: Introduction

CC0.1

Introduction

Please give a general description and introduction to your organization. Operating in the fields of consumer electronics, white goods and information technologies with its more than 13,000 employees, Vestel Group of Companies (Vestel), which is the flagship of Zorlu Group, comprises of 29 companies, 13 of which are abroad. Vestel is one the largest consumer electronics and white goods producers in Turkey and Europe. The Company’s manufacturing facilities are located in Manisa, Turkey and Alexandrov, Russia. The Company enjoys economies of scale which results in productivity, efficiency, and cost advantages by undertaking the majority of its manufacturing within a single 600 thousand square meter area, namely Vestel City, the largest industrial complex in Europe. Vestel Elektronik was established in 1984 and is mainly engaged in production of televisions, set-top-boxes, display panels, touch screens, tablets,handphones, led lightings. The Company is among the leading ODMs ( Original Design Manufacturers ) in World Wide LCD TV market, as ranked #2 in Q4 2014, #2 in Q4 2013 in the European Market (#8 in 2011, #4 in 2012), while enjoys being one of the three major players in the domestic LCD TV market with its well-known Vestel brand. The strategic importance given to R&D has a key role in Vestel’s ability to reach the fast rate of growth and strong competitive position the Company enjoys today. Vestel has improved its superior production technology and design development capability continuously though its team of 900 engineering professionals employed in its R&D centers. The Company is attracting increasing attention with its modern consumer friendly and innovative products. Vestel designs its products and manufacturing processes to maximize productivity, while making a special effort to protect the nature and raise environmental awareness. Vestel places its “friendly technology” concept at the center of its brand culture, strengthening its innovative power with consumer and environmentally friendly products. Underlying Vestel’s unique, pioneering designs and innovative products is the Company’s mission to leave a habitable world for future generations while envisioning the technology of the future. Vestel continually strives to minimize all negative impacts on the environment with its new products and targets to increase its R&D investments toward the direction of sustainable innovation.By producing world-class quality products, Vestel was listed among the “Top 250 Consumer Products Companies list” in Deloitte’s “Global Powers of The Consumer Products Industry 2014” report. Vestel conducts its business processes in accordance with ISO 14001 Environment Management System (EMS), which is integrated with ISO 9001 Quality Management System (QMS) and adopted to Total Quality Approach,since 1998.Vestel also certified its Energy Management System with ISO50001 since 2012. Vestel also implements Total Productive Maintenance (TPM) and Supply Chain Excellence (SCM) methodologies for cost reduction,quality and process improvement while increasing its competitive edge day by day through its flexible production structure.

CC0.2

Reporting Year

Please state the start and end date of the year for which you are reporting data. The current reporting year is the latest/most recent 12-month period for which data is reported. Enter the dates of this year first. We request data for more than one reporting period for some emission accounting questions. Please provide data for the three years prior to the current reporting year if you have not provided this information before, or if this is the first time you have answered a CDP information request. (This does not apply if you have been offered and selected the option of answering the shorter questionnaire). If you are going to provide additional years of data, please give the dates of those reporting periods here. Work backwards from the most recent reporting year. Please enter dates in following format: day(DD)/month(MM)/year(YYYY) (i.e. 31/01/2001).

Enter Periods that will be disclosed

Wed 01 Jan 2014 - Wed 31 Dec 2014

CC0.3

Country list configuration

Please select the countries for which you will be supplying data. If you are responding to the Electric Utilities module, this selection will be carried forward to assist you in completing your response.

Select country

Turkey

CC0.4

Currency selection

Please select the currency in which you would like to submit your response. All financial information contained in the response should be in this currency. TRY

CC0.6

Modules

As part of the request for information on behalf of investors, electric utilities, companies with electric utility activities or assets, companies in the automobile or auto component manufacture sub-industries, companies in the oil and gas sub-industries, companies in the information technology and telecommunications sectors and companies in the food, beverage and tobacco industry group should complete supplementary questions in addition to the main questionnaire. If you are in these sector groupings (according to the Global Industry Classification Standard (GICS)), the corresponding sector modules will not appear below but will automatically appear in the navigation bar when you save this page. If you want to query your classification, please email [email protected]. If you have not been presented with a sector module that you consider would be appropriate for your company to answer, please select the module below. If you wish to view the questions first, please see https://www.cdp.net/en-US/Programmes/Pages/More-questionnaires.aspx.

Further Information

VESTEL Electronics is the TV,smartphone,tablet, Led lightings,infomative screens, set top box manufacturing plant of VESTEL Group of Companies. Employing more than 8000 people, VESTEL’s production facilities are located in MANISA in Turkey. With 256.000 m2 of enclosed space, it has a total annual production capacity of 15 million units.VESTEL Electronics has 6 production facilities; Electronic Board Production,Plastic Injection,Paint Shop,Styrofoam Production, Digital(Smartphone , Tablet , Interactive Smartboards,Informative Screen,Touch screen) Production,Final Assembly Manufacturing (Led TV, Set top Box, Led Lighting) at the highest quality standards requires discipline as well as knowledge and experience. Total Productive Maintenance approach implemented throughout the manufacturing process improves efficiency and productivity in all areas and also ongoing SCM(Supply Chain Excellence) projects , making VESTEL a World Class Manufacturer.

Attachments

https://www.cdp.net/sites/2015/59/21159/Climate Change 2015/Shared Documents/Attachments/ClimateChange2015/CC0.Introduction/2014 AWARDS.pdf https://www.cdp.net/sites/2015/59/21159/Climate Change 2015/Shared Documents/Attachments/ClimateChange2015/CC0.Introduction/Vestel_TPM_Excellence Award_Certificate.jpg https://www.cdp.net/sites/2015/59/21159/Climate Change 2015/Shared Documents/Attachments/ClimateChange2015/CC0.Introduction/Vestel_TPM_Excellence_Award_Certificate2.jpg

Module: Management

Page: CC1. Governance

CC1.1

Where is the highest level of direct responsibility for climate change within your organization?

Board or individual/sub-set of the Board or other committee appointed by the Board

CC1.1a

Please identify the position of the individual or name of the committee with this responsibility

(i)The highest level of direct responsibility for climate change rests with Mr. İhsaner Alkım, who is a member of the Executive Board responsible for top level management of all environmental, energy, and social responsibility issues. (ii)Position in the corporate structure and climate change related responsibilities: Mr. İhsaner Alkım reports directly to the Group CEO, Mr. Turan Erdoğan.

CC1.2

Do you provide incentives for the management of climate change issues, including the attainment of targets?

Yes

CC1.2a

Please provide further details on the incentives provided for the management of climate change issues

Who is entitled to benefit from these incentives?

The type of incentives

Incentivized performance

indicator

Comment

All employees Recognition (non-monetary)

Emissions reduction target Energy reduction project

Employees can submit ideas for new environmental programs, and are eligible to receive spot awards such as gifts for coming up with ideas that enhances the company's overall environmental performance, including those that result in greenhouse gas emissions reductions according to TPM Suggestion&Appreciation Evaluation System.

Who is entitled to benefit from these incentives?

The type of incentives

Incentivized performance

indicator

Comment

Business unit managers Monetary reward

Emissions reduction project Energy reduction project Efficiency project

Notable performance on environment and climate change issues (e.g. site activities for GHG reduction and product design that contributes to energy efficiency) and prevention of environmental incidents are reflected on the annual performance evaluation of Business Units

Executive officer Monetary reward

Emissions reduction project Energy reduction project Efficiency project Behaviour change related indicator

Notable performance on environment and climate change issues (e.g. site activities for GHG reduction and product design that contributes to energy efficiency) and prevention of environmental incidents are reflected on the annual performance evaluation of Business Units

Environment/Sustainability managers

Monetary reward

Emissions reduction project Emissions reduction target Energy reduction project Energy reduction target Efficiency project Efficiency target Behaviour change related indicator

Notable performance on environment and climate change issues (e.g. site activities for GHG reduction and product design that contributes to energy efficiency) and prevention of environmental incidents are reflected on the annual performance evaluation of Business Units

Further Information

VESTEL ELECTRONICS is continue to impelement TPM (Total Productive Maintenance) program and was awarded by Japan Institute of Plant Maintenance at the end of 2012. In the framework of this program , Vestel slogan comes from the fact that Vestel is friend to its employees, customers,suppliers, share holders, the community and beyond all, mother earth. Vestel Electronics started TPM program to avoid any sacrifice of quality while remaining competitive. In accordance with this aims, Vestel mainly focused on following items: Reducing number of work accidents, Increasing production capacity (OEE), Decreasing unit cost ,Increasing First time true rate, Reducing Scrap rate, Decreasing Breakdowns, Decreasing Service Call Rate, Reducing Maintenance Costs , Decreasing spare part stocks and usage cost, Improving Time to delivery, Shortening lead times on all processes, Decreasing Setup times, Becoming a benchmark plant in 5S achievement and creating a better working environment, Reducing Energy use, Increasing Number of suggestions, Reducing Environmental pollution, Reducing Consumable material usage. These aims can serve reducing carbon disclosure;directly or indirectly. In order to reach these goals, VESTEL builds up 9 committees and Suggestion and Appreciation System all around the factory. Then,VESTEL identified and set the rules for evaluation and awarding. The TPM excellence and TPM excellence continuity award of VESTEL can be seen attached.

Attachments

https://www.cdp.net/sites/2015/59/21159/Climate Change 2015/Shared Documents/Attachments/ClimateChange2015/CC1.Governance/TS EN ISO 14001_Environmental Management System Certificate.pdf https://www.cdp.net/sites/2015/59/21159/Climate Change 2015/Shared Documents/Attachments/ClimateChange2015/CC1.Governance/TS EN ISO 50001_Energy Management System Certificate.pdf https://www.cdp.net/sites/2015/59/21159/Climate Change 2015/Shared Documents/Attachments/ClimateChange2015/CC1.Governance/Vestel_TPM_Excellence Award_Certificate.jpg https://www.cdp.net/sites/2015/59/21159/Climate Change 2015/Shared Documents/Attachments/ClimateChange2015/CC1.Governance/TS 18001_Labour Health and Safety Certificate.pdf https://www.cdp.net/sites/2015/59/21159/Climate Change 2015/Shared Documents/Attachments/ClimateChange2015/CC1.Governance/TS EN ISO 9001_Quality Management System Certificate.pdf https://www.cdp.net/sites/2015/59/21159/Climate Change 2015/Shared Documents/Attachments/ClimateChange2015/CC1.Governance/Vestel_TPM_Excellence_Award_Certificate2.jpg https://www.cdp.net/sites/2015/59/21159/Climate Change 2015/Shared Documents/Attachments/ClimateChange2015/CC1.Governance/TS ISO IEC 27001_Information Security Management System Certificate.pdf

Page: CC2. Strategy

CC2.1

Please select the option that best describes your risk management procedures with regard to climate change risks and opportunities

Integrated into multi-disciplinary company wide risk management processes

CC2.1a

Please provide further details on your risk management procedures with regard to climate change risks and opportunities

Frequency

of monitoring

To whom are results

reported?

Geographical areas

considered

How far into

the future are risks

considered?

Comment

Annually

Board or individual/sub-set of the Board or committee appointed by the Board

The assessment of risks is mainly relying on monitoring of environmental data related to climate change in domestic and external markets.

> 6 years

(i)Zorlu Holding's Corporate Risk Management Department commenced -at first quarter of 2012- its operations as support. In this context, to be effective for all of the associated companies operating within Zorlu Holding, Zorlu Risk Policy;Procedure and Enterprise Risk Management , Key Risk Criteria framework was prepared. Studies as well as the evaluation of 9 risk item financial risks, operational, environmental technological, etc. are included in the risk management system. (ii)Periodical "Vestel Search Conference" is done once a 5 years with participation of board members and employees from different levels and attendies evaluate long term risks and opportunities for future of Vestel by workshops.

CC2.1b

Please describe how your risk and opportunity identification processes are applied at both company and asset level

The risk management procedure related to climate change risks and opportunities basically involves consideration of regulatory and reputational risks, which may have the highest impact on the demand for our products (prioritization criteria). The procedure is mostly influenced by the climate change awareness among the top-level management and the requests/feedback of our consumers and retailers concentrating more on climate change/energy efficiency related performance. The assessment of risks is mainly relying on monitoring of environmental data related to climate change such as GHG emissions and emission intensity (i.e. GHG emissions per product) which is being collected and processed by the Management Systems unit. Zorlu Risk Management Group and Chief of Management Systems regularly report to the responsible executive board member and observed risks (if any) are being discussed by the Board and actions are being defined by the top management. Physical risks (risks/opportunities at an asset level) are also assessed by Zorlu Risk Management Group and related departments like IT,Maintenance&Investment etc..They continuously evaluate Vestel factory and office facilities.

CC2.1c

How do you prioritize the risks and opportunities identified?

