Accessing Asian Capital by Canadian Companies the case for ...

KPMG ENTERPRISE

Canadian Private Companies Canadian Private Companies ––Financial Statement Disclosures Financial Statement Disclosures and Access to Creditand Access to Credit

2© 2009 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

FEI Toronto:Introducing our panelistsFEI Toronto:Introducing our panelists

Bob Young, PartnerNational Assurance and Professional Practice, KPMG Enterprise

Mark Walsh, PrincipalAccounting Standards Board, CICA

Todd Shute, Vice PresidentCommercial Financial ServicesHSBC

Stephen Cummings, Principal, Lumira CapitalChair, CFO Task ForceCanadian Venture Capital Association

Peter Hatges, PartnerKPMG Enterprise

John Forester, CFONUCAP Industries Ltd.

3© 2009 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

Financial Statement Disclosuresand

Access to Credit“It’s a Matter of Trust”

Financial Statement Disclosuresand

Access to Credit“It’s a Matter of Trust”

4© 2009 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

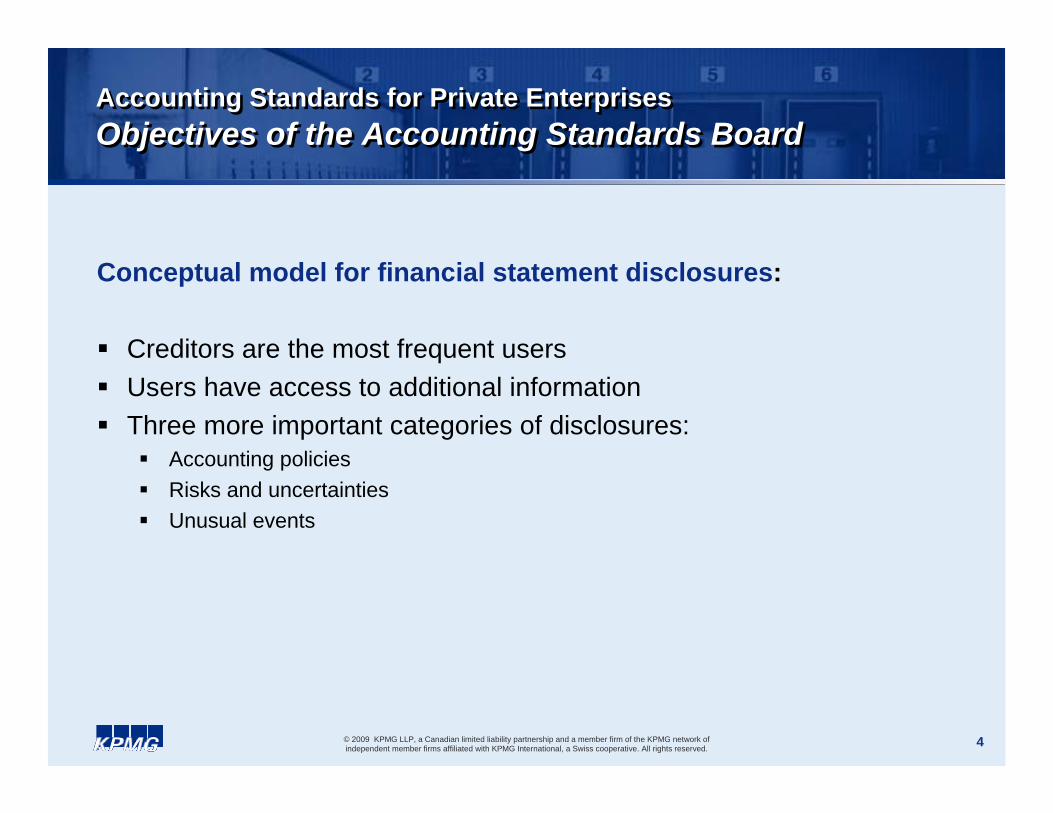

Accounting Standards for Private EnterprisesObjectives of the Accounting Standards BoardAccounting Standards for Private EnterprisesObjectives of the Accounting Standards Board

Conceptual model for financial statement disclosures:

Creditors are the most frequent usersUsers have access to additional informationThree more important categories of disclosures:

Accounting policiesRisks and uncertaintiesUnusual events

5© 2009 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

Accounting Standards for Private EnterprisesAccounting Standards for Private Enterprises

Fair Presentation – what does it mean?

