CASH MANAGEMENT AND GROWTH OF SMALL SCALE...

51

MAKERERE UNIVERSITY CASH MANAGEMENT AND GROWTH OF SMALL SCALE BUSINESSES IN NTUNGAMO MARKET BY ARIHOONA FESTUS 07/ U/6734/EXT SUPERVISOR: TUSUBIRA NYENDE FESTO A RESEARCH REPORT SUBMITTED TO MAKERERE UNIVERSITY IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE AWARD OF BACHELORS DEGREE OF COMMERCE OF MAKERERE UNIVERSITY. JUNE 2011

Transcript of CASH MANAGEMENT AND GROWTH OF SMALL SCALE...

1

MAKERERE UNIVERSITY

CASH MANAGEMENT AND GROWTH OF SMALL SCALE BUSINESSES

IN NTUNGAMO MARKET

BY

ARIHOONA FESTUS

07/ U/6734/EXT

SUPERVISOR:

TUSUBIRA NYENDE FESTO

A RESEARCH REPORT SUBMITTED TO MAKERERE UNIVERSITY IN PARTIAL

FULFILLMENT OF THE REQUIREMENTS FOR THE AWARD

OF BACHELORS DEGREE OF COMMERCE OF

MAKERERE UNIVERSITY.

JUNE 2011

i

DECLARATION

I ARIHOONA FESTUS declare that this report has not been produced anywhere for the award

of bachelor of commerce degree of Makerere university.

The report was written basing on the findings and information collected about the study of cash

management and growth of small scale businesses.

SIGNED…………………………………………………………..

ARIHOONA FESTUS

DATE…………………………………….

ii

APPROVAL

This is to certify that the study carried out by ARIHOONA FESTUS under the title Cash

Management and Growth of Small Scale Businesses was carried out under my supervision as a

university Supervisor.

This is work has been submitted with my approval.

Signed:…………………………….. Date:………………………………..

SUPERVISOR: TUSUBIRA NYENDE FESTO

iii

DEDICATION

I dedicate this research to my parents for their guidance and tireless support throughout my

studies.

I also want dedicate this report to my brothers, my dear friend Naume. K, Davis.N, my sisters

and relatives who sacrificed their time to work with me to make this report a success.

iv

ACKNOWLEDGEMENT

My sincere thanks go the people of Ntungamo market for providing the necessary information

during the research.

Lots of thanks go to my supervisor, Mr. Tusubira Nyende Festo for proof reading the material

and critically molding it.

v

ABSTRACT

This study was carried out in Ntungamo municipality on the topic cash management and growth

of small scale businesses. Literature has existed about cash management as a pre-requisite for

better growth small scale businesses. The study was based on the objectives which included,

finding out cash management policy adopted by business owners, to establish the rate at which

small scale businesses are growing and to establish the relationship between cash management

and growth of small scale businesses.

Data used included both primary and secondary with primary data collected by use of self

administered questionnaires. The study covered a sample of 38 respondents with all the 38 questi

The findings revealed that there is a significant correlation of 0.05 between cash management

and growth of small scale businesses. Cash as an important current asset that needs critically

planned for optimal balance to enable business activities take place smoothly. If cash

management is maximally ensured in business ventures, holding other factors positive the

business must boom and serve the public as expected reflecting better and improved performance

with high growth rates.

Regression analysis also revealed that cash contributes a highest percentage. This implies, failure

to implement cash management policies leads to negative consequences.

However, poor cash management practices constrains business operations and some customers

who are not satisfied with the services run away signifying poor performance and hence

retardation in the business growth.

vi

TABLE OF CONTENTS

DECLARATION ............................................................................................................................. i

APPROVAL ................................................................................................................................... ii

DEDICATION ............................................................................................................................... iii

ACKNOWLEDGEMENT ............................................................................................................. iv

ABSTRACT .................................................................................................................................... v

LIST OF TABLES ......................................................................................................................... ix

CHAPTER ONE ........................................................................................................................... 1

BACK GROUND OF THE STUDY .............................................................................................. 1

1.1 INTRODUCTION .................................................................................................................... 1

1.2 STATEMENT OF THE PROBLEM ........................................................................................ 2

1.3 Purpose of the study .................................................................................................................. 3

1.4 Objectives of the study.............................................................................................................. 3

1.5 Research questions .................................................................................................................... 3

1.6 Scope of the study ..................................................................................................................... 3

1.7 Significance of the study ........................................................................................................... 3

CHAPTER TWO .......................................................................................................................... 5

LITERATURE REVIEW ............................................................................................................... 5

2.0 Introduction ............................................................................................................................... 5

2.1 Cash management ..................................................................................................................... 5

2.2.1 Importance of cash management .......................................................................................... 5

2.2.2 Motives for holding cash. ..................................................................................................... 6

vii

2.2.3 Strategies to ensure good cash management ......................................................................... 6

2.3 Growth of small scale businesses ............................................................................................. 7

2.3.1 Factors that affect growth of small businesses. ..................................................................... 7

2.4 Cash management and growth of small scale ........................................................................... 8

CHAPTER THREE .................................................................................................................... 14

METHODOLOGY ....................................................................................................................... 14

3.0 Introduction. ............................................................................................................................ 14

3.1 Research design. ..................................................................................................................... 14

3.2 Study area................................................................................................................................ 14

3.3 Study population ..................................................................................................................... 14

3.4 Sample size and sampling techniques ..................................................................................... 14

3.5 Methods of data collection. .................................................................................................. 14

3.6 Data analysis and management ............................................................................................... 15

3.7 Limitations of the study .......................................................................................................... 15

CHAPTER FOUR ....................................................................................................................... 16

PRESENTATION AND DISCUSSION OF FINDINGS ............................................................. 16

4.0 INTRODUCTION .................................................................................................................. 16

4.1 Demographic information ....................................................................................................... 16

4.2 Finding on cash management.................................................................................................. 19

4.3 Findings on growth of small scale business ............................................................................ 25

4.4 Relationship between cash management and growth of small scale business ........................ 30

viii

CHAPTER FIVE ........................................................................................................................ 32

SUMMARY, CONCLUSION AND RECOMMENDATIONS ................................................... 32

5.0 INTRODUCTION .................................................................................................................. 32

5.1 Summary ................................................................................................................................. 32

5.2 Conclusion .............................................................................................................................. 32

5.3 Recommendations ................................................................................................................... 33

5.3.2 Growth of small scale businesses ........................................................................................ 33

5.4 Areas for further research ....................................................................................................... 33

REFERENCES: .......................................................................................................................... 34

APPENDICES: ............................................................................................................................ 41

ix

LIST OF TABLES

Table 1: Age distribution .............................................................................................................. 16

Table 2: Gender............................................................................................................................. 17

Table 3: Showing educational level .............................................................................................. 18

Table 4: Experience of the proprietor ........................................................................................... 18

Table 5: Strictness on cash management ...................................................................................... 19

Table 6: Control over cash received, collected and banked .......................................................... 20

