Can 123 Variables Say Something About Inflation in … · Can 123 Variables Say Something About In...

49

Introduction Empirical estimations Results and conclusion Can 123 Variables Say Something About Inflation in Malaysia? Kue-Peng Chuah 1 Zul-fadzli Abu Bakar Preliminary work - please do no quote First version: January 2015 Current version: April 2017 TIAC - BNM Workshop Monetary Policy In Theory and Practice Session 2: Measuring Inflation Dynamics 23 May 2017 1 Presentation by Kue-Peng Chuah, [email protected] The opinions expressed in these slides and presentation are solely the responsibility of the authors and do not necessarily reflect the views of Bank Negara Malaysia. 1 / 31

-

Upload

truongdieu -

Category

Documents

-

view

221 -

download

7

Transcript of Can 123 Variables Say Something About Inflation in … · Can 123 Variables Say Something About In...

Introduction Empirical estimations Results and conclusion

Can 123 Variables Say SomethingAbout Inflation in Malaysia?

Kue-Peng Chuah1

Zul-fadzli Abu Bakar

Preliminary work - please do no quoteFirst version: January 2015

Current version: April 2017

TIAC - BNM WorkshopMonetary Policy In Theory and PracticeSession 2: Measuring Inflation Dynamics

23 May 2017

1Presentation by Kue-Peng Chuah, [email protected]

The opinions expressed in these slides and presentation are solely the responsibility of theauthors and do not necessarily reflect the views of Bank Negara Malaysia. 1 / 31

Introduction Empirical estimations Results and conclusion

Outline

1 IntroductionWhat we do in the paperContributionMotivation

2 Empirical estimationsDataMethodology

3 Results and conclusion

2 / 31

Introduction Empirical estimations Results and conclusion

Outline

1 IntroductionWhat we do in the paperContributionMotivation

2 Empirical estimationsDataMethodology

3 Results and conclusion

3 / 31

Introduction Empirical estimations Results and conclusion

What we do in the paper

Create a new measure of core inflation for Malaysia

Measure inflationary pressure using the underlying inflationgauge UIG

Summarise a pool of information for a large heterogeneousdataset (123 variables) - beyond price data

Use the generalised dynamic factor model (DFM) - a unifiedsystematic and efficient approach

4 / 31

Introduction Empirical estimations Results and conclusion

What we do in the paper

Create a new measure of core inflation for Malaysia

Measure inflationary pressure using the underlying inflationgauge UIG

Summarise a pool of information for a large heterogeneousdataset (123 variables) - beyond price data

Use the generalised dynamic factor model (DFM) - a unifiedsystematic and efficient approach

4 / 31

Introduction Empirical estimations Results and conclusion

What we do in the paper

Create a new measure of core inflation for Malaysia

Measure inflationary pressure using the underlying inflationgauge UIG

Summarise a pool of information for a large heterogeneousdataset (123 variables) - beyond price data

Use the generalised dynamic factor model (DFM) - a unifiedsystematic and efficient approach

4 / 31

Introduction Empirical estimations Results and conclusion

What we do in the paper

Create a new measure of core inflation for Malaysia

Measure inflationary pressure using the underlying inflationgauge UIG

Summarise a pool of information for a large heterogeneousdataset (123 variables) - beyond price data

Use the generalised dynamic factor model (DFM) - a unifiedsystematic and efficient approach

4 / 31

Introduction Empirical estimations Results and conclusion

Contribution to the literature

Numerous measures of core inflation have been proposed

No single best measure of core inflation - each measure hasbenefits and costs (e.g. CPI ex food and energy)

UIG is a new measure to gain traction in central banksReplication of Amstad et al. (2009, 2013 and 2014)

– Switzerland: > 400 variables– USA: > 300 variables– China: > 400 variables

Others: Canada (Khan et al. 2013), UK (Kapetanios, 2002), euro area(Hahn, 2003 and Cristadoro et al., 2005), New Zealand (Giannone andMatheson, 2007), Iceland (Einarsson, 2015)

