Cabot Oil & Gas Slide Presentation at Merrill Lunch Energy Conference

22

INVESTOR PRESENTATION BAML Global Energy Conference November 13, 2014

-

Upload

marcellus-drilling-news -

Category

News & Politics

-

view

646 -

download

3

description

The slide presentation used by Cabot Oil & Gas at the November 2014 Merrill Lynch Energy Conference in Miami, FL. The slides provide an update on Cabot's Marcellus Shale drilling program in Susquehanna County, PA, along with details on their new and growing Eagle Ford drilling program.

Transcript of Cabot Oil & Gas Slide Presentation at Merrill Lunch Energy Conference

INVESTOR PRESENTATION BAML Global Energy Conference November 13, 2014

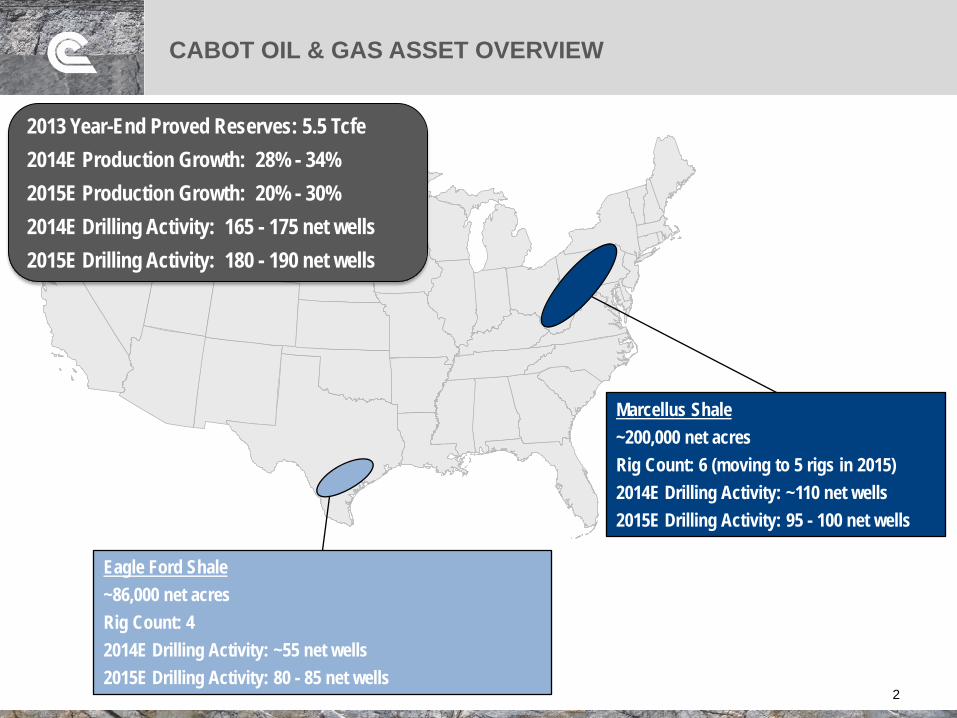

CABOT OIL & GAS ASSET OVERVIEW

2

Marcellus Shale ~200,000 net acres Rig Count: 6 (moving to 5 rigs in 2015) 2014E Drilling Activity: ~110 net wells 2015E Drilling Activity: 95 - 100 net wells

Eagle Ford Shale ~86,000 net acres Rig Count: 4 2014E Drilling Activity: ~55 net wells 2015E Drilling Activity: 80 - 85 net wells

2013 Year-End Proved Reserves: 5.5 Tcfe 2014E Production Growth: 28% - 34% 2015E Production Growth: 20% - 30% 2014E Drilling Activity: 165 - 175 net wells 2015E Drilling Activity: 180 - 190 net wells

WELL POSITIONED TO NAVIGATE A CHALLENGING MARKET IN 2015

3

Cabot’s best-in-class asset base provides competitive rates-of-return at “downside” commodity prices

– Marcellus: ~37% IRR at $2.00/Mmbtu realized price

– Eagle Ford: ~34% IRR at $70.00/Bbl realized price

Strategy is to provide returns-focused growth as opposed to “growth for the sake of growth”

– Cabot expects to generate >20% production growth in 2015 despite a challenged commodity price environment based on relatively flat drilling and completion spending

– However, we will remain flexible and may call an audible, if necessary, if our outlook changes throughout the year

