FRAUD complaint against Nithyananda by Ex-donor Popatlal Savla - Extracts

19/08/17

1

CA Deepali Mehta

Shah & Savla LLP Chartered Accountants

Returns – GSTR-1, GSTR-2, GSTR-3 & GSTR-3B

Tran-1 & Tran-2 - Intensive Study Circle - GSTPAM

Matters to be covered

Returns;

GSTR-3B

GSTR-1

GSTR-2

GSTR-3

Matching Concept

2

19/08/17

2

Returns under GST

3

Every registered person is required to file

(i) Details of Outward Supply;

(ii) Details of Inward Supply; and

(iii) Return

for the prescribed tax period.

UN agencies have to file return for the month during which they make purchases.

They would not be required to file regular return.

Common return is prescribed for CGST, SGST, IGST and UGST.

CA Deepali Mehta

Returns

4

19/08/17

3

CA Deepali Mehta

5

Sales Register including debit notes & Credit notes

Purchase register, Expense Register, Fixed Asset register – sale or Purchase

Details of Non GST Supply. NIL rated & Exempt Supply

Check List for

Return filing

Inward /outward supply of

petrol, diesel, Liquor for

human consumption, sale of

Flat, Land, Securities. Details

of outward supply on which

RCM is paid by recipient

Calculation of IGST, CGST

& SGST Output tax

Calculation of ITC, Reversal

of ITC, Ineligible ITC ,

adjustment of IGST, CGST

& SGST Credit against

output liability

19/08/17

4

GSTR-3B return must be filed by all persons having GST registration for the month

of July 2017 and August 2017 on the 20th of August and 20th September 2017

respectively. Today we look at GSTR-3B return filing in detail along procedure for

filing online

Normal schedule of filing GSTR-3 will start for the month of September in October.

GSTR-3 also needs to be filed for the month of July & August in the month of

September.

CA Deepali Mehta

GSTR - 3B

7

The Government has mentioned that during the GST transition period, leniency would be shown to

taxpayers to familiarize themselves with the GST provisions. Hence, no penalty has so far been

announced for not filing GSTR-3B return. However, it is expected that taxpayers who fail to file

GSTR-3B returns would be ineligible to being filing GSTR-1, GSTR-2 and GSTR-3 returns from the

month of October. Failure to file GSRT-1, GSTR-2 and GSTR-3 returns will attract penalty of Rs.100

per day.

GSTR-3B is a simplified GST return, in which outward supplies and inward supplies are not matched.

Hence, the taxpayer while filing GSTR-3B return is required to furnish details of both outward supplies

and inward supplies.

CA Deepali Mehta

GSTR - 3B

8

19/08/17

5

It is Mandatory to file GSTR-3B. File NIL return if no sale & purchase. Therefore all dealers who are

required to file monthly returns under the GST Regime are required to file GSTR-3B. Composition

dealers are required to file quarterly returns therefore dealers who have opted for composition scheme

are not required to file GSTR-3B.

GSTR-3B is not the final return for the month of July’2017 this is only a provisional return. GSTR-1,

GSTR-2, GSTR-3 for July’2017 are still required to be filed.

GSTR-3B cannot be revised. Any revision in the figures for July’2017 has to be done through GSTR-

1, 2 and 3 to be filed later on. Any taxes due for July’2017 have to be paid before filing GSTR-3B

If there is any change in the figures at the time of filing forms GSTR-1,2 & 3 and if there is excess

tax payable then the same will have to be paid with interest before filing GSTR-3 due in

September. CA Deepali Mehta

Imp Points for GSTR - 3B

9

If your input credits are more than your output in GSTR-3B then you need not pay any taxes before

filing this return. However, it is to be noted that no refund can be claimed in form GSTR-3B and excess

credit will be credited to the ITC Ledger.

A very important point to remember about filing GSTR-3B is that the transitional credits available from

the previous VAT/Service Tax/Excise regimes will not be available for credit and use in GSTR-3B. Any

such credits have to be shown by filing form TRAN-1 and will be available for use only after filing

TRAN-1

GSTR-3B is to be filed from the period from which the registration is taken by the supplier. Therefore,

if you have taken registration in the month of August’2017 the option for filing GSTR-3B for July’2017

will not be available and the no GSTR-3B is to be filed for July’2017.

CA Deepali Mehta

Imp Points for GSTR - 3B

10

19/08/17

6

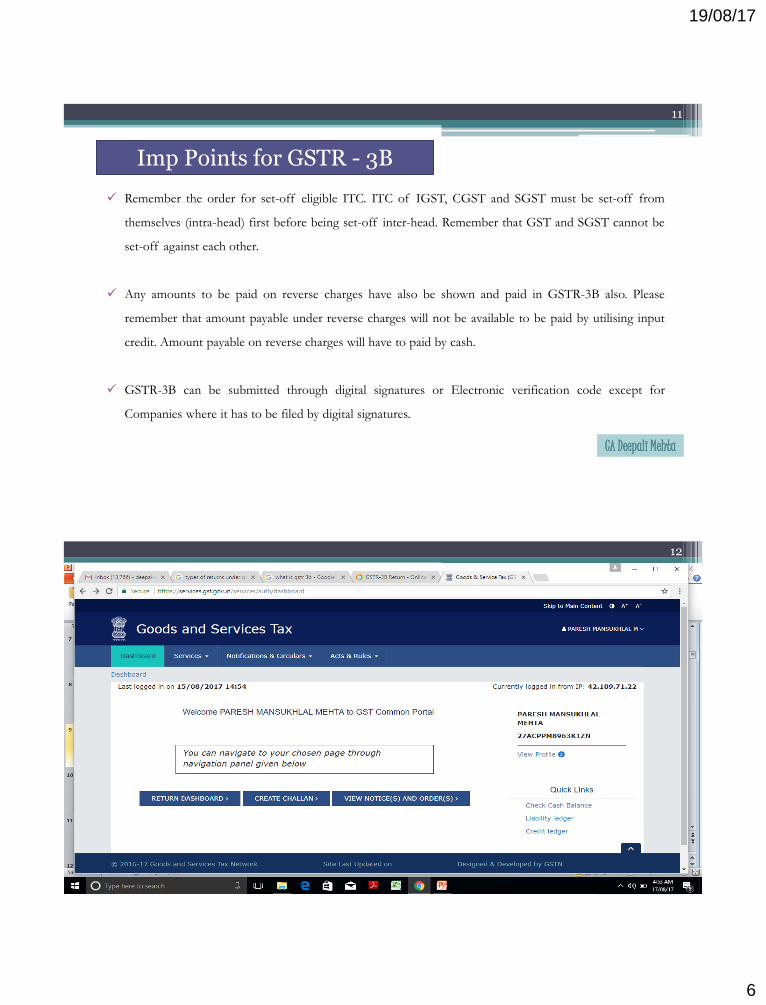

Remember the order for set-off eligible ITC. ITC of IGST, CGST and SGST must be set-off from

themselves (intra-head) first before being set-off inter-head. Remember that GST and SGST cannot be

set-off against each other.

Any amounts to be paid on reverse charges have also be shown and paid in GSTR-3B also. Please

remember that amount payable under reverse charges will not be available to be paid by utilising input

credit. Amount payable on reverse charges will have to paid by cash.

GSTR-3B can be submitted through digital signatures or Electronic verification code except for

Companies where it has to be filed by digital signatures.

CA Deepali Mehta

Imp Points for GSTR - 3B

11

CA Deepali Mehta

12

19/08/17

7

GSTR-3B 13th August, 2017 CA. Gopal Kedia

13

GSTR-3B 13th August, 2017 CA. Gopal Kedia

14

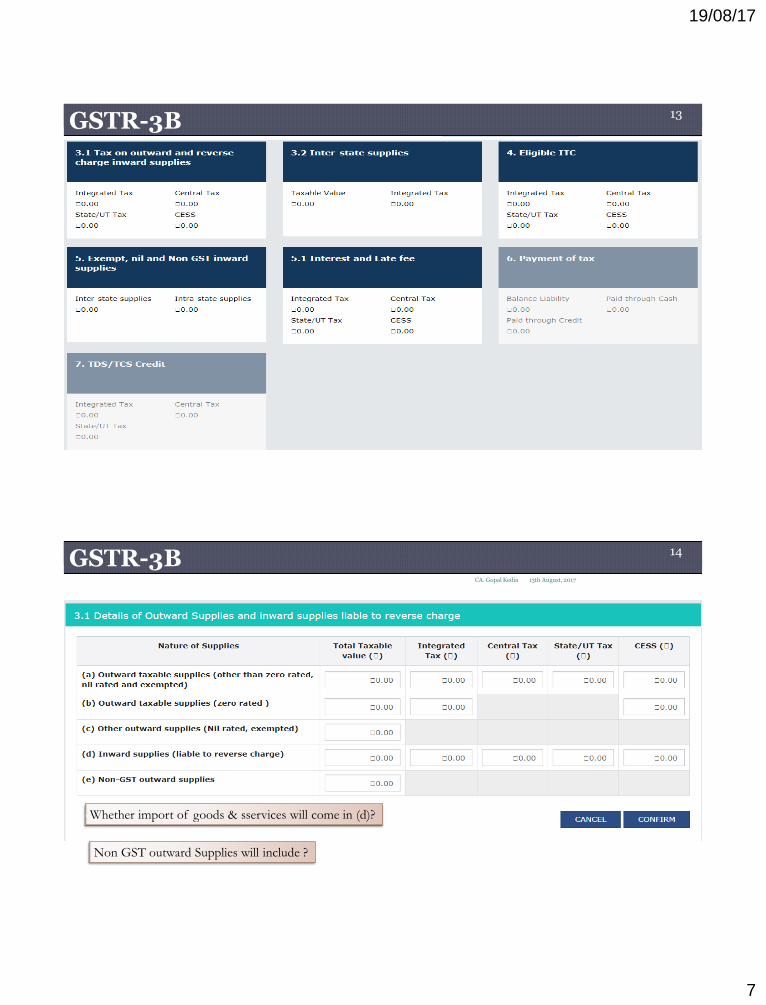

Whether import of goods & sservices will come in (d)?

Non GST outward Supplies will include ?

