Chief Meaning Officer: Tangible Ways to Create Intangible Value

date post

21-Dec-2015Category

view

219download

2

BUS780

Chapter 8

Long-Lived Tangible and Intangible Assets: The Source of

Operating Capacity

Long-Lived Tangible and Intangible Assets2

Long-Lived Operational Assets

Long-lived operational assets include: Tangible Assets: land, buildings,

factory plants, computers, machinery, etc. Intangible assets: patents, copyrights,

franchises, goodwill, organization costs, trade names, trademarks, etc.

Natural Resources: oil and gas reserves, timber, mineral deposits.

Long-Lived Tangible and Intangible Assets3

Tangible Assets: Property, Plant and Equipment (PPE)

Tangible assets are productive assets deriving their value from the use of them in operations.

Tangible assets are:Assets used in operations (not for

resale).Long-term in Nature (Economic Life >

one year).Possess physical substance.$ must be material.

Long-Lived Tangible and Intangible Assets4

Intangible Assets

Assets --

a. with future economic benefits,

b. no physical substance,

c. with high degree of uncertainty concerning the future benefit.

Long-Lived Tangible and Intangible Assets5

Objectives of the Chapter

1. To understand the concept of expensing versus capitalizing expenditures.

2. To learn the valuation of long-lived assets at acquisition.

3. To learn the cost allocation process of long-lived assets after acquisition (i.e., depreciation, amortization) including changes in estimates of depreciation.

Long-Lived Tangible and Intangible Assets6

Objectives of the Chapter (Contd.)

4. To learn the accounting treatment for asset impairment of long-lived assets.

5. To understand the accounting treatment for the disposition of long-lived assets.

Long-Lived Tangible and Intangible Assets7

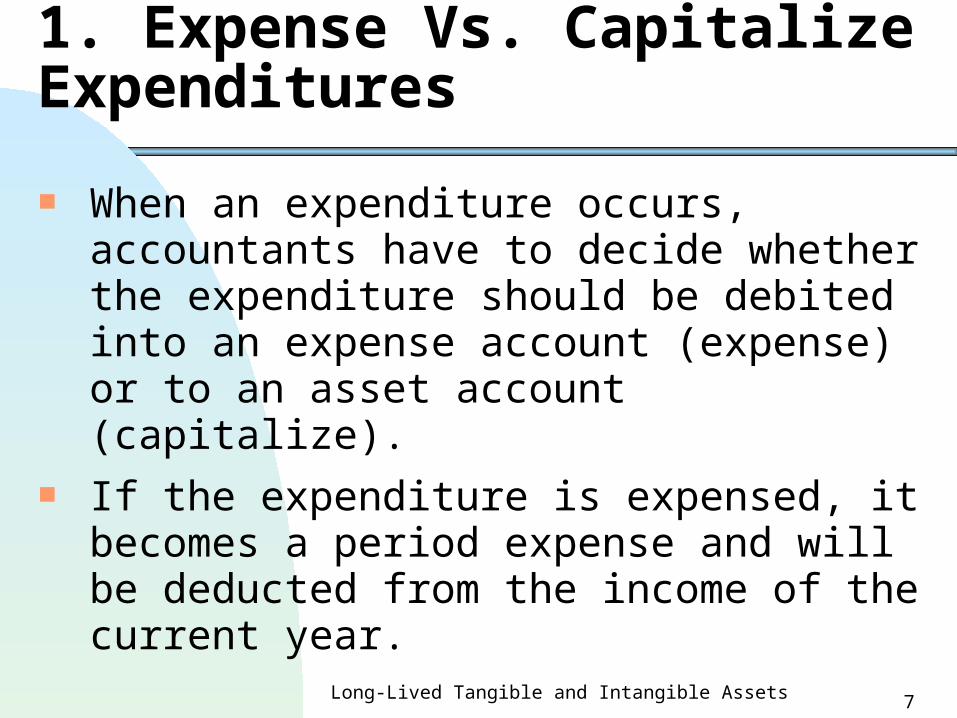

1. Expense Vs. Capitalize Expenditures

When an expenditure occurs, accountants have to decide whether the expenditure should be debited into an expense account (expense) or to an asset account (capitalize).

If the expenditure is expensed, it becomes a period expense and will be deducted from the income of the current year.

Long-Lived Tangible and Intangible Assets8

Expense Vs. Capitalize Expenditures (Contd.)

Expense an expenditure may have tax benefit (thus, increase cash flows) if it is tax deductible but it will reduce the current year’s income.

If an expenditure is capitalized, it will be reported on the balance sheet as an asset and will be subject to depreciation or amortization in the future years.

Long-Lived Tangible and Intangible Assets9

Expense Vs. Capitalize Expenditures (contd.)

The Impact of expenditure capitalization: a. The expenditure will be recognized as

an asset and will not reduce current year’s income.

b. the cost allocation of the asset over the life of the asset (i.e., depreciation expense) will reduce future year’s income.

Long-Lived Tangible and Intangible Assets10

Improper Capitalization Examples- WorldCom

“WorldCom Inc. consistently met Wall Street's targets for earnings during 2000 and the first three quarters of 2001. But the company now says it improperly capitalized $3.8 billion dollars of expenses to inflate profits, in what could be the largest accounting fraud ever.”

(Wall Street Journal, 8/5/2002)

Long-Lived Tangible and Intangible Assets11

Improper Capitalization – WorldCom (Contd.)

According to Stickney and Weil (2006), the impact of the improper capitalization of costs that WorldCom paid to other carriers of the telecommunication lines results in an increase of earnings by $53.1 billion and $17.1 billion in 2000 and 2001, respectively.

