C7 - 1 Learning Objectives Power Notes 1.Classification of Receivables 2.Internal Control of...

23

C7 - 1 Learning Objectives Power Notes 1. Classification of Receivables 2. Internal Control of Receivables 3. Uncollectible Receivables 4. Uncollectibles – Allowance Method 5. Uncollectibles – Direct Write-Off Method 6. Characteristics of Notes Receivable 7. Accounting for Notes Receivable 8. Balance Sheet Presentation 9. Financial Analysis and Interpretation Chapter F7 C7 Receivables Receivables

-

Upload

ezra-harris -

Category

Documents

-

view

222 -

download

3

Transcript of C7 - 1 Learning Objectives Power Notes 1.Classification of Receivables 2.Internal Control of...

C7 - 1

Learning Objectives

Power Notes

1. Classification of Receivables2. Internal Control of Receivables3. Uncollectible Receivables4. Uncollectibles – Allowance Method5. Uncollectibles – Direct Write-Off Method6. Characteristics of Notes Receivable7. Accounting for Notes Receivable8. Balance Sheet Presentation9. Financial Analysis and Interpretation

Chapter F7

C7

Receivables Receivables

C7 - 2

• Receivables – Classification and Control• Uncollectibles – Direct Write-Off Method• Uncollectibles –Allowance Method• Accounting for Notes Receivable• Balance Sheet Presentation• Accounts Receivable Turnover• Number of Days’ Sales in Receivables

Slide # Power Note Topics

2

4

6

15

20

21

22

Note: To select a topic, type the slide # and press Enter.

Power NotesChapter F7

Receivables Receivables

C7 - 3

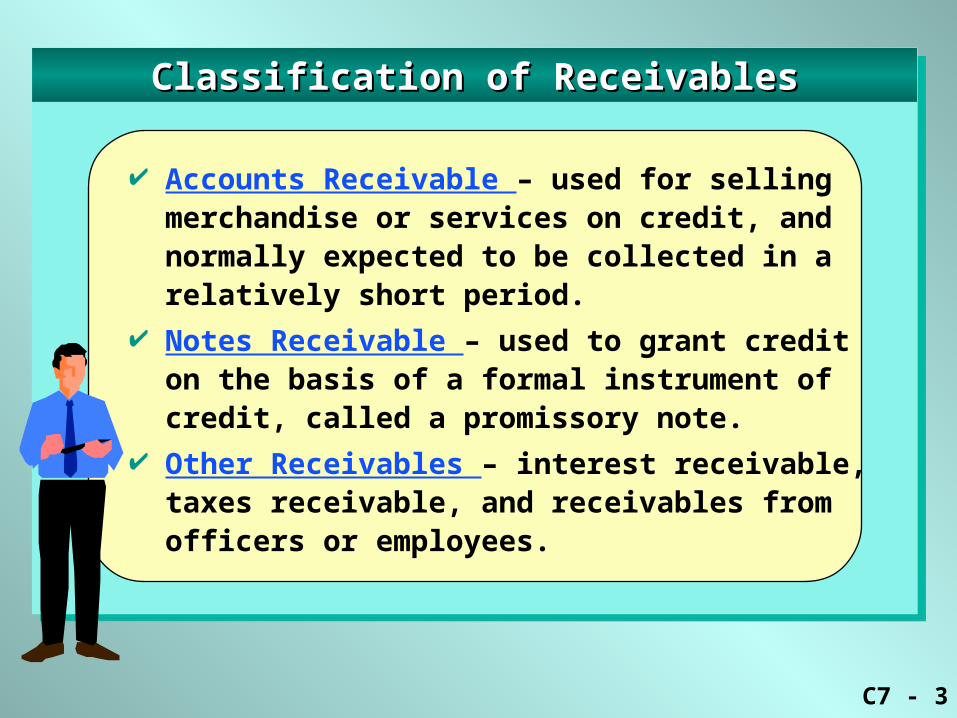

Classification of ReceivablesClassification of Receivables

Accounts Receivable – used for selling merchandise or services on credit, and normally expected to be collected in a relatively short period.

Notes Receivable – used to grant credit on the basis of a formal instrument of credit, called a promissory note.

Other Receivables – interest receivable, taxes receivable, and receivables from officers or employees.

C7 - 4

Accounting for Uncollectible Accounts ReceivableAccounting for Uncollectible Accounts Receivable

• This method is not consistent with the matching principle.