The major environmental and energy performance reporting including performance related to climate change is done by our ISO 14001 Environmental Management representative and ISO 50001 Energy Management Representative at the annual screening meeting. However, chief of Management Systems and Facility Energy Manager have continuous and direct communication with the responsible executive board member for matters that require earlier consideration. There also the Audit Committee, operating under Zorlu Holding, implementing audits also on our environmental and energy performance, which identifies any problems related to environmental compliance and implementation of environmental strategy. Included in the collected environmental data, the GHG emissions data is presented with Scope 1, Scope 2 and Scope 3 emissions. , Zorlu Holding's Corporate Risk Management Department commenced -at first quarter of 2012- its operations as support. In this context, to be effective for all of the associated companies operating within Zorlu Holding, Zorlu Risk Policy;Procedure and Enterprise Risk Management framework was prepared. Studies as well as the evaluation of financial risks, operational, environmental technological, etc. are included in the non-financial risks.

CC2.1d

Please explain why you do not have a process in place for assessing and managing risks and opportunities from climate change, and whether you plan to introduce such a process in future

Main reason for not having a process

Do you plan to introduce a process?

Comment

CC2.2

Is climate change integrated into your business strategy?

Yes

CC2.2a

Please describe the process of how climate change is integrated into your business strategy and any outcomes of this process

Having received significant attention of governments, investors and also individuals over the last decades, the risks associated with the climate change are inevitably affecting the manufacturing industry as well as all industries, although the risks are assumed not to have considerably higher impacts as in the case of energy sector and/or energy intensive industries. As Vestel Electronics, we are placing ‘environmental sustainability’ and decreasing the ecological footprint of our products at the core of our business strategy. Furthermore, as being the manufacturer of high technology energy efficient products, which help our consumers to actually reduce

their footprint, we have increased awareness on the impacts of climate change on our business. Climate drivers are important factors that we pay attention in building our broad company strategy that addresses; •Caring for the environment and climate starting from the designing phase of our products to the manufacturing phase •Prioritizing investment and expansion in manufacturing of the most energy efficient products in our production portfolio •Increasing RD activities and dedicated budget for developing new production methodologies and products with decreased ecological footprint •Continuously looking for opportunities to reduce waste and enable use of materials suitable for reuse and recycle • Promoting use of new technologies to save energy and to boost energy efficiency in all operations •Raising employees’ and consumers’ awareness on environmental protection and energy efficiency •Ensuring effective communication to stakeholders and proper disclosure of environmental and climate performance The basic influence of climate change in our strategy is that we have taken the first step in preparing our company for the impacts by working on understanding how our business activities and investments are affected by climate change and preparing the infrastructure to make it a part of our management culture also by identifying the interdependencies between climate change risks and other risks relevant to our company. Investing in R&D has always been valued by our company, and R&D that is directed to serving for eliminating climate risks, such as developing practices and/or products that improve efficiency and/or eliminate emissions both on the production side and on the consumer side, has become our leading strategy. While building our climate strategy, in the short term, we have started by quantifying our emissions broadly and we are planning to prepare a detailed carbon emission inventory and seek for third party verification. In the medium term, we will also be identifying and quantifying the carbon impacts along our value chain. In the long terms we will be planning for putting targets related to our climate performance. On the product end, our strategy has basically led to manufacturing of Energy Class A TVs and to our decision in expanding business in manufacturing of LED TVs&eco TVs and LED lightings in 2014 by increasing our production capacity. We also spared an unlimited R&D budget for developing products with improved environmental performance. Vestel Electronics, which is already a strong market player, is gaining distinctive competency through implementation of its business strategy, which enables our company to be the manufacturer of most energy efficient products with decreased ecological footprint, which are being preferred by the environmentally conscious consumers, who are increasing with a sharp pace.

CC2.2b

Please explain why climate change is not integrated into your business strategy

CC2.2c

Does your company use an internal price of carbon?

No, and we currently don't anticipate doing so in the next 2 years

CC2.2d

Please provide details and examples of how your company uses an internal price of carbon

CC2.3

Do you engage in activities that could either directly or indirectly influence public policy on climate change through any of the following? (tick all that apply)

Direct engagement with policy makers Trade associations

CC2.3a

On what issues have you been engaging directly with policy makers?

Focus of legislation

Corporate Position

Details of engagement

Proposed legislative solution

Energy efficiency

Support

We are engaging with policy makers, i.e. Ministry of Environment and Urbanisation, Ministry of Energy and Natural Sources, Ministry of Science, Industry and Technology as an individual company as well as with trade associations. During the EU energy labeling adaptation process in Turkey, Vestel shared its opinions with Ministry of Science, Industry and Technology.

Energy Labeling Regulation is completely supported by Vestel.

Other: Support

We are engaging with Turkish Standards Institution via Mirror Committees. Because Turkish Standards Institution is a member of International Organization for Standardization (ISO), and the International Electrotechnical Commission (IEC) on 26 May 1955 and 1 January 1956 respectively, we as Vestel Electronics directly influence the consumer products, energy consumption and environment related standards.

As a major player, by joining Mirror Committees, we support the creation and improvement of the standards.

CC2.3b

Are you on the Board of any trade associations or provide funding beyond membership?

Yes

CC2.3c

Please enter the details of those trade associations that are likely to take a position on climate change legislation

Trade association

Is your position

on climate change

consistent with

theirs?

Please explain the trade association's position

How have you, or are you attempting to, influence the position?

TESİD Consistent

The Electronic Industries in Turkey are organized in an independent association in order to deal with the common interests of the individual companies. In 2000, due to rapid changes in the high tech industry TESID has decided to widen its scope and include software houses and telecom operators accordingly. MISSION: Leading the Turkish Electronics Industry, Information Technologies and related service sectors towards continuous competitiveness and increasing its contributions to the national economy and the people. VISION: 1. Encouraging and supporting technological creativity to achieve a common goal among universities, industry and the government so that competitive, flexible, productive and high quality goods and services are produced. 2. To support: b) the development of a modern, globally competitive electronics industry. c) the expansion of capacity and productivity as well as the enchancement of the investment opportunities of the industry. d) the improvement of the standard of living of employees, for greater employee satisfaction. 3. Concerning policies, strategies, standards and development within the electronics industry. 4. Supporting the Electronics Industry to develop into a strong, environmentally aware, safety conscious establishment that is an overall positive contributor to the community.

Supporting the Electronics Industry to develop into a strong, environmentally aware, safety conscious establishment that is an overall positive contributor to the community.

TÜRKBESD Consistent

White Goods Manufacturers’ Association of Turkey, whose acronym is TÜRKBESD, was established in 1986 as White Goods Manufacturers’ Association (BESD) by the leading white goods companies of the sector. In 1999, following its membership to the European Union’s senior organization of the field CECED (European Committee of Domestic Equipment Manufacturers), the association received permission to use “Turkey” in its name through a Cabinet of Ministers decree, and changed its name to White Goods Manufacturers’ Association of Turkey (TÜRKBESD). Currently, the association has six members: Arçelik, B/S/H,

Vestel is one of the board members of TURKBESD and works close with other members to drive TURKBESD policies related with energy efficiency, environmental compliance regulations. For instance, recent studies are about the determining control and collect methods of waste electrical and electronic equipments via directives such as AEEE.

Trade association

Is your position

on climate change

consistent with

theirs?

Please explain the trade association's position

How have you, or are you attempting to, influence the position?

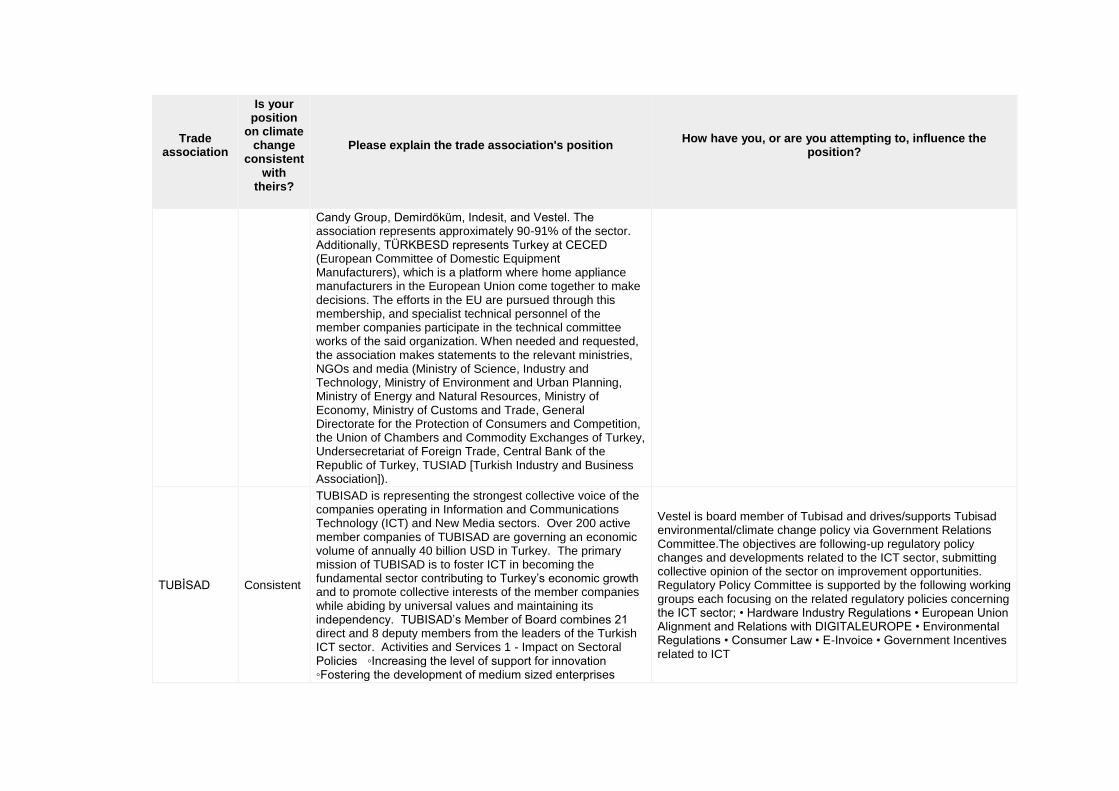

Candy Group, Demirdöküm, Indesit, and Vestel. The association represents approximately 90-91% of the sector. Additionally, TÜRKBESD represents Turkey at CECED (European Committee of Domestic Equipment Manufacturers), which is a platform where home appliance manufacturers in the European Union come together to make decisions. The efforts in the EU are pursued through this membership, and specialist technical personnel of the member companies participate in the technical committee works of the said organization. When needed and requested, the association makes statements to the relevant ministries, NGOs and media (Ministry of Science, Industry and Technology, Ministry of Environment and Urban Planning, Ministry of Energy and Natural Resources, Ministry of Economy, Ministry of Customs and Trade, General Directorate for the Protection of Consumers and Competition, the Union of Chambers and Commodity Exchanges of Turkey, Undersecretariat of Foreign Trade, Central Bank of the Republic of Turkey, TUSIAD [Turkish Industry and Business Association]).

TUBİSAD Consistent

TUBISAD is representing the strongest collective voice of the companies operating in Information and Communications Technology (ICT) and New Media sectors. Over 200 active member companies of TUBISAD are governing an economic volume of annually 40 billion USD in Turkey. The primary mission of TUBISAD is to foster ICT in becoming the fundamental sector contributing to Turkey’s economic growth and to promote collective interests of the member companies while abiding by universal values and maintaining its independency. TUBISAD’s Member of Board combines 21 direct and 8 deputy members from the leaders of the Turkish ICT sector. Activities and Services 1 - Impact on Sectoral Policies ◦Increasing the level of support for innovation ◦Fostering the development of medium sized enterprises

Vestel is board member of Tubisad and drives/supports Tubisad environmental/climate change policy via Government Relations Committee.The objectives are following-up regulatory policy changes and developments related to the ICT sector, submitting collective opinion of the sector on improvement opportunities. Regulatory Policy Committee is supported by the following working groups each focusing on the related regulatory policies concerning the ICT sector; • Hardware Industry Regulations • European Union Alignment and Relations with DIGITALEUROPE • Environmental Regulations • Consumer Law • E-Invoice • Government Incentives related to ICT

Trade association

Is your position

on climate change

consistent with

theirs?

Please explain the trade association's position

How have you, or are you attempting to, influence the position?

◦Facilitating standardization of regulations imposed on taxation and foreign trade and auditing of compliance with them ◦Advocating widespread compliance with the copyright protection laws ◦Increasing the number of public services offered via electronic platforms ◦Supporting environment-friendly technologies 2 - Increasing Publicity and Awareness about the Sector ◦Creating awareness about the economic importance of the sector ◦Announcing nationwide and international success stories ◦Communicating collective objectives of the sector ◦Building strong relationships with the local and foreign press 3 - Sectoral Growth and Profitability ◦Development of local value added solutions and services ◦Launching sectoral standards, certification programmes and regulations ◦Fostering high quality in education and employment ◦Establishing proper conditions for fair competition ◦Fostering export sales of technological products and services ◦Enabling collaboration and information sharing among companies in sector 4 - Center for Reliable Commercial and Intellectual Information ◦Reliable sectoral data creation and sharing ◦Performing sectoral data analysis and market research ◦Informing the society about sectoral trends and estimates

EU Trade Associations

Consistent

Vestel Electronics has membership on Trade Associations of some European countries via its sales offices i.e. Vestel Germany, Vestel UK, Vestel France, Vestel Italy, Vestel Iberia which are located in these countries.

