Canadian Institute Conference - Arvind Mani's Presentation - Final - April 1 2015

48

pdci.ca ©2015 PDCI Market Access Global Trends: Drug Pricing, Reimbursement and Market Access Arvind Mani Director, Market Access and Policy Research E-mail: [email protected] 1 ©2015 PDCI Market Access

-

Upload

arvind-mani -

Category

Documents

-

view

280 -

download

3

Transcript of Canadian Institute Conference - Arvind Mani's Presentation - Final - April 1 2015

pdci.ca

©2015 PDCI Market Access

Global Trends: Drug Pricing, Reimbursement and Market Access

Arvind ManiDirector, Market Access and Policy Research

E-mail: [email protected]

1©2015 PDCI Market Access

2

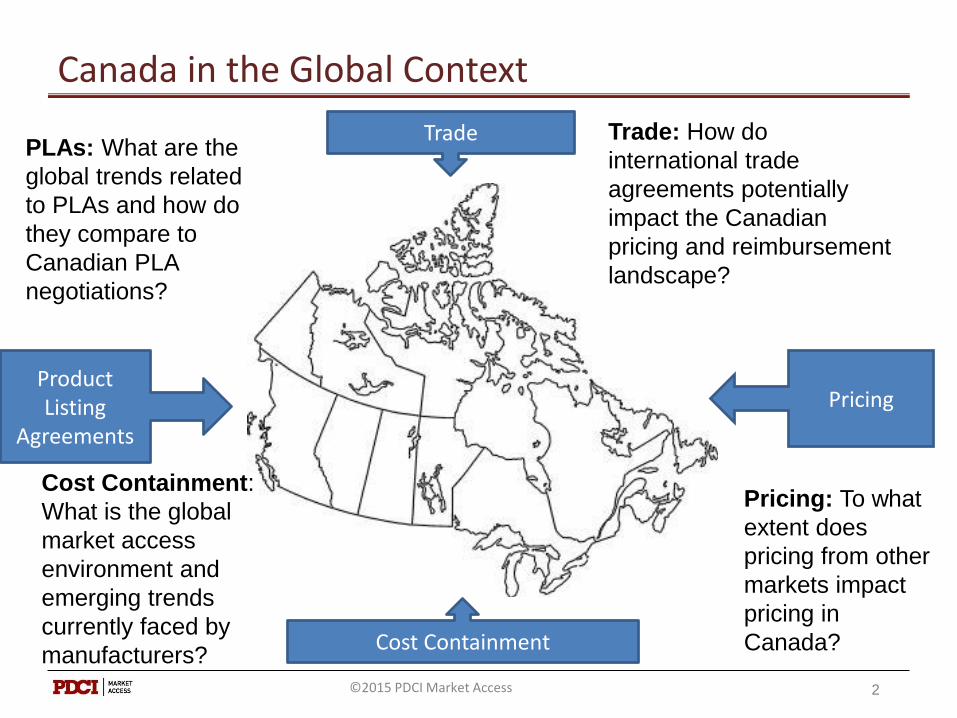

Canada in the Global Context

Product Listing

Agreements

Pricing

Cost Containment

Trade Trade: How do

international trade

agreements potentially

impact the Canadian

pricing and reimbursement

landscape?

Pricing: To what

extent does

pricing from other

markets impact

pricing in

Canada?

Cost Containment:

What is the global

market access

environment and

emerging trends

currently faced by

manufacturers?

PLAs: What are the

global trends related

to PLAs and how do

they compare to

Canadian PLA

negotiations?

©2015 PDCI Market Access

Context

3©2015 PDCI Market Access

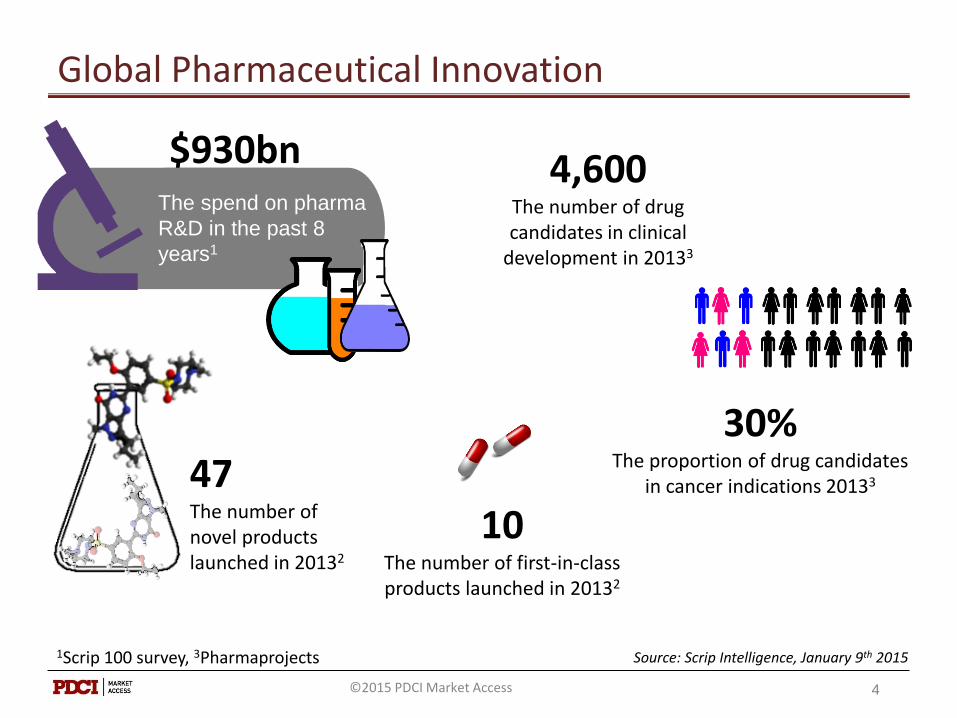

4,600The number of drug candidates in clinical

development in 20133

$930bnThe spend on pharma

R&D in the past 8

years1

30%The proportion of drug candidates

in cancer indications 20133

1Scrip 100 survey, 3Pharmaprojects Source: Scrip Intelligence, January 9th 2015

4

47The number of novel products launched in 20132

Global Pharmaceutical Innovation

10The number of first-in-class products launched in 20132

©2015 PDCI Market Access

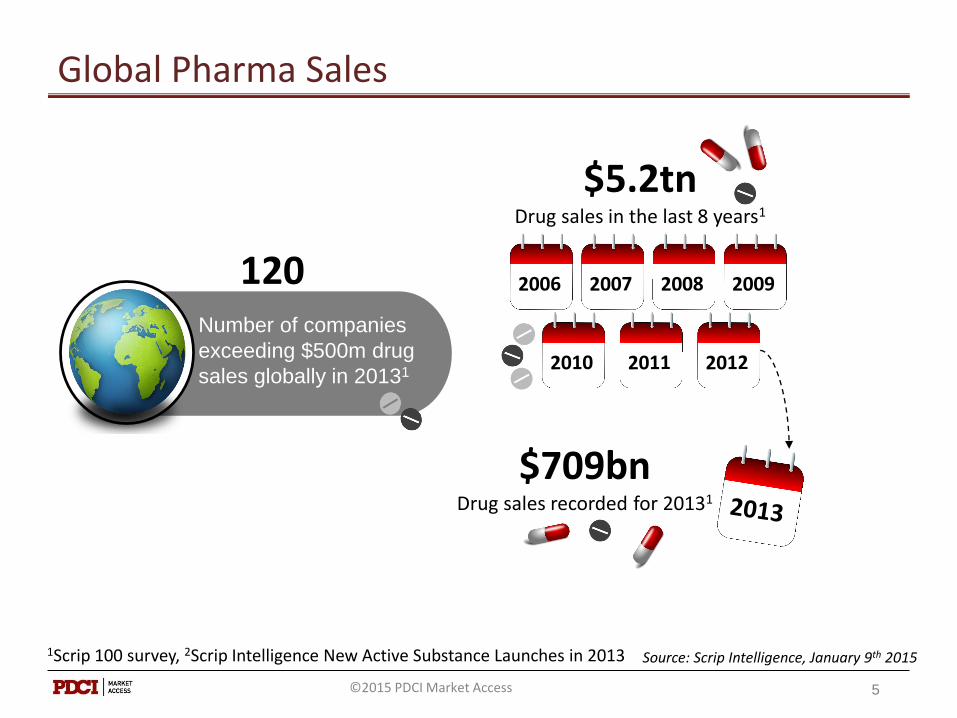

120Number of companies

exceeding $500m drug

sales globally in 20131

$5.2tnDrug sales in the last 8 years1

$709bnDrug sales recorded for 20131

1Scrip 100 survey, 2Scrip Intelligence New Active Substance Launches in 2013 Source: Scrip Intelligence, January 9th 2015

