Calyon Securities’ US Nuclear Forum New York,...

19

Company Update Calyon Securities’ US Nuclear Forum New York, NY Robert Van Namen – Senior Vice President, Uranium Enrichment Steven Wingfield Director Investor Relations Steven Wingfield – Director, Investor Relations December 2, 2008 NYSE: USU www.usec.com

Transcript of Calyon Securities’ US Nuclear Forum New York,...

Company Update

Calyon Securities’ US Nuclear ForumNew York, NY

Robert Van Namen – Senior Vice President, Uranium EnrichmentSteven Wingfield Director Investor RelationsSteven Wingfield – Director, Investor Relations

December 2, 2008

NYSE: USU

www.usec.com

Legal Notice

This presentation contains “forward-looking statements” – that is, statements related to future events. In this context, forward-looking statements may address our expected future business and financial , g y pperformance, and often contain words such as “expects,” “anticipates,” “intends,” “plans,” “believes,” “will” and other words of similar meaning. Forward-looking statements by their nature address matters that are, to different degrees, uncertain. For USEC, particular risks and uncertainties that could cause our actual future results to differ materially from those expressed in our forward-looking statements include, but are not limited to: the success of the demonstration and deployment of our American Centrifuge technology including our ability to meet our performance targets and schedule for theCentrifuge technology including our ability to meet our performance targets and schedule for the American Centrifuge Plant; the cost of the American Centrifuge Plant and our ability to timely secure a loan guarantee or other financing; the cost of electric power used at our gaseous diffusion plant; our dependence on deliveries under the Russian Contract and on a single production facility; our inability under most existing long-term contracts to pass on to customers increases in SWU prices under the Russian Contract resulting from significant increases in market prices; changes in existing restrictions on imports of Russian enriched uranium; the elimination of duties charged on imports of foreignon imports of Russian enriched uranium; the elimination of duties charged on imports of foreign-produced low enriched uranium; pricing trends in the uranium and enrichment markets and their impact on our profitability; changes to, or termination of, our contracts with the U.S. government and changes in U.S. government priorities and the availability of government funding, including loan guarantees; the impact of government regulation; the outcome of legal proceedings and other contingencies (including lawsuits and government investigations or audits); the competitive environment for our products and services; changes in the nuclear energy industry; the potential impact of volatile financial market conditions on our pension assets and credit and insurance facilities; and other risks and uncertainties discussed in our filings with the Securities and Exchange Commission, including our Annual Report on Form 10-K/A and subsequent quarterly Form 10-Qs. Revenue and operating results can fluctuate significantly from quarter to quarter, and in some cases, year to year. We do not undertake to update our forward-looking statements except as required by law.

Page 1

our forward looking statements except as required by law.

USEC’s Role in the Nuclear Fuel Cycle

Cameco, Denison, Areva, Rio Tinto

ConverDyn, Cameco, Areva

USEC, Urenco, Areva, Tenex

GE, Areva,

Toshiba/Westinghouse

Page 2

Enrichment is a Key Element of the Fuel Cycle

*** 2007 Share of Worldwide Deliveries**2007 Front-End Nuclear Fuel Market Costs*

Front-End Nuclear Fuel Industry: $24 Billion

Enrichment Industry: 41 MMSWU*** or $6 Billion

*Based on TradeTech LLC 2007 average market term prices and assumes 4 0% enriched 0 30% tailsBased on TradeTech, LLC 2007 average market term prices and assumes 4.0% enriched, 0.30% tails**NAC FuelTrac, TradeTech, Ux Consulting, USEC*** NAC FuelTrac estimate

Nuclear Power Sustains Competitive Advantage

Comparative Generation & Fuel Costs12 0

1.28

8.0

10.0

12.0

er k

Wh

O&MFuel

6.78¢

10.26¢

6.28

8.98

0.49

4.0

6.0

2007

cen

ts p

e

1 76¢2.47¢

6 8¢

0.471.911.290.56

0.0

2.0

Nuclear Coal Gas Oil

1.76¢

Source: NEI

• Nuclear power enjoys a substantial production cost advantage over other forms of electricity generation

% Fuel Cost 27% 77% 93% 86%

forms of electricity generation• Carbon taxes/GHG emissions standards would greatly benefit nuclear power

Nuclear Power Construction Remains Strong

New Reactors Under Construction or Planned/Approved by Countryas of October 2008

i Operating Reactors: 439i Long-term shutdown: 5i Under Construction: 36i Planned/Approved: 99

