By Ms. Watana Tiranuchit Ms. Nopalak Rakthum TRIS Rating ... · Ms. Nopalak Rakthum TRIS Rating...

117

By Ms. Watana Tiranuchit Corporate Credit Rating 1 Ms. Watana Tiranuchit Ms. Nopalak Rakthum TRIS Rating Co., Ltd. 3 September 2015

Transcript of By Ms. Watana Tiranuchit Ms. Nopalak Rakthum TRIS Rating ... · Ms. Nopalak Rakthum TRIS Rating...

ByMs. Watana Tiranuchit

Corporate Credit Rating

1

Ms. Watana TiranuchitMs. Nopalak RakthumTRIS Rating Co., Ltd.

3 September 2015

Content (1)

Importance of Credit Rating

Definitions and Symbols

Credit Rating Process

Credit Rating Methodology

2

TRIS Rating Statistics

Credit Rating Fee

FAQ

Credit Rating Methodology

Importance of Credit Rating

3

Importance of Credit Rating

Why do companies need ratings?• To issue debt in capital market (wider fund

raising alternatives in terms of size, maturity, covenant packages)

• Required by the SEC

4

• Required by the SEC– Bond sold to retail investors– Bond with complicate structure

• Required by the investors

• To negotiate more favorable terms with banks• To evaluate its credit risk

Bond market vs. Bank loan Bank Loan

Indirect Lending

Bank Companydeposit Lend

Depositor

Bond Market Direct Lending

5

Investors Company

Bonds

Lend

Rating Agency

Comparison of MLR and Bond Yield

6

*Average 3-year bond yield

20,000,000

25,000,000

30,000,000

35,000,000

Thai Financial Markets

Ba

ht

Mil

lio

nEquity = 44%

Lending = 49%

Debt market = 7%

7

-

5,000,000

10,000,000

15,000,000

Equity Market Lending from Financial Institutions Debt Market

Ba

ht

Mil

lio

n

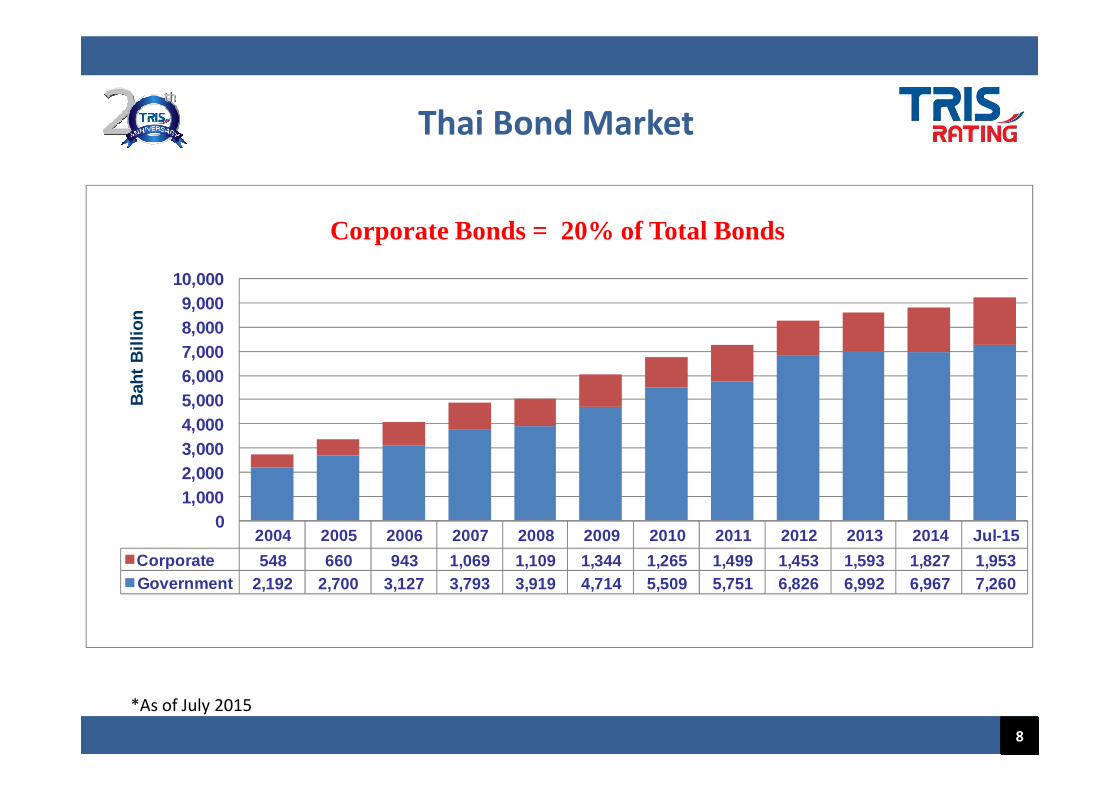

Thai Bond Market

5,0006,0007,0008,0009,000

10,000

Bah

t B

illio

n

Corporate Bonds = 20% of Total Bonds

8

Source: Thai BMA

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 Jul-15

Corporate 548 660 943 1,069 1,109 1,344 1,265 1,499 1,453 1,593 1,827 1,953 Government 2,192 2,700 3,127 3,793 3,919 4,714 5,509 5,751 6,826 6,992 6,967 7,260

01,0002,0003,0004,0005,000B

aht

Bill

ion

*As of July 2015

New Corporate Bond Issuance

300,000

400,000

500,000

600,000B

aht M

illio

n

Fixed Income Instruments9

0

100,000

200,000

300,000

Bah

t Mill

ion

40%

50%

60%

70%

80%

90%

100%

New Corporate Bond Issuance by sector

10

0%

10%

20%

30%

40%

2007 2008 2009 2010 2011 2012 2013 2014 Jul-15

Bank Leasing Energy Residential Telecom Others

Definitions and Symbols

11

Meanings of the Credit Rating

“The opinion of the rating agency about relative ability and the willingness of the company to repay ability and the willingness of the company to repay its obligations, including principal and interest, in full and on time”