5

Global Pharma Sales

©2015 PDCI Market Access

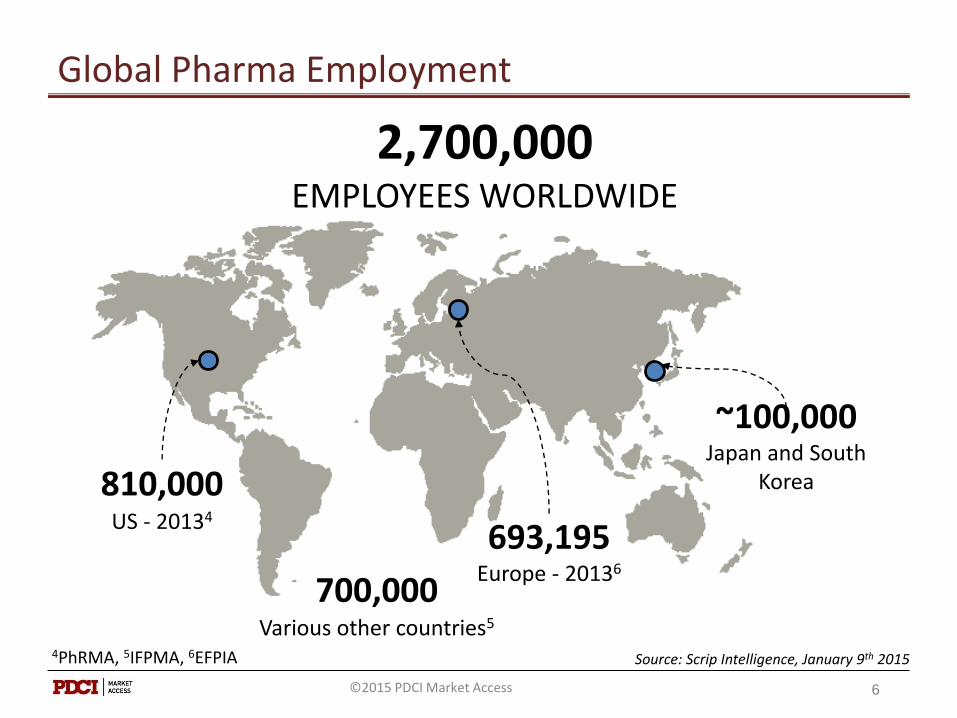

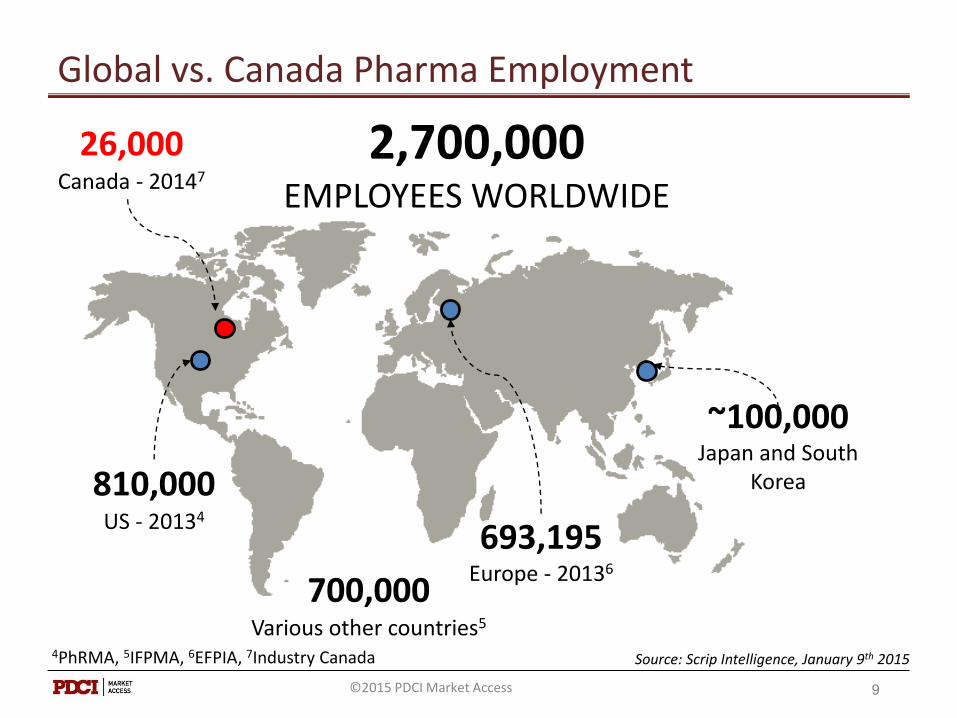

2,700,000EMPLOYEES WORLDWIDE

810,000US - 20134

700,000Various other countries5

693,195Europe - 20136

~100,000Japan and South

Korea

4PhRMA, 5IFPMA, 6EFPIA Source: Scrip Intelligence, January 9th 2015

Global Pharma Employment

6©2015 PDCI Market Access

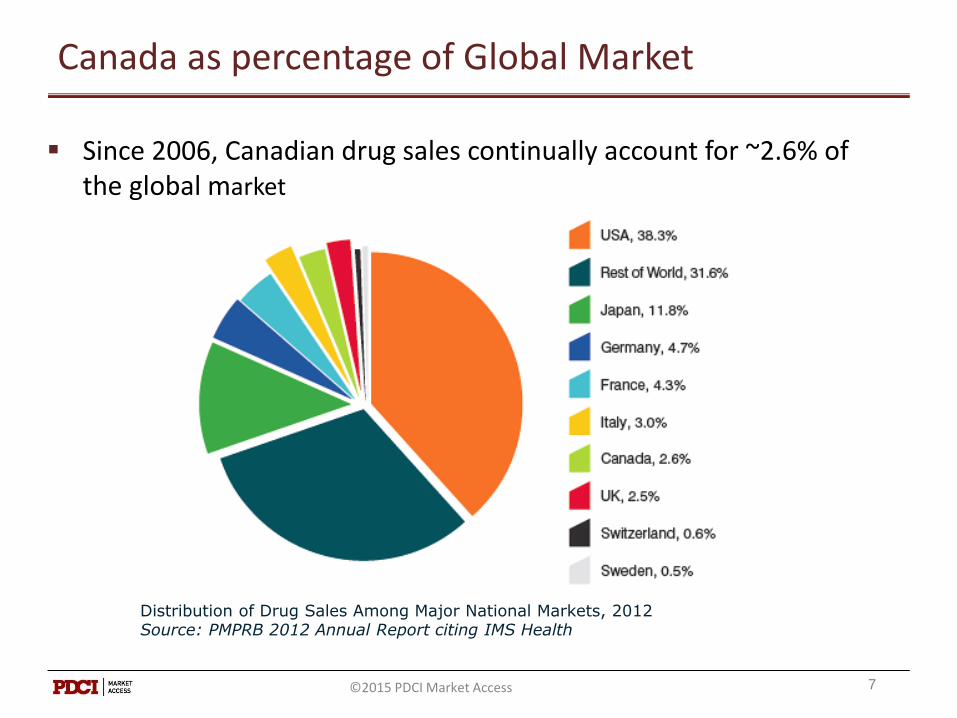

Canada as percentage of Global Market

Since 2006, Canadian drug sales continually account for ~2.6% of the global market

7

Distribution of Drug Sales Among Major National Markets, 2012Source: PMPRB 2012 Annual Report citing IMS Health

©2015 PDCI Market Access

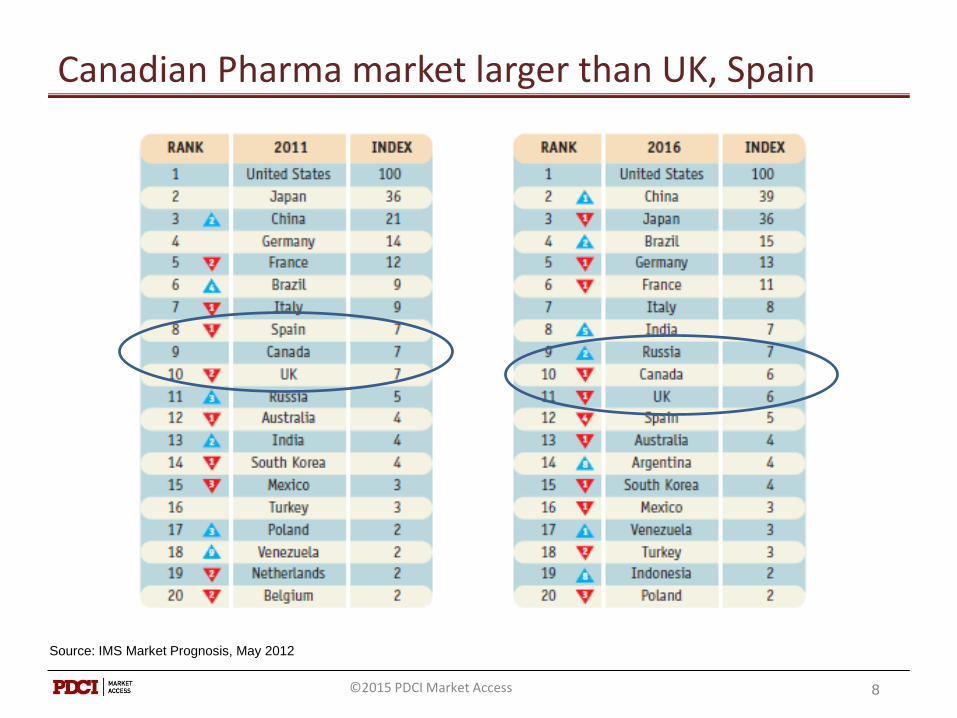

Canadian Pharma market larger than UK, Spain

8

Source: IMS Market Prognosis, May 2012

©2015 PDCI Market Access

2,700,000EMPLOYEES WORLDWIDE

810,000US - 20134

700,000Various other countries5

693,195Europe - 20136

~100,000Japan and South

Korea

4PhRMA, 5IFPMA, 6EFPIA, 7Industry Canada Source: Scrip Intelligence, January 9th 2015

Global vs. Canada Pharma Employment

9

26,000Canada - 20147

©2015 PDCI Market Access

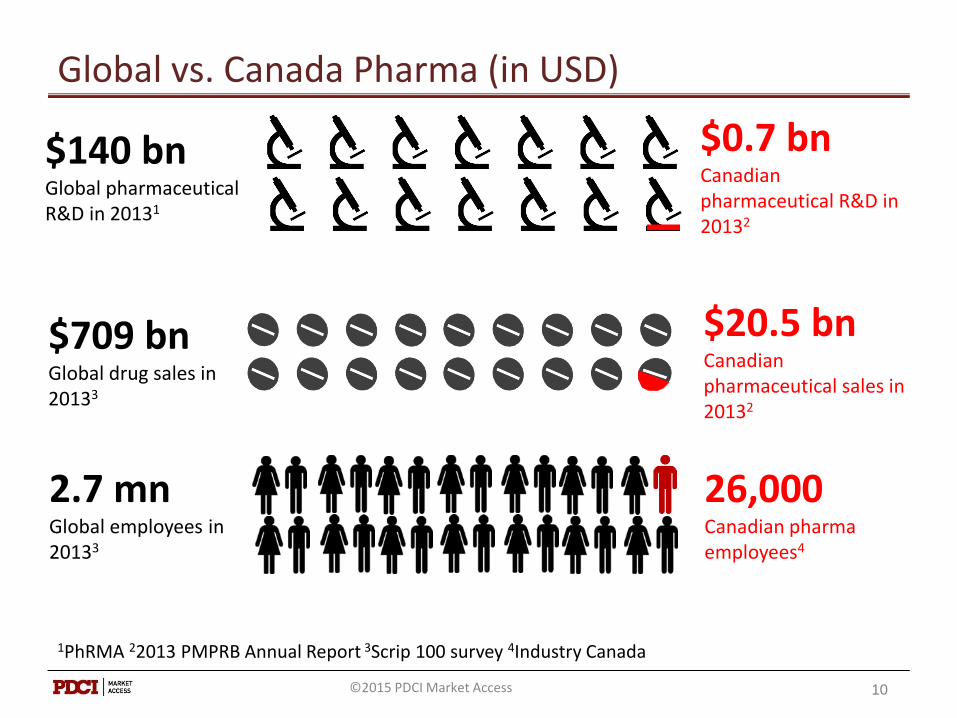

Global vs. Canada Pharma (in USD)

1PhRMA 22013 PMPRB Annual Report 3Scrip 100 survey 4Industry Canada

10

$140 bnGlobal pharmaceutical R&D in 20131

$0.7 bnCanadian pharmaceutical R&D in 20132

$709 bnGlobal drug sales in 20133

$20.5 bnCanadian pharmaceutical sales in 20132

26,000Canadian pharma employees4

2.7 mnGlobal employees in 20133

©2015 PDCI Market Access

Trade

11

Product Listing

Agreements

Pricing

Cost Containment

Trade

©2015 PDCI Market Access

Canada - EU Trade Agreement - CETA

Comprehensive Economic and Trade Agreement (CETA):Pharma IP Provisions: (Details still to be announced)

