BUY PSL Limited - Sify.comim.sify.com/sifycmsimg/dec2009/Finance/14925047_PSL_Sep09_Results.pdf ·...

19

____________________________________________________________________________________________ Firstcall India Equity Advisors Pvt. Ltd 1 Steel-Tubes/Pipes INDIA Market Cap Rs.8798.16 mn 26 th December, 2009 BCBBB NAGAR CONST BSE SENSEX CMP: Rs.168.00 (As on 26 th Dec, 2009) EQUITY RESEARCH PSL Limited • We initiated the coverage of Time PSL Ltd and set a target price of Rs.200.00. It is one of the largest HSAW pipe manufacturers in India with the installed capacity of 1.475 MTPA of pipes. • The company’s current order book stands at Rs16.00 billion, which will get executed within this financial year. • Recently PSL has raised Rs 1493.2mn worth of fresh funds via Qualified Institutional Placement (QIP). • PSL is likely to diversify into development of special economic zones (SEZs). • PSL is setting up additional capacities of 450,000 TPA of pipe manufacturing which include 225,000 TPA HSAW pipe mill at Sharjah, UAE and another 225,000 PTA spiral pipe mill project at Vishakhapatnam. • The top line and bottom-line of the company are expected to grow at a CAGR of 13.41% and 8.99% respectively over FY08 to FY11E. One-year comparative graph with BSE PSL BSE SENSEX Key Financials FY08 FY09 FY10E FY11E Key Data Net Sales(mn) 22188.50 35499.5 28145.23 32367.0 Face Value (Rs.) 10.00 EBITDA(Rs.mn) 2332.10 2845.20 3093.16 3333.80 Shares Outstanding 52.37 mn EBITDA Margin (%) 10.51% 8.01% 10.99% 10.30% 52 wk. High/Low Rs.188. 0/59.50 Net Profit (Rs.Mn) 847.70 859.30 1064.37 1097.49 Volume (2wk.Avg.) 311991 Net profit Margin (%) 3.82% 2.42% 3.78% 3.39% BSE Code 526801 U. Janakirao Analyst Equity Research Desk [email protected] V.S.R Sastry Vice president Equity Research Desk 91-22-25276077 [email protected] Dr. V.V.L.N. Sastry Ph.D. Chief Research Officer [email protected] BUY Target price: Rs.200.00 (For Medium to Long term)

-

Upload

hoangkhuong -

Category

Documents

-

view

225 -

download

0

Transcript of BUY PSL Limited - Sify.comim.sify.com/sifycmsimg/dec2009/Finance/14925047_PSL_Sep09_Results.pdf ·...

____________________________________________________________________________________________

Firstcall India Equity Advisors Pvt. Ltd

1

Steel-Tubes/Pipes

INDIA

Market Cap

Rs.8798.16 mn

26th December, 2009

BCBBB

NAGAR CONST BSE SENSEX

CMP: Rs.168.00 (As on 26th Dec, 2009)

EQUITY RESEARCH

PSL Limited

• We initiated the coverage of Time PSL Ltd and set a target price of Rs.200.00. It is one of the largest HSAW pipe manufacturers in India with the installed capacity of 1.475 MTPA of pipes.

• The company’s current order book stands at Rs16.00 billion, which will get executed within this financial year.

• Recently PSL has raised Rs 1493.2mn worth of fresh funds via Qualified Institutional Placement (QIP).

• PSL is likely to diversify into development of special economic zones (SEZs).

• PSL is setting up additional capacities of 450,000 TPA of pipe manufacturing which include 225,000 TPA HSAW pipe mill at Sharjah, UAE and another 225,000 PTA spiral pipe mill project at Vishakhapatnam.

• The top line and bottom-line of the company are expected to grow at a CAGR of 13.41% and 8.99% respectively over FY08 to FY11E.

One-year comparative graph with BSE

PSL BSE SENSEX

Key Financials

FY08

FY09

FY10E

FY11E

Key Data

Net Sales(mn) 22188.50 35499.5 28145.23 32367.0 Face Value (Rs.)

10.00

EBITDA(Rs.mn) 2332.10 2845.20 3093.16 3333.80 Shares Outstanding

52.37 mn

EBITDA Margin (%) 10.51% 8.01% 10.99% 10.30%

52 wk. High/Low

Rs.188.0/59.50

Net Profit (Rs.Mn) 847.70 859.30 1064.37 1097.49

Volume (2wk.Avg.)