5 / 31

Introduction Empirical estimations Results and conclusion

Contribution to the literature

Numerous measures of core inflation have been proposed

No single best measure of core inflation - each measure hasbenefits and costs (e.g. CPI ex food and energy)

UIG is a new measure to gain traction in central banksReplication of Amstad et al. (2009, 2013 and 2014)

– Switzerland: > 400 variables– USA: > 300 variables– China: > 400 variables

Others: Canada (Khan et al. 2013), UK (Kapetanios, 2002), euro area(Hahn, 2003 and Cristadoro et al., 2005), New Zealand (Giannone andMatheson, 2007), Iceland (Einarsson, 2015)

5 / 31

Introduction Empirical estimations Results and conclusion

Contribution to the literature

Numerous measures of core inflation have been proposed

No single best measure of core inflation - each measure hasbenefits and costs (e.g. CPI ex food and energy)

UIG is a new measure to gain traction in central banksReplication of Amstad et al. (2009, 2013 and 2014)

– Switzerland: > 400 variables– USA: > 300 variables– China: > 400 variables

Others: Canada (Khan et al. 2013), UK (Kapetanios, 2002), euro area(Hahn, 2003 and Cristadoro et al., 2005), New Zealand (Giannone andMatheson, 2007), Iceland (Einarsson, 2015)

5 / 31

Introduction Empirical estimations Results and conclusion

Contribution to the literature

Numerous measures of core inflation have been proposed

No single best measure of core inflation - each measure hasbenefits and costs (e.g. CPI ex food and energy)

UIG is a new measure to gain traction in central banksReplication of Amstad et al. (2009, 2013 and 2014)

– Switzerland: > 400 variables– USA: > 300 variables– China: > 400 variables

Others: Canada (Khan et al. 2013), UK (Kapetanios, 2002), euro area(Hahn, 2003 and Cristadoro et al., 2005), New Zealand (Giannone andMatheson, 2007), Iceland (Einarsson, 2015)

5 / 31

Introduction Empirical estimations Results and conclusion

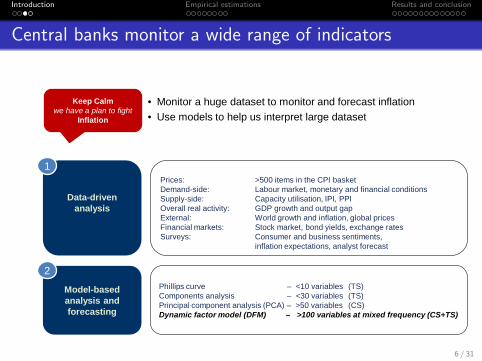

Central banks monitor a wide range of indicators

• Monitor a huge dataset to monitor and forecast inflation • Use models to help us interpret large dataset

Data-driven analysis

Model-based analysis and forecasting

Prices: >500 items in the CPI basket Demand-side: Labour market, monetary and financial conditions Supply-side: Capacity utilisation, IPI, PPI Overall real activity: GDP growth and output gap External: World growth and inflation, global prices Financial markets: Stock market, bond yields, exchange rates Surveys: Consumer and business sentiments, inflation expectations, analyst forecast

Phillips curve – <10 variables (TS) Components analysis – <30 variables (TS) Principal component analysis (PCA) – >50 variables (CS) Dynamic factor model (DFM) – >100 variables at mixed frequency (CS+TS)

1

2

Keep Calm we have a plan to fight

Inflation

6 / 31

Introduction Empirical estimations Results and conclusion

Measuring core inflation

Exclude volatile items

i.e. food and energy

Re-weight items in CPI

that are volatile or

price administered

Cross section (CS)

Univariate

• MA

• Trimmed mean

• Filters: HP,

band-pass, Kalman

Multivariate

• SVAR

• Kalman

Time series (TS)

Principal Component

Analysis (PCA)

Dynamic factor model

(DFM)