The restated earnings of WorldCom indicated a net loss of $48.9 billion and $15.6 billion for 2000 and 2001, respectively.

Long-Lived Tangible and Intangible Assets12

Improper Capitalization- Global Crossing

(WSJ, 7/1/2002)

Mr. Olofson's (Finance Executive of Global Crossing) August, 2001 letter says the company may have improperly capitalized the real-estate lease on its Madison, N.J., headquarters building.”

Long-Lived Tangible and Intangible Assets13

Improper Capitalization -Global Crossing (contd.)

"This is just another example of Global Crossing's methods of meeting its numbers,…," said Paul Murphy, his attorney at O'Neill Lysaght & Sun. “

“ Global Crossing also used “swap” transactions (i.e., trading same amounts of telecom capacity with another telecom corp. and recorded the trade as revenue and the costs as capital expenditures).”

Long-Lived Tangible and Intangible Assets14

Accounting Scandals-Time Warner (WSJ, 3/22/2005)

“the SEC found that AOL had improperly capitalized certain advertising costs that should have been expensed, inflating revenue for six of eight quarters in fiscal 1995 and 1996.”

“The Securities and Exchange Commission slapped Time Warner Inc. with a $300 million fine, its second-biggest fine in history.”

Long-Lived Tangible and Intangible Assets15

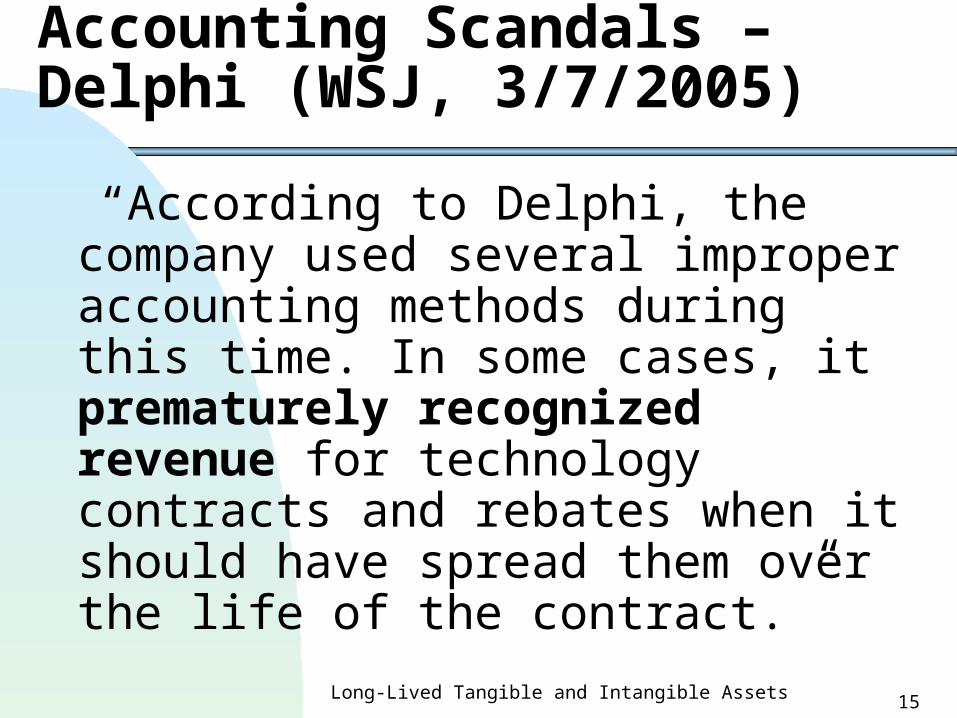

Accounting Scandals –Delphi (WSJ, 3/7/2005)

“According to Delphi, the company used several improper accounting methods during this time. In some cases, it prematurely recognized revenue for technology contracts and rebates when it should have spread them over the life of the contract.”

Long-Lived Tangible and Intangible Assets16

Accounting Scandals –Delphi (Cont.)

“Other times it improperly capitalized expenses over time, rather than recognizing them immediately. It also boosted cash flow from operations and pretax earnings by claiming it sold assets and inventory that it had actually agreed to buy back later.”

Long-Lived Tangible and Intangible Assets17

Treatment of Expenditures with Potential Long-Term Benefit – Acquired Externally

Tangible IntangibleLand, Building Patent (a) (Merck, expl. 6) Equipment (asset) Copyright (a) Goodwill (a) Trade name (a) Proved technologies (a) In-Process technologies (e)a = asset; e = expense (Merck, expl. 9 on p370)(source: figure 8.3 of textbook)

