Capital Markets Insights: Credit Availability for the Middle Market Remains Robust

8

Industry Insights: Capital Markets November 2015 Highlights Credit activity remains robust despite recent volatility in global markets “Flight to quality” has contributed to a modest increase in non-investment grade bond and leveraged loan yields over Q3 2015 Moderate increase in yields of middle market credits has been tempered by fuller covenant packages and continued robust investor demand for private (and illiquid public) debt exposure Traditional bank lenders tightened credit parameters citing macroeconomic volatility and energy sector weakness, leading to a partial reallocation of capital structures Market volatility in China triggered a global slowdown in demand for commodities and finished goods

-

Upload

duff-phelps -

Category

Economy & Finance

-

view

106 -

download

1

Transcript of Capital Markets Insights: Credit Availability for the Middle Market Remains Robust

Industry Insights:

Capital Markets

November 2015

Highlights

Credit activity remains robust despite recent volatility in global markets

“Flight to quality” has contributed to a modest increase in non-investment grade bond and leveraged loan yields over Q3 2015

Moderate increase in yields of middle market credits has been tempered by fuller covenant packages and continued robust investor demand for private (and illiquid public) debt exposure

Traditional bank lenders tightened credit parameters citing macroeconomic volatility and energy sector weakness, leading to a partial reallocation of capital structures

Market volatility in China triggered a global slowdown in demand for commodities and finished goods

The third quarter began rather benignly for the credit markets and became increasingly volatile as the months progressed. While domestic macroeconomic fundamentals steadily improved over the quarter, the ongoing uncertainty concerning the timing and magnitude of monetary policy adjustments garnered considerable market attention. More significant, the sharp slowdowns experienced in the Eurozone and Asia—China in particular—soon carried over into the commodity and equity markets. Increases in credit spreads soon followed. Non-investment grade bond yields increased by over 150bp over the quarter (Barclays U.S. Corporate High Yield Index) while leveraged loan spreads experienced a 40bp increase (S&P/LSTA U.S. Leveraged Loan 100 Index).

The middle market, the focus of our private capital markets practice at Duff & Phelps, moved in tandem with the public markets, though with a few key differences. First, we observed a relatively modest (~50bps) increase in private note yields. Second, a trimming in first lien debt appetite resulted in a higher proportion of second lien and junior debt in capital structures. We believe the fuller covenant packages typical of the private market, combined with unabated growth in private investor capital formation, have served to differentiate middle market conditions from those of the broader liquid markets. Thus, while the weighted average cost of debt for middle market issuers has increased modestly, credit availability—both in terms of leverage multiples and cost—is robust.