• Patent Term Restoration

Extended Data Protection

• Innovator Right of Appeal

12©2015 PDCI Market Access

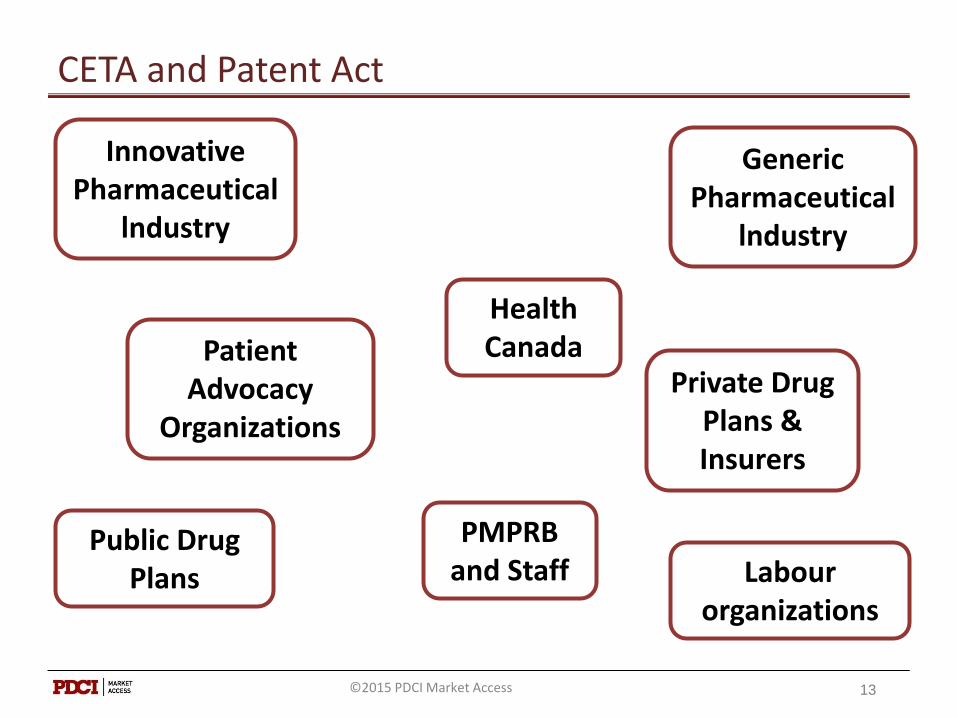

CETA and Patent Act

13

Innovative Pharmaceutical

lndustry

Generic Pharmaceutical

lndustry

Private Drug Plans & Insurers

PMPRB and Staff

Patient Advocacy

Organizations

Health Canada

Public Drug Plans Labour

organizations

©2015 PDCI Market Access

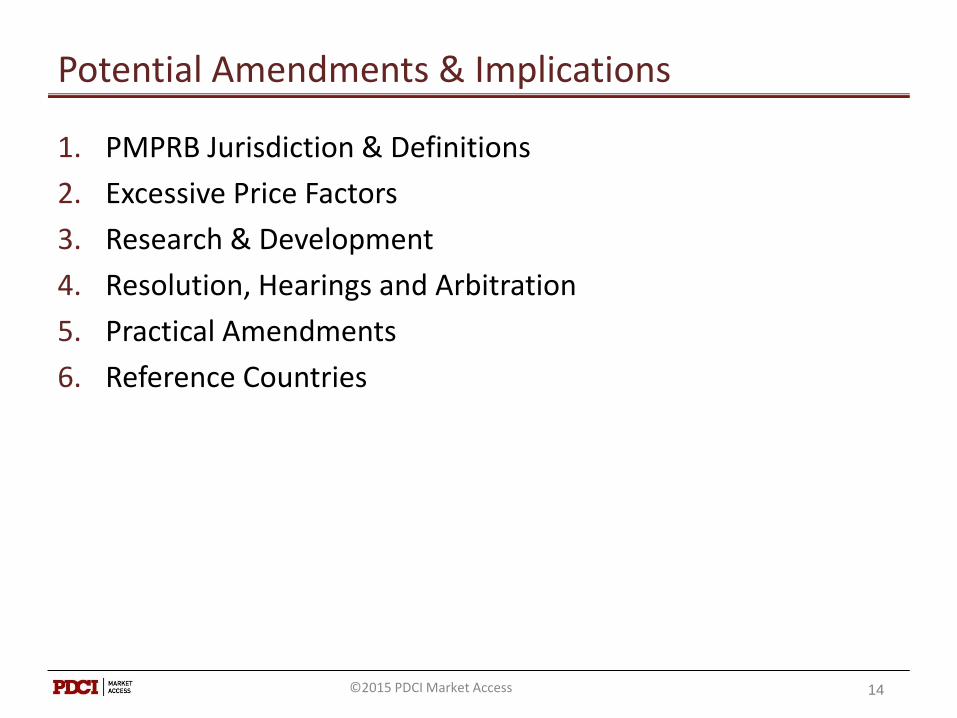

Potential Amendments & Implications

1. PMPRB Jurisdiction & Definitions

2. Excessive Price Factors

3. Research & Development

4. Resolution, Hearings and Arbitration

5. Practical Amendments

6. Reference Countries

14©2015 PDCI Market Access

Pricing

15

Product Listing

Agreements

Pricing

Cost Containment

Trade

©2015 PDCI Market Access

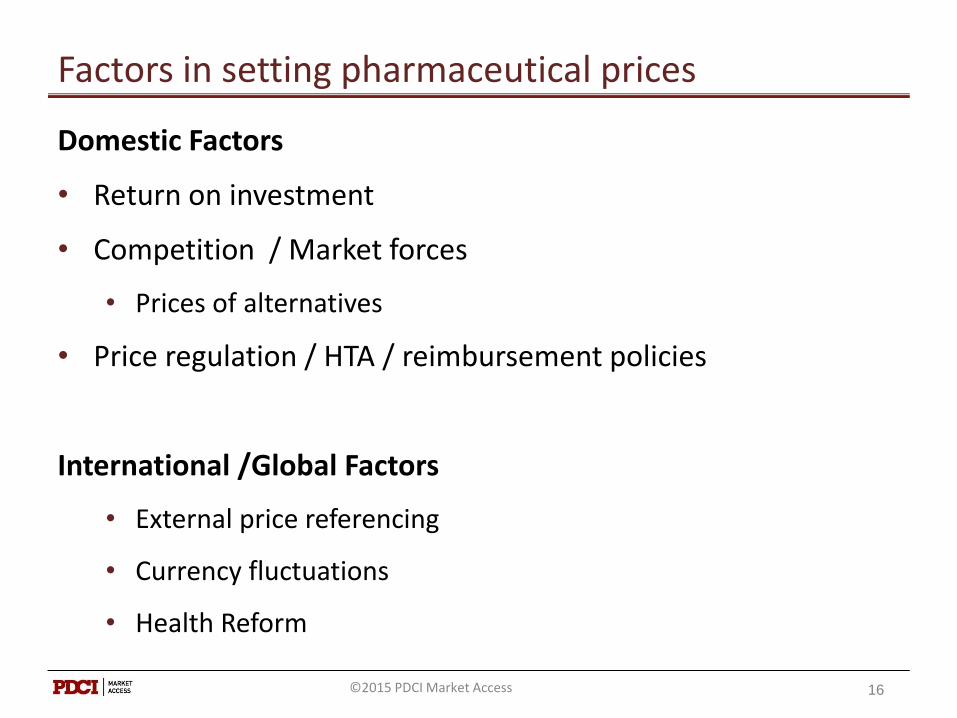

Factors in setting pharmaceutical prices

Domestic Factors

• Return on investment

• Competition / Market forces

• Prices of alternatives

• Price regulation / HTA / reimbursement policies

International /Global Factors

• External price referencing

• Currency fluctuations

• Health Reform

16©2015 PDCI Market Access

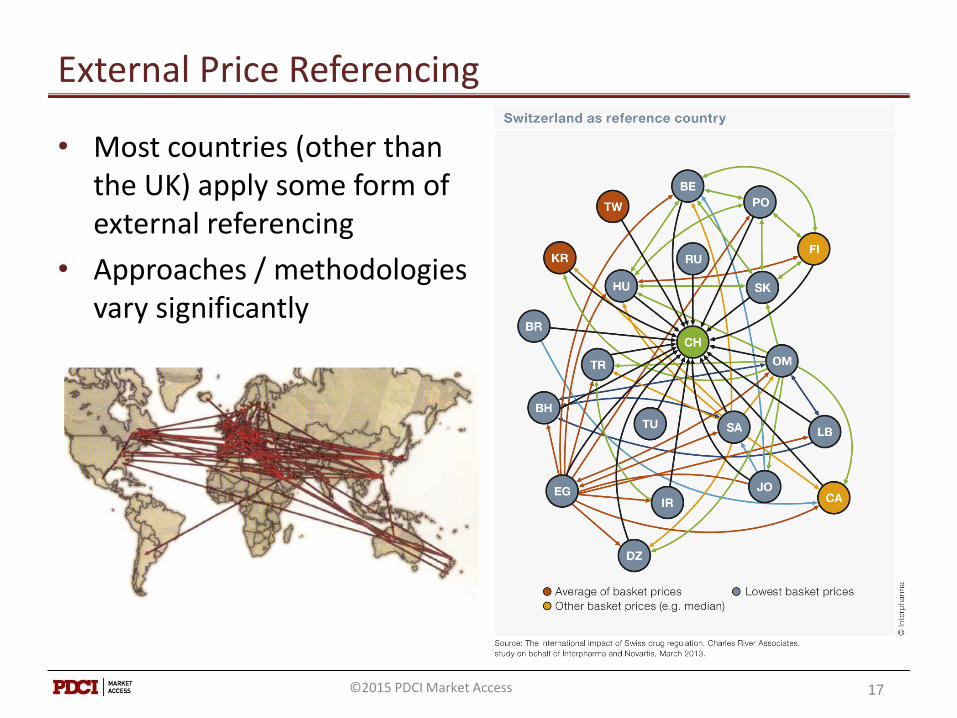

External Price Referencing

• Most countries (other than the UK) apply some form of external referencing

• Approaches / methodologies vary significantly

17©2015 PDCI Market Access

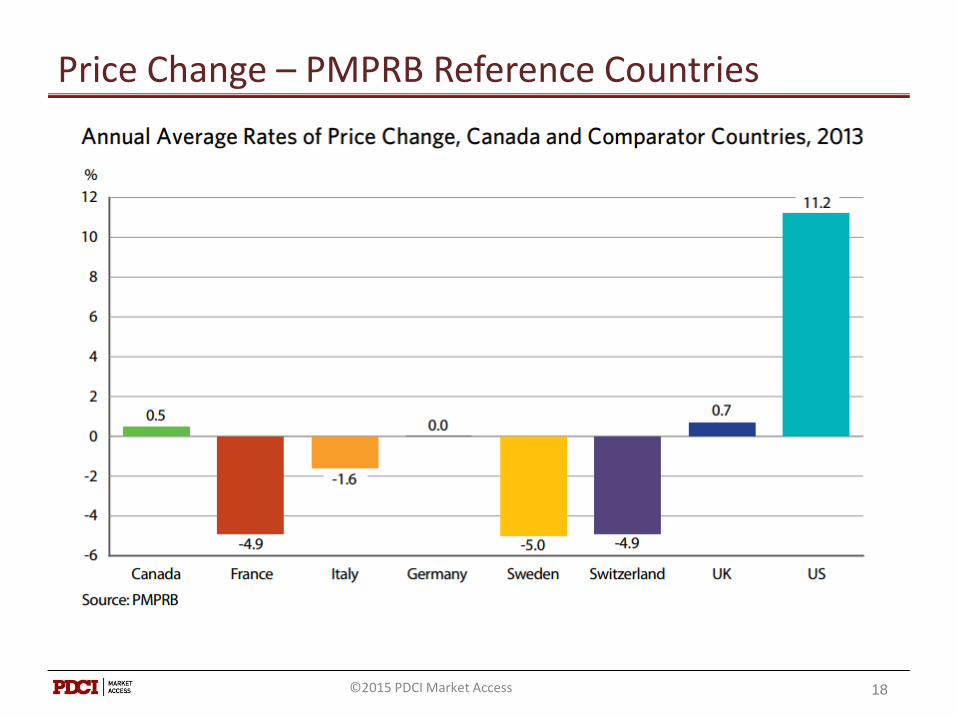

Price Change – PMPRB Reference Countries

18©2015 PDCI Market Access

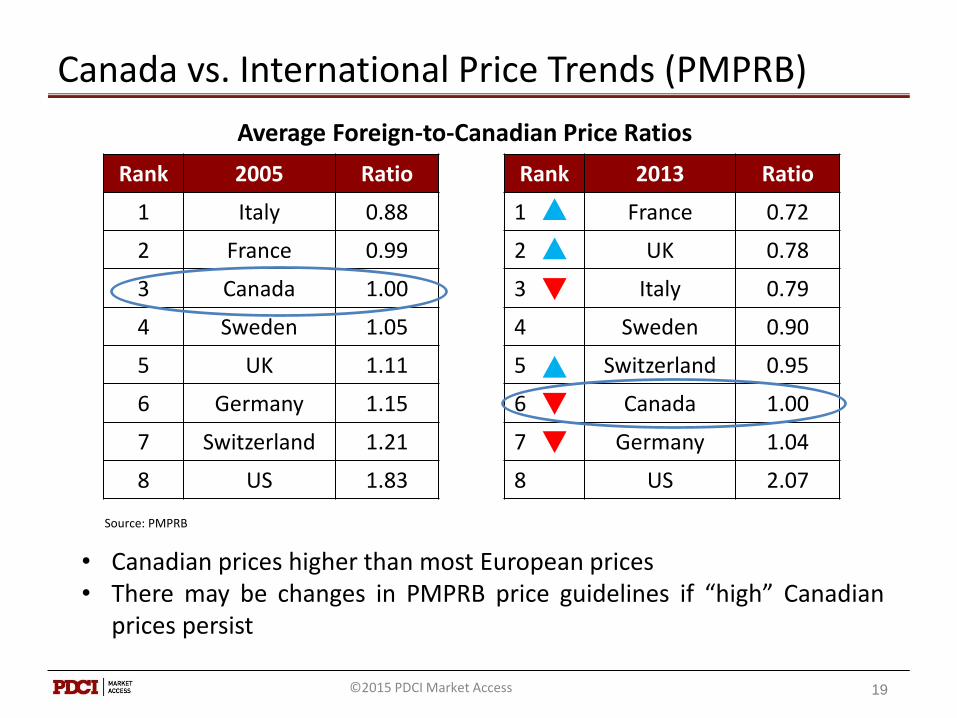

Canada vs. International Price Trends (PMPRB)

Rank 2005 Ratio

1 Italy 0.88

2 France 0.99

3 Canada 1.00

4 Sweden 1.05

5 UK 1.11

6 Germany 1.15

7 Switzerland 1.21

8 US 1.83

19

Rank 2013 Ratio

1 France 0.72

2 UK 0.78

3 Italy 0.79

4 Sweden 0.90

5 Switzerland 0.95

6 Canada 1.00

7 Germany 1.04

8 US 2.07

• Canadian prices higher than most European prices• There may be changes in PMPRB price guidelines if “high” Canadian

