CAGP-ACPDP Conference Planned Giving Presentation ROBERT KLEINMAN FCA Mr. Prospect Thursday, May 13,...

31

CAGP-ACPDP Conference Planned Giving Presentation ROBERT KLEINMAN FCA Mr. Prospect Thursday, May 13, 2010 9:30am

-

Upload

ronald-andrews -

Category

Documents

-

view

214 -

download

0

Transcript of CAGP-ACPDP Conference Planned Giving Presentation ROBERT KLEINMAN FCA Mr. Prospect Thursday, May 13,...

CAGP-ACPDP ConferencePlanned Giving Presentation

ROBERT KLEINMAN FCA

Mr. Prospect

Thursday, May 13, 2010 9:30am

LEAVE A LEGACY

The legacy

The movement of the use of assets to community purposes at death

THE LEGACY DECISION TREE

LIFE INCO M E PLANS

TAX HELPNO T NEEDED

ESTATE PLANINSURANCE ?

TAX HELP NEEDEDAT DEAT H

W ILL BEQ UEST LIFE INSURANCEG IFT O R REPLACEM ENT

LEAVE A LEG ACY?

WILL BEQUEST

The will is an expression of final intentions Charitable gifts Designated for institution Designated for use Endowment, expense, equipment? Family philanthropy

LEGACY WILL METHOD

Complete will change or first will to be drawn up Codicil Concern over deductibility if institutions not spelled out-

leave to JCF with trustees Leave to JCF with a side contract-easier to change

your mind

Is mandate necessary?

TAX EFFECTS OF THE WILL

2 INCREDIBLE PROVISIONS

Will gift deemed to have been made in the year of death

Donation limit in the year of death (and preceding year) 100% of income

TAX PLANNING

Anticipate taxable income on death Tax shelter? Will gift!!!! Taxable income $200,000 Will gift $200,000 No tax

GIFT ON DEATH INTENTION

No tax need

Consider life income plans

Why? Effective gift on death Receive tax help now

CHARITABLE REMAINDER TRUST

Transfer property to a trust today Income beneficiary during lifetime- donor

(+spouse) Capital beneficiary

– Lifetime- none– Upon death- charity

CHARITABLE REMAINDER TRUST

Tax receipt today PV- (capital,mortality, interest) Ex. $100,000 male age 78 PV- ($100,000,8.1 years,4.5%) =$70,010

LIFE INSURANCE

Leave a larger gift Or to replace the gift capital for family

Traditional Charity owner + beneficiary Donor donates premiums

REPLACEMENT INSURANCE

Donate $300,000 RRSP’s Life insurance to estate $300,000

No gift RRSP’s worth $150,000 to family Insurance proceeds of $300,000 less cost of

premiums,say $75,000

NEW INSURANCE PRODUCTS

Corporate-owned Borrow from a bank for premiums and interest At death proceeds pay off loan Excess used to fund will gift CDA substantial

ESTATE PLANNING

A co.

Life Insurance

JCF

proceeds

Mr. A

•Taxable Income: $1,000,000•Will Gift: $1,000,000•Tax $0.00

•Tax Savings: $480,000•Insurance Cost: ?

ESTATE PLANNING - Illustration

Corporation to purchase $1,000,000 life insurance policy on last to die basis

On last to die, donors leave $1,000,000 in their wills to JCF At the second death, the corporation will receive

$1,000,000 tax free The corporation will remit $1,000,000 tax free to the estate

to pay will gift The deceased final tax return will utilize a $1,000,000 tax

receipt from the JCF, saving $480,000 of tax

ESTATE PLANNING - IllustrationPresent value of financial considerationsLife expectancy based on life insurance tables

Estate savings- 480,000$ 12 years at 4.5% 283,039$

Premium costs

year premium PV at 4.5%1 37,200$ 37,200$ 2 37,200$ 35,598$ 3 37,200$ 34,065$ 4 37,200$ 32,598$ 5 37,200$ 31,194$ 6 37,200$ 29,851$ 7 37,200$ 28,566$ 8 37,200$ 27,336$ 9 37,200$ 26,158$

10 37,200$ 25,032$ 11 37,200$ 23,954$ 12 37,200$ 22,923$

354,476$

ESTATE PLANNING - Illustration

The cost of life insurance, at present value is With no life insurance purchase, the corporation

would transfer to the estate $354,476 on which the estate would pay 24% tax, leaving the estate with

The estate will save $480,000 on the deceased final tax return which, at present value represents

The net cost of creating $1,000,000 of charity is a saving of

$354,476

$269,402

$283,039

$13,637

PREFERRED SHARES

$1 million of preferred Gift to JCF Insurance on children Saves $500,000 in cash flow Continuation of estate freeze

PREFERRED SHARES

Aco BcoAco subscribes for preferred shares of Bco

JCF BcoOwns preferred shares of Bco

•Gift to JCF: $2,000,000•Tax Saving: $1,000,000•Insurance Cost: ?