We are engaging with European countries' policy makers by sharing our comments via Vestel sales offices.

CECED Consistent Vestel Electronics has membership on CECED (The European Committee of Domestic Equipment Manufacturer ).The membership type is direct membership.

Vestel is one of the direct members of CECED and works close with other members to drive CECED policies related with energy efficiency, environmental compliance regulations.

CC2.3d

Do you publicly disclose a list of all the research organizations that you fund?

CC2.3e

Do you fund any research organizations to produce or disseminate public work on climate change?

CC2.3f

Please describe the work and how it aligns with your own strategy on climate change

CC2.3g

Please provide details of the other engagement activities that you undertake

CC2.3h

What processes do you have in place to ensure that all of your direct and indirect activities that influence policy are consistent with your overall climate change strategy?

We are engaging with policy makers, i.e. Ministry of Environment and Urbanisation, Ministry of Energy and Natural Resources, Ministry of Science,Industry and Technology, Turkish Standards Institution as an individual company and also through TESID (Turkish Association of electronics and Information Industries), TURKBESD (Turkish White Goods Manufacturers' Association) , TUBISAD (Informatics Industry Association) CECED(The European Committee of Domestic Equipment Manufacturer ). and European countries' trade associations via Vestel sales offices. We have been invited by the Climate Platform, which we welcomed as it presents us the opportunity to engage in climate change issues within a network of companies having increased awareness. Our engagement with policy makers is mainly providing our feedback on transposition and/or implementation of relevant EU Directives. We have been advocating all actions that serve for improving the environmental performance required from our sector both related to manufacturing processes and the products themselves. We were the first company to have complied with the EU Directives relevant for our sector that encourages improving products energy efficiency and we have given our feedback many times in the process of aligning our legislation with the EU including, Energy Related Products(ErP) Eco-Design Directive, Energy Labeling Directive, Waste Electrical and Electronic Equipment (WEEE) Directive and Restriction Of The Use Of Certain Hazardous Substances (RoHS) Directive.

CC2.3i

Please explain why you do not engage with policy makers

CC2.4

Would your organization's board of directors support an international agreement between governments on climate change, which seeks to limit global temperature rise to under two degree Celsius from pre-industrial levels in line with IPCC scenarios such as RCP2.6?

No

CC2.4a

Please describe your board's position on what an effective agreement would mean for your organization and activities that you are undertaking to help deliver this agreement at the 2015 United Nations Climate Change Conference in Paris (COP 21)

Further Information

Page: CC3. Targets and Initiatives

CC3.1

Did you have an emissions reduction target that was active (ongoing or reached completion) in the reporting year?

Absolute target

CC3.1a

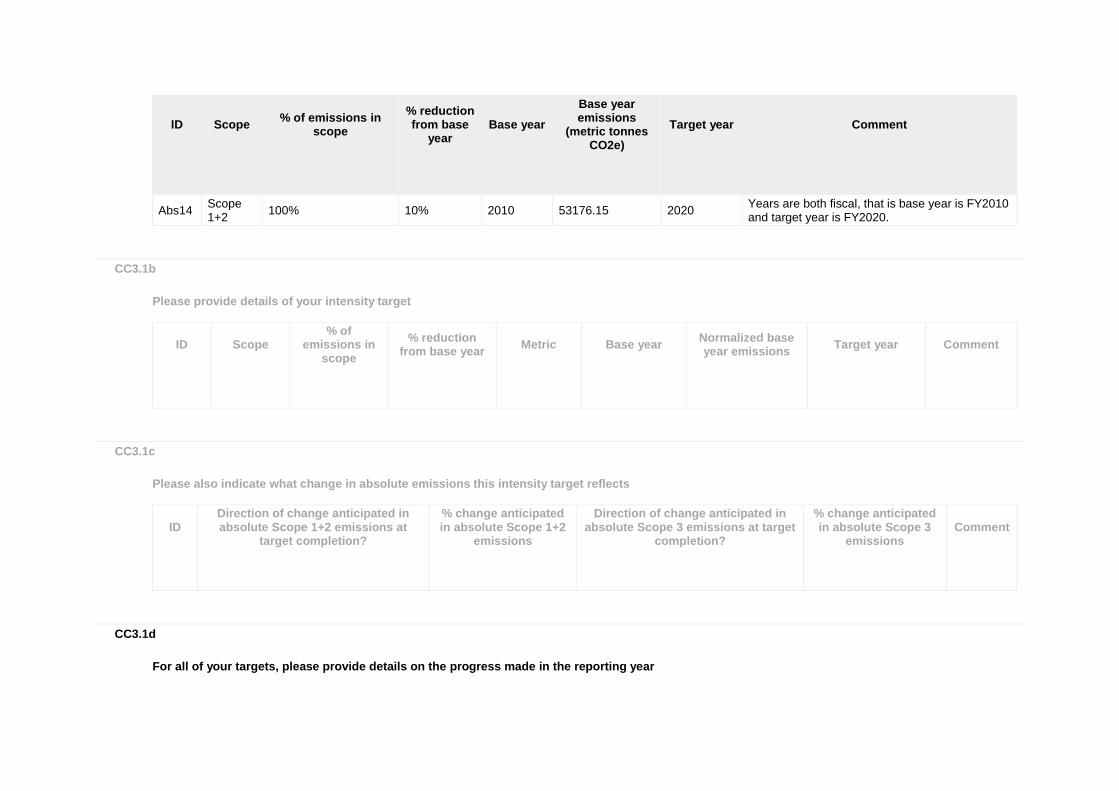

Please provide details of your absolute target

ID

Scope

% of emissions in scope

% reduction from base

year

Base year

Base year emissions

(metric tonnes CO2e)

Target year

Comment

Abs14 Scope 1+2

100% 10% 2010 53176.15 2020 Years are both fiscal, that is base year is FY2010 and target year is FY2020.

CC3.1b

Please provide details of your intensity target

ID

Scope

% of emissions in

scope

% reduction from base year

Metric

Base year

Normalized base year emissions

Target year

Comment

CC3.1c

Please also indicate what change in absolute emissions this intensity target reflects

ID

Direction of change anticipated in absolute Scope 1+2 emissions at

target completion?

% change anticipated in absolute Scope 1+2

emissions

Direction of change anticipated in absolute Scope 3 emissions at target

completion?

% change anticipated in absolute Scope 3

emissions

Comment

CC3.1d

For all of your targets, please provide details on the progress made in the reporting year

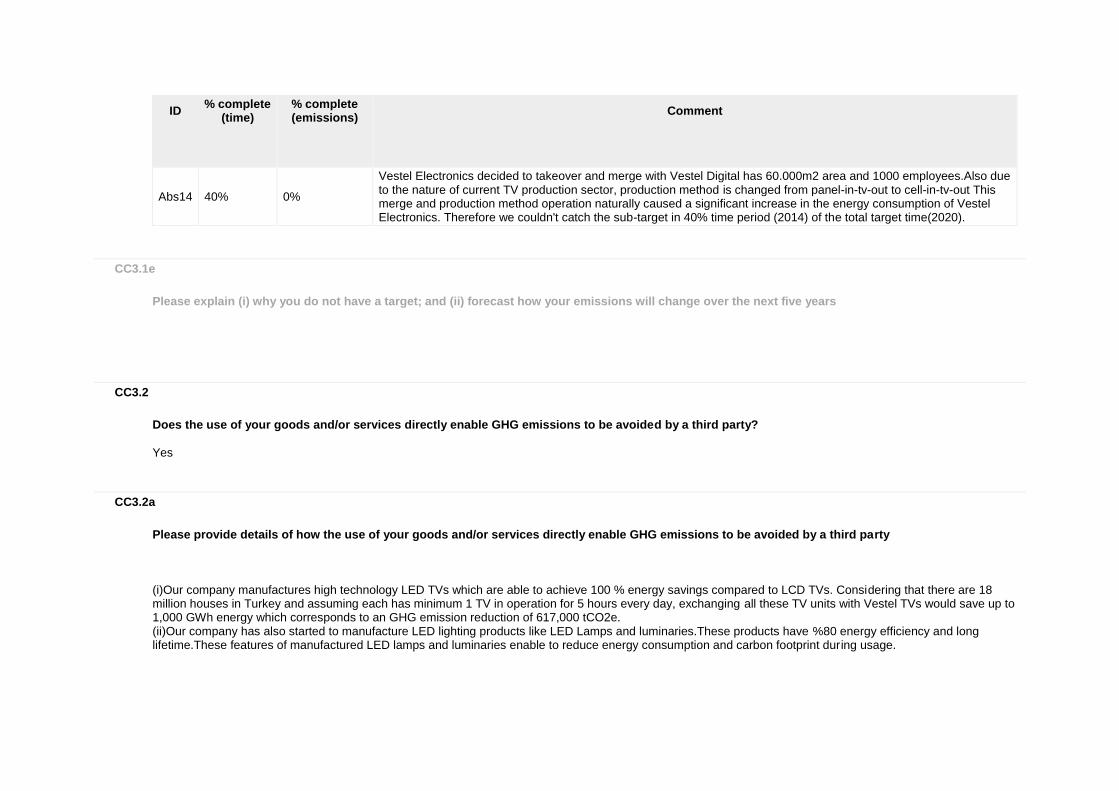

ID

% complete (time)

% complete (emissions)

Comment

Abs14 40% 0%

Vestel Electronics decided to takeover and merge with Vestel Digital has 60.000m2 area and 1000 employees.Also due to the nature of current TV production sector, production method is changed from panel-in-tv-out to cell-in-tv-out This merge and production method operation naturally caused a significant increase in the energy consumption of Vestel Electronics. Therefore we couldn't catch the sub-target in 40% time period (2014) of the total target time(2020).

CC3.1e

Please explain (i) why you do not have a target; and (ii) forecast how your emissions will change over the next five years

CC3.2

Does the use of your goods and/or services directly enable GHG emissions to be avoided by a third party?

Yes

CC3.2a

Please provide details of how the use of your goods and/or services directly enable GHG emissions to be avoided by a third party

(i)Our company manufactures high technology LED TVs which are able to achieve 100 % energy savings compared to LCD TVs. Considering that there are 18 million houses in Turkey and assuming each has minimum 1 TV in operation for 5 hours every day, exchanging all these TV units with Vestel TVs would save up to 1,000 GWh energy which corresponds to an GHG emission reduction of 617,000 tCO2e. (ii)Our company has also started to manufacture LED lighting products like LED Lamps and luminaries.These products have %80 energy efficiency and long lifetime.These features of manufactured LED lamps and luminaries enable to reduce energy consumption and carbon footprint during usage.

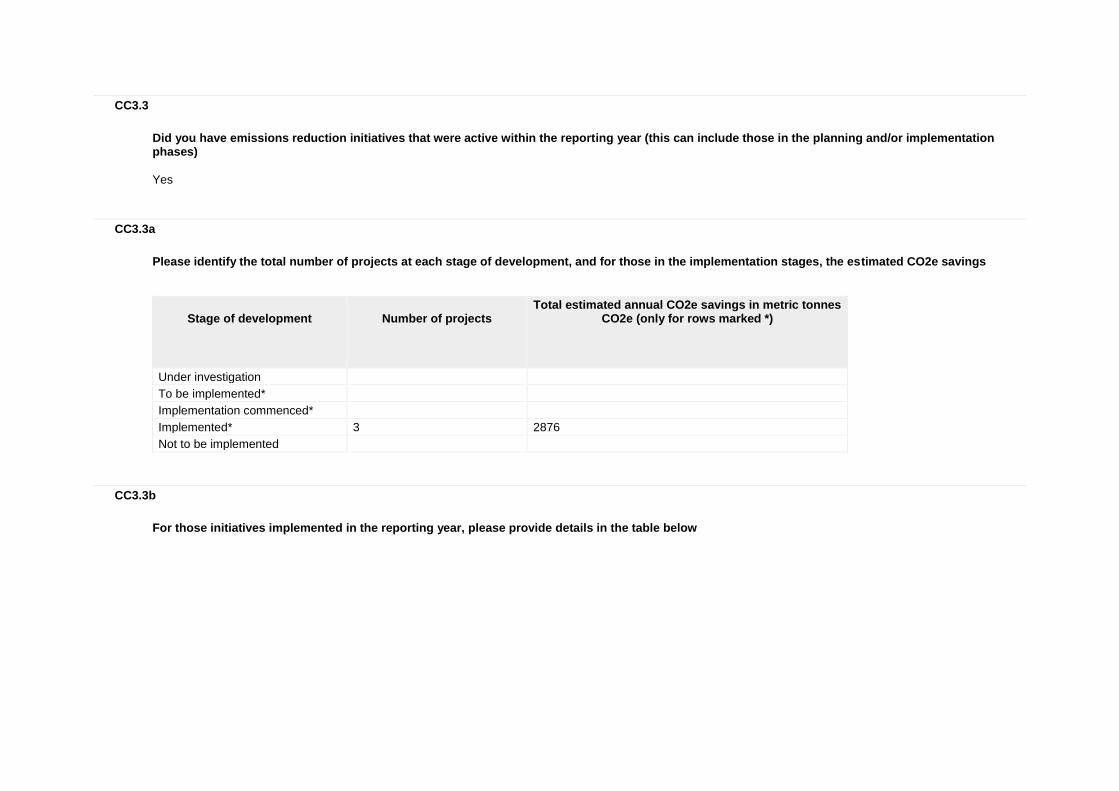

CC3.3

Did you have emissions reduction initiatives that were active within the reporting year (this can include those in the planning and/or implementation phases)