51

2

19

1 222

i Proposed: 232

i The International Atomic Energy Agency projects at l t 27% i i

8

2

1233

16

313

3

1

1

22

2

least a 27% increase in nuclear capacity by 20301

12

1-2 new reactors

3-6 new reactors

7-10 new reactors

Over 10 new reactors

2 1

Page 5

Sources: World Nuclear Association; IAEA Energy, Electricity and Nuclear Power Estimates for the Period up to 2030, Reference Data Series No.1 2008 Edition1 IAEA Low Estimate for nuclear capacity growth by 2030. IAEA High Estimate expects a 46% increase in nuclear capacity by 2030

WNA Enrichment Demand ScenariosDemand expected to grow 75% to 138% by 2030p g y

Page 6

Source: WNA Market Report 2007

SWU Market Prices Improve

Prices reflect higher power costs for GDPs, greater demand for enrichment and higher uranium pricesand higher uranium prices

Page 7

Source: TradeTech, LLC, month-end prices

Gaseous Diffusion Operations

• Paducah GDP operating at its highest efficiency and capacity in decades • Production in 2007 was at its highest level in 10 years• Five-year pricing agreement with TVA provides greater certainty and e yea p c g ag ee e t t p o des g eate ce ta ty a d

flexibility of operations, but fuel cost adjustment has increased power cost

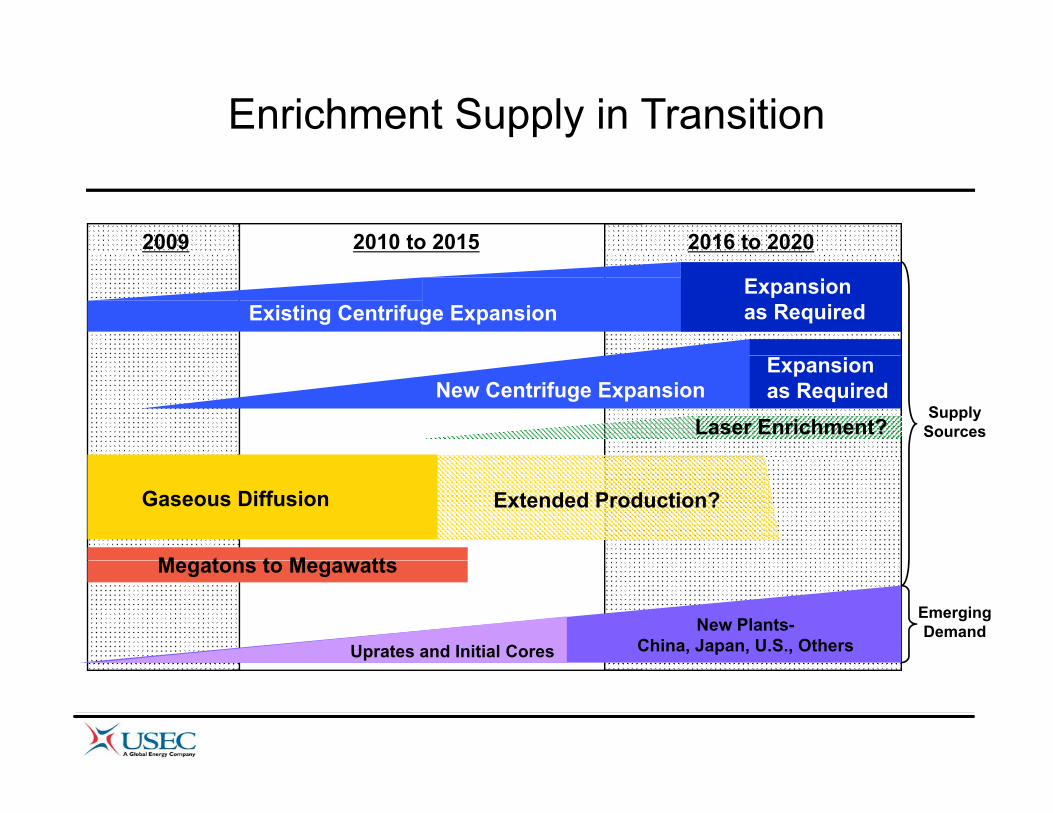

Enrichment Supply in Transition

2009 2010 to 2015 2016 to 2020

Expansionas RequiredExisting Centrifuge Expansion

New Centrifuge Expansion

Laser Enrichment?Supply

Sources

Expansion as Required

M t t M tt

Gaseous Diffusion Extended Production?

