BULLETI FEDERAL RESERVNE Reserve Bulletin/Federal Reserve Bulletin...maintained their profit margins...

137

VOLUME 74 • NUMBER 9 • SEPTEMBER 1988 FEDERAL RESERVE BULLETIN BOARD OF GOVERNORS OF THE FEDERAL RESERVE SYSTEM, WASHINGTON, D.C. PUBLICATIONS COMMITTEE Joseph R. Coyne, Chairman • Michael Bradfield • S. David Frost • Griffith L. Garwood • Donald L. Kohn • Michael J. Prell • Edwin M. Truman The FEDERAL RESERVE BULLETIN is issued monthly under the direction of the staff publications committee. This committee is responsible for opinions expressed except in official statements and signed articles. It is assisted by the Economic Editing Section headed by Mendelle T. Berenson, the Graphic Communications Section under the direction of Peter G. Thomas, and Publications Services supervised by Linda C. Kyles.

Transcript of BULLETI FEDERAL RESERVNE Reserve Bulletin/Federal Reserve Bulletin...maintained their profit margins...

VOLUME 74 • NUMBER 9 • SEPTEMBER 1988

FEDERAL RESERVE

BULLETIN

BOARD OF GOVERNORS OF THE FEDERAL RESERVE SYSTEM, WASHINGTON, D.C.

PUBLICATIONS COMMITTEE

Joseph R. Coyne, Chairman • Michael Bradfield • S. David Frost• Griffith L. Garwood • Donald L. Kohn • Michael J. Prell • Edwin M. Truman

The FEDERAL RESERVE BULLETIN is issued monthly under the direction of the staff publications committee. This committee is responsible foropinions expressed except in official statements and signed articles. It is assisted by the Economic Editing Section headed by Mendelle T.Berenson, the Graphic Communications Section under the direction of Peter G. Thomas, and Publications Services supervised by Linda C. Kyles.

Table of Contents

591 PERSONAL BANKRUPTCIES

This article describes the evolution of bank-ruptcy law, discusses the causes and effectsof personal bankruptcy, and examines thehistorical trends in bankruptcy filings, par-ticularly since 1984, which marked the be-ginning of a countercyclical upswing in thenumber of bankruptcy filings.

604 INDUSTRIAL PRODUCTION

Industrial production increased an esti-mated 0.4 percent in June.

607 STATEMENT TO CONGRESS

Alan Greenspan, Chairman, Board of Gov-ernors, reviews the recent and prospectivemonetary policy and the economic outlook,including our nation's longer-term eco-nomic objectives, the overall strategy forfiscal and monetary policies needed toreach those objectives, and the appropriatetactics for implementing monetary policywithin that strategic framework, before theSenate Committee on Banking, Housing,and Urban Affairs, July 13, 1988.

614 ANNOUNCEMENTS

Appointment of John P. La Ware as a mem-ber of the Board of Governors.

Publication of a new handbook for the Reg-ulatory Service.

Two studies on managing risk in the pay-ments system now available.

Update to staff guidelines under RegulationAA.

Revised List of OTC Stocks Subject toMargin Regulations now available.

Extension of comment period on same-daypayment of checks.

Informal hearing held on proposed rule toimplement the limitations placed on grand-fathered nonbank banks by the CompetitiveEquality Banking Act of 1987.

Change in Board staff.

617 LEGAL DEVELOPMENTS

Various bank holding company, bank ser-vice corporation, and bank merger orders;and pending cases.

630 MEMBERSHIP OF THE BOARD OFGOVERNORS OF THE FEDERALRESERVE SYSTEM, 1913-88.

List of appointive and ex officio members.

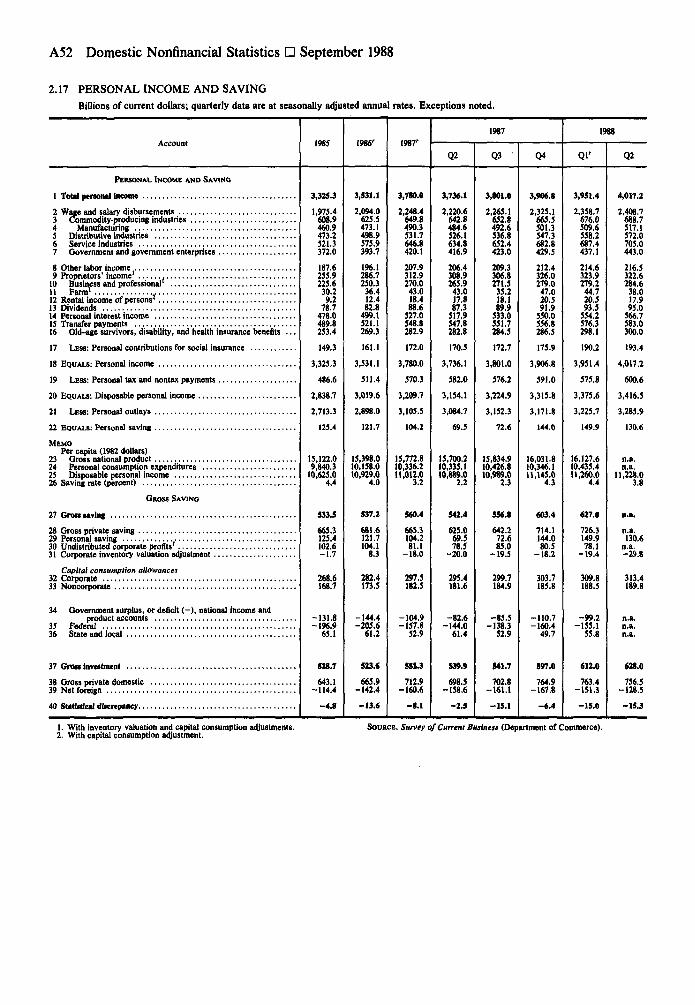

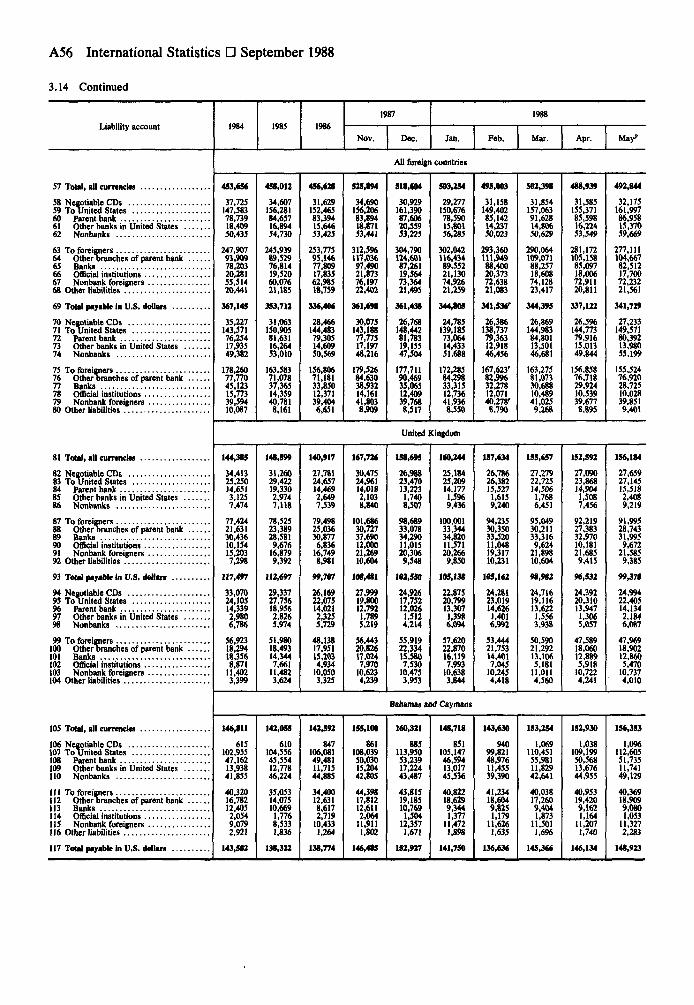

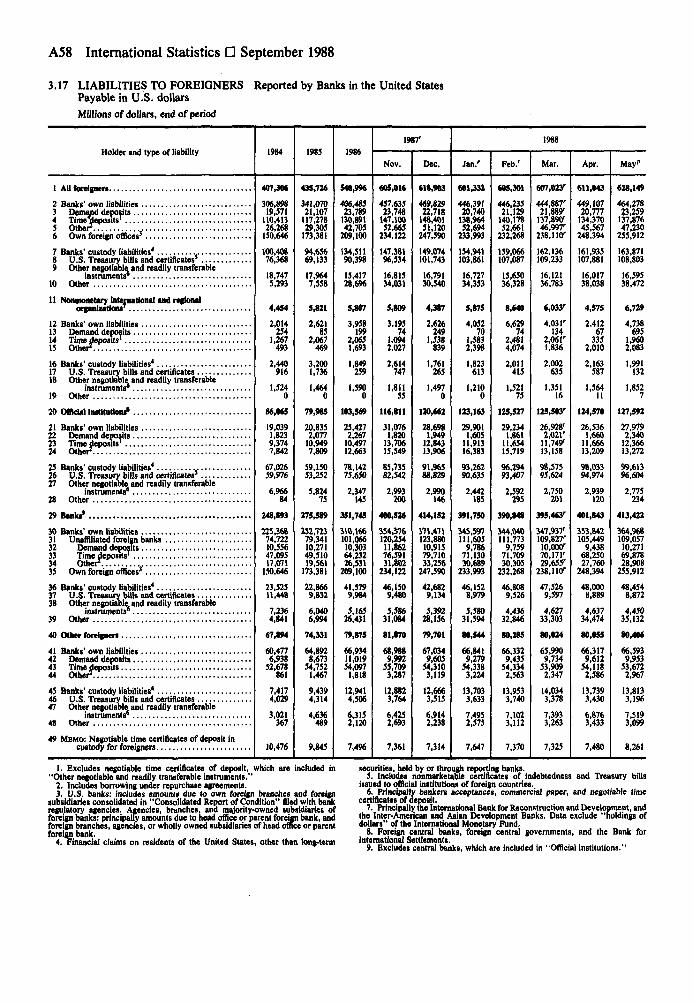

AI FINANCIAL AND BUSINESS STATISTICSThese tables reflect data available as ofJuly 28, 1988.