Yes

CC3.3a

Please identify the total number of projects at each stage of development, and for those in the implementation stages, the estimated CO2e savings

Stage of development

Number of projects

Total estimated annual CO2e savings in metric tonnes CO2e (only for rows marked *)

Under investigation

To be implemented*

Implementation commenced*

Implemented* 3 2876

Not to be implemented

CC3.3b

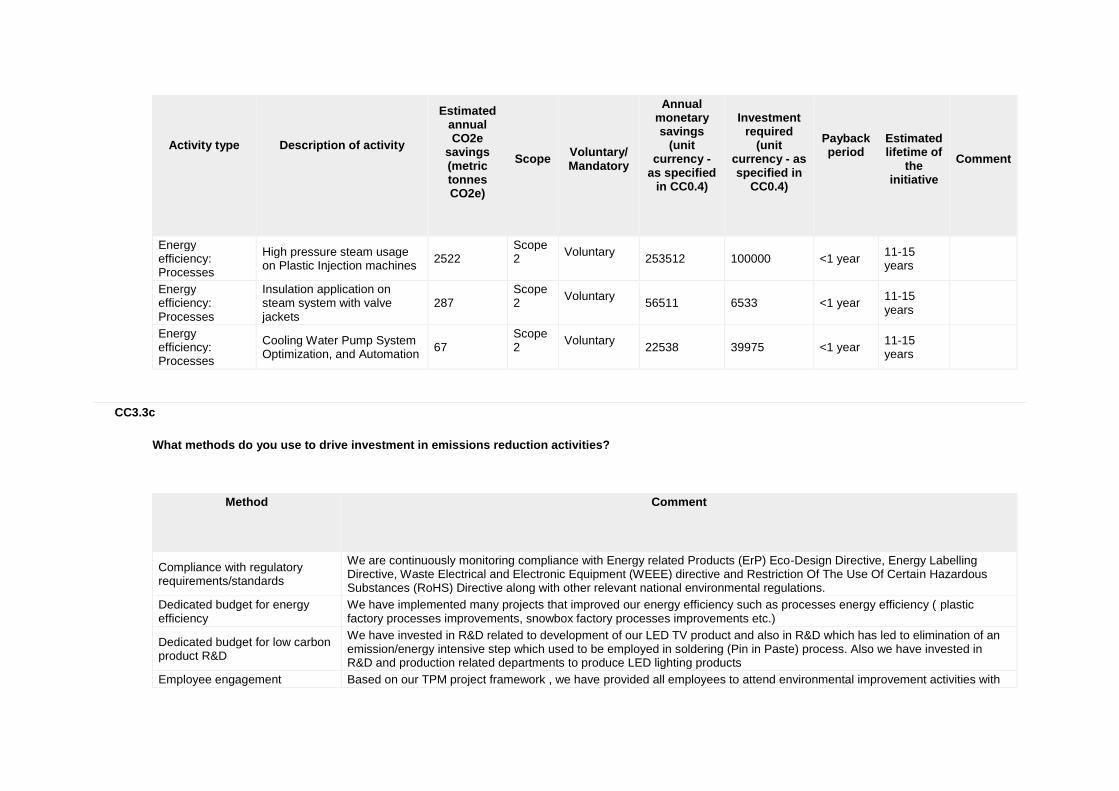

For those initiatives implemented in the reporting year, please provide details in the table below

Activity type

Description of activity

Estimated annual CO2e

savings (metric tonnes CO2e)

Scope

Voluntary/ Mandatory

Annual monetary savings

(unit currency -

as specified in CC0.4)

Investment required

(unit currency - as specified in

CC0.4)

Payback period

Estimated lifetime of

the initiative

Comment

Energy efficiency: Processes

High pressure steam usage on Plastic Injection machines

2522 Scope 2

Voluntary

253512 100000 <1 year 11-15 years

Energy efficiency: Processes

Insulation application on steam system with valve jackets

287 Scope 2

Voluntary

56511 6533 <1 year 11-15 years

Energy efficiency: Processes

Cooling Water Pump System Optimization, and Automation

67 Scope 2

Voluntary

22538 39975 <1 year 11-15 years

CC3.3c

What methods do you use to drive investment in emissions reduction activities?

Method

Comment

Compliance with regulatory requirements/standards

We are continuously monitoring compliance with Energy related Products (ErP) Eco-Design Directive, Energy Labelling Directive, Waste Electrical and Electronic Equipment (WEEE) directive and Restriction Of The Use Of Certain Hazardous Substances (RoHS) Directive along with other relevant national environmental regulations.

Dedicated budget for energy efficiency

We have implemented many projects that improved our energy efficiency such as processes energy efficiency ( plastic factory processes improvements, snowbox factory processes improvements etc.)

Dedicated budget for low carbon product R&D

We have invested in R&D related to development of our LED TV product and also in R&D which has led to elimination of an emission/energy intensive step which used to be employed in soldering (Pin in Paste) process. Also we have invested in R&D and production related departments to produce LED lighting products

Employee engagement Based on our TPM project framework , we have provided all employees to attend environmental improvement activities with

Method

Comment

suggestion evaluation and appreciation recognazition system which has over 1.000.000 TRY investment cost and it will continue untill 2020.

CC3.3d

If you do not have any emissions reduction initiatives, please explain why not

Further Information

Attachments

https://www.cdp.net/sites/2015/59/21159/Climate Change 2015/Shared Documents/Attachments/ClimateChange2015/CC3.TargetsandInitiatives/Vestel Elektronik-Energy Saving Projects.pdf

Page: CC4. Communication

CC4.1

Have you published information about your organization’s response to climate change and GHG emissions performance for this reporting year in places other than in your CDP response? If so, please attach the publication(s)

Publication

Status

Page/Section reference

Attach the document

In voluntary communications Underway - previous year

pg.149-167 https://www.cdp.net/sites/2015/59/21159/Climate Change 2015/Shared Documents/Attachments/CC4.1/ZORLU HOLDİNG 2014.pdf

Publication

Status

Page/Section reference

Attach the document

attached

In mainstream financial reports in accordance with the CDSB Framework

Complete pg.46-51 https://www.cdp.net/sites/2015/59/21159/Climate Change 2015/Shared Documents/Attachments/CC4.1/vestel_elektronik_faaliyet raporu2014.pdf

In other regulatory filings Complete pg.2-3 https://www.cdp.net/sites/2015/59/21159/Climate Change 2015/Shared Documents/Attachments/CC4.1/Enerji Tüketim Bildirim Formu_2014.pdf

Further Information

Module: Risks and Opportunities

Page: CC5. Climate Change Risks

CC5.1

Have you identified any inherent climate change risks that have the potential to generate a substantive change in your business operations, revenue or expenditure? Tick all that apply

Risks driven by changes in regulation Risks driven by changes in physical climate parameters Risks driven by changes in other climate-related developments

CC5.1a

Please describe your inherent risks that are driven by changes in regulation

Risk driver

Description

Potential impact

Timeframe

Direct/ Indirec

t

Likelihood

Magnitude of

impact

Estimated financial

implications

Management method

Cost of management

Fuel/energy taxes and regulations

We may be exposed to the risk of carbon taxes via our suppliers operating in certain parts of the world, where these taxes expected in the near future.

Increased operational cost

Unknown Indirect (Supply chain)

More likely than not

Medium-high

%10 of reveneu

Following and Managing of domestic and worldwide regulations, Zorlu Risk Management Group

Department and consultancy costs

Product efficiency regulations and standards

If we fail to comply with the product efficiency regulations and standards required for selling our products to EU and Domestic Market, there is a risk for us to loose 95% of our market.

Reduced demand for goods/services

Up to 1 year

Direct Very unlikely

High loose %95 of market

Following and Managing of domestic and worldwide regulations, Zorlu Risk Management Group, powerfull R&D

Department,research&development and consultancy costs

Risk driver

Description

Potential impact

Timeframe

Direct/ Indirec

t

Likelihood

Magnitude of

impact

Estimated financial

implications

Management method

Cost of management

Product labelling regulations and standards

If we fail to comply with the product efficiency regulations and standards required for selling our products to EU and Domestic Market, there is a risk for us to loose 95% of our market.

Reduced demand for goods/services

Up to 1 year

Direct Very unlikely

High loose %95 of market

Following and Managing of domestic and worldwide regulations, Zorlu Risk Management Group, powerfull R&D

Department,research&development and consultancy costs

CC5.1b

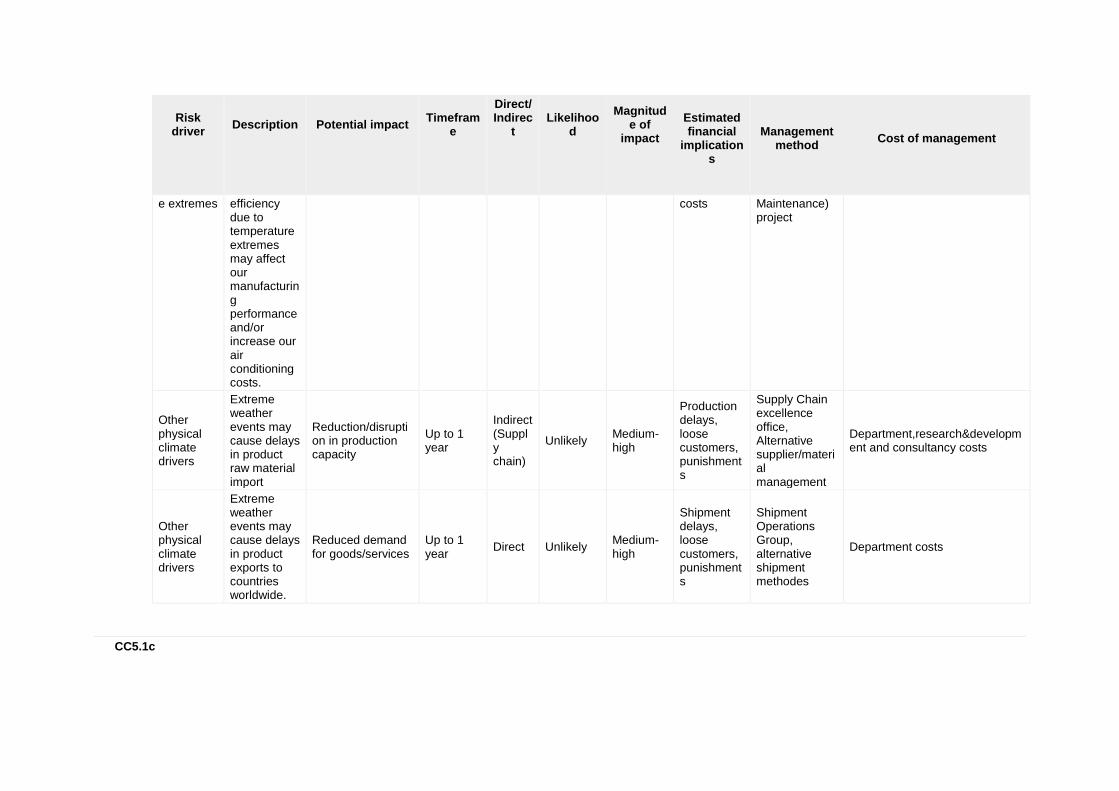

Please describe your inherent risks that are driven by change in physical climate parameters

Risk driver

Description

Potential impact

Timeframe

Direct/ Indirec

t

Likelihood

Magnitude of

impact

Estimated financial

implications

Management

method

Cost of management

Change in temperatur

Reduced equipment

Increased operational cost

1 to 3 years

Direct Unlikely Low-medium

%10 equipment

TPM(Total Productive

Department and consultancy costs

Risk driver

Description

Potential impact

Timeframe

Direct/ Indirec

t

Likelihood

Magnitude of

impact

Estimated financial

implications

Management

method

Cost of management

e extremes efficiency due to temperature extremes may affect our manufacturing performance and/or increase our air conditioning costs.

costs Maintenance) project

Other physical climate drivers

Extreme weather events may cause delays in product raw material import

Reduction/disruption in production capacity

Up to 1 year

Indirect (Supply chain)

Unlikely Medium-high

Production delays, loose customers, punishments

Supply Chain excellence office, Alternative supplier/material management

Department,research&development and consultancy costs

Other physical climate drivers

Extreme weather events may cause delays in product exports to countries worldwide.