Applying Generally Accepted Accounting Principles

Providing sufficient information about transactions or events . . . that are of such size, nature and incidence that their disclosure is necessary to understand that effect (the “stand-back” test)

6© 2009 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

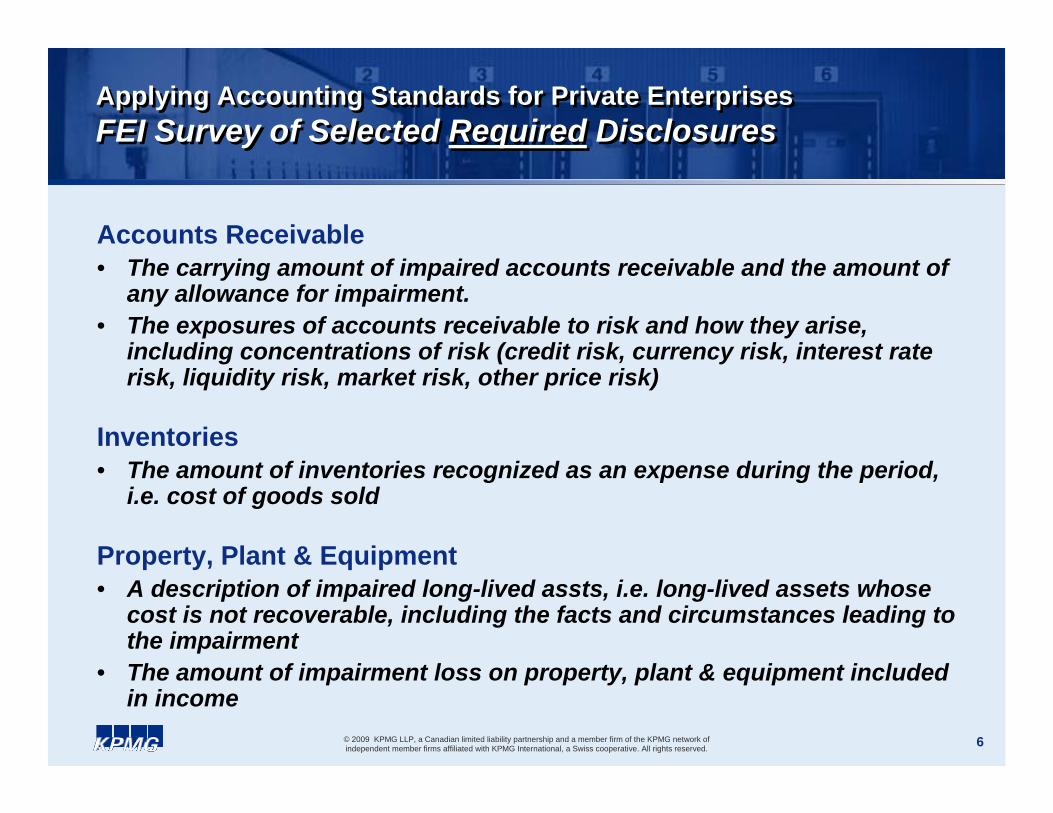

Applying Accounting Standards for Private EnterprisesFEI Survey of Selected Required DisclosuresApplying Accounting Standards for Private EnterprisesFEI Survey of Selected Required Disclosures

Accounts Receivable• The carrying amount of impaired accounts receivable and the amount of

any allowance for impairment.• The exposures of accounts receivable to risk and how they arise,

including concentrations of risk (credit risk, currency risk, interest rate risk, liquidity risk, market risk, other price risk)

Inventories• The amount of inventories recognized as an expense during the period,

i.e. cost of goods sold

Property, Plant & Equipment• A description of impaired long-lived assts, i.e. long-lived assets whose

cost is not recoverable, including the facts and circumstances leading to the impairment

• The amount of impairment loss on property, plant & equipment included in income

7© 2009 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

Applying Accounting Standards for Private EnterprisesFEI Survey of Selected Required DisclosuresApplying Accounting Standards for Private EnterprisesFEI Survey of Selected Required Disclosures

Trade Accounts Payable• The amounts payable at the end of the period in respect of government

remittances

Long-term Debt• Any debt instrument in default or breach of any term or covenant that

would permit a lender to demand accelerated repayment.• Whether any default was remedied or the terms of the liability were

renegotiated before the financial statements were completed.• The exposures of long-term debt to risk and how they arise (credit risk,

currency risk, interest rate risk, liquidity risk, market risk, other price risk)

Cash Flows• Investing and financing transactions that do not require the use of cash

or cash equivalents, including all relevant information

8© 2009 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

Applying Accounting Standards for Private EnterprisesFEI Survey of Selected Required DisclosuresApplying Accounting Standards for Private EnterprisesFEI Survey of Selected Required Disclosures