Long-Lived Tangible and Intangible Assets18

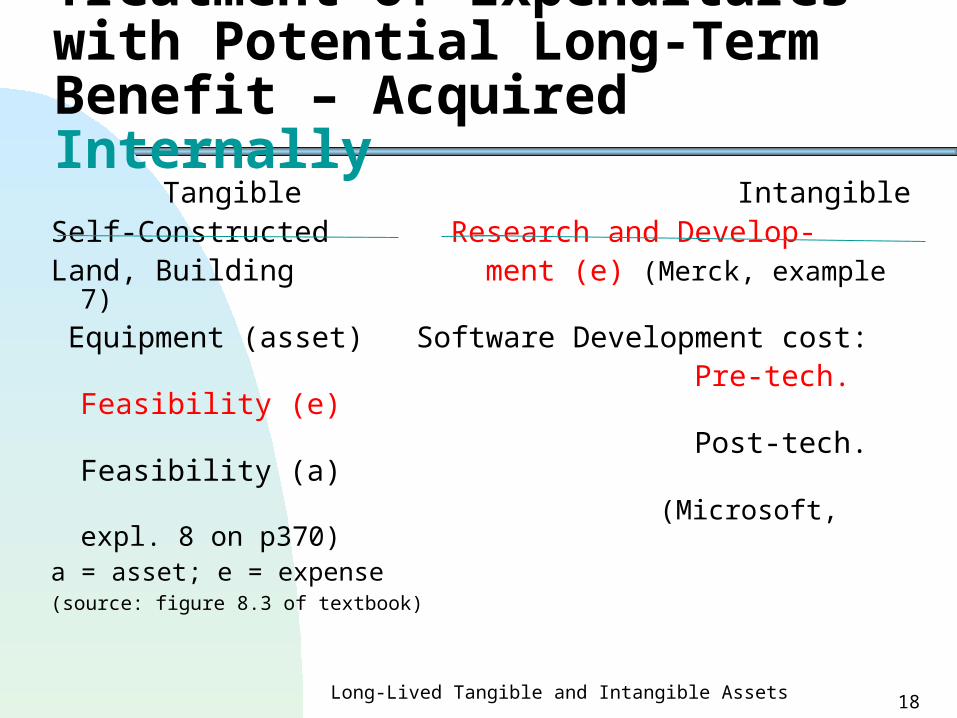

Treatment of Expenditures with Potential Long-Term Benefit – Acquired Internally

Tangible IntangibleSelf-Constructed Research and Develop-Land, Building ment (e) (Merck, example 7) Equipment (asset) Software Development cost: Pre-tech. Feasibility (e) Post-tech. Feasibility (a) (Microsoft, expl. 8 on p370)a = asset; e = expense (source: figure 8.3 of textbook)

Long-Lived Tangible and Intangible Assets20

Cost of PPE (contd.)

PPE (except for land) is subject to depreciation.

Depreciation is a process of cost allocation, not a process of asset valuation.

If the acquisition cost or the self-constructed cost is greater than the market value at time of delivery, Lower of cost or market is applied (see Wal-Mart, expl. 5 on p370).

Long-Lived Tangible and Intangible Assets21

Determination of Acquisition Cost

Cost of Land Cost of Buildings Cost of Equipment Cost of Self-Constructed Assets

Long-Lived Tangible and Intangible Assets22

Cost of Land(held for operation, not for resale)

Any cost occurred before the land is ready for its intended use should be capitalized as cost of land.

Long-Lived Tangible and Intangible Assets23

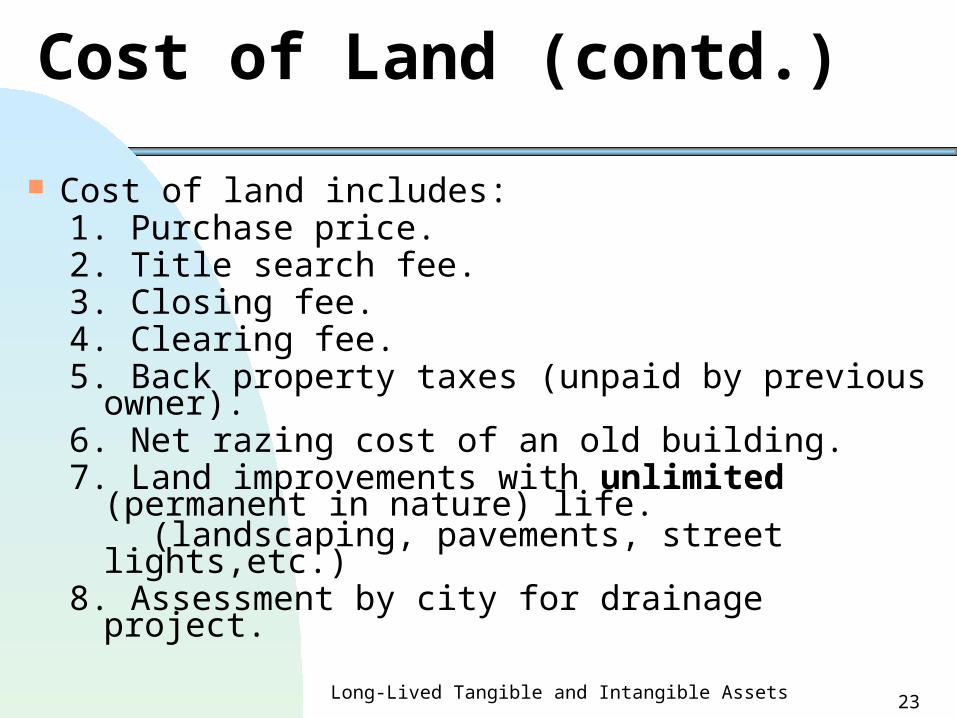

Cost of Land (contd.)

Cost of land includes:1. Purchase price.2. Title search fee.3. Closing fee.4. Clearing fee.5. Back property taxes (unpaid by previous

owner).6. Net razing cost of an old building.7. Land improvements with unlimited

(permanent in nature) life. (landscaping, pavements, street lights,etc.)8. Assessment by city for drainage project.

