CALIFORNIA ENERGY COMMISSION California Energy Commission Spring 2006 Price Spike Report Media...

42

CALIFORNIA ENERGY COMMISSION California Energy Commission Spring 2006 Price Spike Report Media Briefing August 15, 2006 Joseph Desmond Undersecretary of Energy Affairs, Resources Agency

-

Upload

adela-mathews -

Category

Documents

-

view

213 -

download

0

Transcript of CALIFORNIA ENERGY COMMISSION California Energy Commission Spring 2006 Price Spike Report Media...

CALIFORNIA ENERGY COMMISSION

California Energy CommissionSpring 2006 Price Spike Report

Media Briefing

August 15, 2006

Joseph DesmondUndersecretary of Energy Affairs, Resources Agency

CALIFORNIA ENERGY COMMISSION

• Factors identified that contributed to price spike• Economic impact quantified for California consumers

and businesses• Regional extent of price spike analyzed in detail• Statewide variability of gasoline retail prices was

characterized• Financial information assessed to identify levels of

profitability for petroleum companies operating in California

• Recommendations developed to enable more thorough monitoring and analysis of California’s petroleum market

California Energy CommissionReport Results

CALIFORNIA ENERGY COMMISSION

Price Spikes and the Petroleum Market

CALIFORNIA ENERGY COMMISSION

California Retail Fuel PricesGasoline and Diesel Fuel versus

Alaska North Slope (ANS) Crude OilJanuary 2005 through July 2006

80

130

180

230

280

330

380

1/3

/20

05

2/3

/20

05

3/3

/20

05

4/3

/20

05

5/3

/20

05

6/3

/20

05

7/3

/20

05

8/3

/20

05

9/3

/20

05

10

/3/2

00

5

11

/3/2

00

5

12

/3/2

00

5

1/3

/20

06

2/3

/20

06

3/3

/20

06

4/3

/20

06

5/3

/20

06

6/3

/20

06

7/3

/20

06

8/3

/20

06

Ce

nts

Pe

r G

all

on

Gasoline

Diesel Fuel

ANS Crude Oil

Sources: Energy Information Administration (EIA) – California retail prices. Alaska crude oil prices – Wall Street Journal.

