BUILDING ASIA’S DIGITAL FUTURE - … Asia's... · CRM system, and around four ... The survey for...

20

A MINGTIANDI CHINA REAL ESTATE INTELLIGENCE REPORT 明天地 SPONSORED BY BUILDING ASIA’S DIGITAL FUTURE IS ASIAN REAL ESTATE READY FOR PROPTECH? MINGTIANDI ASIA REAL ESTATE TECHNOLOGY SURVEY RESULTS December 2017

Transcript of BUILDING ASIA’S DIGITAL FUTURE - … Asia's... · CRM system, and around four ... The survey for...

A MINGTIANDI CHINA REAL ESTATE INTELLIGENCE REPORT

明天地

SPONSORED BY

BUILDING ASIA’S DIGITAL FUTUREIS ASIAN REAL ESTATE READY FOR PROPTECH?

MINGTIANDI ASIA REAL ESTATE TECHNOLOGY SURVEY RESULTS December 2017

ABOUT BUILDING ASIA’S DIGITAL FUTUREThe Building Asia’s Digital Future report was researched and published with the objective of promoting understanding of the state of technology adoption in Asia’s real estate industry, as well as looking at where the sector is headed in the next five to ten years.

The findings are based on the Mingtiandi Asia Real Estate Technology Survey, which was conducted in September 2017. Mingtiandi is solely responsible for the report and its contents.

AUTHORMichael Cole

DESIGNShiny Leung

Additional copies may be obtained upon request.

ABOUT MINGTIANDI Mingtiandi is China’s independent source for China real estate intelligence. Our daily-updated coverage of China’s major property investors, publicly-listed real estate developers and market transactions now helps more than 1,000 visitors every day to make better informed decisions and gain an edge over the competition.

In addition to producing the industry-leading website, Mingtiandi.com, Mingtiandi’s corporate arm, RightSite Consulting, provides bespoke research and advice on real estate trends and transactions involving Chinese companies and mainland consumers for some of the world’s best known property investors and developers.

We concentrate on issues relating to China’s commercial property industry, and specialise in covering developments related to real estate finance, Chinese outbound investment, and logistics. Mingtiandi’s customer list includes The Carlyle Group, CBRE, Fosun, JLL, Morgan Stanley and The Redwood Group.

ABOUT YARDI SYSTEMS Yardi® develops and supports industry-leading investment and property management software for all types and sizes of real estate companies. Established in 1984, Yardi is based in Santa Barbara, California, and has Asia Pacific offices in Australia, Hong Kong, mainland China and Singapore, serving clients worldwide. For more information on how Yardi is Energized for Tomorrow, visit yardi.com.

CONTACTMingtiandiwww.mingtiandi.com+852-8191-1896inquiries@mingtiandi.com Copyright © Mingtiandi.com 2017

TABLE OF CONTENTS

EXECUTIVE SUMMARY

01. ASSESSING THE STATE OF TECH IN ASIAN REAL ESTATE

02. SERVING ENTERPRISE NEEDS WITH BASIC TOOLS

03. UNDERSTANDING WHO RESPONDED TO THE SURVEY

04. SETTING TECH GOALS AND PRIORITIES

05. CONCLUSIONS AND RECOMMENDATIONS

Building Asia’s Digital FuturePg. 3

EXECUTIVE SUMMARYThe application of online solutions to enhance real estate development and investment has become one of the hottest areas of technology investment in the US and Europe, as entrepreneurs and investors look for ways to harness “proptech” to build a more efficient property industry. In Asia, however, development of real estate and investment of the sector remains firmly-rooted in the PC age. The most common tech tools in use are primarily personal productivity programs such as Excel, which are then shared among groups. The industry on the whole has been slow to make the jump to database-enabled online solutions to marketing, analysis and property management challenges, which offer the opportunity to more efficiently manage large scale businesses, offer greater security and provide superior reporting functions.

THE MAINLAND HAS AN EDGE OVER HONG KONG AND SINGAPORE AS REAL ESTATE MOVES ONLINE To find out where Asia’s property industry stands along the productivity evolution from ledgers to big data, Mingtiandi conducted its first survey of technology adoption within the Asian real estate industry in September 2017.

This survey of real estate professionals looked into challenges and opportunities for adoption of technology systems in Asia via an online poll, which took in 169 responses representing primarily Asia-based real estate developers, investors and other industry professionals.

MAINLAND REAL ESTATE GAINS A TECH ADVANTAGEThe responses indicate that while mainland China’s real estate developers and investors overwhelmingly see their industry as lagging the West in tech adoption, these industry players may already have gained an edge over their counterparts from Hong Kong and Singapore.

The mainland-based respondents to the survey led their counterparts from the south in adoption of each basic type of tech system measured, including software for property management, sales management and ERP systems. While the mainland-based respondents were not necessarily employed by Chinese-owned firms, individuals employed by real estate investment or development firms based in China who participated in the survey were nearly three times as likely as their Hong Kong-based counterparts to be using a CRM system, and around four times more likely than their

Building Asia’s Digital FuturePg. 4

counterparts in Singapore to be using the popular sales management tools.

