BUS210 Introduction to Liabilities: Economic … 2014/Handout.CL.pdf · BUS210 Introduction to...

35

BUS210 Introduction to Liabilities: Economic Consequences, Current Liabilities and Contingencies Problems: E10-2, E10-4, E10-7, E10-10, P10-1, P10-4

Transcript of BUS210 Introduction to Liabilities: Economic … 2014/Handout.CL.pdf · BUS210 Introduction to...

BUS210

Introduction to Liabilities: Economic Consequences,

Current Liabilities and Contingencies

Problems:

E10-2, E10-4, E10-7, E10-10, P10-1, P10-4

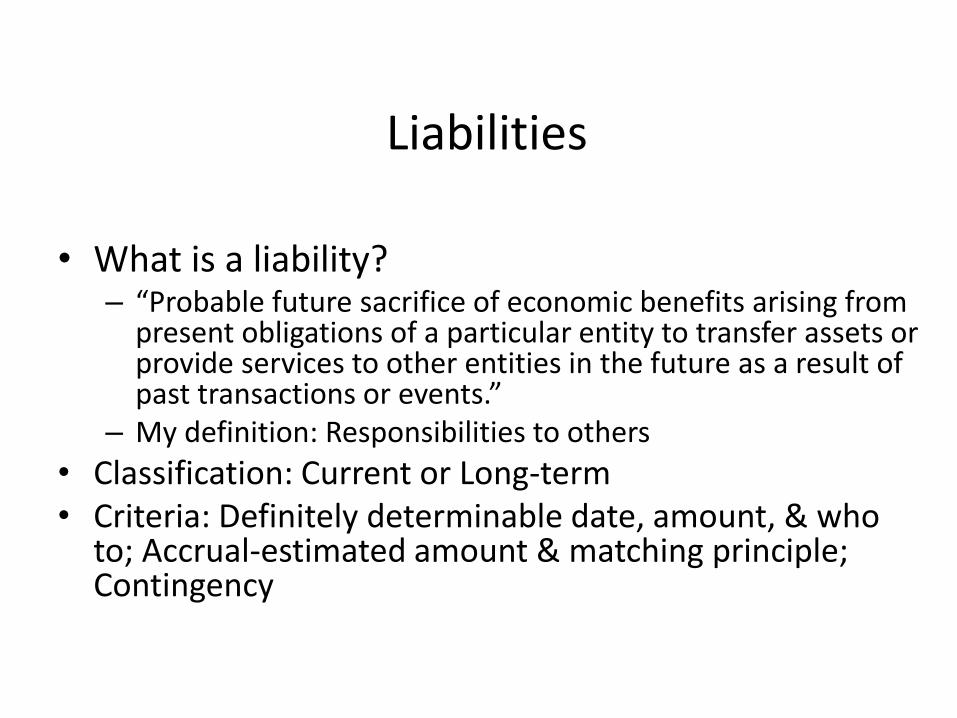

Liabilities

• What is a liability? – “Probable future sacrifice of economic benefits arising from

present obligations of a particular entity to transfer assets or provide services to other entities in the future as a result of past transactions or events.”

– My definition: Responsibilities to others

• Classification: Current or Long-term • Criteria: Definitely determinable date, amount, & who

to; Accrual-estimated amount & matching principle; Contingency

Current Liabilities

• Classification

– expected to require the use of current assets (or the creation of other current liabilities) to settle the obligation.

• Valuing current liabilities on the balance sheet

– Report at face value (Ignore present value)

• Reporting current liabilities

– Primary problem is ensuring that all existing current liabilities are reported on the balance sheet.

P10-1 Current Liabilities and Long-term Liabilities

1. Accounts payable of $170,000 owed to suppliers for inventory.

2. $60,000 note payable due in 3 months. Company plans to acquire a 5 year loan to pay off note. Bank has agreed to grant loan.

3. $500,000 mortgage: $75,000 payable within 12 months, and the remainder payable over the next six years.

4. $8,000 owed to phone company for December services. 5. Advances of $25,000 received from customer. If services

not performed within 6 months the, $25,000 will be returned to the customer.

6. $15,000 due federal government for income taxes withheld from employees during last quarter, must be submitted by end of next quarter.

7. $125,000 note: $30,000 is payable with 12 months and the remainder over the next two years. Current payment will be made by issuing common stock.

8. Company declares a cash dividend of $50,000 on 12.29. Dividend will be paid next year on 1.21.

Classify 1-8 as current or long-term as of the end of the year. Compute to total CL and LTL amounts.