CALIFORNIA ENERGY COMMISSION

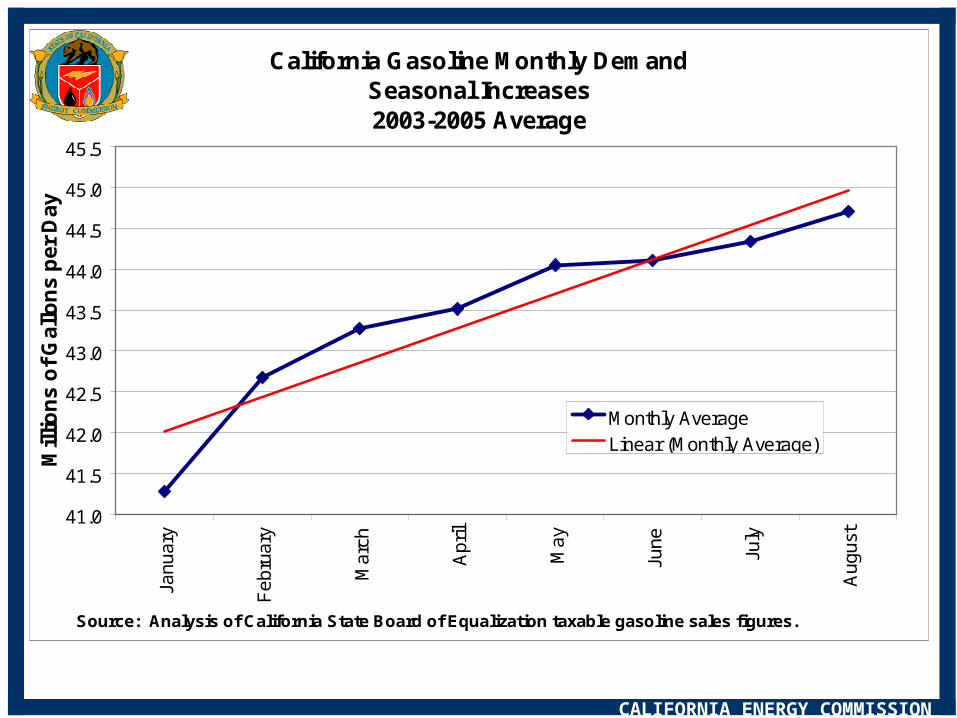

California Gasoline Monthly DemandSeasonal Increases2003-2005 Average

41.0

41.5

42.0

42.5

43.0

43.5

44.0

44.5

45.0

45.5Ja

nuar

y

Feb

ruar

y

Mar

ch

Apr

il

May

June

July

Aug

ust

Mill

ion

s o

f G

allo

ns

per

Day

Monthly AverageLinear (Monthly Average)

Source: Analysis of California State Board of Equalization taxable gasoline sales figures.

CALIFORNIA ENERGY COMMISSION

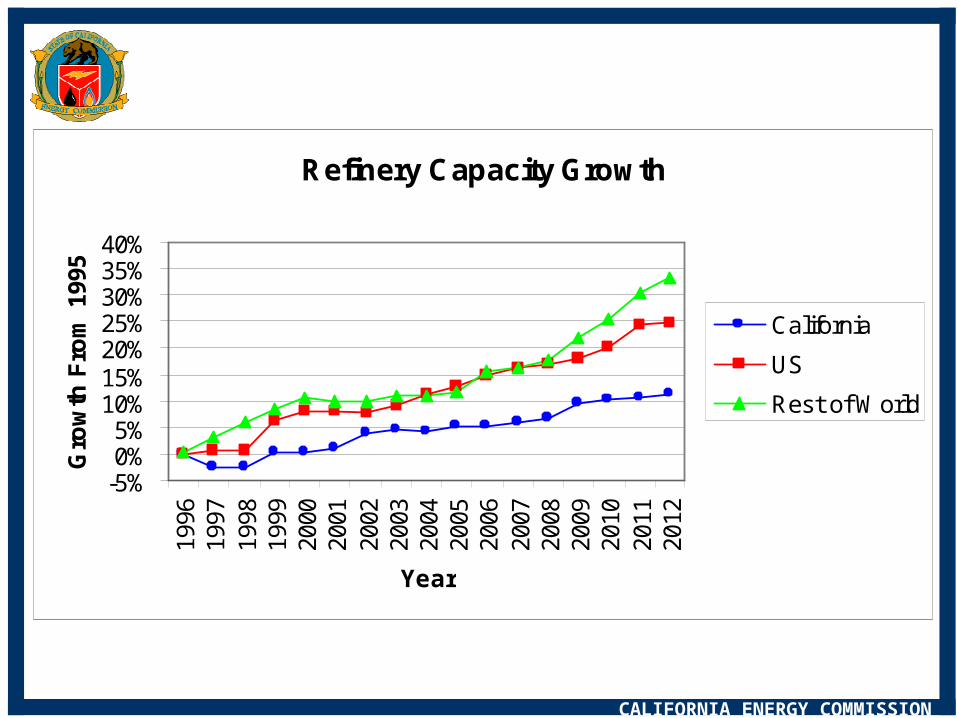

Refinery Capacity Growth

-5%0%5%

10%15%20%25%30%35%40%

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Year

Gro

wth

Fro

m 1

995

California

US

Rest of World

Avg Annual Growth

CA: 0.7%US: 1.5%

World: 2.0%

CALIFORNIA ENERGY COMMISSION

Refinery Count

0255075

100125150175200

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

Year

Nu

mb

er o

f R

efin

erie

s

Rest of US

California

CALIFORNIA ENERGY COMMISSION

Types of petroleum products that are produced by refineries are influenced by:– fuel specifications– quality of the crude oil processed– complexity of the refinery– supply/demand balance of the local petroleum

markets

CALIFORNIA ENERGY COMMISSION

California Refinery Output in 2005 by Product Type

CARB Compliant Gasoline*

43.1%

CARB Diesel11.6%

Jet Fuel12.4%

Non-California Gasoline

7.4%

EPA Diesel4.7%

*Note: Does not include ethanol.