Megatons to Megawatts

New Plants-China, Japan, U.S., OthersUprates and Initial Cores

Emerging Demand

Enrichment Capacity Transitioning to Centrifuge

2010 expected capacity 2020 expected capacity

Laser Technology? ≈4%

Centrifuge96%

Page 10

Implications of Transition to Centrifuge

• Energy intensive and high variable GDP capital intensive and lower production centrifuge enrichmentproduction centrifuge enrichment

• GDP has significant production flexibility

• Tails assay flexibility is narrowing in new USEC contracts

• Modular design allows additional capacity to be added quicklyModular design allows additional capacity to be added quickly

• Increased financial imperative for customer and supplier to work together to match capacity to demand

Page 11

USEC’s American Centrifuge

• Lower-cost Production– Uses approximately 95% less electricity

American Centrifuge Lead Cascade in Piketon, Ohio in January 2008

pp y ythan current gaseous diffusion technology

• Higher Efficiency– Design ≈ 350 SWU/machine/yearg y– More productive than competition– Tests show higher potential output

• Modular Expansionp– Production can begin incrementally as

machines are installed– Allows for potential future expansion

beyond expected initial 3.8 million SWU

• Security of Supply– Enhances long-term nuclear fuel supply – Supports national energy security

Page 12

pp gy y– Develops an essential U.S. technology and

related manufacturing capacity

Managing ACP to Detailed Budget

• Approximate split of project costs • Budget of $3.5 billion includes ≈ $1 billion spent through 9/30/08 but not financing costs or financial assuranceDemo &

program • Management reserve included

• Budget reflects bottom-up, roll-up detailed work-breakdown structure

Machine manufacturing and assembly

program mgmt15%

• Contracts signed with strategic suppliers, including $1 billion contract that includes cost-reduction incentives

ith EPC t t Fl

and assembly45%Commercial

plant 40%

with EPC contractor Fluor

Page 13

American Centrifuge Progress and Schedule

High volume manufacturing U/ y

ear)

≈ 3.8 million SWU at end of 2012

1 MMSWU capacity

(≈ 400 centrifuges per month)

Commence li it d

AC100cascade testing

ges

(mill

ion

SWU

Lead cascade closed- I iti l

limited commercial operations

nsta

lled

Cen

trifu

closed-loop tests

begin

Initial AC100design freeze

ion

Cap

acity

of I

n

AC100 T i d Hi h V l C ifL d C d

Prod

ucti

Page 14

AC100 Testing and Initial Deployment

High-Volume Centrifuge Deployment

Lead Cascade Test Program

Re-establishing Manufacturing BaseWorking with suppliers to build thousands of American Centrifuge machines

• Babcock & Wilcox Co. managing high precisionmanaging high-precision machining at USEC’s Technology and Manufacturing Center in Oak gRidge,Tenn.

• ATK building rotor tubes in Rocket Center W VaRocket Center, W.Va.

• Major Tool and Machine casting steel casings for machines in Indianapolis, Ind.

• Teledyne Brown building service modules in Huntsville

• Fluor serves as EPC contractor for balance of plant at ACP in Piketon, Ohio

Page 15

service modules in Huntsville, Ala.

Financing the ACP

• Submitted both parts of DOE Loan C l ti ti i t d diSubmitted both parts of DOE Loan Guarantee application during summer 2008. Final DOE deadline is December 2, 2008

$3.5

$4.0

Cumulative anticipated spending on ACP over the next five years

• $2 billion set aside in program for “front end” of nuclear fuel cycle

$1 5

$2.0

$2.5

$3.0

• ACP meets DOE criteria, ideally suited for loan guarantee program

$0.0

$0.5

$1.0

$1.5

Thru 2007 2008 2009 2010 2011 2012

• USEC seeking a timely commitment from DOE for the project

Page 16

ACP Expansion Potential

Existing buildings (3.8 MM SWU) Available land

& g. Process

enan

ce &

mbl

y B

ld ProcessBldg. 1

ProcessBldg. 2M

aint

eA

ssem

En ironmental impact Current U.S. market

Page 17

Environmental impact evaluated for 7 MM SWU

Current U.S. marketis 12 MM SWU

SummaryMaximizing shareholder valueg

We are focused on delivering shareholder valueWe are focused on delivering shareholder valueand our goals are to:

• Continue solid progress on deployment of the American Centrifuge as we actively seek DOE Loan Guarantee program financing for the ACP

• Control production costs and continue to operate the Paducah plant efficiently during the transition to the American Centrifuge

• Maintain strong customer relationships as we secure new long-term sales contracts that reflect today’s higher market prices

Page 18