Use of Financial Information

0 20 40 60 80 100

Carrying amount ofimpaired A/R

A/R exposures tocredit risk

Cost of sales

Impaired long-livedassets - description

Amount ofimpairment loss in

income

Governmentremittances

payable

Debt instruments indefault

Remedied defaults

LTD Risks

Non-cashtransactions

Disc

losu

re

Percentage of users

Cash FlowSecurityLiquidity

9© 2009 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

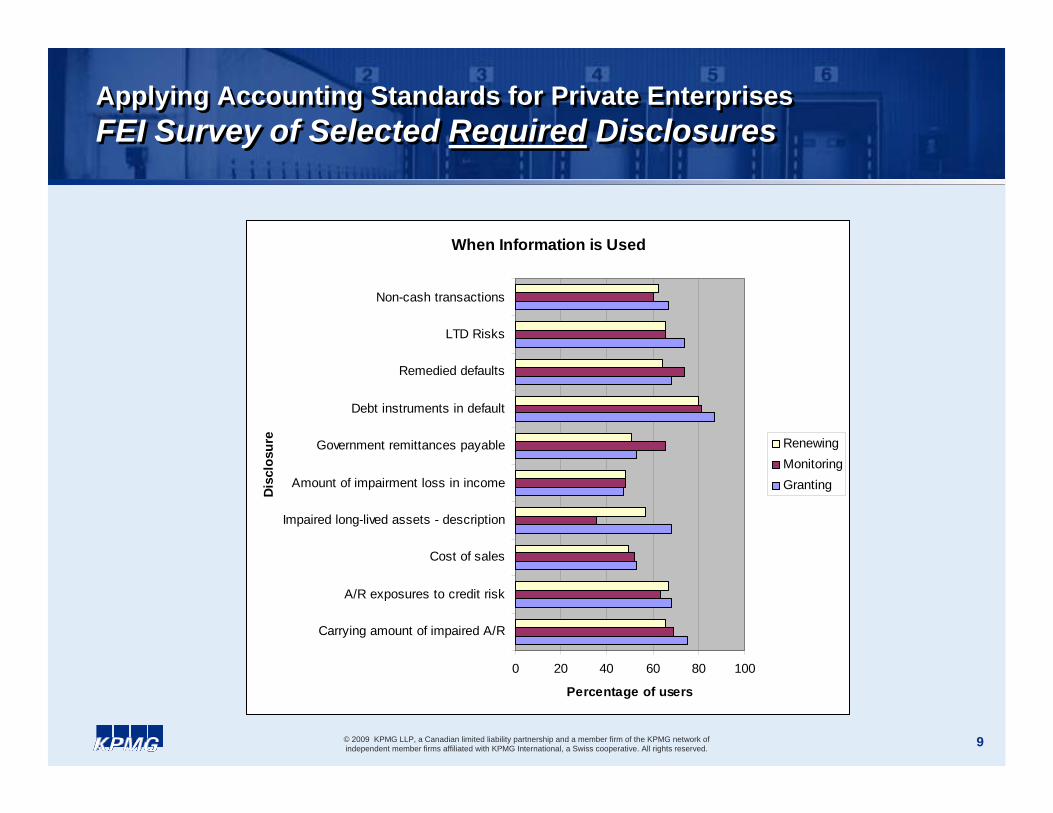

Applying Accounting Standards for Private EnterprisesFEI Survey of Selected Required DisclosuresApplying Accounting Standards for Private EnterprisesFEI Survey of Selected Required Disclosures

