Canada’s 88(1)(d) Tax Cost Bump: A ... - Mining Tax Canada

23

Canada’s 88(1)(d) Tax Cost Bump: A Guide for Foreign Purchasers by Steve Suarez Reprinted from Tax Notes Int’l, December 9, 2013, p. 957 Volume 72, Number 10 December 9, 2013 (C) Tax Analysts 2013. All rights reserved. Tax Analysts does not claim copyright in any public domain or third party content.

Transcript of Canada’s 88(1)(d) Tax Cost Bump: A ... - Mining Tax Canada

Canada’s 88(1)(d) Tax Cost Bump:A Guide for Foreign Purchasers

by Steve Suarez

Reprinted from Tax Notes Int’l, December 9, 2013, p. 957

Volume 72, Number 10 December 9, 2013

(C)

TaxA

nalysts2013.A

llrightsreserved.

TaxA

nalystsdoes

notclaim

copyrightin

anypublic

domain

orthird

partycontent.

Canada’s 88(1)(d) Tax Cost Bump: A Guide for ForeignPurchasersby Steve Suarez

The increase (or bump) in the cost of property per-mitted under paragraph 88(1)(d) of the Income

Tax Act (Canada) is one of the most powerful andcomplex tax planning tools in the Canadian incometax system. Commonly known as the 88(1)(d) bump,this cost basis increase reduces or completely elimi-nates accrued gains that would otherwise be taxed on adisposition of property. It is particularly relevant toforeign purchasers of Canadian corporations, althoughit is often unavailable to those foreign purchasers intransactions in which something other than money(that is, shares or other securities of the foreign pur-chaser) is used to pay for the acquisition. This articlegives the reader an understanding of the basic param-eters of the 88(1)(d) bump: the intent behind the provi-sion, when it can be used, its most common applica-tions, and its major limitations.

I. Overview of the 88(1)(d) Bump

Most taxation systems record the amount paid by ataxpayer to acquire a property as the taxpayer’s cost ofthe property for tax purposes (tax cost), which may ormay not correspond to its cost for accounting purposes.When the property is disposed of, any sale proceedsthe taxpayer receives (or is deemed to receive) are meas-ured against the taxpayer’s tax cost of the property todetermine whether the taxpayer has realized a gain ora loss. The benefit of the 88(1)(d) bump is to increasethe tax cost of property and thus reduce or eliminatethe amount of any gain realized on a future dispositionof that property.

The 88(1)(d) bump is available only in one specificsituation: when one taxable Canadian corporation (the

parent) owning all the shares of another taxable Cana-dian corporation (the subsidiary) causes the subsidiaryto wind up or merge into the parent. Such a wind-upor merger is referred to herein as the wind-up. Thegeneral rule in the ITA on wind-ups is that the parentacquires all the subsidiary’s property at whatever taxcost the subsidiary had in that property without anygain or loss being realized on the wind-up:1 that is, theparent steps into the shoes of the subsidiary, inheritingany accrued gains or losses.

When applicable, however, the 88(1)(d) bump allowsthe parent to increase the tax cost of certain propertyacquired from the subsidiary on the wind-up, poten-tially up to an amount equal to the property’s fair mar-ket value as of the time the parent acquired control ofthe subsidiary. This opportunity arises when the par-ent’s tax cost of its shares in the subsidiary (sometimescalled the outside basis) is greater than the subsidiary’saggregate net tax cost of all of its property (inside ba-sis). On a wind-up, the parent’s outside basis is elimi-nated when its subsidiary shares are canceled. Withoutan 88(1)(d) bump, if the outside basis exceeds the sub-sidiary’s inside basis, the parent simply loses the excessbasis and is disadvantaged by the wind-up in terms oflost tax cost.2 The 88(1)(d) bump effectively permits the

1Subsection 88(1) of the ITA. These rules also provide thatthe parent’s shares in the subsidiary disappear generally withoutany gain or loss realized.

2There are many reasons why the parent may wish to mergewith the subsidiary, including to consolidate the parent’s ex-penses (for example, interest and other financing charges) with

Steve Suarez is with Borden Ladner Gervais LLP in Toronto.

The author acknowledges with appreciation the assistance of Stephanie Wong in updating this article.

(Footnote continued on next page.)

TAX NOTES INTERNATIONAL DECEMBER 9, 2013 • 935

(C) T

ax Analysts 2013. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

parent to apply some of its excess outside basis to in-crease the tax cost of the eligible subsidiary assets ac-quired on the wind-up, and thus mitigates what couldotherwise be an unfavorable tax consequence of awind-up.

Figure 1 illustrates the basic result of the 88(1)(d)bump. A Canadian corporation (CanAcquireCo) pur-chases all the shares of another Canadian corporation(CanCo) from an unrelated third party for $100, whichrepresents CanAcquireCo’s tax cost of its CanCoshares. CanCo owns property eligible for the 88(1)(d)bump (eligible property), as well as other property thatis not eligible for the increase. Immediately before theacquisition, CanCo’s eligible property has an FMV of$60 and a tax cost of $20 (an accrued gain of $40).Following the acquisition, CanAcquireCo winds upCanCo, acquiring its property. Ordinarily, CanAcquire-Co’s $100 tax cost would disappear on the wind-upand its tax cost of the acquired property would be thesame as CanCo’s tax cost ($20 and $30, respectively).Subject to various limitations, the 88(1)(d) bump allowsCanAcquireCo to increase its tax cost of the eligibleproperty up to an amount not exceeding its FMV($60), reducing or eliminating the accrued gain.

II. Applications of the 88(1)(d) BumpThe benefit of increased tax cost in eligible property

is realized only when the property is disposed of, re-ducing any gain otherwise recognized. Consequently,the benefit of the 88(1)(d) bump in any particular casedepends on the facts of the situation — that is, the sizeof any accrued gain on eligible property, and how soona disposition is likely to occur.

A. Sale to Third PartyCanAcquireCo may intend to sell some of CanCo’s

eligible property to a third party as quickly as possiblefollowing its acquisition of the CanCo shares. It maynot want to keep some of CanCo’s eligible propertythat it views as being non-core assets or outside thescope of management’s ability to effectively administer.CanAcquireCo may need to sell some of CanCo’sproperty to finance the purchase of CanCo.3 Acquirersmay also find that antitrust laws require them to divestsome of the property owned by a corporation theyhave acquired in order to preserve competition withinan industry. In any of these circumstances, the 88(1)(d)bump will be of immediate benefit and may be essen-tial to completing the acquisition.

B. Internal ReorganizationEven when no third-party disposition is planned, the

88(1)(d) bump may be of immediate benefit. In cross-border takeovers, it is common for Canadian target cor-porations to have foreign subsidiaries in other coun-tries. It is generally not tax efficient for a foreignacquirer to hold those foreign subsidiaries through aCanadian entity, since in those circumstances the re-sulting sandwich structure creates an extra taxing juris-diction:

• whose controlled foreign corporation rules mustbe managed;

• which will potentially seek to tax any future ac-crued gains; and

• through which dividends and other amounts mayneed to flow in order to redeploy funds within thegroup.

the subsidiary’s income for tax purposes. Canada does not havea group relief or consolidation tax system. The government wasexamining possible new rules for the taxation of corporategroups, but it announced in its 2013 federal budget that ‘‘movingto a formal system of corporate group taxation is not a priorityat this time.’’

3An example of this is the 2005 agreement between BarrickGold Corp. and Goldcorp Inc., in which Barrick’s takeover bidfor Placer Dome Inc. was based on Barrick’s selling to Goldcorpover $1 billion of property owned by Placer and acquired by Bar-rick following the successful completion of the takeover in early2006.

Table 1. 88(1)(d) Bump Summary• Applicable only when a wholly owned taxable Canadian corporation (subsidiary) winds up or merges into

its parent taxable Canadian corporation (parent) on a tax-deferred basis.• Permits the parent to push down its cost basis in its subsidiary shares into cost basis of eligible nondepreciable

capital property acquired from the subsidiary upon wind-up or merger.• Reduces or eliminates capital gains otherwise realized when the parent disposes of property acquired from its

subsidiary (for example, on completing a third-party sale, reorganizing an internal group, or managing newforeign affiliate dumping rules).

• Cost basis of property cannot be increased above its fair market value at the time the parent acquired controlof subsidiary.

• May be optimized by planning undertaken by the subsidiary before the parent acquires control of the sub-sidiary (that is, pre-closing planning on a friendly acquisition).

• No 88(1)(d) bump allowed on any property if former subsidiary shareholders (or non-arm’s-length persons)acquire prohibited property as part of the relevant series of transactions.

SPECIAL REPORTS

936 • DECEMBER 9, 2013 TAX NOTES INTERNATIONAL

(C) T

ax Analysts 2013. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

The 88(1)(d) bump makes it possible to move thesubsidiary’s foreign affiliates out from under the Cana-dian tax system without incurring Canadian capitalgains tax.