Table 7: Cash Planning ................................................................................................................. 21

Table 8: Strongest credit policy over debt collections .................................................................. 22

Table 9: Various sources of cash inflows ..................................................................................... 23

Table 10: Control of cash outflows ............................................................................................... 24

Table 11: Growth of small scale businesses ................................................................................. 25

Table 12: Keenness on growth of the businesses.......................................................................... 26

Table 13: Satisfaction with the current rate growth ...................................................................... 27

Table 14: Procedures to follow while collecting debts ................................................................. 28

Table 15: Effect on Inadequate financing on growth rate............................................................. 29

Table 16: Correlations................................................................................................................... 30

Table 17: Regression..................................................................................................................... 31

1

CHAPTER ONE

BACK GROUND OF THE STUDY

1.1 INTRODUCTION

There is no universal definition of small scale businesses. However, different scholars, writers,

researchers and policy makers have used different definitions for small scale businesses basing

on the number of people employed, capital employed among other relevant factors. A business is

approved to be called small scale enterprise in Uganda; if it employs a number of people ranging

from 5-50.This number differs from a country to a country (Hamm; Harvad, 2002).

Recently there is no proper agreement as to the capital employed though a figure ranging from

USD5000-50000 is a reasonable estimate. The Ugandan investment authority (UIA) has put this

figure to now Shs 50m (about USD300).

The annual sales turn over in Ugandan conditions for small scale enterprises to participate in

value added tax (VAT) is now a figure of shs20m (USD200) which was agreed on as threshold.

Monthly sales turnover of about 1.5m (usd1500) and daily turnover of aboutshs7500 (usd75) is

also estimated. Therefore shs50m (USD50000) would be an ideal average turn over for

identification of small scale enterprise (Balunywa, 2003).

Small scale businesses are characterized by single ownership controlled by one person with a

limited liability and has no separate legal entity. In other words they cannot sue or be sued and

have no government control (Balunywa, 2003).

Irrespective of boundaries of definitions, small scale businesses play a vital role in the economy

and are seen increasing in number every time now and then for future growth. The y contributes

to domestic product (GDP) generate employment and provide consumer goods inter mediate

good sand food stuffs (Arinaitwe, 2006).

cash as important asset contributes about 70% of the current assets and its management affects

both liquidity and profitability as well as the over all growth and development of the

business(kakuru j, 2001).

2

Cash management is a strategy by which an enterprise administers and invests its cash. It also

seen as control of cash collection. Cash management is an essential tool which aims at

establishing the financial position of the business. It is a set of guidelines established by

management to ensure that the business has optimal cash balance to meet the business goals

(Huang; Ramachandran, 2009).

Basically cash management is concerned with managing cash flows that is cash inflows and cash

out flows. Mojar sources of cash inflow include cash from operating activities, sell of business

assets among others. Sources of cash out flows include settling of creditors, purchase of

inventory among others. Cash needs to be efficiently managed and allocated to meet routine

business objectives. The gap between cash expenses and cash co0llection enhances liquidity

position, profitability leading to over all business growth over a period of time (Brinchk, soeren

& Gemuenden, 2011).

1.2 Statement of the problem

The success of many small businesses in Ntungamo municipality has been identified as a tool for

economic development .cash as an important asset in business enterprises, keeps them running

continuously(Arinaitwe,2006) .Therefore its management is not a matter of choice but something

that must be undertaken in any business organization.

Many owners of the business enterprises do not plan for their cash requirements. They have slow

cash inflow generation procedures with high rate of cash outflow, limited skills of handling cash

balances and do not strategically invest surplus cash(Joseph;Hannington,2011).

Many of small scale business owners do not understand the significance of proper management

of business resources and tend to believe that the business will get better on its own.

The owners of the business have put strict controls over cash by insisting that all cash received is

banked, receipt issued after sale of goods, proper debt collection procedures put in place and any

one suspected of fraud/embezzlement dismissed(Tong;miao,2011).

Despite all the measures employed to manage cash, there is a slow growth rate of small scale

business in Ntungamo market.

3

1.3 Purpose of the study

The purpose of the study was intended to establish whether there exists a relationship between

cash management and growth of small scale businesses.

1.4 Objectives of the study

i) To identify cash management policy adopted by owners /managers of small scale businesses

in Ntungamo market.

ii) To establish the rate at which small scale businesses are growing.

iii) To establish the relationship between cash management and growth of small scale

businesses in Ntungamo market.

1.5 Research questions

i) What is the cash management policy adopted by owners /managers of small scale businesses

in Ntungamo market?

ii) What is the rate at which small scale businesses are growing in Ntungamo market?

iii) What is the relationship between cash Management and growth of small scale businesses

Ntungamo market?

1.6 Scope of the study

The study was conducted in Ntungamo municipality with a focus on commercial activities like

buying the produce, shop keeping, market vending, communication services, secretarial services

among others.

The study mainly focused on the relationship between cash management and growth of Small

scale businesses.

1.7 Significance of the study

i) The study will help to guide and stimulate other researchers who may wish to undertake a

similar research.

4

ii) The study helped the researcher to identify current challenges affecting small scale businesses.

iii) The findings of the study will be beneficial to associations like Uganda small industries

association (USSIA), policy makers, Uganda revenue revenue authority (URA) to understand

better taxable capacity.

5

CHAPTER TWO

LITERATURE REVIEW

2.0 Introduction

This chapter presents the principles and concepts that have been explored and brought up by

various scholars in the existing literature on cash management and growth of small scale

business.

2.1 Cash management

This study explores cash management and its impact on business growth. The firm needs cash

primarily to make payments for purchases, electricity bills and operating expenses. The need to

hold cash would not raise if there is perfect synchronization between cash receipts and cash

payments. Cash management involves identifying both cash in flows and cash outflows and their

optimal use (Banker;Huang & Ramchandran, 2009).

Cash planning is the technique to plan and control cash. It protects the financial condition of the

business by developing a projected cash statement from a forecast of expected inflows and out

flows from a given period (lorek;willinger, 2011).

The term cash includes coins, currency and cheques held by the firm and the balances in its bank

account.

The business should keep sufficient cash neither more or less as cash shortages disrupt the

business operations while excess cash will remain idle (chen;zhihong;wei, 2011). The above

components of cash management are utilized in the transaction process and there fore the

quantities and qualities of these components are vital in determining the level of sales,

profitability that result in business growth.

2.2.1 Importance of cash management

Cash management is important because of the following reasons (pandey, 2000)

6

Cash constitutes the smallest portion of current assets there fore its management contributes

much towards day today operations of the business.

Cash is used to pay business obligations. Cash management assumes more importance than any

other current asset and the major aim is to maintain adequate control over cash position to keep

the firm with sufficient liquid and use the excess cash in some profitable way.

Prediction of cash may be difficult. Some times cash outflows may exceed cash inflows because

of payment of taxes, acquisition of business assets among others. Cash in flows may exceed cash

outflows because of large sales, prompt cash receipts, sell of business assets among others.

