Buying Real Estate with Your IRA

35

\ REAL ESTATE IN YOUR IRA February 14, 2017 www.AdvantaIRA.com

-

Upload

mike-cornetet -

Category

Economy & Finance

-

view

21 -

download

0

Transcript of Buying Real Estate with Your IRA

\REAL ESTATE IN YOUR IRAFebruary14,2017

www.AdvantaIRA.com

KEY POINTS TO TAKE AWAYReal Estate in Your IRA

You choosethe investment

All expenses are paid bythe IRA and all incomeis received by the IRA

Any IRA or formeremployer plan qualifies

Advanta IRA is a self-directed retirement plan administrator serving clients nationwide. We provide our clients

exceptional personal service, experience, and knowledge that is paramount in administrating self-directed IRAs.

With a combined 20+ years in our industry, Advanta IRA is the nation’s premier self-directed IRA administrator. We also provide a more flexible fee schedule than most custodians.

EXPERIENCED

We use multiple banks that are insured by the FDIC to protect the undirected cash held within your IRA.

SECURE

With clients across the nation, Advanta IRA holds over $700 million in assets and partners with a network of trusted CPAs and attorneys.

TRUSTED

Our account manager system guarantees clients concierge-style personal service. Advanta IRA also offers cutting-edge educational tools for all types of investors.

PERSONAL

WHO WE AREAbout Advanta IRA

OUR LOCATIONSAbout Advanta IRA

We serve clients nationwide with regional offices in Florida and Georgia.Call us at 800.425.0653 or visit www.AdvantaIRA.com today.

OUR LEARNING CENTERAbout Advanta IRA

ADVANTA ON-DEMANDADVANTAIRA.COM/LEARNING-CENTER

Watch free investment training videos and learn how to build a

self-directed plan that’sright for you

THE ADVANTA BLOGBLOG.ADVANTAIRA.COM

Get the latest industry news, updates, and insights from our

team of professionals

ADVANTA EVENTSADVANTAIRA.COM/EVENTS

Seminars, webinars, networking, and lunch and learn events to help

you learn the ins and outs of self-direction

Powerful knowledge about self-directed retirement plans and alternativeinvestments is available at your fingertips:

Did you know self-directed accounts only add up to less than 2% of IRA investments.

HAVEN’T HEARD OF A SELF-DIRECTED IRA?

Maybe it is because the most common IRAs are administered by banks and investment brokers who offer limited investment products.

However, the IRS regulations allow a much broader range of investments.

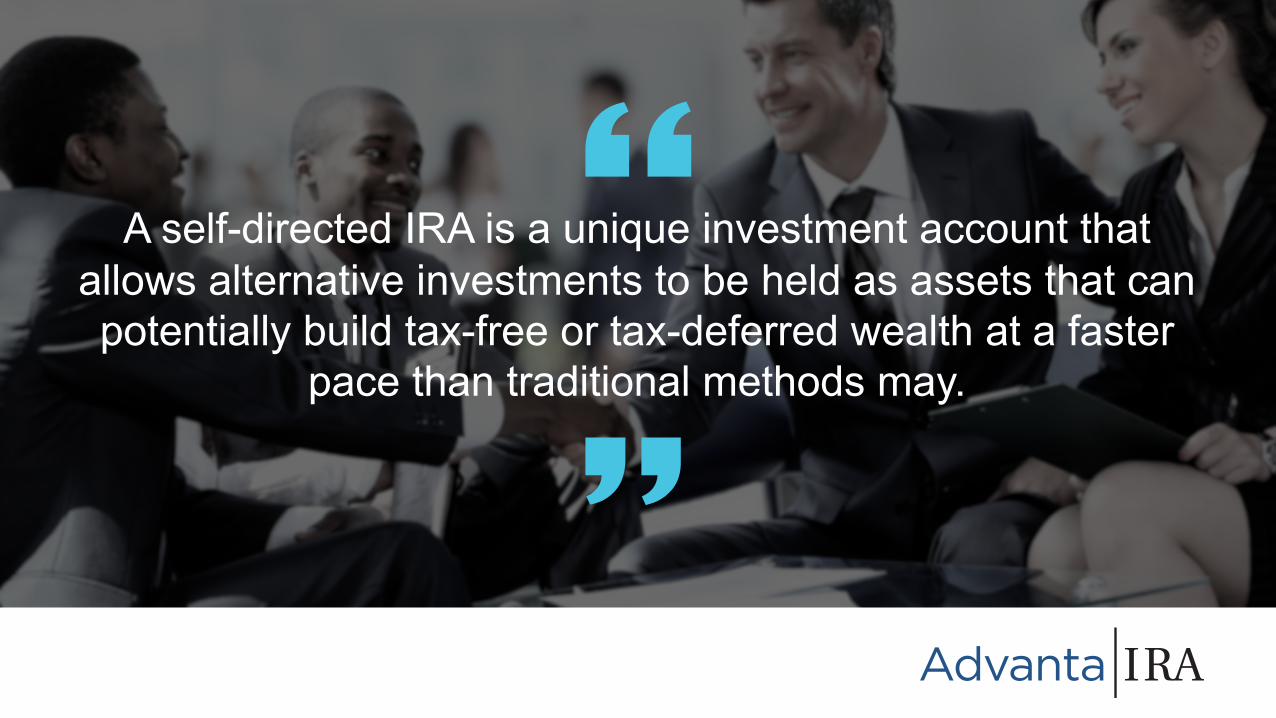

What Is a Self-Directed IRA?