Returning to the example in Figure 1, if CanCoowns shares of foreign affiliates with significant ac-crued gains, such shares are generally eligible propertyand the 88(1)(d) bump can eliminate those gains forCanadian tax purposes, allowing those shares to bedistributed out of Canada to the foreign acquirer with-out realizing any capital gains in Canada. Consider, forexample, the fact pattern in Figure 2, in which the for-eign acquirer (U.S. Parent) has created CanAcquireCoand funded it with $100 to purchase all the shares ofCanCo.4 Following the wind-up of CanCo, CanAc-quireCo can use the 88(1)(d) bump to increase the taxcost of CanCo’s U.S. subsidiary (U.S. SubCo) up to$60, eliminating the accrued gain. CanAcquireCo canthen distribute the U.S. SubCo shares to U.S. Parent byeffecting a return of capital for Canadian corporate lawpurposes (that is, not a dividend). As long as theamount of the distribution ($60) does not exceed thetax cost and the paid-up capital (PUC)5 of U.S. Par-ent’s shares of CanAcquireCo ($100), no capital gain

or dividend arises for Canadian tax purposes and theamount of the distribution reduces these tax attributes(to $40). The adverse tax implications of a sandwichstructure are thereby avoided using the 88(1)(d) bump.

The introduction of the foreign affiliate dumping(FAD) rules in 20126 makes the 88(1)(d) bump moreimportant than ever to foreign purchasers. The FADrules create significant adverse (and ongoing) Canadiantax consequences for foreign-controlled Canadian cor-porations with foreign subsidiaries, and they effectivelyencourage Canadian group members to dispose of ex-isting foreign affiliates whenever possible. Amendmentsmade to the version of the FAD rules enacted in late2012 facilitate the use of the 88(1)(d) bump in thesecircumstances, and when the 88(1)(d) bump is availableto reduce or eliminate Canadian CGT on shares offoreign affiliates (and there are no tax impediments inthe foreign affiliate’s home country), it will generallybe the primary tool used by foreign purchasers of a

4Foreign purchasers of Canadian corporations usually struc-ture acquisitions through a Canadian purchaser corporation for avariety of tax and nontax reasons, including access to the88(1)(d) bump.

5PUC represents amounts received by a corporation on theissuance of its shares, and it is essentially the tax version of thecorporate law concept of share capital. In this example, in which

U.S. Parent delivers $100 to CanAcquireCo in exchange for Can-AcquireCo shares to fund its purchase of CanCo shares, the taxcost and (subject to the foreign affiliate dumping rules) the PUCof the CanAcquireCo shares issued will be $100. Unlike in manyother countries, including the United States, a distribution madeby CanAcquireCo as a return of capital on its shares will not betreated as a dividend as long as it does not exceed the PUC ofthose shares: In Canada there is no concept of corporate distri-butions being deemed to come first out of earnings and profits.

6See Steve Suarez, ‘‘New Foreign Affiliate ‘Dumping’ RulesConstitute Major Canadian Tax Policy Change,’’ Tax Notes Int’l,Dec. 17, 2012, p. 1145.

Figure 1. Basic Bump Transaction

1. Acquisition of CanCo 2. Wind-Up of CanCo

Seller

$100

Seller CanAcquireCo(Parent)

Tax cost = $100FMV = $100

Tax cost = $20FMV = $60

Tax cost = $30FMV = $40

EligibleProperty

OtherProperty

CanAcquireCo

CanCo(Subsidiary)

CanCo

EligibleProperty

OtherProperty

Tax cost/FMV = $60

Tax cost = $30FMV = $40

SPECIAL REPORTS

(Footnote continued in next column.)

TAX NOTES INTERNATIONAL DECEMBER 9, 2013 • 937

(C) T

ax Analysts 2013. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

Canadian corporation that owns foreign subsidiaries toavoid having to contend with the FAD rules on an on-going basis.

There are other potential applications of the 88(1)(d)bump that are beyond the scope of this discussion, butthe foregoing examples illustrate the potential of thisprovision.

III. Qualifications and RestrictionsWhile the 88(1)(d) bump rules are complex and

technical, at a conceptual level they can be brokendown into four core requirements, as illustrated in Fig-ure 3:

• Qualifying Wind-Up or Amalgamation. The 88(1)(d)bump arises only on a wind-up or amalgamationof one taxable Canadian corporation into anotherthat meets certain requirements.

• Determination of Eligible Property. Not all propertyis eligible for the 88(1)(d) bump; there are rulesgoverning which items are eligible properties.

• Calculation of Maximum Bump. There are limits onthe amount that the tax cost of any eligible prop-erty can be increased, and on the overall increasein the tax cost of all the subsidiary’s eligible prop-erties.

• Compliance With Bump Denial Rule. There is anoverarching ‘‘bump denial’’ rule that if contra-vened, completely eliminates any 88(1)(d) bumpfor all property of the subsidiary. This technicaland complex requirement can deny an 88(1)(d)bump even when there is no clear tax policy basis

for doing so. Among its other consequences, thisrule generally forces foreign acquirers wanting touse the 88(1)(d) bump to structure acquisitions sothat either (1) the shareholders of the Canadiantarget corporation receive exclusively cash in ex-change for their shares, or (2) the foreign acquireris so much larger than the Canadian target corpo-ration that post-acquisition, the Canadian targetcorporation will represent no more than 10 per-cent of the foreign acquirer’s equity value.

Before discussing these four requirements in greaterdetail, it is useful to briefly review a few core conceptsthat recur throughout the 88(1)(d) bump rules.

A. Related PersonsAn important element of the 88(1)(d) bump is the

concept of related persons. A natural person is relatedto his spouse and blood relatives (children, parents, andsiblings). A corporation is related to a shareholder whocontrols it and to any person related to that controllingshareholder. Two corporations are related if one con-trols the other, if both are controlled by the same per-son, or if each is controlled by a person or group ofpersons that is related to the other’s controlling share-holder or group of shareholders.7 The term ‘‘control’’generally means ownership of enough shares to elect amajority of the corporation’s board of directors. Inmost cases, that means shares that command a major-ity of the votes attributable to all the corporation’s

7Subsection 251(2) of the ITA.

Figure 2. Foreign Subsidiary Extraction

1. Post-CanCo Wind-Up and Bump

U.S. Parent

Tax cost = $100FMV/PUC = $100

Tax cost/FMV = $60

Tax cost = $30FMV = $40

U.S. SubCoOther

Property

CanAcquireCo(Parent)

Tax cost/FMV = $60

Tax cost = $40FMV/PUC = $40

U.S. SubCo

OtherProperty

U.S. Parent

CanAcquireCo

Tax cost = $30FMV = $40

2. CanAcquireCo Capital Return

SPECIAL REPORTS

938 • DECEMBER 9, 2013 TAX NOTES INTERNATIONAL

(C) T

ax Analysts 2013. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

shares. The test is one of de jure or legal control,rather than de facto control. In some cases, for pur-poses of determining whether persons are related, con-trol is determined not only with reference to sharesowned but also to any rights a person may have to ac-quire shares or control how they are voted (251(5)(b)rights).8

B. Non-Arm’s-Length PersonsAnother key concept is that of persons not dealing

at arm’s length. If two persons are related (see above),they are deemed to be non-arm’s-length (NAL). If theyare not related, it is a factual question whether theydeal at arm’s length.9 Unrelated persons can be consid-ered NAL if one exercises sufficient control or influ-ence over the other, or if both are subject to commoncontrol such that they are acting in concert or cannotbe considered to have separate interests. An example ofhow unrelated persons could be considered to be NALmight be a 40 percent shareholder of a public corpora-tion who has de facto control, but not legal control, ofthe corporation because the other 60 percent is widelyheld, meaning the 40 percent shareholder will usuallybe able to control selection of the directors.

C. Acquisition of ControlVarious aspects of the 88(1)(d) bump rules are pre-

mised on the time of the parent’s acquisition of con-

trol (AOC) of the subsidiary. For these purposes, a per-son is generally considered to acquire control of acorporation when it obtains ownership of enoughshares to elect a majority of the corporation’s board ofdirectors. A special provision in the 88(1)(d) bumprules states that for most purposes of these rules, if theparent acquires control of the subsidiary from anotherperson that is NAL with the parent, the parent isdeemed to have acquired control at the earlier timewhen the NAL person acquired control of the subsidi-ary.10

D. Series of Transactions

Some of the 88(1)(d) bump rules refer to the ‘‘seriesof transactions’’ that includes the parent’s AOC of thesubsidiary (the AOC series). While the degree of con-nection necessary to make two events part of the sameseries of transactions is unclear, both the Canada Rev-enue Agency and the jurisprudence to date have inter-preted the term rather broadly.

The determination of what constitutes a series oftransactions involves the common-law definition of theterm ‘‘series of transactions,’’ which has been held tomean transactions that are ‘‘preordained in order toproduce a given result’’ with ‘‘no practical likelihoodthat the pre-planned events would not take place in the

8Para. 251(5)(b) of the ITA.9Subsection 251(1) of the ITA. The arm’s-length concept was

discussed by Stacey Long in ‘‘Canadian Courts Consider Arm’s-Length Dealings,’’ Tax Notes Int’l, Sept. 18, 2006, p. 987.

