Canadian Hydrogen and Fuel Cell Sector Profile 2012 WEB 2389-01 CHFC Sector Profile... ·...

20

Canadian Hydrogen and Fuel Cell Sector Profile 2012

Transcript of Canadian Hydrogen and Fuel Cell Sector Profile 2012 WEB 2389-01 CHFC Sector Profile... ·...

Canadian Hydrogen and Fuel Cell

Sector Profile 2012

ii

Since 2004, the Government of Canada, the Canadian Hydrogen and Fuel Cell Association (CHFCA) and PricewaterhouseCoopers LLP (PwC) have collaborated to provide an extensive profile of the Canadian hydrogen and fuel cell sector. The 2012 Sector Profile follows a similar format to the previous eight editions and provides industry insight on Canada’s hydrogen and fuel cell sector for policy makers, investors and other stakeholders. The research adds value to business strategies, investment decisions, and the overall expertise across our country.

The Profile is published annually to monitor trends and recognize growth and achievements for this key influence of the Canadian economy. We would like to thank all the organizations that contributed to the development of the Canadian Hydrogen and Fuel Cell Sector Profile 2012.

Canadian Hydrogen and Fuel Cell Sector Profile 2012

For a print copy of this publication, please contact:

Publishing and Depository Services Public Works and Government Services Canada Ottawa ON K1A 0S5

Tel. (toll-free): 1-800-635-7943 (Canada and U.S.) Tel. (local): 613-941-5995 TTY: 1-800-465-7735 Fax (toll-free): 1-800-565-7757 (Canada and U.S.) Fax (local): 613-954-5779 Email: [email protected] Website: www.publications.gc.ca

This publication is available upon request in accessible formats. Contact:

Multimedia Services Section Communications and Marketing Branch Industry Canada Room 264D, West Tower 235 Queen Street Ottawa ON K1A 0H5

Tel.: 613-948-1554 Fax: 613-947-7155 Email: [email protected]

This publication is also available electronically on the World Wide Web in HTML format at the following address: www.ic.gc.ca

Permission to Reproduce

Except as otherwise specifically noted, the information in this publication may be reproduced, in part or in whole and by any means, without charge or further permission from Industry Canada, provided that due diligence is exercised in ensuring the accuracy of the information reproduced; that Industry Canada is identified as the source institution; and that the reproduction is not represented as an official version of the information reproduced, nor as having been made in affiliation with, or with the endorsement of, Industry Canada.

For permission to reproduce the information in this publication for commercial redistribution, please email: [email protected]

Cat. No. Iu41-3/2011E - PDF

Aussi offert en français sous le titre Profil de l’industrie canadienne de l’hydrogène et des piles à combustible 2012.

Printed in Canada on paper made from 30% post consumer fibre.

1

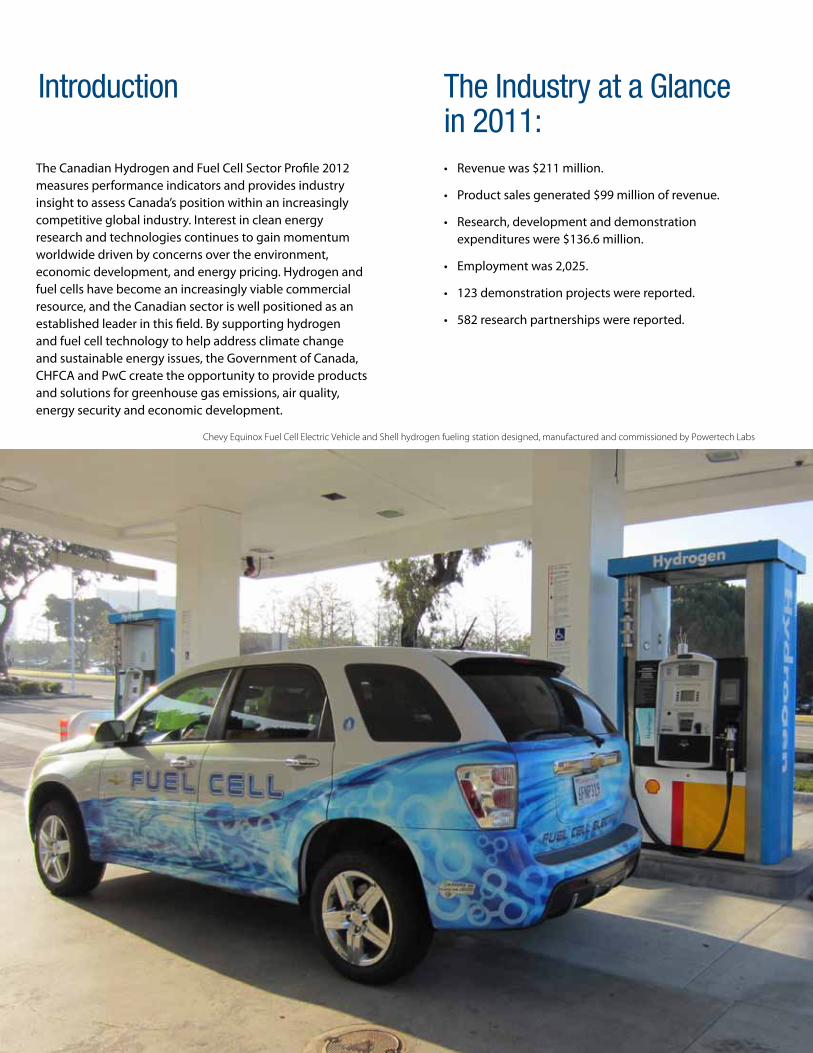

The Canadian Hydrogen and Fuel Cell Sector Profile 2012 measures performance indicators and provides industry insight to assess Canada’s position within an increasingly competitive global industry. Interest in clean energy research and technologies continues to gain momentum worldwide driven by concerns over the environment, economic development, and energy pricing. Hydrogen and fuel cells have become an increasingly viable commercial resource, and the Canadian sector is well positioned as an established leader in this field. By supporting hydrogen and fuel cell technology to help address climate change and sustainable energy issues, the Government of Canada, CHFCA and PwC create the opportunity to provide products and solutions for greenhouse gas emissions, air quality, energy security and economic development.

Introduction The Industry at a Glance in 2011:• Revenuewas$211million.

• Productsalesgenerated$99millionofrevenue.

• Research,developmentanddemonstrationexpenditureswere$136.6million.

• Employmentwas2,025.

• 123demonstrationprojectswerereported.

• 582researchpartnershipswerereported.

Mercedes-Benz F-Cell fuel cell electric vehicle

Chevy Equinox Fuel Cell Electric Vehicle and Shell hydrogen fueling station designed, manufactured and commissioned by Powertech Labs

2

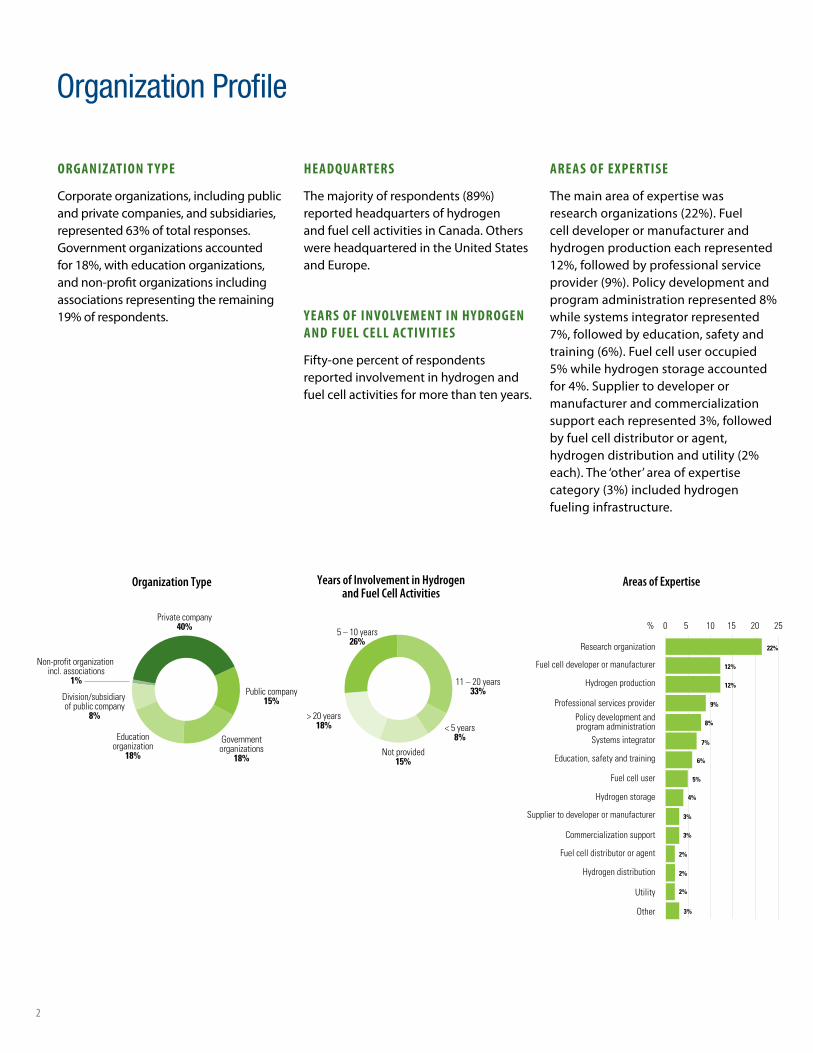

ORganiz atiOn t yPe

Corporate organizations, including public and private companies, and subsidiaries, represented63%oftotalresponses.Government organizations accounted for18%,witheducationorganizations,and non-profit organizations including associations representing the remaining 19%ofrespondents.

HeadquaRteRs

Themajorityofrespondents(89%)reported headquarters of hydrogen and fuel cell activities in Canada. Others were headquartered in the United States and Europe.

yeaRs Of invOlvement in HydROgen and fuel Cell aC tivities

Fifty-one percent of respondents reported involvement in hydrogen and fuel cell activities for more than ten years.

aReas Of exPeRtise

The main area of expertise was researchorganizations(22%).Fuelcell developer or manufacturer and hydrogen production each represented 12%,followedbyprofessionalserviceprovider(9%).Policydevelopmentandprogramadministrationrepresented8%while systems integrator represented 7%,followedbyeducation,safetyandtraining(6%).Fuelcelluseroccupied5%whilehydrogenstorageaccountedfor4%.Suppliertodeveloperormanufacturer and commercialization supporteachrepresented3%,followedby fuel cell distributor or agent, hydrogendistributionandutility(2%each). The ‘other’ area of expertise category(3%)includedhydrogenfueling infrastructure.