Reduced demand for goods/services

Up to 1 year

Direct Unlikely Medium-high

Shipment delays, loose customers, punishments

Shipment Operations Group, alternative shipment methodes

Department costs

CC5.1c

Please describe your inherent risks that are driven by changes in other climate-related developments

Risk driver

Description

Potential impact

Timeframe

Direct/ Indirec

t

Likelihood

Magnitude of

impact

Estimated financial

implications

Management

method

Cost of management

Changing consumer behaviour

Any failure related to implementation of our environment and climate friendly business strategy and reduced environmental performance in our activities may result in losing of our consumers and our market share.

Reduced demand for goods/services

Up to 1 year

Indirect (Client)

Very unlikely

Low-medium

losing of our consumers and our market share.

Following and Managing of domestic and worldwide regulations, Market researchs, Zorlu Risk Management Group, powerfull R&D

Department,research&development and consultancy costs

Reputation

Our company also sees the risk in failing to actively disclose environment and climate related performance to current and potential investors and therefore affecting our

Reduced stock price (market valuation)

Up to 1 year

Direct Very unlikely

Low-medium

reducing of stock prices

Following and Managing of domestic and worldwide regulations,transparent management, Zorlu Risk Management Group, powerfull R&D

Department,research&development and consultancy costs

Risk driver

Description

Potential impact

Timeframe

Direct/ Indirec

t

Likelihood

Magnitude of

impact

Estimated financial

implications

Management

method

Cost of management

stock prices.

CC5.1d

Please explain why you do not consider your company to be exposed to inherent risks driven by changes in regulation that have the potential to generate a substantive change in your business operations, revenue or expenditure

CC5.1e

Please explain why you do not consider your company to be exposed to inherent risks driven by physical climate parameters that have the potential to generate a substantive change in your business operations, revenue or expenditure

CC5.1f

Please explain why you do not consider your company to be exposed to inherent risks driven by changes in other climate-related developments that have the potential to generate a substantive change in your business operations, revenue or expenditure

Further Information

Page: CC6. Climate Change Opportunities

CC6.1

Have you identified any inherent climate change opportunities that have the potential to generate a substantive change in your business operations, revenue or expenditure? Tick all that apply

Opportunities driven by changes in regulation Opportunities driven by changes in physical climate parameters Opportunities driven by changes in other climate-related developments

CC6.1a

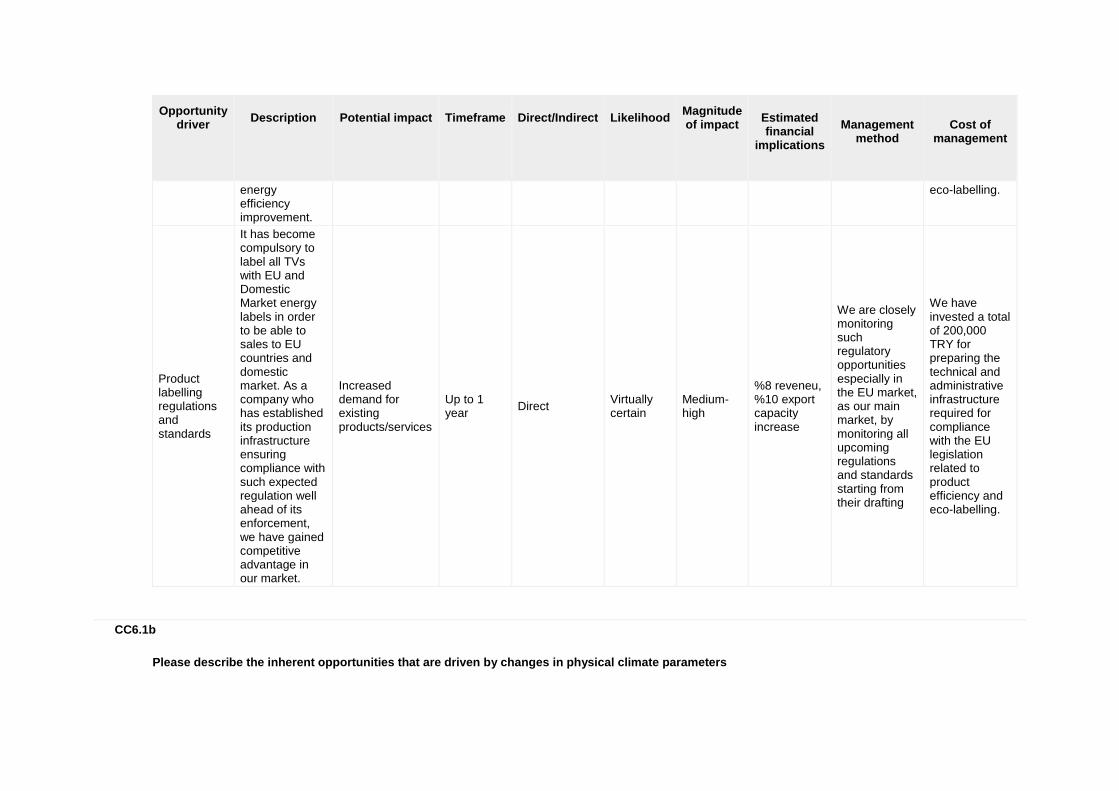

Please describe your inherent opportunities that are driven by changes in regulation

Opportunity driver

Description

Potential impact

Timeframe

Direct/Indirect

Likelihood

Magnitude of impact

Estimated financial

implications

Management

method

Cost of

management

Product efficiency regulations and standards

Our facilities will comply with the "By-Law on Energy Performance of Buildings" and will perform periodic energy audits and performance reporting according to this by-law. This will enable us to identify any

Reduced operational costs

Up to 1 year

Direct Virtually certain

Medium-high

%8 reveneu, %10 export capacity increase

We are closely monitoring such regulatory opportunities especially in the EU market, as our main market, by monitoring all upcoming regulations and standards starting from their drafting

We have invested a total of 200,000 TRY for preparing the technical and administrative infrastructure required for compliance with the EU legislation related to product efficiency and

Opportunity driver

Description

Potential impact

Timeframe

Direct/Indirect

Likelihood

Magnitude of impact

Estimated financial

implications

Management

method

Cost of

management

energy efficiency improvement.

eco-labelling.

Product labelling regulations and standards

It has become compulsory to label all TVs with EU and Domestic Market energy labels in order to be able to sales to EU countries and domestic market. As a company who has established its production infrastructure ensuring compliance with such expected regulation well ahead of its enforcement, we have gained competitive advantage in our market.

Increased demand for existing products/services

Up to 1 year

Direct Virtually certain

Medium-high

%8 reveneu, %10 export capacity increase

We are closely monitoring such regulatory opportunities especially in the EU market, as our main market, by monitoring all upcoming regulations and standards starting from their drafting

We have invested a total of 200,000 TRY for preparing the technical and administrative infrastructure required for compliance with the EU legislation related to product efficiency and eco-labelling.

CC6.1b

Please describe the inherent opportunities that are driven by changes in physical climate parameters

Opportunity driver

Description

Potential impact

Timeframe

Direct/ Indirect

Likelihood

Magnitude of impact

Estimated financial

implications

Management

method

Cost of

management

Snow and ice

We have been observing an increased demand for our products during times when weather conditions encourage and/or force people to stay indoors such as snow and ice.

Increased demand for existing products/services

Unknown Indirect (Client)

Likely Medium

Potential financial implications of the opportunity are hard to determine due to uncertainty related to such physical phenomena.

Managing inventory, advertising and sales channels

Seasonal costs are like high inventory cost and advertising costs.

CC6.1c

Please describe the inherent opportunities that are driven by changes in other climate-related developments

Opportunity driver

Description

Potential impact

Timeframe

Direct/ Indirect

Likelihood

Magnitude of impact

Estimated financial

implications

Management method

Cost of

management

Changing consumer behaviour

It is observed that the consumers’ climate awareness is rising every year. As a company building its strategy upon sustainability of

Increased demand for existing products/services

Up to 1 year

Indirect (Client)

Virtually certain

High

We expect that the eco TV and LED TV market share will expand up to 98 % in 2014 and continue to increase to an estimated 100 % in

Managing regulations, research&development studies, advertising and sales channels

We have made investment worth of 50 million USD in our energy-efficient LED TV , LED Lighting, Touch screens,

Opportunity driver

Description

Potential impact

Timeframe

Direct/ Indirect

Likelihood

Magnitude of impact

Estimated financial

implications

Management method

Cost of

management

natural resources and materials in its operations, and investing in high technology helping to reduce the ecological footprint of its products, we see this as an important opportunity to drive more consumers to buying our products and continue to be an important player and keep our competitiveness in the market. Vestel Electronics is the manufacturer of Eco TVs with reduced power consumption in stand-by and operation mode and energy efficient LED TVs and LED lightings with

2015. We also expect that the share of our eco-products will be 100 % in 2015, as we observe from the buying trends, which favor eco-friendly design and energy efficiency. A review of the global market

Smartphones production plant for business expansion and our R&D investments reached up to 60 million USD in 2014 supported with our ‘unlimited R&D budget’ strategy.

Opportunity driver

Description

Potential impact

Timeframe

Direct/ Indirect

Likelihood

Magnitude of impact

Estimated financial

implications

Management method

Cost of

management

low power consumption and long lifetime.

Reputation

Positive perceptions about VESTELs carbon performance by clients, investors and the general public will enhance its brand equity in the marketplace.

Increased demand for existing products/services

Unknown Indirect (Client)

Very likely Medium

We expect that the eco TV and LED TV market share will expand up to 98 % in 2014 and continue to increase to an estimated 100 % in 2015. We also expect that the share of our eco-products will be 100 % in 2015, as we observe from the buying trends, which favor eco-friendly design and energy efficiency. A review of the global market

Managing regulations, research&development studies, advertising and sales channels

We have made investment worth of 50 million USD in our energy-efficient LED TV, LED Lighting, Touch screens, Smartphones production plant for business expansion and our R&D investments reached up to 60 million USD in 2014 supported with our ‘unlimited R&D budget’ strategy.

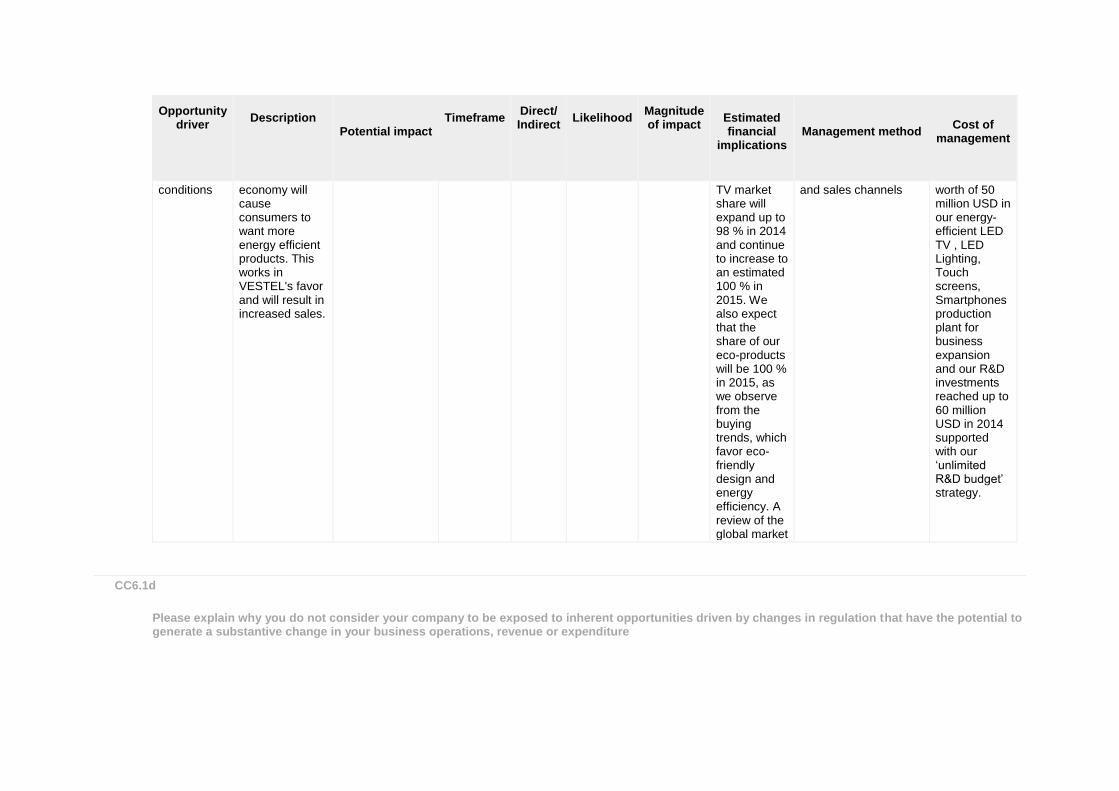

Fluctuating socio-economic

VESTEL is confident that downturns in the

Premium price opportunities

Unknown Direct Very likely Medium-high

We expect that the eco TV and LED

Managing regulations, research&development studies, advertising

We have made investment

Opportunity driver

Description

Potential impact

Timeframe

Direct/ Indirect

Likelihood

Magnitude of impact

Estimated financial

implications

Management method

Cost of

management

conditions economy will cause consumers to want more energy efficient products. This works in VESTEL's favor and will result in increased sales.