Long-Lived Tangible and Intangible Assets24

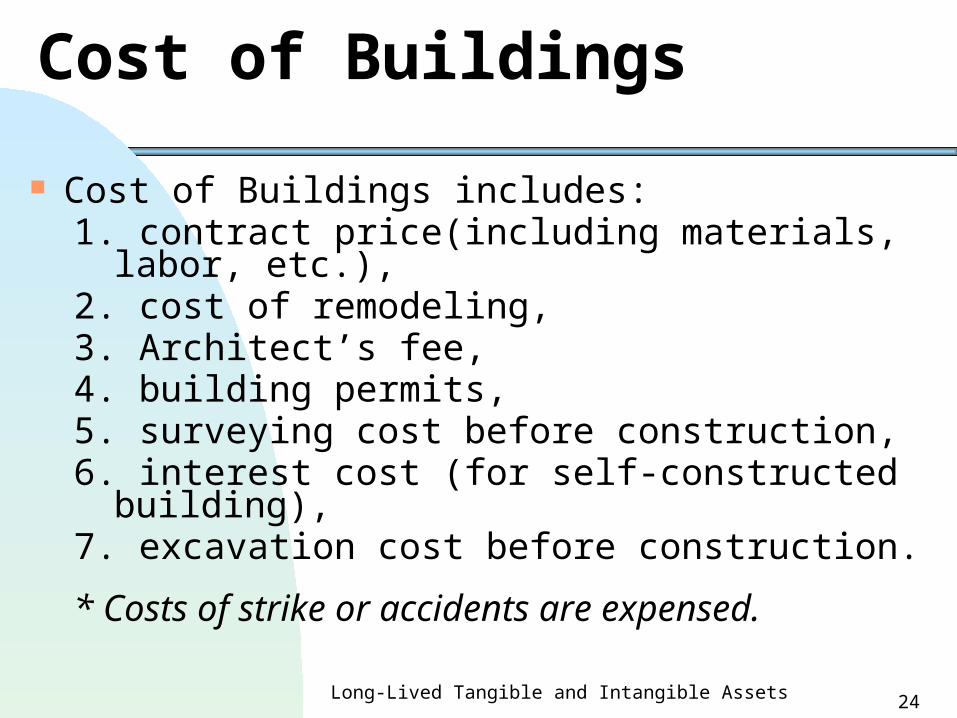

Cost of Buildings

Cost of Buildings includes:1. contract price(including materials, labor,

etc.),2. cost of remodeling,3. Architect’s fee,4. building permits,5. surveying cost before construction,6. interest cost (for self-constructed building),7. excavation cost before construction.

* Costs of strike or accidents are expensed.

Long-Lived Tangible and Intangible Assets25

Cost of Equipment

Any cost occurred to acquire and to bring the equipment to the location and condition for its intended use.

Long-Lived Tangible and Intangible Assets26

Cost of Equipment (contd.)

Cost of Equipment includes:1. purchase price,2. freight-in,3. insurance in transit, and4. foundation cost, installation cost, cost of

test runs and assembling cost. Not including: Cash discount lost,

unnecessary storage cost and hauling charges from storage for delivery of equipment.

Long-Lived Tangible and Intangible Assets27

Example 12 on p372 of the textbook

General Motors incurs the following costs in searching and acquiring the land and building:

1. Purchase price of land and building, $1,000,000.2. Fees paid to lawyers related to the purchase,

$10,000.3. Transfer taxes paid to the city, $2,000.4. Salaries earned by management personnel

during the search for the site and the negotiation of its purchase, $8,000.

Long-Lived Tangible and Intangible Assets28

Example (contd.)

5. Operating expenditures for company automobiles used during the search, $75.

6. Depreciation charges for company automobiles used during the search, $65.

7. Fees paid to engineer for a repot on the structural soundness of the building, $15,000.

8. Uninsured costs to repair automobiles damaged in an car accident during the search, $3,000.

9. Profits lost on sales the company failed to make because, during the search, management paid insufficient attention to a potential new customer, $20,000.

Long-Lived Tangible and Intangible Assets29

Example (contd.)

What is the cost of land and Building? Cost of both land and building: items 1

to 6 Cost of building: item 7 Items 8 and 9 ?

Cost of both land and building should be allocated to cost of land and cost of building, respectively, based on the relative market value of land and building.

Long-Lived Tangible and Intangible Assets30

Cost Allocation of a Lump Sum Purchase – An Example A building and land were purchased at

$100,000. The market value of building and land was $30,000 and $90,000, respectively.

Building 25,0001

Land 75,0002

Cash 100,0001. 30,000/(30,000+90,000)=25%, 25%x100,000 = 25,0002. 90,000/(30,000+90,000)=75%, 75%x100,000 = 75,000

Long-Lived Tangible and Intangible Assets31

Cost of Self-Constructed (S-C) Assets

Cost of self-constructed assets includes:1. direct materials,2. direct labor,3. factory overhead (variable overhead

and fixed overhead).

Long-Lived Tangible and Intangible Assets32

Interest Costs During Construction

Background of SFAS No. 34 (effective in 1979)

Only capitalize the interest on funds borrowed for construction.

Long-Lived Tangible and Intangible Assets33

Interest Costs During Construction (contd.)

Interest can only be capitalized for qualifying assets which must meet the following criteria:

1. Assets are constructed for firm’s own use or constructed as discrete projects for sale or lease to others (i.e., ships, real estate developments).

2. Capitalization will make a difference on the earnings per share.

Long-Lived Tangible and Intangible Assets34

Interest Costs During Construction (contd.) Capitalization period:

Starting when:1. Expenditures for the assets have been

made;2. Construction activities are in progress;

and3. Interest cost is being occurred.

Ending when: Assets are substantially completed and

ready for intended use.

Long-Lived Tangible and Intangible Assets35

Example – interest capitalization for self-constructed asset

The labor, material and overhead totaled $2,400,000 for the construction of a building in 2006. In addition, during 20X6, total interest expense was $1,845,000 of which $159,500 was capitalized as the cost of the self-constructed building and $1,685,500 was charged to expense.

Long-Lived Tangible and Intangible Assets36

Example (contd.)