10Para. 88(1)(d.2) of the ITA. This deeming rule can affectother relevant rules (see, e.g., the discussion associated with note20, infra).

Figure 3. Bump Overview: Summary of Bump Analysis

qualifyingwind-up ofsubsidiaryinto parent?

YesDoes bumpdenial ruleapply?

NoDeterminewhich propertyis bump-eligible

Determineamount ofbump

YesNo

No bumpavailable

No bumpavailable

Exclude:• non-capital property

• depreciable property

• property received on abutterfly

• property caught by anti-stuffing rule

• property not meetingsubsidiary ownershiprequirement

Aggregate limit is tax cost of subsidiary sharesminus (1) cost amount of subsidiary’s propertyand cash less subsidiary’s debts, and (2)subsidiary dividends to parent

Individual property bump limitations:• ACB of property cannot be increased above

its FMV at time of wind-up

• Special limitations for partnership interestsand shares of foreign affiliates

Is there a

SPECIAL REPORTS

TAX NOTES INTERNATIONAL DECEMBER 9, 2013 • 939

(C) T

ax Analysts 2013. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

order ordained.’’11 Subsection 248(10) of the ITA ex-tends the scope of the term to include related transac-tions or events completed ‘‘in contemplation of ’’ thecommon law series. The Supreme Court of Canadahas taken a fairly expansive view of this extendedmeaning of the phrase ‘‘series of transactions,’’ holdingthat a transaction completed ‘‘in contemplation of ’’ aseries of transactions can include a transaction occur-ring either before or after the rest of the series — thatis, the test ‘‘allows either prospective or retrospectiveconnection of a related transaction to a common lawseries.’’12

Further, a ‘‘strong nexus’’ between a transaction andthe series is not necessary to satisfy the test, althoughthe test requires more than a ‘‘mere possibility’’ or aconnection with ‘‘an extreme degree of remoteness,’’and each case must be decided on its own facts.13 TheSupreme Court noted that relevant facts could includethe occurrence of intervening events or the passage oftime between the series and the related transaction.

Based on the jurisprudence to date, it does not ap-pear possible to conclude that a transaction is not partof the same series of transactions that includes othertransactions simply because at the time of the firsttransaction, the other transactions were not anticipated.However, when two transactions are unconnected inthe sense of neither affecting the decision to undertakethe other (or the objectives of the other), it seems un-likely a court would conclude they form part of thesame series.

For ease of reference, Table 2 contains a glossary ofmany of the relevant terms used herein.

IV. Qualifying Wind-Up or Amalgamation

As noted above, the 88(1)(d) bump is available onlyon the wind-up or amalgamation of one taxable Cana-dian corporation into another. A wind-up in this senseis the voluntary dissolution of a corporation, with itsproperty distributed to its shareholders. An amalgama-tion is the merger of two corporations to form a singleentity. A qualifying amalgamation for 88(1)(d) bumppurposes requires that the parent acquire all the prop-erty and assume all the liabilities of the subsidiary,other than any shares of one owned by the other orliabilities owed by one to the other.14 In an 88(1)(d)context, an amalgamation also requires that all the sub-sidiary’s shares be canceled. Amalgamations are gener-ally faster and easier to carry out than wind-ups, and

so are seen much more frequently. In either case, theparent must own all the shares of the subsidiary imme-diately before that time.15

V. Determination of Eligible Property

It is important in any wind-up to identify whichproperties are eligible for the 88(1)(d) bump. There area number of rules governing what constitutes eligibleproperty.

A. Nondepreciable Capital Property

Canadian tax law distinguishes between capitalproperty and all other property. While the determina-tion is highly judgmental, in general terms, capitalproperty is acquired for the purpose of producing in-come from holding or using it (for example, productionequipment) as opposed to property held for resale (in-ventory). The concept of capital property is similar butnot identical to the accounting principle of a capital

11OSFC Holdings Ltd. v. The Queen, 2001 DTC 5471 (FCA).This formulation was endorsed by the Supreme Court of Canadain Canada Trustco Mortgage v. Canada, 2005 SCC 54 (SCC).

12Copthorne Holdings Ltd. v. The Queen, 2011 DTC 5007 (SCC),at para. 56.

13Id. at para. 47.14Subsection 87(11) and (1) of the ITA.

15For a wind-up (but not an amalgamation), the parent mustown at least 90 percent of the outstanding shares of each classof the subsidiary’s shares, with any other shares being owned bypersons dealing at arm’s length with the parent (subsection 88(1)of the ITA). Practically, however, in almost all qualifying wind-ups, the parent owns all of the shares of the subsidiary.

Table 2. Glossary

88(1)(d) bump Increase in tax cost of eligible propertypermitted under section 88(1)(d) of the ITA

Parent Taxable Canadian corporation claiming the88(1)(d) bump

Subsidiary Taxable Canadian corporation that ownseligible property

Wind-up The wind-up or merger of the subsidiaryinto the parent

Eligible property Property that is eligible for the 88(1)(d)bump

Distributedproperty

Property owned by the subsidiary that isacquired by the parent on the wind-up

AOC Acquisition of control of the subsidiary bythe parent

AOC series The series of transactions that includes theAOC

Tax cost Cost basis of property to the owner for taxpurposes

FMV Fair market value

NAL Non-arm’s-length (related persons aredeemed to deal at NAL)

SPECIAL REPORTS

940 • DECEMBER 9, 2013 TAX NOTES INTERNATIONAL

(C) T

ax Analysts 2013. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

asset. The most common forms of capital property in-clude land, buildings, and machinery and equipment,as well as investment securities (corporate shares orinterests in a partnership or trust).16

Some capital property is eligible for an annual de-duction from income for tax purposes corresponding tothe accounting concept of depreciation — that is, taxcost is deducted from income over a period of years.Such depreciable property, which includes most build-ings and machinery and equipment, is not eligible forthe 88(1)(d) bump.17 Only nondepreciable capital prop-erty can be eligible property. In most cases, this re-stricts eligible property to land, shares of corporations,and interests in partnerships or trusts.

B. Owned by Subsidiary and Held Until Wind-Up

Eligible property is limited to property directlyowned by the subsidiary at the time of the AOC andheld continuously thereafter until the time of the wind-up.18 This means that a snapshot is taken of whatproperty the subsidiary directly owns at the time of theAOC, and only that property can qualify.19 There is nolook-through or consolidation concept that allowsproperty owned by another entity in which the subsidi-ary has an interest to become the subject of an 88(1)(d)bump. However, if property that would otherwise beeligible property is not directly owned by the subsidiaryon the AOC and is instead located somewhere in thesubsidiary’s corporate group, it can be made eligibleproperty in some cases. For example, before the AOC,the subsidiary could change the property it owns di-rectly (for example, wind up a corporation whoseshares it owns). Following the AOC, it may also bepossible to obtain an 88(1)(d) bump on property held

down the corporate chain by effecting a series of se-quential qualifying wind-ups and 88(1)(d) bumps.

The time of the AOC is therefore very important. Aspecial rule20 provides that when the parent acquirescontrol of the subsidiary from someone dealing NALwith the parent, the AOC is deemed to have occurredat the earlier time the NAL person acquired control ofthe subsidiary. Deeming the AOC to have occurred atthat earlier time can affect the determination of eligibleproperty (the subsidiary is required to own the propertyat the earlier time) and the amount of the possible88(1)(d) bump (which is based on the property’s FMVat the earlier time). This rule prevents the use of NALtransfers to manipulate the time of the AOC.

The requirement that eligible property be owneddirectly by the subsidiary at the time of the AOCmeans that the subsidiary can influence whether an88(1)(d) bump will be available to the parent followingthe AOC and which properties would be eligible prop-erties. Before the AOC, the subsidiary can changewhich properties it owns directly, sell or acquire prop-erties, or take other steps to affect the parent’s abilityto claim an 88(1)(d) bump. It is often in the parent’sinterests to conclude an agreement with the subsidiary(or its shareholders) before the AOC to prevent thesubsidiary from taking any actions that would impairthe 88(1)(d) bump, or to require the subsidiary to takereasonable actions to enhance the 88(1)(d) bump. Thisform of agreement can add significant value to the par-ent.

Corporate acquisitions of public companies inCanada are usually conducted through takeover bidsgoverned by local securities laws. In a friendly transac-tion, the acquirer and the target often conclude amerger agreement in which the acquirer makes an offerwith agreed terms, and the target recommends the offerto its shareholders and conducts business in an agreed-upon manner until the offer date expires. Those agree-ments provide an opportunity to obtain the target’s co-operation in maximizing the value of the 88(1)(d)bump.

