Business Energy Efficiency Tax Review One Year On

19

THE BUSINESS ENERGY TAX REVIEW – ONE YEAR ON November 2016

-

Upload

emex -

Category

Engineering

-

view

92 -

download

0

Transcript of Business Energy Efficiency Tax Review One Year On

THE BUSINESS ENERGY TAX REVIEW – ONE YEAR ON

November 2016

The review process

• Summer Budget 2015:

• Announced review to consider approaches to simplify and improve effectiveness of regime

• Consultation:

• Informally, and then formally between September & November 2015:

• Simplifying and improving effectiveness

• Reporting of energy & carbon

• Protecting the competitiveness of Energy Intensive Industries

• Incentivising energy efficiency and carbon reduction

• Impacts on public and third sector

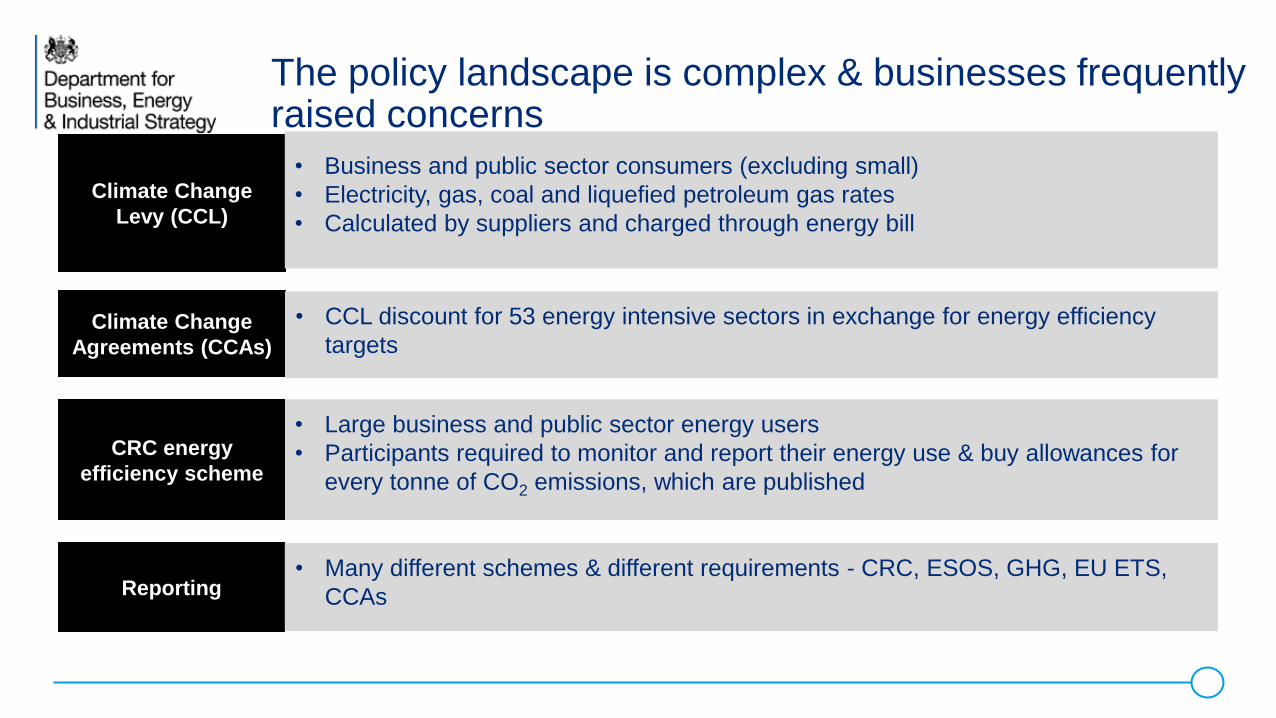

The policy landscape is complex & businesses frequently raised concerns

Climate Change

Levy (CCL)

• Business and public sector consumers (excluding small)