Journal entry to record the construction costs and interest expense for 20x6 is:

Building 2,559,500Interest Expense 1,685,500

Cash4,245,000

Long-Lived Tangible and Intangible Assets37

Example (contd.)

Reporting: Income Statement (for the year ended 12/31/x6) Other Revenues & Expenses:

Interest Expenses $1,845,000 Less: Capitalized Int. (159,500)

$ 1,685,500 Notes:Accounting PolicyCapitalized interest: during 20X6, total interest

expense was $1,845,000 of which $159,500 was capitalized and $1,685,500 was charged to expense.

Long-Lived Tangible and Intangible Assets38

Acquisition Cost for Intangibles

Acquisition cost plus any other costs that are necessary to make the intangible assets ready for the intended uses (i.e., purchase price, legal fees,…)

If intangible assets are developed internally, all the R&D costs are expensed.

Long-Lived Tangible and Intangible Assets39

3. Cost Allocation of Long-Lived Assets Over the Life of the Assets

A firm consumes the services of long-lived assets to generate revenue, the cost of these assets should be expensed over time to match the revenue generated (in compliance with the matching principle).

The process of allocating the depreciable cost (cost – the salvage value) of assets over the estimated economic life is called depreciation (amortization) for tangible (intangible) assets.

Long-Lived Tangible and Intangible Assets40

Cost Allocation of Long-Lived Assets Over the Life of the Assets (contd.)

For intangible assets, the salvage value is zero.

For tangible assets, the salvage value could be either positive, zero or even negative (i.e., dismantling a nuclear power plant).

Long-Lived Tangible and Intangible Assets41

Depreciation and Earnings Quality

The estimation of service life and salvage value is at the discretion of managers (see the case of Waste Management on p378).

The choice of depreciation method is also at the discretion of mangers.

Earnings would be affected when different depreciation methods or different estimates were used.

Long-Lived Tangible and Intangible Assets42

Depreciation Methods (For Financial Reporting Purposes)

1. Time-based methods (time-based)a. Straight-Line.b. Sum-of-the-Years’-Digits (SYD).c. Declining-Balance.

2. Activity-based method (activity-based)

Unit-of-Production.

Note: SYD and Declining balance methods are accelerated depreciation Methods.

Long-Lived Tangible and Intangible Assets43

Straight-Line Method Cost is allocated evenly through the life of the P.P.E. Example 1: Machine costing $10,000 was purchased on

1/1/x1. The estimated residual value of the machine is $2,000 and the estimated life of the machine is 4 years.Depreciation Expense per year:($10,000 - 2,000)/ 4 = $2,000

12/31/x1 Depreciation Expenses 2,000Accumulated Depreciation

2,000

Long-Lived Tangible and Intangible Assets44

Straight-Line Method (contd.) Example 2 (partial year depreciation): Using the

information in example 1, except that the machine was purchased on 3/11/x1 rather than 1/1/x1.

Depreciation Expense of year x1 ==> [($10,000-2,000)/4] x (10/12) = $1,667

Year Depr. Exp Acc. Depr.x1 1667 (10 months) 1,667x2 2000 (12 months) 3,667x3 2000 (12 months) 5,667x4 2000 12 months) 7,667x5 333 (2 months) 8,000

Long-Lived Tangible and Intangible Assets45

Sum-of-the-Years’-Digits (SYD)

Example : Machine costing $10,000 was purchased on 1/1/x1 with an estimated residual value of $2,000 and an estimated life of 4 years.

Depr. **Book ValueYear *Depr. Base Fraction Expense at the end x1 $8,000 4/10 $3,200 6,800 x2 $8,000 3/10 $2,400 4,400 x3 $8,000 2/10 $1,600 2,800 x4 $8,000 1/10 $800 2,000

* Depr. Base= Cost - Residual Value** Book Value= Cost - Acc. Depreciation

Long-Lived Tangible and Intangible Assets46

Declining-Balance Method

Depreciation Exp.= constant rate book value at the beginning of the period Residual value is not considered in the

computation. Assets cannot be depreciated below the

residual value. The constant rate is expressed as a

function of a straight-line annual depreciation rate.

Long-Lived Tangible and Intangible Assets47

Double Declining-Balance Method

Example : Machine costing $10,000 purchased on 1/1/x1, with a residual value of $2,000 and an estimated life of 4 years. A double declining-balance method is used to depreciate the machine. Thus, the constant rate is twice of the S-L Depr. Rate (2 x 25% = 50%).

Long-Lived Tangible and Intangible Assets48

Double Declining-Balance Method

Example (contd.)Book Value

of Assetat Beg. of Constant Depr. Book Value

Year the Year Rate Exp. At the End

x1 $10,000 50% $5,000 $5,000 x2 $5,000 50% 2,500 2,500 x3 $2,500 50% 500* 2,000* x4 2,000 50% 0 2,000

*Assets cannot be depreciated below the residual value.

Long-Lived Tangible and Intangible Assets49

A Comparison of Depreciation Methods

Assuming expected life = 4 years

1. Straight-Line Method2. S-Y-D Method3. Declining-Balance Method

Year

Depreciation Expense

123

Long-Lived Tangible and Intangible Assets50

Income Tax Depreciation: MACRS

Modified Accelerated Cost Recovery System (MACRS) is used to compute tax depreciation expense for assets purchased in or after 1987.

MACRS was enacted by Congress in the Tax Reform Act of 1986. Assets are classified in 8 property classes.

A specified GAAP depreciation method is used in computing the depreciation expense for all classes (i.e., for a 3-year life PPE, DDB is used).

Long-Lived Tangible and Intangible Assets51

MACRS Depreciation Rate MACRS DEPR. RATES BY CLASS OF PROPERTY .