– Anticipate top-tier return-on-capital despite lower realizations

– Modest level of outspend anticipated under budgeted commodity price realizations

Strong balance sheet provides financial flexibility in a low commodity price environment

– Conservative leverage position: Debt / LTM EBITDAX of 1.2x as of 9/30/2014

– Ample liquidity: $1.4 billion revolving credit facility undrawn as of 9/30/2014

– Hedge position provides downside protection: ~25% of 2015E Marcellus natural gas production hedged

KEY INVESTMENT HIGHLIGHTS

4

Extensive Inventory of Low-Risk, High-Return Drilling Opportunities

Top-Tier Production and Reserve Growth

Low Cost Structure

Strong Financial Position and Financial

Flexibility

– Over 3,000 locations in the sweet spot of the Marcellus Shale, implying 25+ years of inventory at current drilling levels

– Peer-leading rates of return and EUR per lateral foot in the Marcellus Shale

– Oil-focused initiative in the Eagle Ford Shale with 1,050 – 1,350 locations (based on 300’ to 400’ spacing)

– 2014 production growth guidance of 28% - 34%

– Initial 2015 production growth guidance of 20% - 30%

– 2013 proved reserve growth of 42% resulting in a three-year reserve CAGR of 26%

– 2013 total company all-sources finding costs of $0.55 per Mcfe

– 2013 Marcellus-only all-sources finding costs of $0.40 per Mcf

– 2014 total company per unit cash cost1 guidance of ~$1.25 per Mcfe

– 2014 Marcellus-only per unit cash cost1 guidance of ~$0.75 per Mcf

– Target investment grade leverage metrics (Debt / LTM EBITDAX2 of 1.2x as of 9/30/2014)

– $1.4 billion of borrowing capacity available under our credit facility as of 9/30/2014

– Continue to opportunistically add to our 2015 hedge position (~25% of 2015E Marcellus production is currently hedged)

1Excludes DD&A, exploration expense, stock-based compensation and pension termination expenses 2 EBITDAX is a non-GAAP measure calculated as follows: Net income + Depreciation, depletion and amortization + (Gain)/loss on sale of assets + Exploration expense + Unrealized (gain)/loss on derivative instruments + Stock-based compensation + (Earnings)/loss on equity method investments + Interest expense + Income tax expense

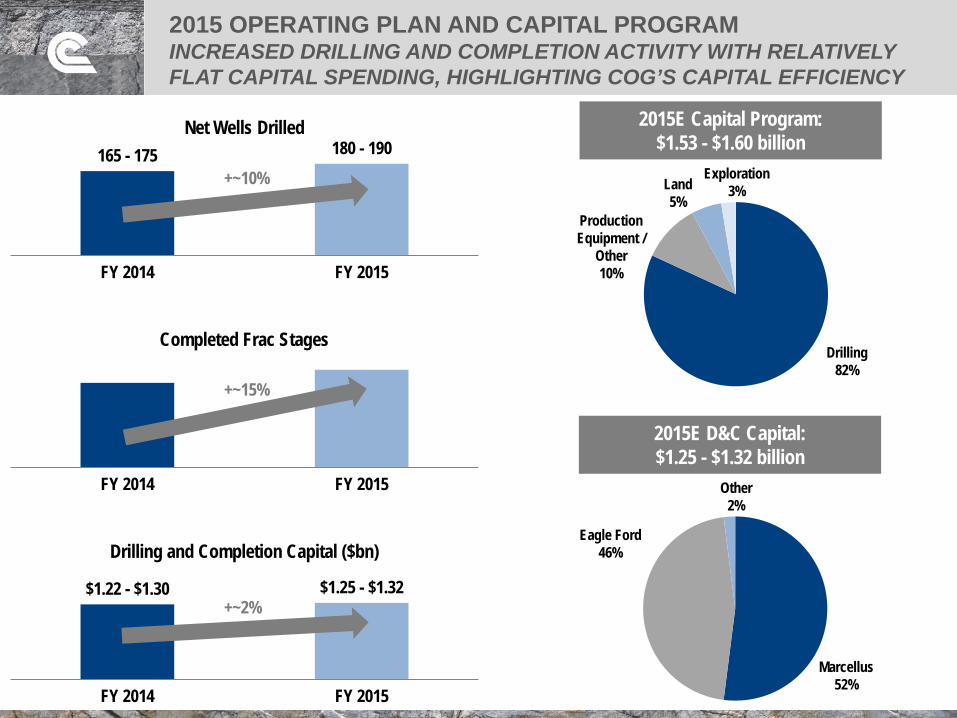

2015E Capital Program: $1.53 - $1.60 billion

Land 5%

Drilling 82%

Production Equipment /

Other 10%

Exploration 3%

2015 OPERATING PLAN AND CAPITAL PROGRAM INCREASED DRILLING AND COMPLETION ACTIVITY WITH RELATIVELY FLAT CAPITAL SPENDING, HIGHLIGHTING COG’S CAPITAL EFFICIENCY