CALIFORNIA ENERGY COMMISSION

2005 Demand for Petroleum and Alternative Fuels (millions of gallons)

53.5955

14,9633,734

2,960

Gasoline (excluding Ethanol)

Jet Fuel

DieselEthanol

Other Alternative Fuels

CALIFORNIA ENERGY COMMISSION

Market Operational Factors that Contributed to the Spring 2006 Price Spike

• Refinery unplanned outages and planned maintenance

• Refinery production of gasoline and diesel fuel• Inventory levels for petroleum products• Pipeline exports to Nevada and Arizona• Congestion of marine infrastructure operations in

Southern California• March 2006 Alaska North Slope crude oil distribution

system leak • Transition to new fuel specifications

CALIFORNIA ENERGY COMMISSION

California Refinery Events - Number of Days (First Six Months of 2005 versus 2006)

632

539

58

175

0

100

200

300

400

500

600

700

Jan-Jun 2005 Jan-Jun 2006

Day

s

Total Planned Maintenance Days

Total Unplanned Outage Days

Source: CEC Petroleum Industry Information Reporting Act (PIIRA) database.

CALIFORNIA ENERGY COMMISSION

Average Number of Days per California Refinery Event (First Six Months of 2005 versus 2006)

20.7

5.3

24.3

9.2

0

5

10

15

20

25

30

Jan-Jun 2005 Jan-June 2006

Day

s

Planned Maintenance

Unplanned Outages

Source: CEC Petroleum Industry Information Reporting Act (PIIRA) database.

CALIFORNIA ENERGY COMMISSION

Number of Event Days for California Refineries April/May 2005 versus April/May 2006

50

8476

75

0

10

20

30

40

50

60

70

80

90

April/May 2005 April/May 2006

Da

ys

Planned MaintenanceUnplanned Outages

7 Events

6 Events 6 Events

9 Events

Source: CEC Petroleum Industry Information Reporting Act (PIIRA) database.

CALIFORNIA ENERGY COMMISSION

5,000

5,500

6,000

6,500

7,000

7,500

8,000

8,500

8/5

/20

05

8/1

9/2

00

5

9/2

/20

05

9/1

6/2

00

5

9/3

0/2

00

5

10

/14

/20

05

10

/28

/20

05

11

/11

/20

05

11

/25

/20

05

12

/9/2

00

5

12

/23

/20

05

1/6

/20

06

1/2

0/2

00

6

2/3

/20

06

2/1

7/2

00

6

3/3

/20

06

3/1

7/2

00

6

3/3

1/2

00

6

4/1

4/2

00

6

4/2

8/2

00

6

5/1

2/2

00

6

5/2

6/2

00

6

6/9

/20

06

6/2

3/2

00

6

7/7

/20

06

7/2

1/2

00

6

8/4

/20

06

Th

ou

sa

nd

s o

f B

arr

els

pe

r W

ee

k

Current Year

CARB Gasoline Production(with 5-Year High-Low Band)

Source: CEC Petroleum Industry Information Reporting Act (PIIRA) database.

CALIFORNIA ENERGY COMMISSION

CALIFORNIA ENERGY COMMISSION

CALIFORNIA ENERGY COMMISSION

CALIFORNIA ENERGY COMMISSION

Weekly Gasoline Pipeline Exports from California(with 5-Year Hi-Lo Band and Retail Gasoline Price Overlay)

0

200

400

600

800

1,000

1,200

1,400

1,6007

/18

/20

05

8/1

/20

05

8/1

5/2

00

5

8/2

9/2

00

5

9/1

2/2

00

5

9/2

6/2

00

5

10

/10

/20

05

10

/24

/20

05

11

/7/2

00

5

11

/21

/20

05

12

/5/2

00

5

12

/19

/20

05

1/2

/20

06

1/1

6/2

00

6

1/3

0/2

00

6

2/1

3/2

00

6

2/2

7/2

00

6

3/1

3/2

00

6

3/2

7/2

00

6

4/1

0/2

00

6

4/2

4/2

00

6

5/8

/20

06

5/2

2/2

00

6

6/5

/20

06

6/1

9/2

00

6

7/3

/20

06

Th

ou

sa

nd

s o

f B

arr

els

pe

r W

ee

k

Shipments

Source: CEC Petroleum Industry Information Reporting Act (PIIRA) database.