• Electricity, gas, coal and liquefied petroleum gas rates

• Calculated by suppliers and charged through energy bill

CRC energy

efficiency scheme

• Large business and public sector energy users

• Participants required to monitor and report their energy use & buy allowances for

every tonne of CO2 emissions, which are published

Reporting • Many different schemes & different requirements - CRC, ESOS, GHG, EU ETS,

CCAs

Climate Change

Agreements (CCAs)

• CCL discount for 53 energy intensive sectors in exchange for energy efficiency

targets

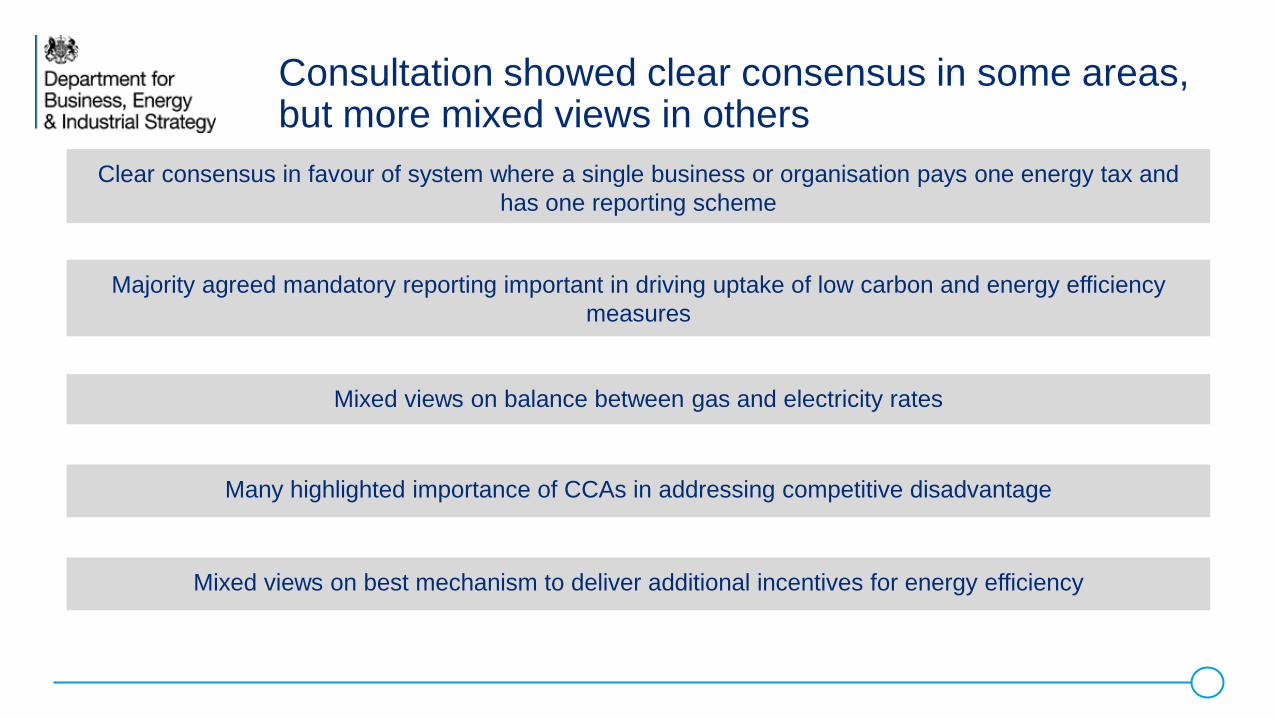

Consultation showed clear consensus in some areas, but more mixed views in others

Clear consensus in favour of system where a single business or organisation pays one energy tax and

has one reporting scheme

Majority agreed mandatory reporting important in driving uptake of low carbon and energy efficiency

measures

Mixed views on balance between gas and electricity rates

Mixed views on best mechanism to deliver additional incentives for energy efficiency

