BVRLA Guide to FCA Compliance · BVRLA Guide to FCA Compliance. 1 The purpose of this document is...

21

BVRLA Guide to FCA Compliance

Transcript of BVRLA Guide to FCA Compliance · BVRLA Guide to FCA Compliance. 1 The purpose of this document is...

BVRLA Guide to FCA Compliance

1 The purpose of this document is to provide general guidance and information only. Although every effort is made to ensure that the content is accurate, the BVRLA cannot accept any liability whatsoever for any inaccuracy contained within it, nor for any damage or loss, direct or indirect, which may be suffered as a result of any reliance placed upon the information provided, whether arising in contract, tort or in any other way. Advice should always be obtained from your own professional advisers before committing to a specific action.

May 2014

Table of Contents Acknowledgments ............................................................................................................................................... 2

What is happening? ............................................................................................................................................. 2

Options for compliance ............................................................................................................................... 2

What does regulation by the FCA look like? ....................................................................................................... 4

Higher risk activities and lower risk activities ............................................................................................. 4

What do I need to do now? ................................................................................................................................. 6

What other steps could I be taking? ................................................................................................................... 7

Updating stationery ..................................................................................................................................... 7

The Principles .............................................................................................................................................. 7

Treating Customers Fairly ............................................................................................................................ 8

Incentives ..................................................................................................................................................... 9

Appoint approved persons .......................................................................................................................... 9

Business plans ............................................................................................................................................ 10

Complaint handling ................................................................................................................................... 11

Process and procedures ............................................................................................................................ 11

Reporting ................................................................................................................................................... 12

Training ...................................................................................................................................................... 13

Supervision ........................................................................................................................................................ 13

Supervision in the interim permission regime .......................................................................................... 13

Supervision once full/limited authorisation is in place ............................................................................. 13

Enforcement ...................................................................................................................................................... 15

Further information ........................................................................................................................................... 16

Annex A .............................................................................................................................................................. 18

Annex B .............................................................................................................................................................. 19

2 The purpose of this document is to provide general guidance and information only. Although every effort is made to ensure that the content is accurate, the BVRLA cannot accept any liability whatsoever for any inaccuracy contained within it, nor for any damage or loss, direct or indirect, which may be suffered as a result of any reliance placed upon the information provided, whether arising in contract, tort or in any other way. Advice should always be obtained from your own professional advisers before committing to a specific action.

Acknowledgments The BVRLA is grateful for the input of Compliancy Services and Regulatory Finance Solutions Ltd into the production of this guide.

What is happening? The Financial Conduct Authority took over regulation of consumer credit activities from the Office of Fair Trading on 1 April 2014. The FCA is one of the UK’s main financial regulators, it regulates more than 26,000 financial companies and the people who work in them – from high street banks, through to the small local financial adviser. The FCA will aim to make markets work well so consumers get a fair deal. There are three broad outcomes it wants to achieve:

♠ consumers get financial services and products that meet their needs, from firms they can trust;

♠ markets and financial systems are sound, stable and resilient, with transparent pricing information; and

♠ firms compete effectively, with the interests of their customers and the integrity of the market at the heart of how they run their businesses.

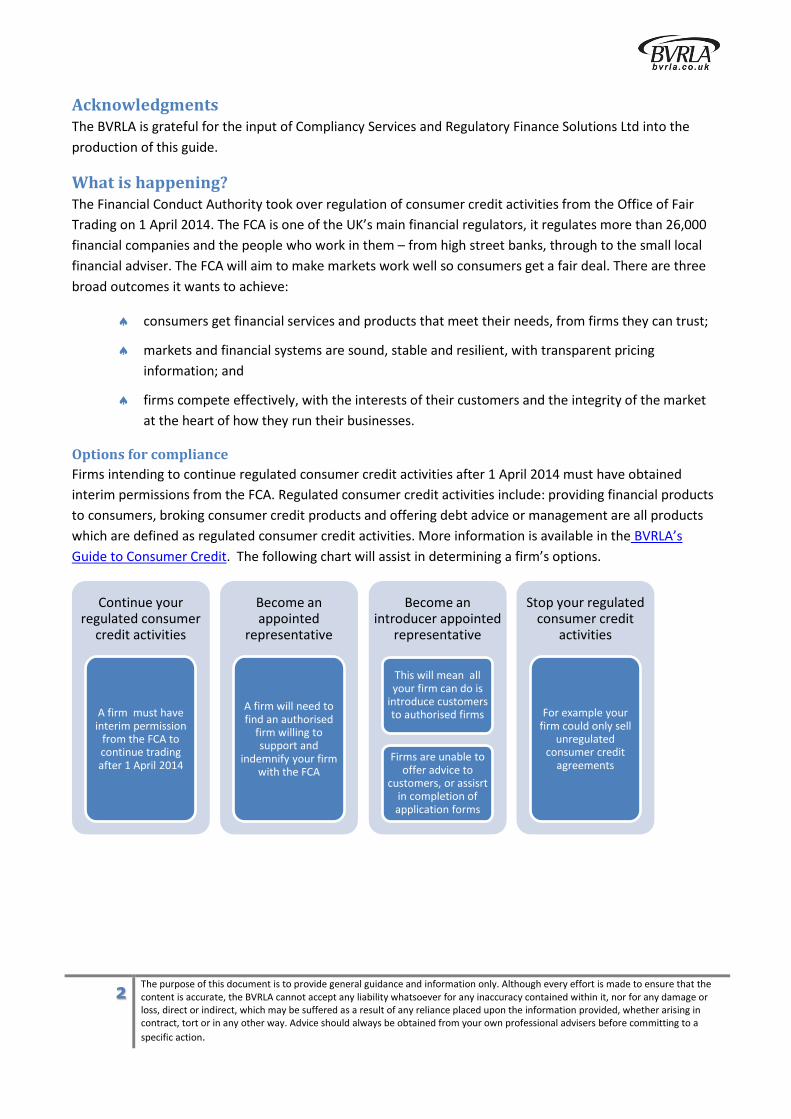

Options for compliance Firms intending to continue regulated consumer credit activities after 1 April 2014 must have obtained interim permissions from the FCA. Regulated consumer credit activities include: providing financial products to consumers, broking consumer credit products and offering debt advice or management are all products which are defined as regulated consumer credit activities. More information is available in the BVRLA’s Guide to Consumer Credit. The following chart will assist in determining a firm’s options.