• Rating reflects the relative ranking of “Default Risk” of the company

12

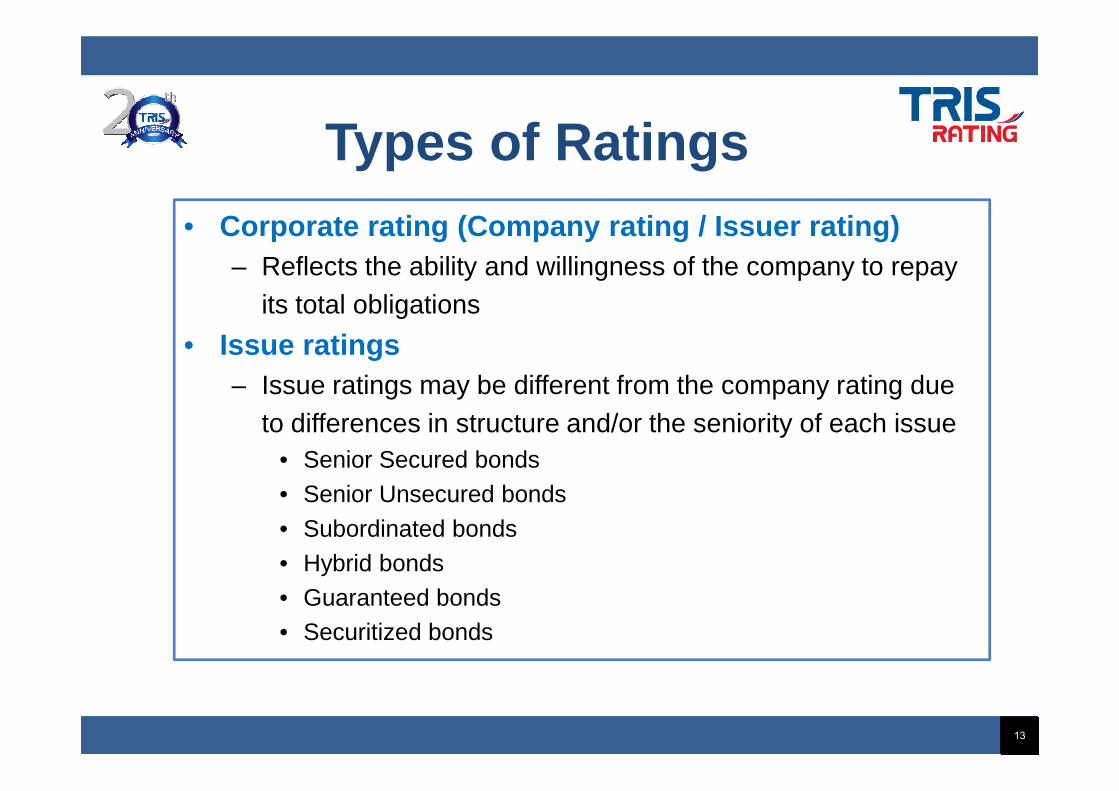

Types of Ratings• Corporate rating (Company rating / Issuer rating)

– Reflects the ability and willingness of the company to repay its total obligations

• Issue ratings– Issue ratings may be different from the company rating due – Issue ratings may be different from the company rating due

to differences in structure and/or the seniority of each issue• Senior Secured bonds• Senior Unsecured bonds