Many highlighted importance of CCAs in addressing competitive disadvantage

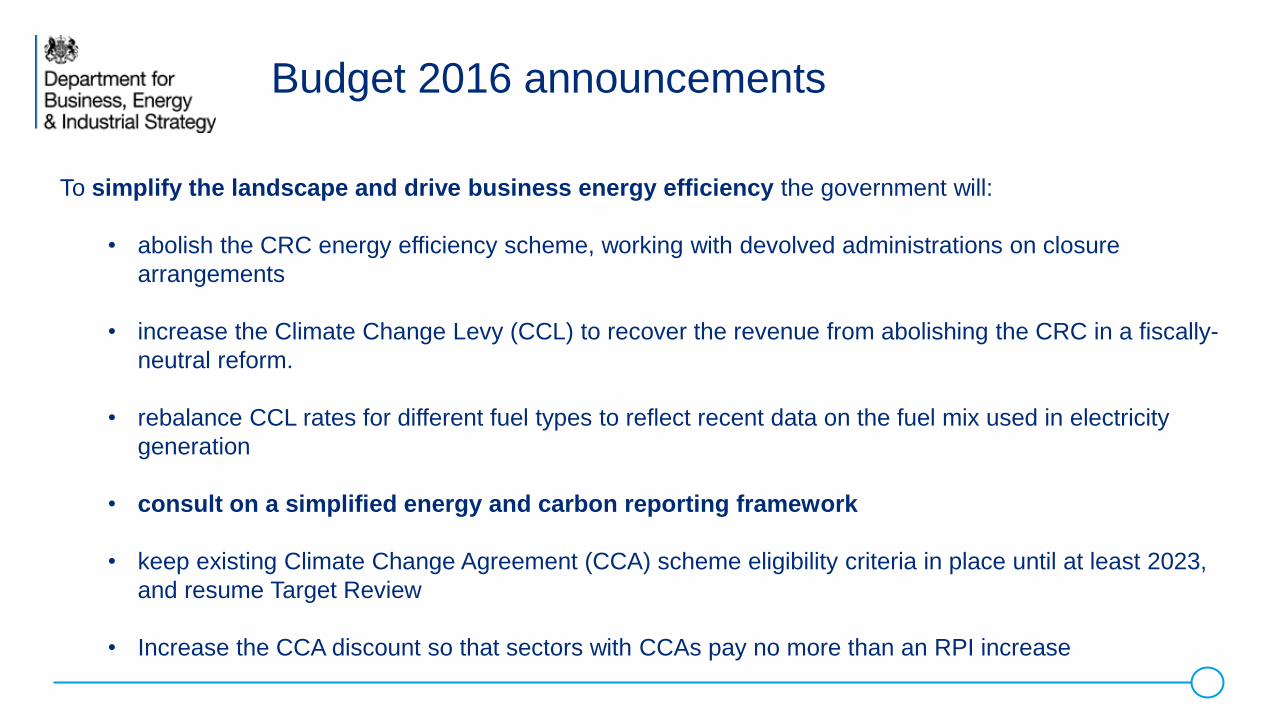

Budget 2016 announcements

To simplify the landscape and drive business energy efficiency the government will:

• abolish the CRC energy efficiency scheme, working with devolved administrations on closure

arrangements

• increase the Climate Change Levy (CCL) to recover the revenue from abolishing the CRC in a fiscally-

neutral reform.

• rebalance CCL rates for different fuel types to reflect recent data on the fuel mix used in electricity

generation

• consult on a simplified energy and carbon reporting framework

• keep existing Climate Change Agreement (CCA) scheme eligibility criteria in place until at least 2023,

and resume Target Review

• Increase the CCA discount so that sectors with CCAs pay no more than an RPI increase

Machinery of Government…..