?

A self-directed IRA is a unique investment account that allows alternative investments to be held as assets that can potentially build tax-free or tax-deferred wealth at a faster

pace than traditional methods may.

The term self-directed simply means that theowner of the IRA has control over what

investments the IRA makes.

DEFINITION

Self-directed IRAs can acquire real estate, hold mortgages and notes, private placements (such as LLCs and trusts), precious metals, invest in foreign currency and participate in futures trading and other investment options.

These plans can certainly hold the traditional stocks, bonds, and mutual funds, but the myriad of alternative investments are what attract owners of these accounts.

What Is a Self-Directed IRA?

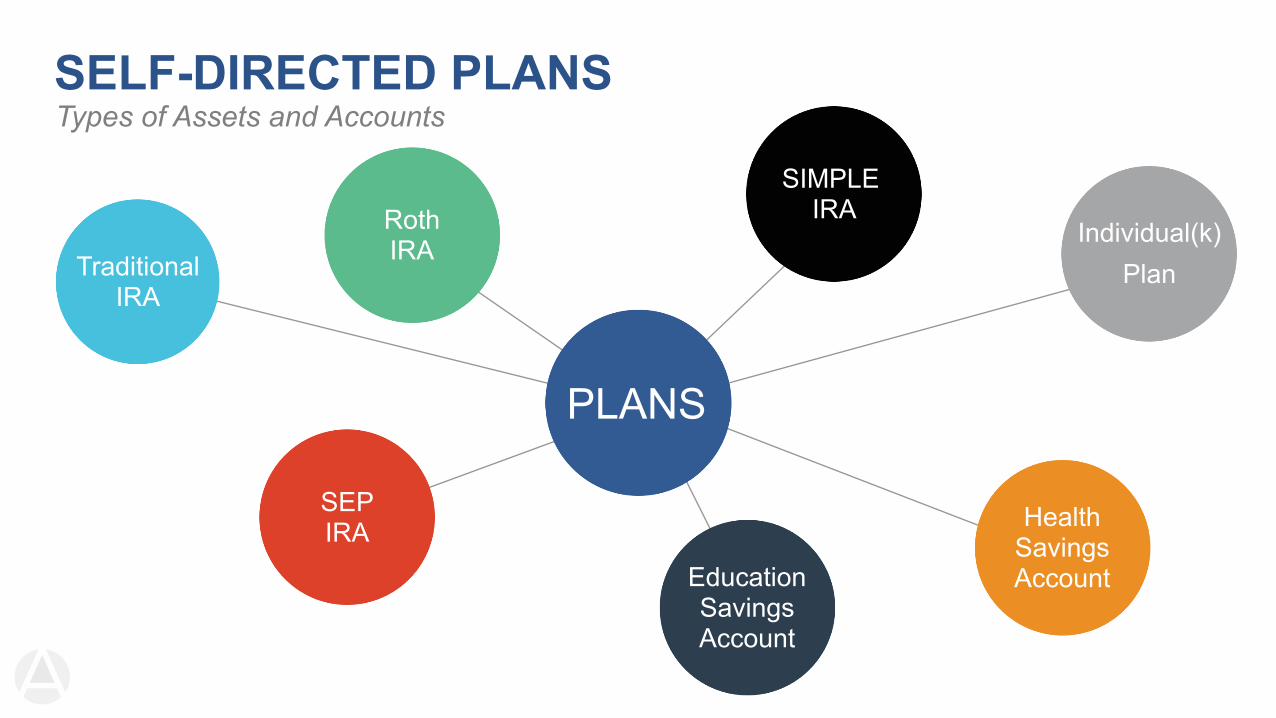

SELF-DIRECTED PLANSTypes of Assets and Accounts

TraditionalIRA

SEPIRA

RothIRA

EducationSavingsAccount

SIMPLE IRA

Individual(k)Plan

HealthSavingsAccount

PLANS

PLANS AT-A-GLANCETypes of Assets and Accounts

TRADITIONAL IRA

CRITERIAAnyone with earned income is eligible to contribute to a traditional

IRA; deductibility may be limited based on annual income

BENEFITSTax deduction, lowering your current tax bill* + Tax-deferred growth +

Former 401(k) can be rolled directly in with no tax consequence +Retirement savings

*Deductibility phased out depending on income

Check with your CPA or accountant to help determine which option would be the best fit for you and your business.