CALIFORNIA ENERGY COMMISSION

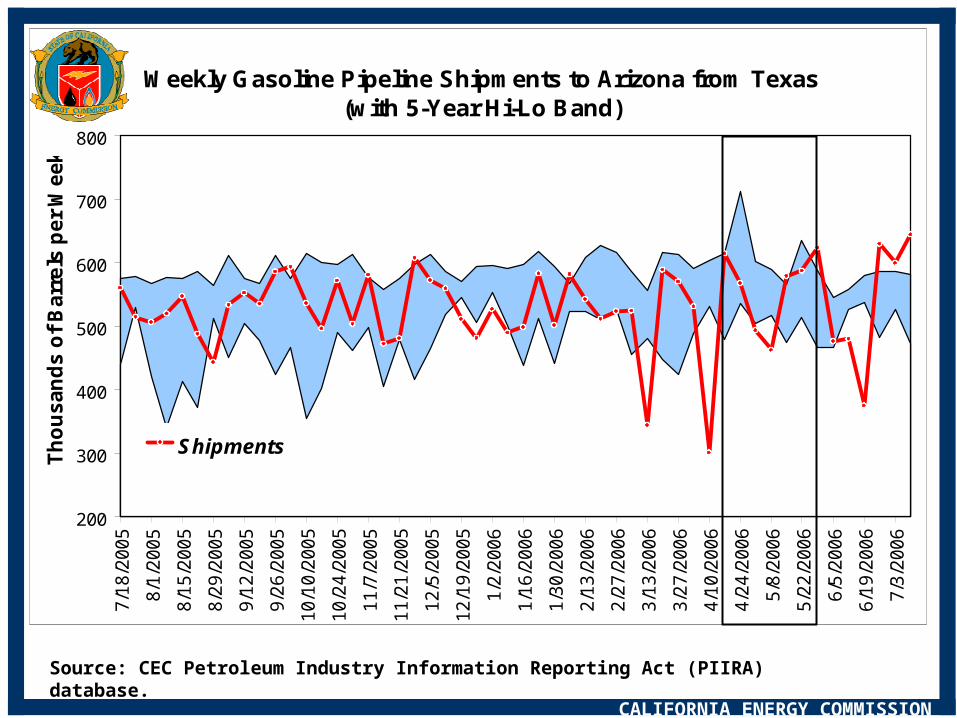

Weekly Gasoline Pipeline Shipments to Arizona from Texas(with 5-Year Hi-Lo Band)

200

300

400

500

600

700

8007

/18

/20

05

8/1

/20

05

8/1

5/2

00

5

8/2

9/2

00

5

9/1

2/2

00

5

9/2

6/2

00

5

10

/10

/20

05

10

/24

/20

05

11

/7/2

00

5

11

/21

/20

05

12

/5/2

00

5

12

/19

/20

05

1/2

/20

06

1/1

6/2

00

6

1/3

0/2

00

6

2/1

3/2

00

6

2/2

7/2

00

6

3/1

3/2

00

6

3/2

7/2

00

6

4/1

0/2

00

6

4/2

4/2

00

6

5/8

/20

06

5/2

2/2

00

6

6/5

/20

06

6/1

9/2

00

6

7/3

/20

06

Th

ou

sa

nd

s o

f B

arr

els

pe

r W

ee

k

Shipments

Source: CEC Petroleum Industry Information Reporting Act (PIIRA) database.

CALIFORNIA ENERGY COMMISSION

Source: CEC analysis of Marine Exchange of Southern California data.

