Building the payment systems capabilities of the nigerian banking industry april 2007

21

Building the payment systems capabilities of the Nigerian Economy

-

Upload

rasheed-adegoke -

Category

Government & Nonprofit

-

view

342 -

download

0

Transcript of Building the payment systems capabilities of the nigerian banking industry april 2007

Building the payment systems capabilities of the Nigerian Economy

Presentation Outline Setting the stage…

Elements of a national payment system National payment systems: the change drivers Why reform the national payment systems?

A model for national payment reform A four-stage, 14-step guideline

Problems, Opportunities & Prospects Question & Answer

>>>

SETTING THE STAGE

Elements of a National Payment System Payment instruments used to initiate and direct thetransfer of funds between the accounts of payers and payeesat financial institutions; Network arrangements for transacting and clearingpayment instruments, processing and communicatingpayment information, and transferring the funds between thepaying and receiving institutions; Institutions that provide payment accounts, instrumentsand services to consumers and businesses and organisationsthat operate payment transaction, clearing and settlementservice networks for those financial institutions; Market conventions, regulations and contractualarrangements for producing, pricing, delivering andacquiring the various payment instruments and services; and Laws, standards, rules and procedures set bylegislators, courts, regulators and payment organisations thatdefine and govern the mechanics of the payment transferprocess and the conduct of payment service markets.

Elements of a National Payment System (graphical illustration)

A complex interaction of instruments, institutions, networks, rules, etc.

National Payment Systems:the change drivers… an increasing awareness of payment system

risks and concerns about financial stability; new developments and increasing user needs

in the financial and non-financial sectorsrequiring new cost-efficient paymentinstruments and services;

a policy decision to comply with internationalstandards for payment systems, sometimesrelated to a country’s entry into regional orglobal trade and financial arrangements; or

evolving central bank responsibilities andpayment needs.

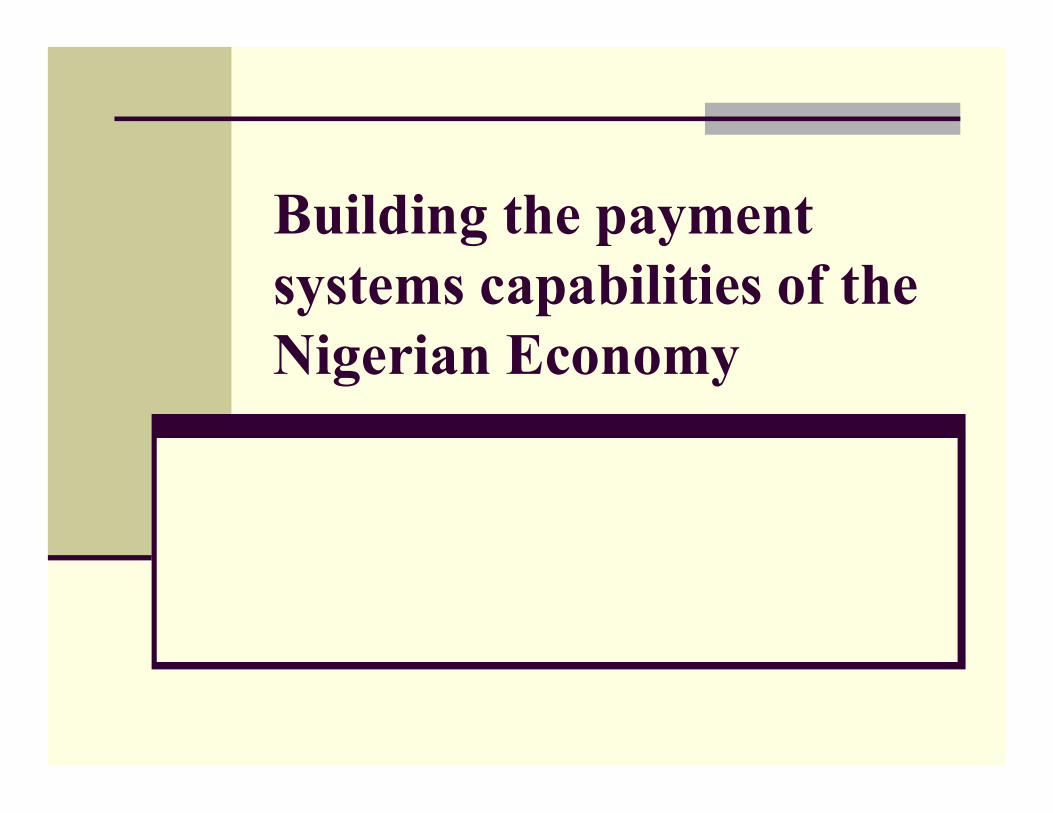

Why countries reform the National Payment Systems To broaden the range of payment instrumentsand services; To better contain legal, operational, financial andsystemic risks in payment infrastructures; To enhance the interoperability and resiliency ofbanking, payment and securities infrastructures; To improve cost efficiency, particularly in termsof operating costs and liquidity usage, andaccess to settlement credit for financialinstitutions; To create a more suitable oversight andregulatory regime for the national paymentsystem; and To establish more efficient and better organisedmarkets for delivering and pricing payment