• The Department brings together responsibilities for business, industrial strategy, science, innovation, energy, and climate change

We are responsible for:

• developing and delivering a comprehensive industrial strategy and leading the government’s relationship with business

• ensuring that the country has secure energy supplies that are reliable, affordable and clean

• ensuring the UK remains at the leading edge of science, research and innovation

• tackling climate change

BEIS announcements

• Carbon Budgets

• CfDs

• Smart Energy call for evidence

• Heat Networks Investment Project

• Non-financial reporting

• CCA Target and Buy-Out review

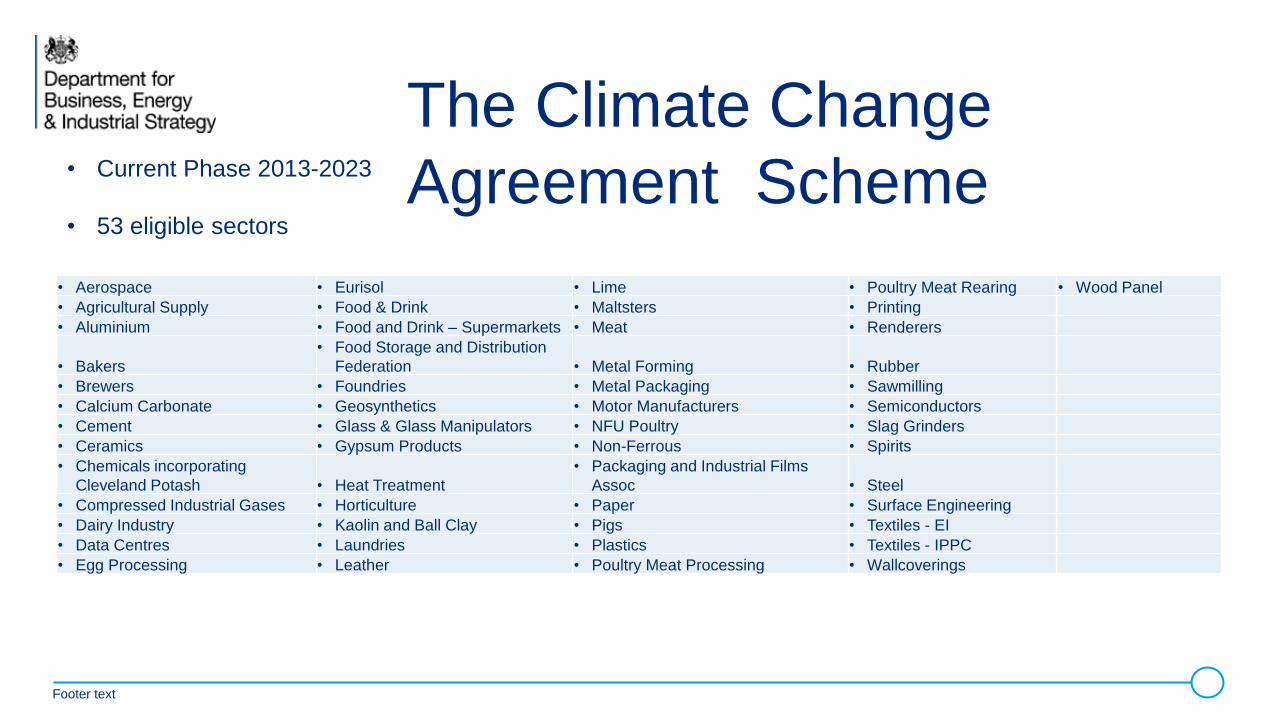

The Climate Change

Agreement Scheme • Current Phase 2013-2023

• 53 eligible sectors

• Aerospace • Eurisol • Lime • Poultry Meat Rearing • Wood Panel

• Agricultural Supply • Food & Drink • Maltsters • Printing

• Aluminium • Food and Drink – Supermarkets • Meat • Renderers

• Bakers

• Food Storage and Distribution

Federation • Metal Forming • Rubber

• Brewers • Foundries • Metal Packaging • Sawmilling

• Calcium Carbonate • Geosynthetics • Motor Manufacturers • Semiconductors

• Cement • Glass & Glass Manipulators • NFU Poultry • Slag Grinders

• Ceramics • Gypsum Products • Non-Ferrous • Spirits

• Chemicals incorporating

Cleveland Potash • Heat Treatment

• Packaging and Industrial Films

Assoc • Steel

• Compressed Industrial Gases • Horticulture • Paper • Surface Engineering

• Dairy Industry • Kaolin and Ball Clay • Pigs • Textiles - EI

• Data Centres • Laundries • Plastics • Textiles - IPPC

• Egg Processing • Leather • Poultry Meat Processing • Wallcoverings

Footer text

Buy-out Price Review Set in 2012 for TP1 (2013-14) and TP2 (2015-16) at £12/tCO2e

CCA Target Review and Buy-out Review Stakeholder Engagement

• increase to £17/tCO2e for TP3 (2017-18) and TP4 (2019-20) Option 1

• increase to £14/tCO2e for TP3 and 4 Option 2 - preferred

• retain present price of £12/tCO2e for TP3 and 4 Option 3

Buy-out Price Review Option 1 - Increase to £17/tCO2e, broadly in line with published 2017/18 CRC allowance prices

Footer text

2012-

2013

2013-

2014

2014-

2015

2015-

2016

2016-

2017

2017-

2018

2018-

2019

CRC

Prices

£/tCO2:

12.00 12.00

Forecast

price 15.60 15.60 16.10 16.60 17.20

Buy-to-

comply

price

16.40 16.90 17.20 17.70 18.30

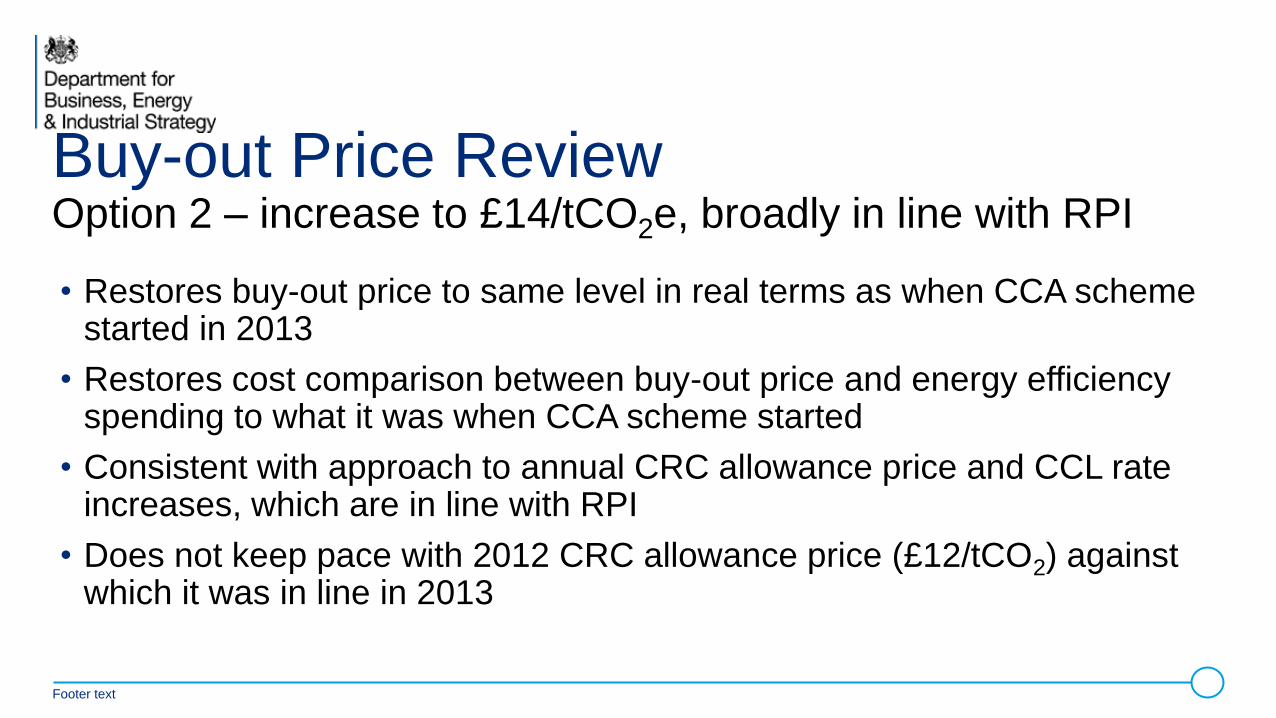

Buy-out Price Review Option 2 – increase to £14/tCO2e, broadly in line with RPI

• Restores buy-out price to same level in real terms as when CCA scheme started in 2013

• Restores cost comparison between buy-out price and energy efficiency spending to what it was when CCA scheme started