prices persist

Average Foreign-to-Canadian Price Ratios

Source: PMPRB

©2015 PDCI Market Access

Pricing & International Price Referencing

• Price increases are possible in the US, and to a limited extent in Canada but rarely in Europe and Japan

• Currency exchange fluctuations are beyond the control of manufacturer

• Price cuts are common in many European markets

• Reimbursement status is reviewed periodically in some markets which can lead to new price negotiations

• New health reform policies (e.g., Germany)

20©2015 PDCI Market Access

Cost Containment

21

Product Listing

Agreements

Pricing

Cost Containment

Trade

©2015 PDCI Market Access

Emerging Developments Related to Cost Containment

1. Delisting of Oncology Treatments

2. Off-Label Prescribing

3. Downgrading Coverage

4. Uptake of Biosimilars

5. Private Payer Exclusivity Arrangements

22©2015 PDCI Market Access

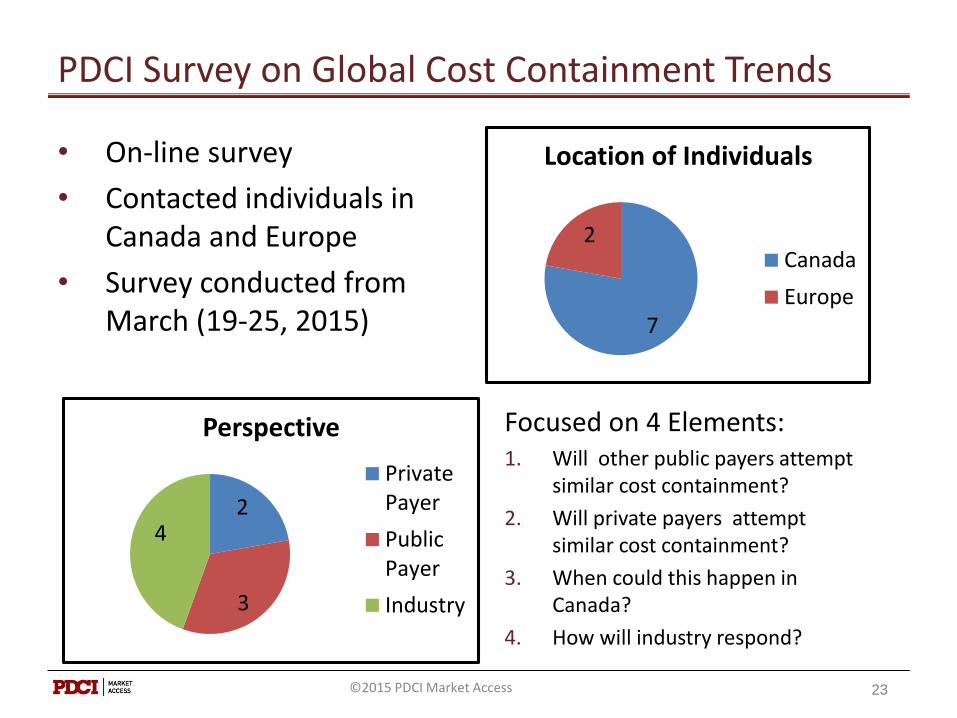

PDCI Survey on Global Cost Containment Trends

7

2

Location of Individuals

Canada

Europe

23

2

3

4

Perspective

PrivatePayer

PublicPayer

Industry

• On-line survey

• Contacted individuals in Canada and Europe

• Survey conducted from March (19-25, 2015)

Focused on 4 Elements:1. Will other public payers attempt

similar cost containment?

2. Will private payers attempt similar cost containment?

3. When could this happen in Canada?

4. How will industry respond?

©2015 PDCI Market Access

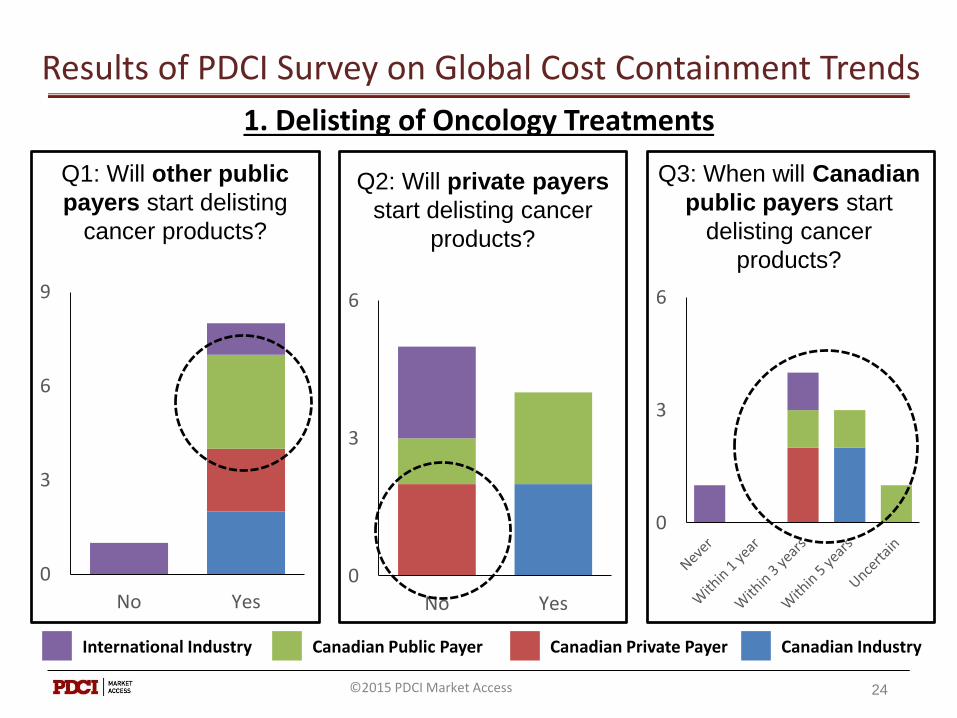

Results of PDCI Survey on Global Cost Containment Trends

24

1. Delisting of Oncology Treatments

International Industry Canadian Public Payer Canadian Private Payer Canadian Industry

Q1: Will other public

payers start delisting

cancer products?

0

3

6

9

No Yes

Q2: Will private payers

start delisting cancer

products?

0

3

6

No Yes

Q3: When will Canadian

public payers start

delisting cancer

products?