A3 Domestic Financial StatisticsA4 Domestic Nonfinancial StatisticsA5 International Statistics

A69 GUIDE TO TABULAR PRESENTATION,STATISTICAL RELEASES, AND SPECIALTABLES

A86 BOARD OF GOVERNORS AND STAFF

A88 FEDERAL OPEN MARKET COMMITTEEAND STAFF; ADVISORY COUNCILS

A90 FEDERAL RESERVE BOARDPUBLICATIONS

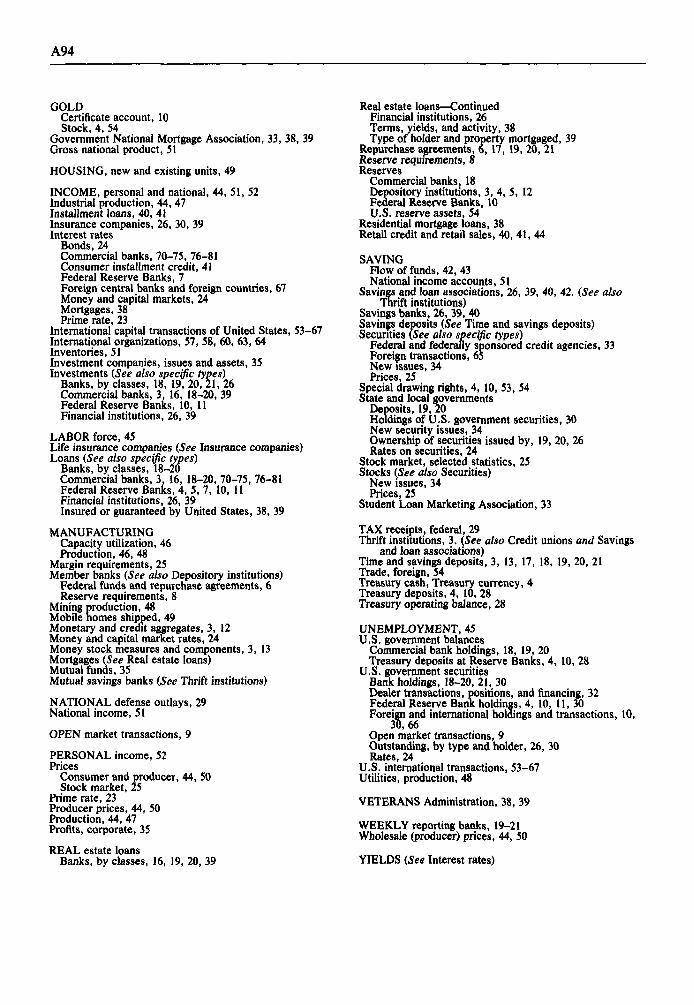

A93 INDEX TO STATISTICAL TABLES

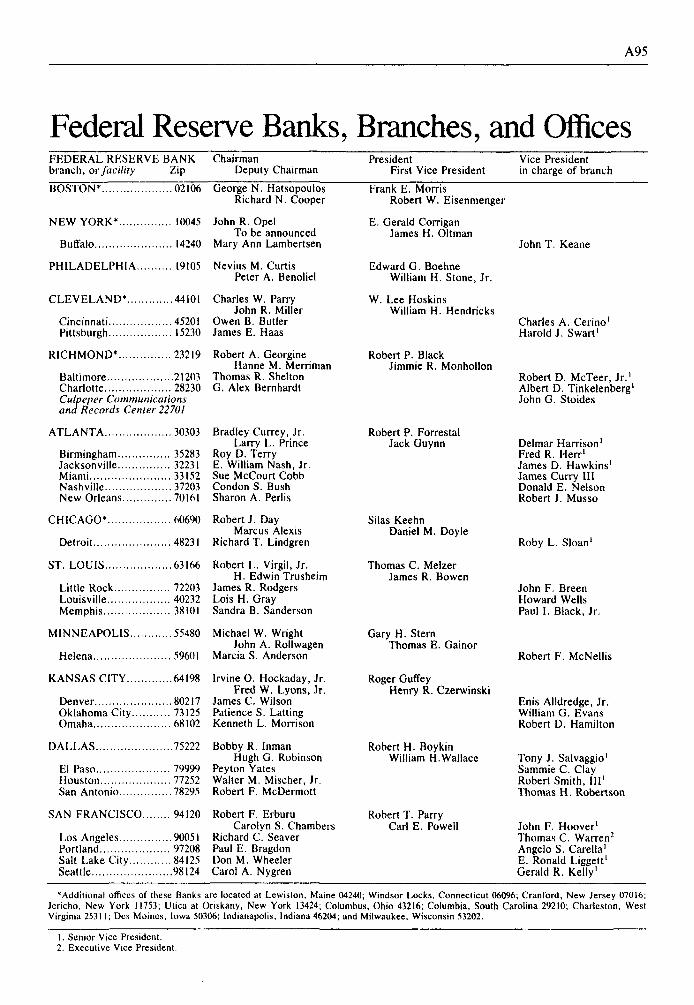

A95 FEDERAL RESERVE BANKS,BRANCHES, AND OFFICES

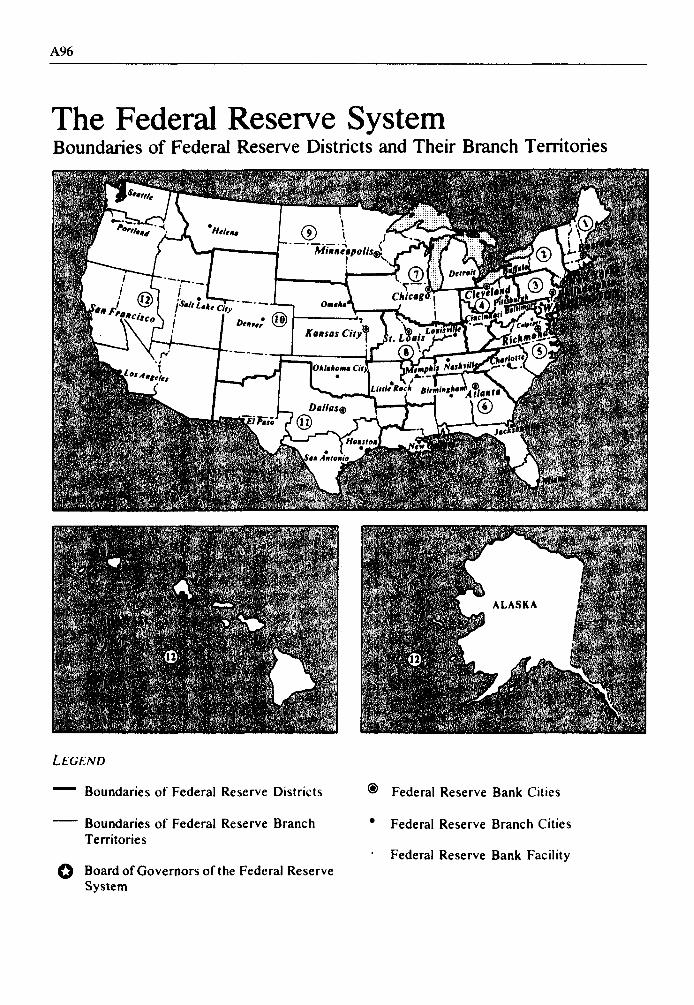

A96 MAP OF FEDERAL RESERVE SYSTEM

Personal Bankruptcies

Charles A. Luckett of the Board's Division ofResearch and Statistics prepared this article withthe assistance of Nellie D. Middleton and WayneC. Cook. Footnotes appear at the end of thearticle.

Declarations of bankruptcy by nonbusiness peti-tioners have risen sharply over the past 3'/2years, even as employment and aggregate per-sonal income registered solid growth. This ratherunusual countercyclical upswing in nonbusinessbankruptcies (hereafter called "personal" bank-ruptcies) has generated considerable puzzlementand some concern.

The consumption-related debt of the house-hold sector also has grown substantially duringthe current economic advance, both absolutelyand relative to disposable income, a trend that islikely a key factor underlying the rise inbankruptcies.1 In addition, revisions to bank-ruptcy laws and changes in consumer attitudestoward bankruptcy may have fostered a climatein which people regard bankruptcy as a moreplausible remedy for financial problems than theyonce did. Despite the rising number of bankrupt-cies, however, credit suppliers apparently havemaintained their profit margins relatively well.So far, the surge in bankruptcies does not seemto have motivated any measurable restriction onthe supply of credit to consumers.

This article will describe the historical trendsof bankruptcy filings and the evolution of bank-ruptcy law, examine the causes and effects ofpersonal bankruptcy, briefly review relevantstudies, and then close with a detailed scrutiny ofthe trend in bankruptcies since 1984.

HISTORICAL I'KISDS IS H.WKRUFK.r

In 1946, personal bankruptcy filings totaled fewerthan 9,000, which last year was about the averagenumber of filings per week.2 In 1946, of course,

the nation was just emerging from World War IIand from the stringent controls imposed duringthe war on the production of consumer goods.With few automobile or refrigerator purchases tobe financed during the war years—and becauserestrictions also were imposed on the making ofconsumer loans—the stock of consumer install-ment debt outstanding at the end of 1945 wasonly $2.5 billion, equivalent to about $16 billionin 1987 dollars. The consumer debt outstandingin 1945 summed to less than 2 percent of theamount of disposable income for all U.S. house-holds; today, this aggregate debt-to-income ratiostands at nearly 19 percent.

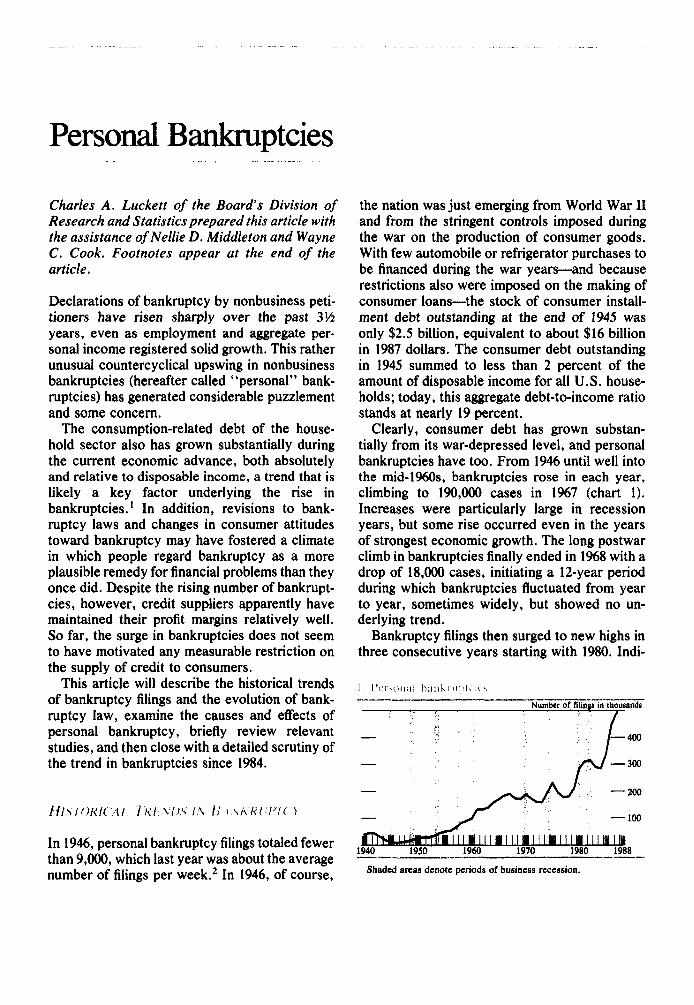

Clearly, consumer debt has grown substan-tially from its war-depressed level, and personalbankruptcies have too. From 1946 until well intothe mid-1960s, bankruptcies rose in each year,climbing to 190,000 cases in 1967 (chart 1).Increases were particularly large in recessionyears, but some rise occurred even in the yearsof strongest economic growth. The long postwarclimb in bankruptcies finally ended in 1968 with adrop of 18,000 cases, initiating a 12-year periodduring which bankruptcies fluctuated from yearto year, sometimes widely, but showed no un-derlying trend.

Bankruptcy filings then surged to new highs inthree consecutive years starting with 1980. Indi-

I . Personal bnnknij)loc\

Number of filings in thousands

1940 1950 1960 1988

Shaded areas denote periods of business recession.

592 Federal Reserve Bulletin • September 1988

viduals had amassed substantial debts during thehigh-inflation years of the late 1970s, and theeconomy endured back-to-back recessions dur-ing the early 1980s that carried the unemploy-ment rate from less than 6 percent to more than10 percent. Moreover, a major revision to federalbankruptcy law took effect in the fall of 1979.This revision made bankruptcy a more attractiveoption to troubled debtors, particularly becauseit increased the amount of assets that could beexempt from liquidation. Whatever the effect ofthese various factors, bankruptcies jumped fromabout 200,000 cases in 1979 to nearly 315,000 in1982. This figure was even understated some-what in comparison with previous years becausehusband-and-wife bankruptcies were treated astwo cases under the old law and as one case afterthe revisions became effective.

