Cable in Europe: Innovation-driven growth in a hyper … · · 2018-01-25Cable in Europe:...

26

Confidential. © 2017 IHS Markit TM . All Rights Reserved. Confidential. © 2017 IHS Markit TM . All Rights Reserved. Cable in Europe: Innovation-driven growth in a hyper-competitive market Maria Rua Aguete, IHS Markit January 2018 maria_aguete

Transcript of Cable in Europe: Innovation-driven growth in a hyper … · · 2018-01-25Cable in Europe:...

Confidential. © 2017 IHS MarkitTM. All Rights Reserved. Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

Cable in Europe: Innovation-driven

growth in a hyper-competitive market Maria Rua Aguete, IHS Markit

January 2018

maria_aguete

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

2

IHS Markit analysts are among the most respected, experienced, influential, and quoted in the business

Who are we? Information, insight, and analytics across critical technology markets

Automotive Electronics

• Electronic systems & semiconductors

• Cost management

• Connected car

Displays

• Display manufacturing

& supply chain

• Display materials & components

• Large displays

• Small & medium displays

• Touch & interface

Enterprise & IT

• Data center & cloud

• Enterprise networks & communication

• Enterprise IT security

• M2M, IoT & connectivity

Healthcare Technology

• Medical devices & equipment

• Healthcare IT

Manufacturing Technology

• Capital equipment & machinery

• Electric motor systems

• Discrete & process automation

Media & Advertising

• Advertising

• TV media & content

• Video

• Digital media

• Games

• Cinema

Mobile & Telecom

• Operators & services

• Mobile innovation

• Mobile networks

• Voice & data networks

• Service provider Broadband & video

• Managed services

Mobile, Consumer & Connected

Devices

• Mobile devices

• Consumer electronics

• Lighting

• Digital signage

• Smart home & appliances

Power & Energy Technology

• Smart grid & energy storage

• Power supplies & wireless charging

• Solar

Security Technology

• Access control & fire

• Video surveillance

• Cybersecurity & digital ID

• Critical communications

Semiconductors

• Semiconductor market

• Semiconductor components

• Semiconductor manufacturing

• MEMS & sensors

• Memory & storage

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

European Broadband Cable 2017

Published in December 2017

Now in it’s 17th year

The only definitive and fully comprehensive data report on the

EU28 cable markets

Historic and current data on the size and value of the industry

Review and analysis of latest industry trends

3

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

0

10

20

30

40

50

60

70

80

90

100

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Penetr

ation (

%)

Pay TV penetration by region

Asia Pacific Eastern Europe Latin America Middle East and Africa Western Europe

Source: IHS Markit

Traditional pay TV is still growing everywhere except North America – cord-cutting

has not spread

• Other regions have not fallen victim to

the same factors that left North America

vulnerable:

> High pay TV penetration – little room

for organic growth

> High price of subscriptions

> Slow response to competition in the

online-video space with innovation of

their own

> Poor and much-maligned customer

service

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

0

10

20

30

40

50

60

70

80

90

100

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Penetr

ation (

%)

Pay TV penetration by region

Asia Pacific Eastern Europe Latin America Middle East and Africa North America Western Europe

Source: IHS Markit

Traditional pay TV is still growing everywhere except North America – cord-cutting

has not spread

• Other regions have not fallen victim to

the same factors that left North America

vulnerable:

> High pay TV penetration – little room

for organic growth

> High price of subscriptions

> Slow response to competition in the

online-video space with innovation of

their own

> Poor and much-maligned customer

service

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

What is the ARPU for Cable TV in the US vs the rest of the world?

$86

$23

$6

$7

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

Triple play package Unbundled set up

£48 a month

£33.49 a month

£7.99 a month (HD Package)

£7.99 a month

(Standard Entertainment

pack)

£7.99 a month

£57.46 a month

Broadband

Netflix

NowTV

Amazon Insant Prime

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

In Europe pay TV is still growing and most Europeans still receive their pay TV via

cable

8

Source: IHS Markit

46

48

50

52

54

56

58

60

62

0

20

40

60

80

100

120

140

160

180

200

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Penetr

ation (

%)

Subscriptions (

m)

Pay TV and online video subscriptions in EU28

Online video

Pay DTT

IPTV

Satellite

Cable

Pay TV penetration (%)

• The role online video has played has been to expand the overall market for subscription video

55.5m

50.1m

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

But Cable TV subscribers have been declining since 2009

0

10

20

30

40

50

60

70

80

-1,200

-1,000

-800

-600

-400

-200

0

200

400

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Penetr

ation (

%)

Net

additio

ns (

000)