Current Liabilities Determinable (how much, when, & who)

1. Accounts payable (Ch 7)

2. Short-term notes

3. Current maturities of long-term debts

4. Dividends payable

5. Unearned revenues (Ch 5)

6. Sales tax payable

7. Income taxes payable (App 10B)

8. Payroll taxes payable

Current Liabilities Estimated Amount & Matching Principle

Accrued liabilities - accrue expense and liability at the end of the current period, and usually paid sometime during the next year. For each item, debit expense and credit liability. Examples include:

– Wages payable

– Salary payable

– Interest payable

– Rent payable

– Insurance payable

– Property taxes payable

– Employee bonuses

Reporting Liabilities on the Balance Sheet: Perspectives

• Shareholders and investors – Debt: interest expense is tax deductible, but more debt

means more risk to shareholders – equity ownership is subordinated to creditors

• Creditors – Debt: restrictive covenants regarding debt limits

• Management – wants to minimize debt on the balance sheet – often looks for “off-balance sheet” financing – less debt now improves ability to borrow in the future – Current & long-term liability mix

Liabilities Disclosures: Coca Cola 2012 & 2011

E10-7 T accounts and inferring payments The following information was taken from the 2008 annual report of Bed Bath & Beyond (dollars in thousands).

a. Assume the accounts payable reflects only inventory suppliers, and compute the cash payments made to suppliers during 2008.

2008 2007

Cost of Goods Sold $4,335,104 $4,123,711

Inventory 1,642,339 1,616,981

Accounts Payable 514,734 570,605

Liabilities and Current Ratio E10-2 Company borrowed $100,000 to finance the purchase of fixed assets. The loan contract provided of a 12% interest rate and that the principal must be paid in full in ten years. The contract also states that current ratio be maintained at 1.5:1. Before the company borrowed the $100,000, the current assets and current liabilities were $130,000 and $80,000 respectively. a. Compute current ratio if invest $50,000 in fixed assets and remainder in short-term investments. To what dollar amount can current liabilities grow before company violates the debt contract? b. Compute current ratio if invest $80,000 in fixed assets and remainder in cash or short-term investments. To what dollar amount can current liabilities grow before company violates the debt contract? c. Compute current ratio if invest $100,000 in fixed assets. To what dollar amount can current liabilities grow before company violates the debt contract?

E10-4 Notes Payable and Actual Interest Rate On 12.1 company borrowed $19,250 from bank signing a 90 day note with a face amount of $20,000. the stated interest rate is 15%. a. Provide journal entry by borrower on 12.1. b. Provide adjusting journal entry on 12.31 before FS are prepared. Show how the note payable would be disclosed on the BS. c. Compute the actual annual interest rate on the note. d. Why is the actual interest rate different from the stated rate?

Contingent Liabilities

• Contingent on some future event or activity in order to know the exact amount.

Examples: warranties, coupons, and lawsuits

• Changes in estimate may be made in subsequent periods, when future event is concluded.

• Under IFRS, much of these transactions are reported in a balance sheet account called “provisions”. – Provisions are more readily booked than contingent liabilities

because IFRS provisions are accrued when the obligation is “more likely than not,” while under US GAAP contingent liabilities are accrued when “highly probable,” which is a much higher threshold.

Figure 10-5

Contingencies & Off Balance Sheet Arrangements: Coca Cola

Warranty A promise by a manufacturer or seller to ensure the quality or

performance of the product for a specific period of time

Almost Honest

JOHN’S Used Cars

I’ll stand behind it for 50 miles

or 50 minutes whichever comes first

Contingent Liabilities Warranties

– Uncertain future costs

Adjusting Entry: Record estimated expense and liability when products are sold (matching concept):

Warranty Expense [on IS] xx

Estimated Warranty Liability[on BS] xx

Actual warranty work: As costs are incurred (usually in subsequent periods), charge expenditure to warranty liability:

Estimated Warranty Liability[on BS] xx

Cash, etc.[on BS] xx

Warranties: Exercise: E10-10(a)

(1) JE to record sale in 2011 (200 @ $250 each): Cash 50,000 Sales revenue 50,000 (2) AJE in 2011 to record estimated warranty for the sales

(200 @ $20): Warranty expense 4,000 Estimated Warr. Liability 4,000 (3) JE to record payment in 2011 for repairs: Est. Warr. Liability 1,400 Cash 1,400 JE to record payment in 2012 for repairs: Est. Warr. Liability 2,600 Cash 2,600

Class Exercise: E10-10(b)

Income effects for the revenue and warranty expense under the two alternative for recognition of expense (expressed in thousands): Accrue Expense Expense as Paid 2011 2012 2011 2012 Revenues 50,000 --- 50,000 --- Warr. Expense (4,000) --- (1,400) (2,600) Note that the accrual method recognizes the expense in the same period as the revenues generated by the sale. MATCHING CONCEPT