Re-covery 3-year 5-year 7-year 10-year

15-year 20-year Year (200% DB) (200% DB) (200% DB)

(200% DB) (150% DB) (150% DB) 1 33.33 20.00 14.29 10.00 5.00 3.750 2 44.45 32.00 24.49 18.00 9.50 7.219 3 14.81* 19.20 17.49 14.40 8.55 6.677 4 7.41 11.52* 12.49 11.52 7.70 6.177 5 11.52 8.93* 9.22 6.93 5.713 6 ……….. 5.76 8.92 7.37 6.23 5.285 7 8.93 6.55* 5.90*4.888 8 4.46 6.55 5.90 4.522 9 6.56 5.91 4.462*

* Switchover to straight-line depreciation.51

Long-Lived Tangible and Intangible Assets52

MACRS Depreciation Rate (Contd.) Re-covery 3-year 5-year 7-year 10-year 15-year 20-year

Year (200% DB) (200% DB) (200% DB) (200% DB) (150% DB) (150% DB) 10 6.55 5.90 4.46111 ……………………………… 3.28 5.91 4.46212 5.90 4.46113 5.91 4.46214 5.90 4.46115 5.91 4.46216 2.95 4.46117 4.46218 4.46119 4.46220 4.46121 2.231

52

Long-Lived Tangible and Intangible Assets53

Amortization of Intangibles

Amortization: a cost allocation of intangibles with finite lives (i.e., patents, copyrights) over the estimated life of intangibles.

Current Practice: to amortize over the shorter of the legal or useful life, not to exceed 40 years

No amortization for trade names, trademarks and goodwill.

Long-Lived Tangible and Intangible Assets54

Amortization Method

Straight-line method (unless the company can prove other methods are more appropriate)

Residual value is, in general, zero and partial year amortization applied

Journal entry for amortization:Amortization Expense xxx

Intangible Asset xxx(i.e., patents).

Long-Lived Tangible and Intangible Assets55

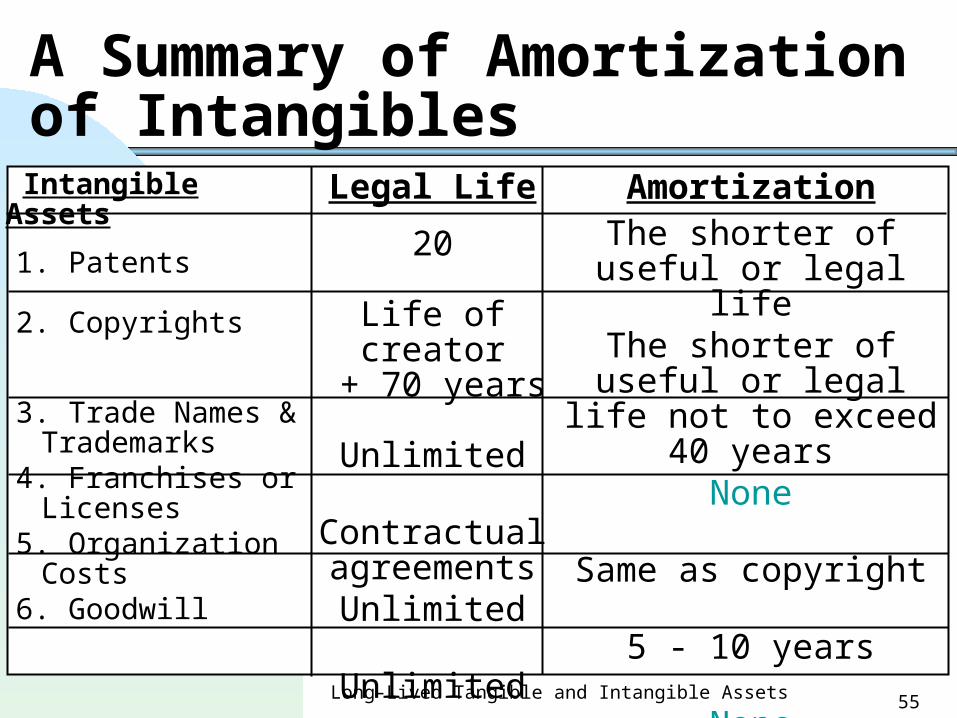

A Summary of Amortization of Intangibles

Intangible Assets

1. Patents

2. Copyrights

3. Trade Names & Trademarks

4. Franchises or Licenses

5. Organization Costs

6. Goodwill

Legal Life

20

Life of creator + 70 years

Unlimited

Contractual agreements

Unlimited

Unlimited

AmortizationThe shorter of useful or

legal lifeThe shorter of useful or legal life not to exceed

40 yearsNone

Same as copyright

5 - 10 years

None

Long-Lived Tangible and Intangible Assets56

Impact of New Information on Long-Lived Assets- Changes In Depreciation Estimate

Accounting treatment: no retroactive effect and make no adjustment for the past years’ misstatement. Spread the remaining undercoated balance (i.e., the book value) less the revised (new) residual value over the revised (new) estimate of the remaining life of the assets.

Long-Lived Tangible and Intangible Assets57

Example: (S-L Depr. Method)

Machine costing $10,000 acquired on 1/1/x1. Revised

EstimatesEstimates

on 1/1/x1 on 1/1/x3

Residual value $2,000 $1,000

Life 4 years 5 years

Long-Lived Tangible and Intangible Assets58

Example: (Contd.)