311991

Net profit Margin (%) 3.82% 2.42% 3.78% 3.39% BSE Code

526801

U. Janakirao Analyst Equity Research Desk [email protected]

V.S.R Sastry Vice president Equity Research Desk 91-22-25276077 [email protected]

Dr. V.V.L.N. Sastry Ph.D. Chief Research Officer [email protected]

BUY Target price: Rs.200.00 (For Medium to Long term)

PSL Ltd-26th December, 2009

___________________________________________________________________________________________

Firstcall India Equity Advisors Pvt. Ltd 2

Table of Contents Page no

1. Peer group Comparisons 03

2. Company Updates 03

3. Company’s profile 06

5. Business Area 06

6. SWOT analysis 10

7. Financials 11

8. Valuation 16

9. Industry overview 17

PSL Ltd-26th December, 2009

___________________________________________________________________________________________

Firstcall India Equity Advisors Pvt. Ltd 3

Peer Group Comparison

Name of the Company

52 wk High /

Low(Rs.)

C.M.P(Rs.)

E.P.S(Rs.)

P/E(x)

PSL 188.00/59.50 168.45 20.18 8.34

Welspun Gujarat Stahl Roh 296.35/48.50 267.05 20.10 13.29

Man Industries 60.90/21.50 50.30 5.27 9.54

Jindal Saw 198.70/27.00 187.65 16.90 11.10

Updates of the Company

• Results Update (Q2 FY10)

For the quarter ended on September 30, 2009 (Standalone) the company has registered a 5.83 % (YOY)

degrowth in the net sales and stood at Rs.6062.20 mn from Rs.6437.800 mn of the corresponding period

of the previous year. The operating profit for the quarter stood at Rs.684.90 mn from Rs.662.50 mn, for

the same quarter of last year. The operating profit margins for the quarter stood at 11.30%. During

Q2FY10 the net profit of the company stood at Rs.215.80 mn. NPM stood at 3.56%. EPS for the quarter

stood at Rs.4.12 per equity share of Rs.10.00.

Quarterly Results –Standalone(Rs in mn)

As at Q2FY09 Q2FY10 %Change

Net Sales 6437.80 6062.20 (5.83)

Net Profit 216.10 215.80 (0.14)

Basic EPS(Rs)* 5.08 4.12 (18.90)

PSL Ltd-26th December, 2009

___________________________________________________________________________________________

Firstcall India Equity Advisors Pvt. Ltd 4

• Margins (%):

Operating Profit Margins (OPM %)

Net Profit Margins (NPM %)

PSL Ltd-26th December, 2009

___________________________________________________________________________________________

Firstcall India Equity Advisors Pvt. Ltd 5

• PSL accumulates Rs.1493.2mn via QIP route

PSL has successfully raised Rs 1493.2mn worth of fresh funds via Qualified Institutional Placement (QIP).

The company has allotted 10,750,000 equity shares of Rs 10 each at a price of Rs 138.90 per share to 20

Qualified Institutional Buyers (QIB's) under this issue. The price band for the issue has been fixed at Rs

138.88 to Rs 160 per share.

• PSL to raise capacity at Vizag, Dubai units

PSL is setting up additional capacities of 450,000 TPA of pipe manufacturing which include 225,000 TPA

HSAW pipe mill at Sharjah, UAE and another 225,000 PTA spiral pipe mill project at Vishakhapatnam.

Current capacities at these two sites are 75,000 TPA each. Both the mills are expected to be completed by

the end of Q1 FY11. The total estimated cost of the project is Rs 2.3 bn. PSL’s total pipe manufacturing

capacity will enhance to 1,925,000 TPA after the expansion. Currently it is 1,475,000 TPA.

• US market opportunities:

More than one mn miles of gas pipelines out of 1.5 mn miles in US have to be replaced as these pipelines

were laid prior to 1975. PSL has recently set up a plant in Mississippi, USA with the total project cost of

USD 103 mn with the capacity of 300,000 MTPA, to tap these opportunities.