Therefore cash needs to be planned and managed (pandey, 2005).

2.2.2 Motives for holding cash.

Transaction motive. This requires the business to hold cash to conduct its activities in the

ordinary course. If cash receipts match with cash payments, there would be no need to hold cash

(kakuru, 2000)

Precautionary motive. This involves holding cash in business to meet un foreseeable future

circumstances. If future cash flows can be predicted with accuracy, less cash will be maintained

(lorek;willinger,2011).s

Speculative motive. This involves holding cash for investment purposes. Speculators invest in

near cash assets. They invest as interest rate reduces until a point reaches below they will no

longer invest.

2.2.3 Strategies to ensure good cash management

Cash planning. This may be done daily, weekly or monthly. The period of frequency depends on

the size of the firm and its management.

Pandey ( 2005), defines cash planning as a technique to plan and control cash.

Cash planning helps the business to prepare projected cash statement for the firm’s growth and

continued success.

7

Managing cash flows: Cash flows should be managed properly. This can be done in the

following ways:

Giving a short credit period. Businesses that offer credit facilities should give customers few

days to pay for the goods once bought to ensure high liquidity.

Seeking credit purchases from suppliers. Business owners maintain liquid cash that help in other

business operation. This ensures business survival and growth.

Ensuring a proper debt collection procedure. This can be done by sending an invoice to remind a

customer when and how much he/she is owed.

Investing surplus cash. The surplus cash balance should be properly invested to generate more

cash inflows hence business growth. (Ohlson;Jagadison, 2009).

2.3 Growth of small scale businesses

Reports point a slow in small scale businesses emanating from inadequate financing, adverse

government policies, poor physical infrastructure and poor managerial practices by business

operators (Wong;poutziouris, 2010).

Performance of business is how well or poorly the business is doing and how well or poorly

manager sets objectives. Business performance is the combination of many factors and better

performance implies business growth.

For a firm to perform well and be successful, it should set clear objectives, aim at quality

management and be able to compete both in long run and short run.

Empirical studies reveal that poor performance in small business result in failure rates.75% fail

with in first two years (Flusche etal 2001) and 95% fail with in the first 5 years (Gerber,2003).

2.3.1 Factors that affect growth of small businesses.

Managing skills. The ability and competence of business operators together with the skills of

identifying cash flows affect greatly the growth business managers/owners of the business

routinely observe the on going conditions of the business for better performance.

8

Credit policy. A lenient credit policy is one where credit will be given to customers with poor

creditworthiness and thus leading to increased debtors and this will affect business performance

that may retard its growth in the near future.

Astringent credit policy only offers to credit worthy customers and reduces the level of creditors.

This ensures business constant cash to run its activities which may lead to increased sales and

other related aspects.

Availability of credit. A business which can access banking facilities easily on favorable

conditions will run its operation smoothly and be able to expand on different dimensions.

Age and experience. Business operators who are mature enough to run any commercial activity

tend to devise different options towards growth of their businesses. It is through this process and

how long businessmen spend in commercial activities that they gain experience contributing to

business growth.

2.4 Cash management and growth of small scale businesses

Strong cash management through proper cash planning will create growth of small scale

businesses. Cash planning helps in forecasting cash inflows and out flows and thus management

will store only adequate cash needed to meet obligations. (Azmat;Samaratunge, 2009).

Proper cash management through investment of surplus cash, enhances growth of small scale

businesses as the firm will benefit profits from invested cash and cash at hand will help to meet

current obligations (Brinchk; Hans; Gemuenden, 2011).

In conclusion, though literature provides that cash management highly affects growth of small

scale businesses, it is not the only factor. Other factors like management skills, nature of goods,

and credit policy among others also affect growth (Arinaitwe, 2006).

Cash management is a broad term that refers to the collection, concentration, and disbursement

of cash. It encompasses a business’s level of liquidity, its management of cash balance, and its

short-term investment strategies (Cardaralla:toni,2010). In some ways, managing cash flow is the

most important job of business managers. If at any time a business fails to pay an obligation

when it is due because of the lack of cash, the business is insolvent. Insolvency is the primary

9

reason firms go bankrupt. Obviously, the prospect of such a direct consequence should compel

businesses to manage their cash with care. Moreover, efficient cash management means more

than just preventing bankruptcy. It improves the profitability and reduces the risk to which the

firm is exposed (Davidson: Charles,2008).

Cash management is particularly important for new and growing businesses. Cash flow can be a

problem even when a small business has numerous clients, offers a superior product to its

customers, and enjoys a real reputation in its industry (Hill: William,2004). Businesses suffering

from cash flow problems have no margin of safety in case of unanticipated expenses. They also

may experience trouble in finding the funds for innovation or expansion. Finally, poor cash flow

makes it difficult to hire and retain good employees and finally retard growth.

It is only natural that major business expenses are incurred in the production of goods or the

provision of services. In most cases, a business incurs such expenses before the corresponding

payment is received from customers (Richard: Patricia,2009). In addition, employee salaries and

other expenses drain considerable funds from most businesses. These factors make effective cash

management an essential part of any business's financial planning. Without cash for inventory,

payroll, and other expenses, an emergency is imminent (shulman: Cox, 2000).

When cash is received in exchange for products or services rendered, many small business

owners, intent on growing their businesses and tamping down debt, spend most or all of these

funds. But while such priorities are impressive, they should leave room for businesses to absorb

lean financial times down the line. The key to successful cash management, therefore, lies in

tabulating realistic projections, monitoring collections and disbursements, establishing effective

billing and collection measures, and adhering to budgetary restrictions( Bhuiana:Bell,2005).

Cash collection systems aim to reduce the time it takes to collect the cash that is owed to a firm.

Some of the sources of time delays are mail float, processing float, and bank float. Obviously, an

envelope mailed by a customer containing payment to a supplier firm does not arrive at its

destination instantly. Likewise, the payment is not processed and deposited into a bank account

the moment it is received by the supplier firm. And finally, when the payment is deposited in the

bank account oftentimes the bank does not give immediate availability to the funds. These three

10

floats are time delays that add up quickly, and they can force struggling or new firms to find

other sources of cash to pay their bills. This impedes business performance (Day G.S,2002).

Cash management attempts, among other things, to decrease the length and impact of these float

periods. A collection receipt point closer to the customer perhaps with an outside third-party

vendor to receive, process, and deposit the payment (check) is one way to speed up the collection

(Cardaralla:Toni,2010). The effectiveness of this method depends on the location of the

customer; the size and schedule of their payments; the firm's method of collecting payment; the

costs of processing payments; the time delays involved for mail, processing, and banking; and

the prevailing interest rate that can be earned on excess funds. The most important element in

ensuring good cash flow from customers, however, is establishing strong billing and collection

practices.