19/08/17

8

GSTR-3B 13th August, 2017 CA. Gopal Kedia

15

GSTR-3B 13th August, 2017 CA. Gopal Kedia

16

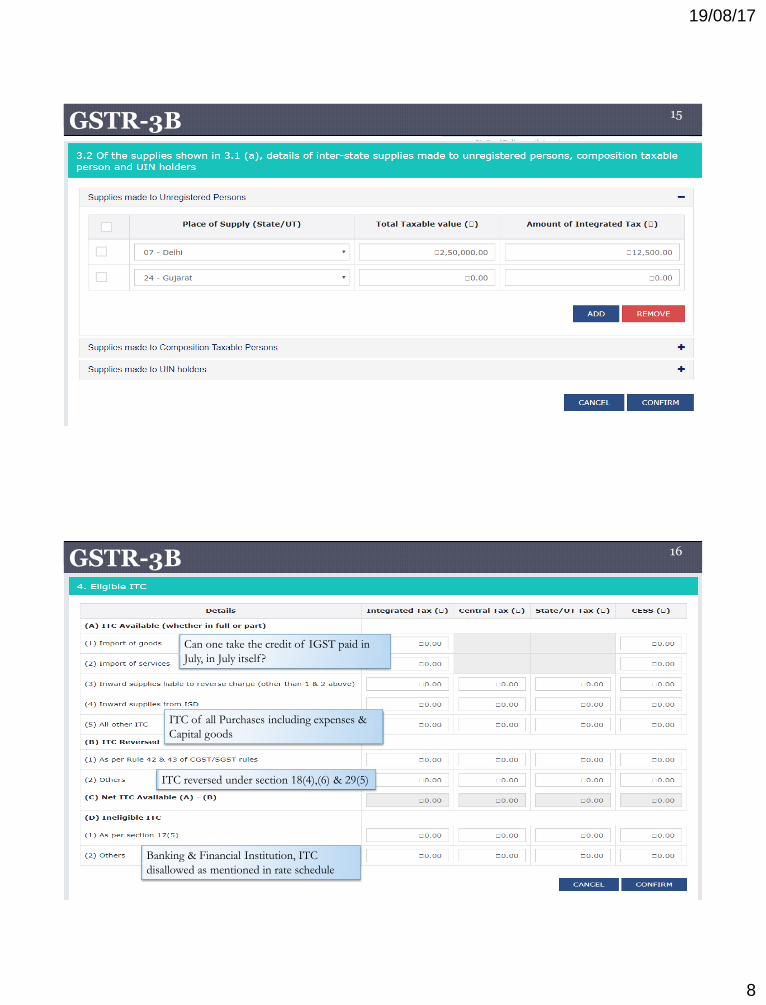

Can one take the credit of IGST paid in

July, in July itself?

ITC of all Purchases including expenses &

Capital goods

ITC reversed under section 18(4),(6) & 29(5)

Banking & Financial Institution, ITC

disallowed as mentioned in rate schedule

19/08/17

9

GSTR-3B 13th August, 2017 CA. Gopal Kedia

17

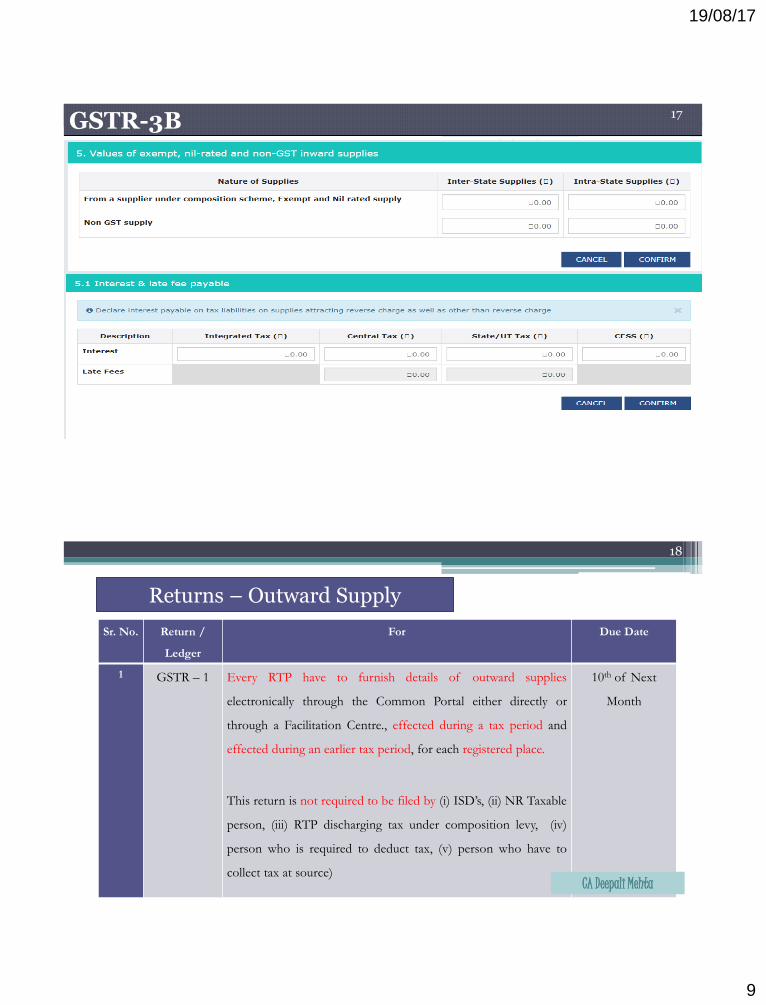

Returns – Outward Supply

18

Sr. No. Return /

Ledger

For Due Date

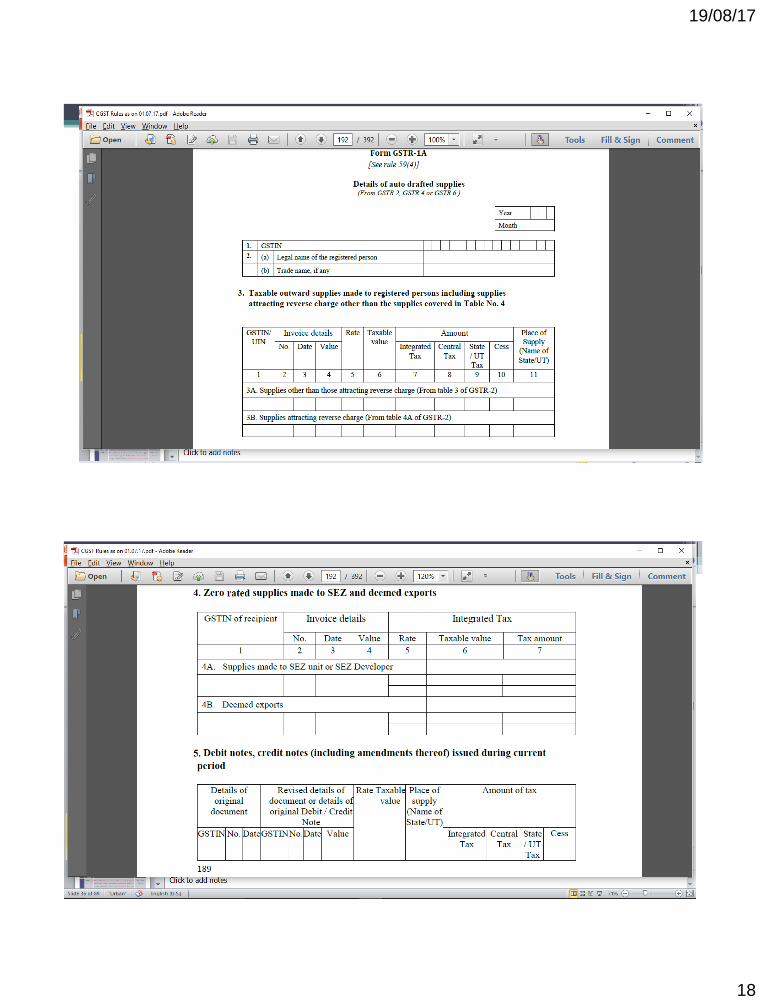

1 GSTR – 1 Every RTP have to furnish details of outward supplies

electronically through the Common Portal either directly or

through a Facilitation Centre., effected during a tax period and

effected during an earlier tax period, for each registered place.

This return is not required to be filed by (i) ISD’s, (ii) NR Taxable

person, (iii) RTP discharging tax under composition levy, (iv)

person who is required to deduct tax, (v) person who have to

collect tax at source)

10th of Next

Month

CA Deepali Mehta

19/08/17

10

19

CA Deepali Mehta

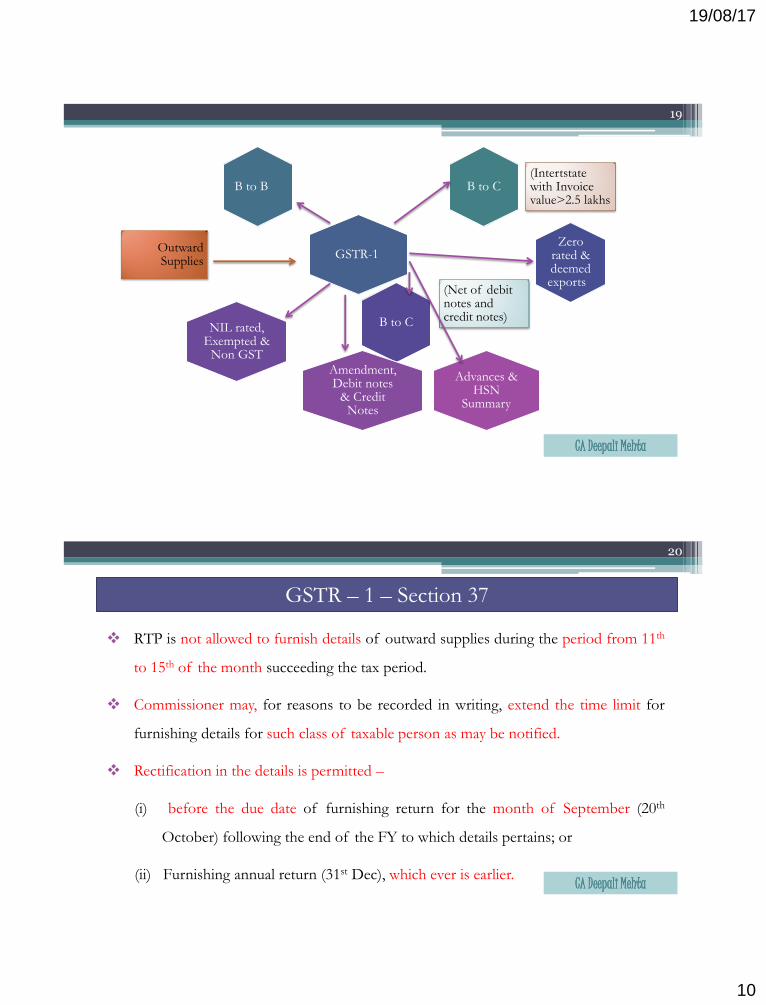

B to C (Intertstate with Invoice value>2.5 lakhs

B to B

GSTR-1 Outward Supplies

Zero rated & deemed exports

B to C

(Net of debit notes and credit notes)

NIL rated, Exempted &

Non GST

Amendment, Debit notes

& Credit Notes

Advances & HSN

Summary

RTP is not allowed to furnish details of outward supplies during the period from 11th

to 15th of the month succeeding the tax period.

Commissioner may, for reasons to be recorded in writing, extend the time limit for

furnishing details for such class of taxable person as may be notified.

Rectification in the details is permitted –

(i) before the due date of furnishing return for the month of September (20th

October) following the end of the FY to which details pertains; or

(ii) Furnishing annual return (31st Dec), which ever is earlier.