ASIA TRAILS THE WEST AND REAL ESTATE LAGS OTHER INDUSTRIESRespondents saw their industry as lagging other sectors, and their region as trailing other parts of the world, with regard to adoption of technical systems that could be used to improve efficiency in their businesses.

Although more than 80 percent of respondents saw themselves as working in an industry where access to information was critical to success, more than 40 percent of those queried indicated that spreadsheets remained a primary tool for information management.

MARKET PRESSURE LEADS TO INNOVATION Within the range of respondents, those managing retail assets, who are among the groups most under pressure in the current market, were both more likely to identify the industry and the region as trailing global standards, and this group was more likely to rely on more advanced tools to manage their information.

The survey findings suggest that should managers of other asset types meet competitive pressures similar to what is happening in retail, that adoption of information technology could accelerate within the coming years.

Building Asia’s Digital FuturePg. 5

The survey for Building Asia’s Digital Future, which was conducted during September 2017, reached some of the region’s biggest real estate investment firms, developers and service providers and sought to find out how they currently employ technology in their businesses, what their goals are for the future and how they see adoption of technology within their industry and within the region, compared to global standards.

The results show that while many companies have already adopted basic systems for managing their information, and are now committing significant expenditure to technology, the majority still see the Asian region in general, and the real estate industry specifically, as lagging world trends.

The gap between world standards and local adoption provides opportunities for tech innovators, while also presenting challenges to companies facing internal resistance to innovation.

COMPARING ADOPTION OF REAL ESTATE TECH Overall, more than 55 percent of respondents indicated that they see Asia as trailing the Western world in the adoption of technology within the real estate industry. Less than 12 percent saw the region as leading the way.

RESPONDENTS IN CHINA WERE MORE LIKELY TO SEE THEIR MARKET AS TRAILING THE WEST

Among real estate investors and developers, this perception of a technology gap was most acute in mainland China. Among respondents in the Middle Kingdom, over 77 percent identified Asia as trailing the West in adoption of real estate technology compared to approximately 57 percent in Hong Kong and 55 percent in Singapore.

Among all respondents, the perception of how Asia stacks up against the West also varied according to real estate sector. For respondents who indicated that their companies own or manage retail real estate assets, the outlook on technology adoption in Asia is much more negative, with over 63 percent seeing Asia as trailing the West.

CHAPTER 1ASSESSING THE STATE OF TECH IN ASIAN REAL ESTATE

Building Asia’s Digital FuturePg. 6

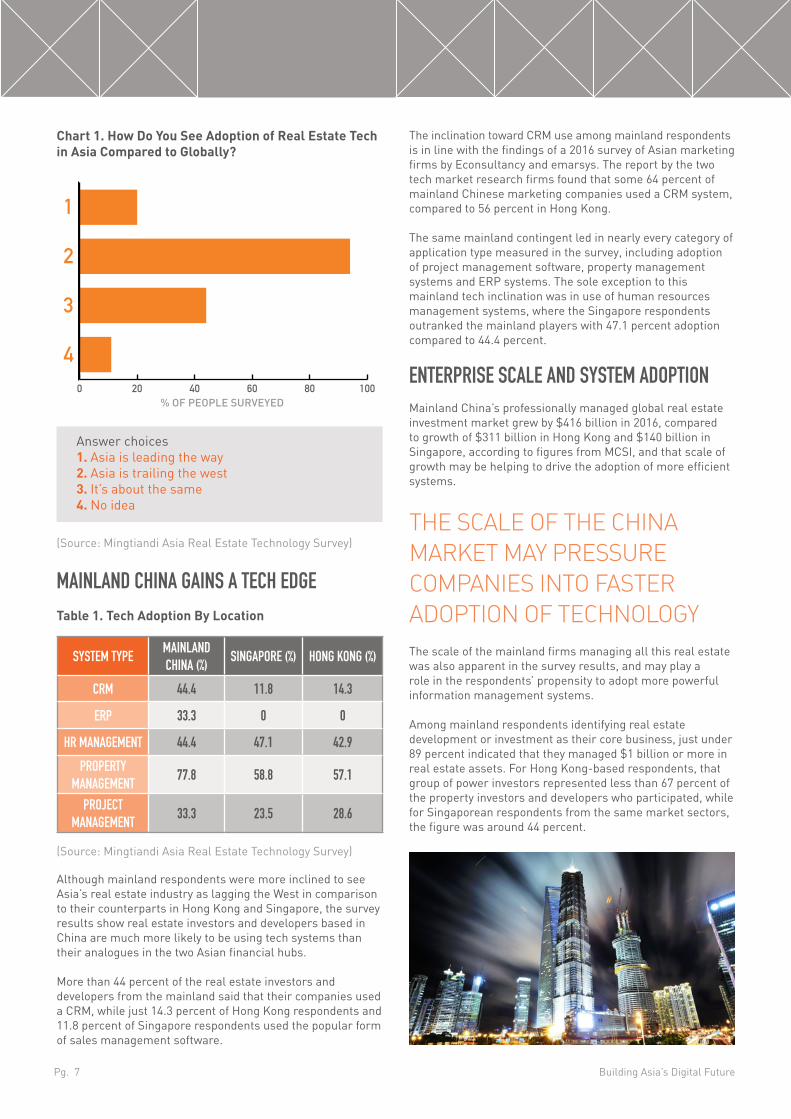

Chart 1. How Do You See Adoption of Real Estate Tech in Asia Compared to Globally?