TV market share will expand up to 98 % in 2014 and continue to increase to an estimated 100 % in 2015. We also expect that the share of our eco-products will be 100 % in 2015, as we observe from the buying trends, which favor eco-friendly design and energy efficiency. A review of the global market

and sales channels worth of 50 million USD in our energy-efficient LED TV , LED Lighting, Touch screens, Smartphones production plant for business expansion and our R&D investments reached up to 60 million USD in 2014 supported with our ‘unlimited R&D budget’ strategy.

CC6.1d

Please explain why you do not consider your company to be exposed to inherent opportunities driven by changes in regulation that have the potential to generate a substantive change in your business operations, revenue or expenditure

CC6.1e

Please explain why you do not consider your company to be exposed to inherent opportunities driven by physical climate parameters that have the potential to generate a substantive change in your business operations, revenue or expenditure

CC6.1f

Please explain why you do not consider your company to be exposed to inherent opportunities driven by changes in other climate-related developments that have the potential to generate a substantive change in your business operations, revenue or expenditure

Further Information

Attachments

https://www.cdp.net/sites/2015/59/21159/Climate Change 2015/Shared Documents/Attachments/ClimateChange2015/CC6.ClimateChangeOpportunities/Vestel Led Lighting.pdf

Module: GHG Emissions Accounting, Energy and Fuel Use, and Trading

Page: CC7. Emissions Methodology

CC7.1

Please provide your base year and base year emissions (Scopes 1 and 2)

Scope

Base year

Base year emissions (metric tonnes CO2e)

Scope 1 Fri 01 Jan 2010 - Fri 31 Dec 2010

1816.31

Scope 2 Fri 01 Jan 2010 - Fri 31 Dec 2010

52608.99

CC7.2

Please give the name of the standard, protocol or methodology you have used to collect activity data and calculate Scope 1 and Scope 2 emissions

Please select the published methodologies that you use

ISO 14064-1

CC7.2a

If you have selected "Other" in CC7.2 please provide details of the standard, protocol or methodology you have used to collect activity data and calculate Scope 1 and Scope 2 emissions

CC7.3

Please give the source for the global warming potentials you have used

Gas

Reference

CO2 IPCC Fourth Assessment Report (AR4 - 100 year)

CH4 IPCC Fourth Assessment Report (AR4 - 100 year)

N2O IPCC Fourth Assessment Report (AR4 - 100 year)

CC7.4

Please give the emissions factors you have applied and their origin; alternatively, please attach an Excel spreadsheet with this data at the bottom of this page

Fuel/Material/Energy

Emission Factor

Unit

Reference

Natural gas 56100 Other: kgCO2 per tJ IPCC(2006)

Natural gas 1 Other: kgCH4 per tJ IPCC(2006)

Diesel/Gas oil 74100 Other: kgCO2 per tJ IPCC(2006)

Diesel/Gas oil 43 Other: tJ/Gg IPCC(2006)

Electricity 617 metric tonnes CO2 per MWh

Turkish Regulation "By-Law on Energy Performance of Buildings

Steam 267 Other: kgCO2 per t supplier's data and rough emission factors

Heat 0.48 Other: kgCO2 per kcal supplier's data and rough emission factors

Further Information

Page: CC8. Emissions Data - (1 Jan 2014 - 31 Dec 2014)

CC8.1

Please select the boundary you are using for your Scope 1 and 2 greenhouse gas inventory

Operational control

CC8.2

Please provide your gross global Scope 1 emissions figures in metric tonnes CO2e

2625.18

CC8.3

Please provide your gross global Scope 2 emissions figures in metric tonnes CO2e

74288.02

CC8.4

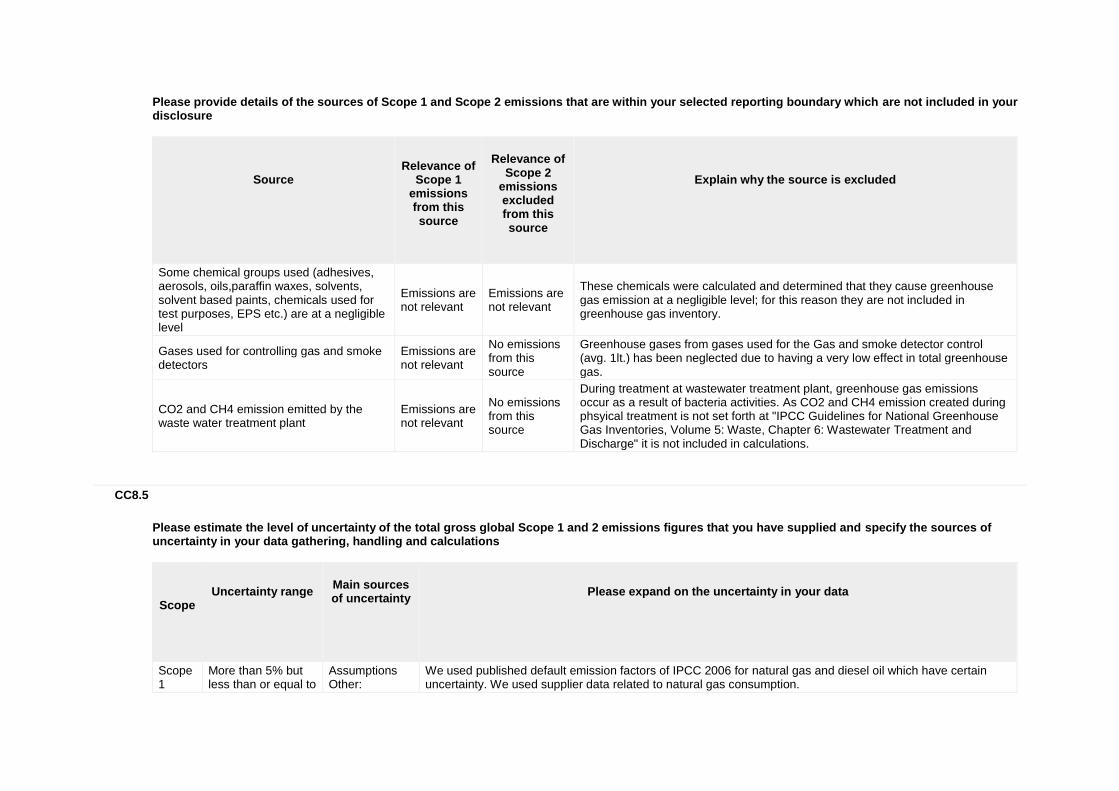

Are there are any sources (e.g. facilities, specific GHGs, activities, geographies, etc.) of Scope 1 and Scope 2 emissions that are within your selected reporting boundary which are not included in your disclosure?

Yes

CC8.4a

Please provide details of the sources of Scope 1 and Scope 2 emissions that are within your selected reporting boundary which are not included in your disclosure

Source

Relevance of

Scope 1 emissions from this source

Relevance of

Scope 2 emissions excluded from this source

Explain why the source is excluded

Some chemical groups used (adhesives, aerosols, oils,paraffin waxes, solvents, solvent based paints, chemicals used for test purposes, EPS etc.) are at a negligible level

Emissions are not relevant

Emissions are not relevant

These chemicals were calculated and determined that they cause greenhouse gas emission at a negligible level; for this reason they are not included in greenhouse gas inventory.

Gases used for controlling gas and smoke detectors

Emissions are not relevant

No emissions from this source

Greenhouse gases from gases used for the Gas and smoke detector control (avg. 1lt.) has been neglected due to having a very low effect in total greenhouse gas.

CO2 and CH4 emission emitted by the waste water treatment plant

Emissions are not relevant

No emissions from this source

During treatment at wastewater treatment plant, greenhouse gas emissions occur as a result of bacteria activities. As CO2 and CH4 emission created during phsyical treatment is not set forth at "IPCC Guidelines for National Greenhouse Gas Inventories, Volume 5: Waste, Chapter 6: Wastewater Treatment and Discharge" it is not included in calculations.

CC8.5

Please estimate the level of uncertainty of the total gross global Scope 1 and 2 emissions figures that you have supplied and specify the sources of uncertainty in your data gathering, handling and calculations

Scope

Uncertainty range

Main sources of uncertainty

Please expand on the uncertainty in your data

Scope 1

More than 5% but less than or equal to

Assumptions Other:

We used published default emission factors of IPCC 2006 for natural gas and diesel oil which have certain uncertainty. We used supplier data related to natural gas consumption.

Scope

Uncertainty range

Main sources of uncertainty

Please expand on the uncertainty in your data

10% supplier's data

Scope 2

More than 5% but less than or equal to 10%

Assumptions Other: supplier's data

The national grid emission factor published in the Turkish Regulation "By-Law on Energy Performance of Buildings" was used. The details and the most recent data used for the calculation of this emission factor is not presented in the regulation hence we assume the uncertainty to be not more than 10% by considering the changes in the grid system. We used the supplier's data and rough emission factors for estimating emissions from purchased steam and heat.

CC8.6

Please indicate the verification/assurance status that applies to your reported Scope 1 emissions

No third party verification or assurance

CC8.6a

Please provide further details of the verification/assurance undertaken for your Scope 1 emissions, and attach the relevant statements

Type of verification or assurance

Attach the statement

Page/section reference

Relevant standard

Proportion of reported Scope 1 emissions verified (%)

CC8.6b

Please provide further details of the regulatory regime to which you are complying that specifies the use of Continuous Emissions Monitoring Systems (CEMS)

Regulation

% of emissions covered by the system

Compliance period

Evidence of submission

CC8.7

Please indicate the verification/assurance status that applies to your reported Scope 2 emissions

No third party verification or assurance

CC8.7a

Please provide further details of the verification/assurance undertaken for your Scope 2 emissions, and attach the relevant statements

Type of verification or assurance

Attach the statement

Page/Section reference

Relevant standard

Proportion of reported Scope 2

emissions verified (%)

CC8.8

Please identify if any data points have been verified as part of the third party verification work undertaken, other than the verification of emissions figures reported in CC8.6, CC8.7 and CC14.2

Additional data points verified

Comment

Additional data points verified

Comment

No additional data verified

CC8.9

Are carbon dioxide emissions from biologically sequestered carbon relevant to your organization?

No

CC8.9a

Please provide the emissions from biologically sequestered carbon relevant to your organization in metric tonnes CO2

Further Information

Page: CC9. Scope 1 Emissions Breakdown - (1 Jan 2014 - 31 Dec 2014)

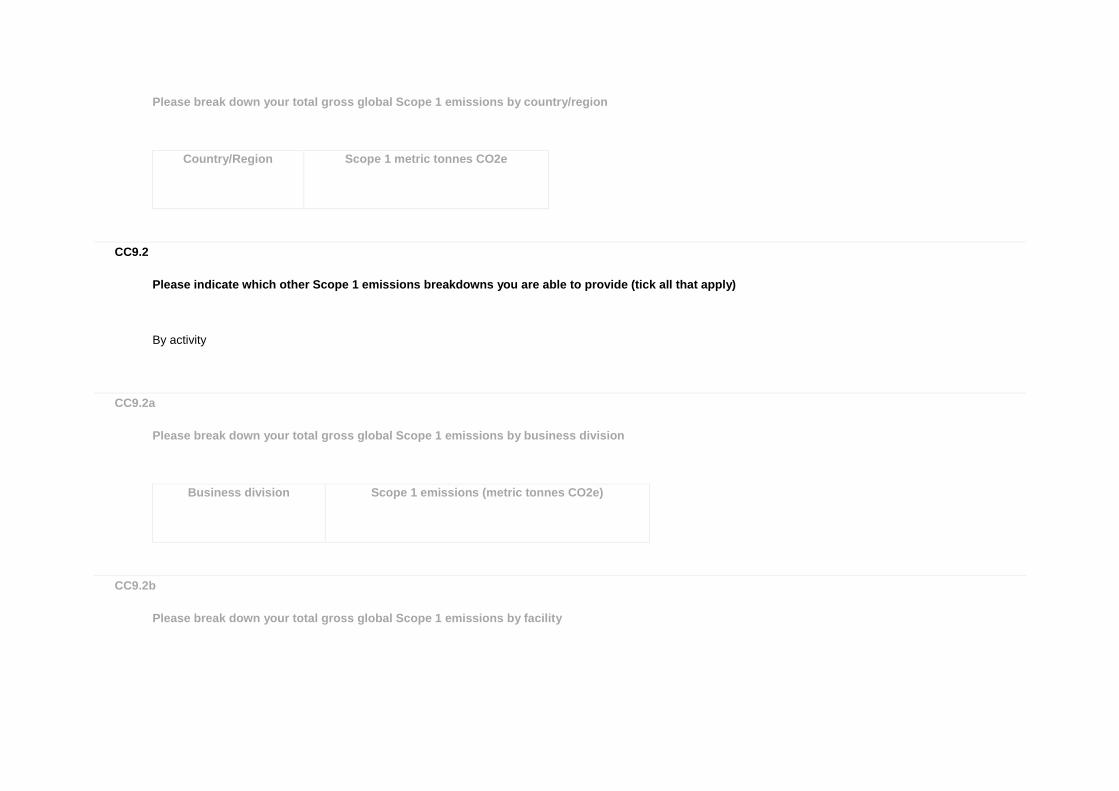

CC9.1

Do you have Scope 1 emissions sources in more than one country?

