CD Melbourne Congress: Ian Martin

14

Ian Martin [email protected] +61 3 9827 8841 A closer look at nbn co financials • Can it sustain A$5bn+ of revenue? • Where are the pressure points in Operating FCF? • What is it worth at sustainable Op FCF? • Can it defer financial restructure to post build? October 2017

-

Upload

decisive-publishing -

Category

Technology

-

view

144 -

download

0

Transcript of CD Melbourne Congress: Ian Martin

Ian Martin

+61 3 9827 8841

A closer look at nbn co financials

• Can it sustain A$5bn+ of revenue?

• Where are the pressure points in Operating FCF?

• What is it worth at sustainable Op FCF?

• Can it defer financial restructure to post build?

October 2017

NBN summary financials FY16-FY17

www.newstreetresearch.com 2

A$billion FY16A FY17A FY18 FY19 FY20 FY21

Revenue 0.4 1.0 1.9 3.5 4.9 5.4

Opex (1.7) (2.1) (2.4) (2.5) (2.7) (2.9)

EBITDA pre PSAA (1.3) (1.1) (0.5) 1.0 2.2 2.5

Subscriber Pays (0.6) (1.6) (2.9) (3.4) (1.5) (0.3)

EBITDA (1.9) (2.7) (3.4) (2.4) 0.7 2.2

Capex (4.7) (5.8) (7.0) (4.2) (1.6) (0.6)

Contingency - - (0.5) (0.6) (0.6) (0.6)

Interest and Working Cap (0.6) 1.3 (0.1) (0.7) (0.9) (0.9)

CashFlow (7.2) (7.2) (11.0) (7.9) (2.4) 0.1

Peak Funding

Equity Funding (20.3) (27.5) (29.5) (29.5) (29.5) (29.5)

Debt Funding - - (9.0) (16.9) (19.3) (19.2)

(20.3) (27.5) (38.5) (46.4) (48.8) (48.7)

Source: nbn co Corporate Plan 2018, p 34

Cashflow

breakeven

target

NBN ‘steady state’ P&L

www.newstreetresearch.com 3

A$billion Completion

Revenue 5.0 8m connections , A$52pm ARPU

Source: New Street Research estimates

NBN ‘steady state’ P&L

www.newstreetresearch.com 4

A$billion Completion

Revenue 5.0 8m connections , A$52pm ARPU

Operating cost (2.0) benchmark to Chorus (59-62%)

Operating EBITDA 3.0 60% EBITDA margin

Source: New Street Research estimates

NBN ‘steady state’ P&L

www.newstreetresearch.com 5

A$billion Completion

Revenue 5.0 8m connections , A$52pm ARPU

Operating cost (2.0) benchmark to Chorus (59-62%)

Operating EBITDA 3.0 60% EBITDA margin

Long term lease (1.0) Definitive Agreements

EBITDA/indicative OpFCF 2.0 40% EBITDA margin (46% CP21)