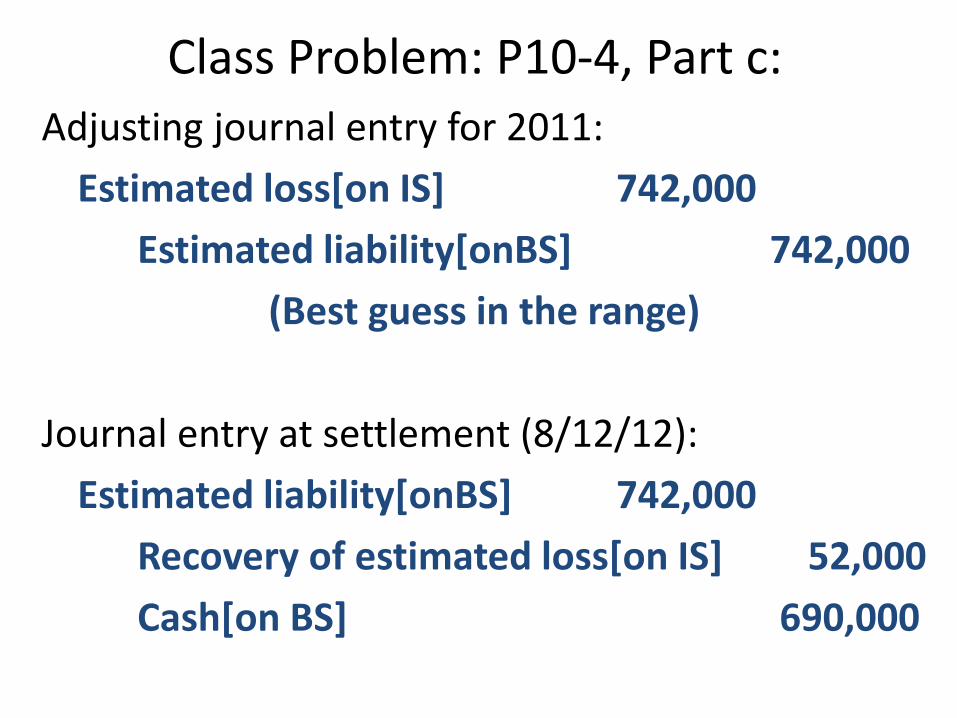

P10-4 Contingent Liability Recognition While shopping, a customer slipped and seriously injured his back. The customer believes the store should have warned him that the floors were slippery, thus he sues the store for damages. At yearend, the suit is still in progress. According to the company’s lawyers, it was probable that the company would lose and the loss could be between $250,000 and $1.5 million, with a best guess of the loss at $742,000. The lawsuit was eventually settled the following year in favor of customer for $690,000. a. Discuss the issues in deciding how to report the lawsuit on this

year’s F/S, store perspective, customer perspective. b. If you were auditing the company, how would you recommend

this lawsuit be reported on this year’s F/S? c. If a contingent liability of $742,000 was accrued at yearend,

what‘s the entry? What’s the entry on the date of settlement?

Potential Lawsuit: P10-4, Parts a & b:

Issues and recommendations: - Likelihood? Probable - Disclose? Yes - Disclosure? Can you estimate? Indicate range and level of probability (250,000 – 1.5 million) - Accrue? Since probable (or greater) and estimable, accrual is required, based on best estimate.

Class Problem: P10-4, Part c:

Adjusting journal entry for 2011:

Estimated loss[on IS] 742,000

Estimated liability[onBS] 742,000

(Best guess in the range)

Journal entry at settlement (8/12/12):

Estimated liability[onBS] 742,000

Recovery of estimated loss[on IS] 52,000

Cash[on BS] 690,000

Deferred Income Tax Liability

Deferred Income Tax Liability Entries

NIKE Deferred Taxes Liabilities Disclosures

Deferred Taxes (App 10B) Generated by the discrepancy between income and expenses for taxation (specified by IRS) and financial reporting (specified by GAAP). Timing Difference Example:

– Equipment purchased on 1/1/09 for $9,000 – 3-year useful life – no salvage value – DDB for income tax purposes – SL for financial reporting purposes – Income tax rate of 30%

Depreciation Schedules

2009 Deferred income tax liability $900

2010 Deferred income tax benefit $300

2011 Deferred income tax benefit $600

Year DDB-TI Exp

SL-IS Exp

Diff Rate Tax Benefit (Disbenefit)

2009 $6000 - 3000 = $3000 X 30% = $900

2010 2000 - 3000 = (1000) X 30% = (300)

2011 1000 - 3000 = (2000) X 30% = (600)

Total $9000 $9000 $0 $0

Leases

• FASB issued SFAS No. 13, which requires certain leases to be recorded as capital leases. – Capital leases record the leased asset as a capital asset, and

reflect the present value of the related payment contract as a liability.

• Requirements of SFAS No. 13 - record as capital lease for the lessee if any one of the following is present in the lease:

– Title transfers at the end of the lease period,

– The lease contains a bargain purchase option,

– The lease life is at least 75% of the useful life of the asset, or

– The lessee pays for at least 90% of the fair market value of the lease.

Economic Consequences of Operating Leases Improved credit ratings can lead to lower borrowing

costs…

Management has strong incentive to manage the

balance sheet by using “off-balance-sheet financing”

Retirement Costs (App 10A) • Defined Contribution Plans

– Less expensive than Defined Benefit Plans – 401(k), 403(b), 457 – The entry to record period contributions is very simple: Dr. Pension Expense Cr. Cash

• Defined Benefit Plans – Benefits must be predicted, therefore several assumptions and

estimates are required – Social Security is form of Defined Benefit Plan

– The entry to record the estimated liability is simple, but the calculations can be quite complicated:

Dr. Pension Expense Cr. Pension Liability

2012-2011 Coca Cola:

Review: Definitely Determinable, Estimated, Commitment, Contingent