When Information is Used

0 20 40 60 80 100

Carrying amount of impaired A/R

A/R exposures to credit risk

Cost of sales

Impaired long-lived assets - description

Amount of impairment loss in income

Government remittances payable

Debt instruments in default

Remedied defaults

LTD Risks

Non-cash transactions

Disc

losu

re

Percentage of users

RenewingMonitoringGranting

10© 2009 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

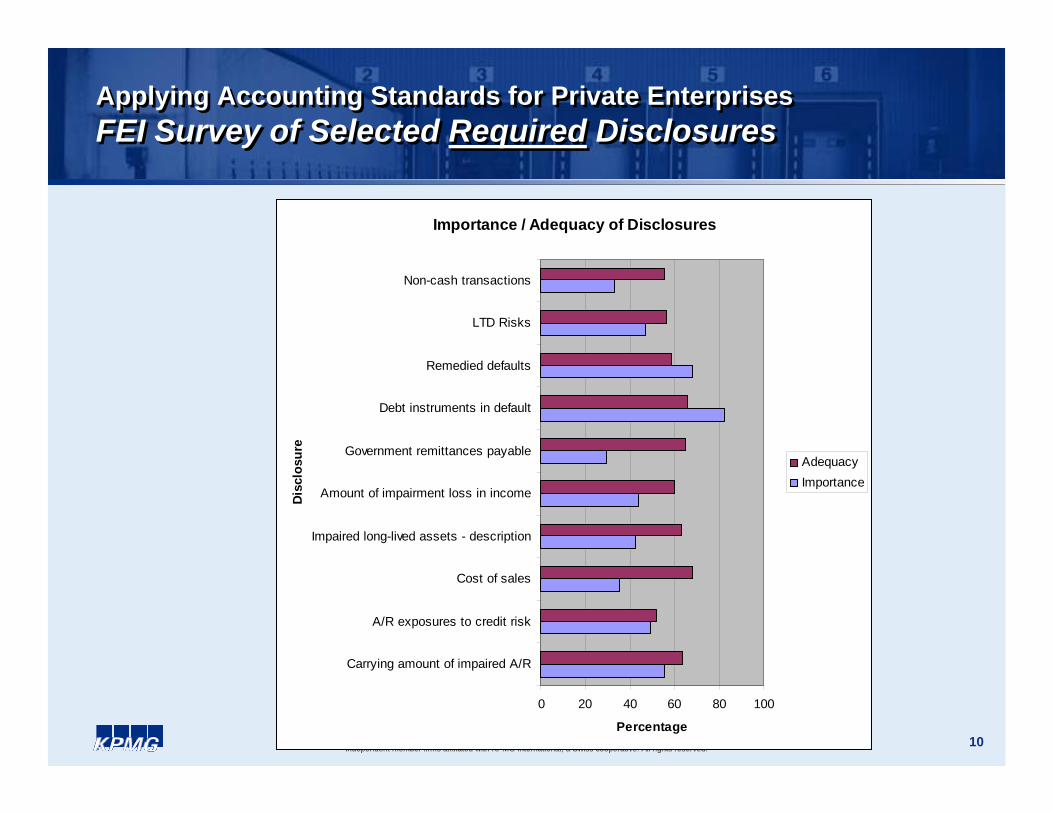

Applying Accounting Standards for Private EnterprisesFEI Survey of Selected Required DisclosuresApplying Accounting Standards for Private EnterprisesFEI Survey of Selected Required Disclosures

Importance / Adequacy of Disclosures

0 20 40 60 80 100

Carrying amount of impaired A/R

A/R exposures to credit risk

Cost of sales

Impaired long-lived assets - description

Amount of impairment loss in income

Government remittances payable

Debt instruments in default

Remedied defaults

LTD Risks

Non-cash transactionsD

iscl

osur

e

Percentage

AdequacyImportance

11© 2009 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

Panel QuestionPanel Question

Of the required disclosures surveyed, which ones do you believe are particularlyuseful / less useful to users of private company financial statements?

Why?

12© 2009 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

Applying Accounting Standards for Private EnterprisesFEI Survey of Selected Possible Additional DisclosuresApplying Accounting Standards for Private EnterprisesFEI Survey of Selected Possible Additional Disclosures

Accounts Receivable• The ageing of accounts receivable, i.e. a maturity analysis.

Inventories• The amount of inventories whose cost exceeds net realizable value.• The circumstances resulting in a provision for impairment or the

subsequent reversal of a write-down of inventories.

Property, Plant & Equipment• The fair value of property, plant & equipment.• The estimated salvage value or disposal value of plant and equipment at

the end of its estimated useful life.

13© 2009 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

Applying Accounting Standards for Private EnterprisesFEI Survey of Selected Possible Additional DisclosuresApplying Accounting Standards for Private EnterprisesFEI Survey of Selected Possible Additional Disclosures

Trade Accounts Payable• The ageing of accounts payable, i.e. a maturity analysis.

Long-term Debt• The priority of security positions on collateral.• The fair value of debt instruments.• A sensitivity analysis for each type of market risk to which the entity is

exposed.

Cash Flows• Cash flows for interest and dividends received and paid.• Cash flows arising from income taxes.

14© 2009 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

Applying Accounting Standards for Private EnterprisesFEI Survey of Selected Possible Additional DisclosuresApplying Accounting Standards for Private EnterprisesFEI Survey of Selected Possible Additional Disclosures

Value of additional disclosures for accessing credit

2.5

2.6

2.9

3

3.1

3.2

3.2

3.2

3.4

3.5

3.8

0 1 2 3 4

A sensitivity analysis for each type of market risk to which the entity is exposed

.

Estimated salvage value or disposal value of plant & equipment at end of estimated useful life

The ageing of accounts payable, i.e. a maturity analysis

The fair value of debt instruments.