Cable TV net additions and digital TV penetration in EU28

Cable TV net adds Digital as a % of total cable TV

9

Source: IHS Markit

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

However, digital transition is helping drive up cable TV ARPUs – up 17% in last 5

years

0

2

4

6

8

10

12

14

16

18

0

2

4

6

8

10

12

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Month

ly A

RP

U (

€)

Revenue (

€bn)

Cable TV revenues by type and monthly ARPU in EU28

Analogue

Digital

TV ARPU

10

Source: IHS Markit

• The higher value of digital TV subscriptions has compensated for overall declines in cable TV customers

• Cable TV subscriptions were worth an average of €16.75 a month in 2017 – lower than satellite (€31.40/month) but higher than IPTV (€14/month)

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

The power of the bundle: cable operators have grown total ARPUs 21% in 5

years by selling more services

0

5

10

15

20

25

30

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

AR

PU

(€)

RG

Us (

m)

Total Europe: cable operator revenue generating units

Total TV Internet Telephony ARPU (€)

11 © 2016 IHS

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

-10

-5

0

5

10

15

20

Western Europe Eastern Europe North America Latin America Middle East and Africa

Net

additio

ns (

m)

Cable Satellite IPTV Pay DTT

0

20

40

60

80

100

120

140

Asia Pacific

Net

additio

ns (

m)

Pay TV net additions by region and platform, 2011-2017

Source: IHS Markit

Cable’s loss has been IPTV and satellite’s gain, with telcos driving subscriber growth