0 20 40 60 80 100% OF PEOPLE SURVEYED

1

2

3

4

Answer choices1. Asia is leading the way2. Asia is trailing the west3. It’s about the same4. No idea

(Source: Mingtiandi Asia Real Estate Technology Survey) MAINLAND CHINA GAINS A TECH EDGETable 1. Tech Adoption By Location Table 1. Tech Adoption by Location Comparing Hong Kong, Singapore and ChinaSYSTEM TYPE

MAINLAND CHINA (%)

SINGAPORE (%) HONG KONG (%)

CRM 44.4 11.8 14.3

ERP 33.3 0 0

HR MANAGEMENT 44.4 47.1 42.9

PROPERTY MANAGEMENT

77.8 58.8 57.1

PROJECT MANAGEMENT

33.3 23.5 28.6

(Source: Mingtiandi Asia Real Estate Technology Survey) Although mainland respondents were more inclined to see Asia’s real estate industry as lagging the West in comparison to their counterparts in Hong Kong and Singapore, the survey results show real estate investors and developers based in China are much more likely to be using tech systems than their analogues in the two Asian financial hubs.

More than 44 percent of the real estate investors and developers from the mainland said that their companies used a CRM, while just 14.3 percent of Hong Kong respondents and 11.8 percent of Singapore respondents used the popular form of sales management software.

The inclination toward CRM use among mainland respondents is in line with the findings of a 2016 survey of Asian marketing firms by Econsultancy and emarsys. The report by the two tech market research firms found that some 64 percent of mainland Chinese marketing companies used a CRM system, compared to 56 percent in Hong Kong.

The same mainland contingent led in nearly every category of application type measured in the survey, including adoption of project management software, property management systems and ERP systems. The sole exception to this mainland tech inclination was in use of human resources management systems, where the Singapore respondents outranked the mainland players with 47.1 percent adoption compared to 44.4 percent.

ENTERPRISE SCALE AND SYSTEM ADOPTIONMainland China’s professionally managed global real estate investment market grew by $416 billion in 2016, compared to growth of $311 billion in Hong Kong and $140 billion in Singapore, according to figures from MCSI, and that scale of growth may be helping to drive the adoption of more efficient systems.

THE SCALE OF THE CHINA MARKET MAY PRESSURE COMPANIES INTO FASTER ADOPTION OF TECHNOLOGY The scale of the mainland firms managing all this real estate was also apparent in the survey results, and may play a role in the respondents’ propensity to adopt more powerful information management systems.

Among mainland respondents identifying real estate development or investment as their core business, just under 89 percent indicated that they managed $1 billion or more in real estate assets. For Hong Kong-based respondents, that group of power investors represented less than 67 percent of the property investors and developers who participated, while for Singaporean respondents from the same market sectors, the figure was around 44 percent.

Building Asia’s Digital FuturePg. 7

HOW REAL ESTATE COMPARES TO OTHER INDUSTRIES IN ADOPTING NEW TECHNOLOGYNearly 77 percent of respondents saw real estate as trailing other industries in tech adoption, while less than six percent saw property companies as taking a leading role.

However, in terms of what systems respondents are already using, more than 53 percent are already using a CRM system, 41 percent had a property management system and 41 percent of readers had an HR management system. More than 15 percent of the respondents said that they had already adopted an ERP system.

Chart 2. How Do You See Adoption of Tech in Real Estate Compared to Other Industries?

0 20 40 60 80 100% OF PEOPLE SURVEYED

1

2

3

4

Answer choices1. Real estate is leading the way2. Real estate trails other industries3. It’s about the same4. No idea

(Source: Mingtiandi Asia Real Estate Technology Survey)

The general perception of a technology adoption deficit in Asia appears to be verified by a report published this year by market research firm Gartner, which found that, worldwide across industry sectors, 91 percent of companies with more than 11 employees use a CRM system.

In their view of tech adoption in real estate compared to other sectors, retail asset owners and managers again took a dimmer view of how the property industry is keeping up, with over 81 percent seeing real estate as lagging other industries in adapting to technological innovation.

76 percent of respondents who said that their companies invest in or develop warehouses – which are increasingly oc-cupied by ecommerce operators – saw the real state industry as trailing other sectors.

ASIA’S COMING PROPTECH REVOLUTION

While the property companies and individuals surveyed by Mingtiandi revealed a level of technology adoption that trails other industries, a current boom in the development and commercialisation of technical applications for the real estate industry – proptech – could soon put pressure on these players to adapt to a changing reality.