As economic activity regained momentum in1983 and 1984, bankruptcies declined once more,as they had during three previous cyclical up-swings. But historical patterns went awry in 1985and 1986 when bankruptcies shot up more than20 percent in each year despite the strength of theeconomy. The uptrend in bankruptcies slowed toa 10 percent rate in 1987, but the number of casesfiled totaled nearly 500,000, substantially abovethe 1982 cyclical high. Sizable additions to con-sumer debt during the period no doubt contrib-uted to the surge in bankruptcies; still, the latestrise in bankruptcies, because it occurred during abusiness expansion, seems larger than the eco-nomic fundamentals would suggest. On thewhole, the 1985-87 surge in bankruptcies is apuzzling development, one that will be addressedfurther in later sections.

iiVOI.UIION ()'. llANKIiUPTCY I .AW

The purpose and characteristics of bankruptcyprocedures in the United States are considerablydifferent from their antecedents in Roman law.For most of history, bankruptcy was a procedureimposed by creditors to confiscate and distributethe assets of a delinquent debtor. In more recenttimes, U.S. bankruptcy law has been restruc-tured to achieve more of a balancing of theinterests of creditors and debtors and to providedebtors with a fresh start.

The word "bankruptcy" has its roots in theLatin words for "bench" and "break"; its literalmeaning is "broken bench." Under Roman law,creditors, after gathering together and dividingup the assets of a delinquent debtor, wouldphysically break the debtor's workbench as apunishment and perhaps as a warning to otherindebted tradesmen. Bankrupts were regarded asperpetrators of fraud who deserved severe pen-alty; the Romans deprived bankrupts of theircivil rights, and many other societies stigmatizedthem by requiring that they dress in a particularidentifying garb.

Early law, then, sought merely to establish anorderly means of satisfying the claims of credi-tors; neither discharge of debt nor rehabilitationof debtors constituted an element of the bank-ruptcy process as it evolved in Western societiesthrough the centuries. Not until 1705 did Englishlaw provide for remission of the debts of bank-rupts, and even then not as a humane gesture togive the bankrupt a new start, but as a practicalmeans to counter the concealment of assets bydebtors. By assuring bankrupts that their credi-tors would forswear future collection efforts if allcurrently owned assets were surrendered, thelaw created an incentive for debtors to comply.

The first bankruptcy law in the United Stateswas passed in 1800, but was repealed three yearslater. Reflecting its heritage from English law,the statute applied only to tradesmen, mer-chants, and others in business (virtually no "con-sumer" credit existed); it made no provision forvoluntary bankruptcy, discharge of debts, ex-emption of any assets, or payment of debts out offuture income. Equally short-lived bankruptcylaws were passed in 1842 and 1867 in response tofinancial panics.

After another major financial crisis in the1890s, the Congress adopted the Bankruptcy Actof 1898, which survived, with amendments, untilenactment of a new statute in 1978. The 1898 actrepresented a significant liberalization of bank-ruptcy practice. It brought consumer as well ascommercial debtors under its wing, and ex-panded bankruptcy from a remedy that wasimposed by creditors to one that could be volun-tarily sought by debtors. It provided for thedischarge of debts that were not satisfied byliquidation of the debtor's assets, and also autho-

Personal Bankruptcies 593

rized state legislatures to establish categories ofassets that would be exempt from the claims ofcreditors. Thus, at the close of the 19th century,a body of law originally designed to serve credi-tors took on a significant aspect of debtor pro-tection.

The most important of several amendments tothe Bankruptcy Act was the Chandler Act in1938, which established a procedure for insolventdebtors to retain their assets and to repay allor part of their obligations over a three-yearperiod with court protection from their credi-tors. Available to employed persons with aregular income, these court-administered repay-ment schedules were known as "wage-earnerplans."

Following extensive study and congressionalhearings on the functioning of the bankruptcyprocess, a revised bankruptcy code, enacted in1978 (the Bankruptcy Reform Act of 1978), tookeffect on October 1, 1979. The code consolidatedsome chapters of previous law pertaining tobusiness reorganizations and sought to stream-line the administration of the bankruptcy courts,but its most sweeping changes involved personalbankruptcy. It erected greater protection againstrepossession of collateral for consumer loans andmade it more difficult for creditors to elicit anindividual's reaffirmation of a discharged debtafter bankruptcy. Most important, the code in-troduced federal asset exemptions ($7,500 ofequity in a home and approximately $3,000 inother designated assets) that were considerablymore generous than were most state exemptions.It also permitted each individual of a marriedcouple to claim such exemptions, thus doublingthe amount of exemptions available to marriedpersons.3

Provisions for the wage-earner repaymentplans were redrafted to cover some debts thatcould not be discharged under "straight" bank-ruptcy, such as student loans, government finesand penalties, and loans obtained through falsefinancial statements. The new code also removeda provision of the old law that creditors mustapprove any plan for repayment, and gave thecourt sole discretion to accept a plan offered by apetitioner. A plan was to be confirmed if thecourt found that it had been proposed in goodfaith, that the amount to be paid the creditors

THE U.S. BANKRUPTCY CODE

In its current form, the U.S. bankruptcy codecontains five "operative" chapters (7, 9, 11, 12,and 13) under which bankruptcy petitions may befiled. Chapter 9 applies exclusively to municipal-ities and chapter 11 primarily to business reorga-nizations. Individuals most commonly file underchapters 7 or 13. Chapter 7 provides for"straight" bankruptcy—that is, liquidation of as-sets and discharge of debts—and may be usedeither by business or nonbusiness petitioners. Itaccounts for about 70 percent of all bankruptcies,and typically, 85 percent of chapter 7 cases areclassified as nonbusiness. Chapter 13 provides forthe "wage-earner plans" that involve the full orpartial repayment of debts while assets areshielded from creditor action. It is limited toindividuals, but insofar as an individual may be asole proprietor with mostly business-relateddebts, chapter 13 also embraces both business andnonbusiness cases. About 95 percent of Chapter13 cases involve nonbusiness petitioners. Chapter12, added to the statute in 1986, is the newestoperative section of the bankruptcy code. Itmakes available to "family farmers" (as definedin the code) the equivalent of a chapter 13 repay-ment program. Chapter 12 cases are classifed asbusiness bankruptcies.

was not less than what would have been paid tothem through liquidation, and that the debtorwould be able to make the payments contem-plated by the plan.

As noted, filings for personal bankruptcy shotup in 1980 and 1981. This surge in filings openeda debate on whether the 1978 reforms had gonetoo far, and led eventually to some retooling ofthe bankruptcy code in 1984. Courts were re-quired, for instance, to prohibit discharge ofdebts that financed eve-of-bankruptcy spendingsprees. Section 707(b) of the code embodied apotentially major change, which provided thatthe court could dismiss a discharge petition of anindividual debtor if it found that the granting ofrelief would constitute "a substantial abuse."The law did not establish specific standards forsuch a finding, however, and in practice thesubstantial-abuse test has not been vigorouslyapplied.

594 Federal Reserve Bulletin • September 1988

w •• n

Reasons for the long postwar uptrend in bank-ruptcies and the more recent large jumps are-generally interpreted from one of two perspec-tives. Some researchers have emphasized amacroeconomic approach that relates the totalnumber of bankruptcy filings in a period tomovements in such broad economic factors asthe rate of unemployment and the degree ofindebtedness. Others have adopted the micro-economic approach of examining individual casehistories to identify economic and demographicattributes that appear to characterize bankruptindividuals.

M<>\

Study of the broad economic forces affectingbankruptcies was relatively neglected until the1980s, when the revisions to the federal bank-ruptcy code and the explosion in the number offilings stimulated several efforts to determinehow much of the rise was attributable to the newlaw. Earlier studies had simply observed, ordemonstrated with a rudimentary statisticalmodel, that the postwar uptrend in bankruptciesrather closely paralleled the expansion of con-sumer debt. One study, for instance, using an-nual data for 1946-70, calculated a high statisti-cal correlation between the number ofbankruptcies per capita and the ratio of con-sumer installment debt to disposable personalincome.4 Such a result is not especially surpris-ing, in that being in debt is a necessary conditionfor bankruptcy. But, without a more rigorouslyspecified model, there is no way to determinewhether other factors might serve either to miti-gate or to intensify the effect of aggregate indebt-edness on total bankruptcies, or whether thesensitivity of bankruptcies to changes in indebt-edness might vary with different absolute levelsof debt burden.

Another study, which examined reasons fordifferences in bankruptcy rates among states,attributed most of the interstate variation todifferences in wage garnishment laws, and rela-tively little to different levels of debt-to-incomeratio and unemployment rate.5 An attempt toassess the effects over time of the economic

variables within each state was largely unsuc-cessful, partly because the number of annualobservations (12) was too few to yield reliableresults.

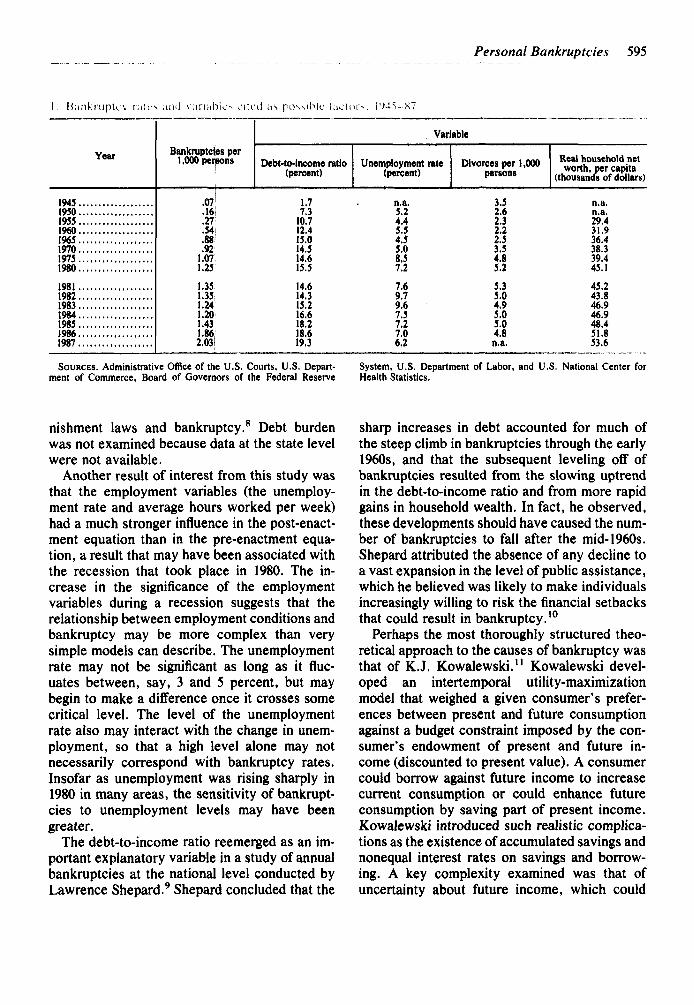

In the early 1980s researchers needed a work-able model of the macroeconomic forces under-lying national bankruptcy trends to help answerquestions about the effects of the new federalbankruptcy law. The typical approach of theirstudies was to estimate the parameters of abankruptcy model for a period ending just beforethe effective date of the law, to project bankrupt-cies into the subsequent period on the basis ofthe model, and to interpret the differences be-tween actual and projected bankruptcies as theresult of the alteration in the legal environment.(Table 1 presents data on bankruptcy rates andsome variables frequently associated with bank-ruptcy.)