CS + TS

Smoothing / filtering

Common shortcoming :

consider a limited fraction of information or

a homogenous data set

Eliminate SR volatility

to smoothen

Eliminate idiosyncratic noise

and some volatility1 2 1 2

3

3

7 / 31

Introduction Empirical estimations Results and conclusion

Outline

1 IntroductionWhat we do in the paperContributionMotivation

2 Empirical estimationsDataMethodology

3 Results and conclusion

8 / 31

Introduction Empirical estimations Results and conclusion

Data

Balanced panel of monthly data from Jan. 2000 to Dec. 2014

𝒙𝟏 𝒙𝟐 𝒙𝟑 𝒙𝟏𝟐𝟑

𝒕 = 𝟏

𝒕 = 𝟐

𝒕 = 𝑻

Prices 54

Financial 15

Real activity 34

Money and credit 16

Labour 1

Prices Real activity

Labour Money

Financial International

International 3

Prices

Real activity

9 / 31

Introduction Empirical estimations Results and conclusion

Data

Broad and large dataset (nominal and real variables)

These relevant data are monitored for surveillance

Standardise each variable prior to estimation

10 / 31

Introduction Empirical estimations Results and conclusion

Data

Broad and large dataset (nominal and real variables)

These relevant data are monitored for surveillance

Standardise each variable prior to estimation

10 / 31

Introduction Empirical estimations Results and conclusion

Data

Broad and large dataset (nominal and real variables)

These relevant data are monitored for surveillance

Standardise each variable prior to estimation

10 / 31

Introduction Empirical estimations Results and conclusion

Methodology

DFM as developed by Forni et al. (2000 and 2005) and applied inAmstad et al. (2014)

Smoothing is done to split noise from trend using FourierTransformation (frequency domain)

Essentially, the DFM summarises the entire dataset into asingle indicator called the UIG

The UIG is a common factor - unobservable - affecting all thevariables

11 / 31

Introduction Empirical estimations Results and conclusion

Methodology

DFM as developed by Forni et al. (2000 and 2005) and applied inAmstad et al. (2014)

Smoothing is done to split noise from trend using FourierTransformation (frequency domain)

Essentially, the DFM summarises the entire dataset into asingle indicator called the UIG

The UIG is a common factor - unobservable - affecting all thevariables

11 / 31

Introduction Empirical estimations Results and conclusion

Methodology

DFM as developed by Forni et al. (2000 and 2005) and applied inAmstad et al. (2014)

Smoothing is done to split noise from trend using FourierTransformation (frequency domain)

Essentially, the DFM summarises the entire dataset into asingle indicator called the UIG

The UIG is a common factor - unobservable - affecting all thevariables

11 / 31

Introduction Empirical estimations Results and conclusion

Methodology

DFM as developed by Forni et al. (2000 and 2005) and applied inAmstad et al. (2014)

Smoothing is done to split noise from trend using FourierTransformation (frequency domain)

Essentially, the DFM summarises the entire dataset into asingle indicator called the UIG

The UIG is a common factor - unobservable - affecting all thevariables

11 / 31

Introduction Empirical estimations Results and conclusion

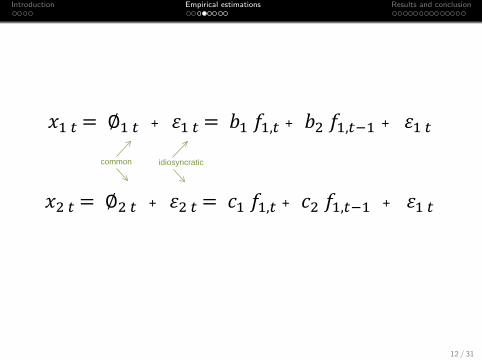

𝑥1 𝑡 = ∅1 𝑡 + 𝜀1 𝑡 = 𝑏1 𝑓1,𝑡 + 𝑏2 𝑓1,𝑡−1 + 𝜀1 𝑡

common idiosyncratic

𝑥2 𝑡 = ∅2 𝑡 + 𝜀2 𝑡 = 𝑐1 𝑓1,𝑡 + 𝑐2 𝑓1,𝑡−1 + 𝜀1 𝑡

12 / 31

Introduction Empirical estimations Results and conclusion

Methodology

DFM imposes assumptions such that each variable can bedecomposed into two unobservable components