• Accounts that prove to be uncollectible are written off in the year they become worthless.

• Uncollectible Accounts Expense is debited and Accounts Receivable is credited for each such transaction.

The Direct Write-Off Method The Direct Write-Off Method

C7 - 5

Calculating Interest and Maturity ValueCalculating Interest and Maturity Value

Interest CalculationInterest Calculation

We received a $2,500, 10%, 90-day note dated March 16, 2000.

Principal x Rate x Time = Interest

$2,500 x 10% x 90 /360 = $62.50

Principal + Interest = Maturity Value

$2,500 + $62.50 = $2,562.50

Maturity Value CalculationMaturity Value Calculation

C7 - 6

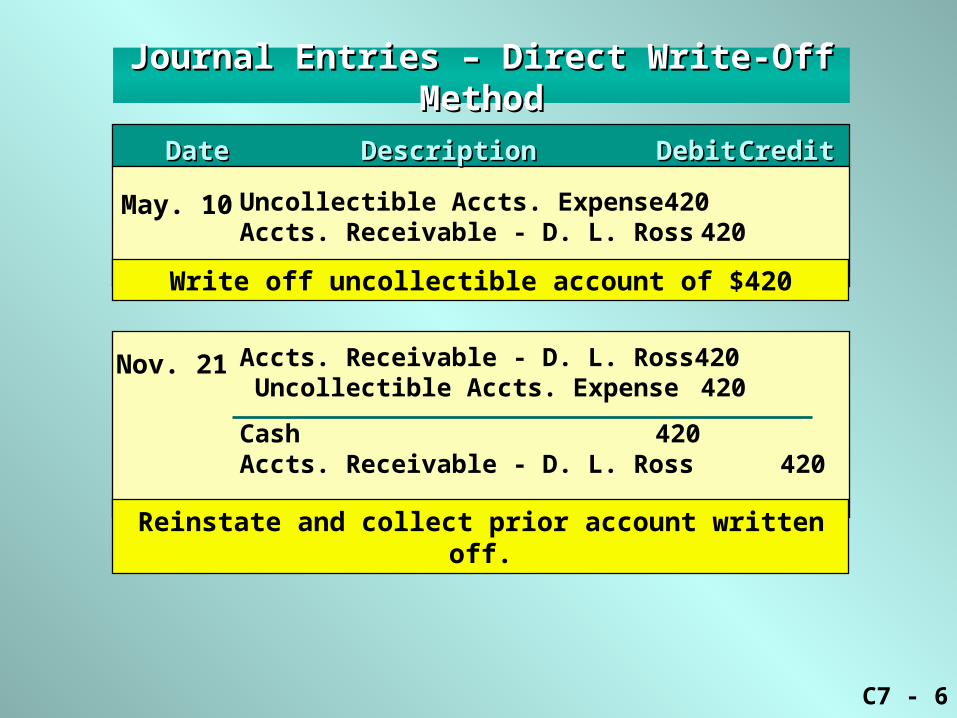

Journal Entries – Direct Write-Off MethodJournal Entries – Direct Write-Off Method

DateDate DescriptionDescription DebitDebit CreditCredit

Uncollectible Accts. Expense 420Accts. Receivable - D. L. Ross 420

Accts. Receivable - D. L. Ross 420 Uncollectible Accts. Expense 420

Cash 420Accts. Receivable - D. L. Ross 420

Write off uncollectible account of $420

Reinstate and collect prior account written off.

May. 10

Nov. 21

C7 - 7

Accounting for Uncollectible Accounts ReceivableAccounting for Uncollectible Accounts Receivable

• This method is consistent with the matching principle.

• Management makes an estimate each year of the portion of accounts receivable that may not be collectible.

• Uncollectible Accounts Expense is debited and Allowance for Doubtful Accounts is credited.

• Actual accounts that prove to be uncollectible are debited to Allowance for Doubtful Accounts and credited to Accounts Receivable.