Petroleum Product Tanker Arrivals/Activitiesin Southern California versus

LA Spot CARBOB Prices (April-May 2006)

0

1

2

3

4

5

6

7

8

4/1

/06

4/5

/06

4/9

/06

4/1

3/0

6

4/1

7/0

6

4/2

1/0

6

4/2

5/0

6

4/2

9/0

6

5/3

/06

5/7

/06

5/1

1/0

6

5/1

5/0

6

5/1

9/0

6

5/2

3/0

6

5/2

7/0

6

5/3

1/0

6

$1.50

$1.75

$2.00

$2.25

$2.50

$2.75

$3.00

$3.25New Arrivals in Region

Number of ActivitiesSpot CARBOB Prices

CALIFORNIA ENERGY COMMISSION

CALIFORNIA ENERGY COMMISSION

• Price spike increased gasoline costs to California consumers by $1.3 billion from April 25 through July 31, 2006

• The impact on businesses due to higher diesel fuel prices over the same period of time was approximately $170 million

• No attempt was made to quantify secondary costs for the California economy as a whole that occur when increased transportation costs are passed to consumers in the form of higher priced goods and services.

Economic Impact on California Consumers and Business

CALIFORNIA ENERGY COMMISSION

2005 and 2006 Average Weekly Retail Gasoline Price Minus Weekly Alaska North Slope (ANS) Crude Oil Price

$1.00

$1.10

$1.20

$1.30

$1.40

$1.50

$1.60

$1.70

$1.804

-Ap

r

11

-Ap

r

18

-Ap

r

25

-Ap

r

2-M

ay

9-M

ay

16

-Ma

y

23

-Ma

y

30

-Ma

y

6-J

un

13

-Ju

n

20

-Ju

n

27

-Ju

n

4-J

ul

11

-Ju

l

18

-Ju

l

25

-Ju

l

Dif

fere

nc

e p

er

Ga

llo

n (

Do

lla

rs)

2005

2006

Sources: Energy Information Administration (EIA) – California retail prices. CA BOE – taxable gasoline fuel sales. Alaska crude oil prices – Wall Street Journal.

CALIFORNIA ENERGY COMMISSION

Incremental Transportation Fuel CostsCalifornia Consumers & Business

$0

$20

$40

$60

$80

$100

$120

$140

$160

5/1

/20

06

5/8

/20

06

5/1

5/2

00

6

5/2

2/2

00

6

5/2

9/2

00

6

6/5

/20

06

6/1

2/2

00

6

6/1

9/2

00

6

6/2

6/2

00

6

7/3

/20

06

7/1

0/2

00

6

7/1

7/2

00

6

7/2

4/2

00

6

7/3

1/2

00

6

Week Ending

Mil

lio

ns

of

Do

lla

rs P

er

We

ek

Gasoline

Diesel Fuel

Sources: Energy Information Administration (EIA) – California retail prices. CA BOE – taxable gasoline fuel sales. Alaska crude oil prices – Wall Street Journal.

CALIFORNIA ENERGY COMMISSION

CALIFORNIA ENERGY COMMISSION

U.S. Annual Indices of Real Disposable Income, Vehicle Miles Traveled, Consumer Price Index (CPI-U), Average Fuel

Economy, and Real Average Retail Gasoline Prices(1978-2004, 1985=100)

0

20

40

60

80

100

120

140

160

180

200

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

Ind

ex (

1985

=10

0)

CPI-U: All Items less food and energy Real Disposable Personal Income

Real Retail Motor Gasoline Prices Vehicle Miles Traveled

24.8 MPG

25.4 MPG26.0 MPG

25.6MPG

24.7 MPG

24.5 MPG

Sources: Energy Information Administration (EIA), National Household Transportation Survey (NHTS), and Bureau of Labor Statistics (BLS).

CALIFORNIA ENERGY COMMISSION

• Price spike was not isolated to California’s market• Retail prices in neighboring states that are supplied by

California refineries demonstrated the closest correlation• States more distant from California did not demonstrate a

similar relationship• California retail distribution margins declined and were

temporarily negative during the spike in wholesale gasoline prices

Regional and Statewide Retail Gasoline Price Variations

CALIFORNIA ENERGY COMMISSION

Retail Gasoline Price Comparisons(Arizona, California, and Nevada)

200

220

240

260

280

300

320

340

36001

/05/

06

01/1

2/0

601

/19/

06

01/2

6/0

602

/02/

06

02/0

9/0

6

02/1

6/0

602

/23/

06

03/0

2/0

603

/09/

06

03/1

6/0

603

/23/

06

03/3

0/0

604

/06/

06

04/1

3/0

604

/20/

06

04/2

7/0

6

05/0

4/0

605

/11/

06

05/1

8/0

605

/25/

06

06/0

1/0

606

/08/

06

06/1

5/0

606

/22/

06

06/2

9/0

607

/06/

06

07/1

3/0

6

07/2

0/0

607

/27/

06

08/0

3/0

6

Cen

ts p

er G

allo

n Arizona California Nevada

Source: Oil Price Information Service (OPIS).