GSTR – 1 – Section 37

20

CA Deepali Mehta

19/08/17

11

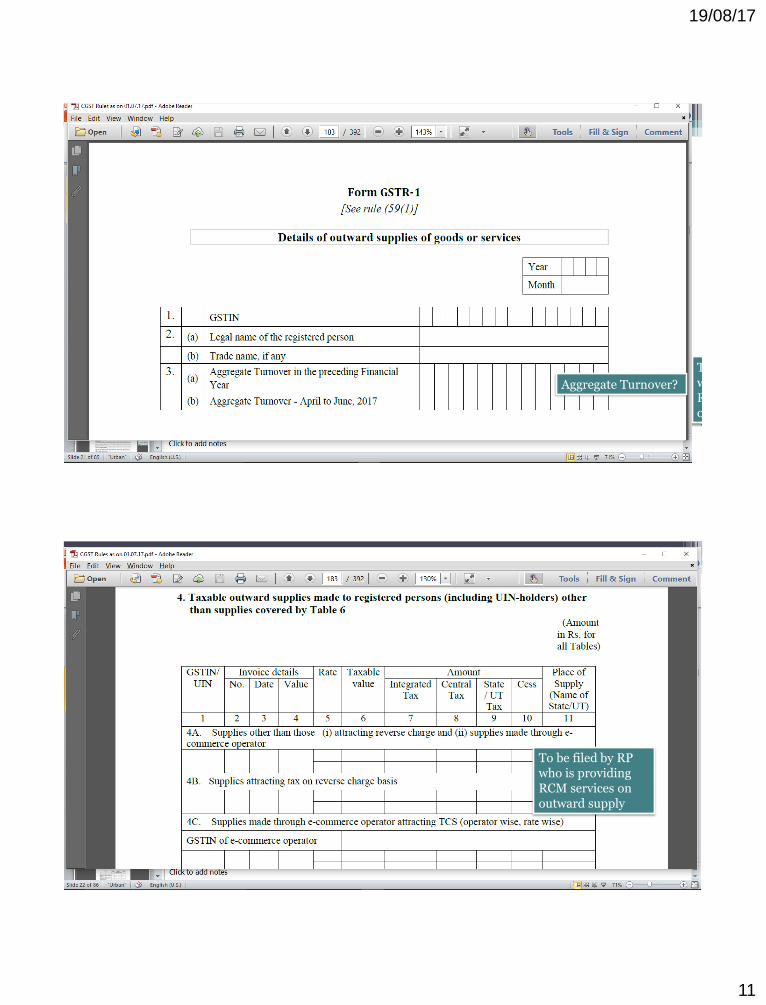

CA Deepali Mehta GSTR – 1

21

To be filed by RP who is providing RCM services on outward supply

Aggregate Turnover?

CA Deepali Mehta GSTR – 1

22

To be filed by RP who is providing RCM services on outward supply

19/08/17

12

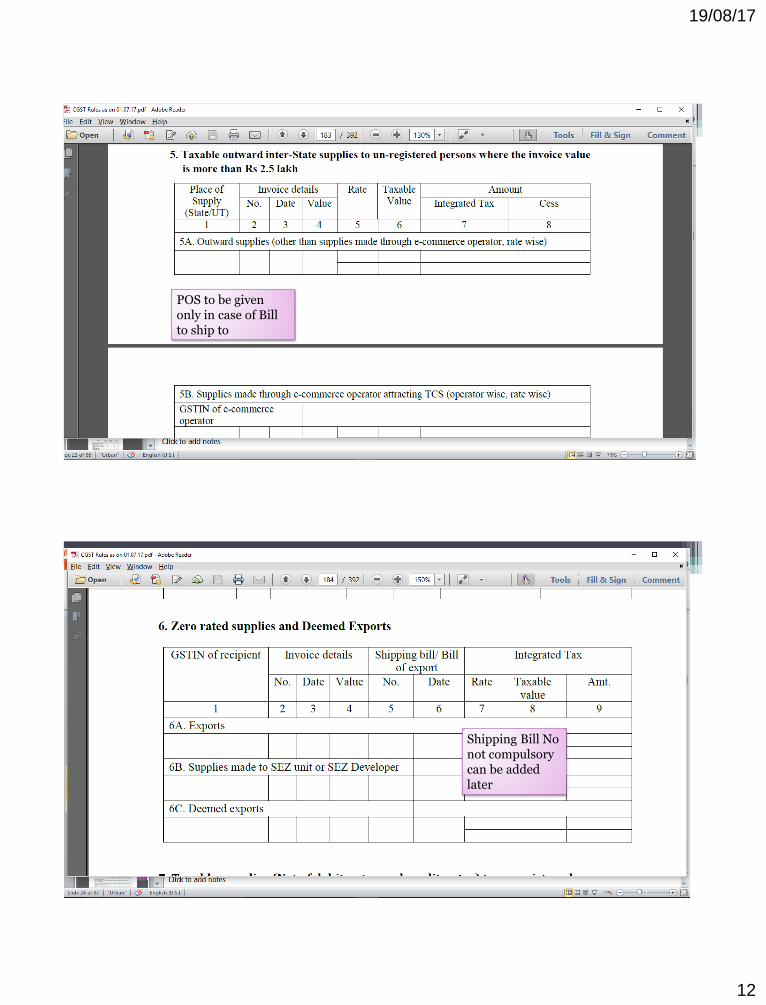

CA Deepali Mehta GSTR - 1

23

POS to be given only in case of Bill to ship to

CA Deepali Mehta GSTR - 1

24

Shipping Bill No not compulsory can be added later

19/08/17

13

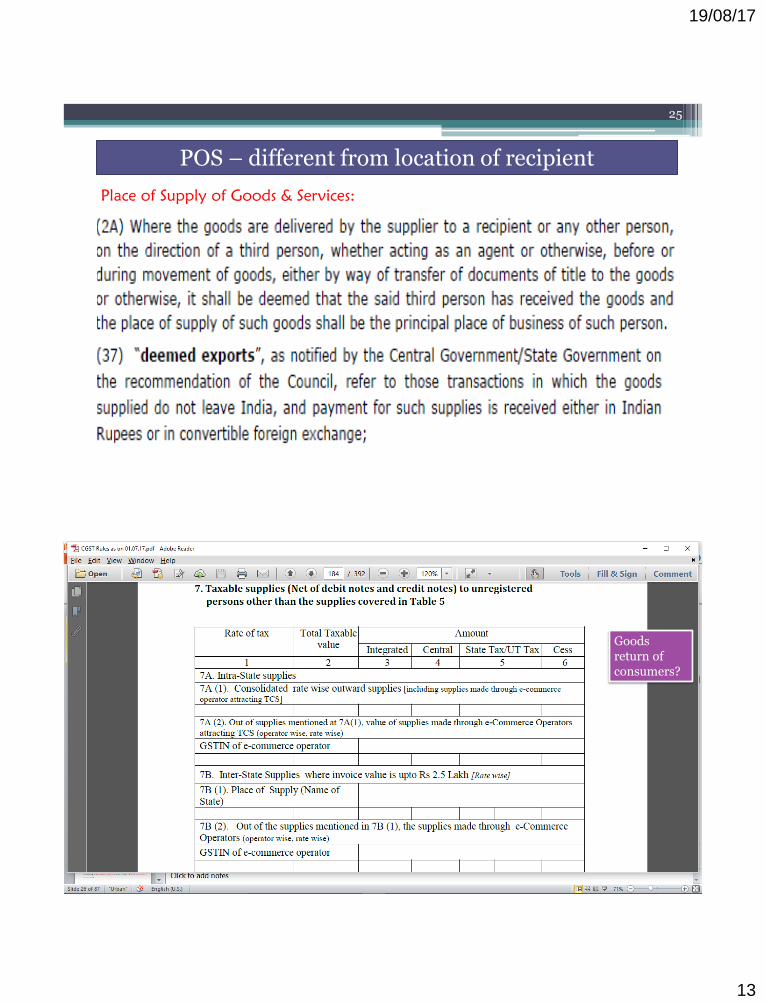

Place of Supply of Goods & Services:

POS – different from location of recipient

25

CA Deepali Mehta GSTR – 1 Cont…..

26

Goods return of consumers?

19/08/17

14

CA Deepali Mehta GSTR – 1 Cont…..

27

CA Deepali Mehta GSTR – 1 Cont…..

28

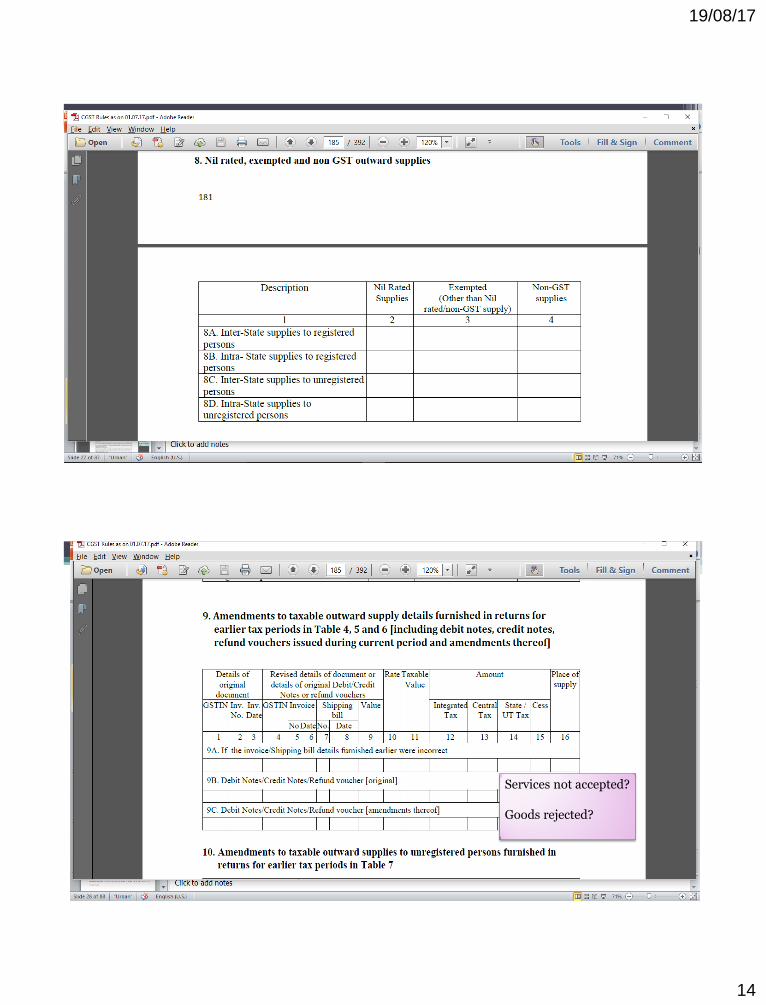

Services not accepted? Goods rejected?

19/08/17

15

CA Deepali Mehta GSTR – 1 Cont…..