Continue your regulated consumer

credit activities

A firm must have interim permission

from the FCA to continue trading after 1 April 2014

Become an appointed

representative

A firm will need to find an authorised

firm willing to support and

indemnify your firm with the FCA

Stop your regulated consumer credit

activities

For example your firm could only sell

unregulated consumer credit

agreements

Become an introducer appointed

representative

This will mean all your firm can do is

introduce customers to authorised firms

Firms are unable to offer advice to

customers, or assisrt in completion of application forms

3 The purpose of this document is to provide general guidance and information only. Although every effort is made to ensure that the content is accurate, the BVRLA cannot accept any liability whatsoever for any inaccuracy contained within it, nor for any damage or loss, direct or indirect, which may be suffered as a result of any reliance placed upon the information provided, whether arising in contract, tort or in any other way. Advice should always be obtained from your own professional advisers before committing to a specific action.

Appointed representatives Becoming an appointed representative (AR) may be of particular interest to small firms carrying on higher-risk credit activities if they do not want to pay the full cost of authorisation or do not have the infrastructure or internal systems and controls to become authorised firms themselves. An AR can conduct any regulated activity for which its principal has permission. An AR is not directly regulated by the FCA, but responsible to the Principal for adhering to its delegated responsibilities.

Being a principal may appeal to firms that rely on intermediaries to find, or deal with, customers on their behalf. For example, a leasing company might want to be a principal to leasing brokers, who would act as their ARs. A principal would need to have a formal agreement in place with all its ARs which should clearly document instructions to its ARs, including any limitations as to what an AR can do in terms of regulated activities. The principal will be required to monitor the quality of service being provided by an AR that is acting as its intermediary. Becoming a principal is a high risk activity. A firm would need to convince the FCA that it had the appropriate resources and skills to become a principal.

A firm who wants to operate with ARs cannot do so until they are fully authorised by the FCA. The FCA will allow firms who want to operate with ARs to apply for full authorisation first for 3 months from 1 June 2014. Further detail is available in the Application periods – Direction to firms.

Introducer appointed representative An ‘introducer appointed representative’ (IAR) is a type of appointed representative whose activity is limited to introducing customers to its principal and distributing non-real time financial promotions. If an IAR’s activities go beyond these limitations and it, for example, provides advice to customers, it cannot be an IAR. Because the activities that an IAR can carry out are limited, it is subject to fewer rules than an AR and is not required to have any approved persons.

Regulating a firm’s AR and IARs Firms that are authorised to do so can appoint as many ARs or IARs as it sees fit, however, the firm would need to be able to demonstrate to the FCA that they have the appropriate resource to monitor the ARs and IARs. Any firm that appoints an AR (whether introducer or not) becomes fully responsible for oversight of that AR for the regulated business they are appointing them to carry out and to ensure the IAR is not exceeding their brief. ARs and IARs have a responsibility to ensure they do not use their status to facilitate unauthorised business that exceeds what they have been appointed for.

Under s.39(3)of the Financial Services and Market Act, the principal firm is responsible for anything done (or omitted) by the appointed representative in carrying on the business for which the principal has accepted responsibility “to the same extent as if he has expressly permitted it”. Thus the principal will be liable to third parties and accountable to the FCA, for the activities of his appointed representative, insofar as this depends on such express permission. Another example is that complaints referred to the Financial Ombudsman Service regarding the credit business of that AR would be the responsibility of the principal firm.

Self-employed agent Some leasing brokers have sales forces who are self-employed. Leasing brokers will need to determine whether the person is carrying on their own business or if they are trading as a self-employed agent. If they

4 The purpose of this document is to provide general guidance and information only. Although every effort is made to ensure that the content is accurate, the BVRLA cannot accept any liability whatsoever for any inaccuracy contained within it, nor for any damage or loss, direct or indirect, which may be suffered as a result of any reliance placed upon the information provided, whether arising in contract, tort or in any other way. Advice should always be obtained from your own professional advisers before committing to a specific action.

are carrying on their own business they will require authorisation from the FCA, or need to become an AR of a directly authorised principal.

The FCA guidance states that meeting the following criteria is likely to mean that a person is an agent of a principal’s business and does not require authorisation on the grounds that they are carrying on the business of the principal and not his own:

♠ the principal appoints the self-employed agent as their agent ♠ the agent can only work for one principal ♠ the principal has FCA permission for every activity the agent is carrying on for which the principal

would need permission as if it was carrying on the activity itself ♠ there is a contract in place setting out effective measures for the principal to control the agent so

the customer is not harmed if the agent becomes insolvent before the money is passed to the principal

♠ the principal accepts full responsibility for the conduct of its agent when it is acting on its behalf in the course of its business

♠ the agent makes it clear to customers that it is representing a principal and the name of that principal

What does regulation by the FCA look like? The Rulebook Authorisation Approval Supervisions of

persons Enforcement and Redress

The FCA is empowered under the Financial Services and Markets Act to make rules which are binding on firms

A firm that wants to carry on regulated activities must be “authorised or exempt”.

The FCA will approve and scrutinise key individuals who perform specific functions

Firms will be subject to ongoing monitoring and supervision

The FCA will have a new toolbox of tough powers to take action against firms and individuals

Detailed rules will complement high-level conduct requirements and “Principles for Business”

Authorisation will allow more robust scrutiny of firms when they apply for authorisation

Individuals must prove they are “fit and proper” in the FCA’s eyes

Companies will be forced to regularly supply critical information to the FCA

New powers will include unlimited fines and forcing companies to redress consumers

Higher risk activities and lower risk activities Firms carrying out higher-risk activities will be subject to close scrutiny by the FCA. Higher risk activities include:

♠ Consumer credit lending (including personal loans, credit card lending, overdrafts, pawnbroking, hire-purchase, conditional sale, etc)

♠ Credit broking (including introducing consumers to lenders as a main business activity)

5 The purpose of this document is to provide general guidance and information only. Although every effort is made to ensure that the content is accurate, the BVRLA cannot accept any liability whatsoever for any inaccuracy contained within it, nor for any damage or loss, direct or indirect, which may be suffered as a result of any reliance placed upon the information provided, whether arising in contract, tort or in any other way. Advice should always be obtained from your own professional advisers before committing to a specific action.