1

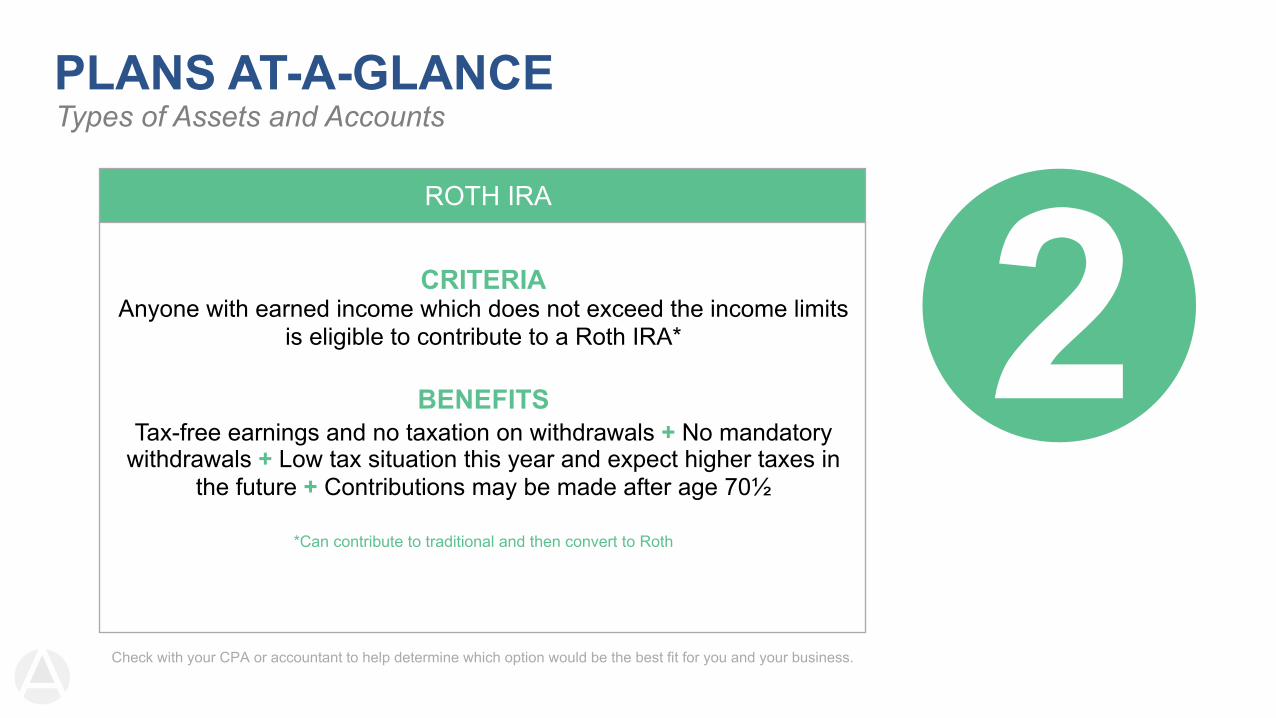

PLANS AT-A-GLANCETypes of Assets and Accounts

ROTH IRA

CRITERIAAnyone with earned income which does not exceed the income limits

is eligible to contribute to a Roth IRA*

BENEFITSTax-free earnings and no taxation on withdrawals + No mandatory

withdrawals + Low tax situation this year and expect higher taxes in the future + Contributions may be made after age 70½

*Can contribute to traditional and then convert to Roth

2Check with your CPA or accountant to help determine which option would be the best fit for you and your business.

PLANS AT-A-GLANCETypes of Assets and Accounts

EMPLOYER-BASED ACCOUNTS: SEP IRA, SIMPLE IRA, 401(K)

WHO THEY ARE FORSole proprietors, independent contractor, self-employed, partner,

corporation, or S corporation

BENEFITSSEP and SIMPLE IRAs offer tax-deferred growth like traditional IRAs, but have larger contributions limits; they also offer lower administrative costs than a 401(k) plan + You must include certain employees in SEP

and SIMPLE + Individual(k) offers largest potential contribution for a business without employees (no discrimination testing necessary) +

Roth individual(k) option available

3Check with your CPA or accountant to help determine which option would be the best fit for you and your business.

PLAN CONTRIBUTION LIMITSTypes of Assets and Accounts

FOR YEAR 2017

Traditional / Roth IRA $5,500 ($6,500 if over 50)

SEP IRA Up to $54,000 (25% of compensation)

SIMPLE IRA $12,500 (additional $3,000 if over 50) +up to 3% of employer match)

401(k) $18,000 (+ $6,000 if over 50) of salary deferral+ 25% employer match up to $54,000 ($60,000)

ESA (education) $2,000 per year, per child

HSA (health) $3,400 individual (+ $1,000 catch-up) / $6,750 family

INVESTMENT OPTIONSTypes of Assets and Accounts

Realestate

Single-member

LLC

Notes &mortgages

Privateplacements/

privatestock

Otherinvestments*

Futurestrading

Foreigncurrency(FOREX)