It is not uncommon for a friendly acquirer to askthe target to prepackage property in a way that opti-mizes the 88(1)(d) bump. For example, if the acquirerproposes to dispose of some of the target’s property(say, a particular division or business) that includes as-sets that cannot be eligible property (for example, de-preciable property), it may be useful for the target totransfer that property to a separate subsidiary beforethe AOC, typically on a tax-deferred basis. This leavesthe target holding shares in the new subsidiary, ratherthan existing properties, at the time of the AOC. Ifthose shares of the new subsidiary are eligible property(as is usually the case), the acquirer can apply an88(1)(d) bump to increase its tax cost of those shares

16The same property can be either capital or noncapital prop-erty depending on its use (for example, land acquired for the pur-pose of building a production facility versus land acquired forthe purpose of resale).

17Subpara. 88(1)(c)(iii) of the ITA. Since the subsidiary shareseliminated on the wind-up (the tax cost of which is effectivelypushed down to eligible property under the 88(1)(d) bump)would not be eligible for tax depreciation, it is logical to limiteligible property to nondepreciable capital property.

18Para. 88(1)(c) of the ITA. The requirement that the subsidiaryhold any eligible property continuously until the wind-up is an-other reason to try to minimize the amount of time between theAOC and the wind-up.

19The continuous ownership requirement is not violated if thesubsidiary amalgamates with another corporation following theAOC, because of a special rule (subsection 88(4) of the ITA)providing that the resulting corporation is deemed to be a con-tinuation of the subsidiary. However, that provision also deemsno AOC to have occurred on an amalgamation (except in limitedcircumstances). As such, acquisitions involving an amalgamationmust be structured so as to include a distinct AOC of the subsidi-ary, in order to establish the time of the AOC for purposes ofdetermining which property was directly owned by the subsidiaryat that time (as well as the FMV of such property at that timefor purposes of calculating the maximum 88(1)(d) bump). 20Para. 88(1)(d.2) of the ITA.

SPECIAL REPORTS

TAX NOTES INTERNATIONAL DECEMBER 9, 2013 • 941

(C) T

ax Analysts 2013. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

when the target is wound up or amalgamated into theacquirer. This leaves the acquirer free to dispose of theshares in the new subsidiary without realizing anygain.

This is illustrated in the example at Figure 4, inwhich CanCo has property with an accrued gain thatis not eligible for the 88(1)(d) bump. Before the AOC,CanCo incorporates a new Canadian subsidiary(SubCo) and transfers the ineligible property to SubCoon a tax-deferred basis in exchange for shares ofSubCo.21 If CanCo holds the SubCo shares as capitalproperty, they would generally be eligible property.22

On the wind-up, CanAcquireCo could apply the88(1)(d) bump to increase the tax cost of the SubCoshares up to their FMV ($40), permitting it to disposeof them freely. In effect, CanCo has prepackaged itsproperty to change what it holds directly from ineli-gible property into eligible property (the SubCo shares).CanAcquireCo can dispose of the SubCo shares,whether to a third party or on an internal group reor-ganization, without realizing any gain. While there areseveral different ways a target’s cooperation can en-hance an 88(1)(d) bump, this simple example illustratesthe basic principle.

C. Not Acquired as Part of AOC SeriesAnother rule is meant to prevent the parent from

transferring property with accrued gains to a subsidiaryon a tax-deferred basis before the AOC and eliminatingthose gains on the wind-up through the 88(1)(d) bump.This ‘‘anti-stuffing’’ rule disqualifies any property thatthe subsidiary acquires (as part of the AOC series)from either the parent or a person dealing NAL withthe parent. That property, as well as any property ac-quired by the subsidiary in substitution for such prop-erty (an issue discussed below), is excluded from beingeligible property.23

D. Not Transferred on Butterfly ReorganizationA ‘‘butterfly’’ reorganization is a particular form of

divisive reorganization under Canadian income tax law.It allows properties held in one Canadian corporationto be divided between two or more Canadian corpora-tions with the same shareholders as the existing corpo-ration, without gains being realized at the corporate orshareholder levels. Property transferred to the parent as

part of a distribution made on a butterfly reorganiza-tion will not qualify as eligible property.24

E. SummaryThe scope of eligible property can be summarized

as property distributed to the parent on the wind-upthat is:

• nondepreciable capital property;

• owned directly by the subsidiary at the time ofthe AOC and held continuously thereafter untilthe wind-up;

• not acquired by the subsidiary from the parent (ora person dealing NAL with the parent) as part ofthe AOC series, or property acquired in substitu-tion for such property; and

• not distributed as part of a butterfly reorganiza-tion.

VI. Calculation of Maximum BumpWhile the simple example in Figure 1 is useful as a

general illustration of what the 88(1)(d) bump canachieve, the limits on the amount of the tax cost in-crease are more complex than described there. Thereare generally two relevant limitations on the amount ofany 88(1)(d) bump for any given wind-up: A limit onthe amount that the tax cost of any particular eligibleproperty may be increased, and an overall limit on theamount the parent can increase the tax cost for all eli-gible properties. Some types of eligible property arealso subject to specific per-property bump limits.

A. Per-Property Limit1. General Limitation. The general limit on the

amount by which the 88(1)(d) bump can increase thetax cost of any particular eligible property is simple toexpress: The property’s tax cost cannot be increased toan amount in excess of its FMV at the time of theAOC.25 Returning to Figure 1, CanAcquireCo cannotincrease the tax cost of CanCo’s eligible property to anamount in excess of $60, so the 88(1)(d) bump is lim-ited to $40. This result holds, even though CanAcquire-Co’s total stepped-up tax cost in the acquired property($90) may be less than the tax cost of the CanCoshares that disappeared on the wind-up ($100). Thedifference ($10) is lost.

More specifically, the general per-property limit onthe amount of any 88(1)(d) bump to an eligible prop-erty is the excess of its FMV at the time of the AOCover its tax cost to the subsidiary at the time of thewind-up. Because the per-property limit is based on theproperty’s FMV at the time of the AOC, it is usuallyadvantageous for the parent to effect the wind-up soonafter the AOC to minimize the risk of intervening

21This can generally be achieved under subsection 85(1) ofthe ITA.

22Shares of a wholly owned subsidiary are normally consid-ered to be capital property to the holder. The efficacy of any pre-packaging transaction must be considered on its particular factsto ensure that all of the 88(1)(d) bump requirements are met —for example, that the parent and the subsidiary are dealing atarm’s length at the time, that the property is capital property,and that no technical anomaly precludes the bump.

23Subpara. 88(1)(c)(v) of the ITA. For this purpose, 251(5)(b)rights to acquire shares are ignored in determining whether aperson deals at NAL with the parent.

24Subpara. 88(1)(c)(iv) of the ITA.25Subpara. 88(1)(d)(ii) of the ITA.

SPECIAL REPORTS

942 • DECEMBER 9, 2013 TAX NOTES INTERNATIONAL

(C) T

ax Analysts 2013. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

Figure 4. Bump Prepackaging Transaction

1. Initial Situation

CanAcquireCo

$100

Seller

FMV = $100

CanCo

Tax cost = $20

FMV = $60

Tax cost = $30

FMV = $40

Eligible

Property

Other

Property

CanAcquireCo

$100

Seller

FMV = $100

CanCo

Tax cost = $20

FMV = $60

Tax cost = $30

FMV = $40

Eligible

PropertySubCo

Tax cost = $30

FMV = $40

Other

Property

3. Acquisition of CanCo

Seller

$100

CanAcquireCo

(Parent)

Tax cost = $100

FMV = $100

CanCo

(Subsidiary)

Tax cost = $20

FMV = $60

Tax cost = $30

FMV = $40

Eligible

PropertySubCo

Tax cost = $30

FMV = $40

Other

Property

CanAcquireCo

(Parent)

Tax cost/

FMV = $60

CanCo

Tax cost/

FMV = $40

Eligible

PropertySubCo

Tax cost = $30

FMV = $40

Other

Property

2. Pre-AOC Dropdown to SubCo

4. Wind-Up of CanCo

SPECIAL REPORTS

TAX NOTES INTERNATIONAL DECEMBER 9, 2013 • 943

(C) T

ax Analysts 2013. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

FMV increases. Going back to Figure 1 again, if Can-AcquireCo winds up CanCo immediately, it will be ina position to transfer eligible property (either within thegroup or to a third party) without any gains being real-ized since the FMV of the property will not exceed itstax cost. However, if CanAcquireCo were to wait ayear before effecting the wind-up, and during that yearthe eligible property’s FMV increased to $70, the88(1)(d) bump could not increase the property’s taxcost to more than $60, being the FMV at the time ofthe AOC a year earlier. CanAcquireCo would be leftwith an accrued gain of $10 on the eligible propertyand would not be able to transfer it freely without real-izing that accrued gain. In most cases, maximum flex-ibility is achieved by causing the wind-up to occur assoon as possible following the AOC.

Under amendments to the ITA announced on De-cember 21, 2012, and before Parliament as Bill C-4 asof late 2013, the per-property limit was amended torespond to perceived avoidance transactions that re-duced the subsidiary’s tax cost of property before thewind-up. The amount by which the tax cost of anyparticular eligible property can be increased using the88(1)(d) bump has been restated as the amount bywhich the FMV of the particular property at the timeof the AOC exceeds the greater of:

• the subsidiary’s tax cost of that particular prop-erty at the time of the AOC; and

• the subsidiary’s tax cost of that property at thetime of the wind-up.