Organization Profile

Organization Type

Private company40%

Public company15%Division/subsidiary

of public company8%

Governmentorganizations

18%

Educationorganization

18%

Non-profit organization incl. associations

1%

p. 2 Organization Type

Apr 2012

Not provided15%

> 20 years18%

11 – 20 years33%

5 – 10 years26%

< 5 years8%

p.2 Years of Involvement in Hydrogen and Fuel Cell Activities

Mobile –Auxiliary Power

5%

Mobile – Primary Power and Drivetrain

24%

Portable(including

micro)11%

Small Stationary 50kW or less

19%

Large Stationary > 50kW

14%HydrogenProduction

and Fueling Infrastructure

27%

p.3 Market Focus

Rest of World7%

Rest of Canada15%

Ontario18%

Quebec9%

Alberta6%

British Columbia22%

USA8%

p.3 Hydrogen and Fuel Cell Facilities by Region

Provision of services

37%

Product sales59%

Canadian government supportrecognized as revenue

1%

p.4 Revenue by Category

Small Stationary50kW or less

14%LargeStationary

> 50kW2%

Mobile –Primary

Power andDrivetrain

13%

Mobile – Auxiliary Power

21%

FuelingInfrastructure

50%

p.7 Focus of Demonstration Projects

Rest of Canada 4%USA5%

Quebec9%

Asia2%

Rest of Europe 6%

British Columbia58%

Ontario13%

p.8 Employment by Region

Government9%

Academia andnon-profit

15%

Corporate76%

p.8 Employment by Organization

Remain the same (+/-5%)

52%

Significant increase(greater than 15%

of current employees)17%

Increase(between 5%

and 15%)23%

p.11 Plans to change employment in the next 18 months

Government13%

Private equity19%

Other10%

Angel Investors4%

Operations52%

p.9 Sources of Funding - Corporate

A-Base15%

Programs85%

p.9 Sources of Funding - Government

Other non-profitorganization

37%

NSERC/Canadian Foundation for Innovation

13%

Other 50%

p.9 Sources of Funding – Academia and Non-Profit

Other OEM13%

Public-privatepartnerships

26%

Hydrogen andfuel cell companies

26%

EnergyProviders

11%

Other 7%

p.10 Strategic Alliances

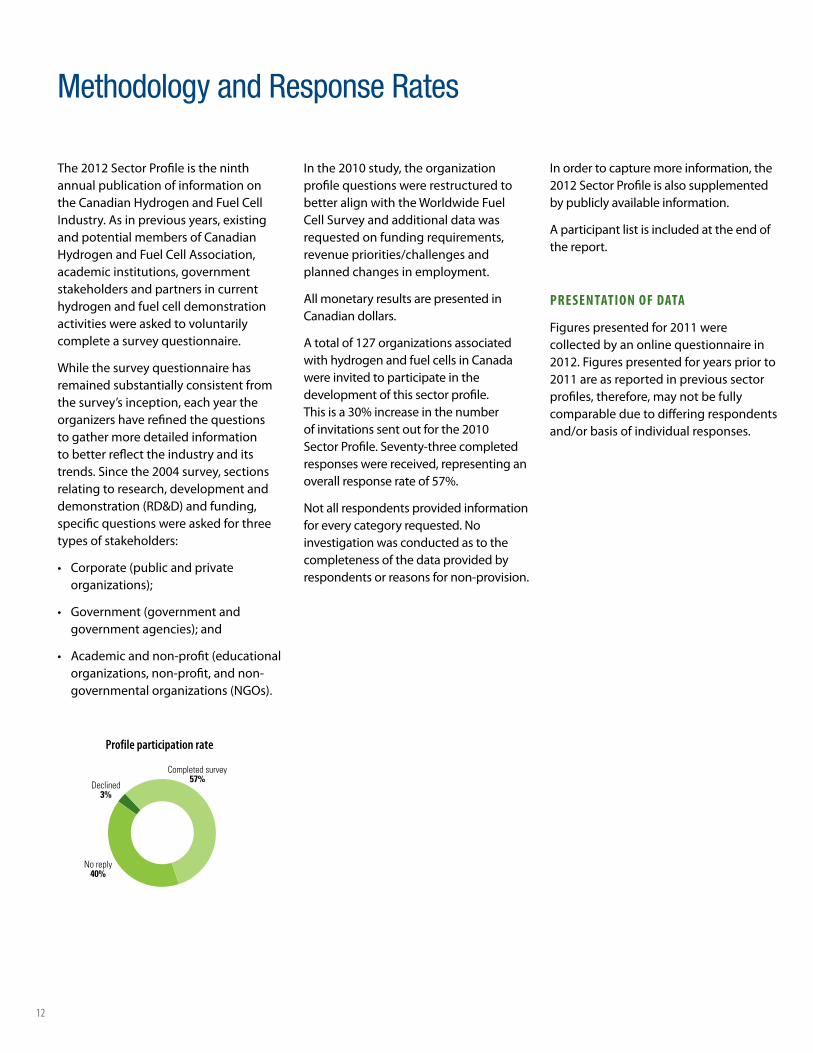

Declined3%

No reply40%

Completed survey57%

p.10 Profile participation rate

Technicians2%

Academic/research staff

26%

Undergraduatestudents

including coop13%

Canadian graduate andpostgraduate students

46%

International graduate andpostgraduate students

13%

p.6 People Involved in Research

USA25%Germany

30%

Asia 4%

Rest of world 5%

BritishColumbia

27%Ontario 1%

Rest of Canada1%Rest of

Europe7%

p.6 R&D by region

British Columbia77%

Rest of the world5%

Ontario10%

Quebec 3%Germany 3%

USA 1%

p.4 Revenue by Region

R&DIn-house

48%

p.9 Funding Allocation by Area - Gov’t & Academia & Non-profit

R&DIntramural

35%

Marketing andbusiness development

1%Education,

safety and training5%

Policy development1%

Monitoringand reporting

1%

Demonstrationand pilot projects

9%

Europe11%

Other 3%

Germany 3%

Significantly decrease (greater than 15%)

3%Decrease

(between 5 and 15%)5%

Japan 1%

Japan4%

Automotive OEM17%

Public capital markets2%

Years of Involvement in Hydrogen and Fuel Cell Activities

Private company40%

Public company15%Division/subsidiary

of public company8%

Governmentorganizations

18%

Educationorganization

18%

Non-profit organization incl. associations

1%

p. 2 Organization Type

Apr 2012

Not provided15%

> 20 years18%

11 – 20 years33%

5 – 10 years26%

< 5 years8%

p.2 Years of Involvement in Hydrogen and Fuel Cell Activities

Mobile –Auxiliary Power

5%

Mobile – Primary Power and Drivetrain

24%

Portable(including

micro)11%

Small Stationary 50kW or less

19%

Large Stationary > 50kW

14%HydrogenProduction

and Fueling Infrastructure

27%

p.3 Market Focus

Rest of World7%

Rest of Canada15%

Ontario18%

Quebec9%

Alberta6%

British Columbia22%

USA8%

p.3 Hydrogen and Fuel Cell Facilities by Region

Provision of services

37%

Product sales59%

Canadian government supportrecognized as revenue

1%

p.4 Revenue by Category

Small Stationary50kW or less

14%LargeStationary

> 50kW2%

Mobile –Primary

Power andDrivetrain

13%

Mobile – Auxiliary Power

21%

FuelingInfrastructure

50%

p.7 Focus of Demonstration Projects

Rest of Canada 4%USA5%

Quebec9%

Asia2%

Rest of Europe 6%

British Columbia58%

Ontario13%

p.8 Employment by Region

Government9%

Academia andnon-profit

15%

Corporate76%

p.8 Employment by Organization

Remain the same (+/-5%)

52%

Significant increase(greater than 15%

of current employees)17%

Increase(between 5%

and 15%)23%

p.11 Plans to change employment in the next 18 months

Government13%

Private equity19%

Other10%

Angel Investors4%

Operations52%

p.9 Sources of Funding - Corporate

A-Base15%

Programs85%

p.9 Sources of Funding - Government

Other non-profitorganization

37%

NSERC/Canadian Foundation for Innovation

13%

Other 50%

p.9 Sources of Funding – Academia and Non-Profit

Other OEM13%

Public-privatepartnerships

26%

Hydrogen andfuel cell companies

26%

EnergyProviders

11%

Other 7%

p.10 Strategic Alliances

Declined3%

No reply40%

Completed survey57%

p.10 Profile participation rate

Technicians2%

Academic/research staff

26%

Undergraduatestudents

including coop13%

Canadian graduate andpostgraduate students

46%

International graduate andpostgraduate students

13%

p.6 People Involved in Research

USA25%Germany

30%

Asia 4%

Rest of world 5%

BritishColumbia

27%Ontario 1%

Rest of Canada1%Rest of

Europe7%

p.6 R&D by region

British Columbia77%

Rest of the world5%

Ontario10%

Quebec 3%Germany 3%

USA 1%

p.4 Revenue by Region

R&DIn-house

48%

p.9 Funding Allocation by Area - Gov’t & Academia & Non-profit

R&DIntramural

35%

Marketing andbusiness development

1%Education,

safety and training5%

Policy development1%

Monitoringand reporting

1%

Demonstrationand pilot projects

9%

Europe11%

Other 3%

Germany 3%

Significantly decrease (greater than 15%)

3%Decrease

(between 5 and 15%)5%

Japan 1%

Japan4%

Automotive OEM17%

Public capital markets2%

Areas of Expertise

Access to markets

Lack of funding

Technology development

p.2 Areas of Expertise

p.3 Technology Focus

p.4 Total Revenue ($ millions)

Hydrogen production

Research organization

Policy development andprogram administration

Fuel cell user

Professional services provider

Hydrogen distribution

Fuel cell developer or manufacturer

5 10 15 20 250

Other

Systems integrator

Education, safety and training

Commercialization support

Supplier to developer or manufacturer

Hydrogen storage

Fuel cell distributor or agent

22%

12%

12%

9%

8%

7%

6%

5%

4%

3%

3%

2%

2%

3%

0 5 10 15 20 25 30 35 40 45

Proton Exchange Membrane

Solid Oxide Fuel Cells

Hydrogen Production

Hydrogen Distribution

Hydrogen Storage

Metal-Air

Molten Carbonate

Direct Liquid

Other

1%

7%

7%

37%

8%

2%

2%

14%

20%

0

50

100

150

200

250

2008

p.8 Employment

28. Growth since 2001

1,500

1,000

0

2,500

2006

2007 20092006

2007 2008 2010

0

50

100

150

200

250

300

2005 2006 2007 201020042003200220010

500

1,000

1,500

2,000

2,500

3,000

R&DRevenue Employees

$

p.7 Patents

200

100

0

300

400

235

351

Alberta

Canadian government (all levels)

Corporate operations

Parent, affiliatedor subsidiary

Research, non-profit,non-governmental institute

Contract work conductedfor another institute

0 20 40 60 80 100

12. Sources of Funding for R&D Expenditure by Organization

23%

68%

7%

7%

9%

Foreign government

University oracademic institute

1%

3%

14%

0% 20% 40% 60% 80% 100%

100%61%

GovernmentCorporate Academic and non-profit

290

179

134

276

188

97

133 135 133

177

128

2011

215

142

Feb 2011

Patentsapproved

Patentspending

p.11 Priorities to enhance competitive performance in 2012

0 5 10 15 20 25

Collaboration/strategic alliances

Gain market share

Better targetingof customers

Improving processes

Better marketor customer data

Plans for expansion(new products/new markets)