Some of the models to project bankruptcieswere specified in no greater detail than the earliermodels had been. One, for instance, simply ex-trapolated previous bankruptcy trends withoutallowing for movements in economic variables;another projected the normal level of bankrupt-cies during 1980, a year of recession, on the basisof the severity of declines in manufacturing em-ployment in 1980 relative to such declines in pastrecessions.6 These studies found as much asthree-fourths of the actual climb in bankruptciesto be unexplained by the projection method, andtherefore attributable to changes in the law, inthe absence of other obvious explanatory fac-tors.

Other studies placed more emphasis on modeldevelopment by testing the explanatory power ofa wider variety of economic variables. Onestudy, by Richard Peterson and Kiyomi Aoki,built upon earlier work by analyzing differencesamong states in numbers of bankruptcies as afunction of both legal and economic variables.7

Using data for two quarters, one before and oneafter the effective date of the new law, the studyestimated explanatory equations for the two pe-riods separately and in combination. In contrastto the earlier study of differences among states inbankruptcy rates, this one found a considerablystronger and more consistent relationship be-tween employment indicators and bankruptcy,and correspondingly weaker links between gar-

Personal Bankruptcies 595

1. Bankruptcy rale*

Year

194J19501955I9601965..197019751980

1981198219831984198519861987

a i l i i v; • i a r

Bankruptcies per1,000 persons

.07

.16

.27;

.54

.88

.92

.07

.25

.35

.35

.24

.20

.438601

i lcu a s p o s s i b l e i . i c l u r s .

Debt-to-income ratio(percent)

Variable

Unemployment rate(percent)

1.77.3

10.712.415.014.514.615.5

14.614.315.216.618.218.619,3

n.a.5.24.45.54.55.08.57.2

7.69.79.67.57.27.06.2

Divorces per 1,000persons

3.52.62.32.22.53.54.85.2

5.35.04.95.05.04.8n.a.

Real household networth, per capita

(thousands of dollars)

n.a.n.a.29.431.936.438.339.445.1

45.243.846.946.948.451.853.6

SOURCES. Administrative Office of the U.S. Courts, U.S. Depart-ment of Commerce, Board of Governors of the Federal Reserve

System, U.S. Department of Labor, and U.S. National Center forHealth Statistics.

nishment laws and bankruptcy.8 Debt burdenwas not examined because data at the state levelwere not available.

Another result of interest from this study wasthat the employment variables (the unemploy-ment rate and average hours worked per week)had a much stronger influence in the post-enact-ment equation than in the pre-enactment equa-tion, a result that may have been associated withthe recession that took place in 1980. The in-crease in the significance of the employmentvariables during a recession suggests that therelationship between employment conditions andbankruptcy may be more complex than verysimple models can describe. The unemploymentrate may not be significant as long as it fluc-uates between, say, 3 and 5 percent, but maybegin to make a difference once it crosses somecritical level. The level of the unemploymentrate also may interact with the change in unem-ployment, so that a high level alone may notnecessarily correspond with bankruptcy rates.Insofar as unemployment was rising sharply in1980 in many areas, the sensitivity of bankrupt-cies to unemployment levels may have beengreater.

The debt-to-income ratio reemerged as an im-portant explanatory variable in a study of annualbankruptcies at the national level conducted byLawrence Shepard.9 Shepard concluded that the

sharp increases in debt accounted for much ofthe steep climb in bankruptcies through the early1960s, and that the subsequent leveling off ofbankruptcies resulted from the slowing uptrendin the debt-to-income ratio and from more rapidgains in household wealth. In fact, he observed,these developments should have caused the num-ber of bankruptcies to fall after the mid-1960s.Shepard attributed the absence of any decline toa vast expansion in the level of public assistance,which he believed was likely to make individualsincreasingly willing to risk the financial setbacksthat could result in bankruptcy.10

Perhaps the most thoroughly structured theo-retical approach to the causes of bankruptcy wasthat of K.J. Kowalewski." Kowalewski devel-oped an intertemporal utility-maximizationmodel that weighed a given consumer's prefer-ences between present and future consumptionagainst a budget constraint imposed by the con-sumer's endowment of present and future in-come (discounted to present value). A consumercould borrow against future income to increasecurrent consumption or could enhance futureconsumption by saving part of present income.Kowalewski introduced such realistic complica-tions as the existence of accumulated savings andnonequal interest rates on savings and borrow-ing. A key complexity examined was that ofuncertainty about future income, which could

596 Federal Reserve Bulletin • September 1988

affect the terms on which lenders would makecredit available: if actual income were to fallshort of the expected level in some future period,a consumer could be unable to meet that period'spayment obligations.

In the empirical estimation of the model,Kowalewski used quarterly data for 1961 through1979, with bankruptcy filings per capita for thenation as a whole as his dependent variable. Asexplanatory variables, he used measures of both"permanent" and "transitory" income, an inter-est rate series, and a variable for "nondiscre-tionary payments" constructed to include expen-ditures on food, utilities, and other necessities,as well as scheduled debt payments. The modelalso included three "portfolio" variables bearingupon the costs and benefits of filing for bank-ruptcy: the stock of consumer durable goods andresidential structures, household liabilities, andhousehold liquid assets, all measured in terms ofconstant dollars per capita. All of the variablesexcept the interest rate series were statisticallysignificant, with expected signs and reasonablecoefficients.12

Inasmuch as the projections of the modelthrough the end of 1981 accounted for a fairlysubstantial portion of the actual numbers ofbankruptcy cases filed, it appeared that observ-able economic factors generated more of thebankruptcy surge than most other researchershad estimated. Kowalewski found that one-thirdof the rise in bankruptcies in the two-year pro-jection period may have been attributable tochanges in the law; estimates of other investiga-tors had ranged from one-half to three-fourths.

Several studies have sought to identify thecauses of bankruptcy by inspecting the demo-graphic and financial characteristics of individualbankrupts, either by examination of actual bank-ruptcy petitions or by personal interview orquestionnaire. The findings of these several stud-ies have been consistent in most respects.

Studies of individual bankrupts in Michiganand Utah in the early 1960s found that most ofthem worked at lower-paying unskilled or semi-skilled manual labor, and that most were em-ployed at the time they filed for bankruptcy.13

These employment characteristics were verifiedby two broader surveys in the 1980s: a study of1,600 bankrupt customers of four finance compa-nies conducted by Brimmer and Company, Inc.,and a study of 1,200 bankrupts from ten differentstates carried out by researchers at PurdueUniversity.14 In both studies, about 80 percent ofthe bankrupts were employed when surveyed,generally in blue collar jobs. The Purdue studyalso observed that about 20 percent of the bank-ruptcies involved two-income families.

Age as well as occupation and income level hasemerged as an important factor in studies ofbankruptcy petitioners. Most studies have foundthat families involved in bankruptcy were rela-tively young and often had more than the averagenumber of children. The Purdue study furtherobserved that persons (of any age) who were notcurrently married and who had children weretwice as common among bankrupts as amongdebtors in general.

Some studies of individual bankrupts haveinquired into the reasons for the bankruptcydeclaration. Results are somewhat difficult tointerpret because some responses, such as "toomuch debt," might reasonably apply in virtuallyevery instance. In a 1971 study of the bankruptcyprocess, David Stanley and Marjorie Girth triedto identify the "underlying" and "immediate"causes of bankruptcy from interviews with 400former bankrupts.15 The most frequently men-tioned underlying cause was poor debt manage-ment, followed closely by family health reasonsand then by job problems, including strikes,layoffs, and loss of overtime. The most commonimmediate causes triggering a bankruptcy werethreats of legal action, poor debt management,actual legal action, and the desire to avoid payingcertain debts. The Brimmer study likewise foundoveruse of credit, employment problems, andmedical expenses among the factors cited mostoften, along with marital problems, which werementioned much more frequently than they werein the Stanley and Girth study.

On balance, then, the various studies of indi-vidual cases agree that bankruptcy (at leastthrough the early 1980s) has been experiencedmainly by lower-income households with princi-pal wage-earners employed as manual, oftenunskilled, workers. Outright unemployment

Personal Bankruptcies 597

seems to have been a less critical determinantthan the researchers had anticipated, althoughjob-related conditions, such as loss of overtime,were frequently a factor. Marital problems, largemedical bills, and other personal trauma contrib-uted to many of the decisions to file for bank-ruptcy, t

iy.'lS ()!•'

The disruption that serious financial stress bringsto individual lives is perhaps the major conse-quence of bankruptcy. It is an important concernfor sociologists and legislators alike, but one thatlies outside the predominantly macroeconomiccontext of this article. This article views theeffects of bankruptcy as they pertain to thefunctioning of the consumer credit markets, ormore broadly, to the major economic aggregates.These two spheres are not entirely separate; anissue such as the impact of personal bankruptcieson lender profit margins, for example, has impli-cations for total consumer spending through itsrole in shaping the aggregate supply function ofconsumer credit.

Effects on Credit Supply

A clear consensus on the effects of personalbankruptcy is that, in the long run, the lossesfrom discharged debts are transmitted to all otherborrowers in the form of more expensive creditor reduced availablity of credit. Researchersusually assert this conclusion on the basis ofwell-known economic principles, but say littleabout the process by which the market arrives atthe ultimate outcome. Two important aspects ofthat process involve the magnitude of the effectsof bankruptcy on profits and the real-world com-plexities faced by creditors having to assess howbankruptcies are affecting profits and to respondin an effective way.

Several studies have attempted to estimate thetotal amount of debts discharged in a year as ameasure of the cost of bankruptcy to the creditindustry and, ultimately, to the economy. Thestudies by Brimmer and Company and by thegroup at Purdue estimated bankruptcy chargeoffsin 1980 and 1981 to be about $3'/4 billion to $4>/4

billion. The Federal Reserve figure for consumercredit outstanding at the end of 1980 was $350billion; estimated losses from bankruptcy thusamounted to about 1 percent of credit outstand-ing, a figure arguably large enough to influencethe behavior of lenders that typically earn be-tween 2 and 3 percent net on their consumerreceivables.

In assessing the implications of such a lossrate, some caveats are in order. One is that asubstantial portion of the debts discharged inbankruptcy are owed to hospitals and otherclaimants that are not part of the consumer creditstatistics; thus the estimated 1 percent rate ofloss no doubt overstates actual rates of bank-ruptcy loss.16 Moreover, since creditors are con-cerned with their overall loan-loss experience,whether or not a particular bad debt was owed bya bankruptcy petitioner may not matter to thecreditor if the debt would have been charged offanyway. Only when bankruptcy results in acreditor writing off a debt that would otherwisehave been paid is the loss attributable in ameaningful way to "bankruptcy." But accordingto findings of the Purdue studies, only about aquarter of the debts owed by bankrupts at thetime of filing would have been recoverable in theabsence of the bankruptcy. That is, only $1billion of the total loss of $4 billion was truly aresult of bankruptcy.

Some data available from trade sources mayhelp to illuminate the issue of how large an effectbankruptcy declarations have on the credit lossesof lenders. The American Bankers Association(ABA) publishes annual statistics covering netloss rates on consumer lending at commercialbanks and also the proportion of losses associ-ated with bankruptcy (table 2), a part of which,as suggested above, would likely be written off inany event.17

According to the ABA data for 1978 to 1986,banks charge off about 0.5 percent of theirclosed-end installment loans in a year, give ortake 0.1 percent; the highest loss rate, in therecession year 1980, was 0.63 percent. The pro-portion of losses identified with bankruptcy dur-ing the period ranged from 15 to 24 percent.Together, these statistics suggest that bank-ruptcy losses amounted to about 0.1 to 0.2 per-cent of credit outstanding. Even during the re-

598 Federal Reserve Bulletin • September 1988

Year

19781979198019811982

1983 . . . .198419851986

19781979198019811982. . . .

