By CA Atul Gupta. Type of Refunds In case of Export of Services In case of Export of Goods For SEZ...

55

Export Refund Claim & By CA Atul Gupta

-

Upload

owen-hamilton -

Category

Documents

-

view

217 -

download

3

Transcript of By CA Atul Gupta. Type of Refunds In case of Export of Services In case of Export of Goods For SEZ...

Export

Refund Claim

&

By CA Atul Gupta

By CA Jai Prakash Aggarwal

Type of Refunds

• In case of Export of Services• In case of Export of Goods• For SEZ Units/developers• Refund under Rule 5B of CENVAT Credit Rules• Refund of excess/wrong Service Tax Paid.

By CA Atul Gupta

Topic To Be DiscussedWhat is Export of Service?

Who can File Refund Claim?

Frequency of Refund Claim.

Quantum of Refund Claim.

Time Limit for Filing Refund Claim

Where to be Filed?

Major Diff b/w Old Provisions and New Provisions.

Procedure for Filing Refund Claim.

Essential Documents

By CA Atul Gupta

Export of Service

Provider of Service is located in Taxable Territory;

Recipient of Service is located outside India;

Service should not be covered under Negative List;

Place of Provision of Service is outside India;

Payment for such service has been received by the provider of service in convertible foreign exchange.

By CA Atul Gupta

A service provider;

Who provides an output service which is Exported;

Without payment of service tax;

Subject to safeguard, conditions & limitations.

Who can File Refund Claim

By CA Atul Gupta

Frequency of Refund Claim

As per Notification No 27/2012 C.E. (NT) dated 18.06.2012 refund claim shall be filed quarterly;

Quarter means a period of three consecutive month starting from 1st April of every year & onwards;

By CA Atul Gupta

As per Rule-5 of CENVAT Credit Rules, 2004 read with Notification No 27/2012 C.E. (NT) dated 18.06.2012 the amount of refund claim may be calculated as under:

Refund Amount = Export Turnover of Services*Net Cenvat CreditTotal Turnover

Net Cenvat Credit = Total CENVAT credit availed on input services by the output service provider during the relevant period;

Export Turnover of Services = Payment received during the relevant period for export of services + export services whose provision has been completed for which payment had been received in advance in any period prior to the relevant period – advance received for export services for which the provision of services has not been completed during the relevant period;

Total Turnover = Total Value of Export Turnover of services as determined above and the value of all other services, during the relevant period

Quantum of Refund Claim

By CA Atul Gupta

As per NN 27/2012 – CE (NT) a refund claim shall be filed:

- Within one year;- From relevant date;- As provided in Section – 11B of Central

Excise Act, 1944;

Relevant Date shall be date of export of service.

Time Limit for Filing Refund Claim

By CA Atul Gupta

As per Rule – 5 read with NN 27/2012 – CE (NT) a refund claim shall be filed:

- With AC/DC of Service Tax;- having jurisdiction over registered

premises of provider of service from which output services are exported is situated.

Where to be Filed

Major Difference b/w Old Provisions and New Provisions

S. No. Old Provisions New Provisions

1. Rule-5 of CCR, 2004 read with Notification No 05/2006 C.E. (NT) dated 14.03.2006 shall be applicable

Rule-5 of CCR, 2004 read with Notification No 27/2012 C.E. (NT) dated 18.06.2012 shall be applicable

2. Refund Amount = ET/TT*Total Credit Taken

Refund Amount = (ET of goods + ET of Services)/Total Turnover*Net CENVAT Credit

3. Value of export of service shall be taken on accrual basis.

Value of export of service shall be taken on receipt basis.

4. Certificate in Annexure-A required to be signed by auditor (Statutory or Income Tax Auditor)

Certificate in Annexure A-I should be signed by auditor (Statutory or any other)

5. Above Certificate is required only if refund claim is more than Rs. 5L

Above Certificate Required with all claims irrespective of amount.

Diff b/w Old Provisions and New Provisions

By CA Atul Gupta

S. No. Old Provisions New Provisions

6. Not more than 1 refund claim should be filed for each quarter except in two cases where refund claim can be filed for each calendar Month.

Shall not submit more than one refund claim in every quarter except in a case where two claims can be filed.

7. Refund claim shall be least of the following: Calculated as per Notification No 05/2006 C.E. (NT). Balance in CENVAT Credit Account lying unutilized.