♠ Debt adjusting, counselling, collection and administration1 ♠ Providing credit information services ♠ Providing credit reference agency services ♠ Peer-to-peer lending

Firms carrying out lower-risk activities will be subject to more limited scrutiny for becoming an authorised firm than higher-risk firms. This reflects the limited scope of activities which firms in this category are permitted to carry out and the more limited nature of the authorisation process and supervisory regime.

Firms with limited permission will:

♠ be subject to mainly reactive supervision, which will primarily respond to intelligence received about existing problems;

♠ report only basic information, for example, revenue or number of transactions; and

♠ have lower authorisation and annual fees.

The following will be classed as lower-risk activities:

1) Broking of vehicle leasing

2) Consumer hire: The FCA see minimal risks to the consumer, given the provisions that will remain in the CCA that protect consumers from getting tied into long-term contracts.

3) Credit broking as a secondary activity: the OFT has not seen significant consumer harm arising from credit broking in these markets.

4) Consumer credit lending: where there are no interest or charges, the risks to consumers are reduced.

Where a business is operating in the main in an activity which is lower risk they can also apply to carry on, as an ancillary activity, debt counselling, debt adjusting and credit information services without requiring full authorisation.

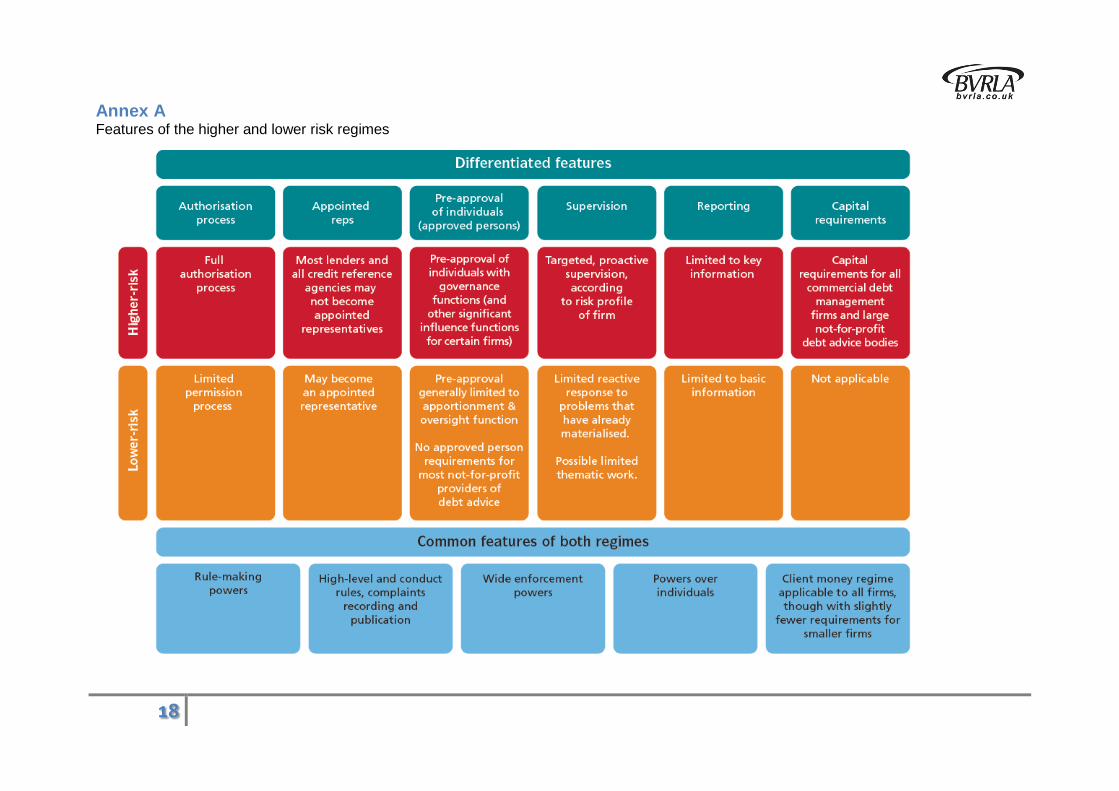

See Annex A for more information on the differences between the higher and lower risk regimes.

See Annex B for more information on the consumer credit licence categories. In broad terms, debt-counselling involves advice about the liquidation of a debt, and debt-adjusting involves negotiating terms for the discharge or liquidation of a debt (i.e. involvement in settlement of an existing credit agreement).

The FCA has confirmed to the BVRLA that activities such as providing advice about early terminating a finance agreement and arranging a new agreement would be classified as debt adjusting. However, where

1 Where a business is operating in the main in an activity which is lower risk they can also apply to carry on, as an ancillary activity, debt counselling, debt adjusting and credit information services without requiring full authorisation.

6 The purpose of this document is to provide general guidance and information only. Although every effort is made to ensure that the content is accurate, the BVRLA cannot accept any liability whatsoever for any inaccuracy contained within it, nor for any damage or loss, direct or indirect, which may be suffered as a result of any reliance placed upon the information provided, whether arising in contract, tort or in any other way. Advice should always be obtained from your own professional advisers before committing to a specific action.

an agreement is changed, due to a mileage adjustment, it is not likely to fall into the definition of debt adjusting.

What do I need to do now? Firms who wish to continue regulated consumer credit activities have to have interim permission in place now for their business. Full or limited authorisation with the FCA will be at some point between 2014 and 2016. The FCA will be writing to firms with interim permission by the end of April 2014 with details of the 3 month window which they will need to apply for full or limited authorisation by. Full details on applying for full or limited authorisation are available here. The key dates are:

♠ Firms who want to operate with appointed representatives will need to apply between 1 June and 1 September 2014

♠ Leasing brokers will need to apply between 1 December 2014 and 1 June 2015, depending on their registered geographic location

♠ Consumer credit firms providing hire purchase and credit sales will need to apply between 1 December 2015 and 1 April 2016, depending on their registered geographic location

♠ Consumer hire businesses will need to apply between 1 June and 1 September 2015

Firms who decide to vary their consumer credit licence will automatically trigger full/limited authorisation.