Other

Outsourcing

8%

1%

8%

21%

8%

Reduce costof operations

7%

6%

19%

12%

10%

p.? challenges faced in 2010

0% 5 10 15 20 25 30

Profitability

Economy

Exchange rates

6%

31%

6%

Other 9%

24%

10%

10%

GermanyUSA

British ColumbiaQuebecOntario

0 5 10 15 20 25 30 35 40 45 50 55 60

16. Demonstration Projects by Region (Number of Projects)

51

Other

GovernmentCorporate Academia and non-profit

%

%

%

Millions Employees

Utility 2%

Direct Methanol 2%

2,000

500

2009

2,001 1,9912,043

1,7651,556

2,025

2011

2010 2011

Competition 4%

Labour shortages

15

12

5

5

4 2

2

1

1

1

12

JapanUK

Rest of Canada

184

136

2008 2009

194

1

1

23

23

195

215 211

133

194

168

237

218211

168

195

211

3

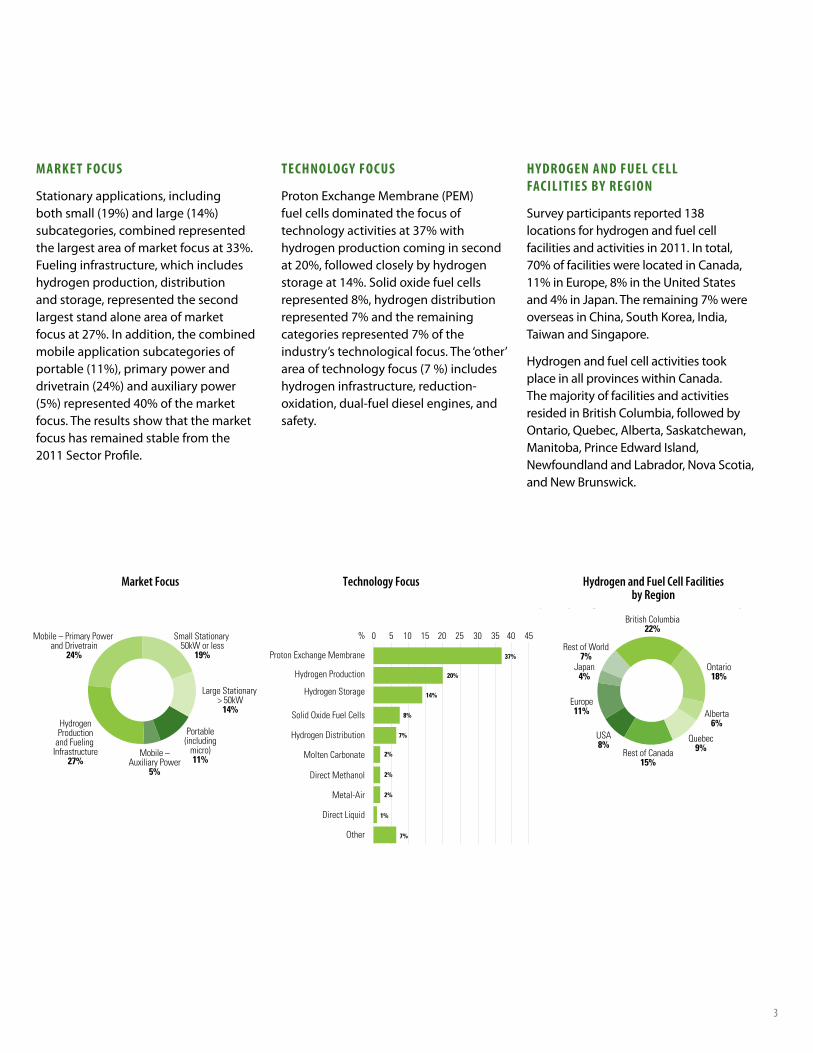

maRket fOCus

Stationary applications, including bothsmall(19%)andlarge(14%)subcategories, combined represented thelargestareaofmarketfocusat33%.Fueling infrastructure, which includes hydrogen production, distribution and storage, represented the second largest stand alone area of market focusat27%.Inaddition,thecombinedmobile application subcategories of portable(11%),primarypoweranddrivetrain(24%)andauxiliarypower(5%)represented40%ofthemarketfocus. The results show that the market focus has remained stable from the 2011 Sector Profile.

teCHnOlOgy fOCus

ProtonExchangeMembrane(PEM)fuel cells dominated the focus of technologyactivitiesat37%withhydrogen production coming in second at20%,followedcloselybyhydrogenstorageat14%.Solidoxidefuelcellsrepresented8%,hydrogendistributionrepresented7%andtheremainingcategoriesrepresented7%oftheindustry’s technological focus. The ‘other’ areaoftechnologyfocus(7%)includeshydrogen infrastructure, reduction-oxidation, dual-fuel diesel engines, and safety.

HydROgen and fuel Cell faCilities by RegiOn

Surveyparticipantsreported138locations for hydrogen and fuel cell facilities and activities in 2011. In total, 70%offacilitieswerelocatedinCanada,11%inEurope,8%intheUnitedStatesand4%inJapan.Theremaining7%wereoverseas in China, South Korea, India, Taiwan and Singapore.

Hydrogen and fuel cell activities took place in all provinces within Canada. Themajorityoffacilitiesandactivitiesresided in British Columbia, followed by Ontario, Quebec, Alberta, Saskatchewan, Manitoba,PrinceEdwardIsland,Newfoundland and Labrador, Nova Scotia, and New Brunswick.

Technology Focus Hydrogen and Fuel Cell Facilities by Region

Market Focus

Private company40%

Public company15%Division/subsidiary

of public company8%

Governmentorganizations

18%

Educationorganization

18%

Non-profit organization incl. associations

1%

p. 2 Organization Type

Apr 2012

Not provided15%

> 20 years18%

11 – 20 years33%

5 – 10 years26%

< 5 years8%

p.2 Years of Involvement in Hydrogen and Fuel Cell Activities

Mobile –Auxiliary Power

5%

Mobile – Primary Power and Drivetrain

24%

Portable(including

micro)11%

Small Stationary 50kW or less

19%

Large Stationary > 50kW

14%HydrogenProduction

and Fueling Infrastructure

27%

p.3 Market Focus

Rest of World7%

Rest of Canada15%

Ontario18%

Quebec9%

Alberta6%

British Columbia22%

USA8%

p.3 Hydrogen and Fuel Cell Facilities by Region

Provision of services

37%

Product sales59%

Canadian government supportrecognized as revenue

1%

p.4 Revenue by Category

Small Stationary50kW or less

14%LargeStationary

> 50kW2%

Mobile –Primary

Power andDrivetrain

13%

Mobile – Auxiliary Power

21%

FuelingInfrastructure

50%

p.7 Focus of Demonstration Projects

Rest of Canada 4%USA5%

Quebec9%

Asia2%

Rest of Europe 6%

British Columbia58%

Ontario13%

p.8 Employment by Region

Government9%

Academia andnon-profit

15%

Corporate76%

p.8 Employment by Organization

Remain the same (+/-5%)

52%

Significant increase(greater than 15%

of current employees)17%

Increase(between 5%

and 15%)23%

p.11 Plans to change employment in the next 18 months

Government13%

Private equity19%

Other10%

Angel Investors4%

Operations52%

p.9 Sources of Funding - Corporate

A-Base15%

Programs85%

p.9 Sources of Funding - Government

Other non-profitorganization

37%

NSERC/Canadian Foundation for Innovation

13%

Other 50%

p.9 Sources of Funding – Academia and Non-Profit

Other OEM13%

Public-privatepartnerships

26%

Hydrogen andfuel cell companies

26%

EnergyProviders

11%

Other 7%

p.10 Strategic Alliances

Declined3%

No reply40%

Completed survey57%

p.10 Profile participation rate

Technicians2%

Academic/research staff

26%

Undergraduatestudents

including coop13%

Canadian graduate andpostgraduate students

46%

International graduate andpostgraduate students

13%

p.6 People Involved in Research

USA25%Germany

30%

Asia 4%

Rest of world 5%

BritishColumbia

27%Ontario 1%

Rest of Canada1%Rest of

Europe7%

p.6 R&D by region

British Columbia77%

Rest of the world5%

Ontario10%

Quebec 3%Germany 3%

USA 1%

p.4 Revenue by Region

R&DIn-house

48%

p.9 Funding Allocation by Area - Gov’t & Academia & Non-profit

R&DIntramural

35%

Marketing andbusiness development

1%Education,

safety and training5%

Policy development1%

Monitoringand reporting

1%

Demonstrationand pilot projects

9%

Europe11%

Other 3%

Germany 3%

Significantly decrease (greater than 15%)

3%Decrease

(between 5 and 15%)5%

Japan 1%

Japan4%

Automotive OEM17%

Public capital markets2%

Private company40%

Public company15%Division/subsidiary

of public company8%

Governmentorganizations

18%

Educationorganization

18%

Non-profit organization incl. associations

1%

p. 2 Organization Type

Apr 2012

Not provided15%

> 20 years18%

11 – 20 years33%

5 – 10 years26%

< 5 years8%

p.2 Years of Involvement in Hydrogen and Fuel Cell Activities

Mobile –Auxiliary Power

5%

Mobile – Primary Power and Drivetrain

24%

Portable(including

micro)11%

Small Stationary 50kW or less

19%

Large Stationary > 50kW

14%HydrogenProduction

and Fueling Infrastructure

27%

p.3 Market Focus

Rest of World7%

Rest of Canada15%

Ontario18%

Quebec9%

Alberta6%

British Columbia22%

USA8%

p.3 Hydrogen and Fuel Cell Facilities by Region

Provision of services

37%

Product sales59%

Canadian government supportrecognized as revenue

1%

p.4 Revenue by Category

Small Stationary50kW or less

14%LargeStationary

> 50kW2%

Mobile –Primary

Power andDrivetrain

13%

Mobile – Auxiliary Power

21%

FuelingInfrastructure

50%

p.7 Focus of Demonstration Projects

Rest of Canada 4%USA5%

Quebec9%

Asia2%

Rest of Europe 6%

British Columbia58%

Ontario13%

p.8 Employment by Region

Government9%

Academia andnon-profit

15%

Corporate76%

p.8 Employment by Organization

Remain the same (+/-5%)