This amendment targeted some transactions occur-ring after the AOC and before the wind-up, which re-duced the subsidiary’s tax cost of certain property,thereby increasing the accrued gain on that propertyand potentially the amount that its tax cost could beincreased under the 88(1)(d) bump rules. Such transac-tions can otherwise result in the 88(1)(d) bump shelter-ing post-AOC increases in the FMV of the subsidiary’seligible property, which is outside the legislative intentof this provision.

2. Partnership Interests. The tax status of partnershipsas transparent entities for Canadian tax purposes26 cre-ates various planning opportunities, some of which taxauthorities perceive to be inappropriate. Under anamendment to the 88(1)(d) bump rules introduced in2012, a specific rule limits the maximum permissibleincrease in the tax cost of interests in a partnership.Unfortunately, its application goes beyond tax planningconsidered to be objectionable.

This amendment reduces the maximum amount ofany 88(1)(d) bump on a partnership interest to the ex-tent that the accrued gain on the partnership interest is

attributable to accrued gains on non-eligible propertyowned by the partnership.27 This is achieved by deem-ing (for this purpose) the FMV of the partnership inter-est at the time of the AOC (which constitutes the up-per limit of the per-property bump under the generallimitation described above) to be a lower amount thanit actually is. Expressed conceptually, the FMV of thepartnership interest is deemed to be reduced by anamount representing that portion of the subsidiary’saccrued gain on the partnership interest that is attribut-able to the sum of:

• the FMV of Canadian or foreign resource prop-erty28 owned by the partnership (directly orthrough other partnerships); and

• the difference between the FMV and cost amountof other forms of non-eligible property (for ex-ample, depreciable property or inventory) ownedby the partnership, either directly or through otherpartnerships.29

For example, consider the case of a partnership in-terest held by the subsidiary at a tax cost of $70 andwhose FMV is $100 (that is, a $30 accrued gain). Ifthe partnership itself owns an eligible property with atax cost of $5 and an FMV of $10, and a non-eligibleproperty with a cost amount of $65 and an FMV of$90, for purposes of the general limitation in SectionVI.A.1 above, the FMV of the partnership interestwould be deemed to be $75 instead of $100.30 Thismeans that the maximum 88(1)(d) bump on such part-nership interest would be $5 ($75-$70).

Before this amendment, it was not uncommon tosee a subsidiary transfer non-eligible property to a part-nership as part of the prepackaging described in Sec-tion V.B above, in anticipation of the subsidiary itself

26A partnership computes its income as if it were a taxpayer,but it is not a taxable entity and instead its income and loss areattributed to its partners and included in computing the incomeand loss of the partners.

27Para. 88(1)(d)(ii.1) of the ITA, added by the 2012 federalbudget, effective for amalgamations that occur and wind-ups thatbegin after March 28, 2012. The 2012 federal budget also intro-duced an antiavoidance rule in paragraph 88(1)(e), which re-duces the FMV of a subsidiary’s partnership interest for the pur-pose of the calculation in subparagraph 88(1)(d)(ii.1) whencertain tax-deferred transfers of property were made on or beforethe AOC in order to increase the bump limitation regarding thepartnership interest.

28Resource properties are generally interests in mining or oiland gas properties.

29The Department of Finance explanatory notes accompany-ing the relevant provisions of the ITA make clear that this ruledoes not reduce the amount of an 88(1)(d) bump regarding aninterest in a partnership that owns shares of a corporation sim-ply because the corporation owns non-eligible property.

30The reduction in the FMV of the partnership interest iscomputed as the portion of the accrued gain on that propertythat is attributable to the notional gains on non-eligible property.Since the notional gains on the non-eligible property representfive-sixths ($25 / ($5 + $25)) of the total accrued gain ($30), forthis purpose the FMV of the partnership interest ($100) is re-duced by $25 (five-sixths of the $30 accrued gain on the partner-ship interest).

SPECIAL REPORTS

944 • DECEMBER 9, 2013 TAX NOTES INTERNATIONAL

(C) T

ax Analysts 2013. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

being acquired, so that the resulting partnership interestcould be the subject of an 88(1)(d) bump. The Depart-ment of Finance was concerned that this could pro-duce objectionable results when, for example, the part-nership interest was transferred to a nonresident ofCanada or to a tax-exempt entity such as a pensionfund.

While the 2012 amendment to the maximum88(1)(d) bump for a partnership interest will certainlyimpede such planning (for pre-AOC transfers to part-nerships, not to corporations), it will also affect othertransactions without such motivations, including88(1)(d) bumps on partnership interests that were ac-quired by the subsidiary well before any acquisition ofthe subsidiary was contemplated.31 It is not obviouswhy the scope of the amendment could not have beenmore precisely targeted to achieve its aims. Indeed, thepartnership bump limitation represents one of a num-ber of recent amendments in the past few years thathave the cumulative effect of making partnershipsmuch more difficult to use from a Canadian tax per-spective.

3. Foreign Affiliate Shares. Shares of a foreign affili-ate32 are likewise subject to an additional specific limi-tation. This limitation is intended to prevent perceivedduplication of favorable tax attributes that might other-wise occur following the parent’s AOC of the subsidi-ary if the subsidiary owns shares of a foreign affiliate.

Earnings of a foreign affiliate of a Canadian resi-dent corporation fall into various categories of surplusfor Canadian income tax purposes, some of which canbe repatriated back to the Canadian corporation free ofCanadian tax and as such are effectively equivalent totax cost in the shares of the foreign affiliate.33 Whencontrol is acquired of a Canadian corporation thatowns shares of a foreign affiliate, Canadian tax au-thorities perceive it as being duplicative to allow (invery general terms) the sum of the tax cost of the Ca-nadian corporation’s shares of the foreign affiliate andthe amount of this ‘‘good’’ surplus the Canadian cor-poration has in the foreign affiliate to exceed the FMVof the Canadian corporation’s shares of the foreignaffiliate.

Accordingly, when the subsidiary owns shares of aforeign affiliate, an 88(1)(d) bump is not permitted toresult in the sum of (1) the parent’s tax cost of thoseshares and (2) the good surplus34 of the foreign affiliateat the time of the AOC exceeding the FMV of thoseshares. A comparable rule applies when the subsidiaryowns shares of a foreign affiliate through a partnership.Reverting back to the example in Figure 2, if USCohad $10 of exempt surplus at the time of the AOC andCanCo’s tax cost in the USCo shares was $20, themaximum 88(1)(d) bump permitted on those shares(assuming their FMV was $60) would be $30, not $40,with the result that CanAcquireCo would have a post-88(1)(d) bump tax cost of $50 (not $60) in the USCoshares (plus the existing $10 of exempt surplus). Effec-tively, good surplus is treated as equivalent to tax cost.

When a foreign purchaser intends to cause the Ca-nadian target corporation to distribute the shares itowns in one or more foreign affiliates out to the for-eign purchaser as illustrated in Figure 2 above, the con-cern over duplication of tax attributes does not exist,since the surplus balances of the foreign affiliate(USCo) become irrelevant once it is no longer ownedby a Canadian resident. As such, the CRA has stated35

that it will not require that a foreign affiliate’s ‘‘good’’surplus be calculated in connection with a bump of theforeign affiliate’s shares if all the following conditionsare met:

• the foreign affiliate (USCo) shares are transferredto U.S. Parent by CanAcquireCo within a reason-able time after the takeover of CanCo;

• the maximum permissible 88(1)(d) bump is other-wise large enough to increase the tax cost of theU.S. SubCo shares to their FMV; and

31This amendment is supported by other provisions affectingtax-deferred transfers of partnership interests or of property to apartnership occurring as part of the relevant series of transac-tions.

32Generally, a corporation resident outside Canada will be aforeign affiliate of a Canadian resident taxpayer if:

• the Canadian resident taxpayer owns at least 1 percentof the foreign corporation’s shares (directly or indi-rectly); and

• the Canadian resident taxpayer and all persons relatedto that taxpayer collectively own at least 10 percent ofthe foreign corporation’s shares (directly or indirectly).

33For more on the types of surplus earned by a foreign affili-ate of a Canadian corporation and their implications, see http://miningtaxcanada.com/investment-outside-of-canada.

34Subpara. 88(1)(d)(ii) of the ITA and subsection 5905(5.4) ofthe Income Tax Regulations, applicable to wind-ups that begin,and amalgamations that occur, after December 20, 2012.‘‘Good’’ surplus of a wholly owned foreign affiliate is generallythe total of:

• the foreign affiliate’s consolidated exempt surplus;• the portion of the foreign affiliate’s hybrid surplus that

would be 100 percent deductible if repatriated toCanada; and

• the portion of the foreign affiliate’s taxable surplus thatwould be sheltered from Canadian tax upon repatriationby the grossed-up amount of underlying foreign tax paidby the foreign affiliate on its taxable surplus.