Refund claim shall be least of the followings: Calculated as per Notification No 27/2012 C.E. (NT) Balance in CENVAT Credit Account as on last date of the period for which refund claim is being filed. Balance in CENVAT Credit Account as on date when refund claim is being filed.

Diff b/w Old Provisions and New Provisions

By CA Atul Gupta

By CA Atul Gupta

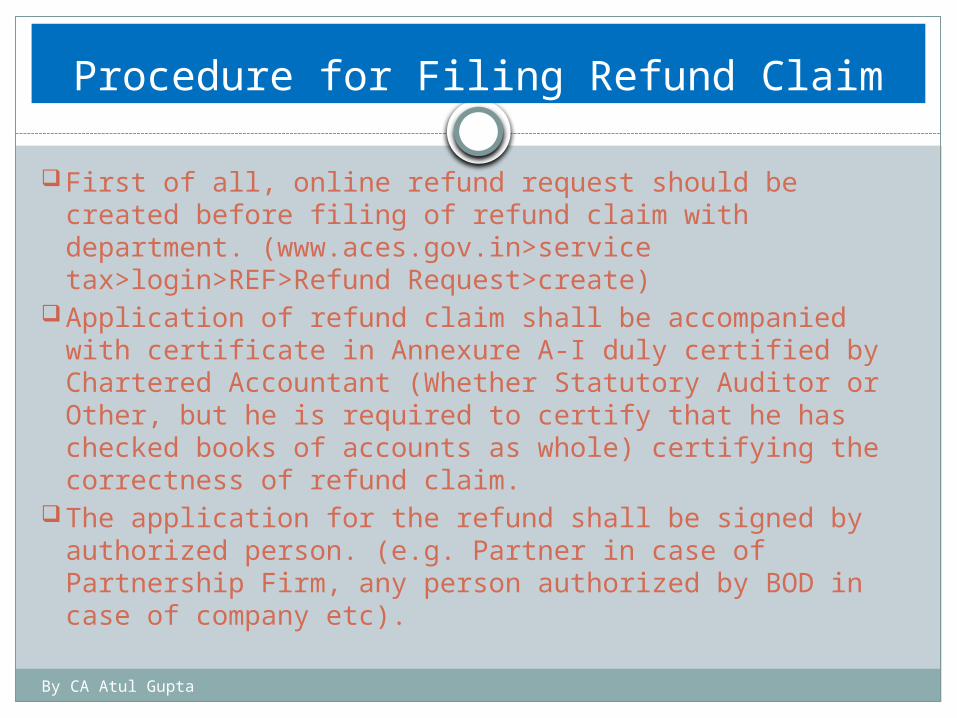

First of all, online refund request should be created before filing of refund claim with department. (www.aces.gov.in>service tax>login>REF>Refund Request>create)

Application of refund claim shall be accompanied with certificate in Annexure A-I duly certified by Chartered Accountant (Whether Statutory Auditor or Other, but he is required to certify that he has checked books of accounts as whole) certifying the correctness of refund claim.

The application for the refund shall be signed by authorized person. (e.g. Partner in case of Partnership Firm, any person authorized by BOD in case of company etc).

Procedure for Filing Refund Claim

By CA Atul Gupta

Following documents are required to be attached along with refund claim application:

Acknowledgment of Online Refund request; Annexure A-I (Certificate from Auditor); Copy of Export Invoices; Copy of agreement entered into with Service Receiver for

Export of Service; Copy of Input Invoices; Bank Statement of relevant period; Justification of availment of input service; Challan(s) of service tax paid; Copy of ST-3 for the relevant period; Copy of ST-2.

Essential Documents

Refund Claim to Exporter of

Goods

By CA Atul Gupta

By CA Atul Gupta

Topic To Be DiscussedNature of Exporter

Who can File Refund Claim?

Relevant Rule and Notification

Frequency of Refund Claim.

Quantum of Refund Claim.

Time Limit for Filing Refund Claim

Where to be Filed?

Procedure for Filing Refund Claim.