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

Cable broadly achieved solid growth in 2017, with broadband the star performer

13.5

4.9

3.5

2.2

-0.1

-5 0 5 10 15

Digital cable TV subscribers

Cable Internet subscribers

Cable telephony subscribers

Total cable RGUs

Total cable TV subscribers

% change

Subscribers and revenue-generating units

13

7.1

4.5

3.8

3.5

1.5

3.4

2.7

-0.8

-2 0 2 4 6 8

Cable Internet revenue

Total cable revenue

Cable ARPU

Cable TV ARPU

Cable Internet ARPU

Cable TV revenue

Cable telephony revenue

Cable telephony ARPU

% change

Revenues and average revenue per user

Growth in key cable metrics in EU28, 2016-2017

Source: IHS Markit

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

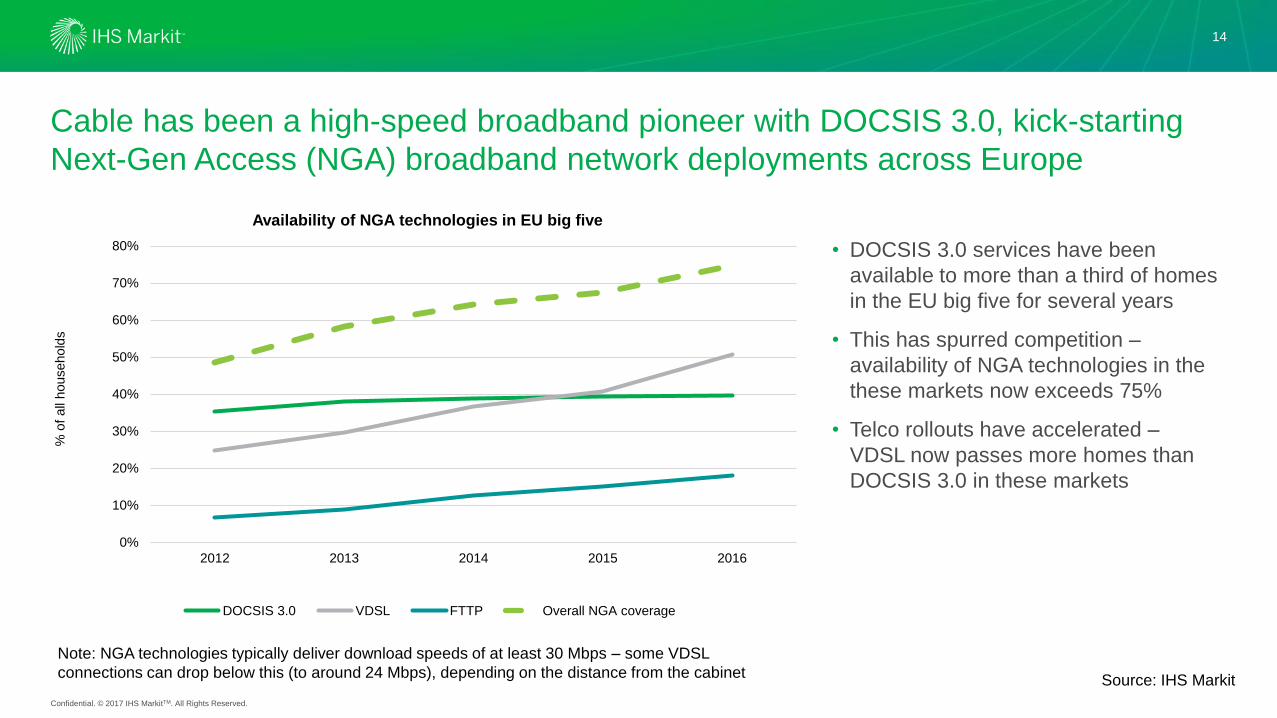

Cable has been a high-speed broadband pioneer with DOCSIS 3.0, kick-starting

Next-Gen Access (NGA) broadband network deployments across Europe

14

0%

10%

20%

30%

40%

50%

60%

70%

80%

2012 2013 2014 2015 2016

% o

f all

household

s

Availability of NGA technologies in EU big five

DOCSIS 3.0 VDSL FTTP Overall NGA coverage

Source: IHS Markit

• DOCSIS 3.0 services have been

available to more than a third of homes

in the EU big five for several years

• This has spurred competition –

availability of NGA technologies in the

these markets now exceeds 75%

• Telco rollouts have accelerated –

VDSL now passes more homes than

DOCSIS 3.0 in these markets

Note: NGA technologies typically deliver download speeds of at least 30 Mbps – some VDSL

connections can drop below this (to around 24 Mbps), depending on the distance from the cabinet

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

But cable is doing a better job of maximising the return on its NGA investment,

converting a higher percentage of subscribers to the faster top-tier technology

15

0%

10%

20%

30%

40%

50%

60%

70%

2011 2012 2013 2014 2015 2016

Convers

ion r

ate

(%

)

DOCSIS 3.0 and VDSL and as a % of total cable and DSL connections in EU big five

VDSL as a % of all DSL connections DOCSIS 3.0 as a % of all cable connections

Source: IHS Markit

• More than two-thirds of all cable broadband subscriptions in the EU big five are NGA, compared to around 15% for DSL

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

DOCSIS 3.0’s success has put broadband on the path to becoming cable’s biggest

revenue generator

€9.6bn 53%

€4.9bn 27%

€3.7bn 20%

2010

TV Internet Telephony

€11.1bn 45%

€8.5bn 35%

€4.9bn 20%

2017

TV Internet Telephony

16

Source: IHS Markit

Cable revenue by source in EU28

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

How important is content for a cable operator?