• Subordinated bonds• Hybrid bonds• Guaranteed bonds• Securitized bonds

13

Example of Issue Rating

Senior secured debentures

A+

Debt Type

14

Senior unsecured debentures

Subordinated debentures

Guaranteed debentures

AAA

A

A-

Issuer Rating

A

Guarantor

AAA

“Credit Rating” V.S. Level of RiskRating Category Risk Grade

AAA Lowest

Investment Grade

AA+

AA

AA-

A+

A

A-

BBB+

15

BBB+

BBB Medium

BBB-

BB+

Speculative Grade

BB

BB-

B+

B

B-

C Highest

D Default

Credit Rating Agency

There are two types of CRAs

1. International Credit Rating Agency : Provide the rating services to both sovereigns and companies

16

rating services to both sovereigns and companies globally

2. Domestic Credit Rating Agency : Provide the rating services to companies within a specific country or region

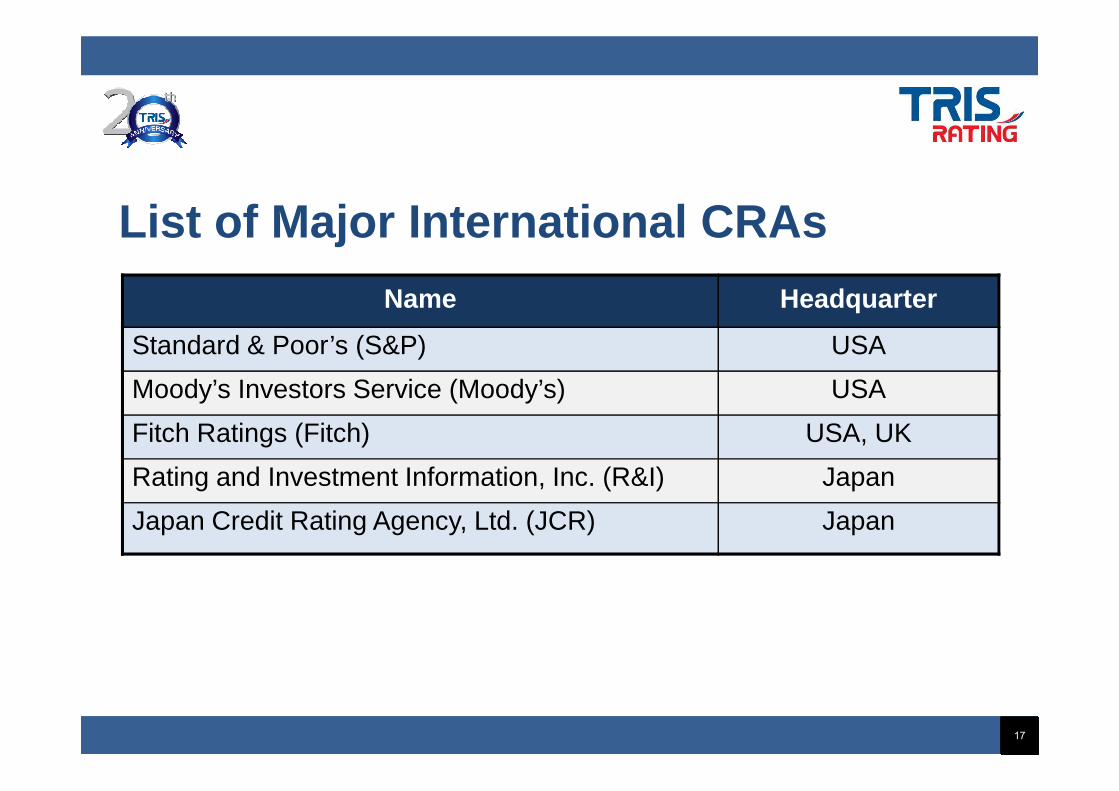

List of Major International CRAs

Name Headquarter

Standard & Poor’s (S&P) USA

Moody’s Investors Service (Moody’s) USA

17

Moody’s Investors Service (Moody’s) USA

Fitch Ratings (Fitch) USA, UK

Rating and Investment Information, Inc. (R&I) Japan

Japan Credit Rating Agency, Ltd. (JCR) Japan

Examples of Local CRAs

Name Headquarter

TRIS Rating Co., Ltd. Thailand

Rating Agency Malaysia Berhad Malaysia

18

Rating Agency Malaysia Berhad Malaysia

CRISIL Limited India

PEFINDO Credit Rating Indonesia Indonesia

Philippine Rating Services Corporation Philippines

S&P Clients in Thailand vs. TRIS Rating

NameS&P

TRIS RatingForeign Local

THAILAND BBB+/Stable A-/Stable

19

BAY BBB+/Stable BBB+/Stable AAA/Stable

PTTEP BBB+/Stable BBB+/Stable AAA/Stable

RATCH BBB+/Stable BBB+/Stable AAA/Stable

TMB BBB-/Stable BBB-/Stable A+/Stable

As of 28 Aug 2015

Rating SymbolTRIS Rating S&P Moody’s

AAA AAA AaaAA+ AA+ Aa1AA AA Aa2AA- AA- Aa3A+ A+ A1A A A2A- A- A3

BBB+ BBB+ Baa1

BBB BBB Baa2BBB - BBB - Baa3

20

BBB - BBB - Baa3

BB+ BB+ Ba1BB BB Ba2

BB- BB- Ba3

B+ B+ B1B B B2

B- B- B3C+ CCC+ Caa1C CCC Caa2C- CCC- Caa3

CC Ca

RD SD and D C

Credit Rating ProcessCredit Rating Process

21

Credit Rating ProcessCredit Rating Process

Initial Rating Process

� INFORMATION GATHERING

� INTERVIEW MAJOR DEPT. & SITE VISIT

� MANAGEMENT/

DISAGREE

RATING COMMITTEE

MEETING

•APPEAL WITHIN 7 DAYS•PROVIDE NEW DATA WITHIN 15 DAYS WITH-

DRAWN

INFORM RATING TO

ISSUER

ANALYSIS

22

� MANAGEMENT/AUDIT COM. MEETING

MEETING

RATING ANNOUNCEMENT

KEEPCONFIDENTIAL

6 WEEKS 2 WEEKS

* For more details, please see www.trisrating.com/ Rating Information/Rating Process

ISSUERACCEPT

MONITOR & ANNUAL REVIEW

MONITOR & ANNUAL REVIEW

Annual Review Process• INFORMATION

UPDATE

• MANAGEMENT MEETING

RATING COMMITTEE

MEETING

2-3 WEEKS 2 WEEKS

INFORM REVIEW RESULT

TO ISSUER

ANALYSIS

23

CANCELLATION ANNOUNCEMENT

RATING ANNOUNCEMENT

KEEPCONFIDENTIAL

* For more details, please see www.trisrating.com/ Rating Information/Rating Process

MONITOR & ANNUAL REVIEW

MONITOR & ANNUAL REVIEW

WITH-DRAWN

List of Preliminary information required

PAST / CURRENT / PROJECTION� Background information of the company� Shareholder structure� Organization of management� Investment in related companies� Business policy / Marketing policy / Pricing policy� Operating data and market research� List of major customers / supplier / competitors� Financial data i.e. breakdown of revenue and cost structure� Debt profile / major loan agreements� Financial projection, including CAPEX & investment plan� Etc. i.e. other contractual agreements, audit committee report

24

Rating Monitoring & Report• Initial Rating & Annual Review

Report:– Assign / affirm / change : Rating and/or Outlook

• New Issue RatingReport:– Assign rating for new issue; – Affirm : Rating and/or Outlook (can be changed if necessary)– Affirm : Rating and/or Outlook (can be changed if necessary)

• Quarterly Monitoring– Projection comparison

• Special Monitoring (event risks)Report:

– Credit Update Affirm / change : Rating and/or Outlook

– Credit Alert Remove Outlook & replace with Alert : positive / negative / developing

25

Credit Rating MethodologyCredit Rating Methodology

26

Credit Rating MethodologyCredit Rating Methodology

• Industry Analysis

• Business Analysis

Key Rating Factors

• Business Analysis

• Financial Analysis

27

Rating ProcessIndustry Analysis Business Analysis

Business Risk Financial Risk

Financial Analysis

28

Rating Assignment by Rating Committee

Monitoring Process

Industry Analysis

1. Nature of the company’s industry2. Industry prospects2. Industry prospects3. Level of competition

29

Industry Analysis (1)

1. Nature of the company’s industry• Cyclicality of the industry, vulnerability to

change in the economychange in the economy

• Evolving or well-established industry

30

Industry Analysis (2)

2. Industry prospects• Demand growth potential • Secular change of product/technology• Secular change of product/technology

31

Industry Analysis (3)

3. Level of competition• Competitive environment: number of players,

demand-supply balance• Barriers to entry: business nature or regulation

• License requirement• Capital intensive• Sophisticated technology

• Threats of substituted products• The degree of product differentiation (branded)