Cash flows arising from income taxes

Inventory where cost>net realizable value

Fair value of property, plant and equipment

Cash flows for interest and dividends received and paid

Cause of provision of inventory impairment & reversal

Priority of security positions on collateral

Ageing of the receivables

Value for accessing credit (5=Very valuable, 1=Not at all valuable)

15© 2009 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

Applying Accounting Standards for Private EnterprisesFEI Survey of Selected Possible Additional DisclosuresApplying Accounting Standards for Private EnterprisesFEI Survey of Selected Possible Additional Disclosures

Possible Disclosures

0 10 20 30 40 50 60 70

Ageing of AR

Inventory - Cost > NRV

Inventory impairment / reversals

Fair value of PP&E

Estimates - salvage value of PP&E

Ageing of AP

Priority of security positions

Fair value of Debt Instruments

Sensitivity analysis to risk factors of LTD

Cash flows from dividends / interest

Cash flows from income taxes

Percentage

Benefits >costAdds Value

16© 2009 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

Panel QuestionPanel Question

Of the possible additional disclosures surveyed, which ones do you believewould be particularly useful / less usefulto users of private company financial statements?

Would the benefit of the disclosure warrant the cost involved to provide the information?

17© 2009 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

Panel QuestionFair Presentation – the “Stand-Back” TestPanel QuestionFair Presentation – the “Stand-Back” Test

What are some examples of situationsthat you believe “are of such size, nature and incidence that their disclosure is necessaryto understand that effect” in order to provide fair presentation.

18© 2009 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

Panel QuestionEBITDA – A Non-GAAP Performance MeasurePanel QuestionEBITDA – A Non-GAAP Performance Measure

EBITDA is a term that underlies many lending agreements. It is not a defined accounting term which precludes its presentation in financial statements.

Should companies be entitled to measure and disclose EBITDA in their financial statements?

What would be the benefits and challenges?

19© 2009 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

Panel QuestionManagement Discussion and AnalysisPanel QuestionManagement Discussion and Analysis

Public companies are required toprovide MD&A to assist the users of theirfinancial statements in understanding significant changes in the business, risk factors, etc.

20© 2009 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

Panel QuestionManagement Discussion and AnalysisPanel QuestionManagement Discussion and Analysis

Principles• enable readers to view the entity through management's eyes;• supplement and complement the information in the financial

statements;• be complete, fair and balanced, and provide information that is material

to the decision-making needs of users;• have a forward-looking orientation;• focus on management's strategy for generating value over time; and• be understandable, relevant, and comparable.

Canadian Performance Reporting Board

21© 2009 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

Panel QuestionManagement Discussion and AnalysisPanel QuestionManagement Discussion and Analysis

Disclosure Framework

• Core businesses and strategy• Key performance drivers• Capability to deliver results• Results and outlook• Risk

22© 2009 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

Panel QuestionManagement Discussion and AnalysisPanel QuestionManagement Discussion and Analysis

Would a framework for an MD&A model for private companies be useful to borrowers and lenders in “putting some color on the canvas”to facilitate access to capital?

23© 2009 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

Accounting Standards for Private EnterprisesAccounting Standards for Private Enterprises

The Future?• Contentious areas• Transition balance sheet• IFRS

24© 2009 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

Accounting Standards for Private EnterprisesAccounting Standards for Private Enterprises

Contentious Areas not Simplified / Amended• Stock-based compensation• Lease accounting• Classification of Callable Debt

Panel Views?

25© 2009 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

Accounting Standards for Private EnterprisesAccounting Standards for Private Enterprises

The Transition Balance Sheet Elections• Fair value items of property, plant and equipment• Write-off certain unrecognized balances

Unamortized gains & losses on defined benefit pension plansCumulative translation account

Panel Views?

26© 2009 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

Accounting Standards for Private EnterprisesAccounting Standards for Private Enterprises

The Future• ASPE – maintain a “made in Canada” solution”• IFRS• IFRS for SMEs• Other

Panel Views?

27© 2009 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

Assurance StandardsChange Here Too!Assurance StandardsChange Here Too!

“Fair Presentation” vs. “Compliance” Frameworks• Today

ContractLegislationRegulation

• TomorrowUnrestricted

Panel Views?

28© 2009 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

Executive Dialogue:Open FloorExecutive Dialogue:Open Floor

Q&A

29© 2009 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

Closing RemarksClosing Remarks

Dennis Fortnum, PartnerNational Leader, KPMG Enterprise

Your feedback is important to us.

Please take a few moments to provide your commentson the evaluation forms and submit to our event team upon your departure.

30© 2009 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.