29

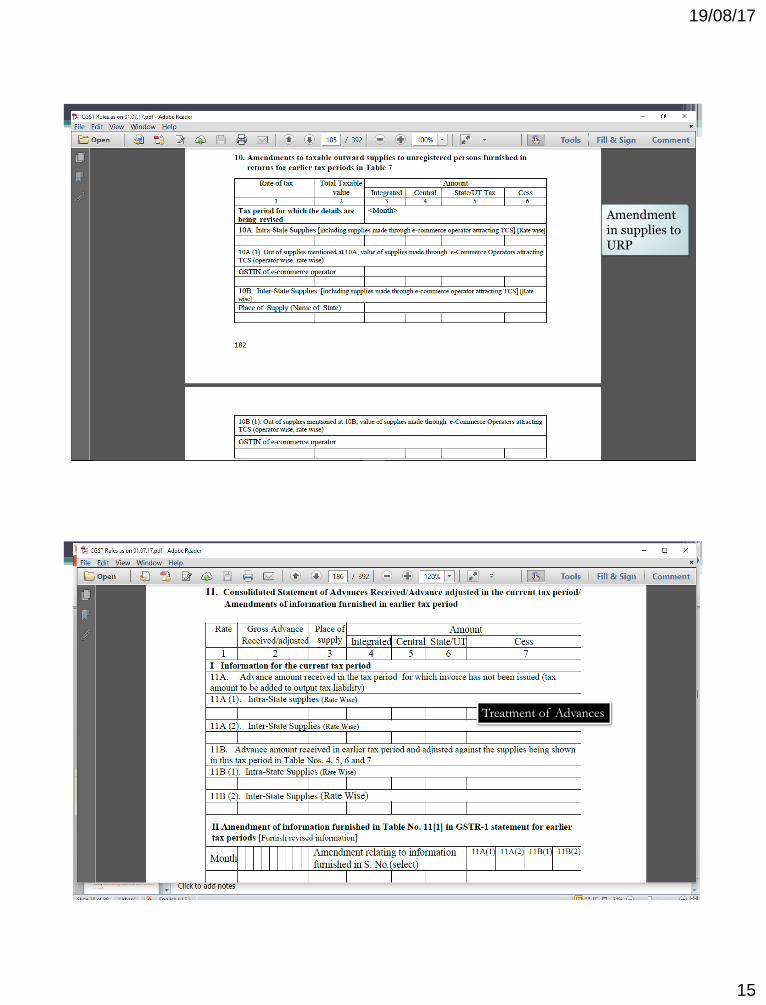

Amendment in supplies to URP

CA Deepali Mehta

Deemed Export

30

Treatment of Advances

19/08/17

16

CA Deepali Mehta

Deemed Export

31

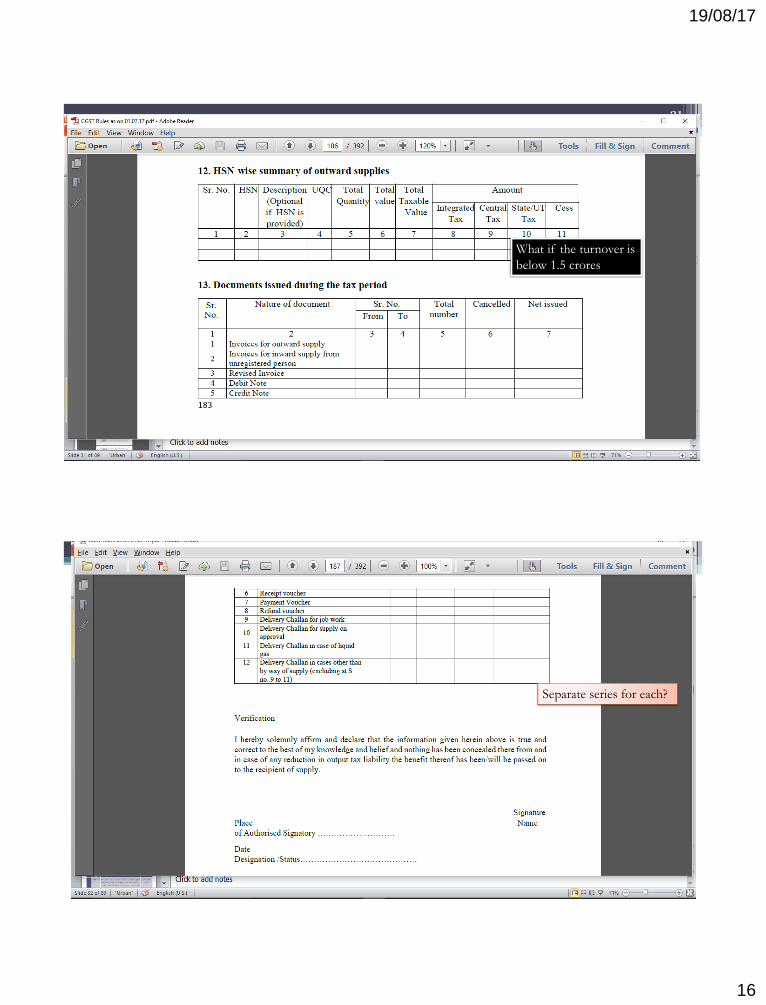

What if the turnover is

below 1.5 crores

CA Deepali Mehta GSTR – 1 Cont…..

32

Separate series for each?

19/08/17

17

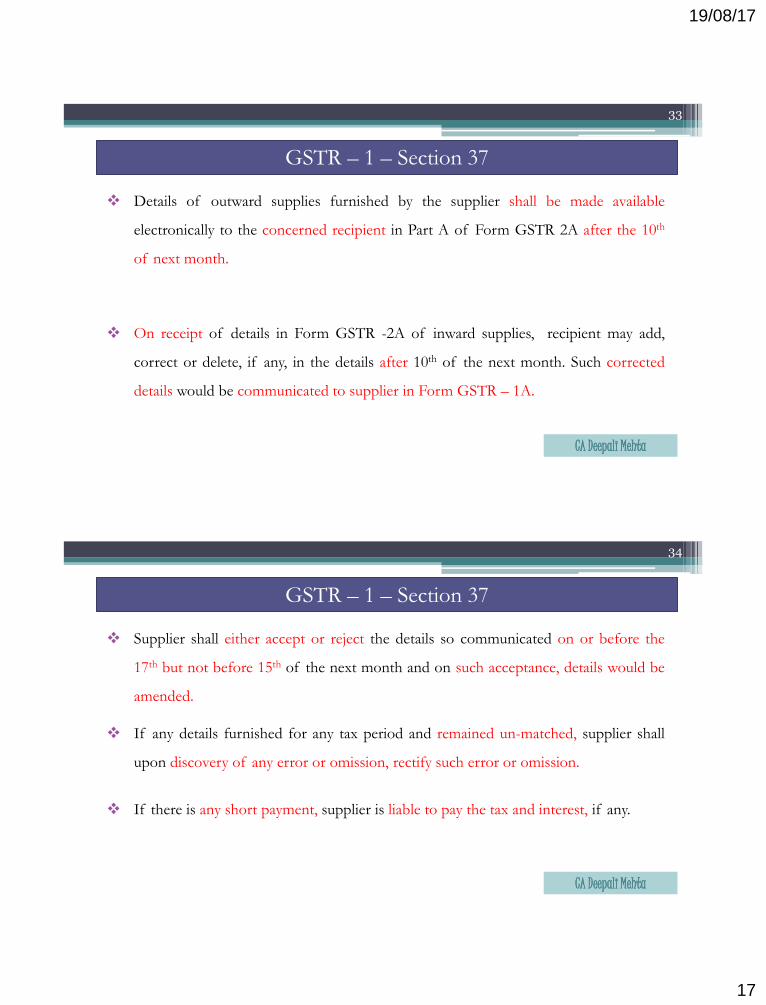

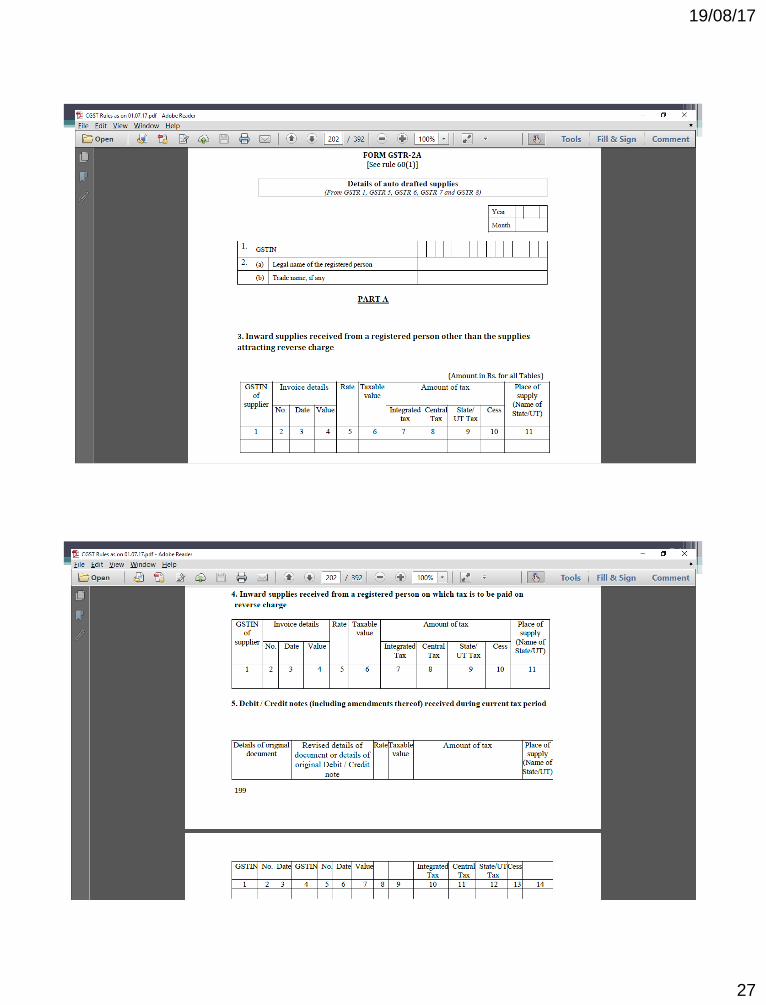

Details of outward supplies furnished by the supplier shall be made available

electronically to the concerned recipient in Part A of Form GSTR 2A after the 10th

of next month.

On receipt of details in Form GSTR -2A of inward supplies, recipient may add,

correct or delete, if any, in the details after 10th of the next month. Such corrected

details would be communicated to supplier in Form GSTR – 1A.

GSTR – 1 – Section 37

33

CA Deepali Mehta

Supplier shall either accept or reject the details so communicated on or before the

17th but not before 15th of the next month and on such acceptance, details would be

amended.

If any details furnished for any tax period and remained un-matched, supplier shall

upon discovery of any error or omission, rectify such error or omission.

If there is any short payment, supplier is liable to pay the tax and interest, if any.

GSTR – 1 – Section 37

34

CA Deepali Mehta

19/08/17

18

Instructions:

CA Deepali Mehta GSTR – 1 Cont…..

35

CA Deepali Mehta GSTR – 1 Cont…..

36

19/08/17

19

CA Deepali Mehta GSTR – 1 Cont…..