Insurance policy

B co. could lend back to A co. at X% int.

Gift

to

JCF

PREFERRED SHARES- Illustration

CASH FLOW FOR DONOR– Gift of preferred shares– Insurance premiums– Tax savings– Net cost for donor

BENEFIT FOR ESTATE– CDA benefit – tax savings on taxable dividend

TOTAL NET FOR DONOR’S FAMILY Life expectancy 25years, interest 4.5%

$2,000,000

$(402,882)

$1,000,000

$ 597,118

$ 218,638

$ 815,755

MARKETABLE SECURITIESTax Advantages

Example: Mr. Jones donates $100,000 of Royal Bank of

Canada stock to the JCF His alternative is to sell the stock and donate

$100,000

SALE vs. GIFT Stock Sale Stock Donation

Combined Federal Quebec Combined

Proceeds $100,000 $100,000 $100,000

Cost $50,000 $50,000 $50,000

Capital Gain $50,000 $50,000 $50,000

Taxable Capital Gain $25,000 $25,000 $25,000

Special Exemption ($0) ($25,000) ($25,000)

Net Income $25,000 $0 $0

Income Taxes Payable

$12,000 $0 $0 $0

Tax Receipt $100,000 $100,000 $100,000

Tax Savings $48,000 $24,000 $24,000 $48,000

Net Tax Savings $36,000 $24,000 $24,000 $48,000

Example:

Holdco makes a gift of $500,000 worth of securities to the JCF.

Adjusted cost base = $0

Capital Gain = $500,000

Tax Implications: Since for Federal and Quebec purposes there is no taxable capital gain, the full $500,000 flows through to Holdco’s CDA and can be paid out tax free to the shareholders of Holdco.

MARKETABLE SECURITIESCORPORATE GIFTS

MARKETABLE SECURITIES POST MORTEM TAX PLANNING

Deemed disposition of all assets on death. Gifts made in the will are deemed to be made

in the year of death. Full amount of donation receipt to be applied to

reduce taxes in the year of death. Reduce death taxes by donating marketable

securities.