Led by a surge of funding for mainland startups, proptech companies in Asia Pacific have raised $4.8 billion in funding since 2013, according to a study released in November 2017 by JLL, accounting for more than 60 percent of investment in the sector globally over the period.

Armed with all that cash, these startups are targeting ways to make real estate companies more efficient, but many are also aiming at disrupting the current business models that currently rule many segments of the property industry.

PROPTECH EVOLVES FROM LISTINGS TO BLOCKCHAIN

Screens from Fang.com mobile app

Building Asia’s Digital FuturePg. 8

With $7.8 billion having been invested in proptech companies since 2013, according to JLL, the sector is rapidly developing more powerful tools to assist occupiers, investors and other industry players.

ASIA’S PROPERTY TECHNOLOGY SECTOR HAS MOVED BEYOND BASIC ONLINE LISTINGSWhile the first generation of property technology firms were involved in information sharing, such as setting up listings portals where tenants and homebuyers could browse available properties online, the latest set of tech-enabled property firms have moved beyond sharing listings of houses and apartments.

In a recent survey of 53 prominent property technology businesses in the US by market research firm CB Insights, over 28 percent were providing property listing or search services, while another 20 percent were market data or analytics providers and over 13 percent were in the investment or crowdfunding space.

Mapping startup Vektor took top honors at southeast Asia’s first proptech hackathon in August. (Image: www.99.co)

Tech-enabled shared office providers such as WeWork form another segment of the proptech sector, and allow occupiers to select and lease space online, while also providing community functions that enable tenants to streamline many back office operations.

Proptech is also rapidly adopting financial technology innovations such as blockchain, and online payment

platforms, to allow retail investors to directly fund real estate projects over the Internet. During 2016 a range of startups, including PeerStreet and Real Crowd, handled some $3.5 billion in real estate transactions globally, according to industry figures, signifying a potential threat to the existing asset management industry.

CHINA LEADS ASIA’S PROPTECH WAVEWith real estate and related sectors estimated to account for between 15 to 20 percent of mainland China’s GDP, and the country’s tech sector experiencing rapid growth, real estate technology has become a top target for Chinese entrepreneurs and investors.

Chart 3. Venture Funding since 2013

VENTURE FUNDING SINCE 2013 (US$M)

China*

India

SE Asia

NE Asia**

ANZ

0 500 1000 1500 2000 2500 3000 3500

(Source: JLL/Tech in Asia)

Of the $4.8 billion raised by Asian proptech startups since 2013, more than $3 billion has gone to China-based companies – accounting for just under 39 percent of capital targetting the market niche globally, according to JLL’s recent report, “Clicks and Mortar: The Growing Influence of Proptech.”

Among these robustly-funded startups, online home listing platform Fangdd.com closed a $223 million series C round of funding in July 2017, and Shanghai-based co-working provider naked Hub is thought to be on the brink of a new round of institutional funding after raising around $33 million from investors including Gaw Capital in 2016.

The scale of the China market, which has led to greater system adoption among companies in the country’s real estate sector, also provides the incentives for investing in startups in the sector, which will both provide tools for, and put pressure on, property companies in the region.