The determination of ‘‘good’’ surplus for this purpose takesinto account the separate rule in subsection 5905(5.2) of the In-come Tax Regulations, which applies on the AOC of a Cana-dian corporation that directly owns shares of a foreign affiliate toreduce the exempt surplus balance regarding that affiliate to theextent that the aggregate of the tax cost of that affiliate’s sharesand the good surplus of that affiliate exceeds the FMV of thataffiliate’s shares immediately before the AOC (that is, tax costplus good surplus cannot exceed FMV).

35CRA document 2011-0404521C6, May 19, 2011.

SPECIAL REPORTS

TAX NOTES INTERNATIONAL DECEMBER 9, 2013 • 945

(C) T

ax Analysts 2013. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

• neither CanCo nor CanAcquireCo receives (or isdeemed to receive) any dividends from U.S.SubCo after the AOC.

B. Overall Limit

The overall limit on the 88(1)(d) bump is describedas follows:36

The first element of the formula (the parent’s taxcost) corresponds to the $100 in Figure 1 that CanAc-quireCo pays for the CanCo shares. The higher theparent’s tax cost of the subsidiary shares is, the greaterthe potential 88(1)(d) bump. In structuring takeovers,an acquirer must consider that offering tax deferral op-portunities to target shareholders (that is, qualifyingshare-for-share exchanges that defer gains on targetshares)37 may reduce the acquirer’s tax cost of targetshares, and therefore reduce the overall limit on theamount of any potential 88(1)(d) bump.

The second element of the formula (net tax cost) isessentially the tax cost of all the subsidiary’s assets lessall its liabilities and some reserves taken for tax pur-poses immediately before the wind-up.38 The third ele-ment of the formula (tax-free dividends)39 supports thesecond element by ensuring that dividends, which havethe effect of reducing the net tax cost of the subsidi-ary’s assets, cannot be used to artificially increase theoverall 88(1)(d) bump limit.

Returning to the simplified example in Figure 1, theoverall 88(1)(d) bump limit would be $50 ($100 taxcost of CanCo shares less $50 pre-wind-up tax cost of

CanCo assets), assuming CanCo had no debts and hadpaid no dividends to CanAcquireCo. Since there isonly $40 of accrued gains on eligible property, $10 ofthe available 88(1)(d) bump amount ($50) goes unused.If the overall bump limit is less than the accrued gainson CanCo’s eligible property, CanAcquireCo maychoose how to allocate the bump amount among theeligible properties in its tax return for the tax year thatincludes the wind-up.

VII. The Bump Denial Rule

The bump denial rule40 looms over any analysis ofwhether the 88(1)(d) bump is available for a particularwind-up. If this rule is contravened for even a singleproperty, even of minimal value, no 88(1)(d) bump canbe claimed for any property distributed on that wind-up. This penalty is more severe than it needs to be forthe bump denial rule to achieve its tax policy objective,and the rule’s complexity is such that even the mostexperienced practitioners can easily overlook somethingthat triggers it. Moreover, even with the recent intro-duction of some important relieving amendments,there are technical anomalies in the legislation thatdeny the 88(1)(d) bump when there is no obvious taxpolicy concern.

The policy behind the bump denial rule is decep-tively simple: The parent should not be able to buy andwind up the subsidiary, claim an 88(1)(d) bump on itsproperty, and then sell some of that property back tothe subsidiary’s former shareholders. Expressed verygenerally, that result could be viewed as inconsistentwith Canada’s rules governing divisive reorganizationsof Canadian corporations.

The tax policy concern is that allowing an 88(1)(d)bump in such circumstances effectively amounts to adivisive reorganization of the subsidiary, which maytrigger a realization of any gains at the level of thesubsidiary’s shareholders — that is, on the sale of thesubsidiary to the parent — but not an appropriate real-ization of the accrued gains on the subsidiary’s ownproperty, since the wind-up is tax deferred and the88(1)(d) bump increases the tax cost of some or all ofthe subsidiary’s property. Hence, the bump denial ruleis intended to prevent backdoor divisive reorganizationsthat achieve results that are comparable to (but are notsubject to the statutory limitations applicable to) thetax-deferred divisive reorganizations permitted undersubsection 55(3) of the ITA. The bump denial rule isnot phrased in such simple terms however.

The bump denial rule can be paraphrased as deny-ing an 88(1)(d) bump on all property distributed on awind-up if, either before or after the AOC, a prohibitedperson acquires prohibited property as part of the

36Para. 88(1)(d) of the ITA.37It is generally possible for a shareholder with, say, $60 of

tax cost in shares of one Canadian corporation to exchangethem for shares of a second Canadian corporation such that nogain is realized and the shareholder’s tax cost of the shares ofthe second corporation and the second corporation’s tax cost inthe shares of the first corporation is $60.

38If this element of the formula is negative (that is, liabilitiesexceed tax cost of assets), it is treated as nil. Because the net taxcost of the subsidiary’s assets (which reduces the overall bumplimit) generally increases over time if the subsidiary is profitable,this creates a further incentive to effect the wind-up quickly afterthe AOC.

39Generally, dividends paid by one Canadian corporation toanother are fully deductible for Canadian income tax purposes.In determining whether a corporation deals NAL with the parentfor this purpose, 251(5)(b) rights to acquire shares are not consid-ered. 40Subpara. 88(1)(c)(vi) of the ITA.

parent’s tax cost of subsidiary shares immediatelybefore the wind-up

less net tax cost of subsidiary’s assets immediately beforethe wind-up

and less tax-free dividends paid by subsidiary to parent or anNAL corporation (ignoring 251(5)(b) rights)

SPECIAL REPORTS

946 • DECEMBER 9, 2013 TAX NOTES INTERNATIONAL

(C) T

ax Analysts 2013. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

AOC series (as noted above, the AOC series is the se-ries of transactions that includes the parent’s AOC ofthe subsidiary). Keeping this core concept in mindmakes it more manageable to explore the bump denialrule’s intricacies in more detail. The complexity of thebump denial rule lies in the breadth of what constitutesprohibited persons and prohibited property. At a corelevel:

• prohibited persons are shareholders of the sub-sidiary at a time that is both before the AOC andduring the AOC series; and

• prohibited property is property distributed to theparent on the wind-up (that is, acquired from thesubsidiary when it is merged or wound up intothe parent).

The basic thrust of the bump denial rule is thatproperty of the subsidiary that is distributed to the par-ent on the wind-up (herein, distributed property)should not, as part of the AOC series, be acquired bypersons who were significant subsidiary shareholders ata time during the AOC series and before the parentacquired control of the subsidiary. The term ‘‘signifi-cant’’ for this purpose essentially means holding 10percent or more of a class of the subsidiary’s shares,individually or collectively.

This bump denial rule is, unfortunately, more com-plex than this. The range of prohibited persons in-cludes far more than just pre-AOC shareholders of thesubsidiary, and prohibited property comprises muchmore than just distributed property. While the breadthof the bump denial rule may defeat avoidance schemesdesigned to circumvent the basic prohibition, it makesthe rule very complex (even by tax standards) and canresult in the 88(1)(d) bump being denied inappropri-ately. As a result, on any given transaction, one must

consider very carefully the three key elements of thebump denial rule that prohibited persons not acquireprohibited property as part of the AOC series.

A. Prohibited Persons

The first step in the analysis is to identify those per-sons whose acquisition of property could trigger thebump denial rule. In all cases, the parent and anyonerelated to the parent (other than by virtue of 251(5)(b)rights) at the relevant time are deemed not to be pro-hibited persons,41 and the subsidiary itself is alsodeemed not to be a prohibited person.

The most useful way to illustrate the wide range ofpotential prohibited persons is by using the exampleshown in Figure 6, as annotated by the discussion inthe text accompanying footnotes 42-47 and 51.

1. Persons Owning (or Deemed to Own) 10-Plus Percent ofa Relevant Class of Shares Pre-AOC. The prohibited per-sons concept centers on persons who are specifiedshareholders of the subsidiary at a time that is bothbefore the AOC and during the AOC series (herein, apre-AOC subsidiary specified shareholder). In simpleterms, a specified shareholder of a corporation is a per-son who owns 10 percent or more of any class of the

41If the parent is incorporated during the AOC series (as isoften the case) and the relevant time is before that incorporation,each person who is related to the parent throughout the periodthat begins when the parent is incorporated and ends at the timeimmediately before the wind-up is deemed not to be a prohibitedperson. Absent this deeming rule in subparagraph 88(1)(c.2)(i) ofthe ITA, no person could be related to the parent before its in-corporation (since the parent would not exist at that time).

Identify prohibited

persons (see Figure 6)

1. 10+% pre-AOC share-

holders of subsidiary or

a related upstream

corporation

2. Persons dealing NAL

with persons in 1

3. Sub-10% shareholders,

if collectively would

own >10%

4. Exclude parent and

persons related to

parent

Identify prohibited

property (see Figure 8)

1. Distributed property (DP)

2. Property received in

exchange for DP

3. Property deriving >10% of

its value post-AOC from

DP

4. Exclude exceptions

Has a prohibited person

acquired prohibited property

as part of the AOC series?