The Allowance Method The Allowance Method

C7 - 8

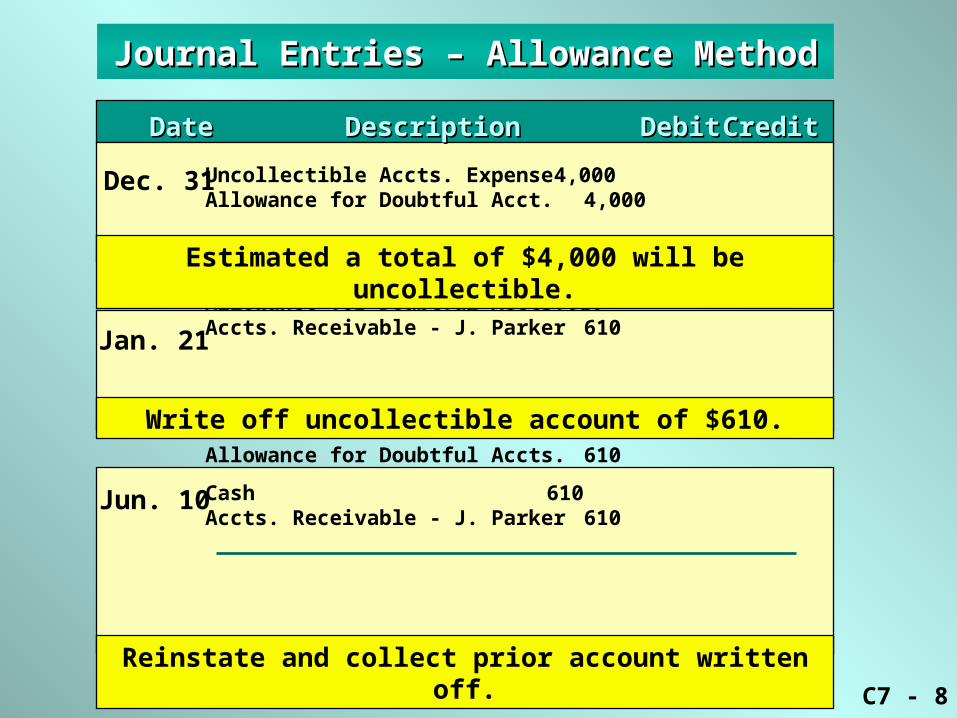

Journal Entries – Allowance MethodJournal Entries – Allowance Method

DateDate DescriptionDescription DebitDebit CreditCredit

Uncollectible Accts. Expense 4,000Allowance for Doubtful Acct. 4,000

Allowance for Doubtful Accts. 610Accts. Receivable - J. Parker 610

Accts. Receivable - J. Parker 610Allowance for Doubtful Accts. 610

Cash 610Accts. Receivable - J. Parker 610

Estimated a total of $4,000 will be uncollectible.

Write off uncollectible account of $610.

Reinstate and collect prior account written off.

Dec. 31

Jan. 21

Jun. 10

C7 - 9

Estimating Uncollectible Accounts ExpenseEstimating Uncollectible Accounts Expense

1. Estimate based on a percentage of sales.

If credit sales for the period are $300,000 and it is estimated that 1% will be uncollectible, the Uncollectible Accounts Expense Uncollectible Accounts Expense is $3,000.

2. Estimate based on analysis of receivables.

If it is estimated that $3,390 of the receivables will be uncollectible and the Allowance for Uncollectible Accounts is $510, the Uncollectible Uncollectible Accounts Expense Accounts Expense is $2,880 ($3,390 – $510).

The allowance method uses two ways to estimate the amount debited to Uncollectible Accounts ExpenseUncollectible Accounts Expense.

C7 - 10

Accounts Receivable Aging and UncollectiblesAccounts Receivable Aging and Uncollectibles

Days Past Dueover

Customer Balance Past Due 1-30 31-60 61-90 91-180 181-365 365

Ashby & Co. $ 150 $ 150B. T. Barr 610 $ 350 $260Brock Co. 470 $ 470

J. Zimmer Co. 160 160

Total $86,300 $75,000 $4,000 $3,100 $1,900 $1,200 $800 $300

Total accounts receivable shown by age.