INVESTMENT

OPTIONS

*Other investments include: Oil and gas rights � Tax certificates � Structured settlements � Commercial paper � Convertible notes � Commodities � Livestock �Timberland � Rights or warrants � Accounts receivable factoring � Equipment leasing � and more

TYPES OF ASSETSTypes of Assets and Accounts

Real Estate Assets• Commercial• Rehabs/flips• Timeshares• Residential• Condos• Duplexes

TYPES OF ASSETSTypes of Assets and Accounts

Paper Assets• Mortgage loans• Tax liens• Unsecured notes• Debenture notes• Option contracts• Assignments• Joint venturing• Accounts receivable

TYPES OF ASSETSTypes of Assets and Accounts

Other Alternative Assets• LLCs• Farm animals• Partnerships• Movie projects• Precious metals• Equipment leasing• Forex accounts• Private stock• Commodities• Oil/gas

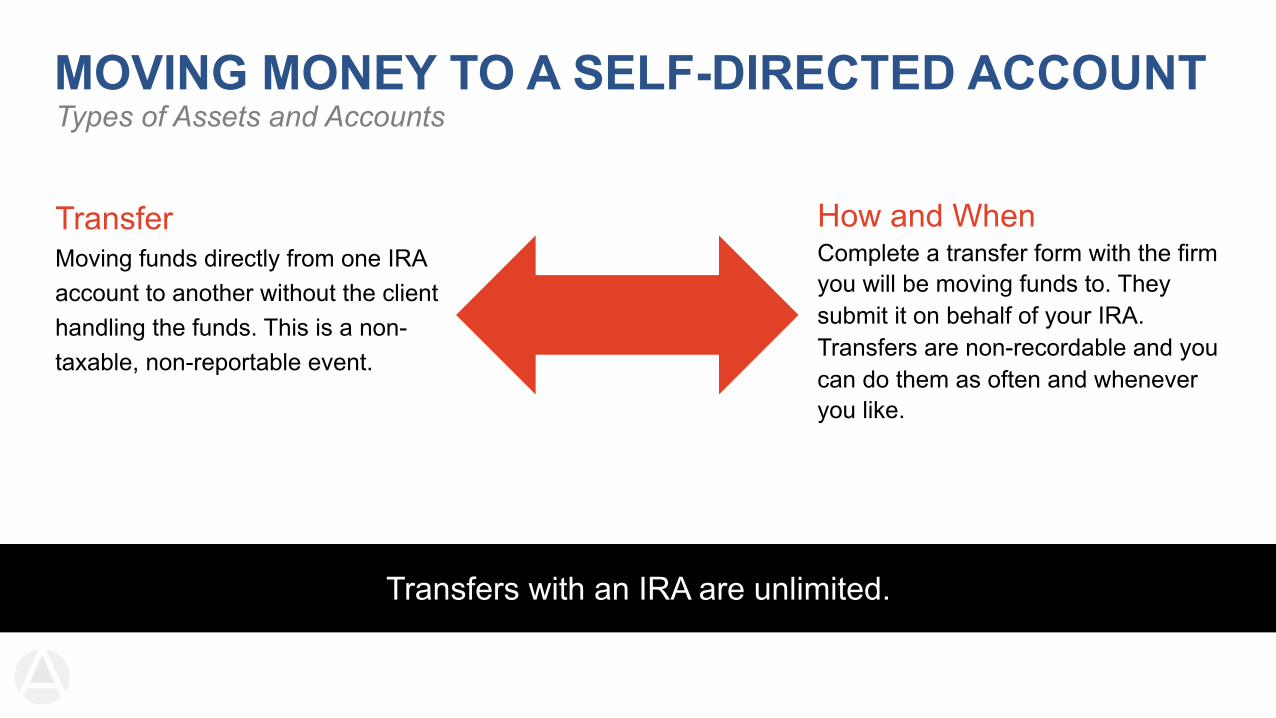

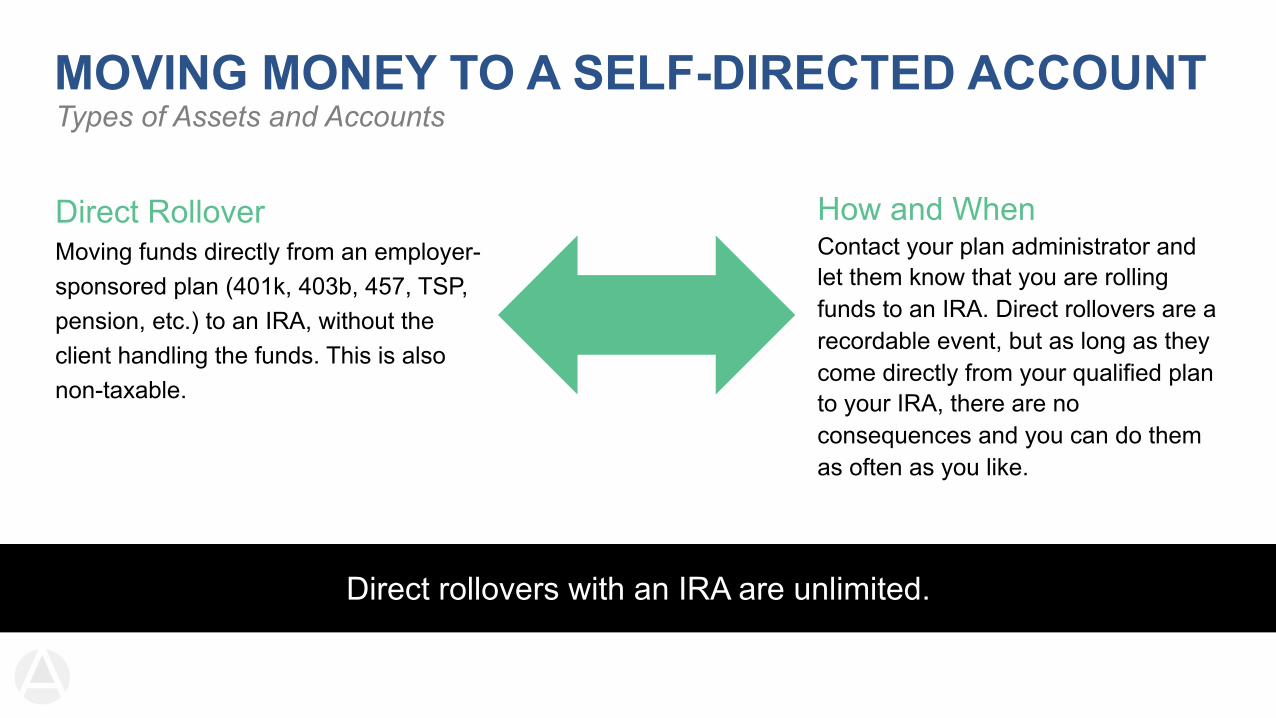

MOVING MONEY TO A SELF-DIRECTED ACCOUNT

TransferMoving funds directly from one IRA account to another without the client handling the funds. This is a non-taxable, non-reportable event.

Types of Assets and Accounts

Transfers with an IRA are unlimited.

How and WhenComplete a transfer form with the firm you will be moving funds to. They submit it on behalf of your IRA. Transfers are non-recordable and you can do them as often and whenever you like.

MOVING MONEY TO A SELF-DIRECTED ACCOUNT

Direct RolloverMoving funds directly from an employer-sponsored plan (401k, 403b, 457, TSP, pension, etc.) to an IRA, without the client handling the funds. This is also non-taxable.

Types of Assets and Accounts

Direct rollovers with an IRA are unlimited.

How and WhenContact your plan administrator and let them know that you are rolling funds to an IRA. Direct rollovers are a recordable event, but as long as they come directly from your qualified plan to your IRA, there are no consequences and you can do them as often as you like.

MOVING MONEY TO A SELF-DIRECTED ACCOUNT

Indirect RolloverIf you personally take possession of the funds from an IRA or employer plan, you have 60 calendar days to move those funds back to an IRA to avoid taxes. This can only be done once per 12 months.