FY 2014 FY 2015

Completed Frac Stages

165 - 175 180 - 190

FY 2014 FY 2015

Net Wells Drilled

$1.22 - $1.30 $1.25 - $1.32

FY 2014 FY 2015

Drilling and Completion Capital ($bn)

+~10%

+~15%

+~2%

2015E D&C Capital: $1.25 - $1.32 billion

Marcellus 52%

Eagle Ford 46%

Other 2%

PROVEN TRACK RECORD OF PRODUCTION GROWTH…

6

130.6

187.5

267.7

413.6

0

100

200

300

400

500

600

700

2010 2011 2012 2013 2014E 2015E

Bcfe

LiquidsGas

43.5%

42.8%

54.5%

2014 Guidance: 28% - 34%

2015 Guidance: 20% - 30%

~7% liquids in 2015, up from ~5% in 2014

…AND RESERVE GROWTH

7

2.7 3.0

3.8

5.5

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

2010 2011 2012 2013 2014E 2015E

Tcfe

LiquidsGas

12.3%

26.7%

41.9%

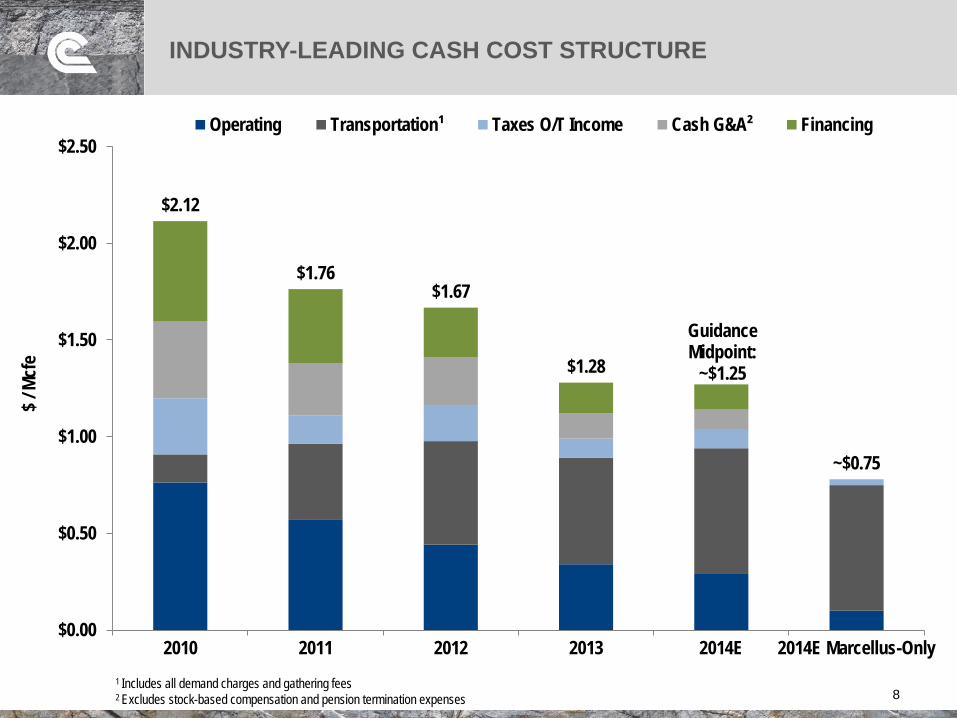

INDUSTRY-LEADING CASH COST STRUCTURE

8

$2.12

$1.76 $1.67

$1.28

Guidance Midpoint:

~$1.25

~$0.75

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

2010 2011 2012 2013 2014E 2014E Marcellus-Only

$ / M

cfe

Operating Transportation¹ Taxes O/T Income Cash G&A² Financing

1 Includes all demand charges and gathering fees 2 Excludes stock-based compensation and pension termination expenses

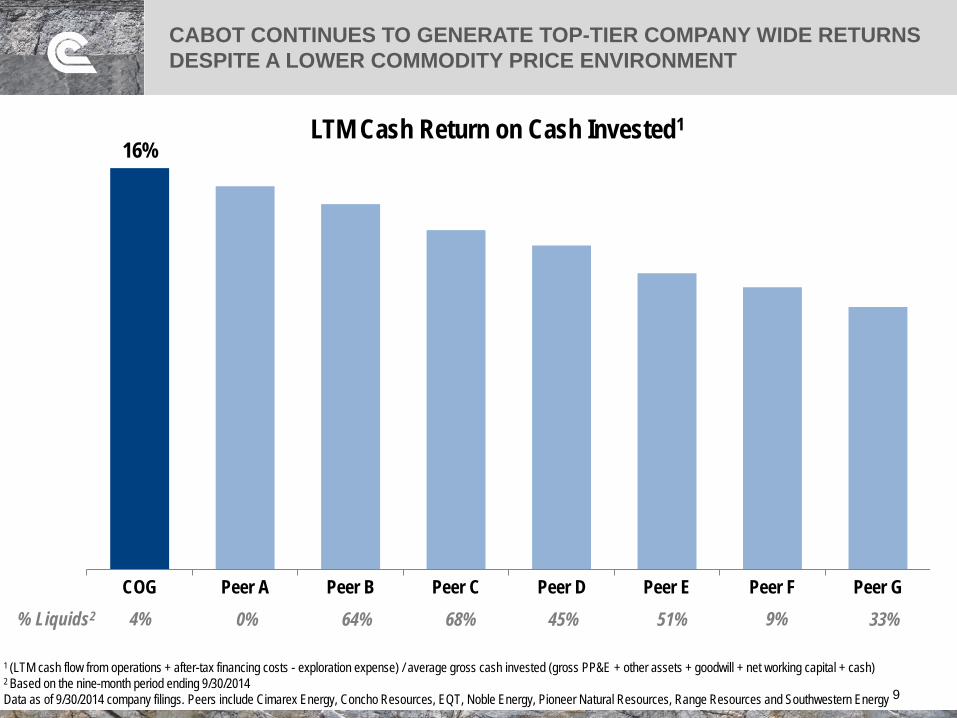

CABOT CONTINUES TO GENERATE TOP-TIER COMPANY WIDE RETURNS DESPITE A LOWER COMMODITY PRICE ENVIRONMENT

16%

COG Peer A Peer B Peer C Peer D Peer E Peer F Peer G

LTM Cash Return on Cash Invested1

% Liquids2 4% 0% 64% 68% 45% 51% 9% 33%

1 (LTM cash flow from operations + after-tax financing costs - exploration expense) / average gross cash invested (gross PP&E + other assets + goodwill + net working capital + cash) 2 Based on the nine-month period ending 9/30/2014 Data as of 9/30/2014 company filings. Peers include Cimarex Energy, Concho Resources, EQT, Noble Energy, Pioneer Natural Resources, Range Resources and Southwestern Energy

9

FOCUSED ON ENHANCING SHAREHOLDER VALUE

Repurchased 4.3mm shares YTD and 9.1mm shares since Q3 2013

10

Added 33,000 net acres in the Eagle Ford during 2014

High-graded our asset portfolio through non-core asset sales totaling over $365mm since Q3 2013 with proceeds used to

fund share repurchases and Eagle Ford expansion

Currently testing downspacing in both the Marcellus and Eagle Ford, potentially resulting in further resource / NAV expansion

Continue to test exploration concepts throughout our portfolio

Continue to optimize operating efficiencies resulting in continued cost savings

CABOT’S MARCELLUS SHALE SUMMARY

~200,000 net acres

Operated rig count: 6 (decreasing to 5 in 2015)

2015E drilling activity: 95 - 100 net wells

2015E gross daily production: 1.8 – 2.0 Bcf/d

– Production levels will ultimately be dictated by price realizations

– Flexibility to accelerate / decelerate completion capital throughout the year

Reduction in drilling and completion activity in 2015 is predicated on lower anticipated natural gas price realizations throughout Appalachia as we await the in-service of new takeaway capacity

COG plans to re-accelerate activity upon the in-service of Constitution Pipeline in late 2015 / 2016

COG’s best-in-class Marcellus assets generate >80% IRR at our 2015 budget price realization of $2.80

Currently testing 500’ downspacing between laterals, which would increase inventory / resource potential / NAV, if successful