Another aspect of cash management is knowing the businesses’ optimal cash balance. There are

a number of methods that try to determine this mysterious cash balance, which is the precise

amount needed to minimize costs yet provide adequate liquidity to ensure bills are paid on time

hopefully with something left over for emergency purposes (Davison:Charles,2008). One of the

first steps in managing the cash balance is measuring liquidity, or the amount of money on hand

to meet current obligations. There are numerous ways to measure this, including: the Cash to

Total Assets ratio, the Current ratio (current assets divided by current liabilities), the Quick ratio

(current assets less inventory, divided by current liabilities), and the Net Liquid Balance (cash

plus marketable securities less short-term notes payable, divided by total assets). The higher the

number generated by the liquidity measure, the greater the liquidity. However, there is a trade off

between liquidity and profitability which discourages firms from having excessive liquidity.

Many small business experience cash flow difficulties, especially during their first years of

operation. This in the long run affects business performance and hence slow growth rate (Lorek;

willinger,2011). But entrepreneurs and managers can take steps to minimize the impact of such

problems and help maintain the continued viability of the business. Suggested steps to address

temporary cash flow problems include:

Create a realistic cash flow budget that charts finances for both the short term and longer term.

11

Redouble efforts to collect on outstanding payments owed to the business. The faster you mail an

invoice, the faster you will be paid .If deliveries do not automatically trigger an invoice, establish

a set billing schedule, preferably weekly. Businesses should also include a payment due date.

Offer small discounts for prompt payment.

Consider compromising on some billing disputes with clients. Small business owners are

understandably reluctant to consider this step, but in certain cases, obtaining some cash even if

the business is not at fault in the dispute for products sold or services rendered may be required

to pay basic expenses.

Closely monitor and prioritize all cash disbursements.

Contact creditors (vendors, lenders, and landlords) and attempt to negotiate mutually satisfactory

arrangements that will enable the business to weather its cash shortage. In some cases, it is good

to arrange better payment terms from suppliers or banks. Better credit terms translate into

borrowing money interest free.

Liquidate surplus inventory.

Assess other areas where operational expenses may be cut without permanently disabling the

business, such as payroll or goods/services with small profit margins.

Growth of small scale businesses is greatly contributed by the following factors. They

include;

Age. Age exerts a positive and significant influence on business success.

Entrepreneur traits. The entrepreneurial traits variable shows a positive and significant

influence on innovative behavior. The entrepreneurial traits variable has no direct and

significant influence on business achievement, but through innovative behavior it has an

indirect and significant influence on business success.

12

Inconsequential personality. The inconsequential personality typology variable has a

direct and significant influence on the formation of innovative behavior. The Minor

personality typology variable has no direct and significant influence on business success.

However, through innovative behavior it has indirect and significant influences on

business achievement

Experience. Experience asserts that experience is the best predictor of business success,

especially when the new business is related to earlier business experiences. Entrepreneurs with

vast experiences in managing business are more capable of finding ways to open new business

compared to employees with different career pathways. The importance of experience for

small-scale business success is also underscored by other experts. Haswell et al. (in Zimmerer

& Scar-borough, 2006) note that prominent reasons behind business failures are managerial and

experiential in capabilities

Education. Entrepreneurs with higher levels of education are more successful because

university education provides them with knowledge and modern managerial skills, making

them more conscious of the reality of the business world and thus in a position to use their

learning capability to manage business.

Super salesperson, real manager, and expert idea generator can predict success in any field of

business. Any entrepreneur will be successful if he follows a business pathway congruent with

his personality traits. The personal achiever will gain success if he continuously overcomes

challenges and crises, and behaves positively in facing them.

The super salesperson will experience success if he uses a lot of time to sell and invite

others to manage his business.

The real manager will succeed if he starts a new business and manages the business

himself. A successful entrepreneur tends to have a real manager personality type because

his studies are needed to validate this assertion. Succeed if the starts a new business and

leads the business himself.

13

The expert idea generator will succeed by entering the high technical business area have

success ladder with hopes of reaching the highest place. They may stop for a while to

reconsider strategy and collect energy, but they eventually climb higher.

Elasticity towards numerous obstacles consists of four components: reach, ownership and

originality, control, and endurance. However, if his theory is valid the adversity quotient should

be able to predict someone's resilience in the face of obstacles. This characteristic generally

describes creative individuals and successful

14

CHAPTER THREE

METHODOLOGY

3.0 Introduction.

This chapter involves research design, study population , sample size and sampling techniques

study area, methods of data collection and methods of data analysis and data quality control.

3.1 Research design.

The study used both quantitative and qualitative approaches. It is quantitative in nature in the

sense that both statistical and financial information were collected

3.2 Study area.

The study was carried out in Ntungamo municipality with high number of business units. The

study focused on commercial activities of trade like retail trade and informal manufacturing

industries like bakeries.

3.3 Study population

The study targeted the following categories of people;15 shop keeping, 6 hardware 4 hotel, 2

payphone 4 saloon, 3 shoe making, 2 butchery, and 3 tomato selling.

3.4 Sample size and sampling techniques

A sample size of 38 respondents was selected and this was drawn from the whole market. The

researcher used stratified random sampling because of mutually exclusive events and internally

homogeneous strata of business that were identified.

3.5 Methods of data collection.

The study used both primary and secondary methods of data collection.

15

Primary methods include the following;

Observation. This is one of the most appropriate methods of data collection which the researcher

employed in the research study to generate the required data. This required the researcher to go

the field directly to check on the practical transactions on the ground to show that cash

management has significant impact on growth of small scale businesses. The observed

phenomena were recorded by the researcher.

Questionnaires. The researcher used questionnaires that were given to the respondents. This

method was used because of the advantages like ability to realize high response rates and

encourages respondent’s privacy in answering the questions.

Secondary methods involved review of all relevant documents such as financial statements, text

books, journals which helped to provide a quantitative data necessary.

3.6 Data analysis and management

The questionnaires were thoroughly checked for the purposes of editing to ensure accuracy and

completeness relating to the cash management and growth of small scale businesses. The

relevant of data was also sorted out upon which individual interpretations, judgments,

conclusions and recommendations were made.

3.7 Limitations of the study

Majority of traders do not keep records which may hinder the measurement of the performance

of the business.

The other challenge which the researcher encountered in the study was inadequacy of finance,

biasness caused by traders who tried to give answers that are aimed at impressing.

Time was also another limiting factor given the fact that the researcher was faced with a lot of

course works and preparing for exams.

16

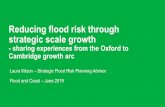

age of the respondents

age of the respondents

over 50 yrs35-50 yrs18-35 yrsunder 18 yrs

Perc

ent

100

80

60

40

20

0

CHAPTER FOUR

PRESENTATION AND DISCUSSION OF FINDINGS

4.0 INTRODUCTION

This chapter presents the interpretation and discussion of the findings. The order of the

presentation, discussion and interpretation is based on the research objectives and questions.