• Consistent with approach to annual CRC allowance price and CCL rate increases, which are in line with RPI

• Does not keep pace with 2012 CRC allowance price (£12/tCO2) against which it was in line in 2013

Footer text

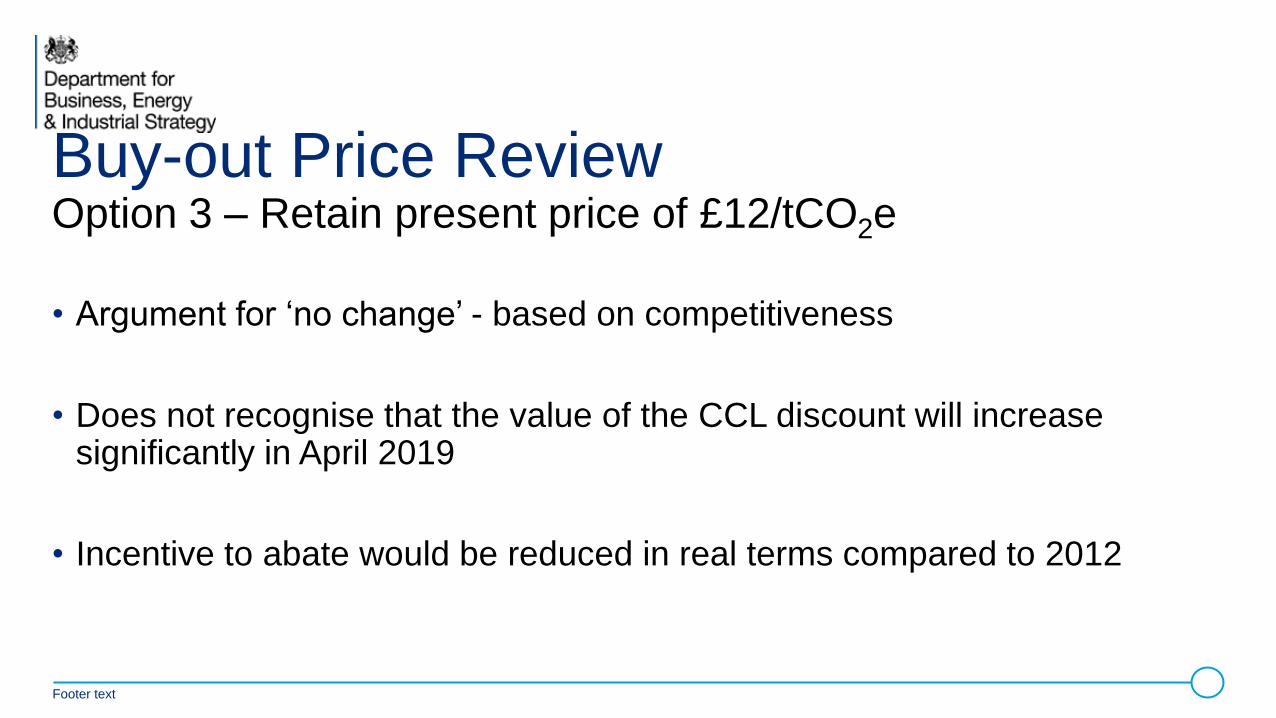

Buy-out Price Review Option 3 – Retain present price of £12/tCO2e

• Argument for ‘no change’ - based on competitiveness

• Does not recognise that the value of the CCL discount will increase significantly in April 2019