*including Hong Kong **excluding Mainland China & Hong Kong

Building Asia’s Digital FuturePg. 9

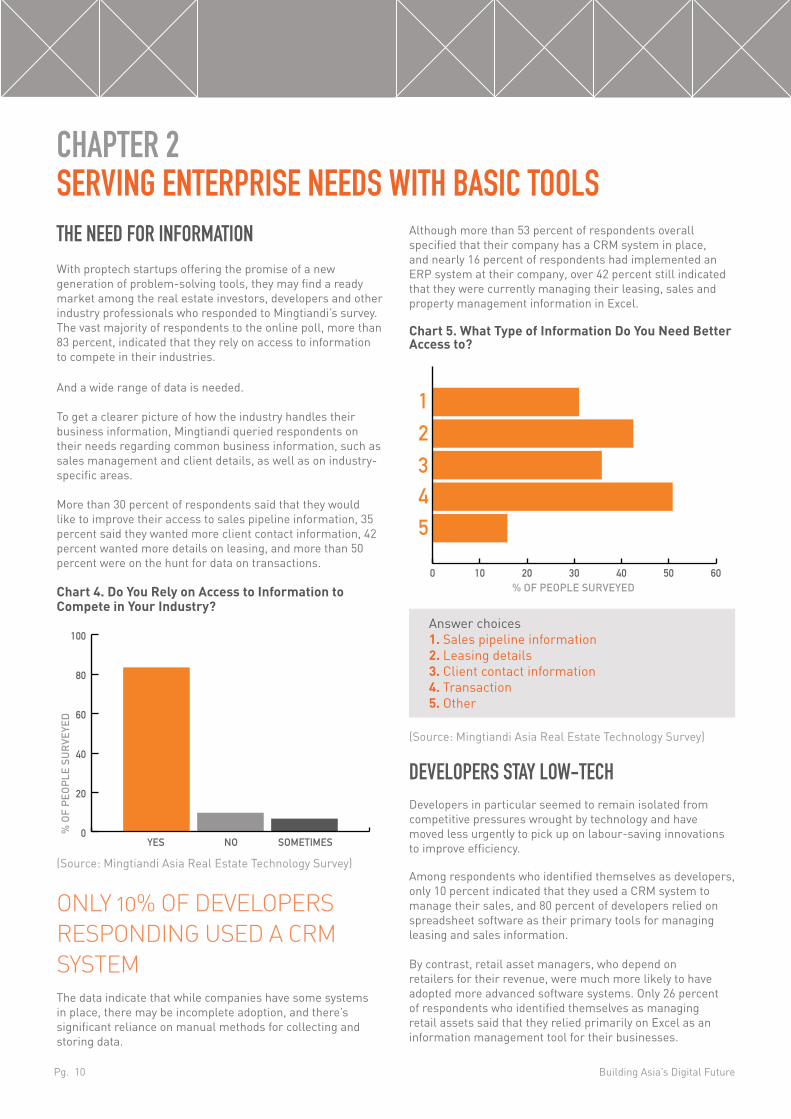

THE NEED FOR INFORMATION With proptech startups offering the promise of a new generation of problem-solving tools, they may find a ready market among the real estate investors, developers and other industry professionals who responded to Mingtiandi’s survey. The vast majority of respondents to the online poll, more than 83 percent, indicated that they rely on access to information to compete in their industries. And a wide range of data is needed.

To get a clearer picture of how the industry handles their business information, Mingtiandi queried respondents on their needs regarding common business information, such as sales management and client details, as well as on industry-specific areas.

More than 30 percent of respondents said that they would like to improve their access to sales pipeline information, 35 percent said they wanted more client contact information, 42 percent wanted more details on leasing, and more than 50 percent were on the hunt for data on transactions.

Chart 4. Do You Rely on Access to Information to Compete in Your Industry?

YES NO SOMETIMES

% O

F P

EOP

LE S

UR

VEYE

D

0

20

40

60

80

100

(Source: Mingtiandi Asia Real Estate Technology Survey)

ONLY 10% OF DEVELOPERS RESPONDING USED A CRM SYSTEMThe data indicate that while companies have some systems in place, there may be incomplete adoption, and there’s significant reliance on manual methods for collecting and storing data.

CHAPTER 2SERVING ENTERPRISE NEEDS WITH BASIC TOOLS

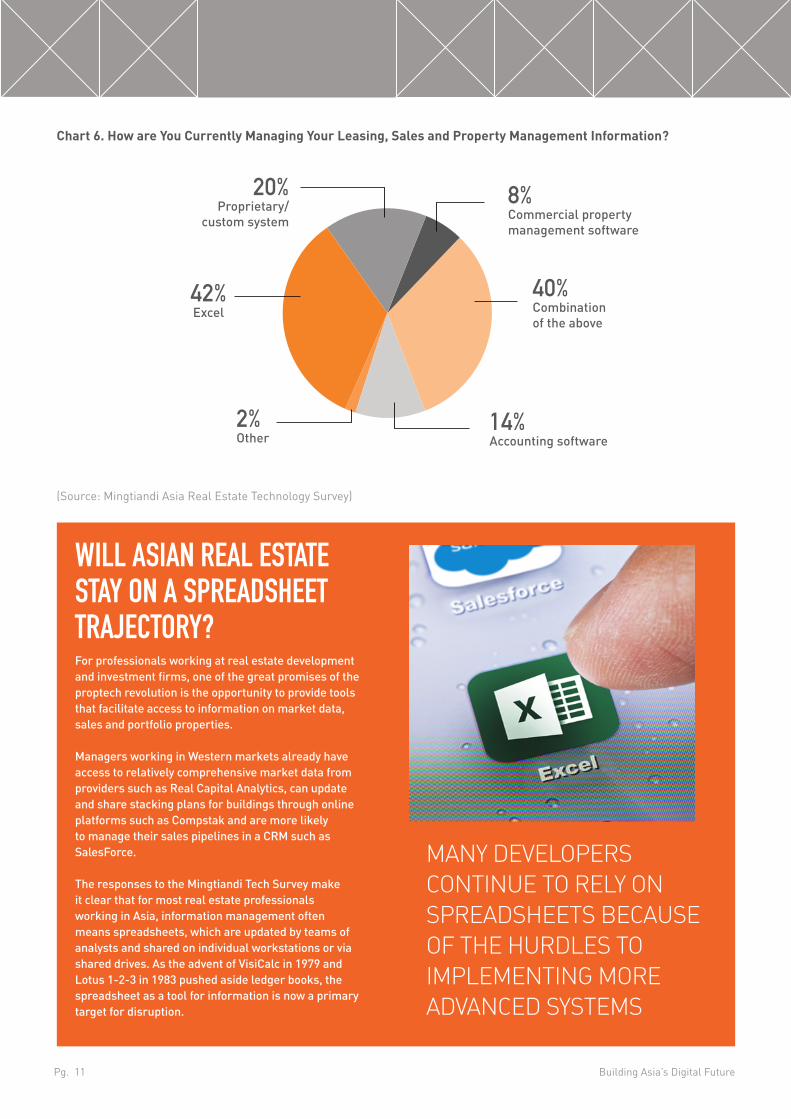

Although more than 53 percent of respondents overall specified that their company has a CRM system in place, and nearly 16 percent of respondents had implemented an ERP system at their company, over 42 percent still indicated that they were currently managing their leasing, sales and property management information in Excel. Chart 5. What Type of Information Do You Need Better Access to?