Common component represented by sum of unobservablefactors (f ) - strong correlation with whole dataset

Each variable has different weights (b) - react differently tothe common shock

13 / 31

Introduction Empirical estimations Results and conclusion

Methodology

Set frequency at [12 months] to capture shocks that persist(transitory vs. persistent shocks)

Set number of common factors at [two] - sufficiently reflectdataset, selection criteria using Bai and Ng (2008)

Set lag to [one] (distributed lag structure)

With new data release, DFM allocates a new set of weightswhen extracting underlying common factor to estimate theUIG

14 / 31

Introduction Empirical estimations Results and conclusion

inflation

signal

idiosyncratic

Unobserved Use all information in entire panel

UIG

Unobserved Noise

MR/LR

SR

15 / 31

Introduction Empirical estimations Results and conclusion

Benefits of DFM

Embracing large heterogenous dataset(e.g. granular and rich, big data)

Pool models vs. pool information

Agnostic about structure of economy, let data speak(applicable to EME)

Reliable or clearer signal to guide policy(common vs. idiosyncratic)

16 / 31

Introduction Empirical estimations Results and conclusion

Benefits of DFM

Embracing large heterogenous dataset(e.g. granular and rich, big data)

Pool models vs. pool information

Agnostic about structure of economy, let data speak(applicable to EME)

Reliable or clearer signal to guide policy(common vs. idiosyncratic)

16 / 31

Introduction Empirical estimations Results and conclusion

Benefits of DFM

Embracing large heterogenous dataset(e.g. granular and rich, big data)

Pool models vs. pool information

Agnostic about structure of economy, let data speak(applicable to EME)

Reliable or clearer signal to guide policy(common vs. idiosyncratic)

16 / 31

Introduction Empirical estimations Results and conclusion

Benefits of DFM

Embracing large heterogenous dataset(e.g. granular and rich, big data)

Pool models vs. pool information

Agnostic about structure of economy, let data speak(applicable to EME)

Reliable or clearer signal to guide policy(common vs. idiosyncratic)