Not

C7 - 11

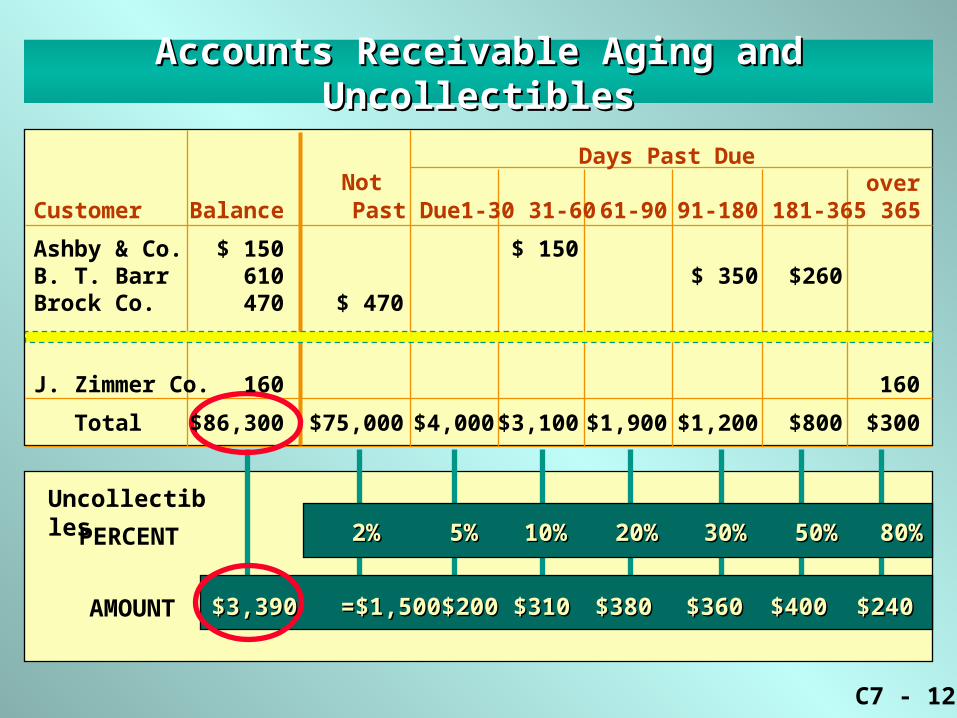

Accounts Receivable Aging and UncollectiblesAccounts Receivable Aging and Uncollectibles

2%2% 5%5% 10%10% 20%20% 30%30% 50%50% 80% 80%

Uncollectibles

PERCENT

Days Past Dueover

Customer Balance Past Due 1-30 31-60 61-90 91-180 181-365 365

Ashby & Co. $ 150 $ 150B. T. Barr 610 $ 350 $260Brock Co. 470 $ 470

J. Zimmer Co. 160 160

Total $86,300 $75,000 $4,000 $3,100 $1,900 $1,200 $800 $300

Uncollectible percentages based on experience and industry averages.

Not

C7 - 12

Accounts Receivable Aging and UncollectiblesAccounts Receivable Aging and Uncollectibles

2%2% 5%5% 10%10% 20%20% 30%30% 50%50% 80% 80%

Uncollectibles

PERCENT

AMOUNT

Days Past Dueover

Customer Balance Past Due 1-30 31-60 61-90 91-180 181-365 365

Ashby & Co. $ 150 $ 150B. T. Barr 610 $ 350 $260Brock Co. 470 $ 470

J. Zimmer Co. 160 160

Total $86,300 $75,000 $4,000 $3,100 $1,900 $1,200 $800 $300

$3,390 =$3,390 = $1,500$1,500 $200$200 $310$310 $380$380 $360$360 $400$400 $240 $240