% OF PEOPLE SURVEYED0 10 20 30 40 50 60

12345

Answer choices1. Sales pipeline information2. Leasing details3. Client contact information4. Transaction5. Other

(Source: Mingtiandi Asia Real Estate Technology Survey)

DEVELOPERS STAY LOW-TECHDevelopers in particular seemed to remain isolated from competitive pressures wrought by technology and have moved less urgently to pick up on labour-saving innovations to improve efficiency.

Among respondents who identified themselves as developers, only 10 percent indicated that they used a CRM system to manage their sales, and 80 percent of developers relied on spreadsheet software as their primary tools for managing leasing and sales information.

By contrast, retail asset managers, who depend on retailers for their revenue, were much more likely to have adopted more advanced software systems. Only 26 percent of respondents who identified themselves as managing retail assets said that they relied primarily on Excel as an information management tool for their businesses.

Building Asia’s Digital FuturePg. 10

40%Combination of the above

20%Proprietary/

custom system

8%Commercial property management software

42%Excel

14% Accounting software

2% Other

Chart 6. How are You Currently Managing Your Leasing, Sales and Property Management Information?

WILL ASIAN REAL ESTATE STAY ON A SPREADSHEET TRAJECTORY?For professionals working at real estate development and investment firms, one of the great promises of the proptech revolution is the opportunity to provide tools that facilitate access to information on market data, sales and portfolio properties. Managers working in Western markets already have access to relatively comprehensive market data from providers such as Real Capital Analytics, can update and share stacking plans for buildings through online platforms such as Compstak and are more likely to manage their sales pipelines in a CRM such as SalesForce.

The responses to the Mingtiandi Tech Survey make it clear that for most real estate professionals working in Asia, information management often means spreadsheets, which are updated by teams of analysts and shared on individual workstations or via shared drives. As the advent of VisiCalc in 1979 and Lotus 1-2-3 in 1983 pushed aside ledger books, the spreadsheet as a tool for information is now a primary target for disruption.

MANY DEVELOPERS CONTINUE TO RELY ON SPREADSHEETS BECAUSE OF THE HURDLES TO IMPLEMENTING MORE ADVANCED SYSTEMS

(Source: Mingtiandi Asia Real Estate Technology Survey)

Building Asia’s Digital FuturePg. 11

EXCEL STILL RULES IN ASIA 42 percent of the overall survey respondents and 80 percent of developers responding indicated that they were currently managing their leasing, sales and property management information in Excel.

Spreadsheet programs such as Excel have the advantage that information data sets are easy to set up and revise, and most people already have the software installed on their desktop. However, the problems around using spreadsheets rather than database-driven programs, either in the cloud or in local installations, increase as organisations grow.

While Excel-based systems can be quickly set up by an experienced analyst and don’t require new subscriptions or complicated development procedures, they become increasingly prone to problems with data entry errors and version control as companies and their datasets grow. Larger scale operations will also find that spreadsheet-based systems often mean devoting additional resources to maintaining multiple, often redundant data sets.

MISSION COMPLEXITY RAISES CHANCE OF DATA DISASTER Although studies of the cost of maintaining – or failing to maintain – properly structured datasets in the real estate industry are few, the field of rocket science provides a $125 million example of the cost of improperly structured data. In 1999 NASA’s Mars Climate Orbiter disintegrated while unexpectedly entering the Martian atmosphere, after two engineering teams had created data systems based on differing units. According to a review of the mission, a team based in Colorado, which prepared data for putting the spacecraft into orbit, had used pounds in preparing their information. The California-based team that implemented that information entered it directly in non-converted metric units, resulting in the eventual loss of the $125 million spacecraft.

Real estate developers and investors are not yet sending rockets to Mars, however, as their businesses grow beyond single markets, they often face many challenges regarding datasets that need to work in differing currencies, area measurements and other metrics depending on locations. And many of their missions require investments larger than $125 million.

Problems with sharing data made NASA’s Mars Climate Orbiter into a $125M mistake

Building Asia’s Digital FuturePg. 12

CREATING QUICKEN FOR REAL ESTATENo one sets out to crash a spacecraft, or to incur a one-month delay before obtaining an occupancy permit, however, the survey respondents provided insight into the obstacles preventing real estate professionals from migrating away from spreadsheet-based systems. Just under 48 percent of respondents indicated that changing existing behaviour was the biggest barrier to overcome, and another 30 percent cited the need for development and customisation resources as holding back adoption of new systems.

Software already exists to tackle most of the challenges facing real estate developers, investors and other industry professionals, however, the pain involved in system implementation may still be an obstacle, although one which is rapidly being reduced as software providers build up development resources and roll out more sophisticated versions.