POST MORTEM TAX PLANNING CONTINUED

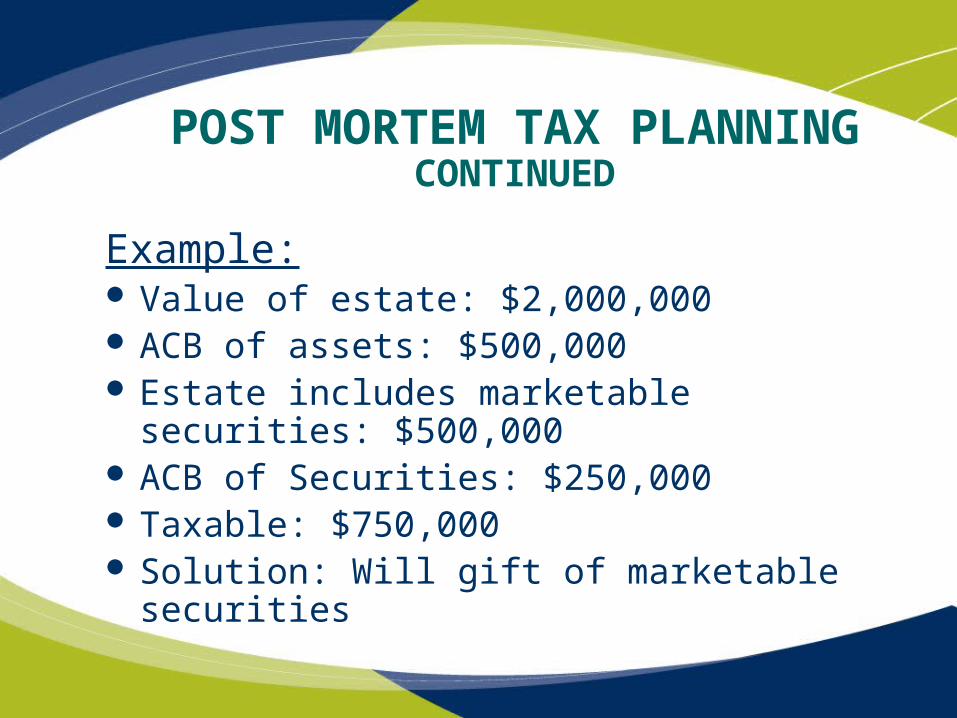

Example: Value of estate: $2,000,000 ACB of assets: $500,000 Estate includes marketable securities:

$500,000 ACB of Securities: $250,000 Taxable: $750,000 Solution: Will gift of marketable securities

POST MORTEM TAX PLANNING CONTINUED

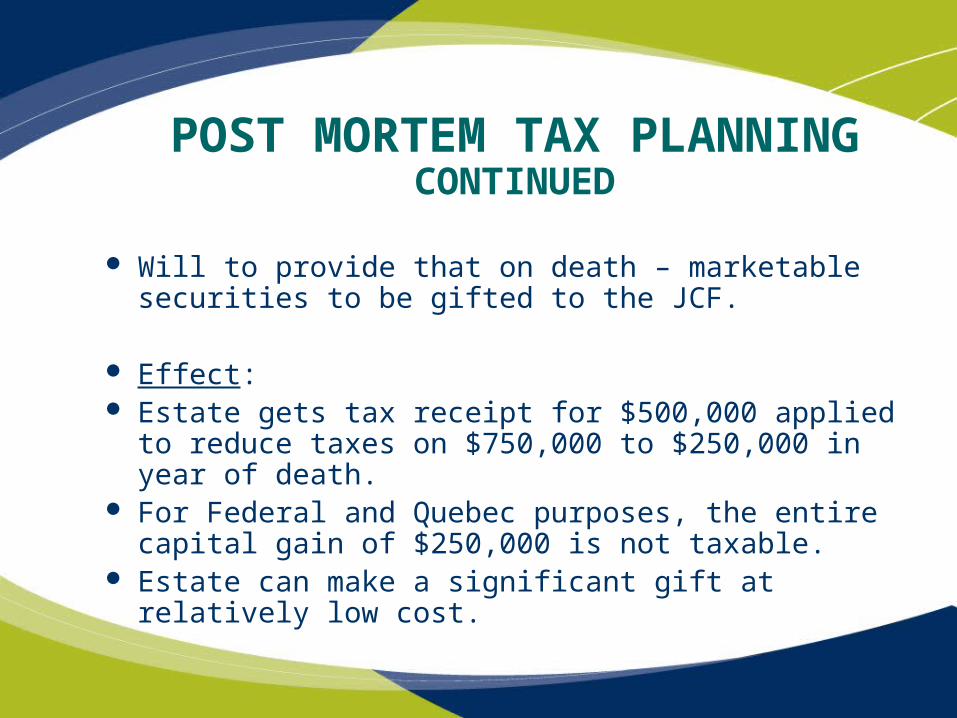

Will to provide that on death – marketable securities to be gifted to the JCF.

Effect: Estate gets tax receipt for $500,000 applied to reduce

taxes on $750,000 to $250,000 in year of death. For Federal and Quebec purposes, the entire capital

gain of $250,000 is not taxable. Estate can make a significant gift at relatively low cost.

MARKETABLE SECURITIES FLOW THROUGH SHARES

Donor may purchase resource (mining or oil and gas) partnership units, convert the units into shares and then donate these shares to a charity.

Flow- thrus

Public ruling Combination of 2 incentives Popular today

example

Acquisition $211,423

Federal 211423 x .2422 51,207 Quebec 211423 x 150% x .24 76,112 Federal credit .15 x 211423 31,713 Income inclusion 31,713 x .2422 -7,681 Donation 117,457 x .4822 56,638

Net cost $3,434 Charity receives $117,457 Fees to sell 17,457 Net charity $100,000

issues

Must do exploration Value of receipt- high fees Need lots of taxable income- AMT

corporate

100% write off only CDA account huge Cost 20 cents After cda value -negative