37

`

Returns

38

Sr. No. Return /

Ledger

For Due Date

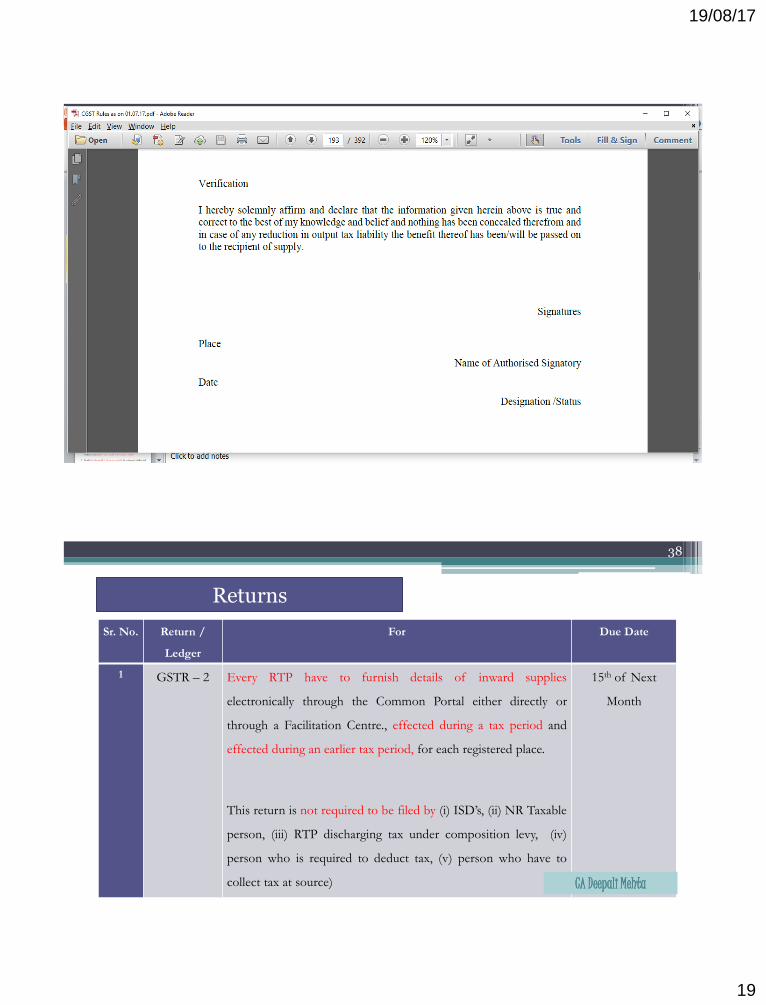

1 GSTR – 2 Every RTP have to furnish details of inward supplies

electronically through the Common Portal either directly or

through a Facilitation Centre., effected during a tax period and

effected during an earlier tax period, for each registered place.

This return is not required to be filed by (i) ISD’s, (ii) NR Taxable

person, (iii) RTP discharging tax under composition levy, (iv)

person who is required to deduct tax, (v) person who have to

collect tax at source)

15th of Next

Month

CA Deepali Mehta

19/08/17

20

Details shall include inter-alia –

i. Inward supplies of taxable goods or services or both;

ii. Inward supplies of goods or services or both, on which tax is discharged under

Reverse Charge Mechanism;

iii. Inward supplies of goods or services or both, taxable under IGST Act or on which

tax is payable under section 3 of Customs Act, 1975;

iv. Debit or Credit notes received in respect of such supply.

GSTR – 2 – Section 38

39

CA Deepali Mehta

Details shall include inter-alia –

v. Debit or Credit notes received in respect of such supplies during a tax period after

the 10th but on or before 15th of the succeeding tax period;

vi. Recipient of goods or services or both shall specify the inward supplies which is not

eligible for ITC if it is determined at invoice level. Moreover, he has to also

determine quantum of ineligible ITC which is relatable to a non-taxable supplies or

for purposes other than business and can not determined at the invoice level.

GSTR – 2 – Section 38

40

CA Deepali Mehta

19/08/17

21

Commissioner may, for reasons to be recorded in writing, extend the time limit for

furnishing details for such class of taxable person as may be notified.

Details of supplies modified, deleted or included by the recipient and furnished shall

be communicated to the supplier concerned in Form GSTR 1A.

GSTR – 2 – Section 38

41

CA Deepali Mehta

If any details furnished for any tax period and remained un-matched, supplier shall

upon discovery of any error or omission, rectify such error or omission.

If there is any short payment, supplier is liable to pay the tax and interest, if any.

Rectification in the details is permitted –

(i) before the due date of furnishing return for the month of September (20th

October) following the end of the FY to which details pertains; or

(ii) Furnishing annual return (31st Dec), which ever is earlier.

GSTR – 2 – Section 38

42

CA Deepali Mehta

19/08/17

22

CA Deepali Mehta GSTR – 2

43

GSTR-2

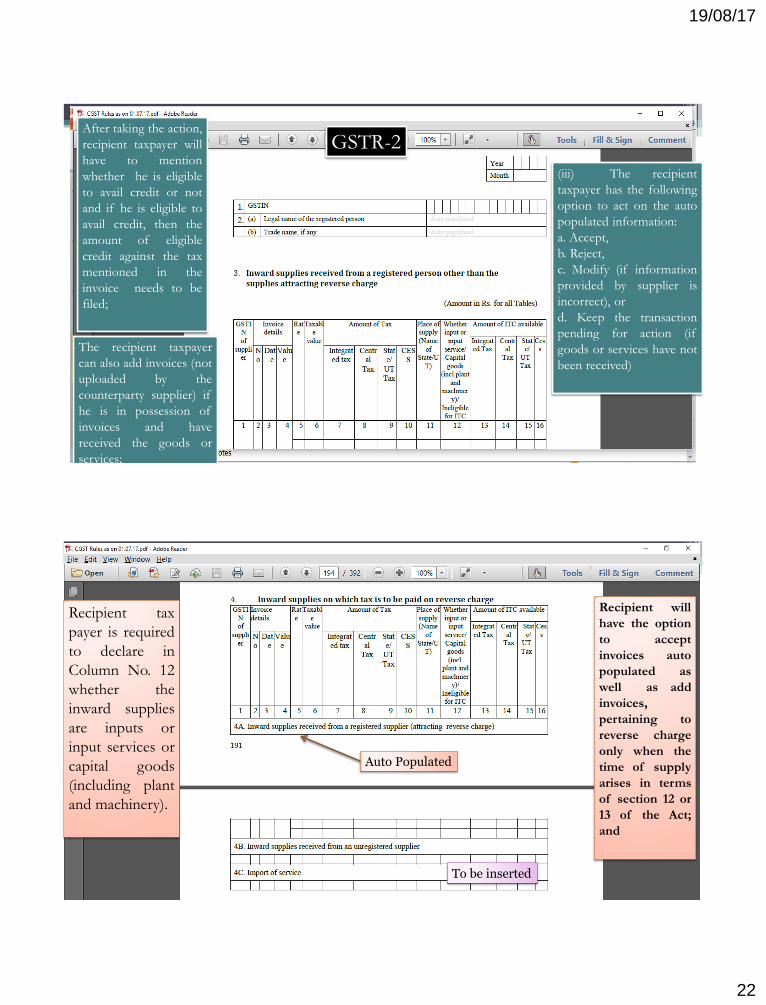

(iii) The recipient

taxpayer has the following

option to act on the auto

populated information:

a. Accept,

b. Reject,

c. Modify (if information

provided by supplier is

incorrect), or

d. Keep the transaction

pending for action (if

goods or services have not

been received)

After taking the action,

recipient taxpayer will

have to mention

whether he is eligible

to avail credit or not

and if he is eligible to

avail credit, then the

amount of eligible

credit against the tax

mentioned in the

invoice needs to be

filed;

The recipient taxpayer

can also add invoices (not

uploaded by the

counterparty supplier) if

he is in possession of

invoices and have

received the goods or

services;

CA Deepali Mehta GSTR – 2

44

Auto Populated

To be inserted

Recipient will

have the option

to accept

invoices auto

populated as

well as add

invoices,

pertaining to

reverse charge

only when the

time of supply

arises in terms

of section 12 or

13 of the Act;

and

Recipient tax

payer is required

to declare in

Column No. 12

whether the

inward supplies

are inputs or

input services or

capital goods

(including plant

and machinery).

19/08/17

23

CA Deepali Mehta GSTR – 2

45

Taxable Value in

Table 5 means

assessable value

for customs

purposes on which

IGST is computed

(IGST is levied on

value plus

specified customs

duties). In case of

imports, the

GSTIN would be

of recipient tax

payer.