No

CC9.1a

Please break down your total gross global Scope 1 emissions by country/region

Country/Region

Scope 1 metric tonnes CO2e

CC9.2

Please indicate which other Scope 1 emissions breakdowns you are able to provide (tick all that apply)

By activity

CC9.2a

Please break down your total gross global Scope 1 emissions by business division

Business division

Scope 1 emissions (metric tonnes CO2e)

CC9.2b

Please break down your total gross global Scope 1 emissions by facility

Facility

Scope 1 emissions (metric tonnes CO2e)

Latitude

Longitude

CC9.2c

Please break down your total gross global Scope 1 emissions by GHG type

GHG type

Scope 1 emissions (metric tonnes CO2e)

CC9.2d

Please break down your total gross global Scope 1 emissions by activity

Activity

Scope 1 emissions (metric tonnes CO2e)

Stationary Combustion 1696.74

Mobile Combustion 875.37

Generators 53.06

CC9.2e

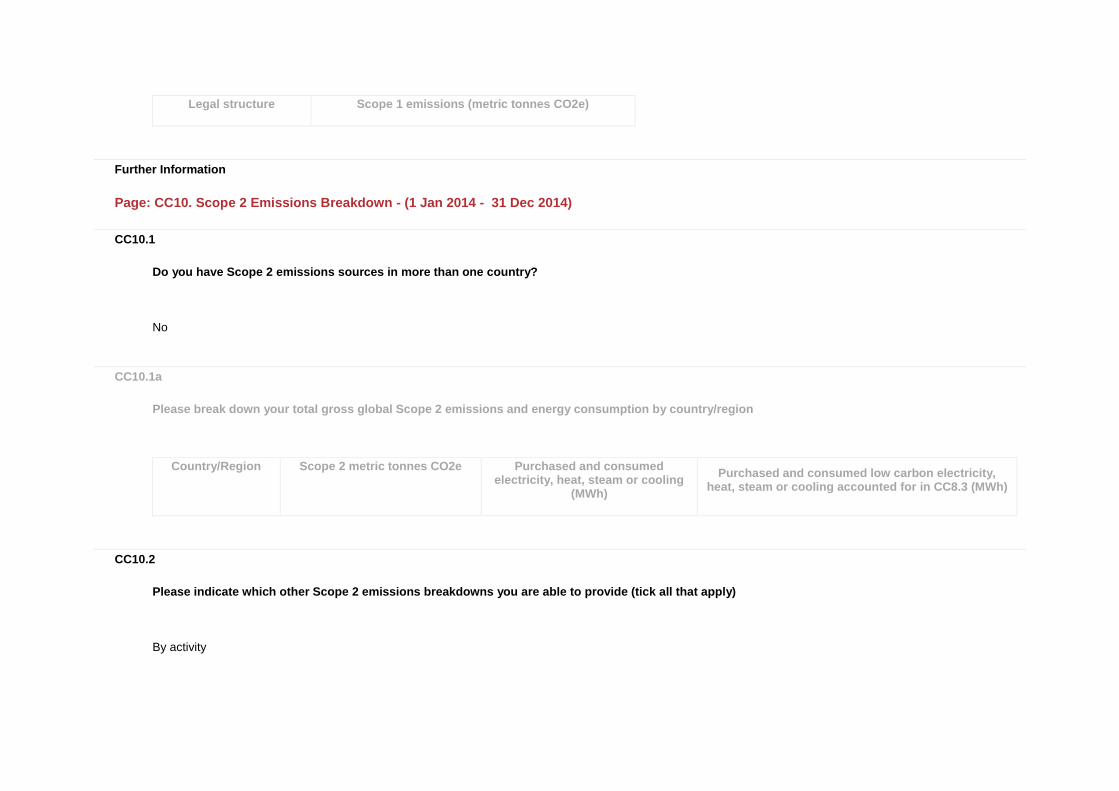

Please break down your total gross global Scope 1 emissions by legal structure

Legal structure

Scope 1 emissions (metric tonnes CO2e)

Further Information

Page: CC10. Scope 2 Emissions Breakdown - (1 Jan 2014 - 31 Dec 2014)

CC10.1

Do you have Scope 2 emissions sources in more than one country?

No

CC10.1a

Please break down your total gross global Scope 2 emissions and energy consumption by country/region

Country/Region

Scope 2 metric tonnes CO2e

Purchased and consumed electricity, heat, steam or cooling

(MWh)

Purchased and consumed low carbon electricity, heat, steam or cooling accounted for in CC8.3 (MWh)

CC10.2

Please indicate which other Scope 2 emissions breakdowns you are able to provide (tick all that apply)

By activity

CC10.2a

Please break down your total gross global Scope 2 emissions by business division

Business division

Scope 2 emissions (metric tonnes CO2e)

CC10.2b

Please break down your total gross global Scope 2 emissions by facility

Facility

Scope 2 emissions (metric tonnes CO2e)

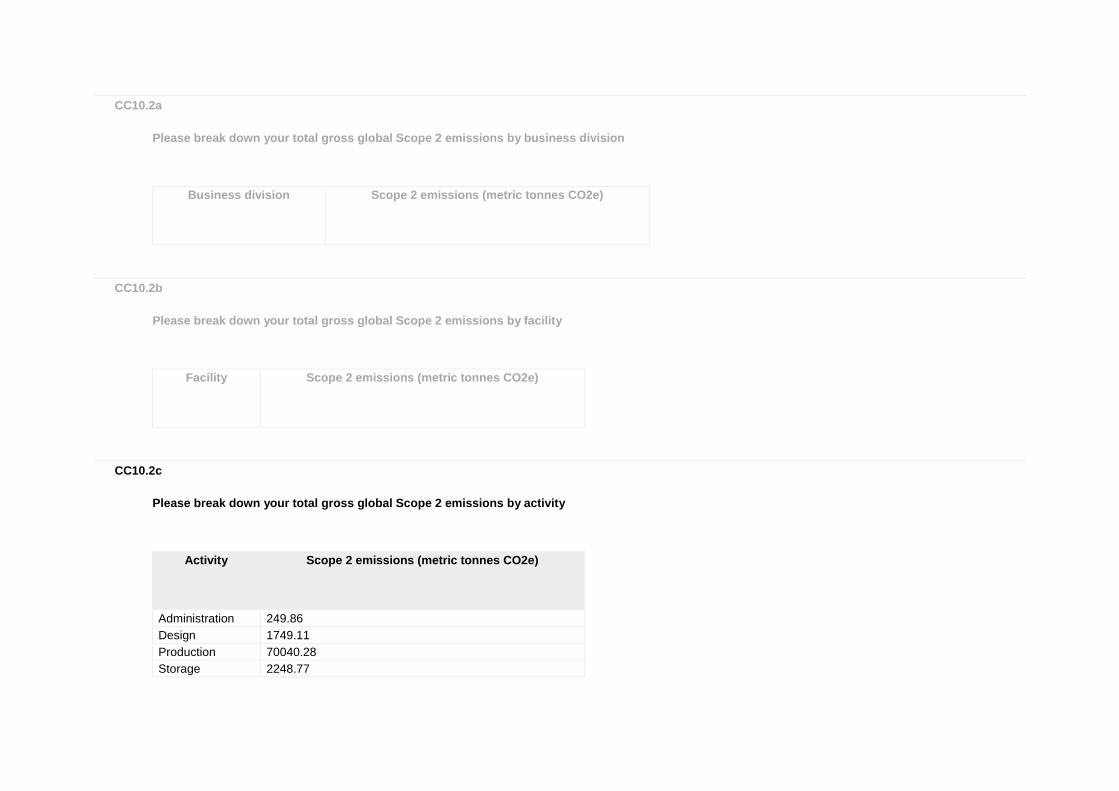

CC10.2c

Please break down your total gross global Scope 2 emissions by activity

Activity

Scope 2 emissions (metric tonnes CO2e)

Administration 249.86

Design 1749.11

Production 70040.28

Storage 2248.77

CC10.2d

Please break down your total gross global Scope 2 emissions by legal structure

Legal structure

Scope 2 emissions (metric tonnes CO2e)

Further Information

Page: CC11. Energy

CC11.1

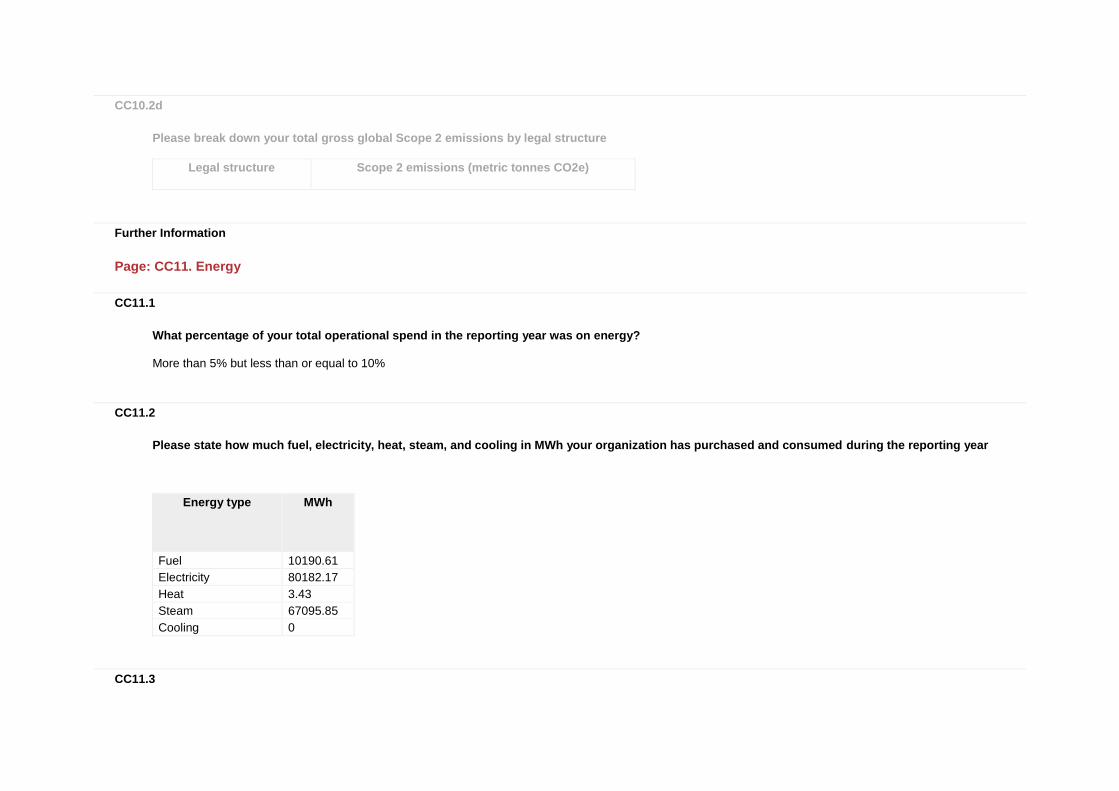

What percentage of your total operational spend in the reporting year was on energy?

More than 5% but less than or equal to 10%

CC11.2

Please state how much fuel, electricity, heat, steam, and cooling in MWh your organization has purchased and consumed during the reporting year

Energy type

MWh

Fuel 10190.61

Electricity 80182.17

Heat 3.43

Steam 67095.85

Cooling 0

CC11.3

Please complete the table by breaking down the total "Fuel" figure entered above by fuel type

Fuels

MWh

Natural gas 7377.17

Diesel/Gas oil 2813.44

CC11.4

Please provide details of the electricity, heat, steam or cooling amounts that were accounted at a low carbon emission factor in the Scope 2 figure reported in CC8.3

Basis for applying a low carbon emission factor

MWh associated with low carbon electricity, heat, steam or cooling

Comment

No purchases or generation of low carbon electricity, heat, steam or cooling accounted with a low carbon emissions factor

0 Vestel is located in Manisa Industrial Zone and purchases its energy i.e. electricity, natural gas, heat, steam from Manisa Industrial Zone Energy Facility. For now, there is no low carbon/renewable energy availability in this Industrial Area.