Not

C7 - 13

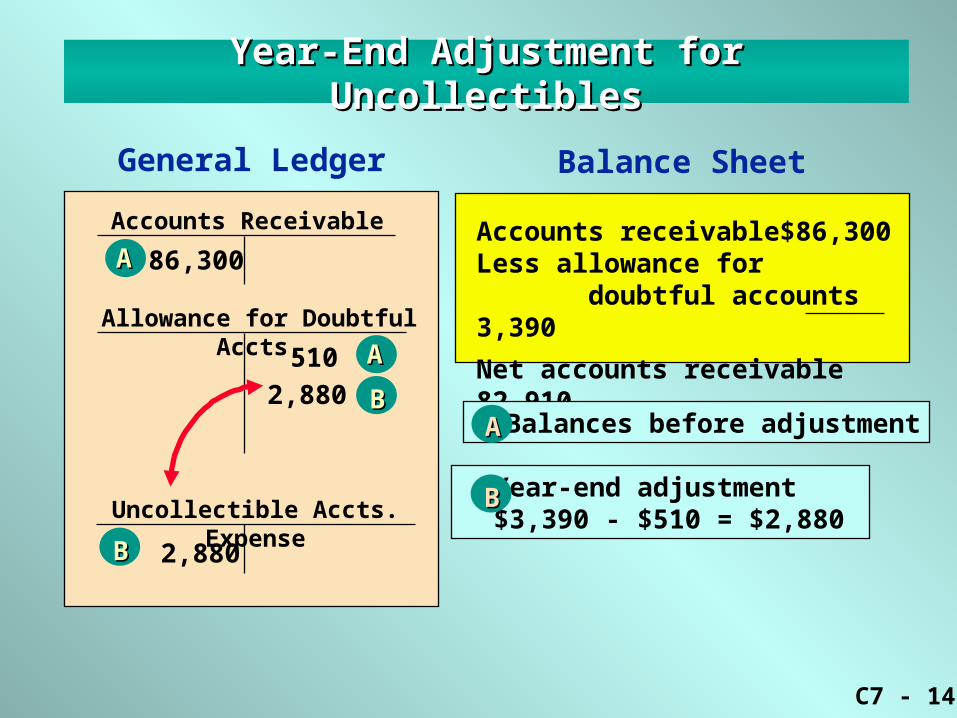

Year-End Adjustment for UncollectiblesYear-End Adjustment for Uncollectibles

General Ledger

Accounts Receivable

86,300AA

Allowance for Doubtful Accts.

510

Uncollectible Accts. Expense

Accounts receivable $86,300Less allowance for doubtful accounts 3,390

Net accounts receivable 82,910

Balance Sheet

Balances before adjustment

AA

AA

C7 - 14

Year-End Adjustment for UncollectiblesYear-End Adjustment for Uncollectibles

General Ledger

Accounts Receivable

86,300AA

Allowance for Doubtful Accts.

510

Uncollectible Accts. Expense

2,880

Accounts receivable $86,300Less allowance for doubtful accounts 3,390

Net accounts receivable 82,910

Balance Sheet

Balances before adjustment2,880

AA

BB

BB

Year-end adjustment $3,390 - $510 = $2,880

AA

BB

C7 - 15

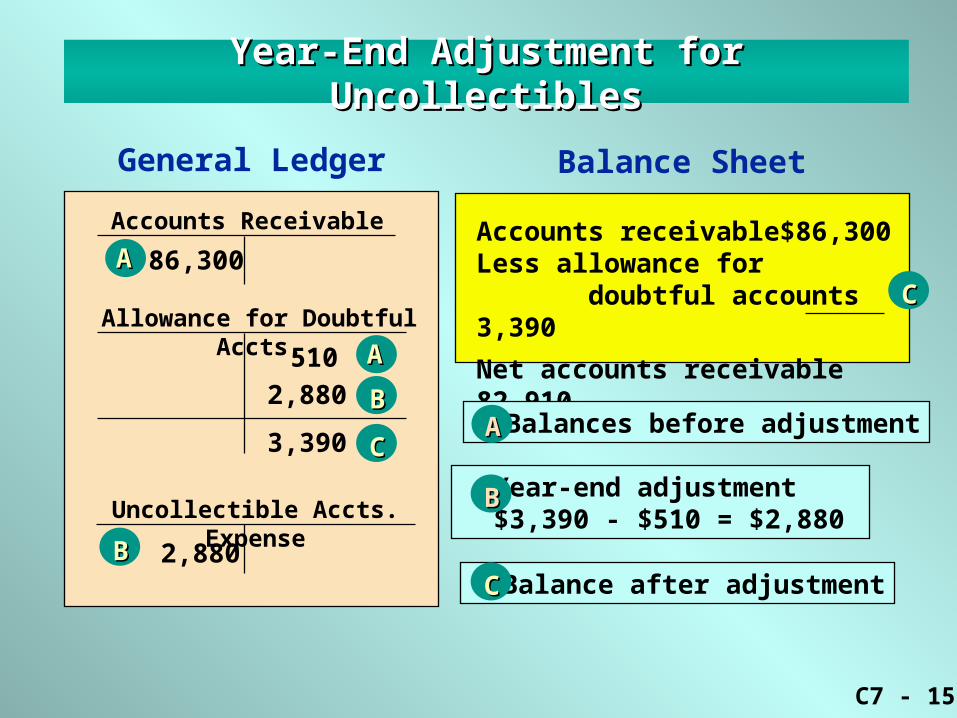

Year-End Adjustment for UncollectiblesYear-End Adjustment for Uncollectibles

General Ledger

Accounts Receivable

86,300AA

Allowance for Doubtful Accts.