4.1 Demographic information

Source: primary data

38 questionnaires were distributed and all returned. Of these, 10.5% fell under 18 years,

76.3% between 18-35 years, 7.3%between 36-50 years and only 5.3%over 50 years. 29

age of the respondents

4 10.5 10.5 10.5

29 76.3 76.3 86.8

3 7.9 7.9 94.7

2 5.3 5.3 100.0

38 100.0 100.0

under 18 yrs

18-35 yrs

35-50 yrs

over 50 yrs

Total

ValidFrequency Percent Valid Percent

CumulativePercent

Table 1: Age distribution

Bar graph showing age of respondents

17

Gender of the respondnets

17 44.7 44.7 44.7

21 55.3 55.3 100.0

38 100.0 100.0

male

Female

Total

ValidFrequency Percent Valid Percent

CumulativePercent

Gender of the respondnets

Gender of the respondnets

Femalemale

Perc

ent

60

50

40

30

20

10

0

reflects a highest percentage where the population of young and energetic. They can collect

data, control plan and implement policies as regards cash management and growth of small

scale businesses. This age bracket is composed of both skilled and non skilled respondents

together with less experienced ones that may affect growth of their business.

Source: Primary data

Of the respondents 44.7% were males and 55.3% were females. Many females participated in

the study. Females in most dominate in running of small scale business especially in most of

Ugandan markets. They have got their own inefficiencies that lead to negative contribution

towards, the success of a given venture. The success in particular is as a result of

combination of a high percentage of men and that of females.

Table 2: Gender

Bar graph showing gender of respondents

18

educational level

5 13.2 13.2 13.2

11 28.9 28.9 42.1

9 23.7 23.7 65.8

13 34.2 34.2 100.0

38 100.0 100.0

'o' level

'A' Level

tertiary

University

Total

ValidFrequency Percent Valid Percent

CumulativePercent

Exepreince of the proprietor

2 5.3 5.3 5.3

17 44.7 44.7 50.0

15 39.5 39.5 89.5

4 10.5 10.5 100.0

38 100.0 100.0

less than 1 year

1-2 years

3-5 yrs

6-10 years

Total

ValidFrequency Percent Valid Percent

CumulativePercent

Exepreince of the proprietor

Exepreince of the proprietor

6-10 years3-5 yrs1-2 yearsless than 1 year

Perc

ent

50

40

30

20

10

0

Table 3: Showing educational level

Source: Primary data

Of the respondents, 34.2% university, 23.7% tertiary 28.9% A’ level, 13.2% O’level and no one

with a primary certificate. Today, small scale business have rescued most educated individuals to

earn a living reflected by an average percentage of 28.3% from university, tertiary, A, level and

O’ level. This means all categories of individuals participate in operation of small scale business

which in turn contributes more to wards growth domestic product (GDP) of the economy.

Table 4: Experience of the proprietor

Source: Primary data

Source: Primary data

Bar graph showing experience of the proprietor

19

Cash management

8 21.1 21.1 21.1

22 57.9 57.9 78.9

7 18.4 18.4 97.4

1 2.6 2.6 100.0

38 100.0 100.0

strongly agree

agree

Not sure

Strongly disagree

Total

ValidFrequency Percent Valid Percent

CumulativePercent

The respondents experience showed that 2 have less than one year, 17 between 1-2 years, 15 1-5

years and 4, 6-10 years. Most of the respondents have experience of 1-2 years meaning they have

spent little time while running business activities as compared to those with experience of 6- 10

years. These are well conversant with the business challenges and can as well circumvent them

by aligning or matching cash flows and other attributes of the business for ensure its growth.

Respondent less than one year have a lot to consider because their businesses are still in

introduction stage and should ensure all business strategies are put in place in order to become

successful and hence growth.

4.2 Finding on cash management

Respondents were required to tick according to how they felt about the issues on cash

management, growth of small scale businesses and the relation between cash management and

growth of small scale business.

Source: Primary data

Table 5: Strictness on cash management

20

control over cash recieved , colleted and banked

7 18.4 18.4 18.4

12 31.6 31.6 50.0

8 21.1 21.1 71.1

8 21.1 21.1 92.1

3 7.9 7.9 100.0

38 100.0 100.0

strongly agree

agree

Not sure

Disagree

strongly disagree

Total

ValidFrequency Percent Valid Percent

CumulativePercent

Cash management

Cash management

Strongly disagreeNot sureagreestrongly agree

Per

cent

70

60

50

40

30

20

10

0

Source: Primary data

21.1% of the respondents strongly agreed, 57.9% agreed, 18.4% not sure, no one disagreed and

only one respondent strongly disagreed. 21.1% strongly agreed implying they manage business

with the intention of getting a return at the end of the period. They match cash inflows against

cash out flows and critically observe all avenues where a big return could be achieved

(Cardaralla; Toni, 2010). No one disagreed and only one strongly disagreed meaning they

operate business without putting much emphasis about managing cash which in turn will affect

the overall growth of the business (Ohlson; Harvard, 2009). Strictness on cash management

should be emphasized for better performance.

Table 6: Control over cash received, collected and banked

Source: Primary data

Bar graph showing strictness on cash management

21

cash planning

8 21.1 21.1 21.1

8 21.1 21.1 42.1

14 36.8 36.8 78.9

3 7.9 7.9 86.8

5 13.2 13.2 100.0

38 100.0 100.0

Strongly agree

Agree

Not sure

Disagree

Strongly disagree

Total

ValidFrequency Percent Valid Percent

CumulativePercent

control over cash recieved , colleted and banked

control over cash recieved , colleted and banked

strongly disagree

Disagree

Not sure

agree

strongly agree

Perc

ent

40

30

20

10

0

Source: Primary data

Of 38 questionnaires returned, 18.4% strongly agreed, 31.6% agreed 21.6% not sure21.6%

disagreed and 7.9% strongly disagreed. 50% of the respondents, control cash once received from

different source by banking, recording in the books of accounts, issuing receipts to customers

among others. This avails information to the business from where a decision can be made

reflecting improved performance (Davidson; Charles, 2008). However, 11 respondents about

29% conduct business without maximally controlling cash as a major resource. They base on

other factors they believe affects growth severely than managing cash. This creates cash

shortages that affects sooth running of the business activities (lorek; willinger, 2011). 21.1% not

sure implying that respondents do not aim at controlling cash. All business entities should have

cash controls for improved performance.

Table 7: Cash Planning

Source: Primary data

Bar graph showing control of cash received, collected

and banked

22

strongest credit policy over debt collections

8 21.1 21.1 21.1

10 26.3 26.3 47.4

8 21.1 21.1 68.4

7 18.4 18.4 86.8

5 13.2 13.2 100.0

38 100.0 100.0

Strongly agree

Agree

Not sure

Disagree

Strongly Disagree

Total

ValidFrequency Percent Valid Percent

CumulativePercent

cash planning

cash planning

Strongly disagree

Disagree

Not sure

Agree

Strongly agree

Per

cent

40

30

20

10

0

Source: Primary data

42.2% strongly agree that cash planning is aimed at having optimal cash balance meaning they

apportion appropriately cash that makes the business to retain enough cash which can be

invested in other profitable activities that will enable the business grow in all corners and

improve performance (Richard;Partricia,2009). On the other hand 46.9% of the respondents did

not agree at all and were not sure whether cash planning is aimed at having optimal cash balance.