52%

Significant increase(greater than 15%

of current employees)17%

Increase(between 5%

and 15%)23%

p.11 Plans to change employment in the next 18 months

Government13%

Private equity19%

Other10%

Angel Investors4%

Operations52%

p.9 Sources of Funding - Corporate

A-Base15%

Programs85%

p.9 Sources of Funding - Government

Other non-profitorganization

37%

NSERC/Canadian Foundation for Innovation

13%

Other 50%

p.9 Sources of Funding – Academia and Non-Profit

Other OEM13%

Public-privatepartnerships

26%

Hydrogen andfuel cell companies

26%

EnergyProviders

11%

Other 7%

p.10 Strategic Alliances

Declined3%

No reply40%

Completed survey57%

p.10 Profile participation rate

Technicians2%

Academic/research staff

26%

Undergraduatestudents

including coop13%

Canadian graduate andpostgraduate students

46%

International graduate andpostgraduate students

13%

p.6 People Involved in Research

USA25%Germany

30%

Asia 4%

Rest of world 5%

BritishColumbia

27%Ontario 1%

Rest of Canada1%Rest of

Europe7%

p.6 R&D by region

British Columbia77%

Rest of the world5%

Ontario10%

Quebec 3%Germany 3%

USA 1%

p.4 Revenue by Region

R&DIn-house

48%

p.9 Funding Allocation by Area - Gov’t & Academia & Non-profit

R&DIntramural

35%

Marketing andbusiness development

1%Education,

safety and training5%

Policy development1%

Monitoringand reporting

1%

Demonstrationand pilot projects

9%

Europe11%

Other 3%

Germany 3%

Significantly decrease (greater than 15%)

3%Decrease

(between 5 and 15%)5%

Japan 1%

Japan4%

Automotive OEM17%

Public capital markets2%

Access to markets

Lack of funding

Technology development

p.2 Areas of Expertise

p.3 Technology Focus

p.4 Total Revenue ($ millions)

Hydrogen production

Research organization

Policy development andprogram administration

Fuel cell user

Professional services provider

Hydrogen distribution

Fuel cell developer or manufacturer

5 10 15 20 250

Other

Systems integrator

Education, safety and training

Commercialization support

Supplier to developer or manufacturer

Hydrogen storage

Fuel cell distributor or agent

22%

12%

12%

9%

8%

7%

6%

5%

4%

3%

3%

2%

2%

3%

0 5 10 15 20 25 30 35 40 45

Proton Exchange Membrane

Solid Oxide Fuel Cells

Hydrogen Production

Hydrogen Distribution

Hydrogen Storage

Metal-Air

Molten Carbonate

Direct Liquid

Other

1%

7%

7%

37%

8%

2%

2%

14%

20%

0

50

100

150

200

250

2008

p.8 Employment

28. Growth since 2001

1,500

1,000

0

2,500

2006

2007 20092006

2007 2008 2010

0

50

100

150

200

250

300

2005 2006 2007 201020042003200220010

500

1,000

1,500

2,000

2,500

3,000

R&DRevenue Employees

$

p.7 Patents

200

100

0

300

400

235

351

Alberta

Canadian government (all levels)

Corporate operations

Parent, affiliatedor subsidiary

Research, non-profit,non-governmental institute

Contract work conductedfor another institute

0 20 40 60 80 100

12. Sources of Funding for R&D Expenditure by Organization

23%

68%

7%

7%

9%

Foreign government

University oracademic institute

1%

3%

14%

0% 20% 40% 60% 80% 100%

100%61%

GovernmentCorporate Academic and non-profit

290

179

134

276

188

97

133 135 133

177

128

2011

215

142

Feb 2011

Patentsapproved

Patentspending

p.11 Priorities to enhance competitive performance in 2012

0 5 10 15 20 25

Collaboration/strategic alliances

Gain market share

Better targetingof customers

Improving processes

Better marketor customer data

Plans for expansion(new products/new markets)

Other

Outsourcing

8%

1%

8%

21%

8%

Reduce costof operations

7%

6%

19%

12%

10%

p.? challenges faced in 2010

0% 5 10 15 20 25 30

Profitability

Economy

Exchange rates

6%

31%

6%

Other 9%

24%

10%

10%

GermanyUSA

British ColumbiaQuebecOntario

0 5 10 15 20 25 30 35 40 45 50 55 60

16. Demonstration Projects by Region (Number of Projects)

51

Other

GovernmentCorporate Academia and non-profit

%

%

%

Millions Employees

Utility 2%

Direct Methanol 2%

2,000

500

2009

2,001 1,9912,043

1,7651,556

2,025

2011

2010 2011

Competition 4%

Labour shortages

15

12

5

5

4 2

2

1

1

1

12

JapanUK

Rest of Canada

184

136

2008 2009

194

1

1

23

23

195

215 211

133

194

168

237

218211

168

195

211

4

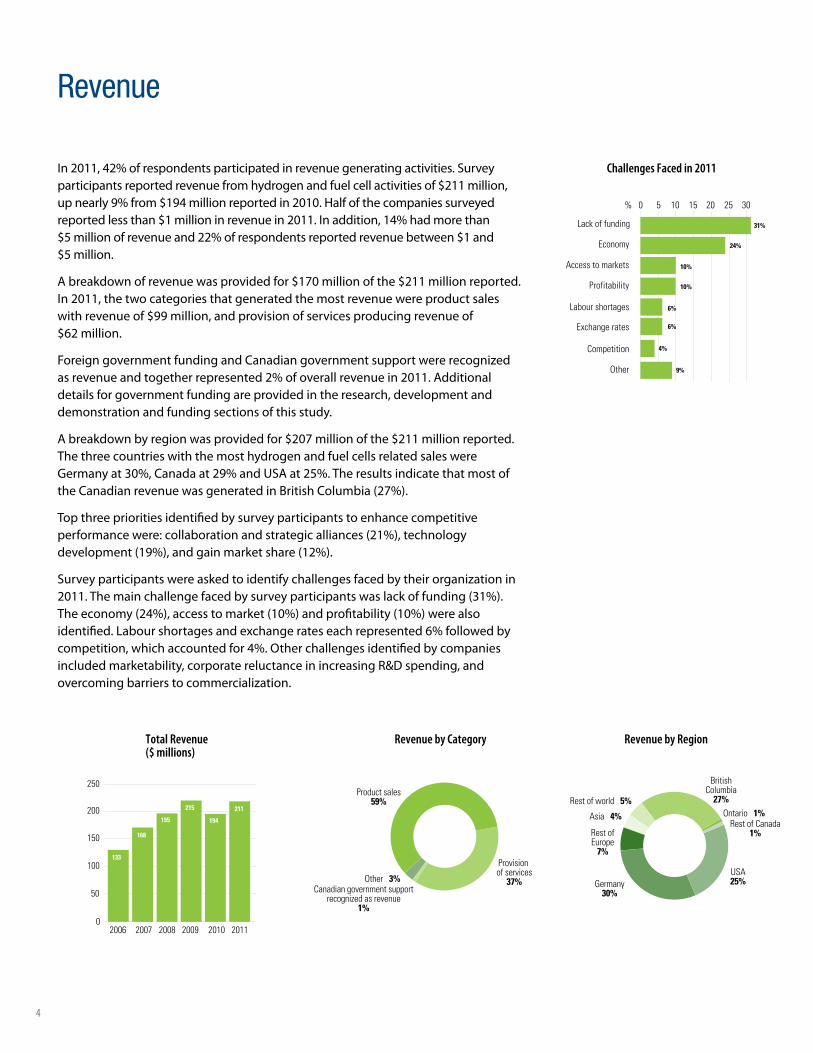

In2011,42%ofrespondentsparticipatedinrevenuegeneratingactivities.Surveyparticipantsreportedrevenuefromhydrogenandfuelcellactivitiesof$211million,upnearly9%from$194millionreportedin2010.Halfofthecompaniessurveyedreportedlessthan$1millioninrevenuein2011.Inaddition,14%hadmorethan$5 millionofrevenueand22%ofrespondentsreportedrevenuebetween$1and$5 million.

Abreakdownofrevenuewasprovidedfor$170millionofthe$211millionreported.In 2011, the two categories that generated the most revenue were product sales withrevenueof$99million,andprovisionofservicesproducingrevenueof$62 million.

Foreign government funding and Canadian government support were recognized asrevenueandtogetherrepresented2%ofoverallrevenuein2011.Additionaldetails for government funding are provided in the research, development and demonstration and funding sections of this study.

Abreakdownbyregionwasprovidedfor$207millionofthe$211millionreported.The three countries with the most hydrogen and fuel cells related sales were Germanyat30%,Canadaat29%andUSAat25%.TheresultsindicatethatmostoftheCanadianrevenuewasgeneratedinBritishColumbia(27%).

Top three priorities identified by survey participants to enhance competitive performancewere:collaborationandstrategicalliances(21%),technologydevelopment(19%),andgainmarketshare(12%).

Survey participants were asked to identify challenges faced by their organization in 2011.Themainchallengefacedbysurveyparticipantswaslackoffunding(31%).Theeconomy(24%),accesstomarket(10%)andprofitability(10%)werealsoidentified.Labourshortagesandexchangerateseachrepresented6%followedbycompetition,whichaccountedfor4%.Otherchallengesidentifiedbycompaniesincludedmarketability,corporatereluctanceinincreasingR&Dspending,andovercoming barriers to commercialization.

Revenue

Revenue by Category

Private company40%

Public company15%Division/subsidiary

of public company8%

Governmentorganizations

18%

Educationorganization

18%

Non-profit organization incl. associations

1%

p. 2 Organization Type

Apr 2012

Not provided15%

> 20 years18%

11 – 20 years33%

5 – 10 years26%

< 5 years8%

p.2 Years of Involvement in Hydrogen and Fuel Cell Activities

Mobile –Auxiliary Power

5%

Mobile – Primary Power and Drivetrain

24%

Portable(including

micro)11%

Small Stationary 50kW or less

19%

Large Stationary > 50kW

14%HydrogenProduction

and Fueling Infrastructure

27%

p.3 Market Focus

Rest of World7%

Rest of Canada15%

Ontario18%

Quebec9%

Alberta6%

British Columbia22%

USA8%

p.3 Hydrogen and Fuel Cell Facilities by Region

Provision of services

37%

Product sales59%

Canadian government supportrecognized as revenue

1%

p.4 Revenue by Category

Small Stationary50kW or less

14%LargeStationary

> 50kW2%

Mobile –Primary

Power andDrivetrain

13%

Mobile – Auxiliary Power

21%

FuelingInfrastructure

50%

p.7 Focus of Demonstration Projects

Rest of Canada 4%USA5%

Quebec9%

Asia2%

Rest of Europe 6%

British Columbia58%

Ontario13%

p.8 Employment by Region

Government9%

Academia andnon-profit

15%

Corporate76%

p.8 Employment by Organization

Remain the same (+/-5%)