Essential Documents

By CA Atul Gupta

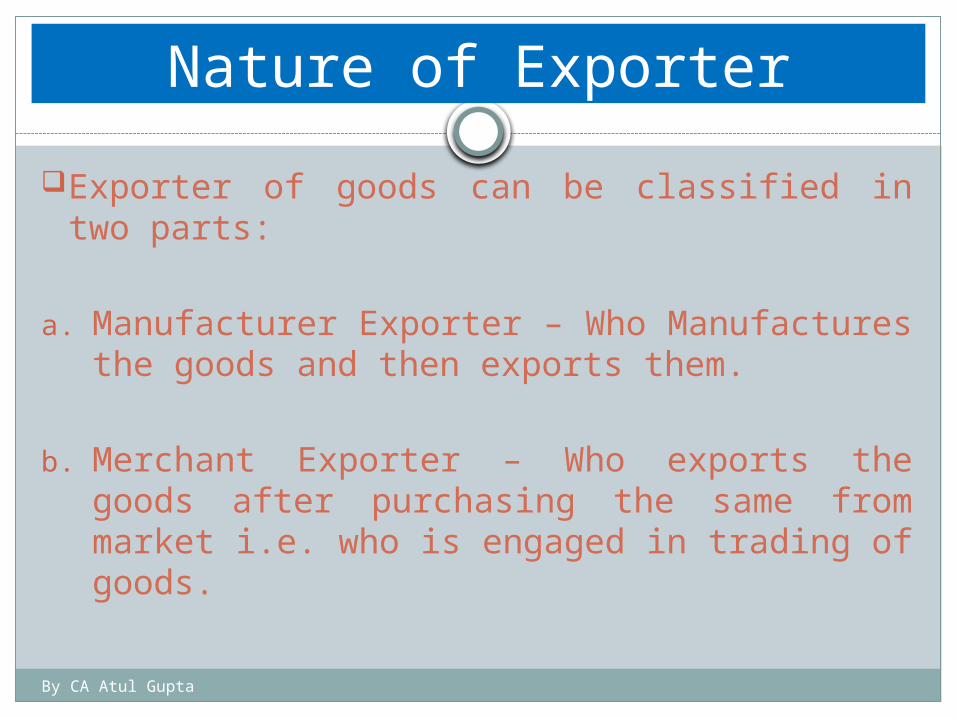

Nature of Exporter

Exporter of goods can be classified in two parts:

a. Manufacturer Exporter – Who Manufactures the goods and then exports them.

b. Merchant Exporter – Who exports the goods after purchasing the same from market i.e. who is engaged in trading of goods.

By CA Atul Gupta

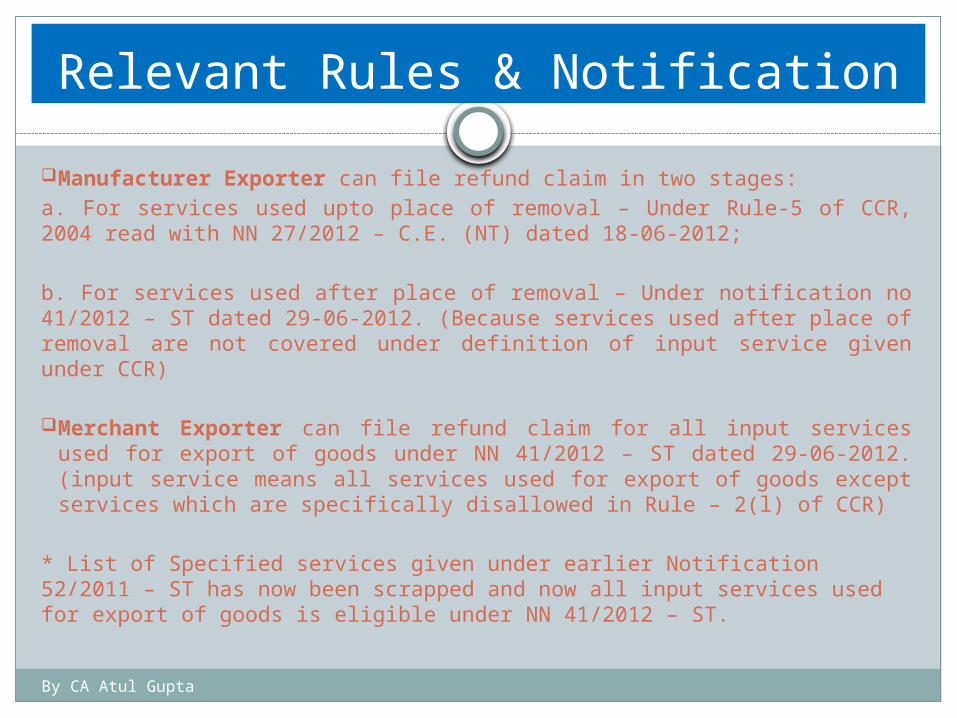

Manufacturer Exporter can file refund claim in two stages:a. For services used upto place of removal – Under Rule-5 of CCR, 2004 read with NN 27/2012 – C.E. (NT) dated 18-06-2012;

b. For services used after place of removal – Under notification no 41/2012 – ST dated 29-06-2012. (Because services used after place of removal are not covered under definition of input service given under CCR)

Merchant Exporter can file refund claim for all input services used for export of goods under NN 41/2012 – ST dated 29-06-2012. (input service means all services used for export of goods except services which are specifically disallowed in Rule – 2(l) of CCR)

* List of Specified services given under earlier Notification 52/2011 – ST has now been scrapped and now all input services used for export of goods is eligible under NN 41/2012 – ST.