CALIFORNIA ENERGY COMMISSION

Retail Gasoline Price Comparisons(California, Montana, and Wyoming)

200

220

240

260

280

300

320

340

36001

/05/

06

01/1

2/0

601

/19/

06

01/2

6/0

602

/02/

06

02/0

9/0

602

/16/

06

02/2

3/0

603

/02/

06

03/0

9/0

603

/16/

06

03/2

3/0

603

/30/

06

04/0

6/0

604

/13/

06

04/2

0/0

604

/27/

06

05/0

4/0

605

/11/

06

05/1

8/0

605

/25/

06

06/0

1/0

606

/08/

06

06/1

5/0

606

/22/

06

06/2

9/0

607

/06/

06

07/1

3/0

607

/20/

06

07/2

7/0

608

/03/

06

Cen

ts p

er G

allo

n Wyoming California Montana

Source: Oil Price Information Service (OPIS).

CALIFORNIA ENERGY COMMISSION

California Gasoline Margins

-25

0

25

50

75

100

125

150

175

200

225

250

275

300

325

35001

/05/

06

01/1

2/0

6

01/1

9/0

6

01/2

6/0

6

02/0

2/0

6

02/0

9/0

6

02/1

6/0

6

02/2

3/0

6

03/0

2/0

6

03/0

9/0

6

03/1

6/0

6

03/2

3/0

6

03/3

0/0

6

04/0

6/0

6

04/1

3/0

6

04/2

0/0

6

04/2

7/0

6

05/0

4/0

6

05/1

1/0

6

05/1

8/0

6

05/2

5/0

6

06/0

1/0

6

06/0

8/0

6

06/1

5/0

6

06/2

2/0

6

06/2

9/0

6

07/0

6/0

6

07/1

3/0

6

07/2

0/0

6

07/2

7/0

6

08/0

3/0

6

Cen

ts p

er G

allo

n

Distribution Margin

Taxes

Refiner Margin

Crude Oil

Source: CEC staff analysis Oil Price Information Service (OPIS) data.

CALIFORNIA ENERGY COMMISSION

CALIFORNIA ENERGY COMMISSION

California City Analysis of Gasoline Prices(May 2006)

$0.00

$0.02

$0.04

$0.06

$0.08

$0.10

$0.12

$0.14

$0.16

$0.18

$0.20

$2.50 $2.70 $2.90 $3.10 $3.30 $3.50 $3.70 $3.90 $4.10

Average Retail Gasoline Price

Sta

nd

ard

De

via

tio

n

High Prices, High VariabilityLow Prices, High Variability

Low Prices, Low Variability High Prices, Low Variability

Shaded area denotes 95 percent of the cities measured in the state.

CALIFORNIA ENERGY COMMISSION

Low Prices, High Variability Cities include Buttonwillow, Concord, Dixon, Marysville, Novato, Suisun City and Woodland. These cities tend to be near major roadways, and the stations can be characterized as having increased sales volumes and possibly increased competition.

High Prices, High Variability Cities such as Beverly Hills, Mill Valley, San Francisco, and South Lake Tahoe fall into this category. These cities can be characterized as having above-average land values that may affect the retail price.

Inc

reas

ing

Va

ria

bili

ty

Low Prices, Low Variability Very few areas of the state fall into the low-price, low-variability category. Cities such as Antelope, Hilmar, Frazier Park, Foresthill, and Shingle Springs fall into this category. These places may be categorized as being close to major roadways, but not directly accessible.

High Prices, Low Variability Cities in more remote regions of the state tend to have above-average prices combined with lower variability. These cities are characterized by having fewer retail outlets, lower volume sales, and higher fuel delivery costs. In some cases, these cities may have only one retail outlet. This high-price, low variability category includes such cities as Baker, Big Bear City, Mount Shasta, and Soledad.