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

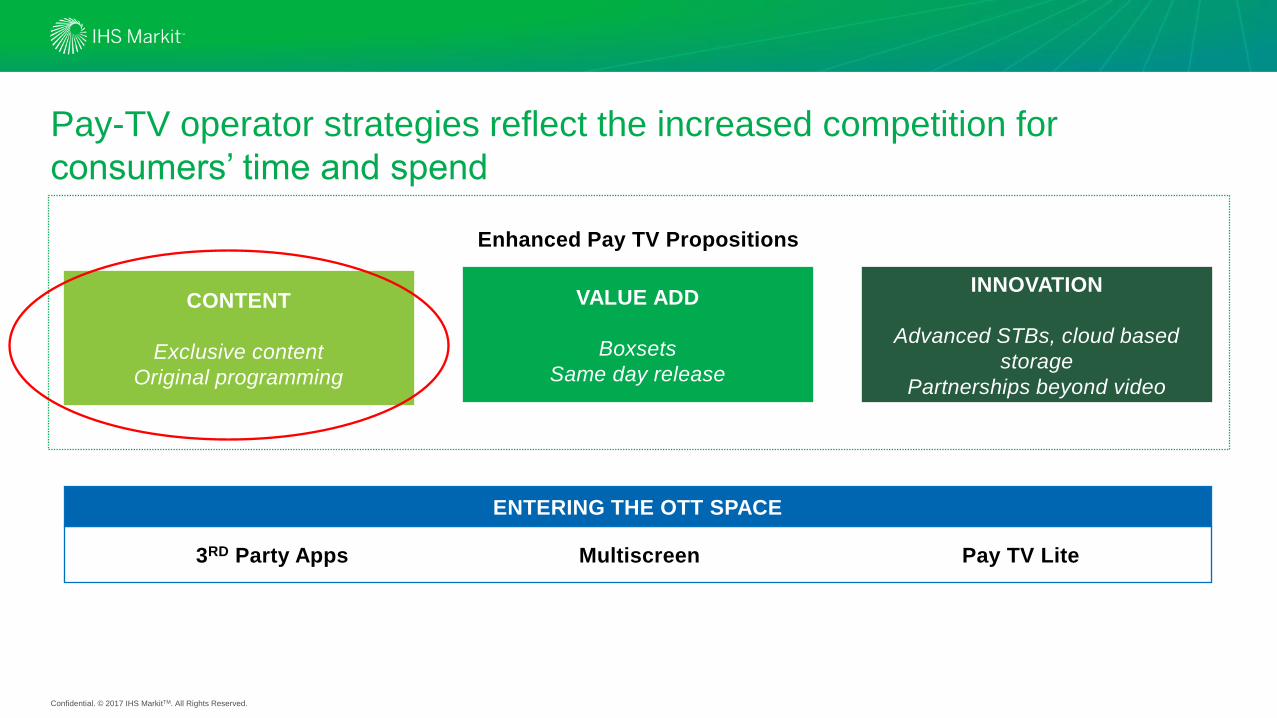

Pay-TV operator strategies reflect the increased competition for

consumers’ time and spend

VALUE ADD

Boxsets

Same day release

INNOVATION

Advanced STBs, cloud based

storage

Partnerships beyond video

ENTERING THE OTT SPACE

3RD Party Apps Multiscreen Pay TV Lite

CONTENT

Exclusive content

Original programming

Enhanced Pay TV Propositions

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

Production &

Distribution

Altice Studio

€40m production

budget for film

Orange Studio

€100m content

creation spend over 5

yrs

Telefonica Studio

€100m investment for

original production

All3 Media (50%),

Lionsgate (3.4%)

Sky Vision

€600m on originals

content creation

spend over 5 yrs

Pay TV operators, particularly telcos, are increasingly investing in original

content

19

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

How much is a series ($)?

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

0

1

2

3

4

5

6

7

8

9

10

Disney NBC Universal Viacom HBO Sky Discovery Netflix Amazon

Spend (

$bn)

Original and acquired programming spend for selected groups

2014 2015 2016 2017

6.7bn

Source: IHS Markit

New online entrants are offering consumers unique content that, in many cases,

complements pay TV

• Scale achieved is driving significant investment in original programming, perpetuating growth

7bn

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

But it is not only pay TV operators investing in content

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

Major online services are operating consumer facing services at

unprecedented global scale

0

50

100

150

200

250

300

Netflix Amazon iTunes BeIN Media Liberty Global DirecTV Sky Telefónica DeutscheTelekom

Vodafone Comcast

Number of countries & territories with consumer video services

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

Virgin Media (UK)

Com Hem (Sweden)

Waoo (Denmark)

Atlantic Broadband (US)

Grande (US)

RCN Corp (US)

Suddenlink (US)

GCI (US)

Midcontinent (US)

Cable ONE (US)

Proximus (Belgium)

Bouygues (France)

Orange (France)

Deutsche Telekom (Germany)

BT (UK)

Dish (US)

TalkTalk (UK)

Optus/Fetch TV (Australia)

Elisa (Finland)

Totalplay (Mexico)

Telecom Italia (Italy)

Vodafone (Spain)

KPN (Netherlands)

Vodafone (Portugal)

Bell (Canada)

SingTel (Singapore)

Vodafone (Ireland)

PCCW (Hong Kong)

StarHub (Singapore)

D’Live (South Korea)

Comcast (US)

Liberty Global (global)

Telia (Finland, Sweden)

Orange (Spain)

2013 2014 2015 2016 2017

Telenor (global)

Bharti Airtel (India)

Videocon (India)

Partner (Israel)

Altice (global)

Telekom Malaysia (Malaysia)

DNA (Finland)

Orange (global)

Cox (US)

Deutsche Telekom (global)

Verizon (US)

Attitudes to Netflix have softened – pay TV’s ‘frenemy’

Support subscriber acquisition by

enhancing content offering – including

4K content

Upsell customers to higher-tier bundles with higher-spec

CPE

Boost the appeal of high-speed

broadband required for streaming video

Boost customer satisfaction/loyalty and reduce churn

Strategic goals of online video partnerships for pay TV operators

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

Conclusions and

recommendations:

• Cable companies should continue to invest in infrastructure to

make sure that they provide fast and reliable connections

• Make ‘frenemies’ of new online channels that add value to your

customers’ subscriptions

• But also consider going beyond partnerships – be on the look out

for strategic investment opportunities

• Seek opportunities to execute a pay TV strategy of your own –

don’t lose touch with the mobile-first generation

• Focus on the core, high-ARPU bundled proposition by delivering

on the promise of anytime-anywhere TV and video

• Invest in new video technologies and standards; metadata, voice,

personalization, smart home.

![VIANA MAPS DRIVEN BY BENEDICKS-CARLESON MAPS · 2018-01-08 · More recently, in [Sol13], Solano proved that for a two-dimensional partially hyper-bolic skew-product map driven by](https://static.fdocuments.us/doc/165x107/5fa802e385838611273462b9/viana-maps-driven-by-benedicks-carleson-maps-2018-01-08-more-recently-in-sol13.jpg)