1983198419851986. . . .

; ! . - • • - . : • . ' • • ;

Losses net ofrecoveries as a

percent ofcredit

outstanding

Percent oflosses due tobankruptcy1

Losses due tobankruptcy asa percent of

creditoutstanding2

Closed-end installment loans

.38

.44

.63

.50

.40

.36

.28

.39

.47

.34

.87'.29.96.67

.34

.27

.35

.40

15.116.419.923.123.6

21.821.923.022.7

Jank-card credit

n.a.n.a.n.a.n.a.n.a.

25.625.237.932.7

.06

.07

.13

.12

.09

.08

.06

.09

.11

n.a.n.a.n.a.n.a.n.a.

.34

.32

.51

.46

1. The ABA reports data for five asset-size categories of banks, butno overall average figure for all banks. For this table, the average forall banks was calculated by weighting the ABA's figure for each sizegroup by the proportion of total consumer installment credit (or totalbank-card credit, as appropriate) held by the given group.

2. Calculated for this table by multiplying column I by column 2.n.a. Not available.SOURCE. American Bankers Association, Retail Bank Credit Re-

port, issues for 1981 through 1987.

cent surge in bankruptcies, losses at commercialbanks due to personal bankruptcy rose only 0.05percentage point—from 0.06 in 1984 to 0.11 per-cent in 1986 (latest data available). While thatperformance represents an increase of 80 per-cent, even steeper than the rise in the number ofbankruptcies nationally, the incremental loss rate

has an almost negligible impact on profitability.Similar statistics for bank credit cards revealhigher loss ratios than for closed-end lending,and somewhat higher proportions attributable tobankruptcies, but they still show rather smallvariations from year to year in the proportion ofoutstandings written off in bankruptcy cases(table 2).

Table 3 presents net earnings and credit lossstatistics on installment loans and bank-cardcredit from another source, the Federal Re-serve's Functional Cost Analysis (FCA).18 Thecredit loss ratios in the FCA are somewhat higherthan the ABA estimates, but are still reasonablyclose and show the same patterns year to year.The loss ratios are clearly high enough relative toearnings so that substantial changes in loss expe-rience could significantly affect a firm's bottomline.

During the years examined, however, lossrates just as clearly have not been the primedeterminant of variation in net earnings onclosed-end installment loans. Net earnings havefluctuated considerably more than have creditlosses for this type of lending. The largest move-ment in loan losses was the increase of 0.28percentage point in 1980, which, other thingsequal, should have reduced net earnings by thatamount. However, net earnings actually declined0.86 percentage point, or three times as much.Similarly, big increases in profitability occurredin 1982 and 1983, but in tandem with only mod-erate dips in loss rates. Then in 1984, profitabilityeased off despite the positive influence of anothersmall decline in chargeoffs. Loss rates have beenhigher on credit cards than on closed-end loans,and a substantial rise in credit-card losses appar-

• . ' ! ] M i ! l ' . i ! U ! .

; ! • • ! - i r , i , V ' . i l i

Type of credit1979

• . ! ( ! o n l . t ; ' • ( < ! : n ! • a i U t n ; - .

1980 1981 1982 1983 1984 1985 1986

Installment creditNet earningsCredit losses

Bank-card creditNet earningsCredit losses

2.20.55

1.801.75

1.34.83

-1.782.35

1.63.66

1.332.15

2.83.55

2.891.72

3.20.42

2.461.21

2.85.38

3.741.09

SOURCE. Federal Reserve Bank of New York, Functional Cost Analysis, annual issues.

2.74.39

3.991.68

2.62.61

3.282.23

Personal Bankruptcies 599

ently accounted for most of a drop in profitabilityin 1986. On the whole, however, for this type oflending also, changes in net earnings do notappear closely related to the pattern of creditlosses.

In trying to make the leap from statisticalevidence about how bankruptcies affect profits tothe long-run adjustments in rates and creditterms that are indicated by theory, considerationof the circumstances in which lenders have tomake their pricing and marketing decisions maybe helpful. A surge in bankruptcies would tend toreduce profits by causing larger writeoffs—but,as just discussed, the size of any drop in profitswould be rather small, making a creditor's re-sponse more problematic. For instance, a lenderfirst would have to decide whether an observeddecline in net earnings from, say, 1.65 percent to1.55 percent, was a development to which aspecific response was needed, and would thenhave to determine whether the worsened perfor-mance was attributable to bankruptcies ratherthan to some other factor.

If bankruptcy were in fact isolated as a causeof the increased writeoffs, the creditor wouldhave to choose among several possible re-sponses: raise interest rate quotations across theboard, set higher minimum standards to qualifyfor loans, increase collateral requirements, orperhaps try to identify potential bankrupts moreprecisely so they can be weeded out. The lastresponse would entail direct costs of its own, andthe other alternatives could have undesirablecompetitive consequences. For instance, unlessother credit suppliers also opted to nudgetheir interest rates up, a price-raising creditormight find itself losing its most creditworthyapplicants.

Another factor that may deter lenders fromresponding quickly to an increase in bankrupt-cies is that other developments in the economycan overshadow the specific effect of bankruptcytrends. For example, if money costs are falling,as they were during the mid-1980s, bottom-lineresults may be improving even if bankruptcylosses are rising. If so, a lender may deliberatelychoose to lower credit standards and tolerate ahigher loss rate because of the enhanced profit-ability of "good" loans.

/.;//< r . ' v •>n flu' IJ <>notnx

The foregoing discussion of the effects of bank-ruptcy on profitability has implications for issuesthat extend beyond the operation of a creditdepartment. Economic policymakers and regula-tors of financial institutions, for instance, mightbe concerned with the possible effects of bank-ruptcy on economic activity and on the sound-ness of lending institutions. On both counts theevidence suggests that such effects are small.With losses due to bankruptcy apparently ac-counting for between 0.1 and 0.5 percent ofvarious types of consumer receivables at banks,and with consumer lending constituting less thana fifth of total bank lending, even sharp increasesin personal bankruptcy seem unlikely to endan-ger the financial health of these institutions toany significant extent. Overall economic activitymight be constrained if financially strapped indi-viduals decided to repair their balance sheets bycutting back on their spending, or if creditorsresponded to rising bankruptcy losses by tight-ening their loan approval standards, thereby pre-venting some credit seekers from makingintended expenditures. But, as the earlierdiscussion has indicated, creditors may well havelittle incentive to change lending standards inview of the relatively small impact of bankrupt-cies on earnings and the uncertain outcome of ashift in strategy.

In practice, the principal macroeconomic useof bankruptcy statistics has been in qualitativeassessments of the financial state of the house-hold sector, in which bankruptcies serve as oneof many barometers of the primary, but harder-to-measure, concept of financial stress. Gener-ally speaking, such variables as bankruptcies andloan delinquency rates have not been very widelyor very successfully used in econometric analy-ses of consumer behavior. They are typicallyviewed as providing supplementary rather thanfundamental clues as to the prospective strengthof consumer demand. Nevertheless, the sharprise in bankruptcies since 1984 has stimulatedwider interest in the causes and consequences ofbankruptcy. The next section provides a detailedexamination of the forces that may underlie thisrecent trend.

600 Federal Reserve Bulletin D September 1988

' . ) } ; i i i l . i l i i i i v ' l i 1 - . . i i i i ! I l l ' " u u n j i ' i i o i i v i l M i n i r i J i ' b l

Number per 1,000 persons

I I I I I i I

' B a n k r u p t c i e s

I 1 I I I I

2.0

1.5

1.0

I I i1965 1970 1975 1980 1985 1988

i'l'Ci'Ni TKi'NDS: A I'lili'l'tll-n LiH/k

What is particularly noteworthy about the surgein bankruptcies since 1984 is that it has occurredduring an extended economic upswing. The ratesof increase in bankruptcy for 1985 and 1986 wereunmatched in any other year since 1950 that wasnot a recession year. Many observers have notedthe unevenness of the current expansion, how-ever, citing persistently distressed conditions inthe "oil patch" states and, until very recently,the centers of heavy manufacturing in the Mid-west. Such regions could be generating a highvolume of personal bankruptcies despite the na-tion's general prosperity.

In fact, the number of bankruptcies has risenmost rapidly in the major oil-producing states.On the other hand, subtracting these states fromthe total still leaves a very rapid rate of increasenationally. Between the second quarters of 1985and 1986, for instance, bankruptcies increased 36percent nationally, while soaring 62 percent infive oil patch states (table 4). Yet, when thesefive states were excluded from the calculations,the growth in bankruptcies still topped 30 percentbetween the two quarters. In fact, nearly three-

fourths of all states experienced increases inbankruptcy of more than 25 percent over thatperiod. Thus the recent surge does not appearattributable in any significant way to specialproblems in specific regions.

Several of the quantitative studies discussedhere cited rapid growth in consumer debt as akey factor underlying rapid growth in bankrupt-cies. Such results, however, were dominated bythe sharp upward movements in both debt andbankruptcy for nearly two decades after WorldWar II; movements in debt (relative to income)and bankruptcies (per capita) were less closelycorrelated after the mid-1960s (chart 2). Both thedebt-burden measure and bankruptcies per cap-ita fluctuated around flat trendlines during the1970s, with little uniformity in the size or timingof movements in the two series. Such diver-gences might indicate an inherently weak rela-tionship between debt and bankruptcy. Or theymight mean only that the relationship is inoper-ative below certain key levels or rates of increasein the burden of debt on income. The linkagebetween aggregate debt and bankruptcy couldstill be strong beyond some threshhold level ofdebt burden, even though it is likely to be ob-

Bnnki upk 'k 's III Ihi' United Stales ami m maior oil producing status

Item

U.S. totalFive "oil patch" states'Total, less oil patch states. . . .

1985:2

84,2438,428

75,815

Number of cases

1986:2

114,38413,682

100,702

1987:2

122,68916,399

106,290

Percent change

1985:2-1986:2 1986:2-1987:2

35.8 7.362.3 19.932.8 5.5

1. Oklahoma. Texas, Louisiana, Colorado, and Wyoming.SOURCE. Administrative Office of the U.S. Courts.

Personal Bankruptcies 601

scured by statistical tests covering periods whengrowth in debt has been subdued.

But, as pointed out, the aggregate debt-to-income ratio broke out of its meandering patternand climbed quite sharply between 1984 and1988. It rose from the level of around 14 percentthat had held during most of the previous decade,to a record 19 percent by mid-1987. Thus, onceagain, during the current business expansion, arapid rise in bankruptcies and a strong upsurge indebt burden have occurred together. This corre-spondence in itself hardly proves that a closecausal connection exists, but, with unemploy-ment trending downward and household wealthand incomes growing substantially during theperiod, the growth of debt appears to be the onemajor macroeconomic force that moved in adirection consistent with increases in bankrupt-cies.

Aggregate figures on debt can mask importantdistributional features that may affect bank-ruptcy rates. Findings from two major surveys ofconsumer finances shed some light on thisissue.19 One fact these findings point up is thatdebt is concentrated among people with theincome and assets to cover it. Nevertheless,between the two survey years of 1983 and 1986,a large increase occurred in the proportion ofdebt that was held by people with high ratios ofdebt to income (40 percent or higher). Theheavily indebted category held 7 percent of thedebt covered in 1983's survey, but those whowere in that category in 1986 held 16 percent, achange that suggests that the pool of potentialbankrupts may have been considerably larger inthe latter year. Only about half of the high-debtrespondents in 1986 had asset holdings (includinghome equity) large enough to fully retire theirdebts—considerably less than the 80 percent ofall debtors whose assets provided full coverageof debts in 1983.