16 / 31

Introduction Empirical estimations Results and conclusion

Outline

1 IntroductionWhat we do in the paperContributionMotivation

2 Empirical estimationsDataMethodology

3 Results and conclusion

17 / 31

Introduction Empirical estimations Results and conclusion

-4

-2

0

2

4

6

8

10

Mar

-01

Aug-

01Ja

n-02

Jun-

02N

ov-0

2Ap

r-03

Sep-

03Fe

b-04

Jul-0

4D

ec-0

4M

ay-0

5O

ct-0

5M

ar-0

6Au

g-06

Jan-

07Ju

n-07

Nov

-07

Apr-0

8Se

p-08

Feb-

09Ju

l-09

Dec

-09

May

-10

Oct

-10

Mar

-11

Aug-

11Ja

n-12

Jun-

12N

ov-1

2Ap

r-13

Sep-

13Fe

b-14

Jul-1

4

UIG vs. Headline Inflation 2001: 2014

UIG Headline

Y-o-Y growth, %

18 / 31

Introduction Empirical estimations Results and conclusion

-2

-1

0

1

2

3

4

5

6

7

8

Mar

-01

Aug-

01Ja

n-02

Jun-

02N

ov-0

2Ap

r-03

Sep-

03Fe

b-04

Jul-0

4D

ec-0

4M

ay-0

5O

ct-0

5M

ar-0

6Au

g-06

Jan-

07Ju

n-07

Nov

-07

Apr-0

8Se

p-08

Feb-

09Ju

l-09

Dec

-09

May

-10

Oct

-10

Mar

-11

Aug-

11Ja

n-12

Jun-

12N

ov-1

2Ap

r-13

Sep-

13Fe

b-14

Jul-1

4

UIG vs. Core (exclusion) Inflation 2001:2014

UIG Core

Y-o-Y growth, %

19 / 31

Introduction Empirical estimations Results and conclusion

-2

-1

0

1

2

3

4

5

6

7

8

Mar

-01

Aug-

01Ja

n-02

Jun-

02N

ov-0

2Ap

r-03

Sep-

03Fe

b-04

Jul-0

4D

ec-0

4M

ay-0

5O

ct-0

5M

ar-0

6Au

g-06

Jan-

07Ju

n-07

Nov

-07

Apr-0

8Se

p-08

Feb-

09Ju

l-09

Dec

-09

May

-10

Oct

-10

Mar

-11

Aug-

11Ja

n-12

Jun-

12N

ov-1

2Ap

r-13

Sep-

13Fe

b-14

Jul-1

4

UIG vs. PCA 2001: 2014

UIG PCA

Y-o-Y growth, %

20 / 31

Introduction Empirical estimations Results and conclusion

-2

-1

0

1

2

3

4

5

6

7

8

Mar

-01

Aug-

01Ja

n-02

Jun-

02N

ov-0

2Ap

r-03

Sep-

03Fe

b-04

Jul-0

4D

ec-0

4M

ay-0

5O

ct-0

5M

ar-0

6Au

g-06

Jan-

07Ju

n-07

Nov

-07

Apr-0

8Se

p-08

Feb-

09Ju

l-09

Dec

-09

May

-10

Oct

-10

Mar

-11

Aug-

11Ja

n-12

Jun-

12N

ov-1

2Ap

r-13

Sep-

13Fe

b-14

Jul-1

4

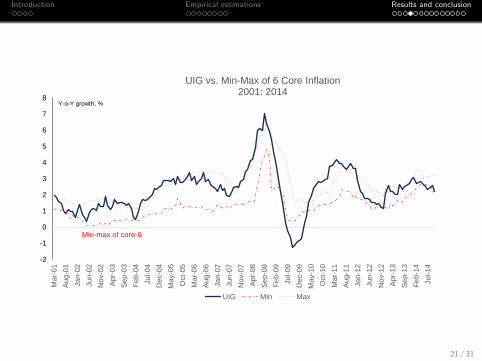

UIG vs. Min-Max of 6 Core Inflation 2001: 2014

UIG Min Max

Y-o-Y growth, %

Min-max of core-6

21 / 31

Introduction Empirical estimations Results and conclusion

-4

-2

0

2

4

6

8

10

Mar

-01

Aug-

01Ja

n-02

Jun-

02N

ov-0

2Ap

r-03

Sep-

03Fe

b-04

Jul-0

4D

ec-0

4M

ay-0

5O

ct-0

5M

ar-0

6Au

g-06

Jan-

07Ju

n-07

Nov

-07

Apr-0

8Se

p-08

Feb-

09Ju

l-09

Dec

-09

May

-10

Oct

-10

Mar

-11

Aug-

11Ja

n-12

Jun-

12N

ov-1

2Ap

r-13

Sep-

13Fe

b-14

Jul-1

4

UIG vs. Headline vs. Core Inflation

UIG Core Headline

UIG (1.38)

PCA (1.31)

Core (1.01)

Core-6 (0.97)

Headline (1.59)

UIG --

PCA 0.78 --

Core 0.74 0.93 --

Core-6 0.79 0.96 0.97

Headline 0.87 0.72 0.71 0.78

Y-o-Y growth, %

22 / 31

Introduction Empirical estimations Results and conclusion

Desirable properties of the UIG

Smoother than headline inflation without losing too muchinformation (e.g. global commodity price boom in 2000s)

Unbiased such that it has the same mean as headline inflation

Tracks inflation dynamics (turning points)

23 / 31

Introduction Empirical estimations Results and conclusion

Desirable properties of the UIG

Smoother than headline inflation without losing too muchinformation (e.g. global commodity price boom in 2000s)