Source: New Street Research estimates

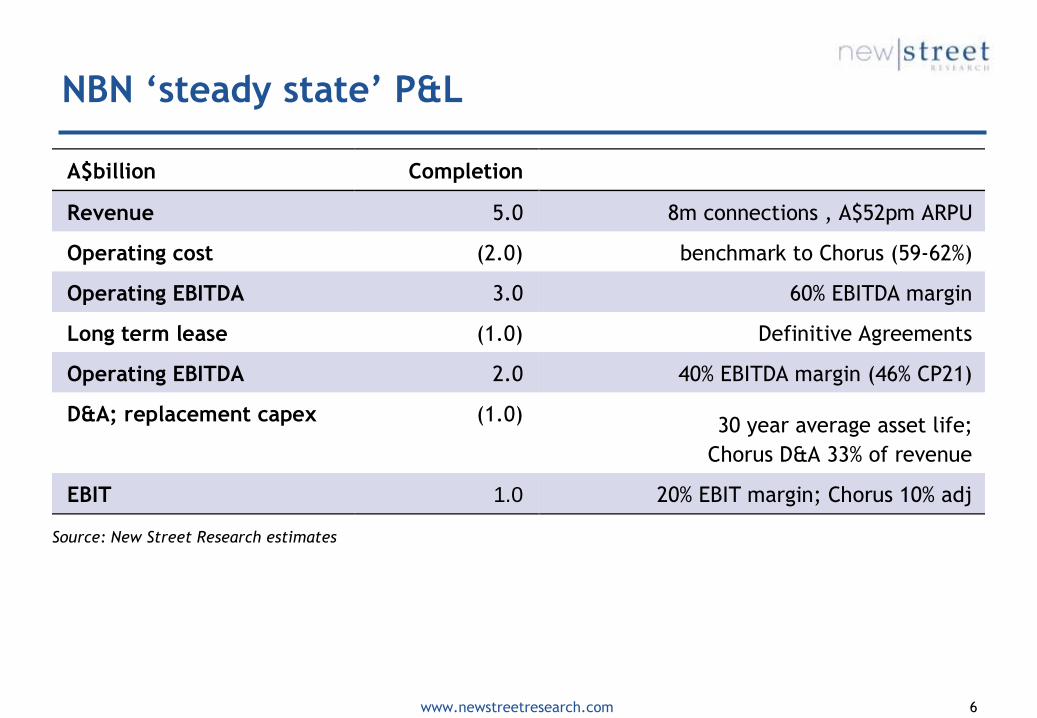

NBN ‘steady state’ P&L

www.newstreetresearch.com 6

A$billion Completion

Revenue 5.0 8m connections , A$52pm ARPU

Operating cost (2.0) benchmark to Chorus (59-62%)

Operating EBITDA 3.0 60% EBITDA margin

Long term lease (1.0) Definitive Agreements

Operating EBITDA 2.0 40% EBITDA margin (46% CP21)

D&A; replacement capex (1.0) 30 year average asset life;

Chorus D&A 33% of revenue

EBIT 1.0 20% EBIT margin; Chorus 10% adj

Source: New Street Research estimates

NBN ‘steady state’ P&L

www.newstreetresearch.com 7

A$billion Completion

Revenue 5.0 8m connections , A$52pm ARPU

Operating cost (2.0) benchmark to Chorus (59-62%)

Operating EBITDA 3.0 60% EBITDA margin

Long term lease (1.0) Definitive Agreements

Operating EBITDA 2.0 40% EBITDA margin (46% CP21)

D&A; replacement capex (1.0) 30 year average asset life;