Relevant Rules & Notification

By CA Atul Gupta

Frequency of Refund Claim

Under Rule – 5 of CCR read with NN 27/2012 C.E. (NT) dated 18.06.2012 refund claim shall be filed QUARTERLY; (quarter means Apr to Jun and so on)

Under NN 41/2012 – ST no such period is defined therefore refund claim can be filed either for quarterly/half yearly/yearly. Generally assessee opts for quarterly refund claim.

By CA Atul Gupta

As per Rule-5 of CENVAT Credit Rules, 2004 read with Notification No 27/2012 C.E. (NT) dated 18.06.2012 the amount of refund claim may be calculated as under:

Refund Amount = Export Turnover of Goods*Net Cenvat CreditTotal Turnover

Net Cenvat Credit = Total CENVAT credit availed on inputs and input services by the manufacturer during the relevant period;

Export Turnover of Goods = Value of Final Product and intermediate product cleared during the relevant period and exported without payment of Central Excise Duty under Bond or Letter of Undertaking. (Value as per Excise Return)

Total Turnover = Value of All Excisable goods Cleared during the relevant period including exempted goods, dutiable goods and excisable goods (Value as per Excise Return)

contd..

Quantum of Refund Claim

By CA Atul Gupta

As per Notification No 41/2012, assessee may file refund claim for, an amount of service tax paid, to input vendors.

It means no ratio shall be applied in this case and refund claim shall be allowed of actual amount paid to vendors.

Quantum of Refund Claim

By CA Atul Gupta

As per NN 27/2012 – CE (NT) a refund claim shall be filed:- Within One Year;- From relevant date;- As provided in Section – 11B of Central Excise Act, 1944;

Relevant Date shall be date of export of service.

As per NN 41/2012 – ST refund claim shall be filed within One Year from the date when custom officer makes an order permitting clearance and loading of goods for exportation (i.e. from Let Export Order Date) .

contd..

Time Limit for Filing Refund Claim

By CA Atul Gupta

The above given date cannot be extended in any circumstances and no authority condones delay in filing of refund claim.

The Apex Court in the case of [ACC Vs. Anam Electrical Mfg. Co. [1997] 90 E.L.T. 260 (SC)] it has been clarified that any appellate court, civil court, high court cannot extend the period of limitation and such a direction will be illegal.

Likewise in the case of [Brite Neon Signs V. Commissioner of Central Excise, New Delhi [2002] 149 E.L.T. 330 (Tribunal Delhi)] It has been observed that Tribunal has no discretion under Section 11B to condone the delay involved in the filing of the refund claim.

Time Limit for Filing Refund Claim

By CA Atul Gupta

In both the cases i.e. under Rule-5 of CCR, 2004 & under NN 41/2012 – ST:

- Refund claim shall be filed;- With AC/DC of Central Excise;- having jurisdiction over registered factory

(Rule-5); or- having jurisdiction over registered factory or

registered office of assessee. (NN 41/2012 – ST)

Where to be Filed?

By CA Atul Gupta

Rule-5 of CCR, 2004:

An online refund request is required to be created before filing of refund claim with department. (www.aces.gov.in > Excise> Login > REF > Refund Request > Create).

Thereafter, signed application along with other documents shall be submitted with department.

A certificate in Annexure A-I, duly signed by the auditor (Statutory or

any other) certifying the correctness of refund claimed in respect of export of service shall be submitted with refund application. (i.e. Under rule-5 of CCR, 2004 CA Certificate is not required)

contd..