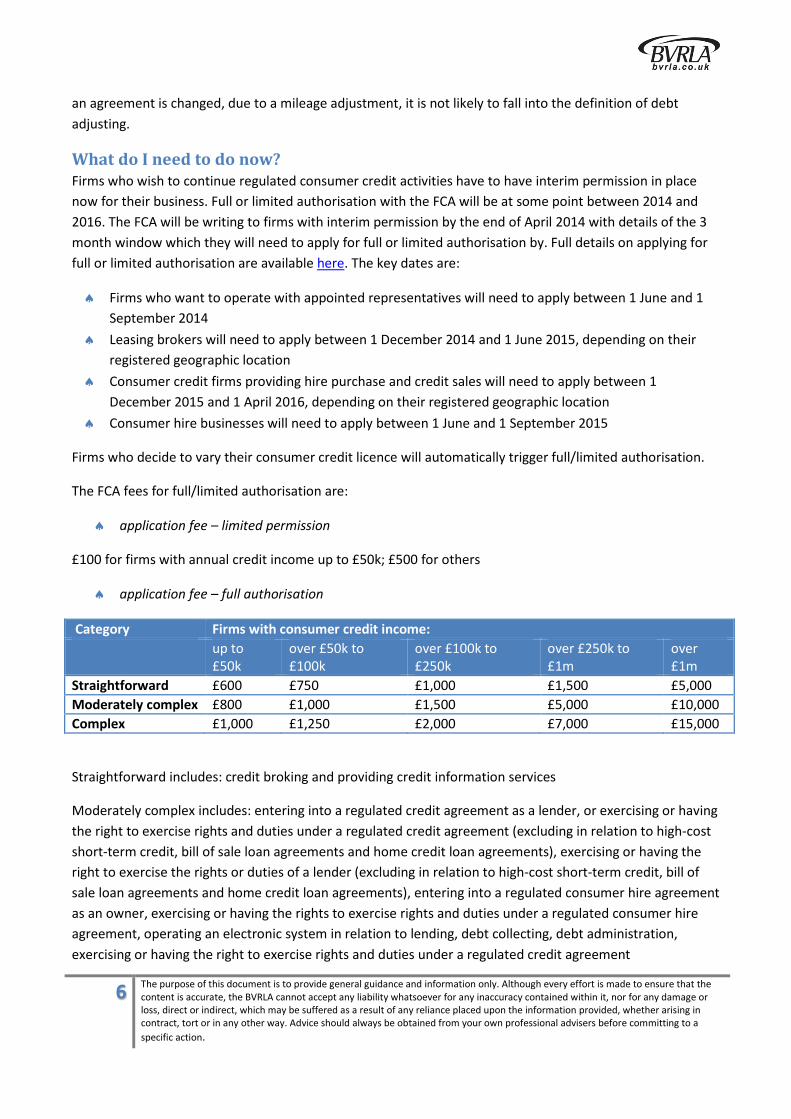

The FCA fees for full/limited authorisation are:

♠ application fee – limited permission

£100 for firms with annual credit income up to £50k; £500 for others

♠ application fee – full authorisation

Category Firms with consumer credit income: up to

£50k over £50k to £100k

over £100k to £250k

over £250k to £1m

over £1m

Straightforward £600 £750 £1,000 £1,500 £5,000 Moderately complex £800 £1,000 £1,500 £5,000 £10,000 Complex £1,000 £1,250 £2,000 £7,000 £15,000

Straightforward includes: credit broking and providing credit information services

Moderately complex includes: entering into a regulated credit agreement as a lender, or exercising or having the right to exercise rights and duties under a regulated credit agreement (excluding in relation to high-cost short-term credit, bill of sale loan agreements and home credit loan agreements), exercising or having the right to exercise the rights or duties of a lender (excluding in relation to high-cost short-term credit, bill of sale loan agreements and home credit loan agreements), entering into a regulated consumer hire agreement as an owner, exercising or having the rights to exercise rights and duties under a regulated consumer hire agreement, operating an electronic system in relation to lending, debt collecting, debt administration, exercising or having the right to exercise rights and duties under a regulated credit agreement

7 The purpose of this document is to provide general guidance and information only. Although every effort is made to ensure that the content is accurate, the BVRLA cannot accept any liability whatsoever for any inaccuracy contained within it, nor for any damage or loss, direct or indirect, which may be suffered as a result of any reliance placed upon the information provided, whether arising in contract, tort or in any other way. Advice should always be obtained from your own professional advisers before committing to a specific action.

Complex includes: entering into a regulated credit agreement as a lender, or exercising or having the right to exercise rights and duties under a regulated credit agreement, in relation to high-cost short-term credit, bill of sale loan agreements and home credit loan agreements, exercising or having the right to exercise the rights or duties of a lender in relation to high-cost short-term credit, bill of sale loan agreements and home credit loan agreements, debt adjusting and debt counselling.

The Government has decided that as a result of the closure of the OFT, there will be rebates given to some consumer credit licence holders. The purpose of the rebate scheme is so that firms do not have to pay for periods of licences after the transfer, since licences will expire on 1 April 2014.The Government has set the main rules of the rebate scheme, which the FCA will administer here.

What other steps could I be taking? Firms will need to be prepared and compliant with the rules of the FCA from 1 April 2014. Firms are expected to have put in place the appropriate compliance planning and monitoring processes by 1 April 2014 and not wait until authorisation.

The BVRLA has produced the following next steps to help members with compliance.

Updating stationery Firms with interim permission are required to ensure all their stationery is updated with the appropriate status disclosure. Firms who have interim permission will need to include on all stationery relating to consumer credit business: "Authorised and regulated by the Financial Conduct Authority"

For firms who are appointed representatives they need to state: “[Name of appointed representative] is an appointed representative of [name of Principal firm] which is [then continue with the required disclosure of the firm]".

FCA Principles The FCA principles set out below are the basis for many of the FCA enforcement actions, they set out the operating guidelines for an FCA authorised firm. Most of the principles are self-explanatory and firms may want to consider each of these when reviewing their business practices.

1. Integrity A firm must conduct its business with integrity.

2. Skill, care and diligence A firm must conduct its business with due skill, care and diligence.

3. Management and control

A firm must take reasonable care to organise and control its affairs responsibly and effectively, with adequate risk management systems.

4. Financial prudence A firm must maintain adequate financial resources.

5. Market conduct A firm must observe proper standards of market conduct.

8 The purpose of this document is to provide general guidance and information only. Although every effort is made to ensure that the content is accurate, the BVRLA cannot accept any liability whatsoever for any inaccuracy contained within it, nor for any damage or loss, direct or indirect, which may be suffered as a result of any reliance placed upon the information provided, whether arising in contract, tort or in any other way. Advice should always be obtained from your own professional advisers before committing to a specific action.