52%

Significant increase(greater than 15%

of current employees)17%

Increase(between 5%

and 15%)23%

p.11 Plans to change employment in the next 18 months

Government13%

Private equity19%

Other10%

Angel Investors4%

Operations52%

p.9 Sources of Funding - Corporate

A-Base15%

Programs85%

p.9 Sources of Funding - Government

Other non-profitorganization

37%

NSERC/Canadian Foundation for Innovation

13%

Other 50%

p.9 Sources of Funding – Academia and Non-Profit

Other OEM13%

Public-privatepartnerships

26%

Hydrogen andfuel cell companies

26%

EnergyProviders

11%

Other 7%

p.10 Strategic Alliances

Declined3%

No reply40%

Completed survey57%

p.10 Profile participation rate

Technicians2%

Academic/research staff

26%

Undergraduatestudents

including coop13%

Canadian graduate andpostgraduate students

46%

International graduate andpostgraduate students

13%

p.6 People Involved in Research

USA25%Germany

30%

Asia 4%

Rest of world 5%

BritishColumbia

27%Ontario 1%

Rest of Canada1%Rest of

Europe7%

p.6 R&D by region

British Columbia77%

Rest of the world5%

Ontario10%

Quebec 3%Germany 3%

USA 1%

p.4 Revenue by Region

R&DIn-house

48%

p.9 Funding Allocation by Area - Gov’t & Academia & Non-profit

R&DIntramural

35%

Marketing andbusiness development

1%Education,

safety and training5%

Policy development1%

Monitoringand reporting

1%

Demonstrationand pilot projects

9%

Europe11%

Other 3%

Germany 3%

Significantly decrease (greater than 15%)

3%Decrease

(between 5 and 15%)5%

Japan 1%

Japan4%

Automotive OEM17%

Public capital markets2%

Revenue by Region

Private company40%

Public company15%Division/subsidiary

of public company8%

Governmentorganizations

18%

Educationorganization

18%

Non-profit organization incl. associations

1%

p. 2 Organization Type

Apr 2012

Not provided15%

> 20 years18%

11 – 20 years33%

5 – 10 years26%

< 5 years8%

p.2 Years of Involvement in Hydrogen and Fuel Cell Activities

Mobile –Auxiliary Power

5%

Mobile – Primary Power and Drivetrain

24%

Portable(including

micro)11%

Small Stationary 50kW or less

19%

Large Stationary > 50kW

14%HydrogenProduction

and Fueling Infrastructure

27%

p.3 Market Focus

Rest of World7%

Rest of Canada15%

Ontario18%

Quebec9%

Alberta6%

British Columbia22%

USA8%

p.3 Hydrogen and Fuel Cell Facilities by Region

Provision of services

37%

Product sales59%

Canadian government supportrecognized as revenue

1%

p.4 Revenue by Category

Small Stationary50kW or less

14%LargeStationary

> 50kW2%

Mobile –Primary

Power andDrivetrain

13%

Mobile – Auxiliary Power

21%

FuelingInfrastructure

50%

p.7 Focus of Demonstration Projects

Rest of Canada 4%USA5%

Quebec9%

Asia2%

Rest of Europe 6%

British Columbia58%

Ontario13%

p.8 Employment by Region

Government9%

Academia andnon-profit

15%

Corporate76%

p.8 Employment by Organization

Remain the same (+/-5%)

52%

Significant increase(greater than 15%

of current employees)17%

Increase(between 5%

and 15%)23%

p.11 Plans to change employment in the next 18 months

Government13%

Private equity19%

Other10%

Angel Investors4%

Operations52%

p.9 Sources of Funding - Corporate

A-Base15%

Programs85%

p.9 Sources of Funding - Government

Other non-profitorganization

37%

NSERC/Canadian Foundation for Innovation

13%

Other 50%

p.9 Sources of Funding – Academia and Non-Profit

Other OEM13%

Public-privatepartnerships

26%

Hydrogen andfuel cell companies

26%

EnergyProviders

11%

Other 7%

p.10 Strategic Alliances

Declined3%

No reply40%

Completed survey57%

p.10 Profile participation rate

Technicians2%

Academic/research staff

26%

Undergraduatestudents

including coop13%

Canadian graduate andpostgraduate students

46%

International graduate andpostgraduate students

13%

p.6 People Involved in Research

USA25%Germany

30%

Asia 4%

Rest of world 5%

BritishColumbia

27%Ontario 1%

Rest of Canada1%Rest of

Europe7%

p.6 R&D by region

British Columbia77%

Rest of the world5%

Ontario10%

Quebec 3%Germany 3%

USA 1%

p.4 Revenue by Region

R&DIn-house

48%

p.9 Funding Allocation by Area - Gov’t & Academia & Non-profit

R&DIntramural

35%

Marketing andbusiness development

1%Education,

safety and training5%

Policy development1%

Monitoringand reporting

1%

Demonstrationand pilot projects

9%

Europe11%

Other 3%

Germany 3%

Significantly decrease (greater than 15%)

3%Decrease

(between 5 and 15%)5%

Japan 1%

Japan4%

Automotive OEM17%

Public capital markets2%

Total Revenue ($ millions)

Challenges Faced in 2011

Access to markets

Lack of funding

Technology development

p.2 Areas of Expertise

p.3 Technology Focus

p.4 Total Revenue ($ millions)

Hydrogen production

Research organization

Policy development andprogram administration

Fuel cell user

Professional services provider

Hydrogen distribution

Fuel cell developer or manufacturer

5 10 15 20 250

Other

Systems integrator

Education, safety and training

Commercialization support

Supplier to developer or manufacturer

Hydrogen storage

Fuel cell distributor or agent

22%

12%

12%

9%

8%

7%

6%

5%

4%

3%

3%

2%

2%

3%

0 5 10 15 20 25 30 35 40 45

Proton Exchange Membrane

Solid Oxide Fuel Cells

Hydrogen Production

Hydrogen Distribution

Hydrogen Storage

Metal-Air

Molten Carbonate

Direct Liquid

Other

1%

7%

7%

37%

8%

2%

2%

14%

20%

0

50

100

150

200

250

2008

p.8 Employment

28. Growth since 2001

1,500

1,000

0

2,500

2006

2007 20092006

2007 2008 2010

0

50

100

150

200

250

300

2005 2006 2007 201020042003200220010

500

1,000

1,500

2,000

2,500

3,000

R&DRevenue Employees

$

p.7 Patents

200

100

0

300

400

235

351

Alberta

Canadian government (all levels)

Corporate operations

Parent, affiliatedor subsidiary

Research, non-profit,non-governmental institute

Contract work conductedfor another institute

0 20 40 60 80 100

12. Sources of Funding for R&D Expenditure by Organization

23%

68%

7%

7%

9%

Foreign government

University oracademic institute

1%

3%

14%

0% 20% 40% 60% 80% 100%

100%61%

GovernmentCorporate Academic and non-profit

290

179

134

276

188

97

133 135 133

177

128

2011

215

142

Feb 2011

Patentsapproved

Patentspending

p.11 Priorities to enhance competitive performance in 2012

0 5 10 15 20 25

Collaboration/strategic alliances

Gain market share

Better targetingof customers

Improving processes

Better marketor customer data

Plans for expansion(new products/new markets)

Other

Outsourcing

8%

1%

8%

21%

8%

Reduce costof operations

7%

6%

19%

12%

10%

p.? challenges faced in 2010

0% 5 10 15 20 25 30

Profitability

Economy

Exchange rates

6%

31%

6%

Other 9%

24%

10%

10%

GermanyUSA

British ColumbiaQuebecOntario

0 5 10 15 20 25 30 35 40 45 50 55 60

16. Demonstration Projects by Region (Number of Projects)

51

Other

GovernmentCorporate Academia and non-profit

%

%

%

Millions Employees

Utility 2%

Direct Methanol 2%

2,000

500

2009

2,001 1,9912,043

1,7651,556

2,025

2011

2010 2011

Competition 4%

Labour shortages

15

12

5

5

4 2

2

1

1

1

12

JapanUK

Rest of Canada

184

136

2008 2009

194

1

1

23

23

195

215 211

133

194

168

237

218211

168

195

211

Access to markets

Lack of funding

Technology development

p.2 Areas of Expertise

p.3 Technology Focus

p.4 Total Revenue ($ millions)

Hydrogen production

Research organization

Policy development andprogram administration

Fuel cell user

Professional services provider

Hydrogen distribution

Fuel cell developer or manufacturer

5 10 15 20 250

Other

Systems integrator

Education, safety and training

Commercialization support

Supplier to developer or manufacturer

Hydrogen storage

Fuel cell distributor or agent

22%

12%

12%

9%

8%

7%

6%

5%

4%

3%

3%

2%

2%

3%

0 5 10 15 20 25 30 35 40 45

Proton Exchange Membrane

Solid Oxide Fuel Cells

Hydrogen Production

Hydrogen Distribution

Hydrogen Storage

Metal-Air

Molten Carbonate

Direct Liquid

Other

1%

7%

7%

37%

8%

2%

2%

14%

20%

0

50

100

150

200

250

2008

p.8 Employment

28. Growth since 2001

1,500

1,000

0

2,500

2006

2007 20092006

2007 2008 2010

0

50

100

150

200

250

300

2005 2006 2007 201020042003200220010

500

1,000

1,500

2,000

2,500

3,000

R&DRevenue Employees

$

p.7 Patents

200

100

0

300

400

235

351

Alberta

Canadian government (all levels)

Corporate operations

Parent, affiliatedor subsidiary

Research, non-profit,non-governmental institute

Contract work conductedfor another institute

0 20 40 60 80 100

12. Sources of Funding for R&D Expenditure by Organization

23%

68%

7%

7%

9%

Foreign government

University oracademic institute

1%

3%

14%

0% 20% 40% 60% 80% 100%

100%61%

GovernmentCorporate Academic and non-profit

290

179

134

276

188

97

133 135 133

177

128

2011

215

142

Feb 2011

Patentsapproved

Patentspending

p.11 Priorities to enhance competitive performance in 2012

0 5 10 15 20 25

Collaboration/strategic alliances

Gain market share

Better targetingof customers

Improving processes

Better marketor customer data

Plans for expansion(new products/new markets)