0

3

6

©2015 PDCI Market Access

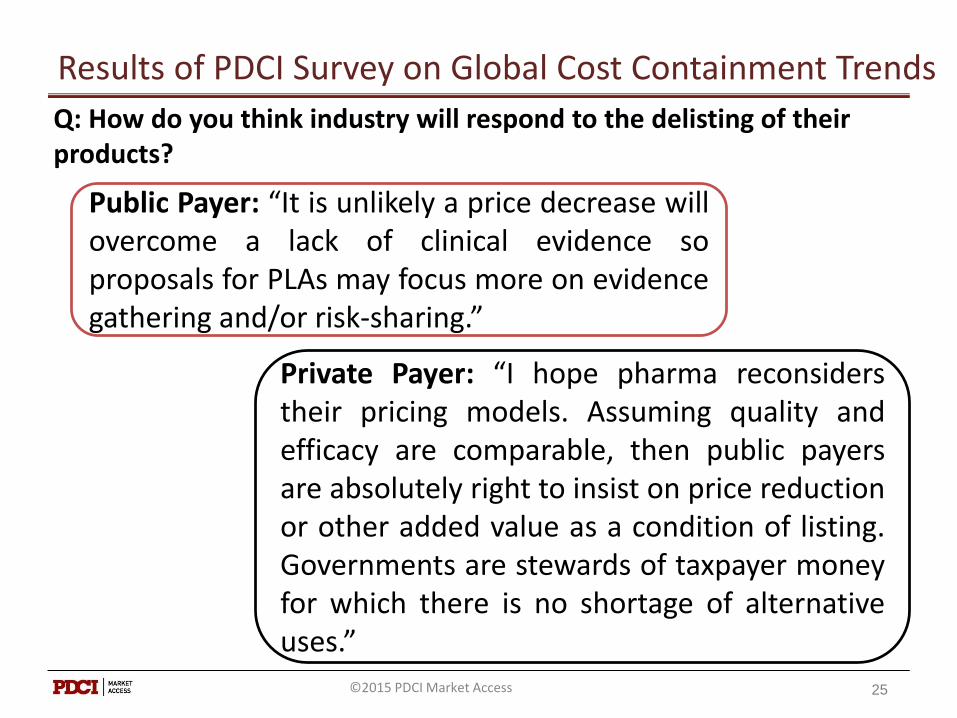

Results of PDCI Survey on Global Cost Containment Trends

25

Public Payer: “It is unlikely a price decrease willovercome a lack of clinical evidence soproposals for PLAs may focus more on evidencegathering and/or risk-sharing.”

Private Payer: “I hope pharma reconsiderstheir pricing models. Assuming quality andefficacy are comparable, then public payersare absolutely right to insist on price reductionor other added value as a condition of listing.Governments are stewards of taxpayer moneyfor which there is no shortage of alternativeuses.”

Q: How do you think industry will respond to the delisting of their products?

©2015 PDCI Market Access

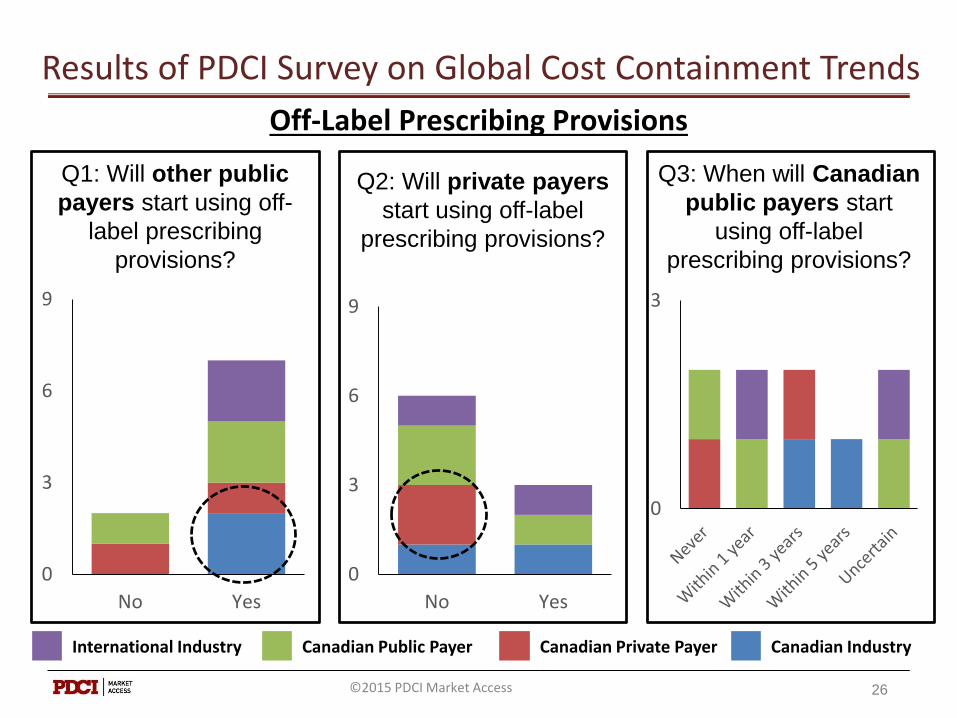

Results of PDCI Survey on Global Cost Containment Trends

26

Off-Label Prescribing Provisions

International Industry Canadian Public Payer Canadian Private Payer Canadian Industry

Q1: Will other public

payers start using off-

label prescribing

provisions?

0

3

6

9

No Yes

Q2: Will private payers

start using off-label

prescribing provisions?

0

3

6

9

No Yes

Q3: When will Canadian

public payers start

using off-label

prescribing provisions?

0

3

©2015 PDCI Market Access

Results of PDCI Survey on Global Cost Containment Trends

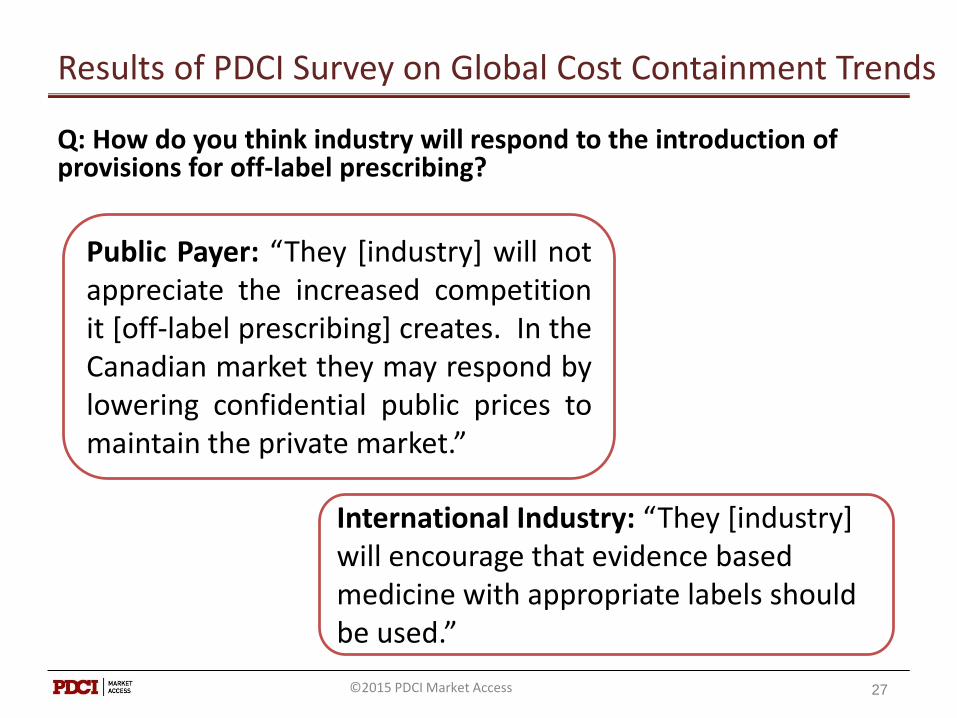

Q: How do you think industry will respond to the introduction of provisions for off-label prescribing?

27

Public Payer: “They [industry] will notappreciate the increased competitionit [off-label prescribing] creates. In theCanadian market they may respond bylowering confidential public prices tomaintain the private market.”

International Industry: “They [industry] will encourage that evidence based medicine with appropriate labels should be used.”

©2015 PDCI Market Access

Results of PDCI Survey on Global Cost Containment Trends

28

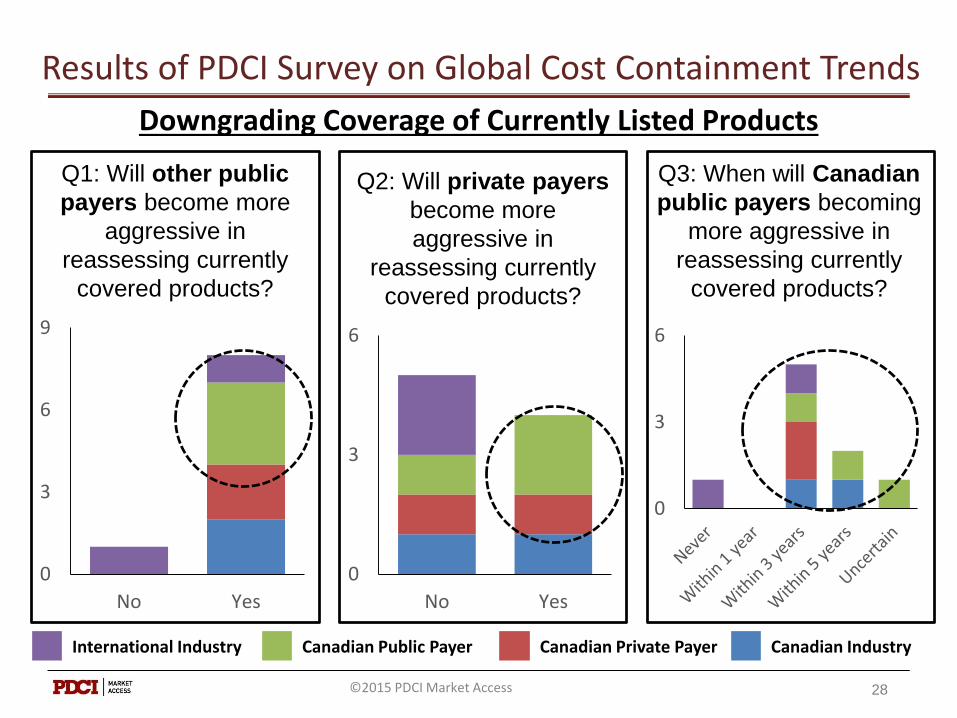

Downgrading Coverage of Currently Listed Products

International Industry Canadian Public Payer Canadian Private Payer Canadian Industry

Q1: Will other public

payers become more

aggressive in

reassessing currently

covered products?

0

3

6

9

No Yes

Q2: Will private payers

become more

aggressive in

reassessing currently

covered products?

0

3

6

No Yes

Q3: When will Canadian

public payers becoming

more aggressive in

reassessing currently

covered products?