Increasing Retail Price

CALIFORNIA ENERGY COMMISSION

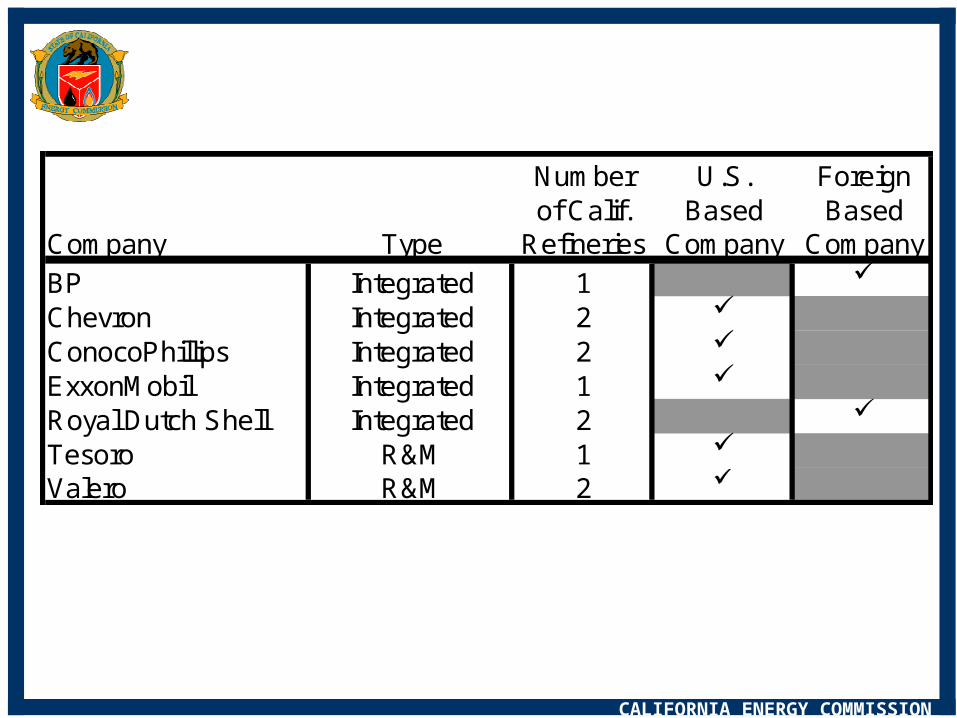

• Petroleum industry has consolidated over the last 50 years• Several measures of profitability were used to compare major oil

companies with other integrated oil companies on an international level.

• The companies in the petroleum industry were grouped into the following categories: exploration & production (E&P), integrated, and refining & marketing (R&M).

Financial Data of Petroleum Companies

CALIFORNIA ENERGY COMMISSION

Source: Used with the written permission of John S. Herold, Inc.

CALIFORNIA ENERGY COMMISSION

Number U.S. Foreignof Calif. Based Based

Company Type Refineries Company Company

BP Integrated 1 Chevron Integrated 2 ConocoPhillips Integrated 2 ExxonMobil Integrated 1 Royal Dutch Shell Integrated 2 Tesoro R&M 1 Valero R&M 2

CALIFORNIA ENERGY COMMISSION

Worldwide Net Income and Sources

-$2,500$0

$2,500$5,000$7,500

$10,000$12,500$15,000$17,500$20,000$22,500$25,000$27,500$30,000$32,500$35,000$37,500$40,000

BP

Ch

evr

on

Co

no

coP

hilli

ps

Exx

onM

ob

il

Sh

ell

Tes

oro

Va

lero BP

Ch

evr

on

Co

no

coP

hilli

ps

Exx

onM

ob

il

Sh

ell

Tes

oro

Va

lero BP

Ch

evr

on

Co

no

coP

hilli

ps

Exx

onM

ob

il

Sh

ell

Tes

oro

Va

lero BP

Ch

evr

on

Co

no

coP

hilli

ps

Exx

onM

ob

il

Sh

ell

Tes

oro

Va

lero

2003 2004 2005 First Half of 2006

Mill

ion

s o

f D

olla

rs

Non-Us Upstream US Upstream Non-US DownstreamUS Downstream Other Total Combined

Source: CEC analysis of company management reports, SEC 10-K, 10-Q, 20-F, and 6-K filings.