• Strong Order book

PSL has the strong order book position of Rs 16 bn, executable within 12 months, of which 70%, 25% and

5% are the orders for pipes, pipe coating and ancellary products and services respectively. The company

hoping for additional orders from the gas grid component, which will come to maturity this year and at

least a part of those orders, will get executed.

• PSL bags orders worth Rs 7 bn from GAIL

PSL has received another prestigious contact from Gail India valuing over Rs 2100 mn. The company had

already bagged an order valuing approximately Rs 5000 mn from Gail India for supplying pipes for their

Dahej-Vijaipur pipeline upgradation project (DVPL-II).The company has received contract for providing

pipe coating services for the entire Dahej-Vijaipur Pipeline upgradation project (DVPL-II). The company

has thus been successful in procuring a total order aggregating to over Rs 7000mn comprising of two

parts, one for supplying of pipes valuing approximately Rs 5000mn and now the other for providing quality

external coating valuing over Rs 2100mn.

PSL Ltd-26th December, 2009

___________________________________________________________________________________________

Firstcall India Equity Advisors Pvt. Ltd 6

• Dividend declared

For the the financial year 2008-09 the company has declared a dividend of 50% (Re.5 per share) on the

face value of equity share Rs.10.00 each.

• PSL to diversify into SEZ development

PSL is likely to diversify into development of special economic zones (SEZ), with the company getting the

stage-1 approval from the Centre to set up an exclusive SEZ for alternative energy and energy ancillaries

at Pipavav in Gujarat. The SEZ will be dedicated to alternative energy products like bio-diesel, solar,

ethanol and wind generation, with units producing equipment needed for such businesses also to be

invited to set up their manufacturing facilities in the zone. This will mark PSL`s first diversification

initiative from its core business of producing cross-country, large-diameter pipelines for transportation of

hydrocarbon and water products.

Company Profile

PSL Ltd (PSL) is one of the largest HSAW pipe manufacturers with the installed capacity of 1.475 MTPA of

pipes. The company has 13 HSAW pipe mills, 11 of which are located in five locations geographically

spread throughout India and one each at UAE and USA. PSL also provide pipe coating and other ancillary

products and services related to pipe industry. About 98% of the revenues of the company are derived

from domestic market.

Business Areas

PSL Ltd-26th December, 2009

___________________________________________________________________________________________

Firstcall India Equity Advisors Pvt. Ltd 7

HSAW Pipes:

PSL manufactures HSAW pipes, which are used in long distance transportation of Oil & Gas and water. Pipes

manufactured by PSL are certified to American Petroleum Institute (API) standards for oil & gas and water

transportation. PSL have the strong hold in the domestic market with the mammoth market share of 70-80%

in HSAW segment. Domestic sales contributed 98% to the topline in FY09.Pipe contributed in excess of 81%

to the topline of the company in FY09

Pipe Coatings:

PSL also provides pipe coating services which includes pipe corrosion protection. There are different types of

coatings such as three layer polyethylene/Fusion bonded epoxy coating, coal tar enamel coating, concrete

weight coating, internal coating etc. PSL undertakes both internal and external coatings.

Ancillary Products and Services

PSL also provides various ancillary products and services, which are related to pipe industry such as

Induction Bending:

It is the process wherein pipes are bent as per the requirement using Induction-heating process.

PSL Ltd-26th December, 2009

___________________________________________________________________________________________

Firstcall India Equity Advisors Pvt. Ltd 8

Sacrificial Anodes:

Basic Function: The basic function of sacrificial anode is to sacrifice itself to protect the offshore pipeline of

offshore platform structures. These are made of aluminium alloy or zinc.

Location and capacity: PSL have state of the art plant in Kandla with the annual capacity if 1,500,000 MT.

Reinforcement bar (Rebar) Coating:

PSL provides rebar coating services and have executed contracts for various infrastructure and construction

players.

Manufacturing of Turnkey HSAW Plant and machinery:

PSL have expertise in the design, manufacture, supply, erection and commissioning of plant, machinery and

equipments catering to pipeline industry.