This means at times they operate with no cash balance which impedes economic growth of the

business. All times a lucrative business should operate with enough cash balance to full fill its

objectives.

Table 8: Strongest credit policy over debt collections

Source: Primary data

Bar graph showing cash Planning

23

various sources of cash in flows

12 31.6 31.6 31.6

10 26.3 26.3 57.9

4 10.5 10.5 68.4

6 15.8 15.8 84.2

6 15.8 15.8 100.0

38 100.0 100.0

strongly agree

agree

Not sure

disagree

Strongly disagree

Total

ValidFrequency Percent Valid Percent

CumulativePercent

strongest credit policy over debt collections

strongest credit policy over debt collections

Strongly Disagree

Disagree

Not sure

Agree

Strongly agree

Perc

ent

30

20

10

0

Source: primary data

21.1% strongly agreed, 26.3% agreed, 21.1% not sure, 18.4% disagreed and 13.2% strongly

disagreed. Small scale business experience both cash sales and credit sales. 47.4% of the

respondents sell on credit, give terms and conditions to buy and ensure that they are

implemented. This helps business owners collect cash easily and as soon as possible which is

turn accelerate business growth (Chen; Wei, 2011). 52.6% of the respondents do not keep

records concerning debits, do not follow debtors, do not give terms and condition. The business

at times fails to access information concerning debtors. This greatly retards growth of small scale

business. All business operators should keep records concerning debtors to easily know the

amount due and how it can be recovered.

Table 9: Various sources of cash inflows

Source: primary data

Bar graph showing strongest credit policy over debt collection

24

various sources of cash in flows

various sources of cash in flows

Strongly disagree

disagree

Not sure

agree

strongly agree

Perc

ent

40

30

20

10

0

Source: Primary data

31.6% strongly agreed, 26.3% agreed, 10.5% not sure 15.8% disagreed and 15.8% strongly

disagreed. Businesses have avenues where they get source of findings that contribute to words

their income. 57..9% of the businesses have different alternative source of cash inflow that

increases on their income base reflecting improved/ increased performance like collecting debts,

sell of business property and cash sales (Ham;Harvard,2002). However 41.1% of the businesses

have few sources of cash inflows. This contributes negatively towards growth of small scale

businesses. In other worlds these businesses grow at slow rate as compared to those with many

sources of cash inflows. For business to grow in all dimensions, it has to identify different

sources of cash inflows and administer them very well.

Table 10: Control of cash outflows control of out put flows

4 10.5 10.5 10.5

9 23.7 23.7 34.2

11 28.9 28.9 63.2

8 21.1 21.1 84.2

6 15.8 15.8 100.0

38 100.0 100.0

strongly agree

agree

Not sure

Disagree

strongly disagree

Total

ValidFrequency Percent Valid Percent

CumulativePercent

Source: Primary data

Bar graph showing various sources of cash inflows

25

growth of small scale businesses hig growth rate

21 55.3 55.3 55.3

11 28.9 28.9 84.2

3 7.9 7.9 92.1

3 7.9 7.9 100.0

38 100.0 100.0

strongly agree

agree

Not sure

Disagree

Total

ValidFrequency Percent Valid Percent

CumulativePercent

Bar graph showing control of cash outflows

control of out put flows

control of out put flows

strongly disagree

Disagree

Not sure

agree

strongly agree

Per

cent

40

30

20

10

0

Source: Primary data

10.5% strongly agreed, 23.7% agreed, 28.9% not sure. 21.1% disagree and 15.8% strongly

disagreed. Only 34.2% of the respondents control cash outflows. This indicates business men

meet business expenses but they do not keep records for future reference (Bhulman; Bell, 2005).

They issue out cash out cash in different activities and don’t justify their expenditure. 65.8% of

the respondents does not issue receipts to customers, invoices, do not follow debtors among

others. This implies the business lacks records for future reference and limits measurement of

performance. There is a need to maintain books of account and other relevant documents towards

cash control.

4.3 Findings on growth of small scale business

Table 11: Growth of small scale businesses

Source: Primary data

Bar graph showing controls of outflows

26

Bar graph showing growth of small scale business

growth of small scale businesses hig growth rate

growth of small scale businesses hig growth rate

DisagreeNot sureagreestrongly agree

Per

cent

60

50

40

30

20

10

0

Source: Primary data

Of the respondents, 55.3% strongly agreed, 28.9% agreed, 7.9%not sure, 7.9%disagreed and no

one strongly disagreed. 32 respondents composing of 84.2% put much emphasis on cash

management in other words lay strategies to increase business income and minimize business

expenses (Arinaitwe; Stephen, 2006). The increases better performance of the business

Only 15.8% of the respondents do not recognize the growth of the small scale business increase

they spend little time to implement cash management policies. This greatly affects the general

business performance and hence decelerates growth. Respondents need to read the available

information concerning growth of small scale businesses and other factors that affect growth.

Table 12: Keenness on growth of the businesses thewness of growth of the business

6 15.8 15.8 15.8

23 60.5 60.5 76.3

9 23.7 23.7 100.0

38 100.0 100.0

Strongly agree

Agree

Not sure

Total

ValidFrequency Percent Valid Percent

CumulativePercent

Source: primary data

27

thewness of growth of the business

thewness of growth of the business

Not sureAgreeStrongly agree

Perc

ent

70

60

50

40

30

20

10

0

Source: Primary Data

Of the respondents, 15.8% strongly agreed, 60.5% agreed, 23.7% not sure and no one neither

disagreed nor strongly disagreed. 29 respondents (76.2%) invest surplus cash in income

generating activities, issue receipts to customers maintain book of account. They tend to make

sure that cash is managed well so as to achieve high business performance. Only 9 respondents

(23.7%) are not so keen to ensure that cash is properly managed. This will create a negative

effect of the business performance and hence low rate of growth (Ham; Harvad, 2002). No one

neither disagreed nor strongly disagreed meaning they all have a feeling of developing their

businesses and reap more. All business operators should be so keen to ensure that their

businesses grow.

Table 13: Satisfaction with the current rate growth satisfaction with the current rate growth

13 34.2 34.2 34.2

8 21.1 21.1 55.3

10 26.3 26.3 81.6

5 13.2 13.2 94.7

2 5.3 5.3 100.0

38 100.0 100.0

strongly agree

agree

Not sure

disagree

Strongly disagree

Total

ValidFrequency Percent Valid Percent

CumulativePercent

Source: Primary data

Bar graph showing keenness on growth of business

28

satisfaction with the current rate growth

satisfaction with the current rate growth

Strongly disagree

disagree

Not sure

agree

strongly agree

Perc

ent

40

30

20

10

0

Source: Primary data

34.2% strongly agreed, 21.1% agreed, 26.3% not sure 13.2%disagreed and 5.3% strongly

disagreed.55.3% observe great satisfaction as a result of cash management policies. This means

the observable changes are fundamental and need to be maintained.