Chorus D&A 33% of revenue

EBIT 1.0 20% EBIT margin; Chorus 10% adj

Interest charge (1.0) 5% on 19bn debt

Profit before tax - slim pickings

Source: New Street Research estimates

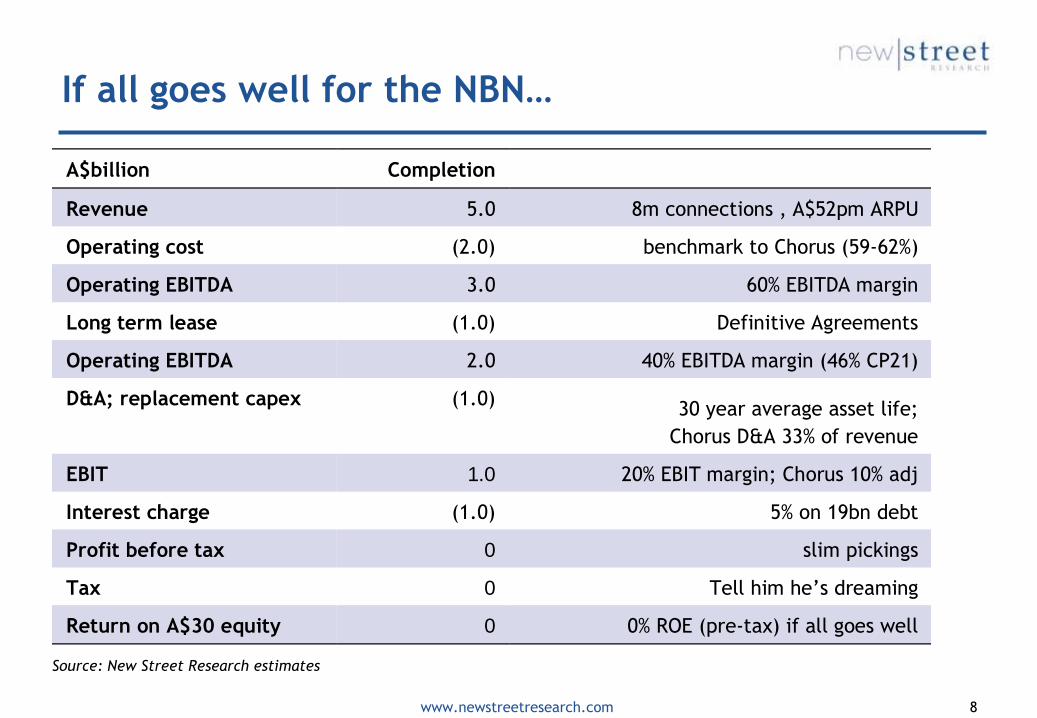

If all goes well for the NBN…

www.newstreetresearch.com 8

A$billion Completion

Revenue 5.0 8m connections , A$52pm ARPU

Operating cost (2.0) benchmark to Chorus (59-62%)

Operating EBITDA 3.0 60% EBITDA margin

Long term lease (1.0) Definitive Agreements

Operating EBITDA 2.0 40% EBITDA margin (46% CP21)

D&A; replacement capex (1.0) 30 year average asset life;

Chorus D&A 33% of revenue

EBIT 1.0 20% EBIT margin; Chorus 10% adj

Interest charge (1.0) 5% on 19bn debt

Profit before tax 0 slim pickings

Tax 0 Tell him he’s dreaming

Return on A$30 equity 0 0% ROE (pre-tax) if all goes well

Source: New Street Research estimates

Estimated Size Aust BB market – Dec 2016

www.newstreetresearch.com 9

TPG MNO coverage and on-net BB footprint

www.newstreetresearch.com 10

BB customer growth, c4% pa in NBN migration, then 1% pa

How many on-net?

• Rate of rollout of mobile network footprint,

especially the wireless access component

(1800MHz and 2500MHz)

• Portion in the wireless access footprint area that can be

offered a commercial service on net

= Fn {usage relative to capacity, fibre backhaul}

900MHz?

1800MHz

3500MHz?2500MHz

700MHz

1500MHz?

Optus Home Wireless Broadband

cf 2016 deal: $70 for 50GB

Up to 12/1 Mbps in 2300 MHz areas.

Up to 5/1 Mbps in other areas

Slowed to 256kbps after 250 GB

usage

Optus likely to expand the market impact of this service in 2H18,

And add 3,500Mhz service as mobile devices come to market in 2018

Telstra Home Gateway

www.newstreetresearch.com 12

Telstra well positioned in Mobile for converged service offerings

All bets for the NBN are off from c 2020

www.newstreetresearch.com 13

A$billion Capital Restructure

Revenue

fewer connections, lower ARPU

Operating cost

limited ability to cut LT opex

Operating EBITDA

EBITDA margin, trends down

Long term lease

Definitive Agreements, secured

Operating EBITDA

May become negative

Replacement capex

would require new funding

EBIT

what level of debt can nbn co service?

Interest charge

will interest rates rise?

Profit before tax

slim pickings

Tax

forget it

Return on A$30 equity

what further equity investment

Source: New Street Research estimates

www.newstreetresearch.com 14

This report was produced by New Street Research LLP. 11 Austin Friars, London EC2N 2HG

This document has been communicated to its clients by New Street Research LLP in accordance with its terms and conditions. This document is confidential and should not be communicated to persons other than the clients of New Street

Research LLP.

The document is directed only to investment professionals, as defined in section 19 of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2001, and other persons to whom financial promotions may be lawfully

communicated. The services provided by New Street Research LLP will only be provided to such persons. Persons who do not have professional experience in matters relating to investments should not rely on the contents of this

document.

New Street Research LLP is authorised and regulated in the conduct of its designated investment business in the United Kingdom by the Financial Services Authority.

The contents of this document are subject to updating, completion, revision, further verification and amendment.

The value of shares and other investments and the income derived from them may go down as well as up, and you may not get back the full amount you originally invested.

© 2016. New Street Research LLP.

![Ian Tyson - Carnero Vaquero [CD Liner Notes]](https://static.fdocuments.us/doc/165x107/563dbac4550346aa9aa7e15f/ian-tyson-carnero-vaquero-cd-liner-notes.jpg)