510

Uncollectible Accts. Expense

2,880

Accounts receivable $86,300Less allowance for doubtful accounts 3,390

Net accounts receivable 82,910

Balance Sheet

Balances before adjustment2,880

AA

BB

BB

3,390 CC

Year-end adjustment $3,390 - $510 = $2,880

Balance after adjustment

AA

BB

CC

CC

C7 - 16

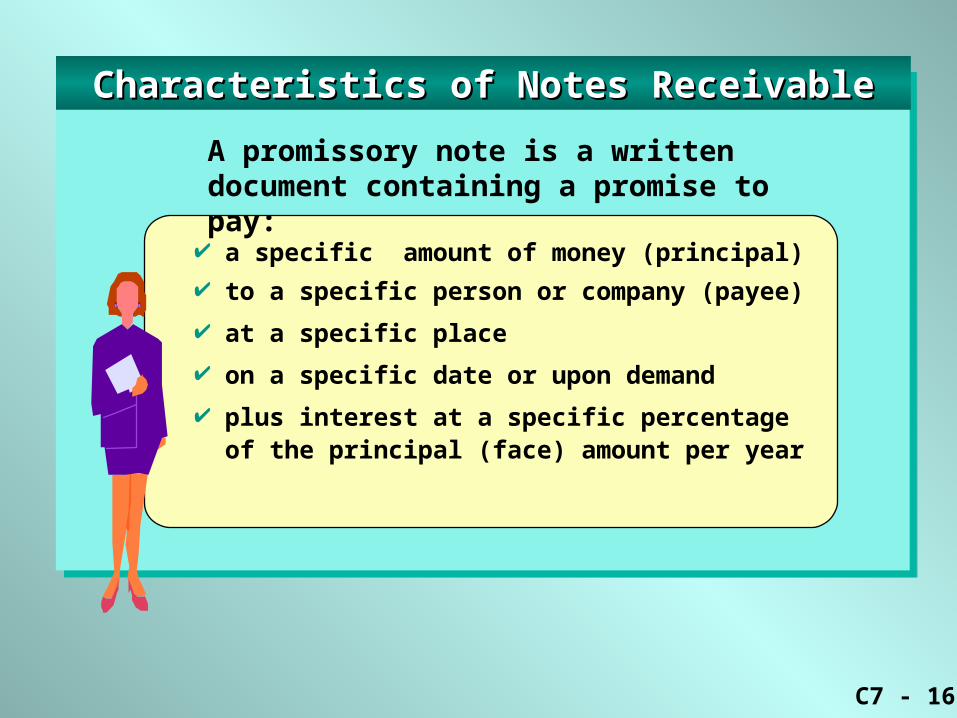

a specific amount of money (principal)

to a specific person or company (payee)

at a specific place

on a specific date or upon demand

plus interest at a specific percentage of the principal (face) amount per year

Characteristics of Notes ReceivableCharacteristics of Notes Receivable

A promissory note is a written document containing a promise to pay:

C7 - 17

Accounting for Notes ReceivableAccounting for Notes Receivable

DateDate DescriptionDescription DebitDebit CreditCredit

Collected amount due on note dated November 21.

Nov. 21

Dec. 21

Notes Receivable 6,000Accts. Receivable - Bunn Co. 6,000

Cash 6,060Notes Receivable 6,000Interest Revenue 60

Principal + Interest = Maturity Value$6,000 + ($6,000 x 12% x 30 / 360) = $6,060

Received a $6,000,30-day, 12% note.

C7 - 18

In commercial transactions it is traditional to use a 360-day year.

The historic rationale for this procedure was ease of calculation which made sense before the computer and calculator age.

Why does this practice continue when most small calculators and desktop computers can present complex interest calculations in a few seconds?