32

Business Analysis

1. Strategy & management

2. Ownership & group support2. Ownership & group support

3. Diversification4. Competitive position

33

Business Analysis (1)

1. Strategy & Management• Long term strategy, strategic planning, decision

makingmaking• Track record and competency of management team• Management team structure, continuity and

succession• Control, auditing, risk management and information

system

34

Business Analysis (2)

2. Ownership & Group support • On-going supports either financially or

operationallyoperationally• Business synergy and group performance• Strengths derived from parent and/or subsidiary

support

35

Business Analysis (3)

3. Diversification• Diversity of business - product lines,

customer base, market segments, customer base, market segments, geographic

• Ability to manage diverse operations

36

Business Analysis (4)

4. Competitive PositionMarket position

– Market share, size, scale– Brand reputation/awareness– Assets quality– Product quality – Marketing networks / logistics / distribution channels – Customer base– Technological advantage, innovation, R&D

37

Business Analysis (5)

4. Competitive Position (cont.)Operational Efficiency/Cost competitiveness– Economies of scale:- capacity and utilization– Economies of scale:- capacity and utilization– Operating skills:- production yield, waste reduction– Procurement of raw materials and inventory management– The efficiency of worker– Quality control– Cost structure

38

Financial Analysis

Qualitative Analysis • Accounting quality• Financial policy• Financial policy

Quantitative analysis• Capital structure• Profitability• Efficiency• Cash flow protection and liquidity

39

Financial Analysis (1)Qualitative Analysis

• Accounting quality– Disclosure of information– Auditor’s report/opinion– Auditor’s report/opinion– Changes in accounting policies

• Financial policy– Funding policy – Target capital structure– Dividend policy– Reserves for bad debts or policies for writing off

obsolete Inventory– Hedging policy

40

Financial Analysis (2)

Quantitative analysis1. Capital structure

• Leverage level, D/E ratio• Leverage level, D/E ratio• ST loans vs. LT loans• Major adjustments for off-balance sheet obligations

– Operating leases – Financial guarantees/ supports provided to related parties– Litigations– Potential penalties

41

Financial Analysis (3)

2. Profitability• Gross profit margin• Operating profit margin• Net Profit Margin• ROA , ROE, ROPC (return on permanent

capital)

42

Financial Analysis (4)

3. Efficiency• Inventory turnover / Inventory days• A/R days• A/R days• A/P days• Operating cash cycle

Very important for trading firms/ retailers to determine level of cash flow needed for normal operation

43

= AR days +Inventory Days – AP days= AR days +Inventory Days – AP days

Financial Analysis (5)4. Cash flow protection and liquidity4.1 Cash Flow Protection

• FFO/total debts• Interest coverage ratio• DSCR = debt service coverage ratio• Refinancing risk

4.2 Liquidity/financial flexibility• Cash on hand• Unused credit lines: committed vs. uncommitted • Accessibility to capital and money markets• Other liquid assets• Support from shareholders

44

Industry

BusinessCompany

Business

Financial

Company

Rating

45

Outlook ���� แนวโน้มอันดับเครดติ

“ Rating outlook will always be assigned to all long-term ratings”

“ Rating outlook ���� potential for change over medium term (1-2 years)”

46

stable (คงที�) = not likely to changepositive (บวก) = likely to be raisednegative (ลบ) = likely to be lowerdeveloping (ยังไม่ชัดเจน) = may be raised, lowered or unchanged

Credit Rating Fee

47

Credit Rating Fee

Credit Rating Fees• Annual Fee

– Company rating– Issue rating– Issue rating

• Site Visit expenses

• Legal Fee (if any)

48

TRIS Rating Statistics

49

TRIS Rating Statistics

TRIS Rating’s Rated Issuers• 370 issuers since 1993, with total issue size of approximately Bt2.9 trillion• 159 outstanding rated issuers as of 19 August 2015 (published 132/ private & in the rating process 27)• Rated issuers include both Thai and multinational corporations• Ratings assigned to diverse sectors