Procedure/Conditions for Filing Refund Claim

By CA Atul Gupta

NN 41/2012 - ST:The refund under Notification No 41/2012 – ST shall be claimed

either on the basis of rates specified in the schedule of rates annexed to this notification or on the basis of documents i.e. on actual basis;

Refund claim on actual basis shall not be allowed to be claimed if amount of refund calculated on actual basis is less than twenty percent (20%) of the refund available on the basis of rates specified in the schedule;

No CENVAT credit of service tax paid has been taken under CENVAT Credit Rules, 2004;

Service provider who has provided services to exporter shall not be eligible to claim refund of such service tax;

Payment should be received in convertible foreign currency within one year.

Procedure/Conditions for Filing Refund Claim

By CA Atul Gupta

Following documents are required to be attached along with refund claim application:

Acknowledgement of Filing Online Refund Request;Copy of Export Invoice(s);Copy of Shipping Bills/Bill of Export;Copy of Bank Realization Certificate;Copy of Input Invoices; Justification for Availment of Input Services for

provision of Export of Goods;Bank Statement for Relevant Period; contd..

Essential Documents

By CA Atul Gupta

Agreement with parties for export of Goods;Form ARE-1;Challan(s) for service tax paid;Copy of ER-1 for relevant period;Form RC i.e. Registration Certificate of Excise

Essential Documents

Refund Claim to Units in

SEZ/Developer of SEZ

Topic To Be DiscussedRelevant Notification and Provisions

Ab-Initio Exemption Versus Refund Claim

Frequency of Refund Claim.

Quantum of Refund Claim.

Time Limit for Filing Refund Claim

Where to be Filed?

Essential Documents

By CA Atul Gupta

Relevant Notifications and Provisions

NN 12/2013 – ST dated 01-07-2013

Exemption is available to Unit(s) located in SEZ/Developer of SEZ;

Exemption is available by two different methods:a. Ab-Initio Exemption; &b. Refund Claim.

Exemption shall be available only for specified services;

“Specified Service” means services used for authorized operations and for which SEZ unit or Developer shall get an approval by Approval Committee.

By CA Atul Gupta

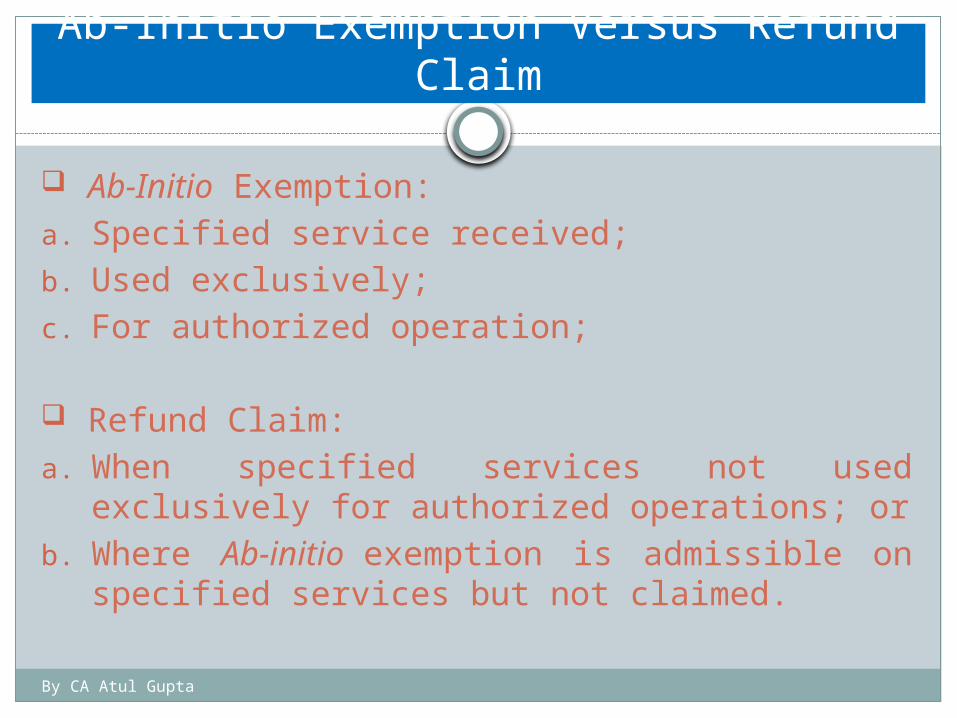

Ab-Initio Exemption:a. Specified service received;b. Used exclusively;c. For authorized operation;

Refund Claim:a. When specified services not used exclusively

for authorized operations; orb. Where Ab-initio exemption is admissible on

specified services but not claimed.