1.5 - 1.6 1.8 – 2.0

FY 2014 FY 2015

Gross Marcellus Production (Bcf/d)

6 5

FY 2014 FY 2015

Marcellus Rig Count

$800 - $850 $650 - $700

FY 2014 FY 2015

Marcellus Drilling and Completion Capital ($mm)

2,190

1,418

824 751 746 634

498 385 346 321

Peer A COG Peer B Peer C Peer D Peer E Peer F Peer G Peer H Peer I

1H 2014 Daily Gross Production From Unconventional Horizontal Wells in Pennsylvania (Mmcfe/d)

# of Hz producing wells 656 307 693 212 262 281 387 152

Source: PA DEP Website; Peers include Anadarko Petroleum, Chesapeake Energy, Chevron, EQT, Range Resources, Seneca Resources, Southwestern Energy, Shell and Talisman 12

223 296

HIGHLY PRODUCTIVE, LOW CAPITAL INTENSITY MARCELLUS ASSETS

13 of the top 20 wells (January to June 2014) 17 of the top 20 wells (July to December 2013) 15 of the top 20 wells (January to June 2013) 10 of the top 20 wells (July to December 2012) 14 of the top 20 wells (January to June 2012) 15 of the top 20 wells (July to December 2011) 7 of the top 20 wells (January to June 2011) 10 of the top 20 wells (July to December 2010)

0%

2%

4%

6%

8%

10%

12%

14%

16%

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

2H 2010 1H 2011 2H 2011 1H 2012 2H 2012 1H 2013 2H 2013 1H 2014

% o

f well

s / p

rodu

ctio

n

# of p

rodu

cing

horiz

onta

l well

s

# of COG Wells # of Total Wells COG % of Wells COG % of Total Production

Source: PA DEP Website; based on horizontal producing wells only 13

CABOT HAS ACCOUNTED FOR ~14% OF PENNSYLVANIA’S PRODUCTION FROM ONLY ~6% OF THE TOTAL PRODUCING WELLS

CABOT’S EUR PER FOOT AND F&D COSTS REMAIN BEST-IN-CLASS IN THE MARCELLUS AND UTICA

$0.40

$0.60

$0.80

$1.00

$1.20

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Impl

ied F

&D C

ost (

$/Mcf

e)

EUR

per 1

,000 f

t. of

late

ral (

Bcfe

)

Source: Company presentations; peers include Antero Resources, EQT Corporation, Gulfport Energy, Noble Energy, Range Resources, and Rice Energy 14

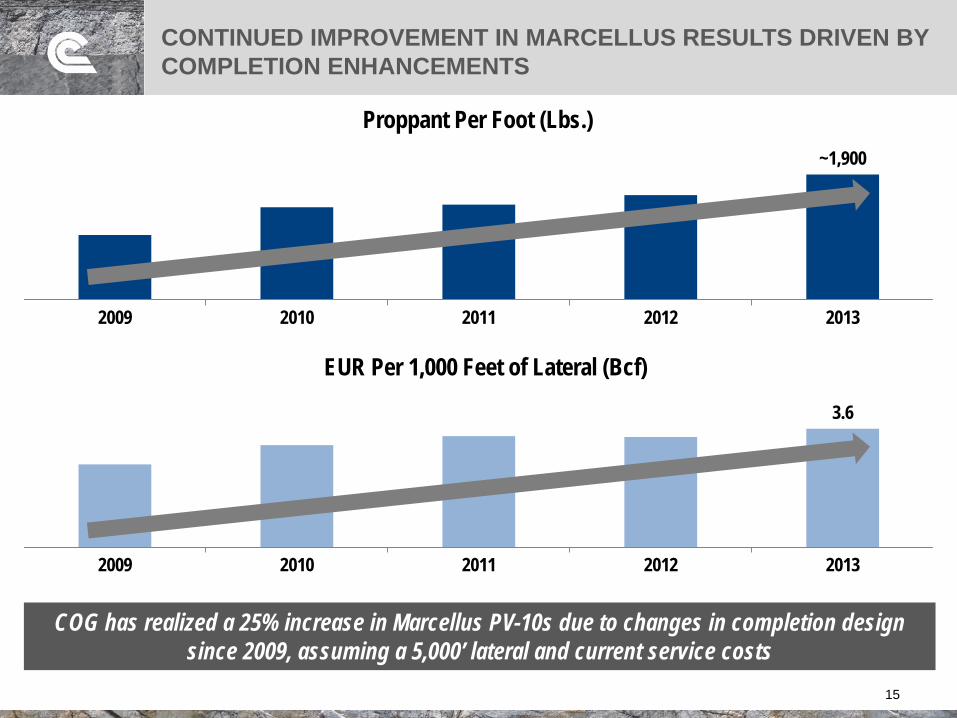

CONTINUED IMPROVEMENT IN MARCELLUS RESULTS DRIVEN BY COMPLETION ENHANCEMENTS

15

~1,900

2009 2010 2011 2012 2013

Proppant Per Foot (Lbs.)