Other

Outsourcing

8%

1%

8%

21%

8%

Reduce costof operations

7%

6%

19%

12%

10%

p.? challenges faced in 2010

0% 5 10 15 20 25 30

Profitability

Economy

Exchange rates

6%

31%

6%

Other 9%

24%

10%

10%

GermanyUSA

British ColumbiaQuebecOntario

0 5 10 15 20 25 30 35 40 45 50 55 60

16. Demonstration Projects by Region (Number of Projects)

51

Other

GovernmentCorporate Academia and non-profit

%

%

%

Millions Employees

Utility 2%

Direct Methanol 2%

2,000

500

2009

2,001 1,9912,043

1,7651,556

2,025

2011

2010 2011

Competition 4%

Labour shortages

15

12

5

5

4 2

2

1

1

1

12

JapanUK

Rest of Canada

184

136

2008 2009

194

1

1

23

23

195

215 211

133

194

168

237

218211

168

195

211

5

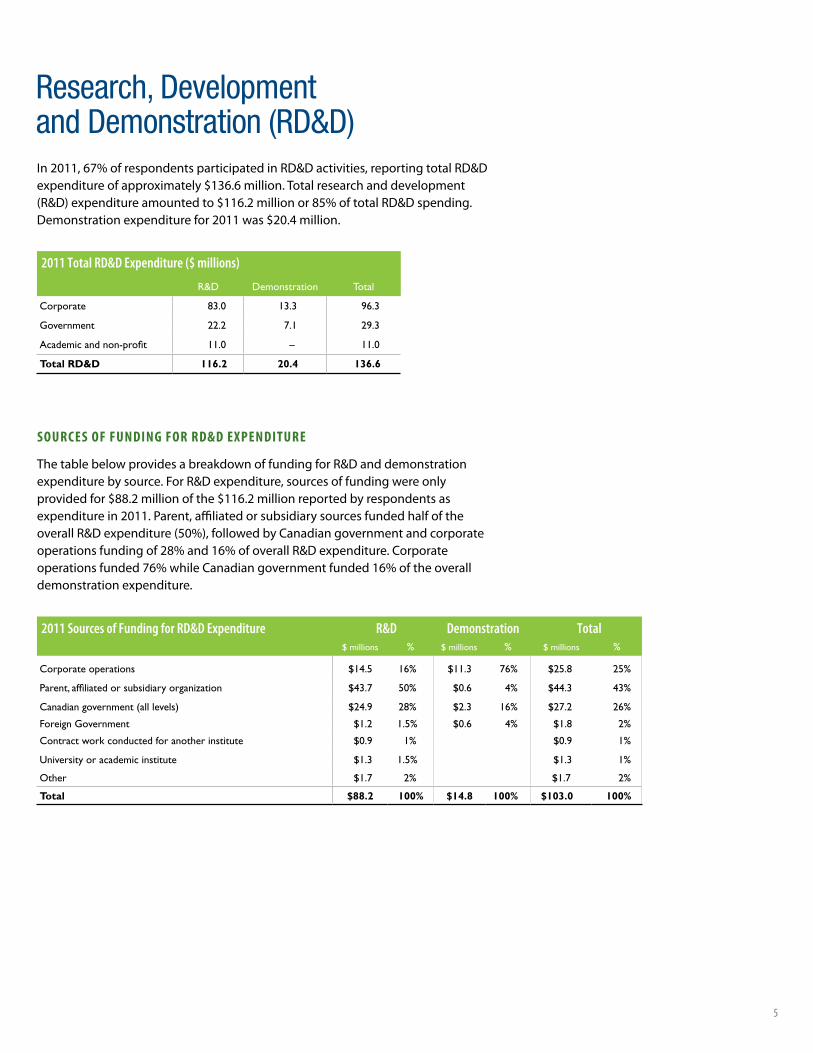

In2011,67%ofrespondentsparticipatedinRD&Dactivities,reportingtotalRD&Dexpenditureofapproximately$136.6million.Totalresearchanddevelopment(R&D)expenditureamountedto$116.2millionor85%oftotalRD&Dspending.Demonstrationexpenditurefor2011was$20.4million.

Research, Development and Demonstration (RD&D)

R&D Demonstration Total

Corporate 83.0 13.3 96.3

Government 22.2 7.1 29.3

Academic and non-profit 11.0 – 11.0

Total RD&D 116.2 20.4 136.6

2011 Total RD&D Expenditure ($ millions)

sOuRCes Of funding fOR Rd&d exPendituRe

ThetablebelowprovidesabreakdownoffundingforR&Danddemonstrationexpenditurebysource.ForR&Dexpenditure,sourcesoffundingwereonlyprovidedfor$88.2millionofthe$116.2millionreportedbyrespondentsasexpenditure in 2011. Parent, affiliated or subsidiary sources funded half of the overallR&Dexpenditure(50%),followedbyCanadiangovernmentandcorporateoperationsfundingof28%and16%ofoverallR&Dexpenditure.Corporateoperationsfunded76%whileCanadiangovernmentfunded16%oftheoveralldemonstration expenditure.

Sources of Funding for R&D Expenditure

$ millions % $ millions % $ millions %

Corporate operations $14.5 16% $11.3 76% $25.8 25%

Parent, affiliated or subsidiary organization $43.7 50% $0.6 4% $44.3 43%

Canadian government (all levels) $24.9 28% $2.3 16% $27.2 26%

Foreign Government $1.2 1.5% $0.6 4% $1.8 2%

Contract work conducted for another institute $0.9 1% $0.9 1%

University or academic institute $1.3 1.5% $1.3 1%

Other $1.7 2% $1.7 2%

Total $88.2 100% $14.8 100% $103.0 100%

2011 Sources of Funding for RD&D Expenditure R&D Demonstration Total

6

Access to markets

Lack of funding

Technology development

p.2 Areas of Expertise

p.3 Technology Focus

p.4 Total Revenue ($ millions)

Hydrogen production

Research organization

Policy development andprogram administration

Fuel cell user

Professional services provider

Hydrogen distribution

Fuel cell developer or manufacturer

5 10 15 20 250

Other

Systems integrator

Education, safety and training

Commercialization support

Supplier to developer or manufacturer

Hydrogen storage

Fuel cell distributor or agent

22%

12%

12%

9%

8%

7%

6%

5%

4%

3%

3%

2%

2%

3%

0 5 10 15 20 25 30 35 40 45

Proton Exchange Membrane

Solid Oxide Fuel Cells

Hydrogen Production

Hydrogen Distribution

Hydrogen Storage

Metal-Air

Molten Carbonate

Direct Liquid

Other

1%

7%

7%

37%

8%

2%

2%

14%

20%

0

50

100

150

200

250

2008

p.8 Employment

28. Growth since 2001

1,500

1,000

0

2,500

2006

2007 20092006

2007 2008 2010

0

50

100

150

200

250

300

2005 2006 2007 201020042003200220010

500

1,000

1,500

2,000

2,500

3,000

R&DRevenue Employees

$

p.7 Patents

200

100

0

300

400

235

351

Alberta

Canadian government (all levels)

Corporate operations

Parent, affiliatedor subsidiary

Research, non-profit,non-governmental institute

Contract work conductedfor another institute

0 20 40 60 80 100

12. Sources of Funding for R&D Expenditure by Organization

23%

68%

7%

7%

9%

Foreign government

University oracademic institute

1%

3%

14%

0% 20% 40% 60% 80% 100%

100%61%

GovernmentCorporate Academic and non-profit

290

179

134

276

188

97

133 135 133

177

128

2011

215

142

Feb 2011

Patentsapproved

Patentspending

p.11 Priorities to enhance competitive performance in 2012

0 5 10 15 20 25

Collaboration/strategic alliances

Gain market share

Better targetingof customers

Improving processes

Better marketor customer data

Plans for expansion(new products/new markets)

Other

Outsourcing

8%

1%

8%

21%

8%

Reduce costof operations

7%

6%

19%

12%

10%

p.? challenges faced in 2010

0% 5 10 15 20 25 30

Profitability

Economy

Exchange rates

6%

31%

6%

Other 9%

24%

10%

10%

GermanyUSA

British ColumbiaQuebecOntario

0 5 10 15 20 25 30 35 40 45 50 55 60

16. Demonstration Projects by Region (Number of Projects)

51

Other

GovernmentCorporate Academia and non-profit

%

%

%

Millions Employees

Utility 2%

Direct Methanol 2%

2,000

500

2009

2,001 1,9912,043

1,7651,556

2,025

2011

2010 2011

Competition 4%

Labour shortages

15

12

5

5

4 2

2

1

1

1

12

JapanUK

Rest of Canada

184

136

2008 2009

194

1

1

23

23

195

215 211

133

194

168

237

218211

168

195

211

Sources of Funding for R&D Expenditure by Organization

Research and Development

R&d by RegiOn

Geographic data was provided for $86.5 millionofR&Dexpenditure.BritishColumbialedallregionswith77%ofR&Dexpenditure.OntarioandQuebeccontributed10%and3%.Globally,Germanyprovided3%withtheUSAandJapaneachproviding1%oftheR&Dexpenditure.RegionsincludedintheRestoftheWorldcategory(5%)includeFrance,Denmark,BelgiumandChina.

PeOPle invOlved in ReseaRCH

Participantsreportedthatatotalof392people were involved in hydrogen and fuel cell related research activity. Of the total people involved in research, 46%wereCanadiangraduateandpostgraduatestudents,26%wereacademic/researchstaff,13%wereundergraduateandpost-graduatestudents,13%were international graduate and post-graduatestudents,and2%weretechnicians.

sOuRCes Of funding fOR R&d exPendituRe

The bar chart below represents sources offundingforR&Dexpenditureby type of organization. Corporate respondents received most of their funding from parent, affiliated or subsidiarysources (68%).Governmentorganizations received all of their funding from Canadian government sources(100%).Academicandnon-profitorganizations also received most of their funding from Canadian government sources(61%).

Private company40%

Public company15%Division/subsidiary

of public company8%

Governmentorganizations

18%

Educationorganization

18%

Non-profit organization incl. associations

1%

p. 2 Organization Type

Apr 2012

Not provided15%

> 20 years18%

11 – 20 years33%

5 – 10 years26%

< 5 years8%

p.2 Years of Involvement in Hydrogen and Fuel Cell Activities

Mobile –Auxiliary Power

5%

Mobile – Primary Power and Drivetrain

24%

Portable(including

micro)11%

Small Stationary 50kW or less

19%

Large Stationary > 50kW

14%HydrogenProduction

and Fueling Infrastructure

27%

p.3 Market Focus

Rest of World7%

Rest of Canada15%

Ontario18%

Quebec9%

Alberta6%

British Columbia22%

USA8%

p.3 Hydrogen and Fuel Cell Facilities by Region

Provision of services

37%

Product sales59%

Canadian government supportrecognized as revenue

1%

p.4 Revenue by Category

Small Stationary50kW or less

14%LargeStationary

> 50kW2%

Mobile –Primary

Power andDrivetrain

13%

Mobile – Auxiliary Power

21%

FuelingInfrastructure

50%

p.7 Focus of Demonstration Projects

Rest of Canada 4%USA5%

Quebec9%

Asia2%

Rest of Europe 6%

British Columbia58%

Ontario13%

p.8 Employment by Region

Government9%

Academia andnon-profit

15%

Corporate76%

p.8 Employment by Organization

Remain the same (+/-5%)

52%

Significant increase(greater than 15%

of current employees)17%

Increase(between 5%

and 15%)23%

p.11 Plans to change employment in the next 18 months

Government13%

Private equity19%

Other10%

Angel Investors4%

Operations52%

p.9 Sources of Funding - Corporate

A-Base15%

Programs85%

p.9 Sources of Funding - Government

Other non-profitorganization

37%

NSERC/Canadian Foundation for Innovation

13%

Other 50%

p.9 Sources of Funding – Academia and Non-Profit

Other OEM13%

Public-privatepartnerships

26%

Hydrogen andfuel cell companies

26%

EnergyProviders

11%

Other 7%

p.10 Strategic Alliances

Declined3%

No reply40%

Completed survey57%

p.10 Profile participation rate

Technicians2%

Academic/research staff

26%

Undergraduatestudents

including coop13%

Canadian graduate andpostgraduate students

46%

International graduate andpostgraduate students

13%

p.6 People Involved in Research

USA25%Germany

30%

Asia 4%

Rest of world 5%

BritishColumbia

27%Ontario 1%

Rest of Canada1%Rest of

Europe7%

p.6 R&D by region

British Columbia77%

Rest of the world5%

Ontario10%

Quebec 3%Germany 3%

USA 1%

p.4 Revenue by Region

R&DIn-house

48%

p.9 Funding Allocation by Area - Gov’t & Academia & Non-profit

R&DIntramural

35%

Marketing andbusiness development

1%Education,

safety and training5%

Policy development1%

Monitoringand reporting

1%

Demonstrationand pilot projects

9%

Europe11%

Other 3%

Germany 3%

Significantly decrease (greater than 15%)