Ab-Initio Exemption Versus Refund Claim

By CA Atul Gupta

Frequency of Refund Claim

NN 12/2013 – ST prescribes that:a. SEZ/Developer of SEZ shall submit;b. only one refund claim;c. For every quarter.d. Quarter means period of 3 consecutive

months with 1st quarter beginning from 1st April of every year & so on.

By CA Atul Gupta

As per NN 12/2013 – ST read with Rule-7 of CENVAT Credit Rules, 2004, refund claim shall be calculated as follows:

Turnover of SEZ = Turnover of Authorized Operations during relevant period;

Total Turnover of All Units = Turnover of SEZ/Developer of Authorized & Unauthorized Operations and DTA Unit(s);

Service tax paid on Services means services which are used commonly for authorized operations in SEZ and operation in (DTA);

Quantum of Refund Claim

Refund Claim

=

Turnover of SEZ Unit/DeveloperTotal Turnover of All Units/Developer

* service tax paid on services used for SEZ and DTA commonly

+ Service tax paid on services used exclusively

By CA Atul Gupta

Time Limit for Filing Refund Claim

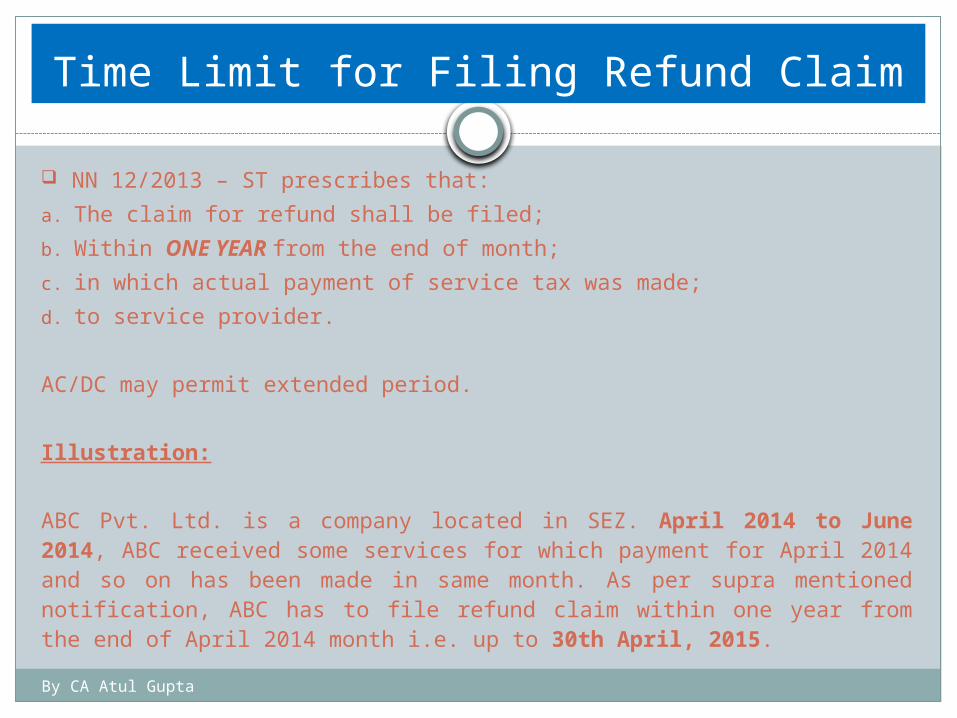

NN 12/2013 – ST prescribes that:a. The claim for refund shall be filed;b. Within ONE YEAR from the end of month;c. in which actual payment of service tax was made;d. to service provider.

AC/DC may permit extended period.

Illustration:

ABC Pvt. Ltd. is a company located in SEZ. April 2014 to June 2014, ABC received some services for which payment for April 2014 and so on has been made in same month. As per supra mentioned notification, ABC has to file refund claim within one year from the end of April 2014 month i.e. up to 30th April, 2015.

By CA Atul Gupta

A unit of SEZ or Developer of SEZ shall:

a. File the claim of refund;

b. With jurisdictional AC/DC of Central Excise ;

c. In Form A-4.

Where to be Filed?

By CA Atul Gupta

Following documents are required to be attached along with refund claim application:

Form A-4 i.e. Application for Refund claim;Acknowledgement of Online Refund Filed;Copy of output invoices;Copy of relevant Input Invoices (on which refund is

being claimed);Registration Certificate i.e. ST-2;Service Tax Return i.e. ST-3; &Bank Statement for the relevant period.