• Incentive to abate would be reduced in real terms compared to 2012

Footer text

Discussion Paper – Key Dates

• Published/Start date for responses - Friday 5th August 2016

• End date for responses - Friday 23rd September 2016

Footer text

Objectives of CRC

• Fill gap in policy incentives for large energy users in businesses and public sector outside the energy intensives regulated by EU

ETS and CCAs

• Address the barriers to uptake of Energy Efficiency identified by the Carbon Trust (2005):

insufficient financial incentives to reduce emissions;

uncertain reputational benefits of demonstrating leadership;

split incentives within and between organisations (e.g. between landlords and tenants);

organisational inertia.

“Despite the cost effective energy efficiency savings available to large public and private sector organisations, their emissions have

remained more or less constant for the last twenty years.”

14 D

CRC: Who is covered?

• Organisations that used 6000 MWh or more of electricity in the qualification year

• Targets large non-energy intensive organisations not covered by the EU ETS or CCA who typically spend at least £0.5 million a year on electricity

• Around 1800 to 2000 participants, UK wide scheme

• 10% of the UK’s greenhouse gas emissions covered

• Energy covered by CCA or EU ETS does not count in CRC qualification / reporting

15 D

Energy Savings Opportunity Scheme • What is ESOS?

• UK-wide mandatory energy measurement and auditing scheme

• Introduced in response to EU Energy Efficiency Directive – aims to help achieve latent cost-effective energy efficiency potential

• Who must comply?

• Large undertakings and large corporate groups across the UK.

• Target highest UK-parent but allow disaggregation

• And by when?

• Initial qualification date - 31 December 2014

• Initial compliance date – 5 December 2015

• Audits must be repeated every four years (i.e. second phase ends 2019)

• Over 90% compliance - EA emphasis now is to confirm the qualification status of organisations and if applicable, take enforcement action to bring them into compliance

• Now evaluating first implementation phase

Energy Savings Opportunity Scheme - Emerging Thinking

Conducting an ESOS assessment

Energy Savings Opportunity Scheme

1. Measure energy use

3. Evaluate opportunities

4. Store data and notify scheme

administrator

5. Implement savings, and

further disclosure (e.g. in annual

report)

2. Identify energy efficiency and

energy management opportunities

Mandatory

Voluntary

Routes to compliance

Energy Savings Opportunity Scheme

ESOS compliant organisation

Previous activity that meets ESOS

standards

DECs / Green Deal

Assessments

ISO 50001

• ISO50001

• Display Energy Certificates

• Previous audits to ESOS standards

And…

• ESOS compliant energy assessments

(either conducted in-house or by

external assessor)

Aim: New framework will reduce the administrative burdens of an overlapping system while improving the

incentive for organisations to save energy and reduce carbon emissions.

Key considerations:

• UK-wide approach e.g. reflecting devolved nature of some schemes

• Mandatory, annual reporting

• Who:

o all large UK businesses (ESOS qualification criteria?),

o &/or apply appropriate thresholds (de minimis arrangements) to focus scheme on higher energy consuming organisations & protect smallest/ lowest energy consumers?

o Equivalent / similar obligations on large public sector / third sector organisations

• Scope - e.g. inclusion of transport / ”grey fleet” / implementation of ESOS audits

• Board/ senior level sign-off, with some public disclosure

• Continued reporting of global GHG emissions by UK quoted companies

• How – annual reports v central IT system

• Will look to streamline data collection and reporting requirements as far as possible

19

Reforming the business energy tax landscape

New Reporting Framework