Year Depr. Exp Acc. Depr Book Valuex1 $2,0001 2,000 8,000x2 $2,0002 4,000 6,000x3 $1,667 5,666.7 4,333.3x4 $1,667 7,333.4 2,666.6x5 $1,667 9,000.1 1,000

1. (10,000-2,000)/4 = $2,0002. (6,000-1,000)/(5-2) =1666.7

Long-Lived Tangible and Intangible Assets59

New Information -Additional Costs Subsequent to Acquisition Basic principle for capitalization of these

costs:Capitalize the cost if it can:a. extend the life of the existing asset, orb. increase the service quality of the

existing asset, orc. increase the productivity of the existing

asset (including the reduction of unit cost).

Otherwise, expense the cost.

Long-Lived Tangible and Intangible Assets60

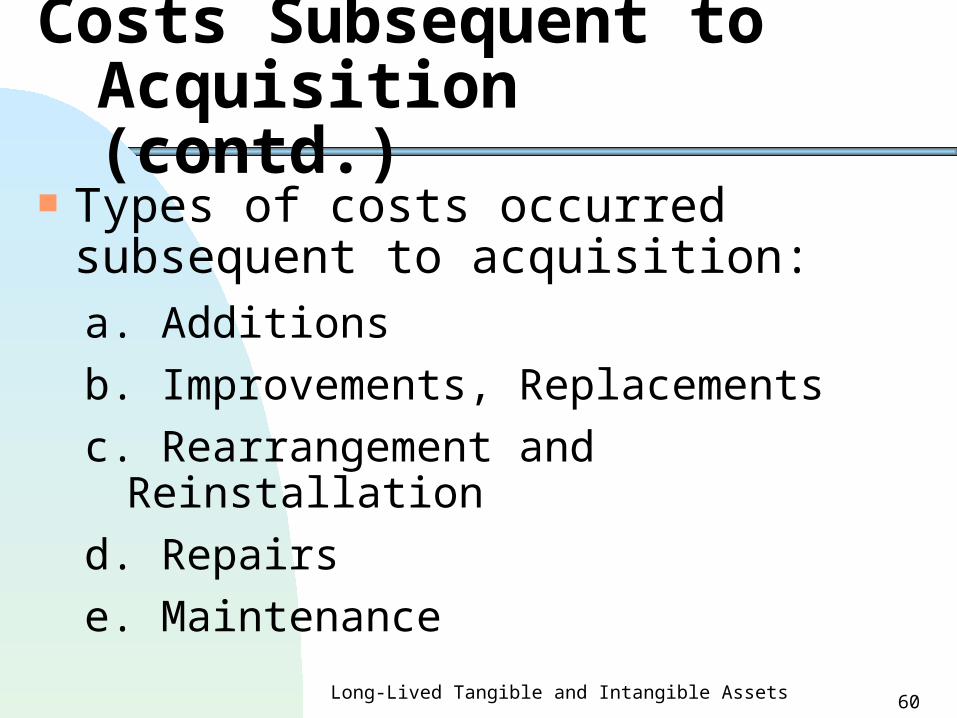

Costs Subsequent to Acquisition(contd.)

Types of costs occurred subsequent to acquisition:a. Additions

b. Improvements, Replacements

c. Rearrangement and Reinstallation

d. Repairs

e. Maintenance

Long-Lived Tangible and Intangible Assets61

4. Impairment of Long-Lived Assets

PPE and Intangibles are reported at cost except for impairments.

An impairment occurs when the book value (cost – accumulated depreciation) of an asset is not fully recoverable.

Long-Lived Tangible and Intangible Assets62

Operational Assets Held for Use –Tangible Assets and Finite-Life Intangibles (Patents, etc)

GAAP requires test for impairment only when events or changes in circumstances indicate that the book value of this asset may not recoverable.

Long-Lived Tangible and Intangible Assets63

The Accounting Treatment for Impairment (for Held for Use Tangible and finite-Life Intangibles)

Steps:

1. Conduct the Recoverability Test.

2. Compute the Impaired Amount.

Long-Lived Tangible and Intangible Assets64

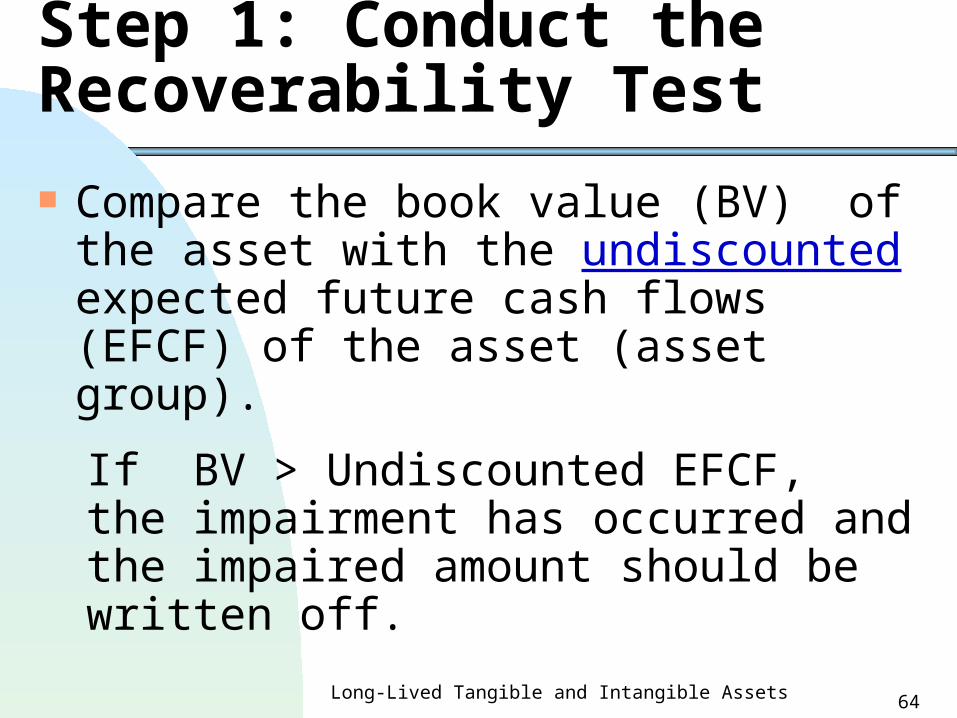

Step 1: Conduct the Recoverability Test

Compare the book value (BV) of the asset with the undiscounted expected future cash flows (EFCF) of the asset (asset group).