Types of Assets and Accounts

Indirect rollovers with an IRA are unlimited.

How and WhenAn indirect rollover occurs when you take a distribution from your IRA or qualified plan. One per 12 month period. This is a recordable event and should the funds fail to be deposited to your IRA account within 60 days, they are forever out of the account.

PROHIBITED TRANSACTIONSTypes of Assets and Accounts

INVESTMENT RESTRICTIONS

Life insurance

Collectibles (antiques, alcohol, artwork, stamps, and coins*)

*Some coins are allowed if they are valued based on the trading value of the metal

✕There are three elements to a prohibited transaction (the IRA, the DP, transactions

between IRA and DP). An IRA cannot lend money to a disqualified person or entity under any circumstance. There are no exceptions to this rule.

PROHIBITED TRANSACTIONSTypes of Assets and Accounts

DISQUALIFIED PERSONS (DP)

IRA owner and spouse

Lineal ascendants of IRA owner (parents and grandparents)

Lineal descendants of IRA owner (kids and grandkids), as well as spouses of lineal descendants

Business or entity owned or controlled by one of the above

Others

✕There are three elements to a prohibited transaction (the IRA, the DP, transactions

between IRA and DP). An IRA cannot lend money to a disqualified person or entity under any circumstance. There are no exceptions to this rule.

PROHIBITED TRANSACTIONSTypes of Assets and Accounts

OTHER CONSIDERATIONS

Dealing with brothers, sisters, other family members for less than fair market value (i.e. lending money to them at less than what a third

party might charge)

Using a middleman between IRA and disqualified person (step transaction doctrine)

A’s IRA lends to B; B’s IRA lends to A

Having an IRA lend money on a note and having that note secured by a collectible (collection/re-possession issue)

There are three elements to a prohibited transaction (the IRA, the DP, transactions between IRA and DP). An IRA cannot lend money to a disqualified person or entity under

any circumstance. There are no exceptions to this rule.