Essential Documents

Refund Claim under Rule 5B of CENVAT Credit

Rules, 2004

Topic To Be DiscussedRelevant Rule and Notification

Specified Services

Frequency of Refund Claim.

Quantum of Refund Claim.

Time Limit for Filing Refund Claim

Where to be Filed?

Essential Documents

By CA Atul Gupta

Relevant Rule and Notification

Refund Claim under Rule – 5B of CENVAT Credit Rules, 2004 is allowed to;

a. A service provider;b. Providing services notified under Section – 68(2);c. Unable to utilized CENVAT Credit;d. For payment of service tax on specified output

services

Introduced w.e.f. 1st July, 2012;Due to partial reverse charge mechanism;Safeguard, conditions & limitations given under NN

12/2014 – C.E. (NT) dated 03-03-2014.

By CA Atul Gupta

Specified Services

NN 12/2014 – C.E. (NT) provides that refund shall be claimed for providing following output services:

a. Renting of Motor Vehicle (Non-Abated);

b. Manpower Supply Services;

c. Security Services;

d. Works Contract Service.

By Individual/HUF/Partnership Firm to Body Corporate.

By CA Atul Gupta

Frequency of Refund Claim

NN 12/2014 – C.E. (NT) prescribes that:a. Refund shall be claimed;b. for a period of Half Year;c. of CENVAT Credit availed during that half

year;d. for providing output services (4 services).e. Half year means period of six consecutive

months with 1st half year beginning from 1st April of every year and 2nd half year from the 1st day of October every year.

By CA Atul Gupta

As per NN 12/2014 – C.E. (NT) refund claim shall be computed as follows:

Where,

contd..

Quantum of Refund Claim

Unutilized CENVAT credit taken on inputs and inputs services during the half year for providing partial reverse charge services

= (A)- (B)

A =

CENVAT credit taken on inputs and input services during the half year

(*)

Turnover of output service under Partial Reverse Charge during the Half YearTotal Turnover of Goods and Services during Half Year

B =Service Tax paid by the service provider for such partial reverse charge services during the half year

By CA Atul Gupta

Quantum of Refund Claim

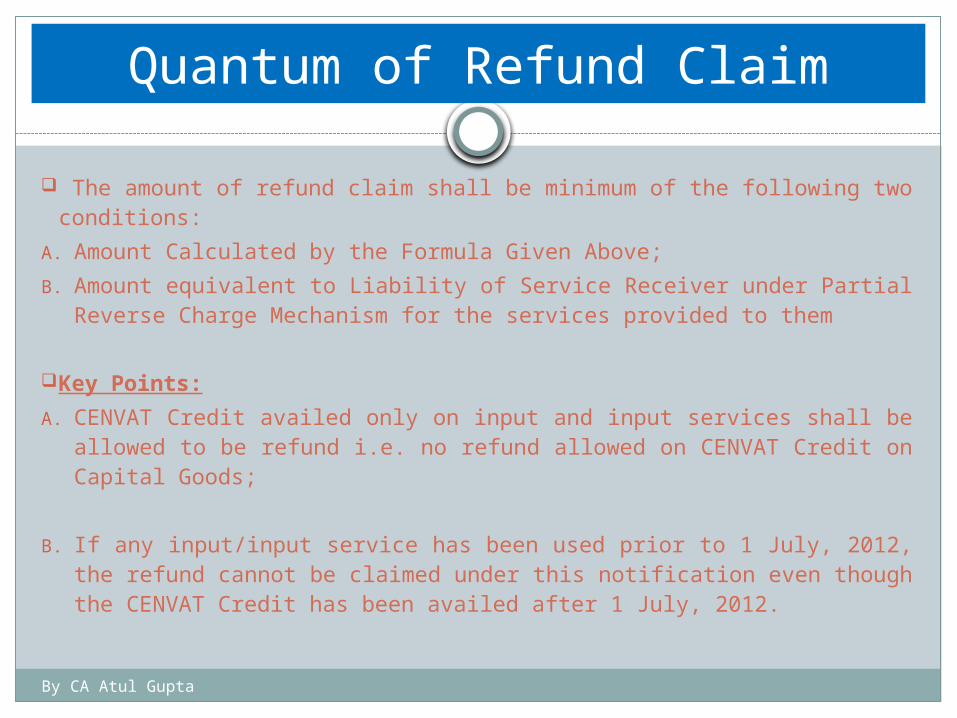

The amount of refund claim shall be minimum of the following two conditions:

A. Amount Calculated by the Formula Given Above;B. Amount equivalent to Liability of Service Receiver under Partial

Reverse Charge Mechanism for the services provided to them

Key Points:A. CENVAT Credit availed only on input and input services shall

be allowed to be refund i.e. no refund allowed on CENVAT Credit on Capital Goods;

B. If any input/input service has been used prior to 1 July, 2012, the refund cannot be claimed under this notification even though the CENVAT Credit has been availed after 1 July, 2012.