No

Bump denial rule not applicable

YesBump denial

rule applies

Figure 5. Bump Denial Rule Summarized

SPECIAL REPORTS

TAX NOTES INTERNATIONAL DECEMBER 9, 2013 • 947

(C) T

ax Analysts 2013. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

corporation’s shares.42 However, the ‘‘specified share-holder’’ definition is expanded as follows:

• Deemed Share Ownership: anyone dealing at NALwith the actual owner of shares is also deemed toown those shares, subject to limited exceptions.As a result, it is possible to be a specified share-holder of a corporation while owning less than 10percent of the corporation’s shares (or withoutactually owning any shares), if NAL persons ownsufficient shares of the corporation.43

• Ownership of Shares in Related Upstream Corporations:a person is deemed to be a specified shareholderof a particular corporation if that person meetsthe 10 percent share ownership (or deemed shareownership) threshold in any other corporationthat both:

— is related to the first corporation; and

— has a ‘‘significant direct or indirect interest’’in the first corporation — that is, an ‘‘up-stream’’ related corporation.44

As such, there are many ways in which a personcan be a pre-AOC subsidiary specified shareholder:While persons who own 10-plus percent of a class ofthe subsidiary’s shares before the AOC constitute thestarting point of the analysis, NAL persons and relatedupstream corporations widen the scope considerably.

2. Other Prohibited Persons. The prohibited person defi-nition goes beyond pre-AOC subsidiary specified share-holders to include the following persons:

(a) any number of persons whose collective shareownership, if aggregated in the hands of one per-son, would make that one person a pre-AOC sub-sidiary specified shareholder45;

(b) a corporation, other than the subsidiary, inwhich a pre-AOC subsidiary specified shareholderis, at any time after the AOC and during theAOC series, a specified shareholder46; or

(c) a corporation, other than the subsidiary, if:

— persons described in (a) above acquired sharesas part of the AOC series; and

— those acquired shares would, if aggregated inthe hands of one person, make that singlenotional person a specified shareholder of thatcorporation at any time after the AOC andduring the AOC series.47

Again, in all cases, the parent and anyone dealing atNAL with the parent will not be a prohibited person.

3. Prohibited Persons: Discussion. Two situations inwhich the scope of prohibited persons is considerablyexpanded are when:

• there is a controlling shareholder of the subsidiarybefore the AOC; and

• 251(5)(b) rights to acquire shares exist (describedin Section III.A), which can cause unrelated per-sons to be related (and therefore deal at NAL),which in turn causes additional persons to bedeemed to own shares they do not in fact own.

In particular, if the subsidiary has a controllingshareholder before the AOC (as opposed to being awidely held public corporation, for example), there canoften be many pre-AOC subsidiary specified sharehold-ers. This is because if a controlling shareholder exists(for example, ControlCo in Figure 6), any corporationcontrolled by the subsidiary will itself be related to(and deemed to deal at NAL with) that controllingshareholder, and thereby be deemed to own the con-trolling shareholder’s shares of the subsidiary. This canproduce anomalous and unintended results. In Figure6, for example (and subject to the comments that fol-low), SubCo 1, SubCo 2, and SubCo 3 are deemed toown the shares of Subsidiary that are owned by Con-trolCo, the entity that controls (and thereby deals atNAL with) Subsidiary, SubCo 1, SubCo 2, and SubCo3.

The December 21, 2012, amendments to the88(1)(d) bump rules created two relieving exclusions indetermining whether a person is a specified share-holder of a corporation, both of which will be particu-larly helpful when:

• the subsidiary/target has a pre-AOC controllingshareholder; and

42For example, ControlCo and DCo in Figure 6 are pre-AOCsubsidiary specified shareholders. Ownership of some fixed-valuenonvoting preferred shares is ignored for this purpose.

43See, e.g., NAL Person 1 in Figure 6, who deals NAL withControlCo and so is deemed to own ControlCo’s shares of thesubsidiary.

44‘‘Specified shareholder’’ definition in subsection 248(1) andclause 88(1)(c.2)(iii)(A) of the ITA. See, e.g., Investor and NALPerson 2 in Figure 6. Investor owns 10 percent of the shares of acorporation (ControlCo) that:

• is related to the subsidiary (since ControlCo has legalcontrol of the subsidiary); and

• has a significant direct or indirect interest in the subsidi-ary.

NAL Person 2 (who deals at NAL with Investor) is deemedto own Investor’s shares of ControlCo, and is thus in the sameposition as Investor.

45For example, see A, B, and C collectively in Figure 6 sincetheir shareholdings would, if aggregated, make the holder aspecified shareholder of the subsidiary by virtue of owning morethan 10 percent of its shares. If A, B, and C all acquired anyprohibited property as part of the AOC series, the bump denialrule would apply.

46See, e.g., Corp. 1 in Figure 6, which is a corporation morethan 10 percent of the shares of which are owned by a pre-AOCsubsidiary specified shareholder (Investor) following the AOC.

47For example, any corporation of which A, B, and C collec-tively own 10 percent or more of the shares of any class, if theyacquired those shares as part of the AOC series.

SPECIAL REPORTS

948 • DECEMBER 9, 2013 TAX NOTES INTERNATIONAL

(C) T

ax Analysts 2013. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

• the parent that is acquiring control of the subsidi-ary plans to sell a corporation controlled by thesubsidiary to an arm’s-length third party.

First, a person who has 251(5)(b) rights to acquire acorporation controlled by the subsidiary and whowould as a result otherwise be deemed to own sharesof the subsidiary (for example, because of beingdeemed to be related to the subsidiary’s controllingshareholder) will not be so deemed to own shares ofthe subsidiary.48 This amendment will prevent a thirdparty from becoming a prohibited person merely by

virtue of entering into an agreement with the parent toacquire shares of a corporation that is controlled bythe subsidiary, and thereby becoming related to (andbeing deemed to own the subsidiary shares owned by)the subsidiary’s controlling shareholder.

Second, for purposes of the rule that deems personsto own shares if they deal at NAL with the actualowner of the shares, corporations will generally not bedeemed to own shares of a corporation that controlsthem. Thus, for example, in Figure 6, SubCos 1, 2, and3 will not be deemed to own the shares of Subsidiarythat are owned by ControlCo, the entity that controls(and thereby deals at NAL with) Subsidiary, SubCo 1,SubCo 2, and SubCo 3.49

48See clause 88(1)(c.2)(iii)(A.2) of the ITA. Subsection 251(3)of the ITA deems two corporations that are each related to athird corporation to themselves be related, meaning that if athird-party buyer enters into an agreement to acquire a corpora-tion controlled by the subsidiary and thereby becomes related tothe corporation that controls the subsidiary, that controller andthe third-party buyer are deemed to be related, the third-party

buyer is deemed to own the controller’s shares of the subsidiary,and the third-party buyer thereby becomes a prohibited person.

49See clause 88(1)(c.2)(iii)(A.1) of the ITA.

Figure 6. Prohibited Persons

NAL Person 2 Investor

Others

90%10%

NAL Person 1 ControlCo

15%

Corp. 1

85%

Others

55%

Subsidiary

SubCo 1 SubCo 2

SubCo 3

2%

A

4%

B

5%

C 12%

DCo

100%

D

22%

Public

(widely

held)

SPECIAL REPORTS

(Footnote continued in next column.)