✕

TRANSACTIONS WITH DISQUALIFIED PERSONSTypes of Assets and Accounts

IRA owns real estate and leases it out to your daughter

Your father’s IRA lends money to you or your son

IRA purchases a piece of real estate from your son

Your IRA makes the down payment for a property andyou personally guarantee

the mortgage

Spouse’s IRA owns a pieceof real estate and wants tosell your IRA a portion ofthat property (could have partnered at the outset?)

Your IRA purchases real estate and hires your son

(or his company) to performthe rehab work

USING IRA FUNDS TO INVEST IN REAL ESTATE

§ Don’t take funds out of your 401(k) to invest in real estate

§ If you remove funds from an IRA or employer’s plan, you are then personally subject to taxes

§ If you then use these funds to invest in real estate, you will have lost 20-30% of your purchasing power to taxes

§ By transferring or rolling these funds over to a self-directed IRA, no taxes are due and you have more cash to invest

Example:

- Client has $100K in an IRA

- Doesn’t know about self-directed IRAs

- Removes cash from current custodian to invest and faces possible 10% early withdrawal penalty and income taxes

- By using self-directed IRA, NO taxes or penalties for early withdrawal to invest

Real Estate in Your IRA

!

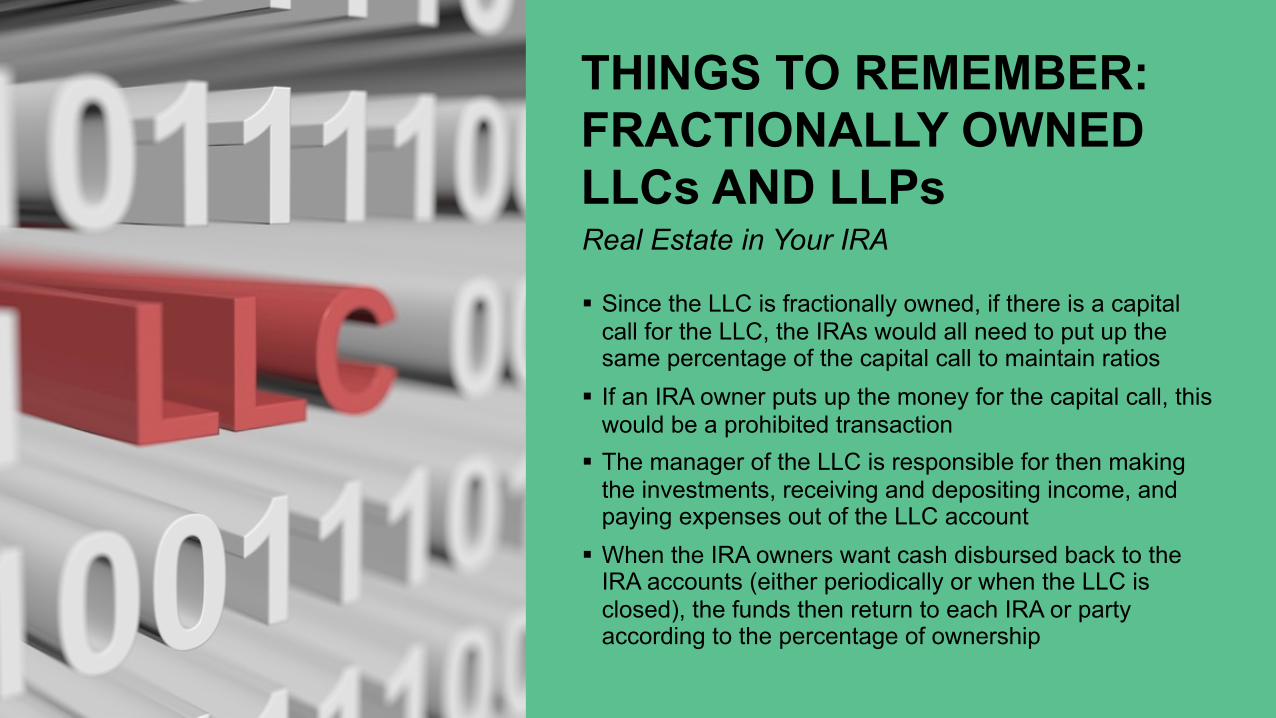

THINGS TO REMEMBER: FRACTIONALLY OWNED LLCs AND LLPs

§ Since the LLC is fractionally owned, if there is a capital call for the LLC, the IRAs would all need to put up the same percentage of the capital call to maintain ratios

§ If an IRA owner puts up the money for the capital call, this would be a prohibited transaction

§ The manager of the LLC is responsible for then making the investments, receiving and depositing income, and paying expenses out of the LLC account

§ When the IRA owners want cash disbursed back to the IRA accounts (either periodically or when the LLC is closed), the funds then return to each IRA or party according to the percentage of ownership