3%Decrease

(between 5 and 15%)5%

Japan 1%

Japan4%

Automotive OEM17%

Public capital markets2%

R&D by Region People Involved in Research

Private company40%

Public company15%Division/subsidiary

of public company8%

Governmentorganizations

18%

Educationorganization

18%

Non-profit organization incl. associations

1%

p. 2 Organization Type

Apr 2012

Not provided15%

> 20 years18%

11 – 20 years33%

5 – 10 years26%

< 5 years8%

p.2 Years of Involvement in Hydrogen and Fuel Cell Activities

Mobile –Auxiliary Power

5%

Mobile – Primary Power and Drivetrain

24%

Portable(including

micro)11%

Small Stationary 50kW or less

19%

Large Stationary > 50kW

14%HydrogenProduction

and Fueling Infrastructure

27%

p.3 Market Focus

Rest of World7%

Rest of Canada15%

Ontario18%

Quebec9%

Alberta6%

British Columbia22%

USA8%

p.3 Hydrogen and Fuel Cell Facilities by Region

Provision of services

37%

Product sales59%

Canadian government supportrecognized as revenue

1%

p.4 Revenue by Category

Small Stationary50kW or less

14%LargeStationary

> 50kW2%

Mobile –Primary

Power andDrivetrain

13%

Mobile – Auxiliary Power

21%

FuelingInfrastructure

50%

p.7 Focus of Demonstration Projects

Rest of Canada 4%USA5%

Quebec9%

Asia2%

Rest of Europe 6%

British Columbia58%

Ontario13%

p.8 Employment by Region

Government9%

Academia andnon-profit

15%

Corporate76%

p.8 Employment by Organization

Remain the same (+/-5%)

52%

Significant increase(greater than 15%

of current employees)17%

Increase(between 5%

and 15%)23%

p.11 Plans to change employment in the next 18 months

Government13%

Private equity19%

Other10%

Angel Investors4%

Operations52%

p.9 Sources of Funding - Corporate

A-Base15%

Programs85%

p.9 Sources of Funding - Government

Other non-profitorganization

37%

NSERC/Canadian Foundation for Innovation

13%

Other 50%

p.9 Sources of Funding – Academia and Non-Profit

Other OEM13%

Public-privatepartnerships

26%

Hydrogen andfuel cell companies

26%

EnergyProviders

11%

Other 7%

p.10 Strategic Alliances

Declined3%

No reply40%

Completed survey57%

p.10 Profile participation rate

Technicians2%

Academic/research staff

26%

Undergraduatestudents

including coop13%

Canadian graduate andpostgraduate students

46%

International graduate andpostgraduate students

13%

p.6 People Involved in Research

USA25%Germany

30%

Asia 4%

Rest of world 5%

BritishColumbia

27%Ontario 1%

Rest of Canada1%Rest of

Europe7%

p.6 R&D by region

British Columbia77%

Rest of the world5%

Ontario10%

Quebec 3%Germany 3%

USA 1%

p.4 Revenue by Region

R&DIn-house

48%

p.9 Funding Allocation by Area - Gov’t & Academia & Non-profit

R&DIntramural

35%

Marketing andbusiness development

1%Education,

safety and training5%

Policy development1%

Monitoringand reporting

1%

Demonstrationand pilot projects

9%

Europe11%

Other 3%

Germany 3%

Significantly decrease (greater than 15%)

3%Decrease

(between 5 and 15%)5%

Japan 1%

Japan4%

Automotive OEM17%

Public capital markets2%

Hydrogen fuel tank

7

sOuRCes Of funding fOR demOnstRatiOn

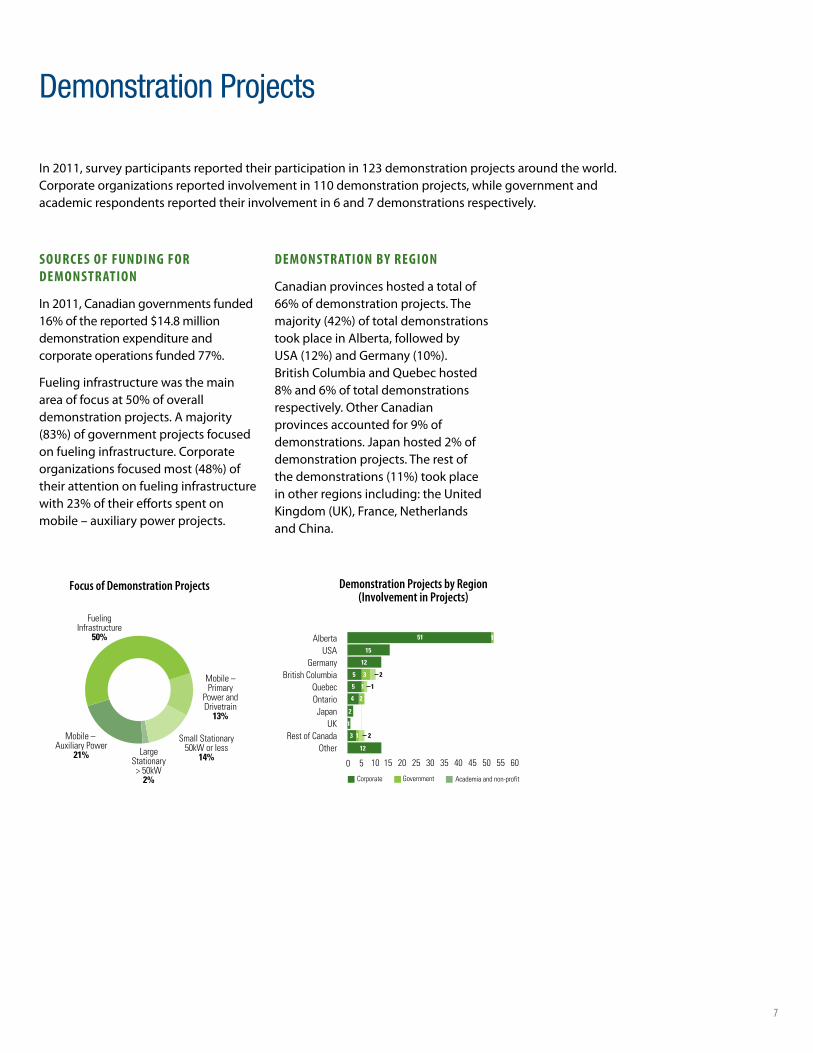

In 2011, Canadian governments funded 16%ofthereported$14.8 milliondemonstration expenditure and corporateoperationsfunded77%.

Fueling infrastructure was the main areaoffocusat50%ofoveralldemonstrationprojects.Amajority(83%)ofgovernmentprojectsfocusedon fueling infrastructure. Corporate organizationsfocusedmost(48%)oftheir attention on fueling infrastructure with23%oftheireffortsspentonmobile–auxiliarypowerprojects.

demOnstRatiOn by RegiOn

Canadian provinces hosted a total of 66%ofdemonstrationprojects.Themajority(42%)oftotaldemonstrationstook place in Alberta, followed by USA(12%)andGermany(10%).British Columbia and Quebec hosted 8%and6%oftotaldemonstrationsrespectively. Other Canadian provincesaccountedfor9%ofdemonstrations.Japanhosted2%ofdemonstrationprojects.Therestofthedemonstrations(11%)tookplacein other regions including: the United Kingdom (UK), France, Netherlands and China.

Demonstration Projects

Private company40%

Public company15%Division/subsidiary

of public company8%

Governmentorganizations

18%

Educationorganization

18%

Non-profit organization incl. associations

1%

p. 2 Organization Type

Apr 2012

Not provided15%

> 20 years18%

11 – 20 years33%

5 – 10 years26%

< 5 years8%

p.2 Years of Involvement in Hydrogen and Fuel Cell Activities

Mobile –Auxiliary Power

5%

Mobile – Primary Power and Drivetrain

24%

Portable(including

micro)11%

Small Stationary 50kW or less

19%

Large Stationary > 50kW

14%HydrogenProduction

and Fueling Infrastructure

27%

p.3 Market Focus

Rest of World7%

Rest of Canada15%

Ontario18%

Quebec9%

Alberta6%

British Columbia22%

USA8%

p.3 Hydrogen and Fuel Cell Facilities by Region

Provision of services

37%

Product sales59%

Canadian government supportrecognized as revenue

1%

p.4 Revenue by Category

Small Stationary50kW or less

14%LargeStationary

> 50kW2%

Mobile –Primary

Power andDrivetrain

13%

Mobile – Auxiliary Power

21%

FuelingInfrastructure

50%

p.7 Focus of Demonstration Projects

Rest of Canada 4%USA5%

Quebec9%

Asia2%

Rest of Europe 6%

British Columbia58%

Ontario13%

p.8 Employment by Region

Government9%

Academia andnon-profit

15%

Corporate76%

p.8 Employment by Organization

Remain the same (+/-5%)

52%

Significant increase(greater than 15%

of current employees)17%

Increase(between 5%

and 15%)23%

p.11 Plans to change employment in the next 18 months

Government13%

Private equity19%

Other10%

Angel Investors4%

Operations52%

p.9 Sources of Funding - Corporate

A-Base15%

Programs85%

p.9 Sources of Funding - Government

Other non-profitorganization

37%

NSERC/Canadian Foundation for Innovation

13%

Other 50%

p.9 Sources of Funding – Academia and Non-Profit

Other OEM13%

Public-privatepartnerships

26%

Hydrogen andfuel cell companies

26%

EnergyProviders

11%

Other 7%

p.10 Strategic Alliances

Declined3%

No reply40%

Completed survey57%

p.10 Profile participation rate

Technicians2%

Academic/research staff

26%

Undergraduatestudents

including coop13%

Canadian graduate andpostgraduate students

46%

International graduate andpostgraduate students

13%

p.6 People Involved in Research

USA25%Germany

30%

Asia 4%

Rest of world 5%

BritishColumbia

27%Ontario 1%

Rest of Canada1%Rest of

Europe7%

p.6 R&D by region

British Columbia77%

Rest of the world5%

Ontario10%

Quebec 3%Germany 3%

USA 1%

p.4 Revenue by Region

R&DIn-house

48%

p.9 Funding Allocation by Area - Gov’t & Academia & Non-profit

R&DIntramural

35%

Marketing andbusiness development

1%Education,

safety and training5%

Policy development1%

Monitoringand reporting

1%

Demonstrationand pilot projects

9%

Europe11%

Other 3%

Germany 3%

Significantly decrease (greater than 15%)