0

3

6

©2015 PDCI Market Access

Results of PDCI Survey on Global Cost Containment Trends

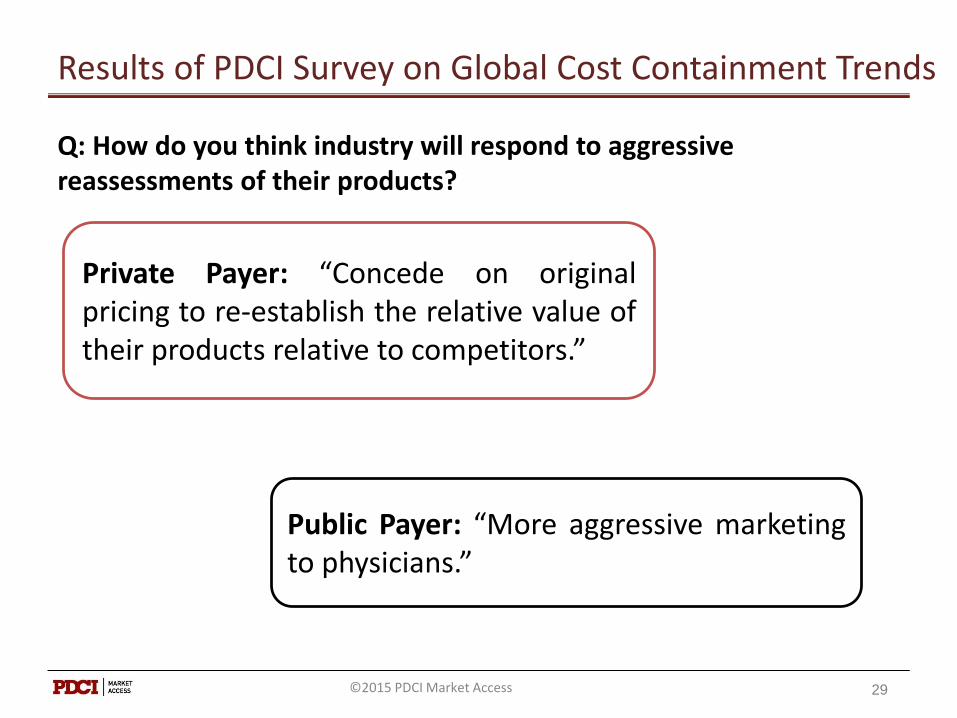

Q: How do you think industry will respond to aggressive reassessments of their products?

29

Private Payer: “Concede on originalpricing to re-establish the relative value oftheir products relative to competitors.”

Public Payer: “More aggressive marketingto physicians.”

©2015 PDCI Market Access

Results of PDCI Survey on Global Cost Containment Trends

30

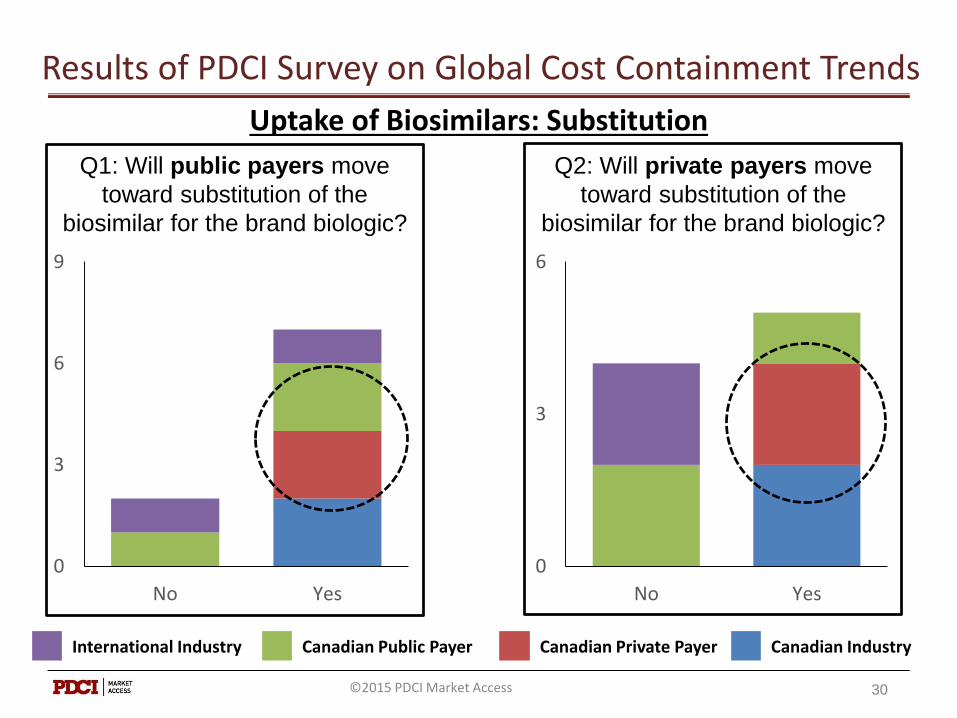

Uptake of Biosimilars: Substitution

International Industry Canadian Public Payer Canadian Private Payer Canadian Industry

Q1: Will public payers move

toward substitution of the

biosimilar for the brand biologic?

0

3

6

9

No Yes

Q2: Will private payers move

toward substitution of the

biosimilar for the brand biologic?

0

3

6

No Yes

©2015 PDCI Market Access

Results of PDCI Survey on Global Cost Containment Trends

31

Uptake of Biosimilars: Therapeutic Priorities

Rank the following biosimilar classes in terms of which will have the most

impact in driving payer adoption of biosimilar. 3 points = most impact; 2 points = medium impact; 1 point = least impact; 0 points = no impact

0

3

6

9

12

15

18

21

24

Rheumatoid Arthritis Diabetes Oncology

International Industry Canadian Public Payer Canadian Private Payer Canadian Industry

©2015 PDCI Market Access

Results of PDCI Survey on Global Cost Containment Trends

32

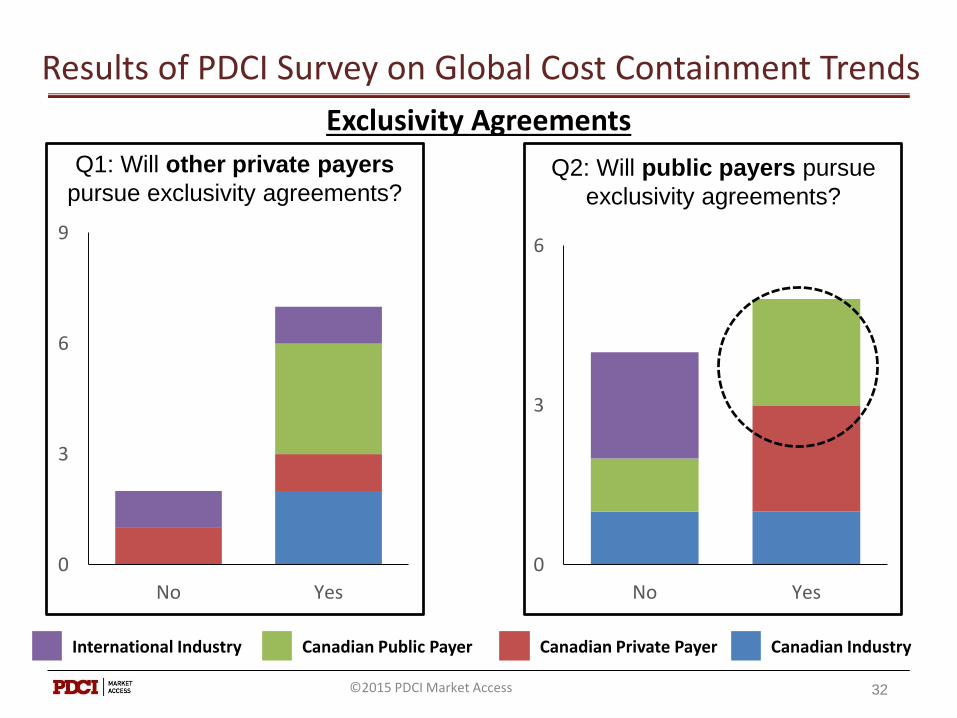

Exclusivity Agreements

Q2: Will public payers pursue

exclusivity agreements?

International Industry Canadian Public Payer Canadian Private Payer Canadian Industry

Q1: Will other private payers

pursue exclusivity agreements?

0

3

6

9

No Yes

0

3

6

No Yes

©2015 PDCI Market Access

Results of PDCI Survey on Global Cost Containment Trends

Q: How do you think industry will respond if private payers start to pursue more exclusivity agreements?

33

Public Payer: “Much the same way as they did to public payers -PLAs, risk-shares and evidence-gathering.”

Private Payer: “More aggressive marketing push direct to members via patient assistance programs, financial assistance”

Public Payer: “The market will become more of an all or nothing for manufacturers. For the aggressive manufacturers there is a chance to get a greater market share. But overall manufacturers will not like this because it ultimately will drive down their profit margin per unit.”

Canadian Industry: “More aggressive PLAs. As we saw years back with PPIs, there will always be a company that is willing to push negotiations for exclusivity”

©2015 PDCI Market Access

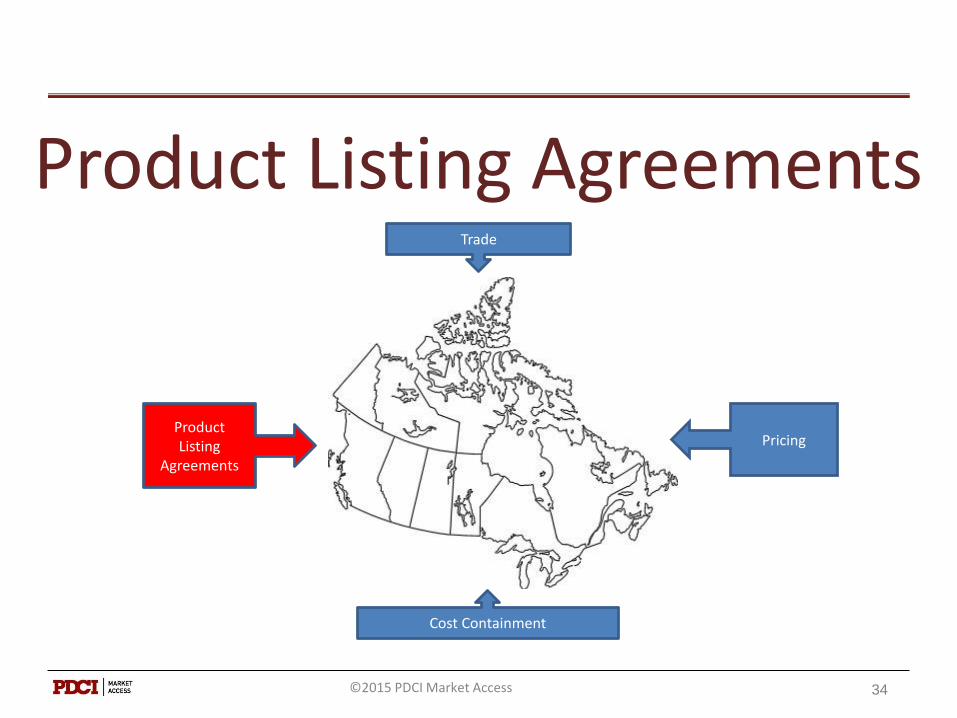

Product Listing Agreements

34

Product Listing

Agreements

Pricing

Cost Containment

Trade

©2015 PDCI Market Access

Product Listing Agreements

35

The Performance Based Risk Sharing (PBRS) web-enabled database was developed by the Pharmaceutical Outcomes Research & Policy Program at the University of Washington https://depts.washington.edu/pbrs/index.php