Subsidiaries:

I. PSL Corrosion Control Services Ltd

II. Pipeline Systems Ltd

III. PSL FZE –UAE

IV. PSL USA INC.

PSL Ltd-26th December, 2009

___________________________________________________________________________________________

Firstcall India Equity Advisors Pvt. Ltd 9

• PSL Corrosion Control Services Limited

This Company is a wholly owned subsidiary of the Company, it is presently engaged in Rebar Coating and

providing Anti-corrosive treatment. In order to focus on the Company’s main activities of Pipe

Manufacturing and providing Anti-corrosive Coating, the Board has accorded its in principle approval to

dispose off, subject to an approval from Members of the Company (which is being sought through Postal

Ballot), its Rebar Plants at Chennai and Vizag to its Subsidiary.

• Pipeline Systems Limited

This Company was incorporated in May, 2006 at Mauritius as a wholly owned subsidiary Company of your

Company. Subsequently, another Company namely PSL FZE was established at Sharjah in UAE as a wholly

owned subsidiary of Pipeline Systems Limited.

• PSL USA INC. & PSL NORTH AMERICA LLC

PSL USA INC was incorporated on 4th December, 2006 under laws of State of Delaware, USA primarily to

bag contracts for manufacture of pipes, keeping in view the upsurge in the pipe laying activity in North

America. This Company holds 78% shareholding in a Joint Venture Company (also incorporated under the

laws of State of Delaware) 12% held by HSAW Solutions LLC and the balance 10% by Lloyd Systems Inc.

Major Clients:

• Oil India

• ONGC

• RIL

• Hindustan Petroleum

• ESSAR

• Oman Oil Company

PSL Ltd-26th December, 2009

___________________________________________________________________________________________

Firstcall India Equity Advisors Pvt. Ltd 10

SWOT Analysis

Strengths Weakness

• Strong Management

• Strong client base

• Innovative Technology

• Market leadership

• Strong product portfolio

• Geographically located plants

• Falling earnings • High Debt.

Opportunities Threats

• Demand for the line pipes in the US is strong,

especially in the large diameter pipes. Simdex

data suggests that nearly 23% of the total

demand over 2007-2011 is set to emerge

from the pipeline projects in North America.

• The pipeline network in India is

approximately 12,200 km, which is much

below global standards and is on a rapid

growth stage.

• Transportation of oil & gas through pipeline is

also being encouraged globally.

• A recent entrant to the growth drivers of

pipes is the demand arising from the

replacement of old pipelines. More than one

mn miles of gas pipelines out of 1.5 mn miles

in US were laid prior to1975.

• Global Economic Slowdown • Rupee – dollar fluctuation • Price Volatility of HR coils • Raising Steel Prices

PSL Ltd-26th December, 2009

___________________________________________________________________________________________

Firstcall India Equity Advisors Pvt. Ltd 11

Financials Result Updates Quarterly Ended Profit & Loss Account (Standalone)

Value(Rs. in million) 31-Mar-09 31-June-09 30-Sep-09 31-Dec-09E

Description 3m 3m 3m 3m

Net sales 12,310.30 6,332.80 6,062.20 6,668.42

Other income - - - -

Total income 12310.30 6332.80 6062.20 6668.42

Expenditure -11,686.00 -5,589.70 -5,377.30 -5928.22

Operating profit 624.30 743.10 684.90 740.19

Interest -296.6 -230.3 -185.8 -199.23

Gross profit 327.70 512.80 499.10 540.96

Depreciation -138.7 -180.3 -180.9 -183.23

PBT 189.00 332.50 318.20 357.73

Tax -53.00 -107.00 -102.4 -118.05

PAT 136.00 225.50 215.80 239.68

Net profit 136.00 225.50 215.80 239.68

Equity capital 425.8 425.8 523.7 523.7

EPS 3.19 5.30 4.12 4.58

Face Value (Rs) 10.00 10.00 10.00 10.00

Total No. of Shares 42.58 42.58 52.37 52.37

PSL Ltd-26th December, 2009

___________________________________________________________________________________________

Firstcall India Equity Advisors Pvt. Ltd 12

Profit & Loss Account 12 Months Ended on March 31st (Standalone)