TAX NOTES INTERNATIONAL DECEMBER 9, 2013 • 949

(C) T

ax Analysts 2013. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

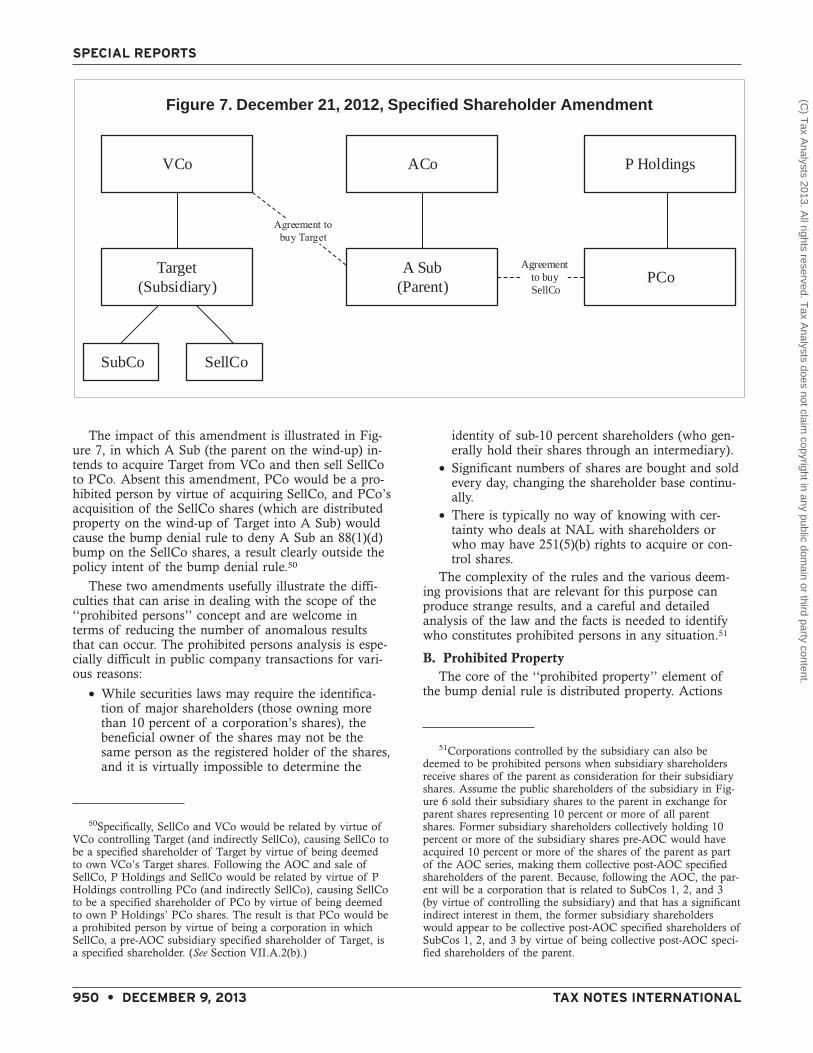

The impact of this amendment is illustrated in Fig-ure 7, in which A Sub (the parent on the wind-up) in-tends to acquire Target from VCo and then sell SellCoto PCo. Absent this amendment, PCo would be a pro-hibited person by virtue of acquiring SellCo, and PCo’sacquisition of the SellCo shares (which are distributedproperty on the wind-up of Target into A Sub) wouldcause the bump denial rule to deny A Sub an 88(1)(d)bump on the SellCo shares, a result clearly outside thepolicy intent of the bump denial rule.50

These two amendments usefully illustrate the diffi-culties that can arise in dealing with the scope of the‘‘prohibited persons’’ concept and are welcome interms of reducing the number of anomalous resultsthat can occur. The prohibited persons analysis is espe-cially difficult in public company transactions for vari-ous reasons:

• While securities laws may require the identifica-tion of major shareholders (those owning morethan 10 percent of a corporation’s shares), thebeneficial owner of the shares may not be thesame person as the registered holder of the shares,and it is virtually impossible to determine the

identity of sub-10 percent shareholders (who gen-erally hold their shares through an intermediary).

• Significant numbers of shares are bought and soldevery day, changing the shareholder base continu-ally.

• There is typically no way of knowing with cer-tainty who deals at NAL with shareholders orwho may have 251(5)(b) rights to acquire or con-trol shares.

The complexity of the rules and the various deem-ing provisions that are relevant for this purpose canproduce strange results, and a careful and detailedanalysis of the law and the facts is needed to identifywho constitutes prohibited persons in any situation.51

B. Prohibited PropertyThe core of the ‘‘prohibited property’’ element of

the bump denial rule is distributed property. Actions

50Specifically, SellCo and VCo would be related by virtue ofVCo controlling Target (and indirectly SellCo), causing SellCo tobe a specified shareholder of Target by virtue of being deemedto own VCo’s Target shares. Following the AOC and sale ofSellCo, P Holdings and SellCo would be related by virtue of PHoldings controlling PCo (and indirectly SellCo), causing SellCoto be a specified shareholder of PCo by virtue of being deemedto own P Holdings’ PCo shares. The result is that PCo would bea prohibited person by virtue of being a corporation in whichSellCo, a pre-AOC subsidiary specified shareholder of Target, isa specified shareholder. (See Section VII.A.2(b).)

51Corporations controlled by the subsidiary can also bedeemed to be prohibited persons when subsidiary shareholdersreceive shares of the parent as consideration for their subsidiaryshares. Assume the public shareholders of the subsidiary in Fig-ure 6 sold their subsidiary shares to the parent in exchange forparent shares representing 10 percent or more of all parentshares. Former subsidiary shareholders collectively holding 10percent or more of the subsidiary shares pre-AOC would haveacquired 10 percent or more of the shares of the parent as partof the AOC series, making them collective post-AOC specifiedshareholders of the parent. Because, following the AOC, the par-ent will be a corporation that is related to SubCos 1, 2, and 3(by virtue of controlling the subsidiary) and that has a significantindirect interest in them, the former subsidiary shareholderswould appear to be collective post-AOC specified shareholders ofSubCos 1, 2, and 3 by virtue of being collective post-AOC speci-fied shareholders of the parent.

VCo

A Sub

(Parent)

Target

(Subsidiary)

ACo

PCo

P Holdings

SubCo SellCo

Agreementto buySellCo

Figure 7. December 21, 2012, Specified Shareholder Amendment

SPECIAL REPORTS

950 • DECEMBER 9, 2013 TAX NOTES INTERNATIONAL

(C) T

ax Analysts 2013. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

taken before the wind-up (transfers of property, pay-ments of liabilities, and the like) may affect what thesubsidiary owns directly at the time of the wind-up,and hence what constitutes distributed property. Dis-tributed property is always prohibited property, withone exception: When a person acquires distributedproperty before the AOC but does not own that prop-erty at any time after the AOC, that person will bedeemed not to have acquired such distributed property,effectively exempting it from being prohibited propertyregarding that person.52

Prohibited property also includes two additionalforms of property (herein, substituted property) thatare based on distributed property:53

• property acquired by any person in exchange fordistributed property; and

• property owned by a person following the AOCwhich, at that time, derives more than 10 percentof its FMV from distributed property.54

Properties meeting one (or both) of these conditionsare nonetheless excluded from being substituted prop-erty if they fall within limited exceptions (see belowunder Section VII.B.3), further complicating the analy-sis. These exceptions make it necessary to determinewhether a property is a substituted property with refer-ence to a particular owner of the property — the sameproperty could be a substituted property regarding oneowner and not another person who later owns thesame property. Figure 8 summarizes the prohibitedproperty analysis described in Section VII.

1. Property Acquired in Exchange for Distributed Property.Once all distributed property has been identified, it isnecessary to assess whether any property has been ac-quired by any person ‘‘in exchange for’’ distributedproperty. For example, if the subsidiary acquired Prop-erty 1 from another person in exchange for Property 2and held Property 1 until the wind-up, Property 1would be distributed property, making Property 2 sub-stituted property (that is, acquired in exchange for adistributed property). Each time a distributed propertyis transferred in exchange for property, a new substi-tuted property (and potential prohibited property) iscreated.55

Note that the relevant question when testingwhether a property is a substituted property is whetherany person exchanged that property for distributedproperty, not merely the particular prohibited personbeing tested. Thus, once such an exchange occurs, theexchanged property will be a substituted property re-garding all owners unless one of the five exceptionsprovided for in paragraph 88(1)(c.3) of the ITA de-scribed below applies. Substituted property can be cre-ated on any such transfer, either before or after thewind-up, although the bump denial rule applies only ifthe other two elements of the test are also met (theproperty was acquired by a prohibited person and aspart of the AOC series).

2. Property Deriving More Than 10 Percent of Its FMVFrom Distributed Property Post-AOC. Typically, the mainconcern with the scope of prohibited property is prop-erty that derives more than 10 percent of its FMVfrom distributed property at a time following the AOCand when owned by the prohibited person (herein, 10percent-plus property). One of the most common ex-amples of 10 percent-plus property is shares of an ac-quirer of the subsidiary (or of that acquirer’s own con-trolling shareholder). For example, if the parentpurchases the subsidiary and delivers parent shares ordebt (or shares or debt of that parent’s own parentcompany) to subsidiary shareholders in payment, thesubsidiary shareholders will own property (parent secu-rities) that derives its value post-AOC partly from thesubsidiary’s own property (which is by definition dis-tributed property on the wind-up). If the parent securi-ties derive more than 10 percent of their FMV fromthe subsidiary’s properties, the parent shares aredeemed to be substituted property and prohibited prop-erty unless an exception to the rule applies.

Some properties specified in the ITA that are 10percent-plus property are excluded from being deemedsubstituted property. Such property (specified property)consists of the following:56

• a share of the parent or another taxable Canadiancorporation that wholly owns the parent, if issuedon the acquisition of shares of the subsidiary bythe parent, the other taxable Canadian corpora-tion, or a wholly owned Canadian subsidiary ofthe parent;

• a share of the parent issued for consideration con-sisting exclusively of money;52Subpara. 88(1)(c.2)(iv) of the ITA.

53Another form of deemed substituted property also exists,but it is generally interpreted as being limited to property thatderives substantially all its value from distributed property, basedon the Department of Finance technical notes describing thisprovision (subpara. 88(1)(c.3)(ii) of the ITA).

54Before December 21, 2012, this was phrased more broadlyto include property whose FMV (any time following the AOC)was wholly or partly attributable to distributed property — thatis, no 10 percent threshold.

55Since only at the time of the wind-up will it be known forsure what the distributed property is, on a pre-wind-up exchange

of property, the parties may not realize that a transferred prop-erty was (that is, would later become) distributed property andthat the property acquired in exchange was therefore substitutedproperty.