6. Customers' interests A firm must pay due regard to the interests of its customers and treat them fairly.

7. Communications with clients

A firm must pay due regard to the information needs of its clients, and communicate information to them in a way which is clear, fair and not misleading.

8. Conflicts of interest A firm must manage conflicts of interest fairly, both between itself and its customers and between a customer and another client.

9. Customers: relationships of trust

A firm must take reasonable care to ensure the suitability of its advice and discretionary decisions for any customer who is entitled to rely upon its judgment.

10. Clients' assets A firm must arrange adequate protection for clients' assets when it is responsible for them.

11. Relations with regulators

A firm must deal with its regulators in an open and cooperative way, and must disclose to the appropriate regulator appropriately anything relating to the firm of which that regulator would reasonably expect notice.

Treating Customers Fairly The FCA has stated that all firms will need to comply with the FCA high-level principles such as ‘treating customers fairly’ (TCF). The TCF principle aims to raise standards in the way firms carry on their business by introducing changes that will benefit consumers and increase their confidence in the financial services industry.

Specifically TCF aims to: ♠ help customers fully understand the features, benefits, risks and costs of the financial products

they buy ♠ minimise the sale of unsuitable products by encouraging best practice before, during and after a

sale In order to satisfy FCA requirements, firms need to take steps to show how you are implementing TCF throughout the business, this could include a review of:

♠ Staff training/awareness of TCF ♠ Product understanding – the product being the repayment plan ♠ Advice and assistance ♠ Complaint handling ♠ Remuneration/incentives ♠ Risk assessment of TCF non-compliance ♠ Record keeping and management information

9 The purpose of this document is to provide general guidance and information only. Although every effort is made to ensure that the content is accurate, the BVRLA cannot accept any liability whatsoever for any inaccuracy contained within it, nor for any damage or loss, direct or indirect, which may be suffered as a result of any reliance placed upon the information provided, whether arising in contract, tort or in any other way. Advice should always be obtained from your own professional advisers before committing to a specific action.

Incentives The FCA published a review in autumn 2011 of sales incentives as it felt the way sales staff are paid influences how and what they sell to consumers. The FCA does not have a problem with incentive schemes, but they must never be at the customer’s expense and the risks need to be managed properly.

The FCA has published detailed guidance in this area which members may wish to review in the light of FCA authorisation to ensure how they are incentivised to sell products and how staff are incentivised is in line with this guidance. The guidance can be accessed here.

The FCA believes that customers are likely to lose out if:

♠ firms reward staff through material incentive schemes based on sales volumes, fee income or similar measures;

♠ firms’ incentive schemes include features that are harder to manage; ♠ management do not understand how the specific features, complexity and value of their incentive

schemes could increase mis-selling; and/or ♠ poor quality sales or mis-selling are not adequately reflected in the eligibility for, or level of,

incentive payments.

It also expects firms to have in place effective controls and governance to monitor incentive schemes which may include:

♠ robust risk-based business quality monitoring and adequate controls to mitigate the risk of inappropriate behaviour during sales conversations;

♠ market intelligence to identify, and act upon, trends or patterns in individual sales staff activity that could indicate an increased risk of mis-selling as a result of features in the incentive scheme. Using this market intelligence to inform the approach to monitoring sale staff incentive risks;

♠ proper management of sales managers’ conflicts of interest; ♠ effective oversight of incentive schemes by appropriate senior management, including approval of

the incentive schemes; and ♠ an effective risk identification and mitigation process, including regular reviews of incentive schemes

and the effectiveness of controls, taking into account customers’ interests.

Appoint approved persons Approved persons are nominated staff, normally senior managers i.e. directors who hold specified roles within an organisation and who are responsible for the regulated firm’s conduct. The FCA believe that operating with an approved person enhances accountability and helps ensure a firm is complying with the FCA rules.

For a limited permission firm, it is likely that only one approved person will be required to cover the apportionment and oversight functions. The approved person will need to ensure that the significant business responsibilities are clearly and appropriately divided among the directors and senior managers of the firm and that they oversee the implementation and maintenance of appropriate systems and controls.

For all other firms there will need to be approved persons for:

10 The purpose of this document is to provide general guidance and information only. Although every effort is made to ensure that the content is accurate, the BVRLA cannot accept any liability whatsoever for any inaccuracy contained within it, nor for any damage or loss, direct or indirect, which may be suffered as a result of any reliance placed upon the information provided, whether arising in contract, tort or in any other way. Advice should always be obtained from your own professional advisers before committing to a specific action.

♠ Governing functions ♠ Apportionment and oversight function ♠ Compliance oversight function (debt management and credit repair only) ♠ Money laundering reporting officer function ♠ Systems and controls functions ♠ Significant management functions ♠ Protecting clients’ money and assets (debt management firms only)

Business plans Business plans will also be a key area of assessment by the FCA, this is common in other industry sectors that the FCA already regulate. Although the FCA has stated that detailed business plans will not be required to be submitted at the application stage for firms which carry out lower risk activity such as vehicle leasing broking, it does expect all firms to have a basic documented business plan in place. The following advice may assist in putting one together:

What is a business plan? A business plan is a living document containing a firm’s aims and objectives and how the firm will organise its resources to achieve them. It is a tool for the board to use in directing the firm’s activities and monitoring performance against these aims and objectives.

Who is the plan for? The main audience of the plan is a firm’s board and not the FCA or funders. The board needs to understand the document and it would be helpful if it was in a format that encourages reading and reviewing. Business plans do not have to be lengthy and complicated documents.

What sort of information should be included in the business plan? The following questions may help in determining what should be included in a plan:

♠ What does the firm want to achieve? ♠ How is the firm going to do it? ♠ What resources do the firm need to do it – e.g. money, staff, systems, etc.? ♠ What might adversely affect what the firm is trying to achieve? ♠ How can the firm mitigate these factors? ♠ What is the firm’s approach towards compliance?

Who is responsible for writing and keeping the business plan up-to-date and how often should it be done? The board of directors or partners are responsible for the content, review and monitoring of the business plan but it may instruct someone else (the chief executive or general manager if there is one, or some other individual who has the necessary knowledge and skills) to physically write and update the business plan. The content of the plan should be reviewed at least annually but should also be reconsidered in light of any significant changes to the strategic aims or assumptions underpinning it. The board’s responsibilities also includes on- going monitoring of the performance and compliance against the plan.