If BV > Undiscounted EFCF, the impairment has occurred and the impaired amount should be written off.

Long-Lived Tangible and Intangible Assets65

Step 2: Compute The Impaired Amount

Impaired amount = Book value - fair value (if the fair value is available) or

Impaired amount = Book value – estimated fair value1

(if fair value is not available)

1. discounted present value of the future cash flows of the asset can be the estimated fair value

Long-Lived Tangible and Intangible Assets66

Write Off the Impaired Amount

Recognition of Impairment Loss:

Loss on Impairment1 $$$$$

Accumulated Depre.$$$$$

1. Reported as part of income from continuing operations, not extraordinary losses.

Long-Lived Tangible and Intangible Assets67

Impairment (contd.)

After the write off, the fair value (or the estimated fair value if fair value is not available) becomes the new cost base for depreciation.

No restoration of impaired loss is allowed for tangibles and finite-life intangibles assets held for use.

Long-Lived Tangible and Intangible Assets68

Impairment (contd.)

Disclosure Requirements of impairment loss:

1. A description of the impaired asset or asset group.

2. The facts and circumstances leading to the impairment.

3.The amount of the loss.

4.The method used to determined the fair value.

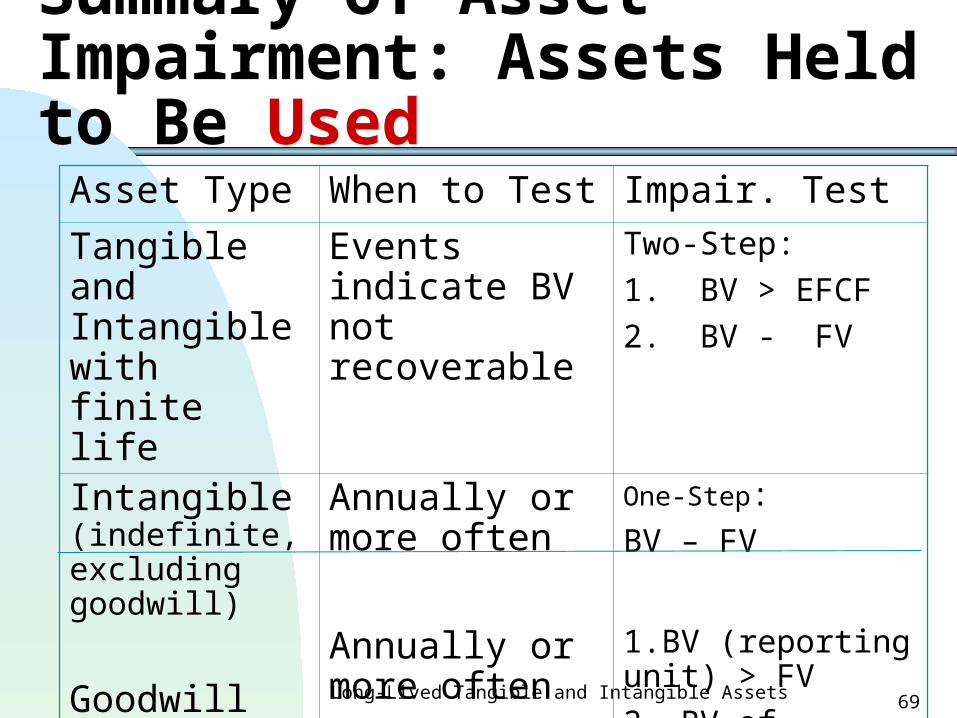

Long-Lived Tangible and Intangible Assets69

Summary of Asset Impairment: Assets Held to Be Used

Asset Type When to Test Impair. Test

Tangible and Intangible with finite life

Events indicate BV not recoverable

Two-Step:

1. BV > EFCF

2. BV - FV

Intangible(indefinite, excluding goodwill)

Goodwill

Annually or more often

Annually or more often

One-Step:

BV – FV

1.BV (reporting unit) > FV

2. BV of goodwill – implied FV

Long-Lived Tangible and Intangible Assets70

5. Disposition of Property, Plant and Equipment- Sold for Cash

Example:

A building costing $300,000 with accumulated depreciation of $200,000 was sold for $70,000. The journal entry to record the transaction is: Cash 70,000Accu. Depre. 200,000Loss 30,000 Building 300,000

Long-Lived Tangible and Intangible Assets71

Disposition of Property, Plant and Equipment- Abandonment

Example:

An automobile costing $20,000 with accumulated depreciation of $15,000 was abandoned. The journal entry to record the transaction is: Accu. Depre. 15,000Loss 5,000 Automobile 20,000

Long-Lived Tangible and Intangible Assets72

Disposition of Property, Plant and Equipment – Exchange of Assets

Cost of old asset =$20,000Book value of old asset = 6,000Fair value of old asset = 4,000Fair value of new asset = 9,000

New Asset 9,000Acc. Depr. 14,000Loss on

Disposal of ass. 2,000 Old ass. 20,000 Cash 5,000