Value(Rs. in million) FY08 FY09 FY10E FY11E

Description 12m 12m 12m 12m

Net sales 22188.50 35499.50 28145.23 32367.01

Other income 429.20 - - -

Total income 22617.70 35499.50 28145.23 32367.01

Expenditure -20285.60 -32654.30 -25052.07 -29033.21

Operating profit 2332.10 2845.20 3093.16 3333.80

Interest -578.60 -1007.20 -900.14 -1029.30

Gross profit 1753.50 1838.00 2193.02 2304.50

Depreciation -511.90 -570.70 -627.77 -690.55

PBT 1241.60 1267.30 1565.25 1613.96

Tax -393.90 -408.00 -500.88 -516.47

Net profit 847.70 859.30 1064.37 1097.49

Equity capital 425.80 425.80 523.70 523.70

Reserves 5229.80 5859.30 6923.67 8021.16

EPS 19.91 20.18 20.20 20.96

Face value(Rs) 10.00 10.00 10.00 10.00

Total No. of Shares 42.58 42.58 52.37 52.37

A=Actual E=Estimated

PSL Ltd-26th December, 2009

___________________________________________________________________________________________

Firstcall India Equity Advisors Pvt. Ltd 13

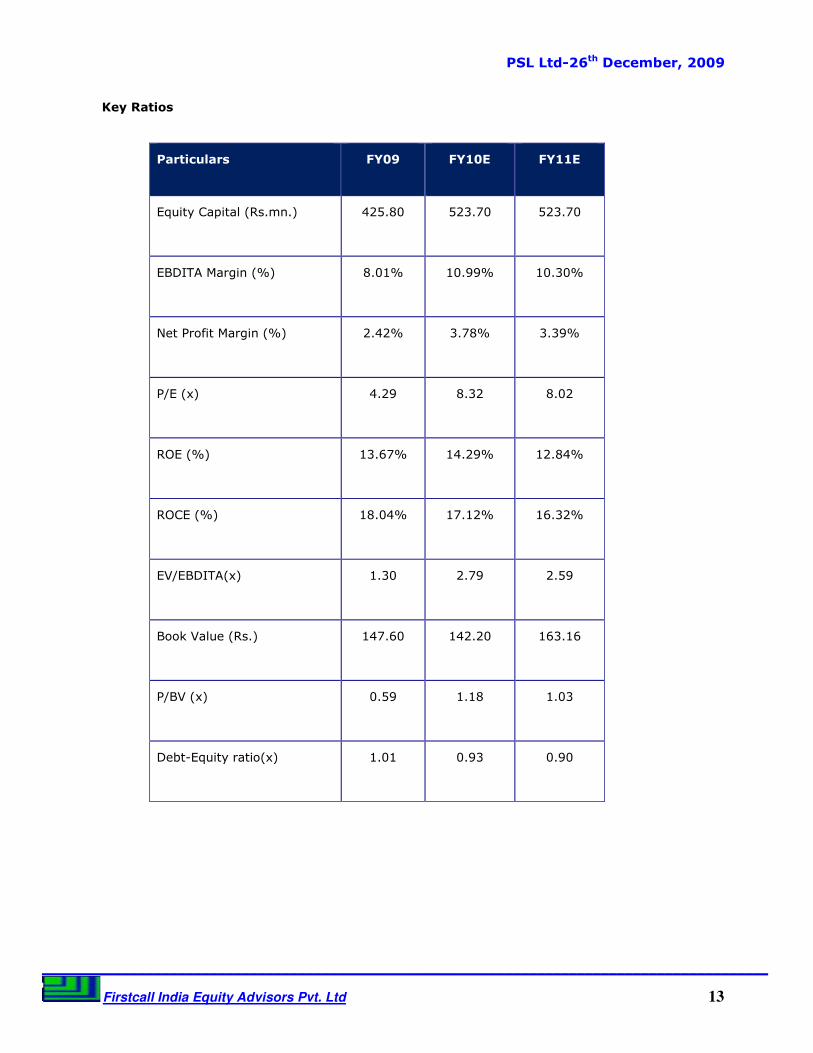

Key Ratios

Particulars FY09 FY10E FY11E

Equity Capital (Rs.mn.) 425.80 523.70 523.70

EBDITA Margin (%) 8.01% 10.99% 10.30%

Net Profit Margin (%) 2.42% 3.78% 3.39%

P/E (x) 4.29 8.32 8.02

ROE (%) 13.67% 14.29% 12.84%

ROCE (%) 18.04% 17.12% 16.32%

EV/EBDITA(x) 1.30 2.79 2.59

Book Value (Rs.) 147.60 142.20 163.16

P/BV (x) 0.59 1.18 1.03

Debt-Equity ratio(x) 1.01 0.93 0.90

PSL Ltd-26th December, 2009

___________________________________________________________________________________________

Firstcall India Equity Advisors Pvt. Ltd 14

Charts A) Net sales & PAT Chart

B) EV/EBITDA chart

PSL Ltd-26th December, 2009

___________________________________________________________________________________________

Firstcall India Equity Advisors Pvt. Ltd 15

C) P/E Chart

D) Debt- Equity ratio chart

PSL Ltd-26th December, 2009

___________________________________________________________________________________________

Firstcall India Equity Advisors Pvt. Ltd 16

Valuation • At the current market price of the stock Rs.168, the stock trades at a P/E of 8.32 x and 8.02 x for FY10E

and FY11E respectively.

• The EPS of the stock is expected to be at Rs.20.20 and Rs.20.96 for the earnings of FY10E and FY11E

respectively.

• The topline and bottom-line of the company are expected to growth a CAGR of 13.41% and 8.99%

respectively over FY08 to FY11E.

• Price to Book Value of the stock is expected to be at 1.16x for FY10E and 1.01 x for FY11E.

• PSL has successfully raised Rs 1493.2mn worth of fresh funds via Qualified Institutional Placement (QIP).

• PSL is likely to diversify into development of special economic zones (SEZ), with the company getting the

stage-1 approval from the Centre to set up an exclusive SEZ for alternative energy and energy ancillaries

at Pipavav in Gujarat.

• PSL is setting up additional capacities of 450,000 TPA of pipe manufacturing which include 225,000 TPA