The GOV.UK website provides templates for writing a business plan and further advice on developing a plan.

11 The purpose of this document is to provide general guidance and information only. Although every effort is made to ensure that the content is accurate, the BVRLA cannot accept any liability whatsoever for any inaccuracy contained within it, nor for any damage or loss, direct or indirect, which may be suffered as a result of any reliance placed upon the information provided, whether arising in contract, tort or in any other way. Advice should always be obtained from your own professional advisers before committing to a specific action.

Complaint handling A complaint is defined by the FCA as any oral or written expression of dissatisfaction, whether justified or not, from, or on behalf of, a person about the provision of, or failure to provide, a financial service or a redress determination which:

a) alleges that the complainant has suffered (or may suffer) financial loss, material distress or material inconvenience; and

b) relates to an activity of that respondent, or of any other respondent with whom that respondent has some connection in marketing or providing financial services or products, which comes under the jurisdiction of the Financial Ombudsman Service (FOS).

Financial services relates to any product that is regulated by the Financial Conduct Authority. It would not include complaints from businesses, unless they were micro-businesses (annual turnover of less than two million euros and fewer than ten employees).

For example if the customer has a complaint about consumer credit or consumer hire arrangements this will be included. But if it is about the quality of the vehicle, performance of the vehicle or the return standards of the vehicle they have leased this will not be included.2

A clear process flow for how complaints are dealt with should be included (see the process and procedures section for more detail)

Process and procedures It may also be necessary to demonstrate to the FCA or self-declare that there are processes and procedures in place for key roles in the business, especially those who handle complaints or have responsibility for selling. For example procedures for the following could be documented and scheduled for regular review:

♠ Assessing a customer’s demands and needs ♠ Assessing financial suitability ♠ Explaining cooling off rights ♠ Complaint handling including use of the BVRLA conciliation service

The BVRLA’s Code of Conduct can assist in terms of standards which can be referred to for these procedures. The standards include, being clear about your complaints procedures, timescales for acknowledging and resolving complaints and maintaining a record of complaints. The table below shows some of the key areas that members will need to consider being able to demonstrate to the FCA that they have robust policies and procedures in place.

Authorisation Conduct of Business

Governance Financial Crime Other

Approved Persons Compliance Manual

Oversight Corporate Governance

Financial Crime Business Continuity

2 This example was provided by the Financial Conduct Authority

12 The purpose of this document is to provide general guidance and information only. Although every effort is made to ensure that the content is accurate, the BVRLA cannot accept any liability whatsoever for any inaccuracy contained within it, nor for any damage or loss, direct or indirect, which may be suffered as a result of any reliance placed upon the information provided, whether arising in contract, tort or in any other way. Advice should always be obtained from your own professional advisers before committing to a specific action.

Compliance Plan: - Principles - Systems and Controls - General Provisions - Authorisations

Complaints Risk - Conduct - Financial Monetary - Internal and Market processes

Anti-Bribery and Corruption

Data Security

Control Functions - Organogram

Advice Process Affordability

Internal Audit Money Laundering

Senior Management Arrangements

Record Keeping

Systems and Controls - Call Monitoring

Threshold Conditions – Financial Capital

Financial Promotions

Due Diligence

Regulatory Business Plan

Treating Customers Fairly

Whistleblowing

Collections and Arrears

Conflicts of interest - Rewards and Incentives

MI and Reporting (internally)

Job Descriptions - Performance Management - Training and Competence

Products and Pricing

MI and Reporting (externally)

Procurement and Outsourcing

Reporting There are reporting requirements for all FCA regulated firms, frequency of reporting will depend on the size of the firm3. They will come into effect from 1 October 2014, but will only commence for firms that are fully authorised from that date onwards.

Firms will submit their data using the FCA ‘GABRIEL’ electronic reporting system - guidance is available to firms that are unfamiliar with the system. Further information is available here.

Firms with limited permission will only need to report: credit related income, total revenue, number of transactions and complaints.

Firms within the higher risk regime will need to provide:

♠ a breakdown of value and amount of loans, arrears and interest rates. ♠ for each activity a firm undertakes, revenue, customer and transaction volume, and an indication of

the main method used to generate income. ♠ key financial figures including capital, assets, liabilities, exposures, income and profit.

3 Firms generating revenue of more than £5million per year from consumer credit business are likely to need to report twice a year.

13 The purpose of this document is to provide general guidance and information only. Although every effort is made to ensure that the content is accurate, the BVRLA cannot accept any liability whatsoever for any inaccuracy contained within it, nor for any damage or loss, direct or indirect, which may be suffered as a result of any reliance placed upon the information provided, whether arising in contract, tort or in any other way. Advice should always be obtained from your own professional advisers before committing to a specific action.

Training The FCA firmly believes in the benefits of staff training and development. Firms will need to ensure they have a training and development plan in place for all staff and that records are kept of what training has been undertaken. This is in line with the conditions of BVRLA membership and the BVRLA Code of Conduct.

Supervision

Supervision in the interim permission regime Whilst a firm is operating in the interim permission regime the FCA’s supervision will be a combination of reactive work and targeted work in areas of greater risk.

Where this work identifies issues that the FCA needs to address, they will take appropriate action where necessary. Where the work identifies harm to consumers the FCA will engage directly with individual firms and communicate with the industry more widely.

The FCA is able to make requests to individual firms for information for a special purpose, but formal regular reporting will not start until after a firm is authorised

During interim permission, a firm’s supervisory contact at the FCA will be the contact centre, whose staff has the expertise to deal with most issues and queries. The contact details are:

♠ UK: 0845 606 9966 (call rates may vary), 0300 500 0597 ♠ From abroad: +44 20 7066 1000 ♠ Email: [email protected]

The contact centre is open 9am to 5pm Monday to Friday. The FCA aim to respond to queries within 12 working days of receiving them.

Supervision once full/limited authorisation is in place The FCA’s supervision work is based around three pillars of activity, which draw on their ongoing analysis of the industry sector a firm is in and the risks within it.

Firms are put into one of four ‘conduct categories’: C1, C2, C3 or C4 based on a firm’s size and customer numbers, and the corresponding level of risk. Firms in category C1 receive the most intensive level of attention from the FCA, firms in C4 the least. Firms are notified of the category they are in once they are authorised. The vast majority of consumer credit firms are likely to be in category C4.

Firms in categories C1 and C2 have a named supervisor at the FCA, but firms in categories C3 and C4 are supervised by flexible teams.