GOODS

Recipient to

provide for Bill

of Entry

information

including six

digits port code

and seven digits

bill of entry

number To be inserted

CA Deepali Mehta GSTR – 2

46

6D Amendment of Debit & Credit Notes of earlier tax periods

To be inserted

19/08/17

24

CA Deepali Mehta GSTR – 2

47

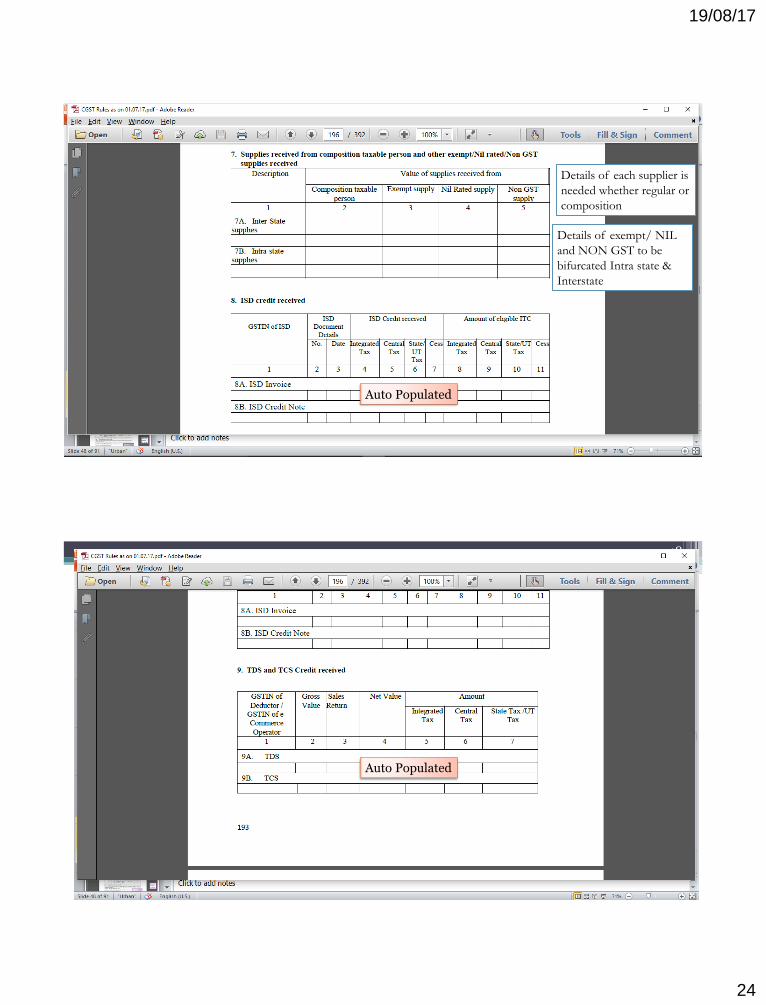

Details of each supplier is

needed whether regular or

composition

Details of exempt/ NIL

and NON GST to be

bifurcated Intra state &

Interstate

Auto Populated

CA Deepali Mehta GSTR – 2

48

Details of each supplier is

needed whether regular or

composition

Details of exempt/ NIL

and NON GST to be

bifurcated Intra state &

Interstate

Auto Populated

Auto Populated

19/08/17

25

CA Deepali Mehta GSTR – 2

49

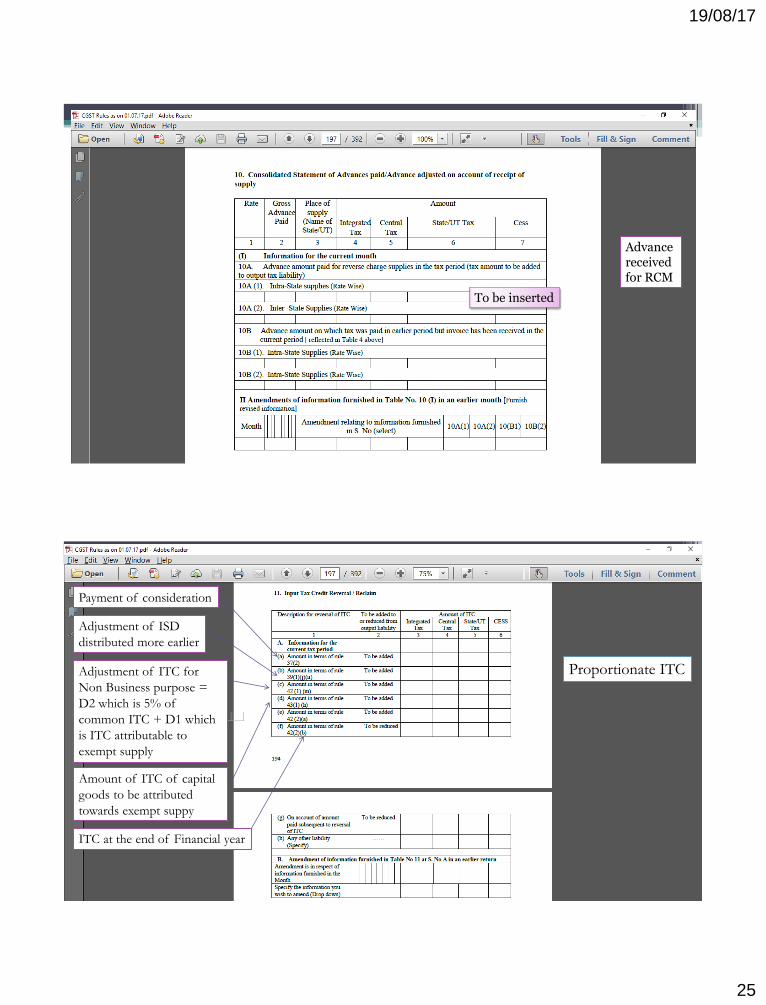

Advance received for RCM

To be inserted

CA Deepali Mehta GSTR – 2

50

Proportionate ITC

Payment of consideration

Adjustment of ISD

distributed more earlier

Adjustment of ITC for

Non Business purpose =

D2 which is 5% of

common ITC + D1 which

is ITC attributable to

exempt supply

Amount of ITC of capital

goods to be attributed

towards exempt suppy

ITC at the end of Financial year

19/08/17

26

CA Deepali Mehta GSTR – 2

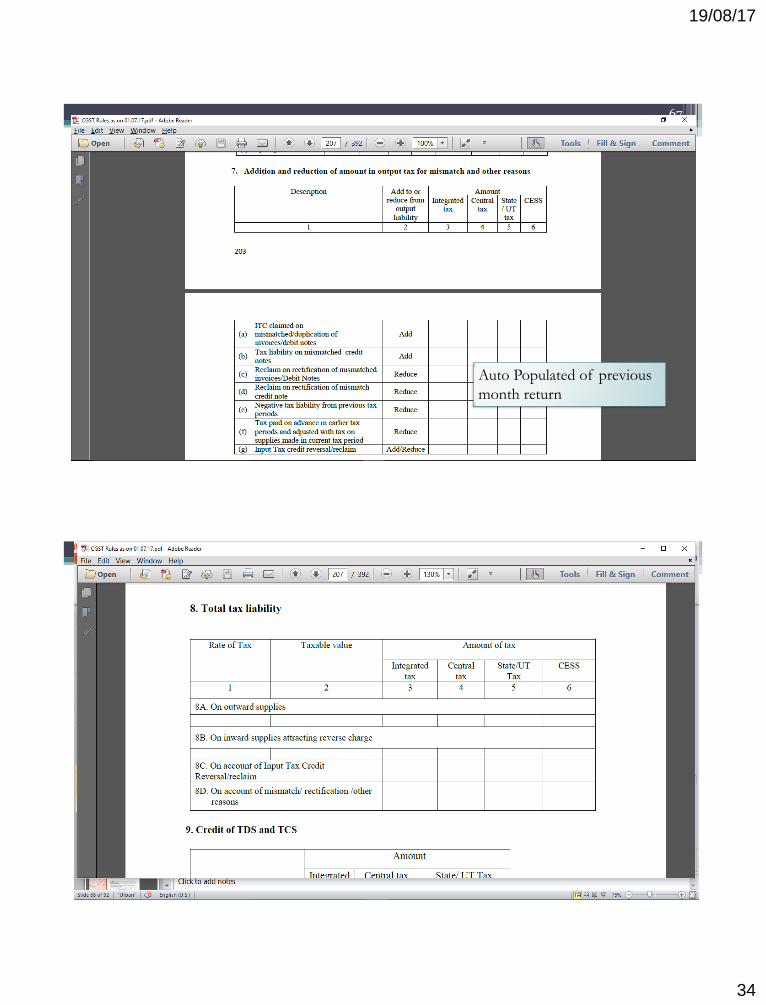

51

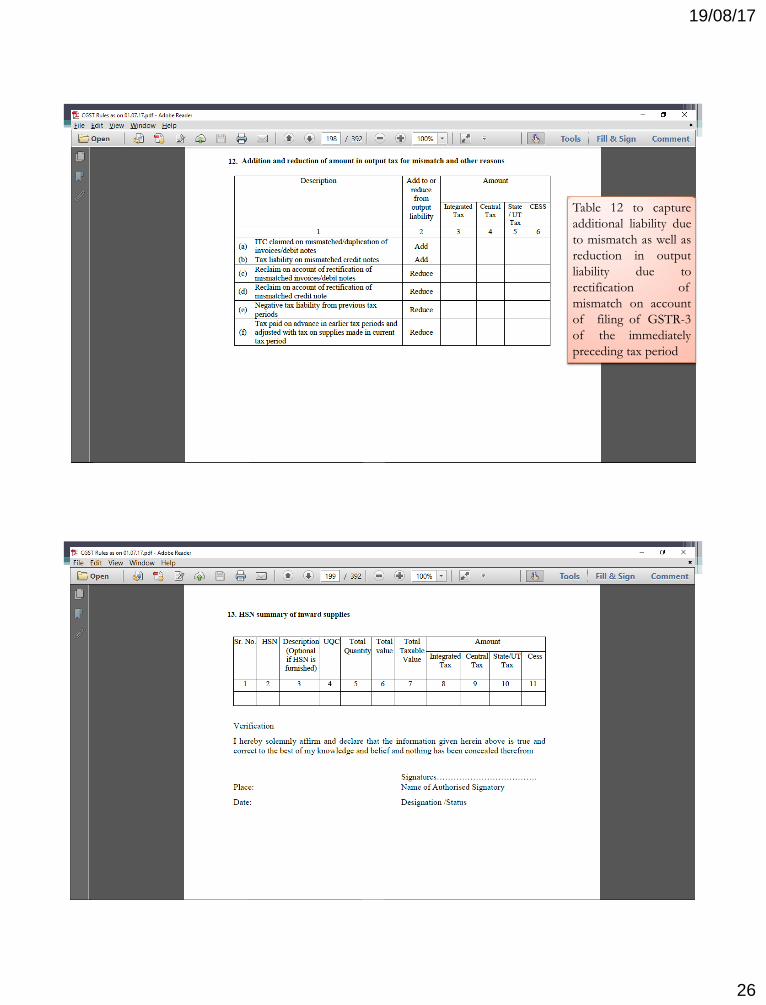

Table 12 to capture

additional liability due

to mismatch as well as

reduction in output

liability due to

rectification of

mismatch on account

of filing of GSTR-3

of the immediately

preceding tax period

CA Deepali Mehta GSTR – 2

52

19/08/17

27

CA Deepali Mehta GSTR – 2

53

CA Deepali Mehta GSTR – 2

54

19/08/17

28

CA Deepali Mehta GSTR – 2

55

Returns

56

Sr. No. Return /

Ledger

For Due Date

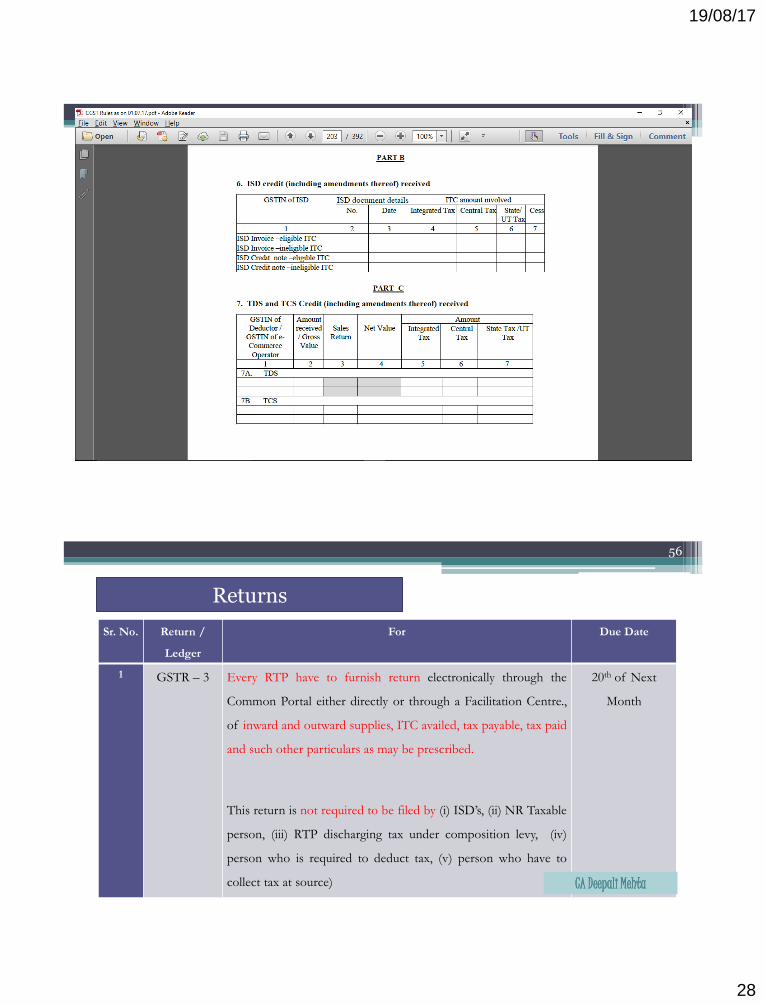

1 GSTR – 3 Every RTP have to furnish return electronically through the

Common Portal either directly or through a Facilitation Centre.,

of inward and outward supplies, ITC availed, tax payable, tax paid

and such other particulars as may be prescribed.