Further Information

Attachments

https://www.cdp.net/sites/2015/59/21159/Climate Change 2015/Shared Documents/Attachments/ClimateChange2015/CC11.Energy/Manisa Industrial Zone Energy Facility.jpg

Page: CC12. Emissions Performance

CC12.1

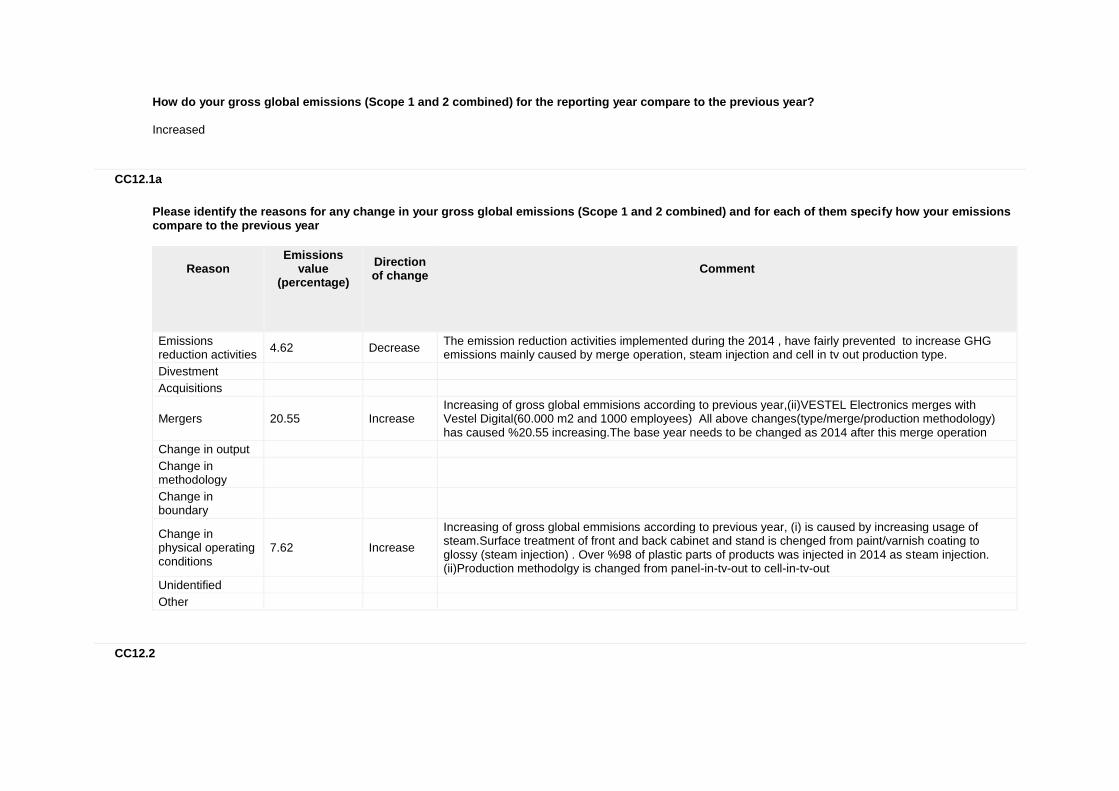

How do your gross global emissions (Scope 1 and 2 combined) for the reporting year compare to the previous year?

Increased

CC12.1a

Please identify the reasons for any change in your gross global emissions (Scope 1 and 2 combined) and for each of them specify how your emissions compare to the previous year

Reason

Emissions value

(percentage)

Direction of change

Comment

Emissions reduction activities

4.62 Decrease The emission reduction activities implemented during the 2014 , have fairly prevented to increase GHG emissions mainly caused by merge operation, steam injection and cell in tv out production type.

Divestment

Acquisitions

Mergers 20.55 Increase Increasing of gross global emmisions according to previous year,(ii)VESTEL Electronics merges with Vestel Digital(60.000 m2 and 1000 employees) All above changes(type/merge/production methodology) has caused %20.55 increasing.The base year needs to be changed as 2014 after this merge operation

Change in output

Change in methodology

Change in boundary

Change in physical operating conditions

7.62 Increase

Increasing of gross global emmisions according to previous year, (i) is caused by increasing usage of steam.Surface treatment of front and back cabinet and stand is chenged from paint/varnish coating to glossy (steam injection) . Over %98 of plastic parts of products was injected in 2014 as steam injection. (ii)Production methodolgy is changed from panel-in-tv-out to cell-in-tv-out

Unidentified

Other

CC12.2

Please describe your gross global combined Scope 1 and 2 emissions for the reporting year in metric tonnes CO2e per unit currency total revenue

Intensity figure

Metric numerator

Metric denominator

% change from

previous year

Direction of change from previous year

Reason for change

0.00001765 metric tonnes CO2e

unit total revenue

14.23 Increase The reason of increasing is the decreasing of consumer electronics sector product prices and as parallel total reveneu is to be realised as low, although production quantity is higher than previous year.

CC12.3

Please describe your gross global combined Scope 1 and 2 emissions for the reporting year in metric tonnes CO2e per full time equivalent (FTE) employee

Intensity figure

Metric numerator

Metric denominator

% change from

previous year

Direction of change from

previous year

Reason for change

0.0266 metric tonnes CO2e

FTE employee

16.7 Decrease

Although Vestel Electronics increased steam usage and change production type and merged with Vestel Digital, this figure has decreased due to studies about reducing carbon emission such as process improvements, designing new processes,usage of new technology equipments, TPM Suggestion Evaluation and Appreciation System etc.

CC12.4

Please provide an additional intensity (normalized) metric that is appropriate to your business operations

Intensity figure

Metric numerator

Metric denominator

% change from previous year

Direction of change from previous year

Reason for change

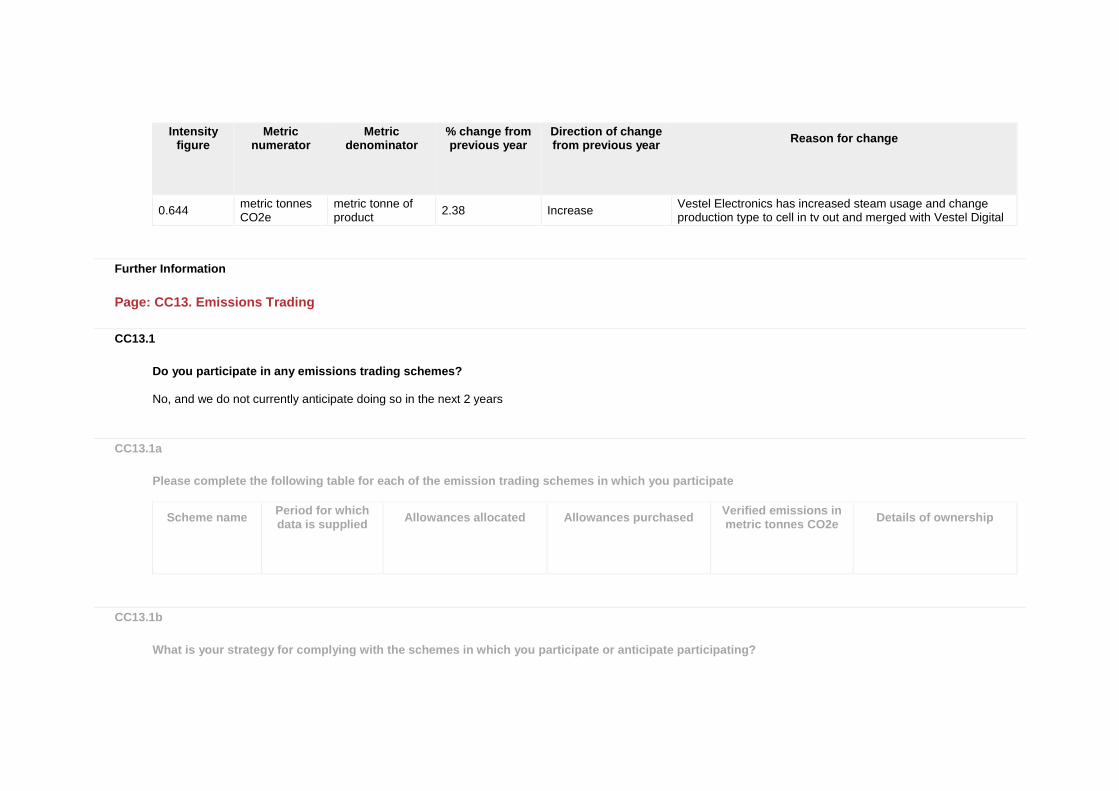

0.644 metric tonnes CO2e

metric tonne of product

2.38 Increase Vestel Electronics has increased steam usage and change production type to cell in tv out and merged with Vestel Digital

Further Information

Page: CC13. Emissions Trading

CC13.1

Do you participate in any emissions trading schemes?

No, and we do not currently anticipate doing so in the next 2 years

CC13.1a

Please complete the following table for each of the emission trading schemes in which you participate

Scheme name

Period for which data is supplied

Allowances allocated

Allowances purchased

Verified emissions in metric tonnes CO2e

Details of ownership

CC13.1b

What is your strategy for complying with the schemes in which you participate or anticipate participating?

CC13.2

Has your organization originated any project-based carbon credits or purchased any within the reporting period?

No

CC13.2a

Please provide details on the project-based carbon credits originated or purchased by your organization in the reporting period

Credit origination

or credit purchase

Project type

Project identification

Verified to which standard

Number of credits (metric

tonnes of CO2e)

Number of credits (metric tonnes

CO2e): Risk adjusted volume

Credits cancelled

Purpose, e.g. compliance

Further Information

Page: CC14. Scope 3 Emissions

CC14.1

Please account for your organization’s Scope 3 emissions, disclosing and explaining any exclusions

Sources of Scope 3 emissions

Evaluation status

metric tonnes CO2e

Emissions calculation methodology

Percentage of

emissions calculated using data obtained

from suppliers or value chain

partners

Explanation

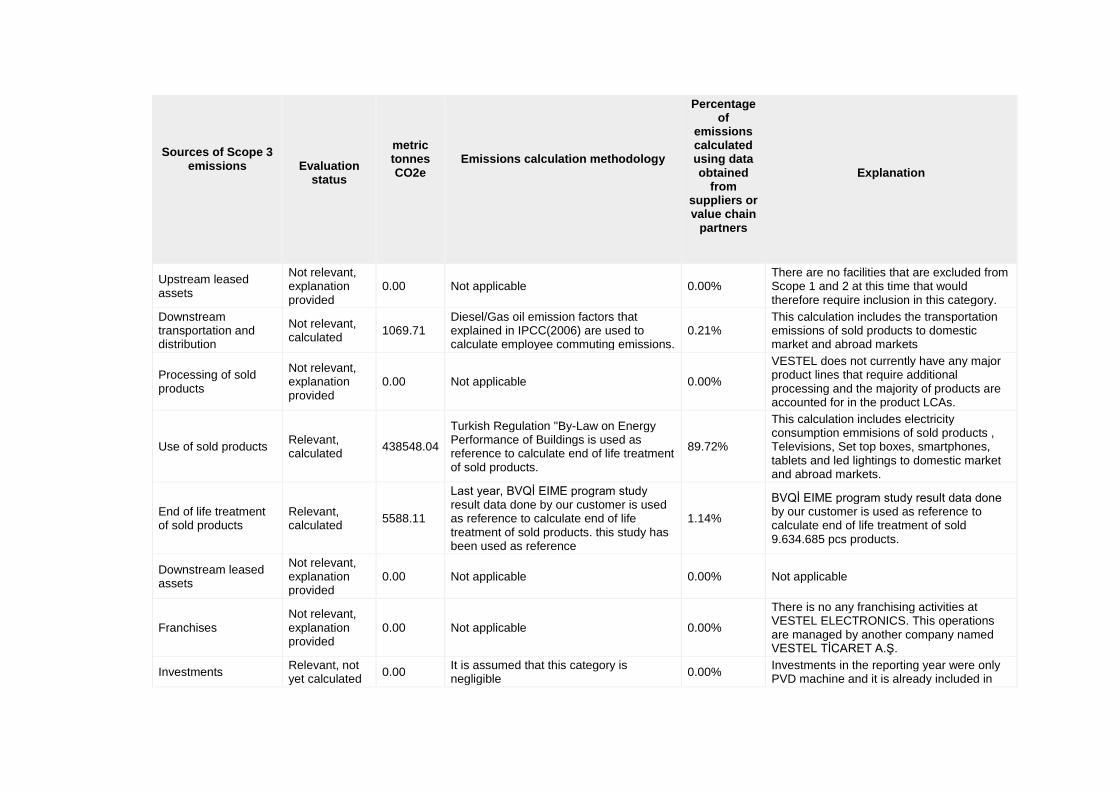

Purchased goods and services

Relevant, calculated

30869 Average data is used to calculate transportation of purchased raw materials.

6.31% This calculation includes the transportation emissions of all materials and components which are purchased during 2014

Capital goods Relevant, calculated

1.31 Average data is used to calculate transportation of purchased raw materials.

0.01%

This calculation includes the transportation emissions of 9 PLASTIC INJECTION MACHINES (ENGEL 1300, ENGEL 1500, ENGEL 2000) which is purchased during in 2014

Fuel-and-energy-related activities (not included in Scope 1 or 2)

Relevant, calculated

990.13

Diesel/Gas oil emission factors that explained in IPCC(2006) are used to calculate emissions of fuel and energy related activities(not included in Scope 1 or 2).

0.20%

This calculation includes fuel consumption of inside transportation cars and manager and top management vehicles provided by Vestel Electronics.

Upstream transportation and distribution

Not relevant, explanation provided

0.00 Not applicable 0.00%