Just as personal financial management softwares gained in popularity as user interfaces improved and reliability increased, the concentration of resources in developing software solutions for real estate problems is rapidly bringing down barriers to adoption.

In the case of China (including Hong Kong), according to a recent report by JLL and Tech in Asia, some $46 million has been invested in developing technological solutions for property management problems since 2013, and another $23 million has been put into growing project development solutions.

With all of this cash aimed at providing alternatives to $125 million disasters, the trajectory of tech adoption in Asia’s real estate industry may be rapidly set to a new course.

Smart buildings may require smarter management systems

Building Asia’s Digital FuturePg. 13

CHAPTER 3UNDERSTANDING WHO RESPONDED TO THE SURVEY

The findings of the survey, regarding the low rate of adoption of technology-enabled information management systems, may be more surprising considering the scale and the nature of the businesses being operated.

38 percent of respondents indicated that they worked at companies that invested in real estate as their core business, and approximately the same number of respondents said that their companies manage more than $1 billion in real estate assets.

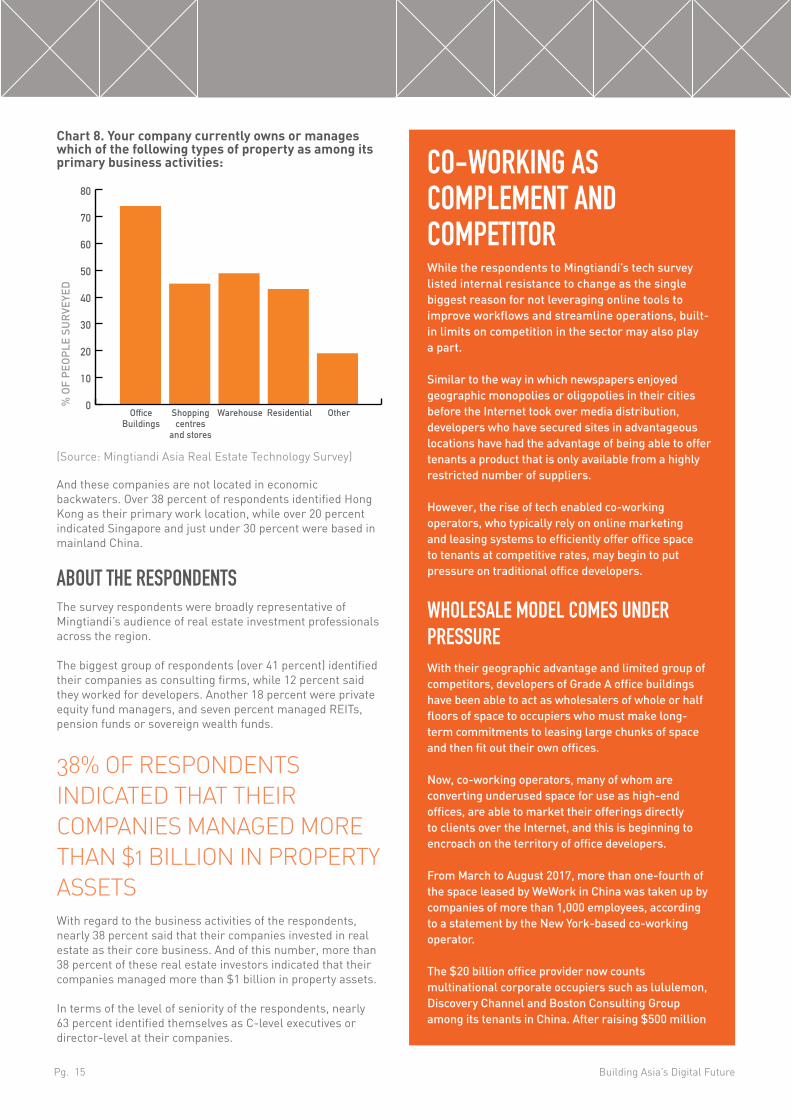

In terms of types of assets being managed, over 74 percent indicated that they managed office buildings, over 48 percent managed warehouses and just under 45 percent managed retail properties.

MORE THAN 38% OF RESPONDENTS WERE BASED IN HONG KONG, 30% WERE IN CHINA AND 20% IN SINGAPORE

Chart 7. Do You Rely on Access to Information to Compete in Your Industry?

0 5 10 15 20 25 30 35 40

% OF PEOPLE SURVEYED

(USD)

DOESN’T APPLY

$1BN+

$500M - $1BN

$250M - $500M

$50M - $250M

$5M - $50M

UNDER $5M

(Source: Mingtiandi Asia Real Estate Technology Survey)

Building Asia’s Digital FuturePg. 14

Chart 8. Your company currently owns or manages which of the following types of property as among its primary business activities:

0

10

20

30

40

50

60

70

80

OfficeBuildings

Shoppingcentres

and stores

Warehouse Residential Other

% O

F P

EOP

LE S

UR

VEYE

D

(Source: Mingtiandi Asia Real Estate Technology Survey)

And these companies are not located in economic backwaters. Over 38 percent of respondents identified Hong Kong as their primary work location, while over 20 percent indicated Singapore and just under 30 percent were based in mainland China.