A MODEL FOR NATIONAL PAYMENT REFORM

>>>

A model for National Payment Systems reformBANKINGSYSTEMREFORM

PAYMENTSYSTEMPLANNINGESTABLISHINSTITUTIONALFRAMEWORK

INFRASTRUCTUREBUILDPAYMENTINFRASTRUCTURE

Stage 1

Stage 2

Stage 3

Stage 4

Stage 1:Banking System ReformStep 1: Keep the Central Bank at the centre Central Bank possible roles include issuer ofmoney, primary creator of liquidity, interbanksettlement agent, provider of payment services,adviser on legislation, overseer, bankingsupervisor, catalyst and user.Step 2: Promote sound banking system There is need for banks; who are the principalproviders of the payment accounts, instrumentsand services; to act cooperatively in the overallinterest of the payment system.

Stage 2:Payment System PlanningStep 3: Recognise complexity The payment system should be seen broadly as a fullset of instruments, networks, rules, procedures &institutions that ensure circulation of money.Step 4: Focus on Needs Identify, and be guided by, the payment needs of all users in the system and by capabilities of the economy.Step 5: Set Clear priorities Plan & prioritize development efforts.Step 6: Implementation is key Develop a clear execution/implementation plan.

Stage 3:Establish institutional frameworkStep 7: Promote market developments Expand & strengthen market arrangements.Step 8: Involve relevant stakeholders Effective & extensive consultation is key.Step 9: Cooperate with other authorities Central Bank must liaise with other authorities including the NFIU, SEC, NDIC, etc.Step 10: Promote legal certainty Develop sound, transparent legal framework for the system.

Stage 4:Build payment infrastructureStep 11: For Retail-give more choice to people Extend choice & coverage of non-cash payments.Step 12: For Large value-build business case RTGS should be based on needs & growth in time-critical interbank payments.Step 13: Securities-plan with payment system Coordinate securities & large-value payment infrastructure.Step 14: Coordinate settlement process Coordinate settlement processes to properly manage related liquidity needs & settlement risks.

PROBLEMS, OPPORTUNITIES & PROSPECTS

>>>

Generic issues/problems in national payment system reforms Limited vision and leadership fordevelopment due to a narrow view as towhat constitutes a national paymentsystem; Limited knowledge of emerging paymentneeds and system capabilities; Weak support and commitment fromstakeholders due to inadequateconsultation; Limited development resources; and Legal, regulatory, public policy and marketbarriers to ongoing development of thenational payment system.

Specific challenges to reforming payment system in Nigeria Poor state of infrastructure especially electricityand telecomms (data services); Low banking penetration especially of ruralcommunities where majority of the populationlives; Low consumer confidence in non-cash paymentinstruments especially cheques & cards due tofrauds & history of failures; Low level of terminal deployment for acceptingnon-cash payments at merchant locations; and High investment value and long payback periodhas historically served as disincentive topotential innovators in the payment systemspace.

Opportunities for payment system reforms in Nigeria Let me start by acknowledging that a lot is

already happening here… There are opportunities to deepen card-based

payment through: Further consumer education/awareness; Increasing reliability & security to prevent frauds; Integrating MFBs into the system in rural areas; Deploying low-cost merchant terminals; Integration with mobile phone operators (mobile

payments) Other short-term opportunities include:

Increasing reliability of cheque-based payments; Reducing payment switching cost for low-value

transactions; and Enforcing blacklist of system abuse(e.g. dud cheques).

Prospects for change:Keeping end-user in focusEnd-user demands are largely: High availability & choice of instruments; Information: on benefits, costs, and risks; Low user costs; Interoperability among rival networks for

the same type of instruments e.g. cards; High information security; and Low legal risk.

Prospects for change:Notes for service providersFinancial institutions demand the

following from service providers: Equitable access to services; Low network participation fees; Fast and predictable delivery of

transaction, clearing & settlementservices;

Low settlement risk; and Settlement finality or non-repudiation

especially for large-value payments.

Closing remarks Nigeria must continue on the path ofreform in the banking & payment spacebeyond current Government; Existing reform agenda should bereviewed periodically for consistency withregional projects e.g. the WAEMU-RTGSproject; Service providers such as Interswitch, e-Transact, Visa/Valucard must cooperatemore in the interest of the system; and Stakeholder early involvement/buy-in andEnd-user education is key to success.

Question & Answer