Sector No. of Rated Issuers

Financial Institutions 41

Property Developers 27

50* As of 19 Aug 2015* As of 19 Aug 2015

Property Developers 27

Energy 18

Agro & Food 15

Engineering & Construction 9

Transportation 7

Telecom 8

Commerce 5

Healthcare Services 3

Others 26

TOTAL 159

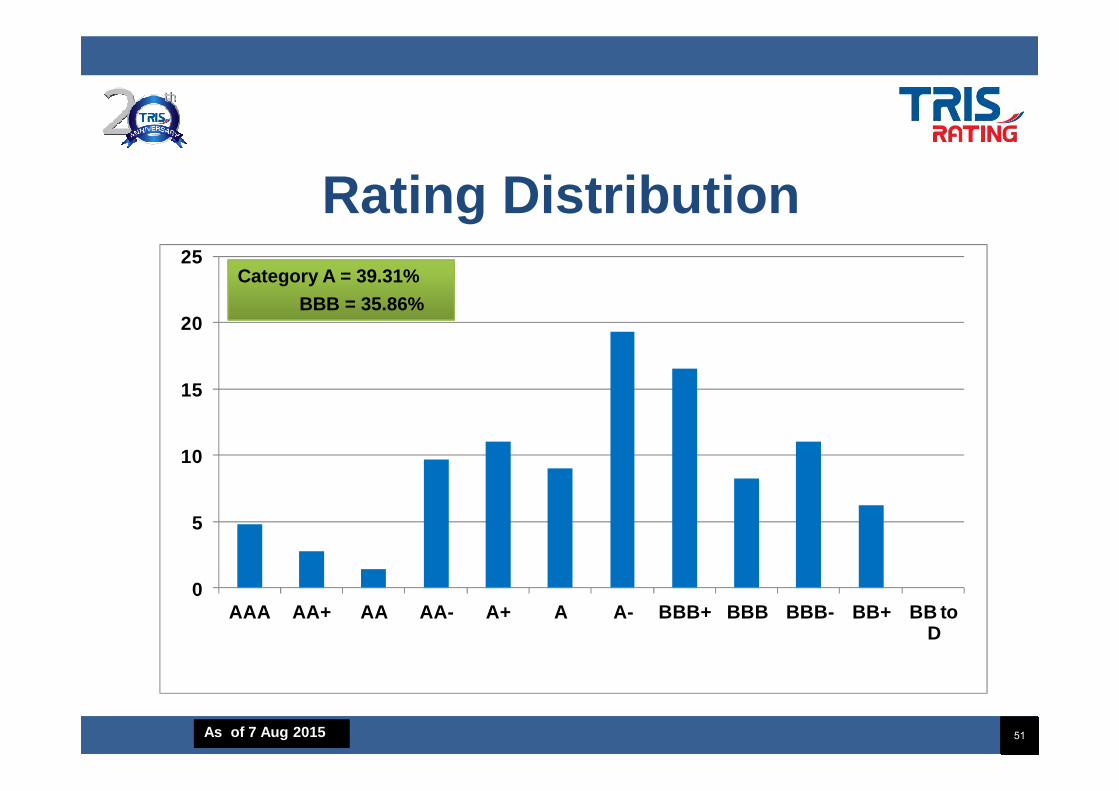

Rating Distribution

15

20

25Category A = 39.31%

BBB = 35.86%

51

0

5

10

15

AAA AA+ AA AA- A+ A A- BBB+ BBB BBB- BB+ BB to D

As of 7 Aug 2015

Engineering & Construction

40

60

80

% N

o. o

f clie

nts

52

AAA AA+ AA AA- A+ A A- BBB+ BBB BBB - BB+ to D

% 0 0 0 0 0 0 22 11 11 56 0

0

20

40

% N

o. o

f clie

nts

As of Aug 2015

Energy

40

60

80

% N

o. o

f clie

nts

53

AAA AA+ AA AA- A+ A A- BBB+ BBB BBB- BB+ to D

% 17 0 0 0 22 6 11 11 22 0 0

0

20

40

% N

o. o

f clie

nts

As of Aug 2015

Agri & Food Industry

40

60

80

% N

o. o

f clie

nts

54

AAA AA+ AA AA- A+ A A- BBB+ BBB BBB- BB+ to D% 0 0 21 21 14 14 0 0 14 0

0

20

40

% N

o. o

f clie

nts

As of Aug 2015

Residential Developers

40

60

80

% N

o. o

f clie

nts

55

AAA AA+ AA AA- A+ A A- BBB+ BBB BBB- BB+ to D

0 0 0 0 5 10 5 19 10 24 14

0

20

40

% N

o. o

f clie

nts

As of Aug 2015

Frequently Asked Questions about Credit Ratings

56

about Credit Ratings

Frequently Asked Questions• Which industry has the high/low credit risk?• How does the industry cycle affect the rating of a

company?• When will the rating change? Time horizon of rating.• When will the rating change? Time horizon of rating.• What is the default rate of each individual rating

category? Can “AAA” default?

57

Which Industry has the High/Low Credit Risk?

58

High/Low Credit Risk?

“Industry risk influences but not the only risk that determine a company credit rating”

Industry risks + Business risks + Financial risks Credit risks Ratings

59

High Risk Industries1. Highly cyclical

� residential property, shipping, steel

2. Intensive competition: many players, commodity products products � petrochemical, construction materials, airline, contractor,

semiconductor

3. Expose to (uncontrollable) external factors� agricultural products, airlines, hotel

60

High Risk Industries4. Rapid change of technology

� internet, semiconductor

61

Low Risk Industries1. Steady demand growth

� Utility i.e. electricity, water

2. Ability to maintain margins� Branded consumer products� Branded consumer products

3. Monopoly� Air traffic control

62

How the Industry Cycle Affects the Rating of a Company?

63

When Will a Rating Change?

“A credit rating for a company at any time incorporates industry cycle and expectation about risks of the expectation about risks of the company over the medium term.”

64

• Industry cycles �demand fluctuation, and swings of supply capacity

• Exception, when the cycle and/or the • Exception, when the cycle and/or the company’s performance is substantially different from initial expectation