Changing attitudes toward bankruptcy may beanother factor that helps to account for theaccelerated pace of bankruptcy filings. This hy-pothesis is not readily testable, however. Attitu-dinal changes are difficult to measure, and be-cause they generally occur gradually, areunlikely to cause sudden shifts in behavior, suchas characterized the course of bankruptcy filingsin 1985-86. On the other hand, a gradual redirec-

tion over the years in attitudes toward bank-ruptcy could have laid the groundwork for amore pronounced response to some other trigger-ing variable, such as debt burden, whenever thatvariable happened to move in a particular way.

The evidence for changing attitudes towardbankruptcy is largely circumstantial. However,several societal developments have seemed todiminish the stigma that once attached to bank-ruptcy. The simple fact that consumer credit ismore widely used today has made bankruptcyless rare, and therefore has rendered the bank-rupt individual a less conspicuous figure. Cer-tainly, too, the many revisions in the laws andregulations concerning debtor rights, from theTruth-in-Lending Act, to restrictions on collec-tion tactics of creditors, to the Bankruptcy Re-form Act of 1978 itself, have fostered the notionthat bankruptcy is not necessarily a shamefulprocess resulting from personal failings, but of-ten a perfectly respectable means of handling asituation for which the debtor may be largelyblameless. By the same token, the laws them-selves may be a reflection of changed attitudes.

Advertising by lawyers—which was made le-gally permissible in 1977—also has been cited bysome commentators as a possible stimulant tobankruptcies. Measurement problems also makethis notion difficult to test empirically, but Peter-son and Aoki attempted to do so by constructinga variable based on a count of the number ofnewspaper ads by bankruptcy attorneys in vari-ous localities. In the two quarters they studied,the variable did not help to explain differences inbankruptcy rates among states; nonetheless, theproposition seems reasonable that such advertis-ing helps create a climate in which the declara-tion of bankruptcy is more readily seen as alegitimate response to financial distress.

Other social factors could be contributing atleast in a small way to the rise in bankruptcies.Some surveys of individual bankrupts have sug-gested that marital problems often play a role inbankruptcy decisions, and the divorce rate—aconcrete, though perhaps imperfect, measure ofsuch problems—rose steadily in the 1960s and1970s. Inclusion of the national divorce rate byShepard in his model of bankruptcy did notenhance the model's explanatory power, but twoother studies have found differences in divorce

602 Federal Reserve Bulletin • September 1988

rates among states to help account for interstatedifferences in the number of bankruptcies percapita.20 In any case, stability in the overalldivorce rate since 1980 seems to belie any notionthat a sudden worsening of marital relationsmight account for the bankruptcy activity inrecent years.

Paradoxically, the trend toward two-earnerfamilies might provide some marginal boost tothe likelihood of bankruptcy. If people base thelevels of their spending and borrowing on thetotal amount of their dual incomes, interruptionof either income stream could jeopardize a fami-ly's financial stability. On the other hand, it couldbe argued, multiple sources of income reduce therisk that any single employment problem willdevastate a family's financial position. A lotwould depend therefore on whether a familytreated a second income as a buffer or used it tosupport proportionally higher levels of spendingand debt.

In sum, the rise in bankruptcies since 1984seems most readily attributable to the large ex-pansion of consumer debt, which has boosted the

aggregate indebtedness of households from 14 to19 cents per dollar of disposable income. Alessening of the stigma of bankruptcy and theevolution of a legal structure favorable to bank-rupts have helped establish a setting in whichbankruptcy may be more readily embraced byfinancially strapped households.

Whether the resort to bankruptcy has becomefrequent enough to provoke a curtailment oflending seems doubtful considering the still smallimpact of bankruptcy on profit margins and theabsence of any evidence that creditors havetightened loan standards. Moreover, the stabilityof the debt-to-income ratio since its peak in early1987 provides some hope of moderation in bank-ruptcy increases—indeed, last year's 10 percentrise (and an equivalent rate of increase early thisyear) already represents considerable abatementfrom the previous two years. Nevertheless, thepossibility that rising numbers of bankruptcieswill begin to affect lending or spending patternscannot be dismissed, particularly if the currentstrength in employment and household net worthshould wane.

1. The discussion of debt in this article is limited toconsumer debt, although home mortgage debt has also grownsubstantially since World War II. However, insofar as amortgage usually represents acquisition of an appreciatingasset and the mortgage lender's lien on the property is notcompromised by a mortgagee's bankruptcy, mortgage debt isseldom a precipitating cause of bankruptcy. Moreover, toinclude mortgage debt in a measure of debt burden withouttaking account of rent payments in some fashion would tendto portray the household sector's financial situation as wors-ening whenever a shift away from renting to homeownershipwas taking place. On the whole, it seemed best to comparebankruptcy trends with a form of debt that was generallyunsecured or eollateralized by depreciating assets, a practicefollowed in most of the research reviewed later in thisarticle.

2. National bankruptcy statistics are compiled by theAdministrative Office of the U.S. Courts from case countsprovided by each district court.

3. At the same time, the code contained an overrideprovision that /permitted states to opt out of the federalexemptions within a two-year period by enacting new legis-lation of their own. In all, 32 states exercised this right. Thenew state exemptions were generally less liberal than thefederal standard, but frequently more liberal than the previ-ous state exemption had been.

4. Frederick C. Yeager, "Personal Bankruptcy and Eco-

nomic Stability," Southern Economic Journal, vol. 41 (July1974), pp. 96-102.

5. Vincent P. Apilado, Joel J. Dauten, and Douglas E.Smith, "Personal Bankruptcies," Journal of Legal Studies,vol. 7 (June 1978), pp. 371-91.

6. William J. Boyes and Roger L. Faith, "Some Effects ofthe Bankruptcy Reform Act of 1978," Journal of Law andEconomics, vol. 29 (April 1986), pp. 139-49; and CharlieCarter, "The Surge in Bankruptcies: Is the New Law Re-sponsible?" Federal Reserve Bank of Atlanta, EconomicReview, vol. 67 (January 1982), pp. 20-30.

7. Richard L. Peterson and Kiyomi Aoki, "BankruptcyFilings Before and After Implementation of the BankruptcyReform Law," Journal of Economics and Business, vol. 36(February 1984), pp. 95-105.

8. By the period studied by Peterson and Aoki, the gar-nishment process had been made generally less onerous thanbefore both by provisions in federal law that took effect in1970 and by widespread revisions at the state level. Theprincipal changes reduced the proportion of a debtor's wagesthat could be garnished and prevented employers from firingworkers because their wages were subjected to garnishment.Some states prohibited garnishment entirely. With generallymore lenient practices and with less variation among states,it is not surprising that garnishment laws were less of a factorin explaining state-level differences in bankruptcies in thePeterson-Aoki study.

9. Lawrence Shepard, "Personal Failures and the Bank-ruptcy Reform Act of 1978," Journal of Law and Economics,vol. 27 (October 1984), pp. 419-37.

Personal Bankruptcies 603

10. While the statistical results were not inconsistent withsuch a thesis, the strong time trends characterizing bothbankruptcies and transfer payments could reflect coincidenceas well as causation. And on strictly theoretical grounds, agenerous system of transfer payments might be expected toserve less as a safety net to make people more comfortableabout bankruptcy than as a buffer to help them avoid bank-ruptcy.

11. K.J. Kowalewski, "Personal Bankruptcy: Theory andEvidence," Federal Reserve Bank of Cleveland, EconomicReview (Spring 1982), pp. 1-29.

12. Another utility-maximization model of bankruptcychoice is presented in Michelle J. White, "Personal Bank-ruptcy Under the 1978 Bankruptcy Code: An EconomicAnalysis," Indiana Law Journal, vol. 63 (1987-88), pp. 1-53.White's incorporation of economic variables is less extensivethan Kowalewski's, but her examination of legal effects ismore direct. In contrast to Kowalewski's aggregate time-series approach, White's model examines differences amongcounties in bankruptcies per capita, a framework that sheuses to study the effects of different levels of asset exemp-tions and to look at straight bankruptcy and wage-earnerplans separately. One conclusion of White's study is that thenumber of bankruptcies responds about equally to differencesof comparable magnitudes in exemption levels and in unem-ployment rates.

13. Robert Dolphin, Jr., "An Analysis of Economic andPersonal Factors Leading to Consumer Bankruptcy," Occa-sional Paper 15 (Michigan State University, Graduate Schoolof Business Administration, Bureau of Business and Eco-nomic Research, 1965); and Grant L. Misbach, "PersonalBankruptcy in the United States and Utah," (MBA thesis,University of Utah, College of Business, May 1964).

14. Andrew F. Brimmer, Public Policy and the EconomicImplications of Personal Bankruptcies, in Hearings on theBankruptcy Reform Act of 1978, before the Subcommittee on

Courts of the Senate Judiciary Committee, 97 Cong. 1 Sess.(Government Printing Office, 1981), pp. 6-38; Credit Re-search Center in cooperation with Arthur D. Little, Inc. andOpinion Research Corporation, Consumers' Right to Bank-ruptcy: Origins and Effects, Consumer Bankruptcy Study,Monograph 23 (Purdue University, Krannert GraduateSchool of Management, Credit Research Center, 1982), vol. 1and A. Charlene Sullivan, Personal Bankruptcy: Causes,Costs and Benefits, Consumer Bankruptcy Study, Mono-graph 24 (Purdue University, Krannert Graduate School ofManagement, Credit Research Center, 1982), vol. 2.

15. David T. Stanley and Marjorie Girth, with the collab-oration of Vern Countryman and others, Bankruptcy: Prob-lem, Process, Reform (Brookings Institution, 1971).

16. Federal Reserve statistics on consumer credit covercommercial banks, finance companies, credit unions, savingsinstitutions (savings and loans, federal savings banks, andmutual savings banks), retail stores, and gasoline companies.

17. American Bankers Association, Retail Bank CreditReport, issues for 1981 through 1987.

18. Federal Reserve Bank of New York, Functional CostAnalysis, annual issues.

19. The surveys were conducted in 1983 and 1986 by theSurvey Research Center at the University of Michigan onbehalf of the Federal Reserve and other sponsoring federalagencies, under the title "Survey of Consumer Finances."Results summarized here were presented in Robert B. Avery,Gregory E. Elliehausen, and Arthur B. Kennickell,"Changes in Consumer Installment Debt: Evidence from the1983 and 1986 Surveys of Consumer Finances," FEDERALRESERVE BULLETIN, vol. 73 (October 1987), pp. 761-78.

20. See White, "Personal Bankruptcy," and A. CharleneSullivan and Debra Drecnik Worden, "The Law, the Econ-omy, and Consumer Demand for Debt Relief under theBankruptcy Code" (Purdue University, Krannert GraduateSchool of Management, no date).