CALIFORNIA ENERGY COMMISSION

Profit Margins from Non-U.S. Operations

0%

5%

10%

15%

20%

25%

30%

35%

40%

Ch

evr

on

Co

no

co P

hill

ips

Exx

on M

ob

il

Ch

evr

on

Co

no

co P

hill

ips

Exx

on M

ob

il

Ch

evr

on

Co

no

co P

hill

ips

Exx

on M

ob

il

Ch

evr

on

Co

no

co P

hill

ips

Exx

on M

ob

il

Ch

evr

on

Co

no

co P

hill

ips

Exx

on M

ob

il

Ch

evr

on

Co

no

co P

hill

ips

Exx

on M

ob

il

Ch

evr

on

Co

no

co P

hill

ips

Exx

on M

ob

il

Ch

evr

on

Co

no

co P

hill

ips

Exx

on M

ob

il

2003 2004 2005 First Half2006

2003 2004 2005 First Half2006

Pro

fit

Mar

gin

(N

et In

co

me

/ Sal

es a

nd

Op

erat

ing

Rev

., in

cl.

inte

rseg

men

t re

v.)

Oil Exploration & Production Refining and Marketing

Source: CEC analysis of company management reports, SEC 10-K, 10-Q, 20-F, and 6-K filings.

CALIFORNIA ENERGY COMMISSION

Profit Margins from U.S. Operations

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Ch

evro

n

Co

noco

Ph

illip

s

Exx

on M

ob

il

Ch

evro

n

Co

noco

Ph

illip

s

Exx

on M

ob

il

Ch

evro

n

Co

noco

Ph

illip

s

Exx

on M

ob

il

Ch

evro

n

Co

noco

Ph

illip

s

Exx

on M

ob

il

Ch

evro

n

Co

noco

Ph

illip

s

Exx

on M

ob

il

Te

soro

Va

lero

Ch

evro

n

Co

noco

Ph

illip

s

Exx

on M

ob

il

Te

soro

Va

lero

Ch

evro

n

Co

noco

Ph

illip

s

Exx

on M

ob

il

Te

soro

Va

lero

Ch

evro

n

Co

noco

Ph

illip

s

Exx

on M

ob

il

Te

soro

Va

lero

2003 2004 2005 First Half2006

2003 2004 2005 First Half 2006

Pro

fit

Mar

gin

(N

et I

nco

me

/ S

ales

an

d O

per

atin

g R

ev.,

in

cl.

inte

rseg

men

t re

v.)

Oil Exploration & Production Refining and Marketing

Source: CEC analysis of company management reports, SEC 10-K, 10-Q, 20-F, and 6-K filings.

CALIFORNIA ENERGY COMMISSION

Summary

CALIFORNIA ENERGY COMMISSION

• Refinery Operations & Impact on Production– Gasoline production was lower due to unplanned refinery outages

• Inventory Levels– Gasoline levels were declining, but that is normal for the spring

• Pipeline Exports to Neighboring States, – Higher than 5 year average for gasoline– Higher than 5 year average for diesel fuel

• Congestion at Marine Terminals for Petroleum Imports– Increased at time of wholesale gasoline price spike

• March 2006 Alaska North Slope crude oil distribution system leak– Crude oil production declined by 100,000 barrels per day for 5 weeks

• Transition to New Fuel Specification– National transition away from MTBE (methyl tertiary butyl ether) to ethanol

increased price for important gasoline blendstock - alkylate– Switch to Ultra Low Sulfur Diesel (ULSD) on June 1, 2006 created a buildup of

inventories that were held in reserve as a precaution against startup problems for the new refinery equipment

Factors that Contributed to Price Spike

![STATE OF CALIFORNIA CALIFORNIA LAW REVISION COMMISSION · 1996] 191 STATE OF CALIFORNIA CALIFORNIA LAW REVISION COMMISSION RECOMMENDATION Unfair Competition Litigation November 1996](https://static.fdocuments.us/doc/165x107/5e087a1589d1845bbb4e6e15/state-of-california-california-law-revision-1996-191-state-of-california-california.jpg)