65

Rating Through the Cycle

Highest

Rating

6666

Lowest

Present Future (3-5 years)Past

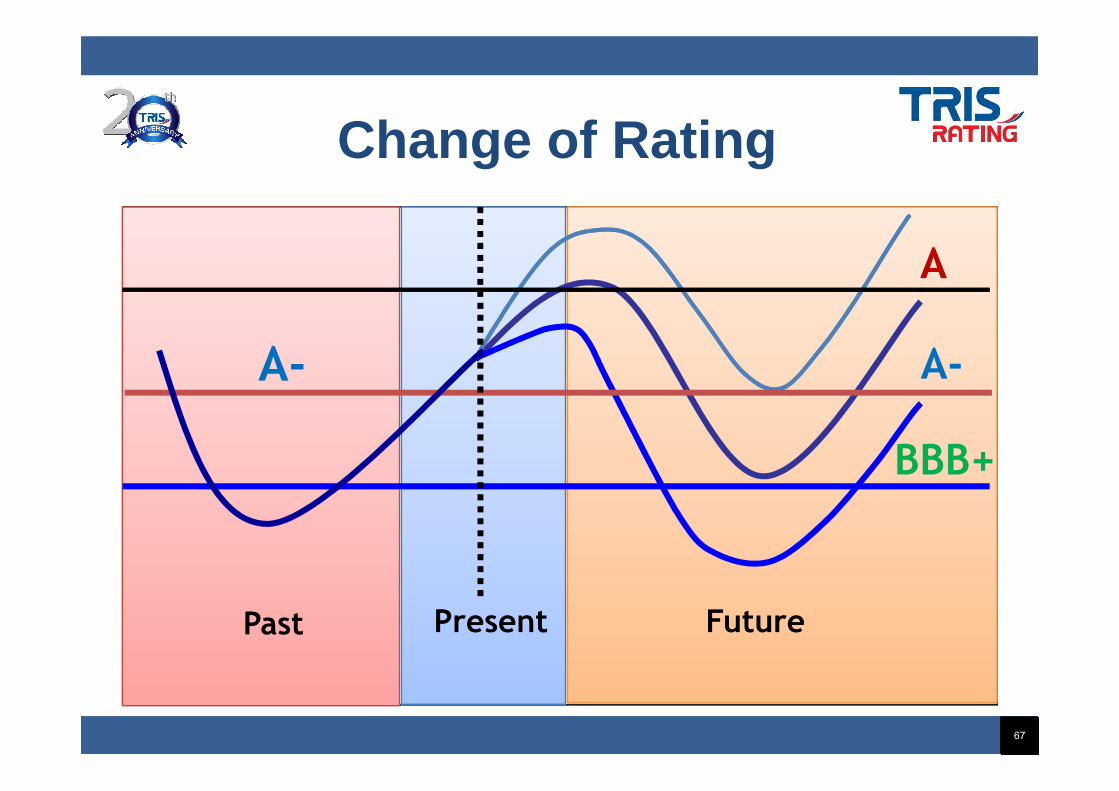

Change of Rating

A-

A

A-

67

FuturePresent

BBB+

Past

“ Rating of a company will be changed when a company risks differ from previous expectation significantly and permanently.”significantly and permanently.”

“ Rating of a lower rated companies will be more likely to change than a higher rated.”

68

What is the Default Rate of Each Individual Rating Category?

69

Can AAA Default?

Cumulative Defaulters By Time Horizon Among Global Corporates, From Original* Rating (1981-2014)

AAA AA A BBB BB B CCC/C TotalNumber of issuers defaulting within

one year 3 12 70 68 153

Three years 1 6 28 132 508 137 812

Five years 4 13 68 273 837 165 1,360

70

Five years 4 13 68 273 837 165 1,360

Seven years 2 7 27 99 365 1,016 174 1,690

Total 8 30 91 191 555 1,242 184 2,301

Source: S&P’s : Default, Transition, and Recovery:

2014 Annual Global Corporate Default Study And Rating Transitions

30-Apr-2015

71

Q & A

THANK YOU

72

Contact Person:

Business Development Department:Ms. Kornkamol Thavisin [email protected]

73

TRIS Rating Co., Ltd.24th Floor, Silom Complex Building

Tel: 0-2231-3011#218Fax: 0-2231-3012www.trisrating.com

Most Frequently Asked Questions About Credit RatingAbout Credit Ratingby

Nopalak Rakthum

1

Emerging of New Financial Instruments

• Over the past 20 years, new financial instruments and rating concepts emerged and developed

– National scale

– Parent guaranteed; Partial guaranteed

Asset-backed securities– Asset-backed securities

– Government related entities

– Hybrid capital instruments

– Sovereign rating and T&C

– Group rating

2

Most Frequently Asked QuestionsAbout Credit Rating

1. What are the differences of the ratings assigned by TRIS Rating vs other CRAs?

2. When the rating could not be assigned?

3. How to rate the related companies (group rating) ?3. How to rate the related companies (group rating) ?

4. How can the rating of issuer be enhanced or notched down or capped?

5. How can the rating of specific issue be enhanced or notched down or capped?

3

Most Frequently Asked QuestionsAbout Credit Rating (continued)

6. What are rating factors of hybrid capital instruments?

7. How much equity content will be given to a specific characters of hybrid capital instruments ?

8. What is the maximum equity content allowed for an issuer?issuer?

9. What are rating factors of sovereign rating ?

10. Can the sovereign rating assigned by TRIS Rating compare with other ratings assigned by TRIS Rating, i.e. corporate ratings?

11. What are factors that TRIS Rating used to assign ratings of companies operated overseas?

4

Concept of credit ratings

• Rating is raking, based on level of credit worthiness

• The measurement of ability and willingness to comply with financial obligations of ultimate obligorultimate obligor

• Specific repayment schedule and measurable amount

“ Technically, dividend payment is not financial obligation” � imputed promised

5

What are the differences of the ratings assigned by TRIS Rating vs other CRAs?CRAs?

6

Three Concepts of Credit Rating Scale

Rating is comparison…

• International (global) comparison �

international scale

• Regional comparison � regional scale• Regional comparison � regional scale

• National (domestic) comparison �

national scale

7

International Scale Ratings

• Global comparison

• Local currency and foreign currency

• Benefits to international investors for global investment decision making.global investment decision making.

• No limits on regional or national boundary.

• Highest rating in a country may not be AAA.

8

National and Regional Scale Ratings

• Comparable within a country (or region) only

• Could not compare with international ratings

• Generally assign only local currency rating

Highest rating of domestic issuers could be • Highest rating of domestic issuers could be AAA,

– mostly assign to the government.

9

National Scale Rating Is Not A Mapping

• TRIS does not map rating of international scale into national scale.

• For parent-guaranteed debentures, TRIS Rating will analyze credit risks using our best effort based on available information.

• The rating of parent company should be rated by TRIS Rating otherwise the rating of parent company rated by NRSROs should not lower than BBB.not lower than BBB.

• TRIS Rating will not use only rating assign by international CRAs to map into national scale. Though the availability of ratings will provide essential information.

• Even though Thai government rated by S&P = A-, TRIS Rating will not reach the national scale rating by the mark up of 6 from international scale. TRIS Rating will evaluate the ratings assigned by other CRAs and assess more detail of the business risks and financial performance.

• Our experience shows that the lower the international scale rating the narrower the rating gap between national vs international scale

10

However, the ratings within TRIS Rating Scale should be comparable, no matter they are should be comparable, no matter they are industrial companies, financial institutions, government-related entities, or sovereigns.

11

When the rating could not be assigned ?assigned ?

12

Rating assigned to credit-based financial obligations

• Interest bearing debts

• Credit based financial obligations

• Specific amount and repayment schedule• Specific amount and repayment schedule

13

CRA will not assign ratings to..

• Equity stock

• Debt instrument which repayment tied with stock index, or commodity prices, etc.

• When information about the issuer is • When information about the issuer is insufficient: very short track record; under restructuring process; no audited financial report, etc.

14

How can the rating of “issuer” and “issue” be enhanced or notched down or capped?down or capped?