Real Estate in Your IRA

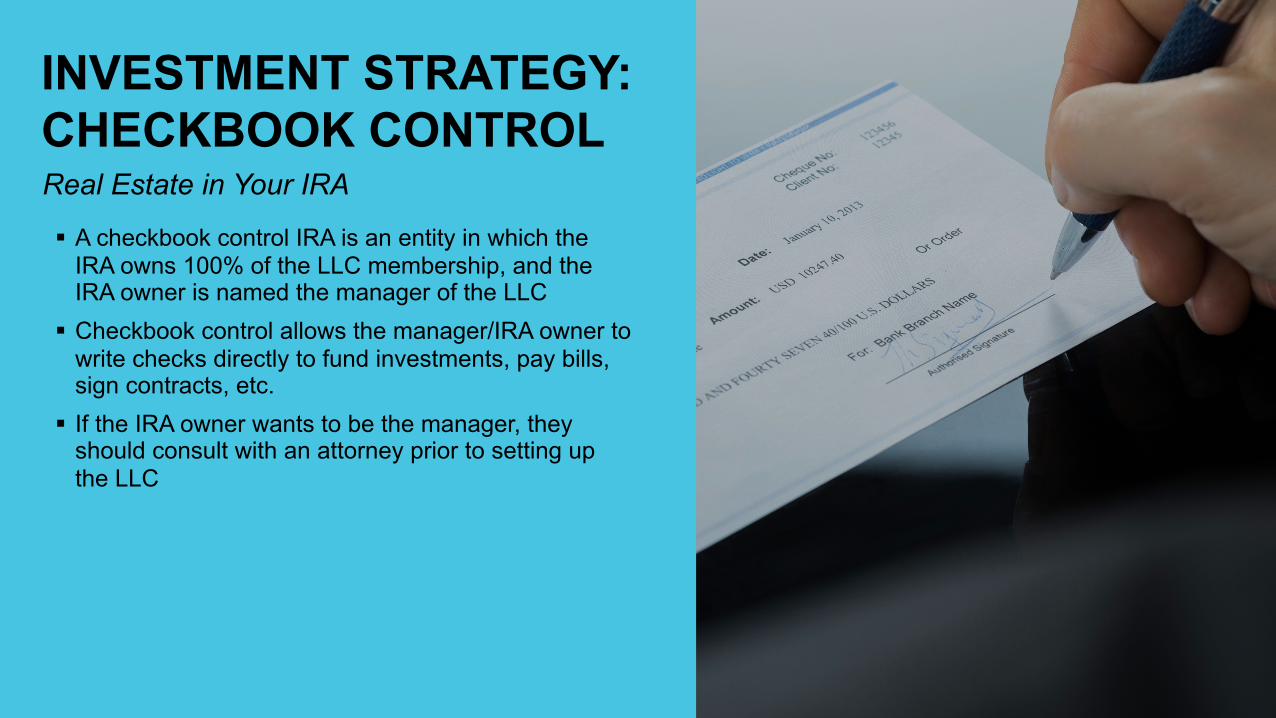

INVESTMENT STRATEGY: CHECKBOOK CONTROL

§ A checkbook control IRA is an entity in which the IRA owns 100% of the LLC membership, and the IRA owner is named the manager of the LLC

§ Checkbook control allows the manager/IRA owner to write checks directly to fund investments, pay bills, sign contracts, etc.

§ If the IRA owner wants to be the manager, they should consult with an attorney prior to setting up the LLC

Real Estate in Your IRA

§ The IRA custodians who offer the “one-stop shop” of an IRA, an LLC, and a checkbook to get started, charge several thousand dollars for this arrangement

§ There is no secret formula that an IRA custodian has that makes an LLC allowed or disallowed by the IRS, and Advanta IRA does permit this investment with a signed disclaimer

§ If you are interested in reading the IRS cases on which the checkbook control IRA is based, they are:

- Swanson v. Commissioner 106 TC 76 (1996)- T. L. Ellis, TC Memo. 2013-245

INVESTMENT STRATEGY: KNOW YOUR FACTSReal Estate in Your IRA

1 2 3PURCHASING REAL ESTATE THROUGH TRUSTSReal Estate in Your IRA

CASE STUDY

The private trust document is drafted

• Within private trust, the IRA is listed as grantor and beneficiary of trust

• Advanta IRA FBO Joe Smith IRA #8001234

• Joe must name a non-disqualified person as trustee

• Trust is not public record

CASE STUDY

The trust document isapproved by Joe

• Joe must read and approve trust and sends approved copy to Advanta IRA

• Joe also has trustee sign trust document

• Advanta signs trust agreement on behalf of IRA

CASE STUDY

Joe opens and funds anAdvanta IRA account

• Completes an IRA application• Transfers/rolls over funds from an

existing IRA or 401(k) • Account number issued in less than

24 hours

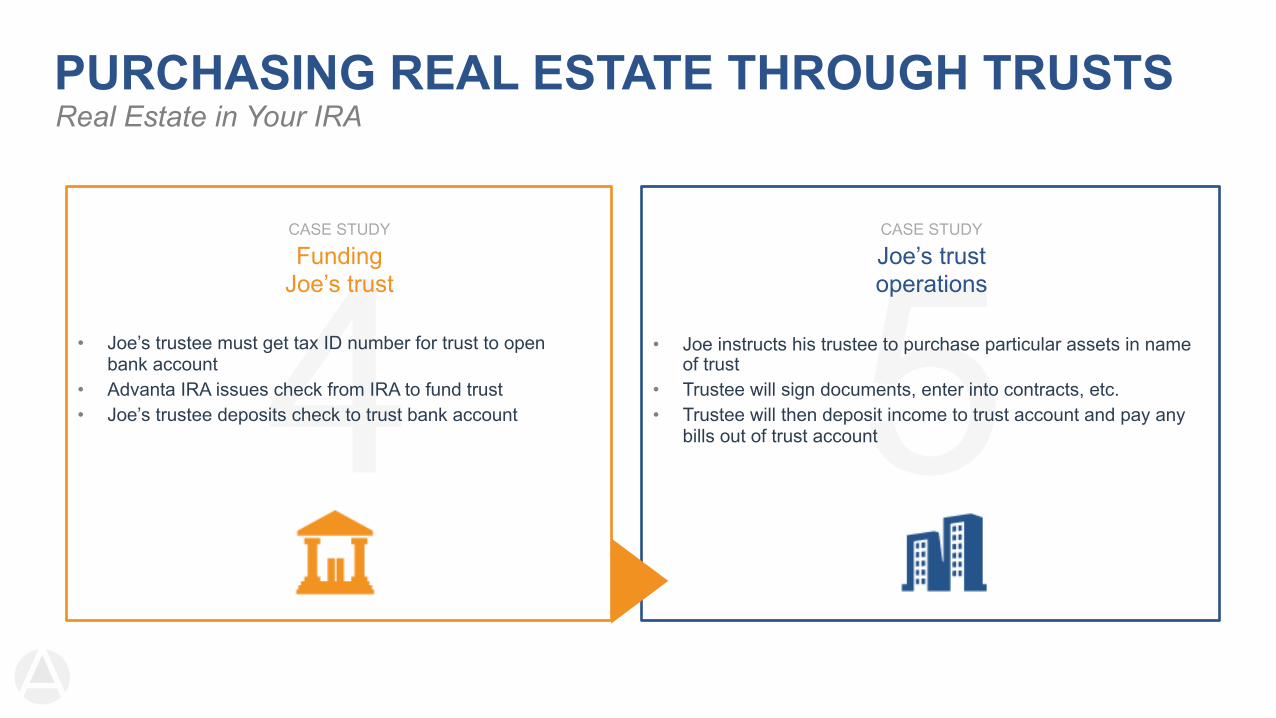

4 5CASE STUDY

Joe’s trust operations

• Joe instructs his trustee to purchase particular assets in name of trust

• Trustee will sign documents, enter into contracts, etc. • Trustee will then deposit income to trust account and pay any

bills out of trust account

CASE STUDY

FundingJoe’s trust

• Joe’s trustee must get tax ID number for trust to open bank account

• Advanta IRA issues check from IRA to fund trust• Joe’s trustee deposits check to trust bank account

PURCHASING REAL ESTATE THROUGH TRUSTSReal Estate in Your IRA

TWO MAIN TYPES OF TRUSTS WITH IRAsReal Estate in Your IRA

PERSONAL PROPERTY (TO HOLD NOTES, MORTGAGES, AND OTHER ASSETS)

Joe’s trustee opens bank accountand purchases assets

Joe’s trustee must maintain records ofincome and expenses

LAND TRUSTS (TO HOLD REAL ESTATE)

Advanta IRA will act as record-keeper

Joe must approve all closing documents

Joe’s trustee signs closing documents

All rents and expenses flow in and out of IRA

USING FINANCING WITH AN IRAReal Estate in Your IRA

UDFI TAX CONSIDERATIONS

Total monthly rents $12,000 $1,000/month

Total rent subject to UDFI $6,000*

Tax rate (using top end) 39%

Total taxes paid $2,340

Net income after UDFI $9,660 $6,000 + $3,660

Monthly payment $3,597.36

Total income minus taxes $5,108.64

*This doesn’t include deductions and depreciations that would limit impact of UDFI.

LET ADVANTA IRA HELP YOU TODAYGetting Started

OPEN ACCOUNT

Opening an account with Advanta IRA only takes

a few minutes. We pair you with your own client services

representative who guides you every step of the way.

DONE STEP1

FUND ACCOUNT

Add funds by making a cash contribution or by moving or transferring funds from an existing IRA or 401(k) plan.

DONE STEP2

START INVESTING

Choose from a wide variety of alternative investments

including real estate, notes and mortgages, single-member

LLCs, private placements and private stock, precious metals,

and other assets.

DONE STEP3

Schedule a consultation and speak one-on-one with a self-directed investment expert today.

Our consultations are always free.