The current growth rate of small scale business is greatly affected by failure to identify to

profitable ventures, government intervention, poor infrastructure where some individuals are not

getting enough satisfaction about 44.7% of the respondents (Azmat; Ramanie,2009). There is

still a need to combine cash management with other factors for greater satisfaction.

Table 14: Procedures to follow while collecting debts procedures to follow while collecting debts

7 18.4 18.4 18.4

10 26.3 26.3 44.7

9 23.7 23.7 68.4

9 23.7 23.7 92.1

3 7.9 7.9 100.0

38 100.0 100.0

strongly agree

agree

Not sure

Disagree

strongly disagree

Total

ValidFrequency Percent Valid Percent

CumulativePercent

Source: Primary data

Bar graph showing satisfaction with current rate growth

29

procedures to follow while collecting debts

procedures to follow while collecting debts

strongly disagree

Disagree

Not sure

agree

strongly agree

Perc

ent

30

20

10

0

Source: Primary data

Of the respondents, 18.4%strongly agreed, 26.3% agreed, 23.7% not sure, 23.7% disagreed and

7.9% strongly disagreed. This means only 44.7% of the respondents have procedures they follow

while collecting debts. They issue invoices, give short credit period to ensure uniform cash

balance in the business (Hill; William, 2004). This enhances business growth due to improved

performance. However, 21 respondents (55.3%) carry out business activities without ensuring

debt collection procedures. This leads to accumulation of debts that reduces on the profits in the

ordinary course of the business hence affect growth. Documents concerning debtors are very

important for easy retrieval of the amount due.

Table 15: Effect on Inadequate financing on growth rate effect of Inadquate financing on growth rate

11 28.9 28.9 28.9

12 31.6 31.6 60.5

7 18.4 18.4 78.9

5 13.2 13.2 92.1

3 7.9 7.9 100.0

38 100.0 100.0

Strongly agree

Agree

Not sure

Disagree

Strongly disagree

Total

ValidFrequency Percent Valid Percent

CumulativePercent

Source: primary data

Bar graph showing procedures to follow while collecting debts

30

Correlations

1.000 .905*

. .035

5 5

.905* 1.000

.035 .

5 5

Pearson Correlation

Sig. (2-tailed)

N

Pearson Correlation

Sig. (2-tailed)

N

cash management

growth of smallscale businesses

cashmanagement

growth ofsmall scalebusinesses

Correlation is significant at the 0.05 level (2-tailed).*.

effect of Inadquate financing on growth rate

effect of Inadquate financing on growth rate

Strongly disagree

Disagree

Not sure

Agree

Strongly agree

Perc

ent

40

30

20

10

0

Source: primary data

28.9%strongly agreed 31.6% agreed 18.4% not sure, 13.2%disagreed and 7.9% strongly

disagreed. 23 respondents (60.5%) finance their business through various ways like seeking

credit facilities from lending institutions, sale of business property, investing surplus cash in

profitable activities among others (Shulman;Cox,2000). This enables the business to perform

well both in long run and short run. 15 respondents (39.5%) carry out their business not aiming

at future prospects like achieving set objectives. They do not adequately finance their business.

This greatly affects business performance and in turn decelerates growth. Businesses should not

be inadequately financed as a result out flows may outweigh inflows that may lead to corrupting

of the business.

4.4 Relationship between cash management and growth of small scale business

Table 16: Correlations

Bar graph showing effect of inadequate financing on growth rate

38 38

38 38

31

The results using Pearson’s correlation coefficient revealed that the relationship is significant at

5%. This means that cash management contributes 3.5% to the growth of small scale businesses

while other factors contribute 96.5%. Efficient cash management is too fundamental for business

growth. Issuing cash receipts, managing both cash flows, reconciling cashbook with the bank

among other factors greatly contributes business growth. When cash is properly managed, better

results as regards growth of small scale businesses will be achieved. (Barney, J.B, 2010)

Table 17: Regression Coefficientsa

26.188 12.248 2.138 .122

.677 .184 .905 3.686 .035

(Constant)

growth of smallscale businesses

Model1

B Std. Error

UnstandardizedCoefficients

Beta

Standardized

Coefficients

t Sig.

Dependent Variable: cash managementa.

Source: primary data

Basing on regression analysis, growth of small scale businesses(x) is a dependent variable and

cash management an independent variable(y).

Y = .122 + .035X

This means other factors like gender, experience and managerial skills, government regulations

among others also contribute to the growth of small scale abusiveness by 96.5% as indicated

above. There cash as a major resource has to efficiently managed for higher growth rates. Poor

cash management constraints many businesses operating activities as a result a few are done.

(Kaplan, R.S & Naton, 2004) Poor cash management results in low rates of growth since growth

depends on cash management as one of the major components.

Dependent variable; Growth of small scale businesses

32

CHAPTER FIVE

SUMMARY, CONCLUSION AND RECOMMENDATIONS

5.0 INTRODUCTION

This chapter presents a summary, conclusion and recommendations of the findings based on the

preceding four chapters. It also presents the researchers proposed areas of further research into

the subject of cash management and growth of small scale businesses.

5.1 Summary

The study revealed that the businesses plan for their cash requirements with the view of attaining

optimal cash balances and there are controls of cash flows. The findings also revealed that there

are controls over cash received, cash collected and cash banked.

The results also indicated that cash management is an essential aspect that the owners/managers

of the businesses have to ensure for better performance.

On growth of small scale businesses, the results revealed that small scale businesses are growing

at slow rate that was contributed by the highest percentage of 43.3% of the respondents.

While attesting management of debtors as a condition for better management of cash, it was

established that business operators put strict procedure they follow while collecting debts. This

ensures liquidity in the business. The results also revealed that business operators make sure that

they maintain cash most of the times to run the business operations smoothly.

The research further showed that there is a significant relationship between cash management

and growth of small scale businesses using Pearson’s correlation coefficient which gave r=0.05.

5.2 Conclusion

The findings of the study show that small scale businesses have cash management system which

is operational though with a few loop holes such as failure to identify cash in flows minimize

cash out flows and cash planning.

33

It was also found that cash management affects growth of small scale businesses by 5%. In

conclusion, the poor performance of the business in terms of growth can be alleviated by a

combination of all other factors that affect it.

5.3 Recommendations

5.3.1 Cash management

To strengthen cash management system, the researcher laid the following suggestions;

i) Business operators should always reconcile cash at hand with cash banked.

ii) There should maintenance of clear debt collection procedures.

iii) Business managers should endeavor study and apply scientific cash management models.

5.3.2 Growth of small scale businesses

Business operators should scan the environment and understand all the possible factors that

severely affect growth of their businesses and try to circumvent them for better performance.

5.4 Areas for further research

Further research should be carried on appropriateness of cash management models, all aspects

that form cash management and their effects on growth of small scale business.