3%Decrease

(between 5 and 15%)5%

Japan 1%

Japan4%

Automotive OEM17%

Public capital markets2%

Focus of Demonstration Projects

Access to markets

Lack of funding

Technology development

p.2 Areas of Expertise

p.3 Technology Focus

p.4 Total Revenue ($ millions)

Hydrogen production

Research organization

Policy development andprogram administration

Fuel cell user

Professional services provider

Hydrogen distribution

Fuel cell developer or manufacturer

5 10 15 20 250

Other

Systems integrator

Education, safety and training

Commercialization support

Supplier to developer or manufacturer

Hydrogen storage

Fuel cell distributor or agent

22%

12%

12%

9%

8%

7%

6%

5%

4%

3%

3%

2%

2%

3%

0 5 10 15 20 25 30 35 40 45

Proton Exchange Membrane

Solid Oxide Fuel Cells

Hydrogen Production

Hydrogen Distribution

Hydrogen Storage

Metal-Air

Molten Carbonate

Direct Liquid

Other

1%

7%

7%

37%

8%

2%

2%

14%

20%

0

50

100

150

200

250

2008

p.8 Employment

28. Growth since 2001

1,500

1,000

0

2,500

2006

2007 20092006

2007 2008 2010

0

50

100

150

200

250

300

2005 2006 2007 201020042003200220010

500

1,000

1,500

2,000

2,500

3,000

R&DRevenue Employees

$

p.7 Patents

200

100

0

300

400

235

351

Alberta

Canadian government (all levels)

Corporate operations

Parent, affiliatedor subsidiary

Research, non-profit,non-governmental institute

Contract work conductedfor another institute

0 20 40 60 80 100

12. Sources of Funding for R&D Expenditure by Organization

23%

68%

7%

7%

9%

Foreign government

University oracademic institute

1%

3%

14%

0% 20% 40% 60% 80% 100%

100%61%

GovernmentCorporate Academic and non-profit

290

179

134

276

188

97

133 135 133

177

128

2011

215

142

Feb 2011

Patentsapproved

Patentspending

p.11 Priorities to enhance competitive performance in 2012

0 5 10 15 20 25

Collaboration/strategic alliances

Gain market share

Better targetingof customers

Improving processes

Better marketor customer data

Plans for expansion(new products/new markets)

Other

Outsourcing

8%

1%

8%

21%

8%

Reduce costof operations

7%

6%

19%

12%

10%

p.? challenges faced in 2010

0% 5 10 15 20 25 30

Profitability

Economy

Exchange rates

6%

31%

6%

Other 9%

24%

10%

10%

GermanyUSA

British ColumbiaQuebecOntario

0 5 10 15 20 25 30 35 40 45 50 55 60

16. Demonstration Projects by Region (Number of Projects)

51

Other

GovernmentCorporate Academia and non-profit

%

%

%

Millions Employees

Utility 2%

Direct Methanol 2%

2,000

500

2009

2,001 1,9912,043

1,7651,556

2,025

2011

2010 2011

Competition 4%

Labour shortages

15

12

5

5

4 2

2

1

1

1

12

JapanUK

Rest of Canada

184

136

2008 2009

194

1

1

23

23

195

215 211

133

194

168

237

218211

168

195

211

Demonstration Projects by Region (Involvement in Projects)

In2011,surveyparticipantsreportedtheirparticipationin123demonstrationprojectsaroundtheworld.Corporateorganizationsreportedinvolvementin110demonstrationprojects,whilegovernmentandacademicrespondentsreportedtheirinvolvementin6and7demonstrationsrespectively.

8

Surveyparticipantsreportedatotalof2,025employeesinvolvedinhydrogenandfuelcellactivitiesin2011.Thisisanearly2%increasefrom1,991employeesreportedin2010anda30%increasefromlevelsreportedduringtherecessionin2008.Surveyparticipantsonlyprovidedabreakdownbyregionfor1,625ofthe2,025employees.

In2011,thelargestproportion(approximately84%)ofindustryemployeeswaslocatedinCanada,5%intheUnitedStates,andtheremaining11%overseasintheUK,France,Denmark,Belgium,Germany,ChinaandSingapore.InCanada,mostemployeeswerelocatedinBritishColumbia(952),followedbyOntario(210)andQuebec(143)withtheremaining64employeesdistributedacrossCanada.

54%ofcompaniessurveyedhadfewerthan10employees,20%had10to25employees,11%hadbetween25and50,and15%hadmorethan50employees.

Based on the data provided for the number of employees and total salaries, theaverageannualsalarypaidtoemployeeswas$57,180.Extrapolatingtheaveragesalaryfor2011tothe1,369employeesinCanada,thesectorcontributedapproximately$78.3millionindirectsalariestothenationaleconomy.

Employment

Access to markets

Lack of funding

Technology development

p.2 Areas of Expertise

p.3 Technology Focus

p.4 Total Revenue ($ millions)

Hydrogen production

Research organization

Policy development andprogram administration

Fuel cell user

Professional services provider

Hydrogen distribution

Fuel cell developer or manufacturer

5 10 15 20 250

Other

Systems integrator

Education, safety and training

Commercialization support

Supplier to developer or manufacturer

Hydrogen storage

Fuel cell distributor or agent

22%

12%

12%

9%

8%

7%

6%

5%

4%

3%

3%

2%

2%

3%

0 5 10 15 20 25 30 35 40 45

Proton Exchange Membrane

Solid Oxide Fuel Cells

Hydrogen Production

Hydrogen Distribution

Hydrogen Storage

Metal-Air

Molten Carbonate

Direct Liquid

Other

1%

7%

7%

37%

8%

2%

2%

14%

20%

0

50

100

150

200

250

2008

p.8 Employment

28. Growth since 2001

1,500

1,000

0

2,500

2006

2007 20092006

2007 2008 2010

0

50

100

150

200

250

300

2005 2006 2007 201020042003200220010

500

1,000

1,500

2,000

2,500

3,000

R&DRevenue Employees

$

p.7 Patents

200

100

0

300

400

235

351

Alberta

Canadian government (all levels)

Corporate operations

Parent, affiliatedor subsidiary

Research, non-profit,non-governmental institute

Contract work conductedfor another institute

0 20 40 60 80 100

12. Sources of Funding for R&D Expenditure by Organization

23%

68%

7%

7%

9%

Foreign government

University oracademic institute

1%

3%

14%

0% 20% 40% 60% 80% 100%

100%61%

GovernmentCorporate Academic and non-profit

290

179

134

276

188

97

133 135 133

177

128

2011

215

142

Feb 2011

Patentsapproved

Patentspending

p.11 Priorities to enhance competitive performance in 2012

0 5 10 15 20 25

Collaboration/strategic alliances

Gain market share

Better targetingof customers

Improving processes

Better marketor customer data

Plans for expansion(new products/new markets)

Other

Outsourcing

8%

1%

8%

21%

8%

Reduce costof operations

7%

6%

19%

12%

10%

p.? challenges faced in 2010

0% 5 10 15 20 25 30

Profitability

Economy

Exchange rates

6%

31%

6%

Other 9%

24%

10%

10%

GermanyUSA

British ColumbiaQuebecOntario

0 5 10 15 20 25 30 35 40 45 50 55 60

16. Demonstration Projects by Region (Number of Projects)

51

Other

GovernmentCorporate Academia and non-profit

%

%

%

Millions Employees

Utility 2%

Direct Methanol 2%

2,000

500

2009

2,001 1,9912,043

1,7651,556

2,025

2011

2010 2011

Competition 4%

Labour shortages

15

12

5

5

4 2

2

1

1

1

12

JapanUK

Rest of Canada

184

136

2008 2009

194

1

1

23

23

195

215 211

133

194

168

237

218211

168

195

211

EmploymentEmployment by Region

Private company40%

Public company15%Division/subsidiary

of public company8%

Governmentorganizations

18%

Educationorganization

18%

Non-profit organization incl. associations

1%

p. 2 Organization Type

Apr 2012

Not provided15%

> 20 years18%

11 – 20 years33%

5 – 10 years26%

< 5 years8%

p.2 Years of Involvement in Hydrogen and Fuel Cell Activities

Mobile –Auxiliary Power

5%

Mobile – Primary Power and Drivetrain

24%

Portable(including

micro)11%

Small Stationary 50kW or less

19%

Large Stationary > 50kW

14%HydrogenProduction

and Fueling Infrastructure

27%

p.3 Market Focus

Rest of World7%

Rest of Canada15%

Ontario18%

Quebec9%

Alberta6%

British Columbia22%

USA8%

p.3 Hydrogen and Fuel Cell Facilities by Region

Provision of services

37%

Product sales59%

Canadian government supportrecognized as revenue

1%

p.4 Revenue by Category

Small Stationary50kW or less

14%LargeStationary

> 50kW2%

Mobile –Primary

Power andDrivetrain

13%

Mobile – Auxiliary Power

21%

FuelingInfrastructure

50%

p.7 Focus of Demonstration Projects

Rest of Canada 4%USA5%

Quebec9%

Asia2%

Rest of Europe 6%

British Columbia58%

Ontario13%

p.8 Employment by Region

Government9%

Academia andnon-profit

15%

Corporate76%

p.8 Employment by Organization

Remain the same (+/-5%)

52%

Significant increase(greater than 15%

of current employees)17%

Increase(between 5%

and 15%)23%

p.11 Plans to change employment in the next 18 months

Government13%

Private equity19%

Other10%

Angel Investors4%

Operations52%

p.9 Sources of Funding - Corporate

A-Base15%

Programs85%

p.9 Sources of Funding - Government

Other non-profitorganization

37%

NSERC/Canadian Foundation for Innovation

13%

Other 50%

p.9 Sources of Funding – Academia and Non-Profit

Other OEM13%

Public-privatepartnerships

26%

Hydrogen andfuel cell companies

26%

EnergyProviders

11%

Other 7%

p.10 Strategic Alliances

Declined3%

No reply40%

Completed survey57%

p.10 Profile participation rate

Technicians2%

Academic/research staff

26%

Undergraduatestudents

including coop13%

Canadian graduate andpostgraduate students

46%

International graduate andpostgraduate students

13%

p.6 People Involved in Research

USA25%Germany

30%

Asia 4%

Rest of world 5%

BritishColumbia

27%Ontario 1%

Rest of Canada1%Rest of

Europe7%

p.6 R&D by region

British Columbia77%

Rest of the world5%

Ontario10%

Quebec 3%Germany 3%

USA 1%

p.4 Revenue by Region

R&DIn-house

48%

p.9 Funding Allocation by Area - Gov’t & Academia & Non-profit

R&DIntramural

35%

Marketing andbusiness development

1%Education,

safety and training5%

Policy development1%

Monitoringand reporting

1%

Demonstrationand pilot projects

9%

Europe11%

Other 3%

Germany 3%

Significantly decrease (greater than 15%)

3%Decrease

(between 5 and 15%)5%

Japan 1%

Japan4%

Automotive OEM17%

Public capital markets2%

Private company40%

Public company15%Division/subsidiary

of public company8%

Governmentorganizations