This return is not required to be filed by (i) ISD’s, (ii) NR Taxable

person, (iii) RTP discharging tax under composition levy, (iv)

person who is required to deduct tax, (v) person who have to

collect tax at source)

20th of Next

Month

CA Deepali Mehta

19/08/17

29

Part A of the return shall be electronically generated on the bases of information

furnished through GSTR-1, GSTR-2, and other liabilities of preceding tax periods;

Taxable person have to discharge his tax liability, interest, penalty, fees by debiting

ECL as per the details contained in Part B of return.

Commissioner may, for reasons to be recorded in writing, extend the time limit for

furnishing details for such class of taxable person as may be notified.

GSTR – 3 – Section 39

57

CA Deepali Mehta

RTP has to furnish return for every tax period whether or not any supplies of goods

or services or both have been made during such tax period.

If there exists or discover any omission or incorrect particulars in return, RTP shall

rectify such omission or incorrect particulars in the return to be furnished for the

month or quarter during which such omission or incorrect particulars are noticed.

However, RTP is liable to pay interest, if there is any short payment of tax.

GSTR – 3 – Section 39

58

CA Deepali Mehta

19/08/17

30

Discovery of any omission or incorrect particulars should not be as a result of

scrutiny, audit, inspection or enforcement activity by the tax authorities.

Rectification in the returns is permitted –

(i) before the due date of furnishing return for the month of September (20th

October) or 2nd Quarter following the end of the FY to which return pertains; or

(ii) actual date of furnishing relevant annual return (31st Dec), which ever is earlier.

GSTR – 3 – Section 39

59

CA Deepali Mehta

RTP shall not be allowed to furnish a return for a tax period if the return for any of

the previous tax periods has not been furnished by him.

GSTR – 3 – Section 39

60

CA Deepali Mehta

19/08/17

31

CA Deepali Mehta GSTR – 2

61

CA Deepali Mehta GSTR – 2

62

Table 4.1 will

not include

zero rated

supplies made

without

payment of

taxes.

19/08/17

32

CA Deepali Mehta GSTR – 2

63

B to B, B to C all totaled up

CA Deepali Mehta GSTR – 2

64

Table 4.3 will not

include amendments

of supplies originally

made under reverse

charge basis.

19/08/17

33

CA Deepali Mehta GSTR – 2

65

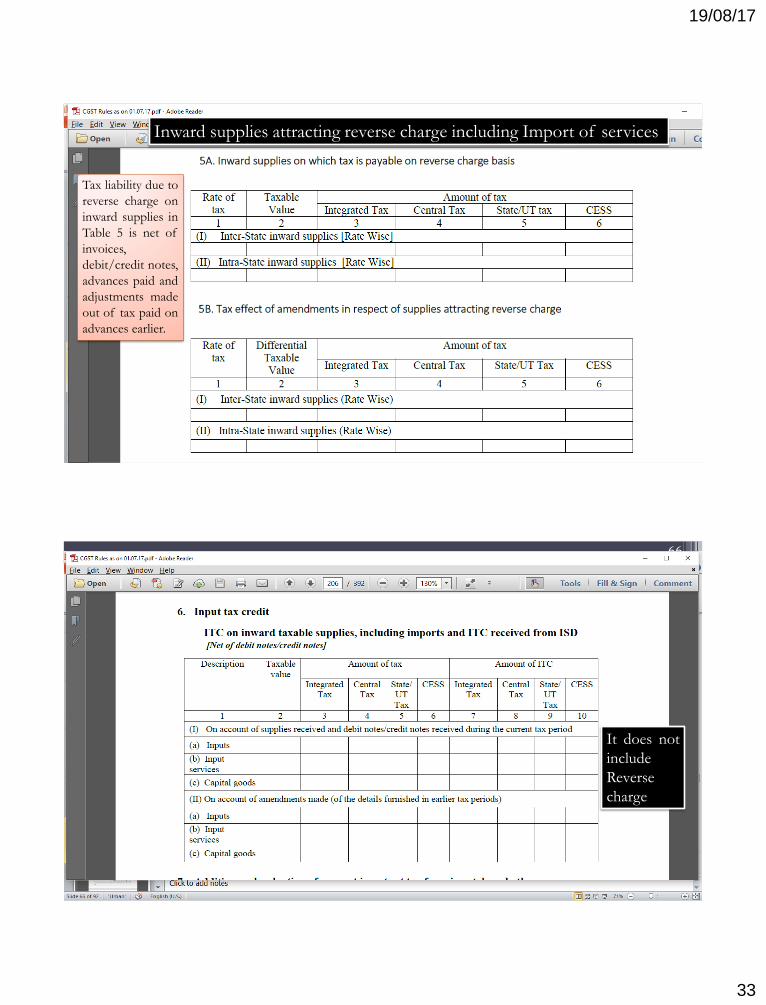

Inward supplies attracting reverse charge including Import of services

Tax liability due to

reverse charge on

inward supplies in

Table 5 is net of

invoices,

debit/credit notes,

advances paid and

adjustments made

out of tax paid on

advances earlier.

CA Deepali Mehta GSTR – 2

66

It does not

include

Reverse

charge

19/08/17

34

CA Deepali Mehta GSTR – 2

67

Auto Populated of previous

month return

CA Deepali Mehta GSTR – 2

68

19/08/17

35

CA Deepali Mehta GSTR – 2

69

CA Deepali Mehta GSTR – 2

70

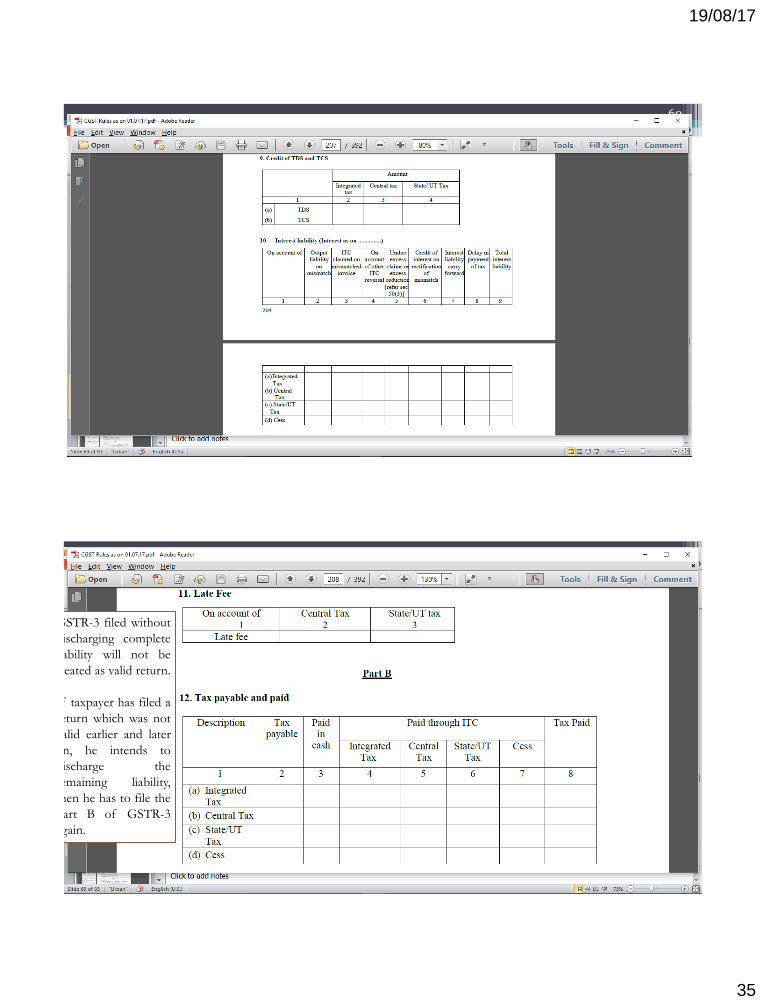

GSTR-3 filed without

discharging complete

liability will not be

treated as valid return.

If taxpayer has filed a

return which was not

valid earlier and later

on, he intends to

discharge the

remaining liability,

then he has to file the

Part B of GSTR-3

again.

19/08/17

36

CA Deepali Mehta GSTR – 2

71

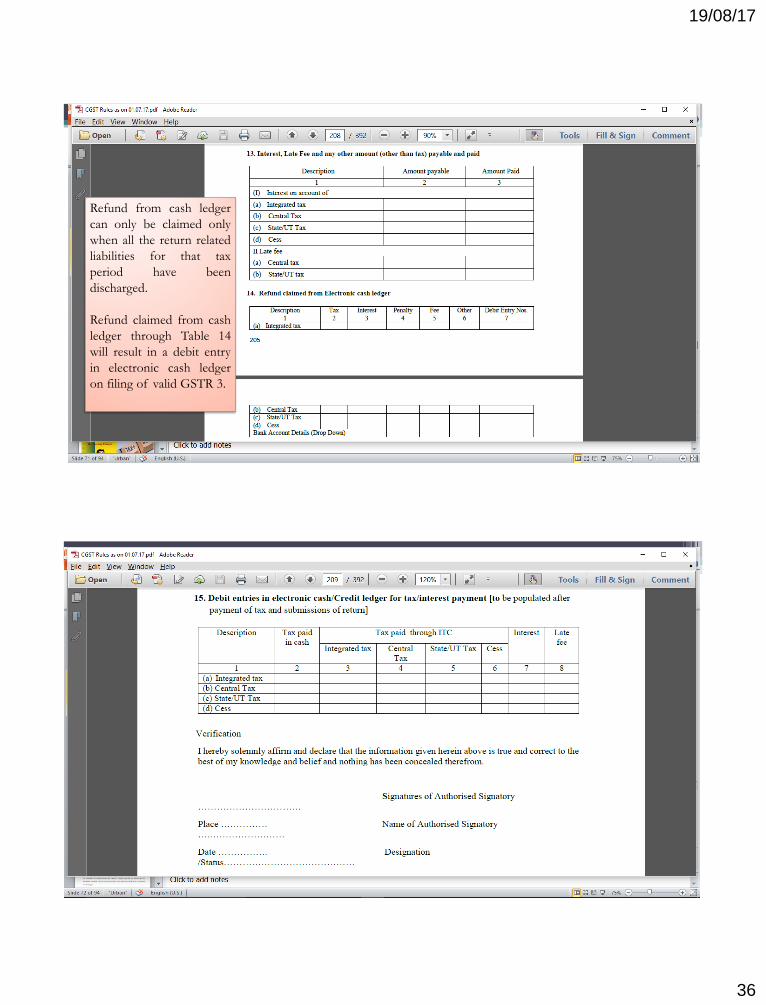

Refund from cash ledger

can only be claimed only

when all the return related

liabilities for that tax

period have been

discharged.