Capital Markets Industry Insights – November 2015

Executive Summary

Duff & Phelps 2

Indicative Middle-Market Credit Parameters

Leverage Multiples EBITDA of $10MM - $20MM EBITDA of $20MM - $50MM

Senior Debt 2.50x - 3.25x 2.00x - 4.00x

Total Debt 3.75x - 4.50x 4.00x - 5.25x

Pricing EBITDA of $10MM - $20MM EBITDA of $20MM - $50MM

First Lien Libor + 3.00% - 4.00% Libor + 2.75% - 3.50%

Second Lien Libor + 6.50% - 9.50% Libor + 6.00% - 9.00%

Subordinated Debt 11.00% - 13.00% 10.00% - 12.00%

Unitranche Libor + 6.50% - 9.00% Libor + 6.00% - 8.50%

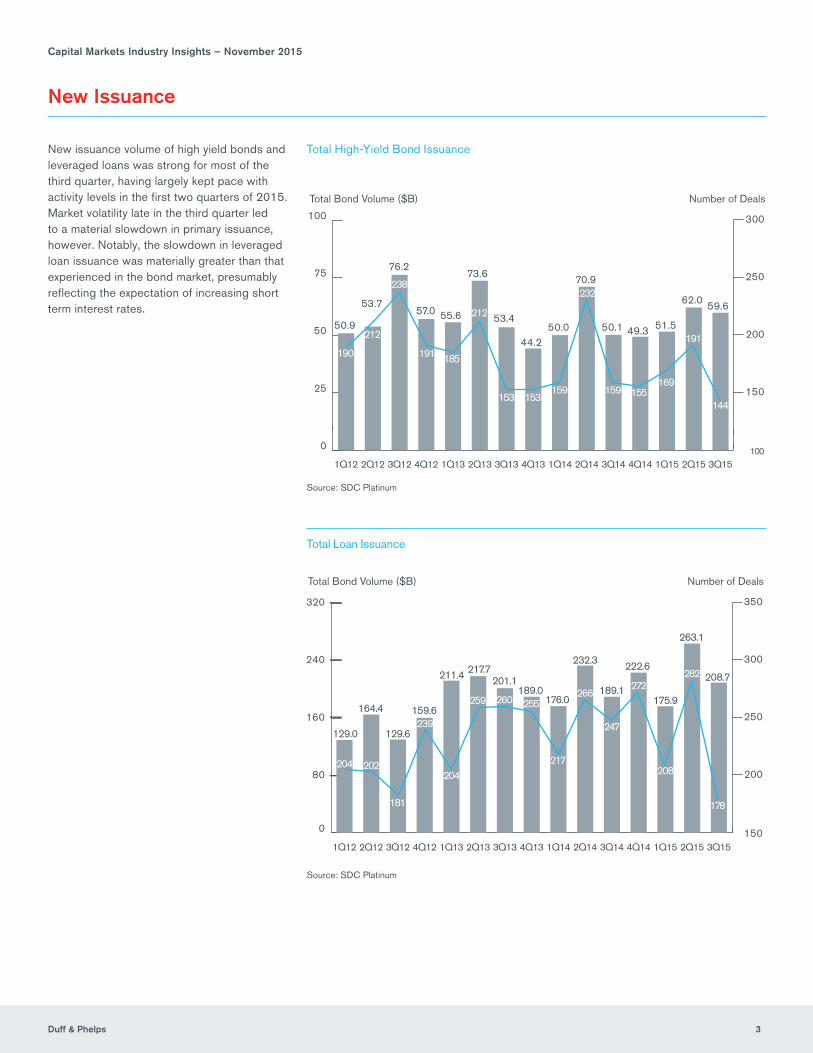

New Issuance

New issuance volume of high yield bonds and leveraged loans was strong for most of the third quarter, having largely kept pace with activity levels in the first two quarters of 2015. Market volatility late in the third quarter led to a material slowdown in primary issuance, however. Notably, the slowdown in leveraged loan issuance was materially greater than that experienced in the bond market, presumably reflecting the expectation of increasing short term interest rates.

0

25

50

75

100

3Q152Q151Q154Q143Q142Q141Q144Q133Q132Q131Q134Q123Q122Q121Q12

Total Bond Volume ($B)

150

200

250

300

100

Number of Deals

50.9

53.7

76.2

57.0 55.6

73.6

53.4

44.250.0

70.9

50.1 49.3 51.5

62.0 59.6

190

212

238

191 185

212

153 153159

232

159 155169

191

144

Total High-Yield Bond Issuance

Total Loan Issuance

Duff & Phelps 3

0

80

160

240

320

3Q152Q151Q154Q143Q142Q141Q144Q133Q132Q131Q134Q123Q122Q121Q12

Total Bond Volume ($B)

200

250

300

350

150

Number of Deals

129.0

164.4

129.6

159.6

211.4 217.7201.1

189.0176.0

232.3

189.1

222.6

175.9

263.1

208.7

204 202

181

239

204

259 260 255

217

266

247

272

208

282

178

Source: SDC Platinum

Source: SDC Platinum

Capital Markets Industry Insights – November 2015

New Issuance - Continued

Duff & Phelps 4

Total Loan Issuance EBITDA < $50MMThe energy and power vertical experienced the sharpest drop in activity, a decline of 54% in the quarter and 25% YTD versus last year (by dollar volume). As collateral bases continue to decline in the space, we anticipate further shrinking in bank debt exposure (largely through redeterminations).

0

10

20

30

40

50

60

3Q152Q151Q154Q143Q142Q141Q144Q133Q132Q131Q134Q123Q122Q121Q12

Total Bond Volume ($B)

75

100

125

150

50

Number of Deals

15.3

22.924.8

35.9

52.7

39.0

32.4

41.5 43.2

51.0

32.2 33.0

18.6

56.4

19.5

5861

65

96

60

96

84

90

79

110

97110

61

108

57

Source: SDC Platinum

U.S. High Yield Bonds by Industry (YTD through Q3)

Total Bond Volume ($B) YTD 2014YTD 2015

0.0

10.0

20.0

30.0

40.0

50.0

60.0

Financ

ials

Energ

y & P

ower

Health

care

Med

ia & E

nter.

Indus

trials

Mate

rials

Telec

om.

Real E

state

Tech

nolog

y

Consu

mer D

iscr.

Retail

Consu

mer S

taples

Source: SDC Platinum

Capital Markets Industry Insights – November 2015

Yield (%)

4.5

5.5

6.5

7.5

8.5

Jan-12 Jul-12 Jan-13 Jul-13 Jan-14 Jul-14 Jan-15 Jul-15

Barclays U.S. Corporate High YieldS&P/LSDA U.S. Leveraged Loan 100

Yields

Yields on high yield bonds and leveraged loans rose 153bps and 42bps, respectively, this quarter. A modest “flight to quality”—especially as the slowdown in economic activity in China became apparent—drove Treasury yields down. The increase in risk premiums, however, dominated as the quarter progressed.

Source: SDC Platinum

Duff & Phelps 5

U.S. Corporate High Yield Bonds and Leveraged Loans

Acquisition Financing

Leverage multiples for middle market change-of-control financings increased by approximately a half turn of EBITDA in the quarter, to ~5.5x, attributable in part to a higher proportion of larger deals. Notably, the increase was funded almost wholly by junior capital providers.