15

Rating Enhancement

• “Issuer rating” will be enhanced if default risk of the issuer is lower by:– Extraordinary support from government (GRE)

– Extraordinary support from parent company or groupgroup

• “Issue rating” will be enhanced if default risk and loss severity of specific debenture are lower by:– Parent guaranteed, subsidiary guaranteed

– Secured by assets or flows of income or reserve account

16

Rating Enhancement

• TRIS Rating generally applies bottomed up approach for issuer rating in a group.

• Rating will be enhanced (notched up) from standalone rating. standalone rating.

17

Rating Factors for Government-Related Entities (GRE)

• Standalone rating � similar factors to other FI or Non-FI corporate

• Degree of government supports � extraordinary supports

• Extraordinary supports: • Extraordinary supports: – Linkages between government and the GRE (the level of

government intervention and proportion of government shares, the existing of guaranteed debts, reputation risks, share names etc.)

– Strategic important of the GRE � ability to use other private company to achieve similar mission, roles of the GRE to deliver government policies and actions

18

Rating Factors for Government-Related Entities (GRE)(continued)

• Issuer rating = Standalone rating+ extraordinary support from government

• Issuer rating of GRE ranges between “standalone rating” and “AAA”rating” and “AAA”

• Ratings of GRE could be very high even its financial performance is miserable if TRIS Rating believes that:– Government views this GRE’s function is very important to

government

– The GRE was considered as state-owned enterprise and its charter indicates that government will responsible to repay debts

19

Rating Notched Down or Capped

• In general, issuer rating of a subsidiary in a group is not higher than (capped by) the group rating.

• Rating of a specific issue could be notched down • Rating of a specific issue could be notched down if :

– It is a junior debt (when portion of senior debts >20% of total assets)

– Issued by structural subordinated entity (eg. pure holding company in a group)

20

How to rate related companies(Group Rating) ?(Group Rating) ?

21

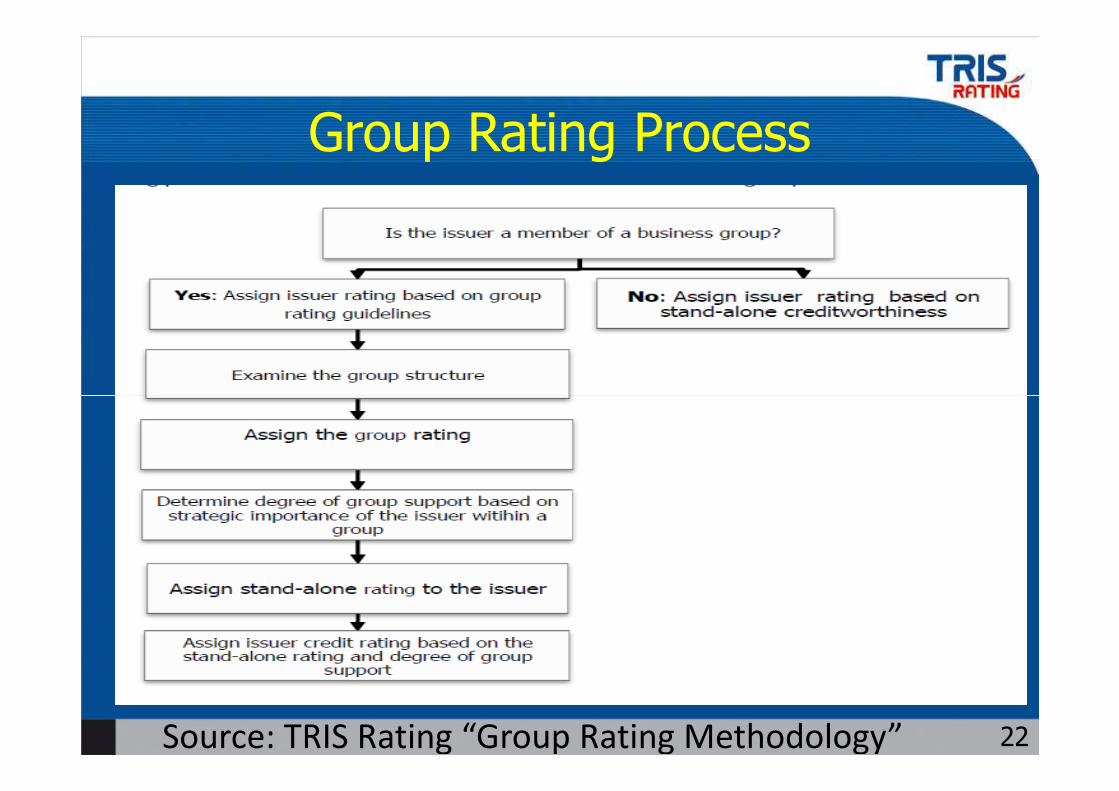

Group Rating Process

Source: TRIS Rating “Group Rating Methodology” 22

Group Rating

• Implicitly assign group rating

• Group of companies comprised those are under controlled of a single group of shareholders or management teams

• A company may be considered as part of a group if • A company may be considered as part of a group if TRIS Rating believes that the company’s business direction and policies are determined by the group.

• Generally a subsidiary is consolidated in a group financial performance and the rating will be capped by the group rating

23

• Issuer rating of core company will be equal to the group (consolidated) rating.

• Issuer rating of subsidiary could be enhanced or capped by the group rating, unless– we are convinced that any financial difficulty borne by the

Issuer Rating of Company in A Group

– we are convinced that any financial difficulty borne by the group will have a limited impact on the issuer’s credit quality

– special purpose vehicle company,

– a project finance company,

– other forms of business that insulate the issuer from its parent company and other group members

– Or when the proportion of minority shareholders is large enough to counter decisions of the major shareholders

24

When Affiliates Are Included in The Group

• A company may be considered as part of a group even when parent company holds less than 50% of its shares.

• Two or more companies may have relationship that enables one company to control, support, or interfere the other firm: the other firm: – common shareholders for both firms, – similar brand names, – majority proportion of board seats, and the role of the

designated directors, – overlapping or complementing lines of businesses, and – historical record of interventions or support

25

Issuer Rating of Subsidiary in The Group

Could be either:

1. Capped by the group rating, or

2. Equal to the group rating, or

3. Enhanced by multiple notches but must be lower 3. Enhanced by multiple notches but must be lower

than group rating by 1 notch, or

4. Enhanced by 1-3 notches from standalone rating

but must be lower than the group rating, or

5. No notch up

26

What are rating factors of hybrid capital instruments?capital instruments?