34

REFERENCES:

Arinaitwe, Stephen.k Journal of American Academy of business, cabridge: Vol.12 Issue 4 P 325-

330, P 20.

Azmat, Fara, Samaratunge, Ramanie.Jounal of business ethics, Dec 2009, vol.90, issue 3, p 437-

452, p16.

Banker, Rajiud;Huang,Rong;Natrajan,Ramachandran. Journal of account reasaerch, June 2009,

vol.47 issue 3, p647-678, 32p

Brinchk Mann, Jan;Salomo, Soeren;Gemuenden, Hans Geog. Entrepreneurship theory and

practice, march 2011 vol.35 issue 2, p217-234, 27p.

Chen, Kevin, c.w; Chen, Zhihong; Wei k.c. John. Journal of financial and

6p. p71-86, 16p.

Ohlson,James A;Aier,Jagadison K.Contemporary accounting finance,2009, vol,

26, issue 4, p1091-1114, 24p.

Peters, Tom. California management review, fall 92, vol.35, issue1, p7-29,23p.

Wong, Yong; Poutziouris, Pankkos.Journal of enterprising culture, Sep 2010,

vol.18, issue 3, p331-354, 24p.

Cardarella, Toni. "Small Businesses Must Put Effort into Getting Customers to Pay on Time."

Knight-Ridder/Tribune Business News, September 21, 2010.

Davidson, Jeffrey P., and Charles W. Dean. Cash Traps: Small Business Secrets for Reducing

35

Costs and Improving Cash Flow. New York: Wiley, 2008.

Hertenstein, Julie H., and Sharon M. McKinnon. "Solving the Puzzle of the Cash Flow

Statement." Business Horizons. January-February 2011.

Hill, Ned C. and William L. Sartoris. Short-Term Financial Management. New York:

Macmillan, 2004.

Outcalt, Richard F., and Patricia Johnson. "Coping with a Cash Crunch." Playthings. March

2009.

Preston, Candace L. "Early Action Avoids Slow Cash Flow." Business First-Columbus.

September 26, 2007.

Shulman, Joel S. and Raymond A.K. Cox. "An Integrative Approach to Working Capital

Management." Journal of Cash Management. November/December 2000.

Baker, W. E., & Sinkula, J. M. (1999). The synergistic effect of business orientation and

learning orientation. Journal of the Academy of business, 27(4), 411-27

Barney, J. B. (2010) Firm resources and sustained competitive advantage. Journal of

Management, 17(1), 99-120.

Hamm, John, Havard.Business review, Dec 2002, vol.80 issue 12, p110-115, march 2006, vol.8

issue 2, p 167-178, 12p). quantitative analysis 02/01/2011, vol.46 issue 1, p171-207,

37p.

Lorek,Keneth.s;Willinger,g.Lee. Accounting horizons, Mar 2011, vol. 25 issue 1, P 200- 230 23p

Tong, Yen; Bin Miao.Acconting horizons, Mar 2011, vol.25, issue 1, p183-205,

36

Orientation and performance. Journal of Business Research, 58(1), 9-17.

Browne, M. W., & Cudeck, R. (2003). Alternative Ways of Assessing Model Fit..

Newbury Park: Sage Publications.

Day, G. S. (2009). The Capabilities of Market-Driven Organizations. Journal of

Acconting, 58(4), 37-52.

Day, G. S. (2002). Managing the market learning process. Journal of Business &

Industrial Marketing, 17(4), 240-252.

Day, G. S., & Wensley, R. (1988). Assessing Advantage: A Framework for Diagnosing

Competitive Superiority. Journal of Marketing, 52(2), 1-20.

Diamantopoulos, A., & Siguaw, J. (2000). Introducing Lisrel: A Guide for the

Uninitiated. London: SAGE.

Jöreskog, Karl, & Sörbom, D. (2001). LISREL 8: User's Reference Guide. Lincolnwood:

SSI (Scientific Software International).

Kaplan, R. S., & Norton, D. P. (2004). The balanced scorecard — measures that drive

performance. Harvard Business Review, 70(1), 71-79.

Kohli, A. K., & Jaworski, B. J. (2007). Market Orientation: The Construct, Research

Propositions, and Managerial Implications. Journal of Marketing, 54(2), 1

Mitronen, L. (2002). Hybridiorganisaation johtaminen. [Management of Hybrid

Organization]. Tampere: Doctoral dissertation, University of Tampere.

Mitronen, L. & Möller, K. (2003). Management of hybrid organisations: a case study in

retailing. Industrial performance, 32(5

37

QUESTIONNAIRES:

MAKERERE UNIVERSITY

FACULTY OF ECONOMICS AND MANAGEMENT

AQUSTIONNAIARE ON CASH MANAGEMENT AND GROWTH OF SMALL SCALE

BUSINESSES

Dear respondent,

I am a student at Makerere University and I am carrying out a research study on the topic cash

management and growth of small scale businesses as a partial requirement for acquisition of

bachelor’s degree of commerce of Makerere University.

I humbly seek your opinion on the issues in the questionnaire to facilitate the study about cash

management and growth of small scale businesses. Your opinion will be highly confidential and

used for academic purposes only.

Name of the researcher………………………………

PART 1

Personal data

Please tick your appropriate option

1. Age

under 18years 18-35years 36-50years over 50years

38

2. Gender

3. Education level

4. The experience of the proprietor in running the business up to:

5. The business you are operating.

………………………………………………………..

Male Female

University tertiary A level O level Primary

Less than 1 year 1-2years 3-5years 6-10years

39

PART II

CASH MANAGEMENT

Please tick your best alternative. SA-Strongly Agree, A-Agree, NS-Not Sure, D-Disagree,

SD-Strongly Disagree.

SA A NS D SD

6 The business is strict on cash management

7 The business has controls over cash received, cash collected and cash banked

8 Cash planning is aimed at having optimal cash balance.

9 The business uses a strongest credit policy over debit collection.

10 The business has various sources of cash in flows.

11 Out flows of the business are controlled /minimized.

12 Expenses are supported by documents like receipts, invoice and vouchers

13 The operating cash balances are maintained for transactions purposes

14 The excess cash in put into income generating activities

40

40

PART III

GROWTH OF SMALL SCALE BUSINESSES

Please tick your best alternative. SA-Strongly Agree, A-Agree, NS-Not Sure,

D- Disagree, SD-Strongly Disagree.

THANK YOU VERY MUCH

SA A NS D SD

15 Your business is growing at a very high rate.

16 You are so keen to ensure growth of your business.

17 You are greatly satisfied with the rate at which your business has been

growing.

18 There are procedures you put in place to follow while collecting debts.

19 Inadequate financing affects your business growth rate.

20 Your business has been in position to retain most of its regular

customers.

21 Your business provides goods and services according to customer

demands.

22 Your business always maintains cash to meet its short term obligations.

41

APPENDICES:

Questionnaire

Introductory letter