Refund claimed from cash

ledger through Table 14

will result in a debit entry

in electronic cash ledger

on filing of valid GSTR 3.

CA Deepali Mehta GSTR – 2

72

19/08/17

37

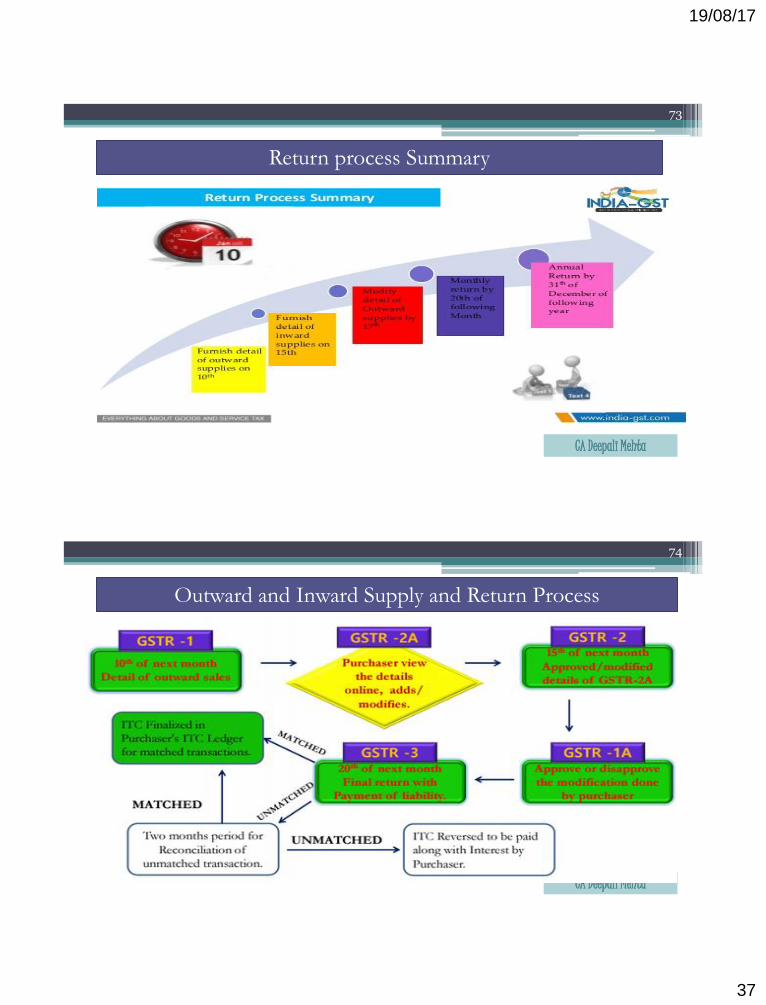

Return process Summary

73

CA Deepali Mehta

Outward and Inward Supply and Return Process

74

CA Deepali Mehta

19/08/17

38

19/08/17

39

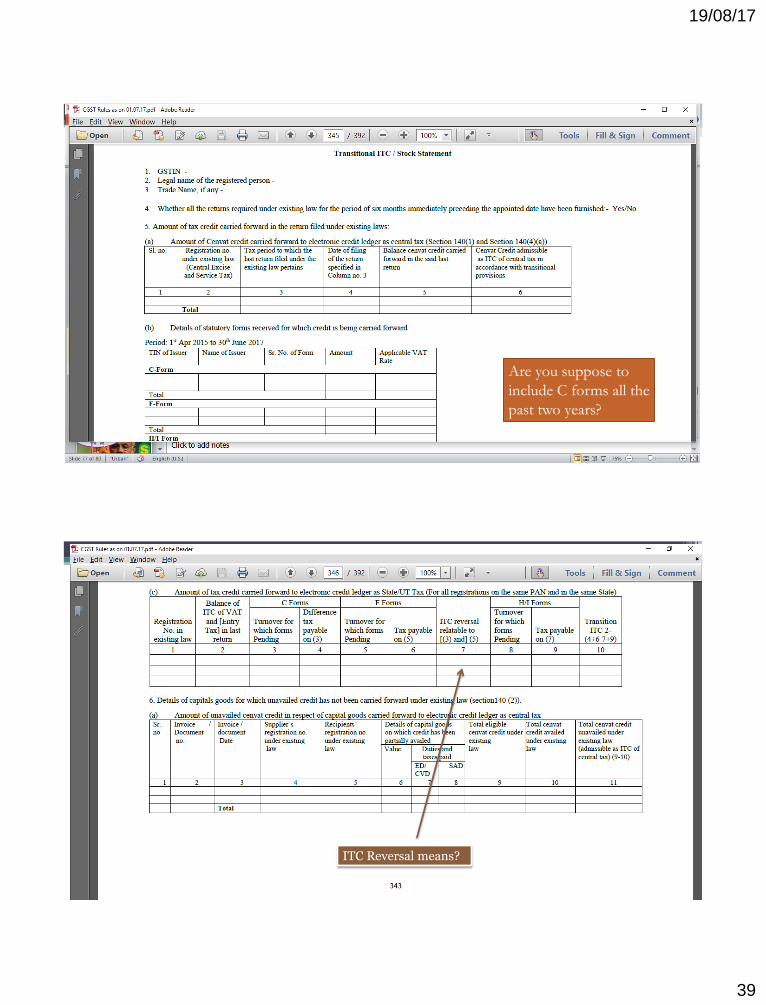

Are you suppose to

include C forms all the

past two years?

ITC Reversal means?

19/08/17

40

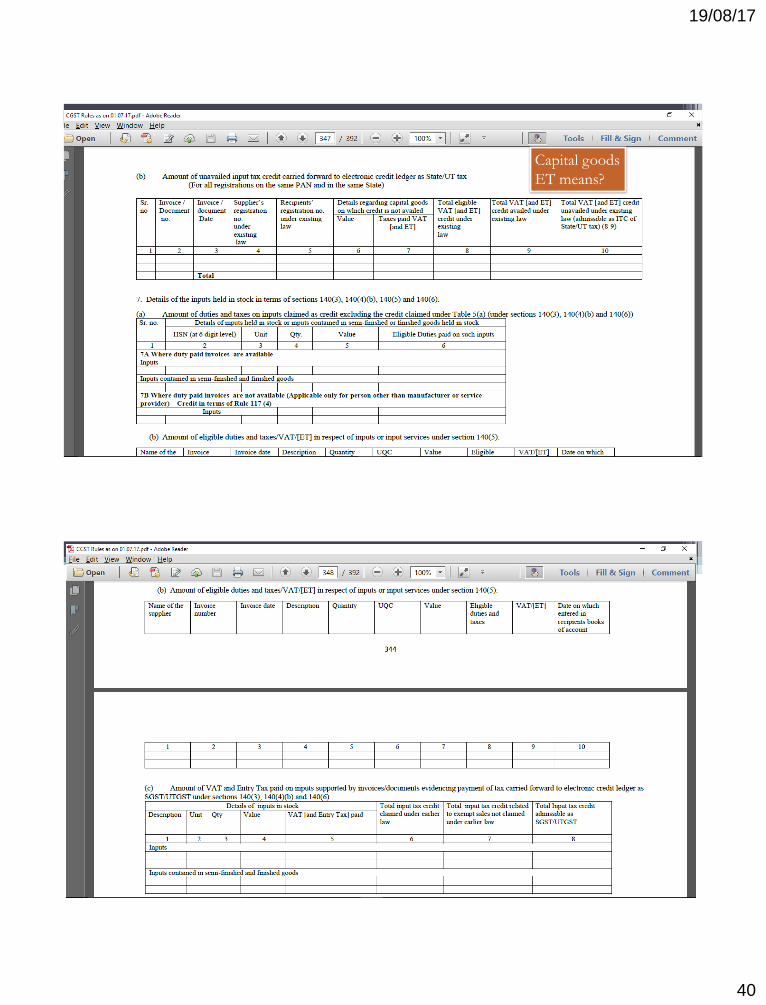

Capital goods

ET means?

19/08/17

41

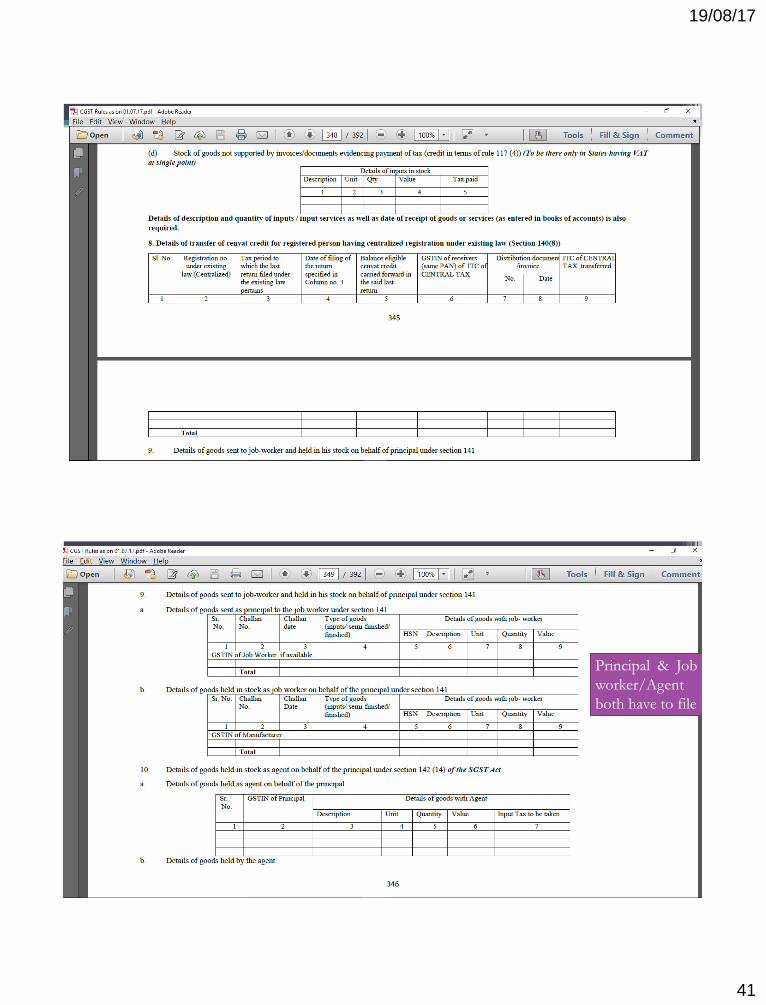

Principal & Job

worker/Agent

both have to file

19/08/17

42

19/08/17

43

CA Deepali Mehta

86

19/08/17

44

CA Deepali Mehta

87

Shah & Savla LLP Chartered Accountants

Visit us at

www.shahnsavla.com

Email: [email protected]

Talk to us at +91 22 61535500

Shah & Savla LLP

88