By CA Atul Gupta

Time Limit for Filing Refund Claim

Application of Refund shall be filed;In Form-A;Before the expiry of One Year from the due date

of filing of service tax return;If time limit to file return has been extended by

CG then one year shall be counted from such extended date.

Illustration:If due date of filing STR for the period Apr’14 to Sep’14 is 25th October, 2014 then last date for filing refund claim shall be 24th October, 2014.

By CA Atul Gupta

A Service provider providing specified services:

a. Shall file the claim of refund;

b. With jurisdictional AC/DC of Central Excise ;

c. In Form A.

Where to be Filed?

By CA Atul Gupta

Following Documents are required to be submitted with refund claim application:

Acknowledgment of Online Refund Request; Attested Copy of Output Invoices; CENVAT Credit Register for Relevant Period; Invoices of Inputs/Inputs Services Received; Copy of challan (if any) for payment of tax; Service tax Return i.e. ST-3; Registration Certificate i.e. ST-2.

Essential Documents

Refund of Excess/Wrong

Service Tax Paid

Topic To Be DiscussedReasons for Excess/Wrong Payment

Legal Provisions

Unjust Enrichment

Time Limit for Filing the Refund Claim

Where to be Filed?

Essential Documents Required for Refund

By CA Atul Gupta

Reasons for Excess/Wrong Payment of Service tax

Clerical Error;Dual Payment of Service tax due to internet

baking error/server error;Omitted to avail the benefit exemption;Due to non availability of data;Incorrect Interpretation of provisions.

By CA Atul Gupta

Refund can be claimed in two ways:a) Self-Adjustment of Service Tax: In accordance with Rule-6(4A) of Service Tax Rules, 1994 which is as follows:

Adjustment can be made:- If assessee has paid any amount in excess;- From service tax liability for a month or quarter;- Assessee may adjust such excess amount;- Against his liability for succeeding month or quarter.

contd..

Legal Provisions

By CA Atul Gupta

b) Refund of Tax - In accordance with Section 11B of the Central Excise Act, 1944 (By Virtue of S-83 of Finance Act, 1994 applicable in service tax)

Refund may be claimed of:- Any duty of Excise or interest paid thereon;- if the incidence of such duty and interest had

not been passed on by assessee to any other person”(Unjust Enrichment)

Legal Provisions

By CA Atul Gupta

Meaning: A Situation when a person undeservedly gets enriched.

Introduction: Term has been introduces by Section 11B of Central Excise Act, 1944.

The burden of proof that incidence of such duty and interest, if any, paid on such duty had not been passed on by him to any other person is on the claimant {Landmark Judgment of Maftalal Industries V. U.O.I (S.C)}Applicability of Unjust Enrichment:

Unjust Enrichment

S. No.

SituationCheck Unjust Enrichment

1. Refund Claim of Tax paid Wrongly – Omitted to Avail Exemption

Yes

2. Refund Claim of Tax paid Wrongly - Twice Payment done No3. Refund to Exporter of Goods or Exporter of Service No4. Refund of CENVAT Credit No

By CA Atul Gupta

As provided in Section – 11B of Central Excise Act, 1944 Refund shall be filed-“ Before the expiry of one year from the Relevant Date”

As per Explanation 2 of Section 11B of Central excise Act, 1944- Relevant Date shall be:

Date of payment of tax/duty

Time Limit for Filing Refund Claim

By CA Atul Gupta

Where

As per Section 11B (1) of Central Excise Act, 1944:

The assessee shall submit an application in Form R and other relevant documents to AC/DC of Central Excise in whose jurisdiction the registered premises of the assessee situated.

Where to Filed?

By CA Atul Gupta

Following is the list of documents required to be attached along with refund claim application:

Form – R; Copy of Challan(s) for payment of tax; Copy of Input Invoice(s) [if payment of service tax made by

utilizing CENVAT]; Excise Return/Service Tax Return for Relevant Period; Excise Registration Certificate/Service Tax Registration

Certificate.

Essential Documents