©2015 PDCI Market Access

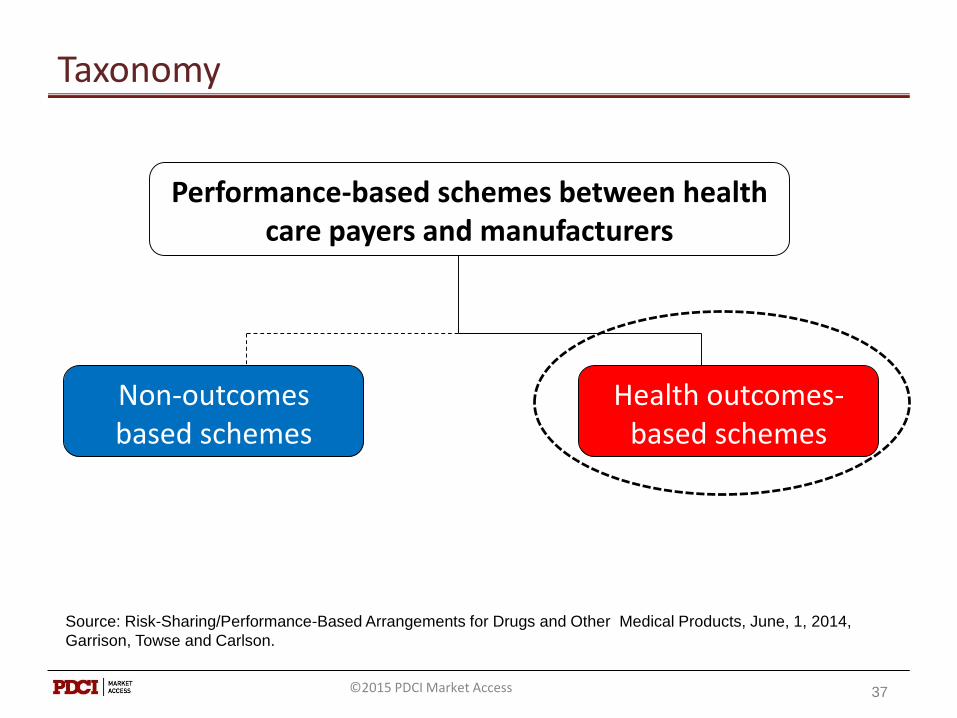

PBRSA - Defined

“Performance-based risk-sharing arrangements (PBRSAs)—involve a plan by which the performance

of the product is tracked in a defined patient population over a specified period of time and the amount or level of reimbursement is based on the

health and cost outcomes achieved.”

36

Source: Risk-Sharing/Performance-Based Arrangements for Drugs and Other Medical Products, June, 1, 2014,

Garrison, Towse and Carlson.

©2015 PDCI Market Access

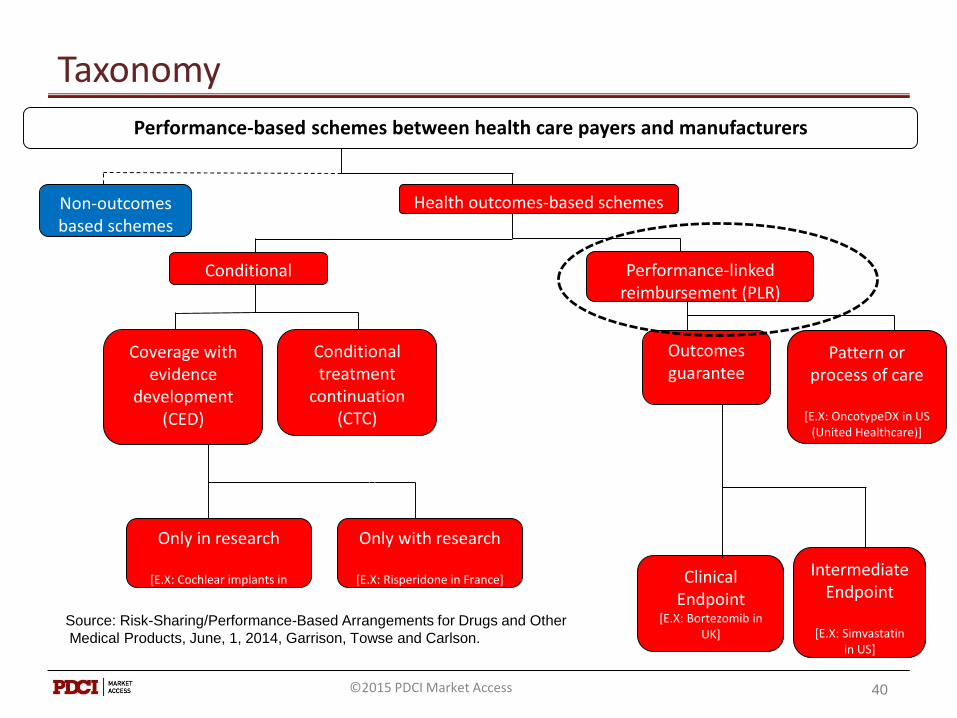

Taxonomy

37

Health outcomes-based schemes

Non-outcomes based schemes

Performance-based schemes between health care payers and manufacturers

Source: Risk-Sharing/Performance-Based Arrangements for Drugs and Other Medical Products, June, 1, 2014,

Garrison, Towse and Carlson.

©2015 PDCI Market Access

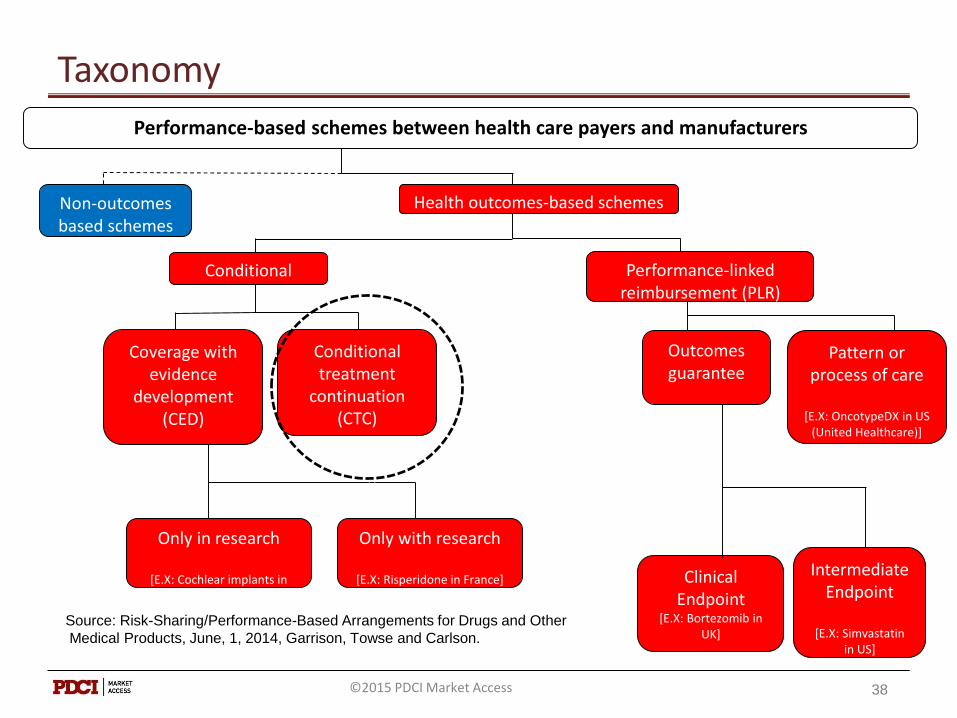

Taxonomy

Outcomes guarantee

Clinical Endpoint

[E.X: Bortezomib in UK]

Intermediate Endpoint

[E.X: Simvastatinin US]

Performance-based schemes between health care payers and manufacturers

Health outcomes-based schemesNon-outcomes based schemes

Performance-linked reimbursement (PLR)

Pattern or process of care

[E.X: OncotypeDX in US (United Healthcare)]

Only in research

[E.X: Cochlear implants in US(CMS)]

Only with research

[E.X: Risperidone in France]

Coverage with evidence

development (CED)

Conditional coverage

Conditional treatment

continuation (CTC)

[E.X: Alzheimer’s drugs in Italy]

38

Source: Risk-Sharing/Performance-Based Arrangements for Drugs and Other

Medical Products, June, 1, 2014, Garrison, Towse and Carlson.

©2015 PDCI Market Access

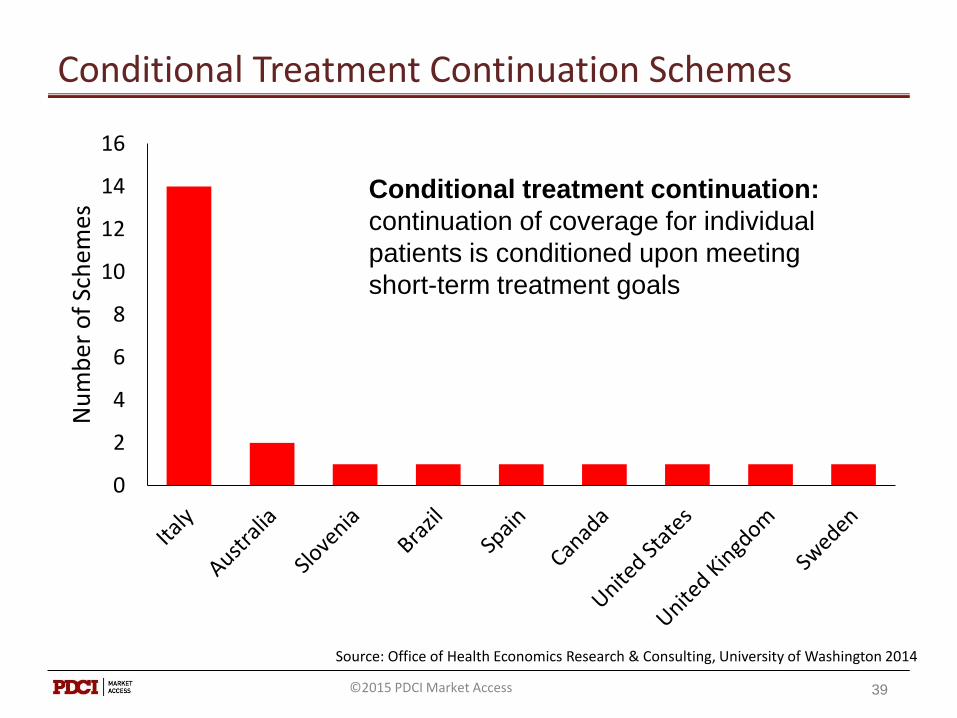

Conditional Treatment Continuation Schemes

0

2

4

6

8

10

12

14

16

Nu

mb

er o

f Sc

hem

es

39

Source: Office of Health Economics Research & Consulting, University of Washington 2014

Conditional treatment continuation:

continuation of coverage for individual

patients is conditioned upon meeting

short-term treatment goals

©2015 PDCI Market Access

Taxonomy

Outcomes guarantee

Clinical Endpoint

[E.X: Bortezomib in UK]

Intermediate Endpoint

[E.X: Simvastatinin US]

Performance-based schemes between health care payers and manufacturers

Health outcomes-based schemesNon-outcomes based schemes

Performance-linked reimbursement (PLR)

Pattern or process of care

[E.X: OncotypeDX in US (United Healthcare)]

Only in research

[E.X: Cochlear implants in US(CMS)]

Only with research

[E.X: Risperidone in France]

Coverage with evidence

development (CED)

Conditional coverage

Conditional treatment

continuation (CTC)

[E.X: Alzheimer’s drugs in Italy]

40

Source: Risk-Sharing/Performance-Based Arrangements for Drugs and Other

Medical Products, June, 1, 2014, Garrison, Towse and Carlson.