Unbiased such that it has the same mean as headline inflation

Tracks inflation dynamics (turning points)

23 / 31

Introduction Empirical estimations Results and conclusion

Desirable properties of the UIG

Smoother than headline inflation without losing too muchinformation (e.g. global commodity price boom in 2000s)

Unbiased such that it has the same mean as headline inflation

Tracks inflation dynamics (turning points)

23 / 31

Introduction Empirical estimations Results and conclusion

Why the UIG is useful

Reliable Timeliness

Forecast inflation

Monetary Policy

24 / 31

Introduction Empirical estimations Results and conclusion

Reliable Timeliness

Forecast inflation

Monetary Policy

• More reliable signal of turning points

• Headline too volatile, core tends to ignore a lot of information

• Use information across variables and time (CS and TS)

25 / 31

Introduction Empirical estimations Results and conclusion

Reliable Timeliness

Forecast inflation

Monetary Policy

• Daily updates to monitor and forecast inflation when new data is released (nowcasting)

26 / 31

Introduction Empirical estimations Results and conclusion

Reliable Timeliness

Forecast inflation

Monetary Policy

• MP transmission has long, variable and uncertain lags, should not react to noise or idiosyncratic effects

• Exclude information not related to policymakers’ decision-making time horizon

27 / 31

Introduction Empirical estimations Results and conclusion

Reliable Timeliness

Forecast inflation

Monetary Policy

• Robust forecasting performance

• Mixed frequency model

28 / 31

Introduction Empirical estimations Results and conclusion

Conclusion (last slide!)

UIG contains desirable properties as a measure of coreinflation - promising preliminary results

UIG can be developed further as a regular feature tocomplement inflation toolkit of policymakers

Future work on UIG

– Expansion of dataset (300 variables)– Robustness analysis– Forecasting performance (horse race)

29 / 31

Introduction Empirical estimations Results and conclusion

Conclusion (last slide!)

UIG contains desirable properties as a measure of coreinflation - promising preliminary results

UIG can be developed further as a regular feature tocomplement inflation toolkit of policymakers

Future work on UIG

– Expansion of dataset (300 variables)– Robustness analysis– Forecasting performance (horse race)

29 / 31

Introduction Empirical estimations Results and conclusion

Conclusion (last slide!)

UIG contains desirable properties as a measure of coreinflation - promising preliminary results

UIG can be developed further as a regular feature tocomplement inflation toolkit of policymakers

Future work on UIG

– Expansion of dataset (300 variables)– Robustness analysis– Forecasting performance (horse race)

29 / 31

Introduction Empirical estimations Results and conclusion

Thank you

Comments welcome

30 / 31

Introduction Empirical estimations Results and conclusion

References

Amstad, M. and Huan, Y. and Ma, G. (2014). Developing an underlying inflation gauge for China. BIS WorkingPaper No. 465.

Bai, J. and Ng, S. (2002). Determining the number of factors in approximate factor models. Econometrica.

Bank Negara Malaysia (2008). Core inflation: measurements and evaluation. Bank Negara Malaysia AnnualReport, Chapter 3.

Bernanke, B., and Boivin, J. (2003). Monetary policy in a data-rich environment. Journal of Monetary Economics.

Chuah, K., Chong, E., and Tan, J. (2015). Global commodity prices and inflation dynamics in Malaysia. BankNegara Malaysia Working Paper No. 5/2015.

Forni, M., Hallin, M., Lippi, M. and Reichlin, L. (2000). The generalized dynamic-factor model: identification andestimation. Review of Economics and Statistics.

Forni, M., Hallin, M., Lippi, M., and Reichlin, L. (2005). The generalized dynamic factor model. Journal of theAmerican Statistical Association.

Hahn, E. (2002). Core inflation in the Euro Area: an application of the generalized dynamic factor model. Centerfor Financial Studies Working Paper No. 2002/11.

Kozicki, S. (2001). Why do central banks monitor so many inflation indicators?. Economic Review Federal ReserveBank of Kansas City.

31 / 31