604

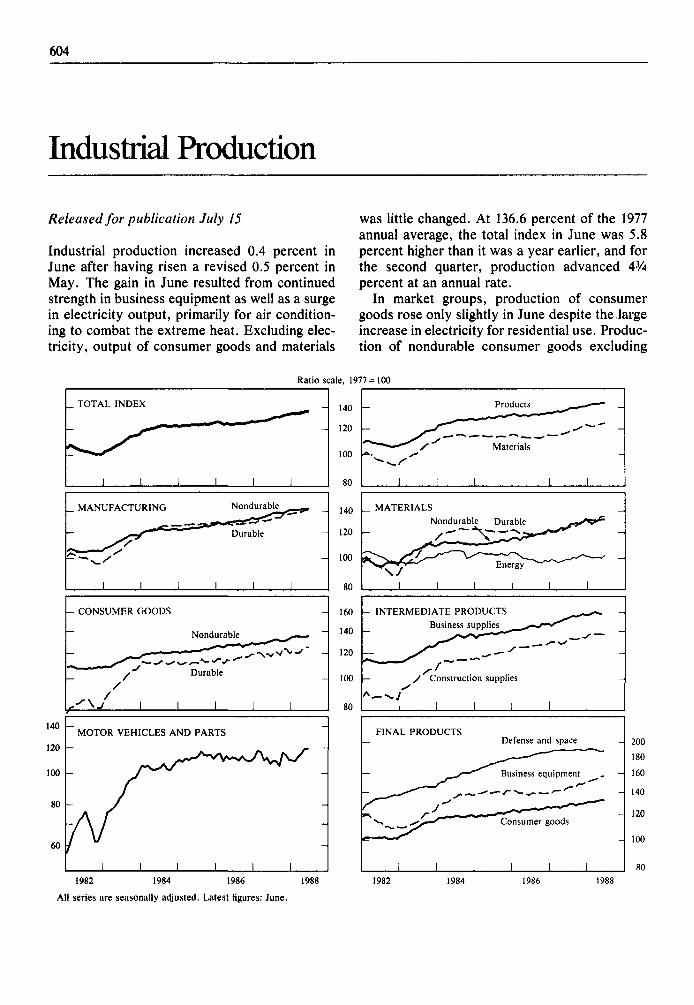

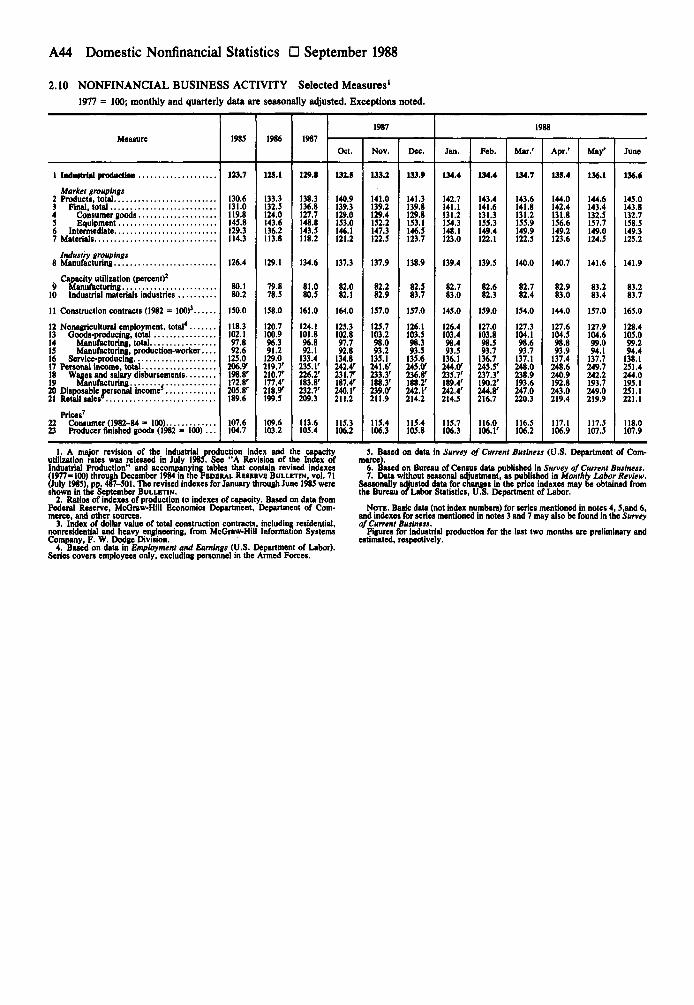

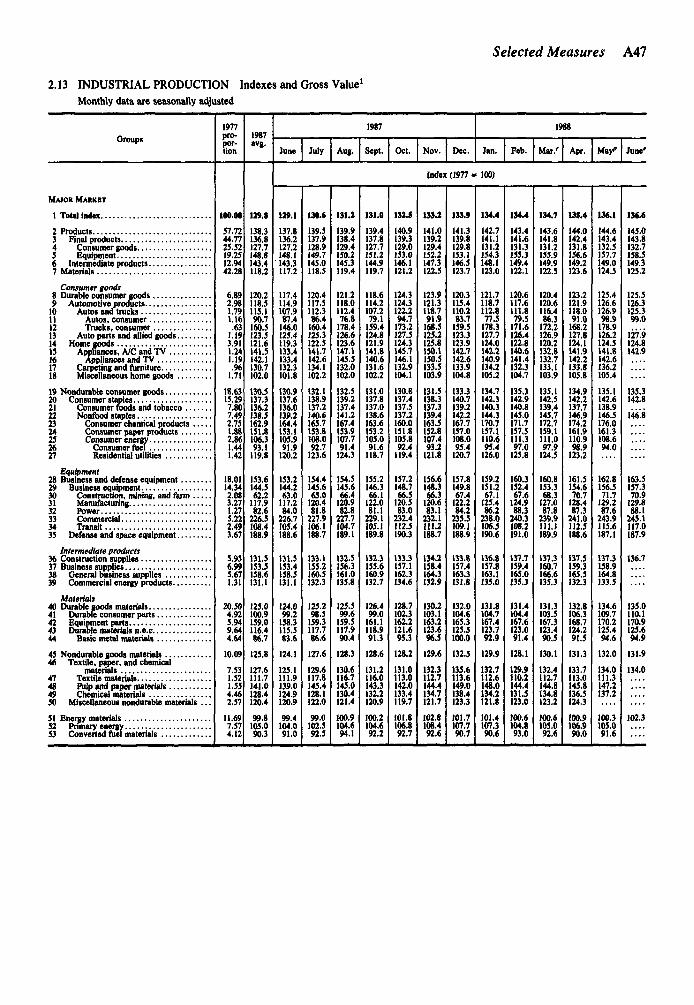

Industrial Production

Released for publication July 15

Industrial production increased 0.4 percent inJune after having risen a revised 0.5 percent inMay. The gain in June resulted from continuedstrength in business equipment as well as a surgein electricity output, primarily for air condition-ing to combat the extreme heat. Excluding elec-tricity, output of consumer goods and materials

was little changed. At 136.6 percent of the 1977annual average, the total index in June was 5.8percent higher than it was a year earlier, and forthe second quarter, production advanced 43Apercent at an annual rate.

In market groups, production of consumergoods rose only slightly in June despite the largeincrease in electricity for residential use. Produc-tion of nondurable consumer goods excluding

Ratio scale, 1977 = 100

140

120

100

80

60

_ TOTAL

1

INDEX

s*—i

_ MANUFACTURING

-

1

y

i

- CONSUMER GOODS

:

—*

~ MOTOR

L-

1

/

1

I

I

1

Nondurable

Durable

1

Nondurable

Durable

1

VEHICLES AND PARTS

y^-A/

/

i 1 1

1

-

1

-

• • —

-

y -

-

_

1

1982 1984 1986 1988

140

120

100

80

140

120

100

80

160

140

120

100

80

-

—

r—^i

Products-^*-——

y Materials

1 1 1

_ MATERIALS

-

1

Nondurable Durable

f_y v ^ \ _^ Energy

1 1 1

- INTERMEDIATE PRODUCTS

-

— ^

Business supplies _^»»

^ '

' Construction supplies

1 1 1

-

\ 1

^ • ^ ^

1 1

. / • —

-

1 1

FINAL PRODUCTSi— Defense and space

-

1

^^-y"^ Business equipment

•f~r Consume

1 1 1

r goods

1 I

200

180

160

140

120

100

80

1982 1984 1986 1988

All series are seasonally adjusted. Latest figures: June.

605

Group

1977 = 100

1988

May June

Percentage change from preceding month

1988

Feb. Mar. Apr. May June

Percentagechange,

June 1987to June

1988

Major market groups

Total industrial production

Products, totalFinal products

Consumer goodsDurableNondurable

Business equipment..Defense and space

Intermediate products..Construction supplies

Materials

ManufacturingDurableNondurable

MiningUtilities

136.1

144.6143.4132.5125.4135.1156.5187.1149.0137.3124.5

136.6

145.0143.8132.7125.5135.3157.3187.9149.3136.7125.2

.0

.5

.3

.1- 1 . 0

.4

.8

.2

.9

.6- .7

.2

.2

.1-.1- .2-.1

.6- .6

.3- .3

.3

.5

.2

.4

.52.3-.2

.8-.7-.5

.1

.9

.5

.4

.6

.61.8.1

1.3- .8-.2-.1

.7

.4

.3

.3

.1

.0

.1

.5

.4

.2- .4

.6

Major industry groups

141.6141.2142.1103.4111.8

5.8

5.25.54.36.93.49.1- . 44.24.06.8

141.9141.7142.2104.0114.7

.1

.4- .2

-1.7.3

.4

.3

.51.2

-2.0

.5

.6

.32.1

-2.2

.6I.I

- . 1-1.4

.9

.2

.3

.1

.62.6

5.97.43.94.94.9

N O T E . Indexes are seasonally adjusted.

electricity was sluggish. Auto assemblies in June,at an annual rate of 7.5 million units, were thesame as in May. Production of light trucks, whilestill at a high level, declined last month. Outputof home goods edged up, but has changed little,on balance, since the end of last year. In con-Total industrial production—RevisionsEstimates as shown last month and current estimates

Month

MarchAprilMayJune

Index (1977=100)

Previous Current

Percentage changefrom previous

months

Previous Current

134.7 134.7 .2 .2135.5 135.4 .6 .5136.0 136.1 .4 .5

136.6 . . . .4

trast, production of business equipment contin-ued to post solid gains in June, with strength inall major components except construction, min-ing, and farm machinery.

Output of construction supplies remainedweak for the fourth successive month. Produc-tion of durable materials rose slightly in Juneafter two months of rapid advances. Nondurablematerials were unchanged as chemicals rose fur-ther, but textiles and paper declined.

In industry groups, manufacturing output rose0.2 percent in June. Durable manufacturing wasup 0.3 percent, with fabricated metals and elec-trical and nonelectrical machinery registering thelargest gains. Production at utilities, mainly elec-tric, was up 2.6 percent, and mining output rose0.6 percent.

Statement to Congress

607

Statement by Alan Greenspan, Chairman, Boardof Governors of the Federal Reserve System,before the Committee on Banking, Housing, andUrban Affairs of the U.S. Senate, July 13, 1988.

I appreciate this opportunity to review with yourecent and prospective monetary policy and theeconomic outlook. I would also like to provide abroader perspective by discussing in some detailour nation's longer-term economic objectives,the overall strategy for fiscal and monetary poli-cies needed to reach those objectives, and theappropriate tactics for implementing monetarypolicy within that strategic framework.

THE ECONOMIC SETTING AND MONETARYPOLICY SO FAR IN 1988

The macroeconomic setting for monetary policyhas changed in some notable respects since Itestified last February. At that time, the fullaftereffects of the stock market plunge on spend-ing and financial markets were still unclear.While most members of the Federal Open Mar-ket Committee were forecasting moderategrowth, in view of rapid inventory building andsome signs of a weakening of labor demand, thepossibility of a decline in economic activity couldnot be ruled out. To guard against this outcome,in the context of a firmer dollar on exchangemarkets, the Federal Reserve undertook a fur-ther modest easing of reserve pressures in lateJanuary, which augmented the more substantialeasing after October 19. Short-term interest ratescame down another notch, and, with a delay,helped to push the monetary aggregates higherwithin their targeted annual ranges.