3.6

2009 2010 2011 2012 2013

EUR Per 1,000 Feet of Lateral (Bcf)

COG has realized a 25% increase in Marcellus PV-10s due to changes in completion design since 2009, assuming a 5,000’ lateral and current service costs

CABOT’S MARCELLUS SHALE ECONOMICS

16

Typical Marcellus Well Parameters (Based on 2013 Program)

EUR: 16.9 Bcf

Well Cost: $7.0 million

Lateral Length: 4,666’

Number of Stages Per Well: 23

Average Working Interest: 100%

Average Revenue Interest: 85%

37% 65%

102%

150%

206%

0%

50%

100%

150%

200%

250%

$2.00 $2.50 $3.00 $3.50 $4.00

BTA

X %

IRR

Realized Natural Gas Price ($/Mmbtu)

Typical Marcellus Well IRR Sensitivity

Cabot plans to drill longer laterals in 2014 relative to the 2013 program

>80% rate of return at 2015 budget realized price of $2.80

600 - 800

1,050 - 1,350

Gross Drilling Locations

~53,000

~86,000

Net Acres

CABOT’S EAGLE FORD SHALE SUMMARY

17

Frio

La Salle

Atascosa

McMullen

COG Eagle Ford Shale Acreage Position

Buckhorn ~75K net acres

Q1 2014 Current

~86,000 net acres

– Buckhorn: ~75,000 net acres

– Presidio: ~11,000 net acres

– ~11,000 net acres of additional exploratory acreage not included in acreage totals

Operated rig count: 4

Q3 2014 net production: 10,347 Boe/d

Plan to place 15 wells on production during Q4 2014

2015E drilling activity: 80 - 85 net wells

2015E net liquids production: 18,000 - 20,000 Bbls/d

Currently testing 300’ downspacing, which would increase gross drilling inventory from ~1,050 to ~1,350

~11 years of drilling inventory at 400’ spacing and ~14 years of drilling inventory at 300’ spacing (based on 2015 drilling program)

Presidio ~11K net acres

1

1 Gross drilling location ranges based on the difference between 300’ and 400’ spacing

0

10,000

20,000

30,000

40,000

50,000

0 30 60 90

Cum

ulat

ive O

il Pro

duct

ion

(Bbl

)

Days on Production

YTD 2014 Program (27 wells) 2013 Program (18 wells) 500 Mboe Type Curve

CABOT’S 2014 EAGLE FORD SHALE PROGRAM CONTINUES TO OUTPERFORM

18 Note: Production data has been normalized to a 7,000’ lateral; not all 27 wells included in the YTD 2014 population have 90 days of production data