Understanding the 360-Day YearUnderstanding the 360-Day Year

C7 - 19

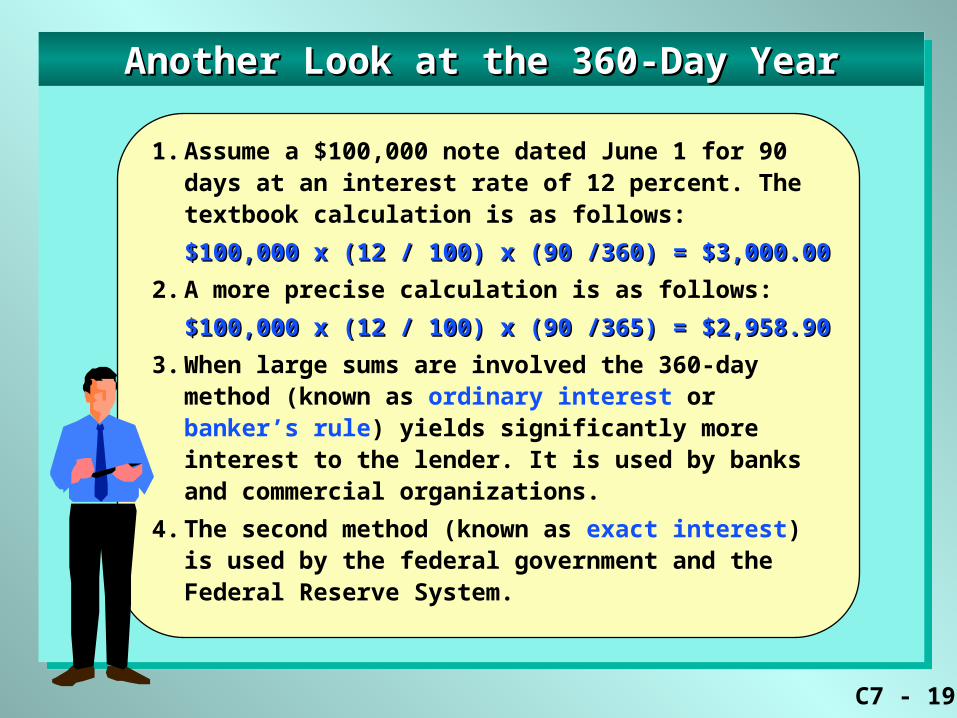

Another Look at the 360-Day YearAnother Look at the 360-Day Year

1. Assume a $100,000 note dated June 1 for 90 days at an interest rate of 12 percent. The textbook calculation is as follows:

$100,000 x (12 / 100) x (90 /360) = $3,000.00$100,000 x (12 / 100) x (90 /360) = $3,000.00

2. A more precise calculation is as follows:

$100,000 x (12 / 100) x (90 /365) = $2,958.90$100,000 x (12 / 100) x (90 /365) = $2,958.90

3. When large sums are involved the 360-day method (known as ordinary interest or banker’s rule) yields significantly more interest to the lender. It is used by banks and commercial organizations.

4. The second method (known as exact interest) is used by the federal government and the Federal Reserve System.

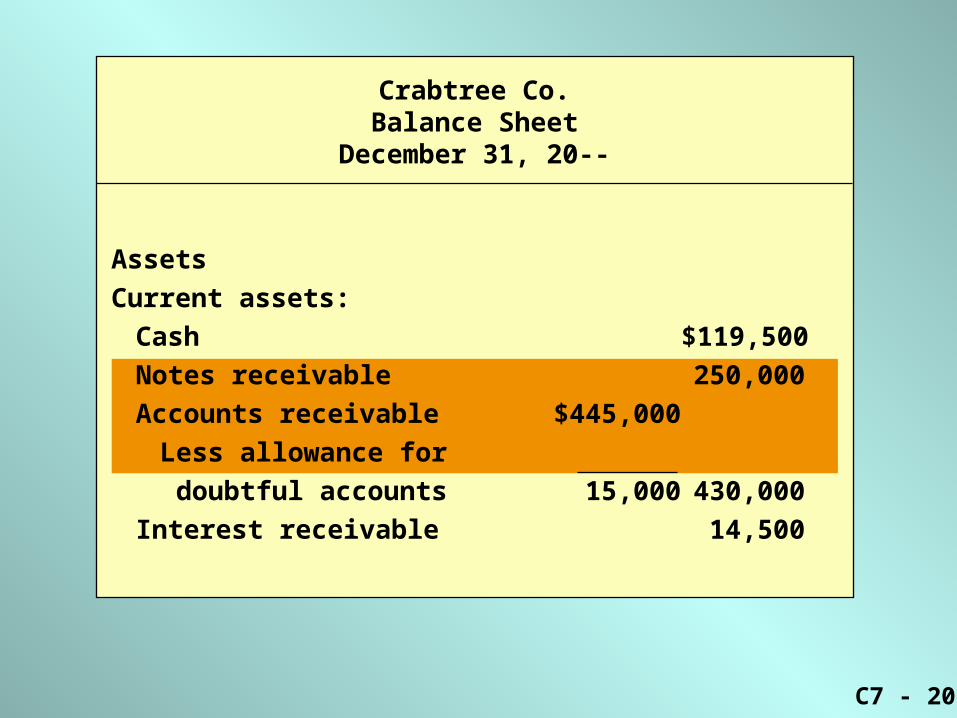

C7 - 20

Assets

Current assets:

Cash $119,500

Notes receivable 250,000

Accounts receivable $445,000

Less allowance for

doubtful accounts 15,000 430,000

Interest receivable 14,500

Crabtree Co.Balance Sheet

December 31, 20--

C7 - 21

Solvency Measures — The Short-Term CreditorSolvency Measures — The Short-Term Creditor

Accounts Receivable TurnoverAccounts Receivable TurnoverAccounts Receivable TurnoverAccounts Receivable Turnover

Use: To assess the efficiency in collecting receivables and in the management of credit.

Use: To assess the efficiency in collecting receivables and in the management of credit.

2000 1999Net sales on account $1,498,000 $1,200,000Accounts receivable (net):

Beginning of year $ 120,000 $ 140,000End of year 115,500 120,000Total $ 235,000 $ 260,000

Average $ 117,500 $ 130,000

Accts. receivable turnoverAccts. receivable turnover 12.7 times12.7 times 9.2 times9.2 times

C7 - 22

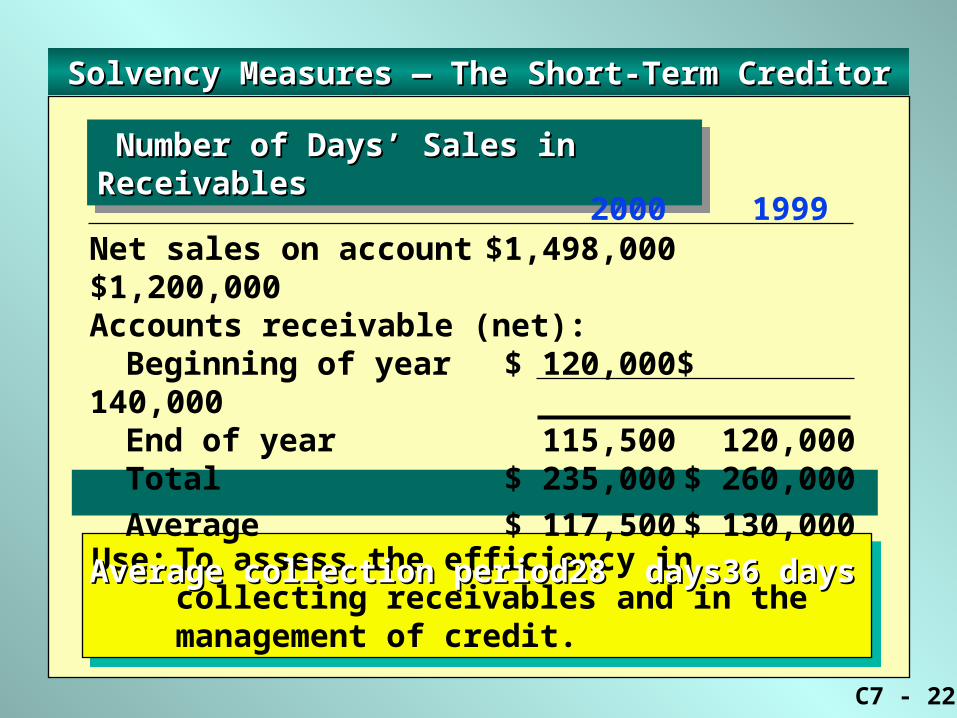

Solvency Measures — The Short-Term CreditorSolvency Measures — The Short-Term Creditor

Number of Days’ Sales in ReceivablesNumber of Days’ Sales in Receivables Number of Days’ Sales in ReceivablesNumber of Days’ Sales in Receivables

Use: To assess the efficiency in collecting receivables and in the management of credit.

Use: To assess the efficiency in collecting receivables and in the management of credit.

2000 1999Net sales on account $1,498,000 $1,200,000Accounts receivable (net):

Beginning of year $ 120,000 $ 140,000End of year 115,500 120,000Total $ 235,000 $ 260,000

Average $ 117,500 $ 130,000

Average collection periodAverage collection period 28 days28 days 36 days36 days

C7 - 23

Note: To see the topic slide, type 2 and press Enter.

This is the last slide in Chapter F7. This is the last slide in Chapter F7.

Power Notes Receivables Receivables

Chapter F7