Anecdotally, in recent weeks we have observed a considerable tightening of credit parameters among regional banks (and, to a lesser degree, money center banks). Lenders with whom we transact attribute the tightening to worries about energy-oriented exposure at least as much as macroeconomic conditions. We anticipate, at this writing, a reordering of capital structures on de novo financings such that one half to a full turn of leverage will reside in a junior position until present challenges are resolved.

LBO Leverage Multiples (EBITDA < $50 MM)

First LienSecond LienSubordinated

3.9x 4.2x 4.3x 4.5x 5.0x 4.5x 4.8x 4.4x 4.7x 4.9x 4.9x 4.7x 4.9x 4.8x 5.5x

0.0x

1.0x

2.0x

3.0x

4.0x

5.0x

6.0x

1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15

EV / EBITDA Multiple

Source: SDC Platinum

Capital Markets Industry Insights – November 2015

0.0%

1.0%

2.0%

3.0%

4.0%

Jan-12 Jul-12 Jan-13 Jul-13 Jan-14 Jul-14 Jan-15 Jul-15

Yield (%)

10 year

2 year

5 year

100

150

200

250

300

Jan-12 Jul -12 Jan-13 Jul -13 Jan-14 Jul -14 Jan-15 Jul -15

Spread (bps)

Macroeconomic Update

In spite of continuing improvement in domestic economic conditions, particularly the labor market, the quarter was characterized by a steady stream of exogenous cross currents.

Slowdowns in Southern Europe, Brazil, and China, Japan and South Korea led to a relative strengthening of the US dollar as well as a sharp downturn in commodity demand. The European Central Bank and central banks in Japan and China moved aggressively to cut interest rates, employ quantitative easing and selectively intervene in public capital markets.

Expectations for most of the quarter of a tightening in US monetary policy (accompanied by a flattening of the yield curve) were dashed in deference to continuing global weakness and the associated decline in U.S. export related activity.

Source: Bloomberg

Source: Bloomberg

2 Year vs. 10 Year Treasury Spread

2, 5 and 10 Year Treasury Yields

Duff & Phelps 6

Capital Markets Industry Insights – November 2015

Macroeconomic Update - Continued

Source: Capital IQ

U.S Employment

Global Commodity Indices

Duff & Phelps 7

The availability and cost of leverage for middle market issuers held up quite well relative to those of the public markets in the third quarter. A combination of fuller covenant protection for private securities and unabated private investor demand largely offset the effects of the quarter’s macroeconomic headwinds. Consequently, middle market issuers continue to enjoy the benefits of “full” leverage, albeit at a slightly higher weighted cost reflecting greater reliance on junior capital.

0

100

200

300

400

500

6.0%

7.0%

8.0%

9.0%

Jan -12 Jul -12 Jan -13 Jul -13 Jan -14 Jul -14 Jan -15 Jul -15

Unemployment Rate Jobs Added (thousands)

Source: Federal Reserve

(100.0%)

(80.0%)

(60.0%)

(40.0%)

(20.0%)

0.0%

20.0%

Jan -12 Jul -12 Jan -13 Jul -13 Jan -14 Jul -14 Jan -15 Jul -15

Dow Jones U.S. Coal IndexS&P GSCI Crude Oil IndexS&P GSCI Copper Index

Capital Markets Industry Insights – November 2015

For more information please visit: www.duffandphelps.com

About Duff & PhelpsDuff & Phelps is the premier global valuation and corporate finance advisor with expertise in complex valuation, dispute and legal management consulting, M&A, restructuring, and compliance and regulatory consulting. The firm’s more than 2,000 employees serve a diverse range of clients from offices around the world.

M&A advisory and capital raising services in the United States are provided by Duff & Phelps Securities, LLC. Member FINRA/SIPC. Pagemill Partners is a Division of Duff & Phelps Securities, LLC. M&A advisory and capital raising services in the United Kingdom and Germany are provided by Duff & Phelps Securities Ltd., which is authorized and regulated by the Financial Conduct Authority.

Contact Us

Michael BrillHead of U.S. Private Capital Markets+1 212 871 [email protected]

Bob Bartell, CFAGlobal Head of Corporate Finance +1 312 697 [email protected]

Steve BurtGlobal Head of M&A+1 312 697 [email protected]

Dave AlthoffGlobal Co-head of Industrials M&A+1 312 697 [email protected]

Josh Benn Global Head of Consumer, Retail, Food, and Restaurants+1 212 450 [email protected]

Brian CullenHead of U.S. Restructuring+1 424 249 [email protected]

Brooks DexterGlobal Head of Healthcare M&A+1 424 249 [email protected]

Kevin IudicelloManaging Director, Technology M&A+1 650 354 [email protected]

Jon MelzerGlobal Co-head of Industrials M&A+1 212 450 [email protected]

Jim RebelloGlobal Head of Energy M&A+1 713 986 [email protected]

Duff & Phelps Copyright © 2015 Duff & Phelps LLC. All rights reserved.