Pillar 1 – Proactive firm supervision The FCA will engage with firms to assess whether you have the interests of your customers and the integrity of the market at the heart of your business. The FCA take a forward-looking approach and use their judgement to address issues that could lead to damage to consumers or markets, with clear personal accountability for your senior management.

14 The purpose of this document is to provide general guidance and information only. Although every effort is made to ensure that the content is accurate, the BVRLA cannot accept any liability whatsoever for any inaccuracy contained within it, nor for any damage or loss, direct or indirect, which may be suffered as a result of any reliance placed upon the information provided, whether arising in contract, tort or in any other way. Advice should always be obtained from your own professional advisers before committing to a specific action.

The FCA provides more detail on the assessment when they authorise a firm. Currently the FCA assesses C4 firms once every four years and other firms more frequently.

The FCA expects reviews for most consumer credit firms could be a phone or face-to-face interview or through its online tool. The format will depend on the risk your firm poses. The content is likely to be the same regardless of which way the review is conducted, and a firm will receive immediate feedback.

If the FCA find that a firm carries significant risks the FCA will do further work, which may include visiting a firm, to better understand the risks and how the firm is dealing with them. The FCA will give detailed feedback about any actions it requires to be undertaken.

Pillar 2 – Event-driven, reactive supervision When the FCA become aware of significant risks to consumers, or when damage has already been done, they will respond swiftly and robustly. The FCA will use information from your firm, data analysis, whistleblowers and consumer complaints to identify risks or problems. Firms have a duty to tell the FCA about any risks or problems that emerge that may have an impact on the FCA’s objectives.

The FCA will ensure a firm mitigate risks, prevents further damage and addresses the root causes of problems. If necessary the FCA can use its formal powers to hold a firm and individuals to account and gain redress for those who have been treated unfairly. Occasionally, they will require firms to appoint a skilled person – an individual or firm with specialist knowledge – to look into a matter and produce a report.

Where an issue is more widespread than one firm the FCA can engage with the industry as a whole to ensure that all firms deal with the risk, consumers are protected and poor behaviour is rectified, with compensation being paid to consumers if necessary.

Contact from the FCA could range from requesting information from firms or visits to their premises, depending on the nature and severity of the risk investigated.

Pillar 3 – Issues and products supervision (known as ‘thematic’ work)

The FCA look across the market to analyse current events and investigate potential causes of poor outcomes for consumers and market participants. The FCA do this on an ongoing basis, so they can address risks that are common to more than one firm or sector before they can cause widespread damage. These could be issues like a trend for a particular business practice, or a problem with a certain product.

This work can include firms in any of the FCA conduct categories, but is less likely to involve firms with limited permission.

Where the FCA find a significant risk, they will do thematic work with a number of firms to assess the issues, and respond appropriately. This could include requesting files and information, visiting a firm or carrying out mystery shopping.

The FCA’s action in this area will be to all firms in the relevant market, not just those that have been involved in the assessment work, and the FCA will expect firms to consider and act as necessary on our findings.

15 The purpose of this document is to provide general guidance and information only. Although every effort is made to ensure that the content is accurate, the BVRLA cannot accept any liability whatsoever for any inaccuracy contained within it, nor for any damage or loss, direct or indirect, which may be suffered as a result of any reliance placed upon the information provided, whether arising in contract, tort or in any other way. Advice should always be obtained from your own professional advisers before committing to a specific action.

Follow-up action could include changes to FCA rules or guidance or publishing consumer communications. The FCA will generally publish the results of thematic work and use it to highlight good practices as well as areas of concern.

The FCA will also carry out studies to analyse the effectiveness of competition in different markets, and identify areas where it can intervene to promote more effective competition.

Enforcement The FCA has the power to stop firms or individuals providing regulated financial services and can levy fines for breaches of FCA rules and other legal requirements, including the Consumer Credit Act and Financial Services and Markets Act.

The FCA strategy is to use these powers to achieve ‘credible deterrence’. Credible deterrence means that the FCA tries to improve standards by showing there are meaningful consequences to breaking the rules.

The FCA follow a set enforcement procedure which is very different to the OFT. For example, the FCA standard practice is to send a Notice of Appointment of Investigators to the firm or individual concerned in most circumstances, and to use statutory powers to require individuals to answer questions in interview.

The FCA will publish information about an enforcement case in a Final Notice or Decision Notice where it considers it appropriate.

All of the FCA’s enforcement decisions must be confirmed by a Regulatory Decisions Committee (RDC), which is made up of industry practitioners to represent the public interest. FCA staff will submit their proposal and the supporting evidence to the RDC. The RDC will review the evidence and, in most cases, seek the views of the relevant firm or individual, before coming to a decision.

Financial crime and intelligence

All consumer credit firms are required to put in place systems and controls to mitigate the risk that they may be used to further financial crime. The FCA look at measures firms take to monitor, detect and prevent financial crime risk effectively. The FCA has published a guide for firms which sets out what firms can do to reduce their financial crime risk.

Whistleblowing

One of the ways the FCA receive information about wrongdoing in firms is from employees or former employees. The FCA will collect and act upon the intelligence received from whistleblowers wherever appropriate and take each individual case seriously. The FCA will place significant value on whistleblowing alerts and seek to provide as much useful feedback to the whistleblower as possible, within the restrictions the FCA are bound by.

The FCA guide to consumer credit provides more information on the FCA’s approach to enforcement and supervision, the guide is available here.

16 The purpose of this document is to provide general guidance and information only. Although every effort is made to ensure that the content is accurate, the BVRLA cannot accept any liability whatsoever for any inaccuracy contained within it, nor for any damage or loss, direct or indirect, which may be suffered as a result of any reliance placed upon the information provided, whether arising in contract, tort or in any other way. Advice should always be obtained from your own professional advisers before committing to a specific action.

Further information For full details on the FCA regime the FCA website provides further guidance and assistance. Leasing broker members may also wish to review some of the best practice documents and guides available from the BVRLA including:

• BVRLA Leasing Broker Code of Conduct • BVRLA Guide to Standard Quotations • Key facts template • BVRLA Consumer Credit Guide

All the BVRLA leasing broker guidance from the BVRLA is available on our website here.

The BVRLA also has two associate members who offer consultancy services to assist with FCA compliance. Their contact details are below and they have both contributed to this guide. The BVRLA does not endorse associates or their services.