HSAW pipe mill at Sharjah, UAE and another 225,000 PTA spiral pipe mill project at Vishakhapatnam.

• PSL is likely to diversify into development of special economic zones (SEZ), with the company getting the

stage-1 approval from the Centre to set up an exclusive SEZ for alternative energy and energy ancillaries

at Pipavav in Gujarat.

• Demand for the line pipes in the US is strong, especially in the large diameter pipes. Simdex data

suggests that nearly 23% of the total demand over 2007-2011 is set to emerge from the pipeline projects

in North America

• We recommend ‘HOLD’ in this particular scrip with a target price of Rs.200.00 for Medium to Long term

investment.

PSL Ltd-26th December, 2009

___________________________________________________________________________________________

Firstcall India Equity Advisors Pvt. Ltd 17

Industry overview

The pipe industry is very much dependent on Oil & Gas industry, globally. In the past few years, global

demand for oil and gas continued to rise reflecting the importance of oil and gas in the energy matrix.

Rising crude prices – Increasing E&P activities:

Encouraged by the continuous rising oil prices, Oil & Gas companies in most region of the world continued to

increase their level of spending and drilling activities to offset declining rate of production from the mature oil

& gas fields and to develop new reserves at the most challenging depths and as well as inaccessible and

dense region. Government of India introduced New Exploration and Licensing Policy (NELP) in 1999 to boost

E&P activities in India. The Government has announced eight rounds of NELPs so far. The Government has

announced eight rounds of NELPs so far.

Inter-regional gas supply to boost pipes demand:

The inter-regional gas supply is also expected to be robust. As per the EIA forecast inter-regional gas trade

will expand faster than output and main gas consuming regions will become increasingly dependent on

import. This will result in tight supply of SAW pipes, globally. The Energy Information Administration (EIA)

forecasts natural gas to form 24% of total energy usage by 2030 with the share of oil falling to 34%.

Increased use of natural gas would require building the infrastructure needed to transport the gas from the

point of production to the end users resulting in construction of large diameter pipelines benefiting pipe

manufacturers.

The city gas distribution (CGD) in India is poised to grow with the extension of the project to thirty cities in

different states by 2009 besides Mumbai and Delhi. Currently CGD is operational in Mumbai and Delhi and

several cities in Gujarat. CGD projects are under implementation in more than half a dozen states including

Uttar Pradesh, Rajesthan, Madhya Pradesh, Maharashtra, Karnataka, Kerala, Andhara Pradesh and West

Bangal. As of now CGD accounts for just 5-6% of the total gas consumption at 5-6 mmscmd, which is likely

to grow to 20 mmscmd in next four years.