©2015 PDCI Market Access

Performance-Linked Reimbursement Schemes

0

5

10

15

20

25

30

Nu

mb

er o

f Sc

hem

es

41

Source: Office of Health Economics Research & Consulting, University of Washington 2014

Performance-linked reimbursement:

reimbursement level for covered

products is tied, by formula, to the

measure of clinical outcomes in the

“real world”

©2015 PDCI Market Access

Taxonomy

42

Health outcomes-based schemes

Non-outcomes based schemes

Performance-based schemes between health care payers and manufacturers

Source: Risk-Sharing/Performance-Based Arrangements for Drugs and Other Medical Products, June, 1, 2014,

Garrison, Towse and Carlson.

©2015 PDCI Market Access

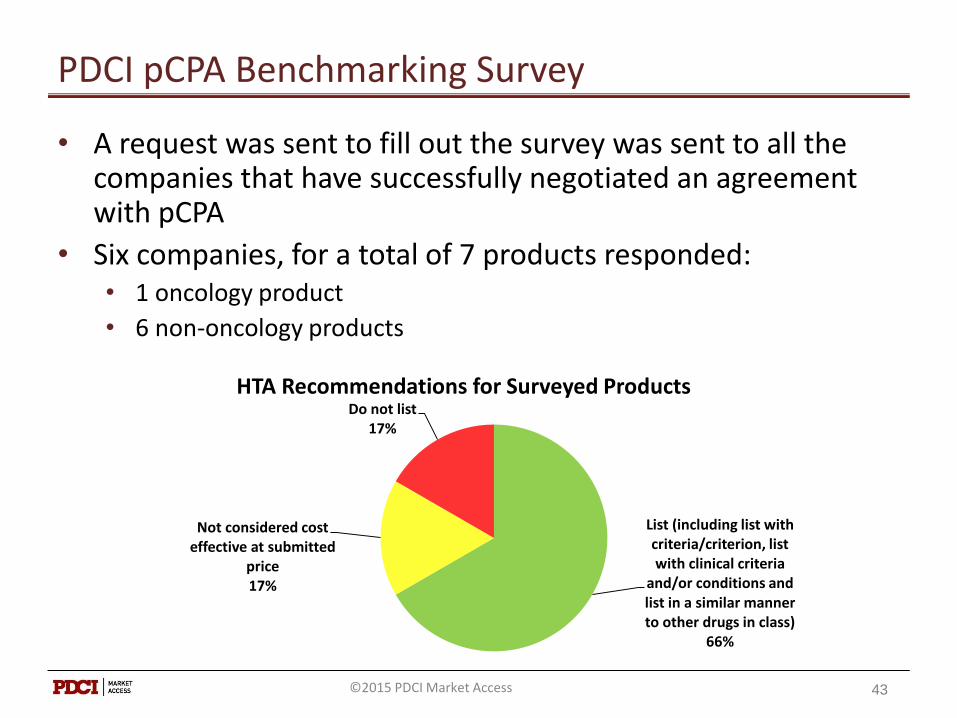

PDCI pCPA Benchmarking Survey

• A request was sent to fill out the survey was sent to all the companies that have successfully negotiated an agreement with pCPA

• Six companies, for a total of 7 products responded: • 1 oncology product

• 6 non-oncology products

List (including list with criteria/criterion, list with clinical criteria

and/or conditions and list in a similar manner to other drugs in class)

66%

Not considered cost effective at submitted

price17%

Do not list17%

HTA Recommendations for Surveyed Products

43©2015 PDCI Market Access

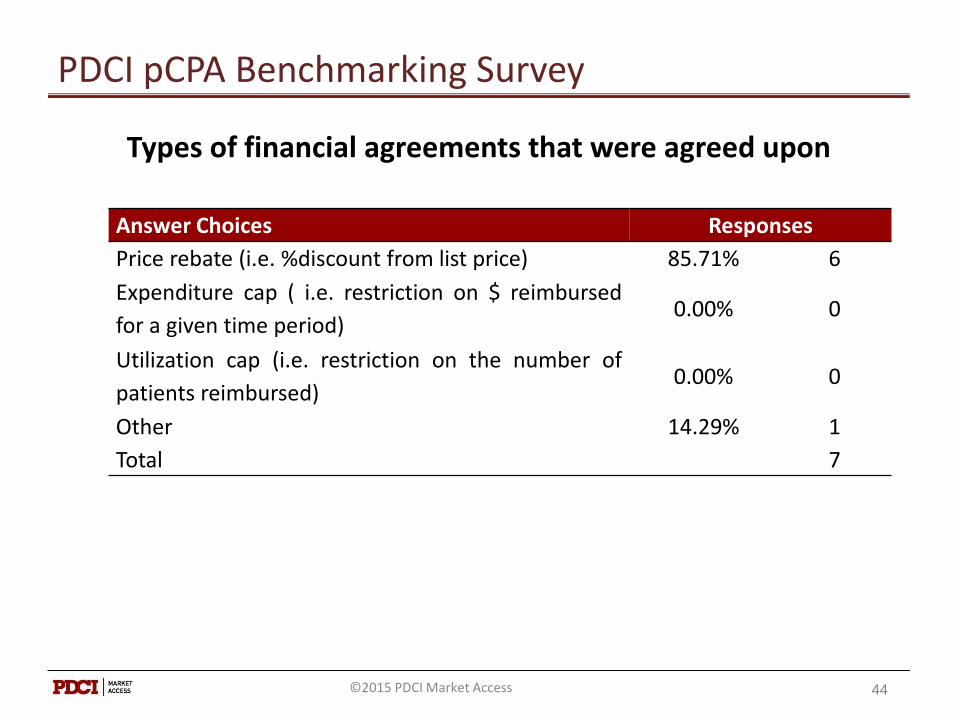

PDCI pCPA Benchmarking Survey

Types of financial agreements that were agreed upon

Answer Choices Responses

Price rebate (i.e. %discount from list price) 85.71% 6

Expenditure cap ( i.e. restriction on $ reimbursed

for a given time period)0.00% 0

Utilization cap (i.e. restriction on the number of

patients reimbursed)0.00% 0

Other 14.29% 1

Total 7

44©2015 PDCI Market Access

45

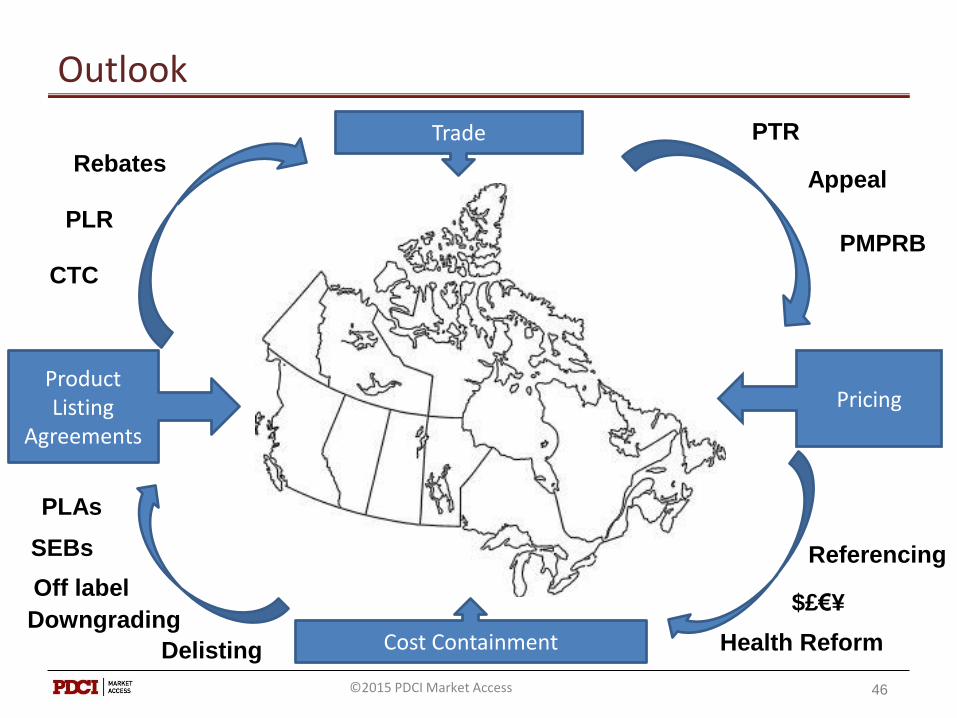

Outlook

©2015 PDCI Market Access

46

Outlook

Product Listing

Agreements

Pricing

Cost Containment

Trade PTR

Appeal

PMPRB

$£€¥

Referencing

Health ReformDelisting

Downgrading

Off label

PLAs

SEBs

Rebates

CTC

PLR

©2015 PDCI Market Access

47©2015 PDCI Market Access

Biography

Arvind ManiDirector, Market Access and Policy Research

PDCI Market Access Inc

www.pdci.ca

Arvind Mani is the Director of Market Access and Policy Research at PDCI. Arvind leads a team of consultants onpharmaceutical reimbursement (budget impact analyses), policy, and patent litigation projects. Arvind has morethan 15 years of experience working in industry, associations and consulting. He provides expert knowledge tocompanies, governments on pharmaceutical pricing, regulatory, market access, and patent issues and is alsoresponsible for contributing to pricing and reimbursement policy and analysis projects. Before joining PDCI,Arvind spent several years as the Director of Corporate Affairs at the National Association of Pharmacy RegulatoryAuthorities (NAPRA) in Ottawa. Prior to NAPRA, he worked for 8 years at Canada’s Research-BasedPharmaceutical Companies (Rx&D), an association that represents the interests of innovative pharmaceuticalcompanies in Canada. Arvind held various positions at Rx&D, including Research Analyst, Director of RegulatoryAffairs, and Director of Policy Development. Prior to joining Rx&D, Arvind was a Market Analyst with Ciba Geigy(now Novartis Pharmaceuticals Canada Inc.).

PDCI Market Access (PDCI) is a leading pharmaceutical pricing and reimbursement (P&R) consultancy based inOttawa and Toronto. Established in 1996, the firm features a senior team of multi-lingual market accessprofessionals with extensive experience assisting clients navigate the complex P&R challenges facing Canadianpharmaceutical manufacturers. PDCI develops successful P&R strategies and prepares comprehensivesubmissions to CDR, pCODR, public & private payers and the PMPRB. The firm’s senior consultants facilitatemeetings with CDR/payers/PMPRB, negotiate product listing agreements (PLAs) and resolve pricing complianceissues with the PMPRB. PDCI maintains databases of international pharmaceutical prices and provincial drugclaims and costs.

48©2015 PDCI Market Access