27

CRA’s Point of Views

• The characteristics of hybrid capital instruments of deferrable, subordination make these instruments more flexible than other debt instruments.

• These characteristics also benefit the issuer during the financial stress scenario.

• On the other hand, these increase repayment risks to • On the other hand, these increase repayment risks to the investors.

• Combined this two characteristics, hybrid capital instruments will be notched down by 2 notches.

• Nonetheless, given the limited benefits of hybrid instruments comparing with other common stocks, CRAs generally limit the proportion of maximum hybrid capital instrument in the company’s capital structure.

28

Maximum Equity Content

• Non-FI: Not more than 25% of capital (equity + hybrid equity credit)

29

TRIS Rating’s Guideline for Equity Content of Non-FI

• High � 100% equity

• Intermediate � 50% equity: 50% debt

• Low � 100% debt with subjective • Low � 100% debt with subjective

adjustment

30

Basic Factors for “Intermediate” Equity Content

To have intermediate equity content, hybrid capital instrument must have

1. Long-life � at least 20 years remaining until effective

maturity date

2. Effective maturity date:

1. Original maturity date of the instrument, or

2. When call option + more than 25 bps step up withoutreplacement capital covenant (RCC), or

3. When call option + more than 100 bps step up

3. Call option should not earlier than 5 years after issue date

31

Basic Factors for “High” Equity Content

• Converts to common equity in short time (not longer than 3 years)

• Coupon varies with stock dividend or financial performanceperformance

• Very easy to be mandatorily deferrable (eg. upon breach of financial or rating trigger that are set close to existing level)

32

Why 25 bps and 100 bps ?

• TRIS Rating believes that the step up of hybrid instrument by over 25 bps will create a cost pressure for issuer to exercise the call option.

• So if the call option comes with the step up of 26-100 bps, the RCC is needed, and it should be 26-100 bps, the RCC is needed, and it should be legally binding RCC, otherwise it would be effective maturity.

• When the step up is higher than 100 bps, the cost pressure to issuer will be overwhelm and it will be effective maturity.

33

“Bank” Hybrid Capital Instrument Rating

• Rating criteria follows BOT guidelines for bank hybrid capital Tier 2 characteristics:

– Perpetual

– Subordination

– Loss absorption mechanism– Loss absorption mechanism

– Deferral

• Factors Definition Notch-down from standalone rating

1. Subordination Debt repayment is lower priority than debenture holders but higher than common stock shareholders.

1

2. Loss absorption mechanism

Supplementary loss-absorption at the point of non-viability in terms of write-down or stock conversion

1

3. Deferrable Mandatory or optional deferrable of coupon payments under financial stress.

1

34

Hybrid Ratings By TRIS Rating

Rating as of 28 August 2015

1. Thanachart Bank Plc. Issuer Rating = AA-

Hybrid Tier 2 Capital = A

2. TISCO Bank Plc. Issuer Rating = A2. TISCO Bank Plc. Issuer Rating = A

Hybrid Tier 2 Capital = BBB+

3. LH Bank Plc. Issuer Rating =A-

Hybrid Tier 2 Capital = BBB

Source: TRIS Rating

35

Sovereign Rating

36

Sovereign rating

• Ability and willingness of sovereign government to repay debt to non-sovereign bond holders.

• Not include debts of multilateral institutions such as IMF, World Bank, ADB.

• Rating factors include quantitative and qualitative • Rating factors include quantitative and qualitative factors.

• Nonetheless, among all, the qualitative which include the credit culture of the government , administrative efficiency of officials, political stability are very important rating factors.

37

Crucial Rating Factors of Laos PDR

1. Relatively low commercial external debts comparing with peers. Most external debts are public debts from ADB and G-to-G.

2. Small scale economy and emerging stage of capital market.

3. Political stability but limited data base and updated 3. Political stability but limited data base and updated information.

4. High willingness to comply with international standard with supports and guidance from international organizations.

5. National income linked with commodity prices but increasing portion of income from hydropower sector sold to Thailand.

38

Lao Sovereign Rating = BBB+

• Thailand national scale

• Comparable to other ratings in TRIS Rating portfolios

• Ability and willingness to repay debts of • Ability and willingness to repay debts of Lao government in terms of Thai-Baht.

39

Ratings Private Companies OverseasOverseas

40

Rating Factors Private Companies Overseas

• Similar to other issuer rating.

• Additional consideration:

– Sovereign risks of country of domicile

– Transferability and convertibility risks – Transferability and convertibility risks

– To mitigate transferability and convertibility risks �

reserve account overseas in USD or other hard currencies.

• The rating will be assigned in Thai Baht, TRIS Rating scale (Thai scale).

41

Could issuer or issue rating of non-sovereign companies higher than sovereign rating?

• Generally, issuer rating of a non-sovereign company could not higher than sovereign rating of the country of its domicile.

• Sovereign government always have ability to determine tax rates, impose regulatory requirement that will enable tax rates, impose regulatory requirement that will enable to increase its ability to repay public debts in local currency.

• Some private companies may have higher issuer rating than government if – its overall local currency rating is higher than the government – the majority of its revenues generated from overseas – revenues mostly are in term of foreign currency.

42

Could issuer or issue rating of non-sovereign companies higher than Sovereign Rating?

• Continued…

• The issue rating of debentures issued by a private company could be higher than sovereign rating if:

The standalone rating of the company is higher than – The standalone rating of the company is higher than sovereign rating

– The debentures are backed by revenues generated in other countries which will be put into reserve account overseas

43

THANK YOU

44

![Bis[tris(1,10-phenanthroline)nickel(II)] tris ... · Bis[tris(1,10-phenanthroline)nickel(II)] tris[dicyanidoargentate(I)] nitrate 4.2-hydrate Muhammad Monim-ul-Mehboob,a Muhammad](https://static.fdocuments.us/doc/165x107/5f74462041fcef38863090d7/bistris110-phenanthrolinenickelii-tris-bistris110-phenanthrolinenickelii.jpg)