Replacement demand – USA:

The replacement of the old pipelines in USA is another growth driver. 1.5 mn miles of pipeline is layed in USA

of which more than 1 mn miles pipelines were layed during 1960’s and 1970’s. Considering that the annual

production of pipes have been over 16-17 mn tones, globally, the replacement of pipelines would take around

25 years. India is set to benefit from this demand – supply imbalance. Majority of the growth in the pipe

industry is expected to come from growth in large diameter pipes.

PSL Ltd-26th December, 2009

___________________________________________________________________________________________

Firstcall India Equity Advisors Pvt. Ltd 18

Indian pipe Industry:

Indian pipe industry is among the world’s top three manufacturing hub after Japan and Europe with the size

of over Rs 165 bn (USD 3.37 bn). The Industry is highly capital intensive. Demand scenario for domestic

market is expected to remain firm in the years to come. India has a relatively under developed gas pipeline

infrastructure which is rapidly scaling up in tandem with the burgeoning demand of pipelines. Oil and gas

transportation through pipelines in India is 30% as against 60% in USA and 65% in France. Currently the

country’s gas requirement is fulfilled by pipeline network of GAIL supported by some pipelines of other PSU’s

such as ONGC and GSPL. Recently RIL has also joined the party. The industry have the business potential of

over USD 3.1 bn (USD 80 bn globally)

Outlook:

• Increased economic activities have led to higher demand of energy resources. According to the

International Energy Outlook for 2007 world demand for primary energy will increase by an average of

2.3% p.a. for the period 2004 to 2010.

• Demand of steel pipes is expected to be higher in the medium term on account of increased exploration

activities and thrust to set infrastructure for transportation of oil and gas.

______________________________________________________________________ Disclaimer:

This document prepared by our research analysts does not constitute an offer or solicitation for the purchase

or sale of any financial instrument or as an official confirmation of any transaction. The information contained

herein is from publicly available data or other sources believed to be reliable but we do not represent that it

is accurate or complete and it should not be relied on as such.Firstcall India Equity Advisors Pvt.Ltd. or any of

it’s affiliates shall not be in any way responsible for any loss or damage that may arise to any person from

any inadvertent error in the information contained in this report. This document is provide for assistance only

and is not intended to be and must not alone be taken as the basis for an investment decision.

PSL Ltd-26th December, 2009

___________________________________________________________________________________________

Firstcall India Equity Advisors Pvt. Ltd 19

Firstcall India Equity Research: Email – [email protected]

B. Harikrishna Banking

B. Prathap IT

A. Rajesh Babu FMCG

C.V.S.L.Kameswari Pharma

U. Janaki Rao Capital Goods

E. Swethalatha Oil & Gas

D. Ashakirankumar Automobile

Rachna Twari Diversified

Kavita Singh Diversified

Nimesh Gada Diversified

Priya Shetty Diversified

Tarang Pawar Diversified

Neelam Dubey Diversified

Firstcall India also provides

Firstcall India Equity Advisors Pvt.Ltd focuses on, IPO’s, QIP’s, F.P.O’s, Takeover

Offers, Offer for Sale and Buy Back Offerings.

Corporate Finance Offerings include Foreign Currency Loan Syndications,

Placement of Equity / Debt with multilateral organizations, Short Term Funds

Management Debt & Equity, Working Capital Limits, Equity & Debt

Syndications and Structured Deals.

Corporate Advisory Offerings include Mergers & Acquisitions (domestic and

cross-border), divestitures, spin-offs, valuation of business, corporate

Restructuring-Capital and Debt, Turnkey Corporate Revival – Planning &

Execution, Project Financing, Venture capital, Private Equity and Financial

Joint Ventures

Firstcall India also provides Financial Advisory services with respect to raising

of capital through FCCBs, GDRs, ADRs and listing of the same on International

Stock Exchanges namely AIMs, Luxembourg, Singapore Stock Exchanges and

Other international stock exchanges.

For Further Details Contact:

3rd Floor, Sankalp, The Bureau, Dr.R.C.Marg, Chembur, Mumbai 400 071

Tel.: 022-2527 2510/2527 6077/25276089 Telefax: 022-25276089

E-mail: [email protected]