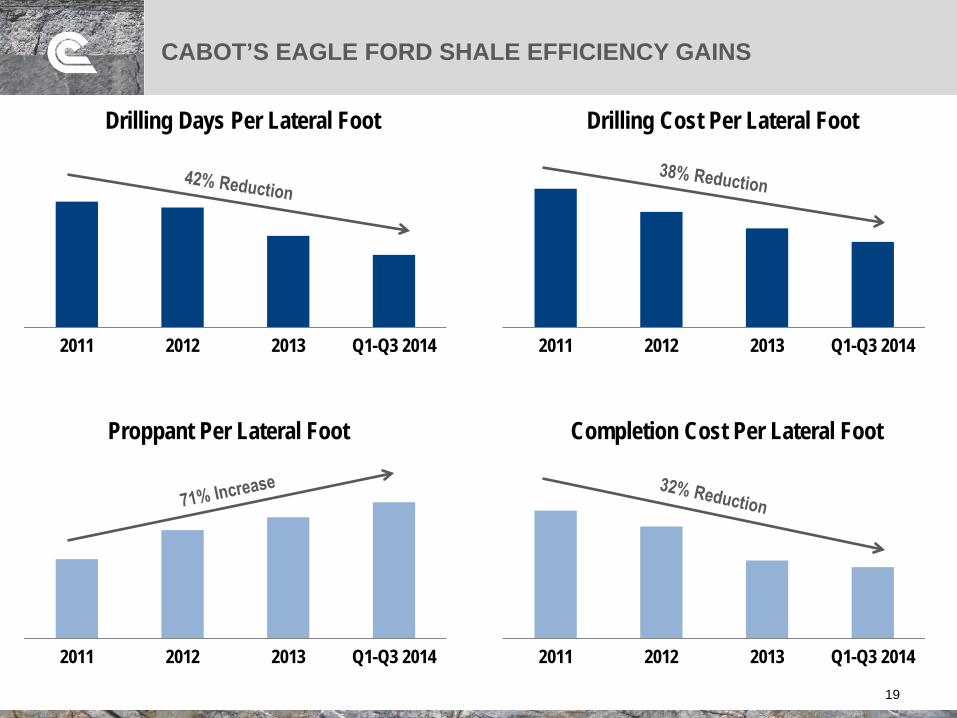

2011 2012 2013 Q1-Q3 2014

Drilling Days Per Lateral Foot

CABOT’S EAGLE FORD SHALE EFFICIENCY GAINS

19

2011 2012 2013 Q1-Q3 2014

Drilling Cost Per Lateral Foot

2011 2012 2013 Q1-Q3 2014

Proppant Per Lateral Foot

2011 2012 2013 Q1-Q3 2014

Completion Cost Per Lateral Foot

34% 48%

66%

86%

0%

20%

40%

60%

80%

100%

$70.00 $80.00 $90.00 $100.00

BTA

X %

IRR

WTI Oil Price ($/Bbl)

CABOT’S EAGLE FORD SHALE ECONOMICS

20

Typical Eagle Ford Well Parameters

EUR: ~500 MBoe

Well Cost: $7.0 million

Lateral Length: 7,000’

Product Mix: ~80% oil / 12% NGL / 8% natural gas

Average Working Interest: 100%

Average Revenue Interest: 75%

Typical Eagle Ford Well IRR Sensitivity

Note: Economics include facilities costs. Assumes Henry Hub price of $4.00 and NGL price of 40% of WTI. 1 2015 WTI strip as of 11/8/2014

>45% rate of return at current 2015 WTI strip of $791

UPDATE ON FUTURE TAKEAWAY / MARKETING OPPORTUNITIES

Constitution Pipeline • FERC issued Final Environmental Impact

Statement (EIS) on Oct. 24th • EIS confirmed that Constitution Pipeline can be

constructed in a manner that minimizes environmental impact

• FERC Order expected as early as Dec. 2014 • Target in-service: Late-2015 through 2016 • Impact to COG: ~500 Mmcf/d of firm capacity

to premium markets in Boston and Long Island

21

Future takeaway projects provide line-of-sight to over 3 Bcf/d of Cabot production by YE 2017

Leidy Southeast Expansion • FERC issued Environmental Assessment (EA)

on Aug. 11th • Target in-service: December 2015 • Impact to COG: ~125 Mmcf/d of firm sales to

shippers on Leidy Southeast; project will move ~525 Mmcf/d off of the Leidy Line and down the Atlantic Seaboard, which could be supportive to Leidy Line prices

Atlantic Sunrise (Central Penn Line) • Currently in the pre-filing process; expected to

file formal application with FERC in Mar. 2015 • ~85% of the preliminary route already surveyed • Target in-service: 2H 2017 • Impact to COG: ~850 Mmcf/d of firm capacity

(100% of volumes already sold under long-term sales contracts); project will move ~1.7 Bcf/d out of the Marcellus producing region, which could be supportive to Appalachia prices

Cove Point LNG Export Project • Dominion accepted FERC order in Sep. 2014 • Initial construction began in Oct. 2014 • Target in-service: 2H 2017 • Impact to COG: ~350 Mmcf/d of long-term

sales to Pacific Summit at Cove Point; project should be supportive to domestic natural gas prices

Thank you

The statements regarding future financial performance and results and the other statements which are not historical facts contained in this presentation are forward-looking statements that involve risks and uncertainties, including, but not limited to, market factors, the market price of natural gas and oil, results of future drilling and marketing activity, future production and costs, and other factors detailed in the Company’s Securities and Exchange Commission filings.

22