In the event, the economy proved remarkablyresilient to the loss of stock market wealth.Economic growth remained vigorous through thefirst half of the year. Continuing brisk advancesin exports, together with moderating growth inimports, supported expansion in output, espe-

cially in manufacturing. Some strengthening alsowas evident in business outlays for equipment,especially computers, and consumer purchasesof durables, including autos.

Financial markets also returned to more nor-mal functioning. Although trading volumes didnot regain precrash levels in many markets, pricevolatility diminished somewhat and quality dif-ferentials stayed considerably narrower than inthe immediate aftermath of the stock marketplunge. In response, the Federal Reserve gradu-ally was able to restore its standard procedure ofgearing open market operations to the intendedpressure on reserve positions of depository insti-tutions. We thereby discontinued the procedureof reacting primarily to day-to-day variations inmoney market interest rates that had beenadopted right after the stock market break.

As the risks of faltering economic expansionand further financial market disruptions dimin-ished, the dangers of intensified inflationary pres-sures reemerged. Utilization of labor and capitalreached the highest levels in many years, andhints of acceleration began to crop up in wageand price data. Strong gains in payroll employ-ment that continued through the spring combinedwith slower growth in the labor force to lower theunemployment rate about V* percentage point,even before the strong labor market report forJune; the industrial capacity utilization ratemoved up as well. In part reflecting the payrolltax increase, broad measures of hourly compen-sation picked up somewhat in the first quarter.Prices for a wide range of domestic and importedindustrial materials and supplies rose even moresteeply than they did last year. The price inflationof finished goods has not reflected this step-up inprice increases for intermediate goods, in part asproductivity gains kept unit labor costs undercontrol. Even so, continued increases in materi-als prices at the recent pace were seen as point-ing to a potential intensification in inflation moregenerally, since based on historical experience

608 Federal Reserve Bulletin • September 1988

such increases have tended to show through tofinished goods prices.

In these circumstances, the Federal Reservewas well aware that it should not fall behind inestablishing enough monetary restraint to effec-tively resist these inflationary tendencies. TheSystem took a succession of restraining stepsfrom late March through late June. The shortest-term interest rates gradually rose to levels nowaround highs reached last fall. Responding aswell to the unwinding of a tax-related buildup inliquid balances, M2 and M3 growth slowed no-ticeably after April.

In contrast to the shortest-maturity interestrates, long-term bond and mortgage rates, thoughalso above February lows, still remain well be-low last fall's peaks. The timely tightening ofmonetary policy this spring, along with percep-tions of better prospects for the dollar in foreignexchange markets in light of the narrowing in ourtrade deficit, seemed to improve market confi-dence that inflationary excesses would beavoided. Both bond prices and the dollar ralliedin June despite increases in interest rates inseveral major foreign countries and jumps insome agricultural prices resulting from thedrought in important growing areas.

THE ECONOMIC OUTLOOK ANDMONETARY POLICY THROUGH 1989

The monetary actions of the first half of the yearwere undertaken so that economic expansioncould be maintained, recognizing that to do soadditional price pressures could not be permittedto build and that progress toward external bal-ance had to be sustained. The projections ofFOMC members and nonvoting presidents indi-cate that they do expect economic growth tocontinue and inflation to be contained.

The central tendency of FOMC members' ex-pectations of 23/4 to 3 percent for real growth ofGNP over the four quarters of this year implies adeceleration over the rest of the year to a pacemore in line with their expectations of realgrowth of 2 to 2'/2 percent over 1989 and with thelong-run potential of the economy. The droughtwill reduce farm output for a time, and it isimportant that nonfarm inventory accumulationslow before long if we are to avoid a troublesome

imbalance. Still, further gains in our internationaltrade position should continue to provide a majorstimulus to real GNP growth through next year,reflecting the lagged effects of the decline in theexchange value of the dollar through the end oflast year. Although the month-to-month patternin our trade deficit can be expected to be erratic,the improvement in the external sector on bal-ance over time is expected to replace much of thereduced expansion in domestic final demandsfrom our consumer, business, and governmentsectors.

Employment growth is anticipated to be sub-stantial, though some updrift in the unemploy-ment rate may occur over the next year and ahalf. Capacity utilization could well top out soon,as growth in demands for manufactured goodsslows to match that of capacity.

Considering the already limited slack in avail-able labor and capital resources, a leveling of theunemployment and capacity utilization rates isessential if more intense inflationary pressuresare to be avoided in the period ahead. Otherwise,aggregate demand would continue growing at anunsustainable pace and would soon begin tocreate a destabilizing inflationary climate. Supplyconditions for materials and labor would tightenfurther, and costs would start to rise more rap-idly; businesses would attempt to recoup profitmargins with further price hikes on final goodsand services. These faster price rises would, inturn, foster an inflationary psychology, cut intoworkers' real purchasing power, and prompt anattempted further catchup of wages, setting inmotion a dynamic process in which neither work-ers nor businesses would benefit. The hard-wongains in our international competitiveness wouldbe eroded, with feedback effects depressing theexchange value of the dollar. Excessive domesticdemands and inflation pressures in this country,with its sizable external deficit, would be disrup-tive to the ongoing international adjustment oftrade and payments imbalances.

Not only the reduced slack in the economy butalso several prospective adjustments in relativeprices have accentuated inflation dangers. One isthe upward movement of import prices relativeto domestic prices, which is a necessary part ofthe process of adjustment to large imbalances ininternational trade and payments. Another is the

Statement to Congress 609

recent drought-related increases in grain andsoybean prices. It is essential that we keep theseprocesses confined to a one-time adjustment inthe level of prices and not let them spill over to asustained higher rate of increase in wages andprices. Elevated import and farm prices must beprevented from engendering expectations ofhigher general inflation, with feedback effects onlabor costs. A more serious long-run threat toprice stability could come from government ac-tions that introduced structural rigidities andincreased costs of production. Protectionist leg-islation, inordinate hikes in the minimum wage,and other mandated programs that would imposecosts on U.S. producers would adversely affecttheir efficiency and international competitive-ness.

The costs to our economy and society ofallowing a more intense inflationary process tobecome entrenched are serious. As the experi-ence in the past two decades has clearly shown,accelerating wages and prices would have to becountered later by quite restrictive policies, withunavoidably adverse implications for productionand employment. The financial health of manyindividual and business debtors, as well as ofsome of their creditors, then would be threat-ened. The long-run costs of a return to higherinflation and the risks of this occurring undercurrent circumstances are sufficiently great thatFederal Reserve policy at this juncture might bewell advised to err more on the side of restric-tiveness rather than of stimulus.

We believe that monetary policy actions todate, together with the fiscal restraint embodiedin last fall's agreement between the Congress andthe administration, have set the stage for contain-ing inflation through next year. The central ten-dency of FOMC members' expectations for in-flation in the GNP deflator ranges from 3 to 33/4percent over this year to 3 to 4'/2 percent nextyear. But in one sense the GNP deflator under-states this year's rate of inflation, and the com-parison with next year overstates the pickup.The deflator represents the average price of finalgoods and services produced in the United Statesor, equivalently, domestic value added, usingcurrent quantity weights. This measure was arti-ficially held down in the first quarter by a shift inthe composition of output; especially by the

surge in sales of computers whose prices havedropped sharply since the 1982 base year usedfor constructing the deflator. Indeed, if the de-flator were indexed with a 1987 base year, itwould have risen appreciably faster in the firstquarter.

Another understatement of inflation in the de-flator this year arises from its exclusion of im-ported goods, which are not directly encom-passed because they are produced abroad. Inpart because import prices have continued to risesignificantly faster than prices of domesticallyproduced goods, consumer price indexes haveincreased more than the GNP deflator.

The FOMC believes that efforts to containinflation pressures and sustain the economic ex-pansion would be fostered by growth of themonetary aggregates over 1988 well within theirreaffirmed annual ranges of 4 to 8 percent, fol-lowed by some slowing in money growth over thecourse of next year. M2 should move close to themidpoint of its range by late 1988 if depositorsreact as expected to the greater attractiveness ofmarket instruments, compared with liquid moneybalances, that was brought about by recent in-creases in short-term market rates relative todeposit rates. M3 could end the year somewhatabove its midpoint, though comfortably within itsrange if depository institutions retain their recentshare of overall credit expansion. The debt ofnonfinancial sectors, which so far this year hasbeen near the midpoint of its reaffirmed monitor-ing range of 7 to 11 percent, is anticipated to postsimilar growth through the year-end.

For 1989, the FOMC has underscored its in-tention to encourage progress toward price sta-bility over time by lowering its tentative rangesfor money and debt. We have preliminarily re-duced the growth range for M2 by 1 full percent-age point, to 3 to 7 percent; last February, theFOMC also had reduced the midpoint of the 1988range for M2 by 1 percentage point from that for1987. We have adjusted the tentative 1989 rangefor M3 downward by Vz percentage point, to VAto Vh percent. This configuration is consistentwith the observed tendency for M3 velocity overtime to fall relative to the velocity of M2; overthe last decade, the Federal Reserve's rangesfrequently allowed for faster growth of M3 thanof M2. The monitoring range for domestic nonfi-

610 Federal Reserve Bulletin • September 1988

nancial debt for 1989 also has been lowered V2percentage point to a tentative 6V2 to IOV2 per-cent.

The specific ranges chosen for 1989 are, asusual, provisional, and the FOMC will reviewthem carefully next February, in light of inter-vening developments. Anticipating today howthe outlook for the economy in 1989 will appearnext February is difficult, and a major reassess-ment of that outlook would have implications forappropriate money growth ranges for that year.Unexpectedly strong or weak economic expan-sion or inflation pressures over the next sixmonths also could have implications for thebehavior of interest rates and their prospects for1989. The sensitivity of the monetary aggregatesto movements in market interest rates means thatthe appropriate growth next year in M2, M3, anddebt could seem different next February fromnow, necessitating a revision in the annualgrowth ranges. As the aggregates have becomemore responsive to interest rate changes in the1980s, judgments about possible ranges for thenext year necessarily have become even moretentative and subject to revision.

THE PERSISTENT U.S. EXTERNAL ANDFISCAL IMBALANCES

Despite the changes in the economic setting overthe last six months, other features of the macro-economic landscape remain much the same.Most notable are the continuing massive deficitsin our external payments and internal fiscal ac-counts. As a nation, we still are living wellbeyond our means; we consume much more ofthe world's goods and services each year than weproduce. Our current account deficit indicateshow much more deeply in debt to the rest of theworld we are sliding each year.

The consequence of this external imbalancewill be a steady expansion in our external debtburden in the years ahead. No household orbusiness can expect to have an inexhaustiblecredit line with borrowing terms that stay thesame as its debt mounts relative to its wealth andincome. Nor can we as a nation expect ourforeign indebtedness to grow indefinitely relativeto our servicing capacity without additional in-

ducements to foreigners to acquire dollar as-sets—either higher real interest returns, or acheaper real foreign exchange value for dollarassets, or both. To be sure, such changes inmarket incentives would have self-correcting ef-fects over time in reducing the imbalance be-tween our domestic spending and income.Higher real interest rates would curtail domesticinvestment and other spending. A lower realvalue of the dollar would make U.S. goods andservices relatively less expensive to both U.S.and foreign residents, damping our spending onimports out of U.S. income and boosting ourexports.

But simply sitting back and allowing such aself-correction to take place is not a workablepolicy alternative. Trying to follow such a coursecould have severe drawbacks now that our econ-omy is operating close to effective capacity andpotential inflationary pressures are on the hori-zon. The time is hardly propitious to discourageinvestment in needed plant and equipment, toadd further impulses for import price hikes ontop of the upward tendencies already in themaking, or to push our export industries as wellas import-competing industries to their capacitylimits.