Compliancy Services 2nd Floor Manor Court 26 Bancroft Hitchin, SG5 1JW Tel: 01462 429705

Regulatory Finance Solutions Ltd Windmill Hill Business Park Whitehill Way Swindon, SN5 6QR Tel: 01793 514 352

Compliancy Services provides specialist consultancy support to businesses that need to achieve and maintain FCA authorisation for consumer credit and other regulated activities. Established in 2003, Compliancy Services is an Associate member of the BVRLA and a leading member of the Association of Professional Compliance Consultants (APCC). Our sole purpose is to reduce the regulatory burden for our clients while ensuring that compliance helps rather than hinders business growth.

BVRLA members can benefit from discounted rates on compliance audits, file checks, e-learning courses and on-site business support days when they subscribe to our online compliance management service. Full details may be found at www.fcaconsumercredit.com/bvrla

To take action on your FCA compliance requirements, call Val Foster-Craddock on 01462 429705.

Consumer Credit Advisory Services (“CCAS”) is a dedicated compliance consultancy company focused on supporting consumer credit lenders with the challenges they face on their journey towards FCA full authorisation, supervision and ongoing regulation. Our unique approach offers the clients that we work with unparalleled experience and expertise as we deliver a holistic solution across compliance, regulation, legal, communications, e-learning and documentation (policies and templates). We believe that this offers our clients unrivalled value and makes a significant contribution to their businesses. Our strong commercial focus, skilled consultants, dedicated specialist team backed-up with leading edge technology ensures best in class delivery. CCAS has amongst its senior managers some of the most experienced individuals in Consumer Credit

17 The purpose of this document is to provide general guidance and information only. Although every effort is made to ensure that the content is accurate, the BVRLA cannot accept any liability whatsoever for any inaccuracy contained within it, nor for any damage or loss, direct or indirect, which may be suffered as a result of any reliance placed upon the information provided, whether arising in contract, tort or in any other way. Advice should always be obtained from your own professional advisers before committing to a specific action.

and high risk firm regulation in the market. We can help you understand the new regulation and how to reduce the risk of this by managing your relationship with the regulator. Based on client demand our latest service is a unique online tool which is designed to help our clients easily review and develop their compliance arrangements using a transparent pricing model http://www.ccas.co.uk/services/ At CCAS we focus on adding value not volume and strive to bring best practice and outcomes for our clients. We spend time with our clients to understand their current situation and the size and scale of what is required. Our breadth and depth of knowledge coupled with our understanding of the regulatory and legislative environment ensures we are in a position to support our clients with their regulatory challenges. Email: [email protected] Website: www.ccas.co.uk

18

Annex A Features of the higher and lower risk regimes

19

Annex B Consumer Credit Licensing Categories

The follow are historic definitions from the former Office of Fair Trading for various categories on the consumer credit licence.

Credit brokerage (C) You may not actually offer to lend money from your own funds but if you will introduce any individual to a third party so they can obtain credit then you will need this category.

It is important to remember that an 'individual' under the Consumer Credit Act 1974 may be a sole trader or small partnership as well as a consumer.

Most financial advisors need this category and almost all appointed representatives need their own licence, for example, to use their own business premises or own trading style.

Introducing people to lenders or other credit brokers for the purposes of obtaining a first charge mortgage is now generally regulated by the FCA.

Many retailers whose customers need to borrow money to buy goods and services for which they would not otherwise have funds and who are introduced to a source of that money by the retailer, also need this category.

This may be the case, for example, in a hire purchase transaction, such as a car purchase, or where a home improvement company recommends a particular credit provider.

An introduction does not depend upon the broker forwarding the application to the lender. A recommendation to deal with a particular lender may amount to credit brokerage.

Credit brokerage also includes introducing people to other credit brokers.

Debt adjusting (D) You may need this category if you will:

• negotiate terms with the creditor on behalf of an individual for the discharge of a debt, or • take over, in return for payments by the debtor, his obligation to discharge a debt, or • engage in any similar activity concerned with the discharging of a debt.

If a customer has existing debts, before you lend or broker additional funds you may undertake to adjust the existing debts owed by the customer. For example this covers the following:

• a car dealer who offers to take over finance already outstanding on an earlier car purchase when arranging part-exchange

• financial advisors who discharge existing debts as they lend additional funds.

You may simply offer to negotiate with creditors on someone's behalf - before you do, you may need this category.

This category is often incorrectly confused with category G, 'Debt administration'.

20

Applicants for this category are likely also to need category E, 'Debt counselling'.

If you apply for category D you will also be required to fill in a competence form.

Debt counselling (E) It would be unusual for any business to adjust a client's debts without having counselled or advised them about it first. It is expected that both Categories D and E are applied for together in such circumstances.

Applicants for this category are likely also to need category D, 'Debt adjusting', however it is possible to engage in debt counselling without engaging in debt adjusting.

Lead generators who introduce clients to debt management companies also often need debt counselling as a licensed category.

If you apply for category E you will also be required to fill in a competence form.

Further information on debt adjusting/counselling For further clarity on what is debt adjusting/counselling the legislation states:

Debt adjusting

39D. (1) When carried on in relation to debts due under a credit agreement—

(a)negotiating with the lender, on behalf of the borrower, terms for the discharge of a debt,

(b)taking over, in return for payments by the borrower, that person’s obligation to discharge a debt, or

(c)any similar activity concerned with the liquidation of a debt,

is a specified kind of activity.

(2) When carried on in relation to debts due under a consumer hire agreement—

(a)negotiating with the owner, on behalf of the hirer, terms for the discharge of a debt,

(b)taking over, in return for payments by the hirer, that person’s obligation to discharge a debt, or

(c)any similar activity concerned with the liquidation of a debt,

is a specified kind of activity.

Debt-counselling

39E. (1) Giving advice to a borrower about the liquidation of a debt due under a credit agreement is a specified kind of activity.

(2) Giving advice to a hirer about the liquidation of a debt due under a consumer hire agreement is a specified kind of activity.

![POLITECNICO DI TORINO · Figure 2.2 FCA Regions [FCA presentation].....24 Figure 2.3 FCA Sales 2017-2018 [Personal processing of FCA data ... This present thesis concerns the subject](https://static.fdocuments.us/doc/165x107/602c67dbc5d9f6029526a4a8/politecnico-di-torino-figure-22-fca-regions-fca-presentation24-figure-23.jpg)