ABOUT THE RESPONDENTS The survey respondents were broadly representative of Mingtiandi’s audience of real estate investment professionals across the region.

The biggest group of respondents (over 41 percent) identified their companies as consulting firms, while 12 percent said they worked for developers. Another 18 percent were private equity fund managers, and seven percent managed REITs, pension funds or sovereign wealth funds.

38% OF RESPONDENTS INDICATED THAT THEIR COMPANIES MANAGED MORE THAN $1 BILLION IN PROPERTY ASSETSWith regard to the business activities of the respondents, nearly 38 percent said that their companies invested in real estate as their core business. And of this number, more than 38 percent of these real estate investors indicated that their companies managed more than $1 billion in property assets.

In terms of the level of seniority of the respondents, nearly 63 percent identified themselves as C-level executives or director-level at their companies.

CO-WORKING AS COMPLEMENT AND COMPETITOR While the respondents to Mingtiandi’s tech survey listed internal resistance to change as the single biggest reason for not leveraging online tools to improve workflows and streamline operations, built-in limits on competition in the sector may also play a part.

Similar to the way in which newspapers enjoyed geographic monopolies or oligopolies in their cities before the Internet took over media distribution, developers who have secured sites in advantageous locations have had the advantage of being able to offer tenants a product that is only available from a highly restricted number of suppliers.

However, the rise of tech enabled co-working operators, who typically rely on online marketing and leasing systems to efficiently offer office space to tenants at competitive rates, may begin to put pressure on traditional office developers.

WHOLESALE MODEL COMES UNDER PRESSURE With their geographic advantage and limited group of competitors, developers of Grade A office buildings have been able to act as wholesalers of whole or half floors of space to occupiers who must make long-term commitments to leasing large chunks of space and then fit out their own offices.

Now, co-working operators, many of whom are converting underused space for use as high-end offices, are able to market their offerings directly to clients over the Internet, and this is beginning to encroach on the territory of office developers.

From March to August 2017, more than one-fourth of the space leased by WeWork in China was taken up by companies of more than 1,000 employees, according to a statement by the New York-based co-working operator.

The $20 billion office provider now counts multinational corporate occupiers such as lululemon, Discovery Channel and Boston Consulting Group among its tenants in China. After raising $500 million

Building Asia’s Digital FuturePg. 15

from Japan’s Softbank and Beijing-based Hony Capital to expand its China operation, WeWork has also been able to win over mainland tech firms Zhaopin.com and bike-sharing startup ofo.

WeWork’s domestic rival, naked Hub, has reported similar results, with the Shanghai-based company counting major multinationals such as AB InBev and Viking Cruises among its tenants, as well as bike-sharing early mover Mobike, and Hong Kong’s Hang Seng Bank.

CO-WORKING OPERATORS START TO LOOK LIKE LANDLORDSAlthough co-working operators primarily operate as service providers for now, there are signs that WeWork, naked Hub and other flexible office firms may move up the real estate value chain.

In October, the New York Times reported that WeWork is buying the Lord and Taylor department store in Manhattan for $850 million, with plans to move its corporate headquarters into the 63,000 square metre New York landmark, with the company leasing the remainder of the space to tenants. During the same month, Bloomberg reported that WeWork is buying an office building in London from Blackstone for GBP 600 million ($785 million).

In Shanghai, naked Hub has taken over a 12,000 square metre building in the city’s Gubei area and converted it into a tech friendly office centre. The two-year old company says that the western Shanghai

project, which is Asia’s largest co-working centre, is now more than 80 percent leased after first opening for occupation in July.

DEVELOPERS CHECK INTO CO-WORKING In a way similar to how traditional publishers bought into fast-growing websites in the first wave of online disruption of offline commerce, as co-working operators start to move into developer territory some traditional builders have been finding ways to pursue this online-to-offline real estate opportunity.

On the mainland, office developer SOHO China has started its own co-working brand, SOHO 3Q, which now has some 19 centres nationwide.

Publicly-listed Singapore developer City Developments Limited (CDL) has gotten involved with the co-working movement by investing in Shanghai-based flexible office operator Distrii. CDL has now led two fund-raising rounds totalling over $30 million for the co-working startup led by former executives of Shanghai’s Greenland Group. Southeast Asia’s largest developer, CapitaLand, is also catching on to co-working after having invested in Singapore startup The Great Room.

With co-working operators becoming involved in real estate investment and development, and traditional developers co-opting innovations from flexible office providers, the shared office sector could rapidly become a major source of change in the region’s property industry, and one which Mingtiandi will track on a quarterly basis beginning in 2018.

Co-working provider naked Hub now counts AB InBev, Viking Cruises and Hang Seng Bank among its tenants.

Building Asia’s Digital FuturePg. 16

Although survey respondents still are in the early stages with regard to adopting technology systems, many participants indicated that they expect to improve their capabilities in the near future.

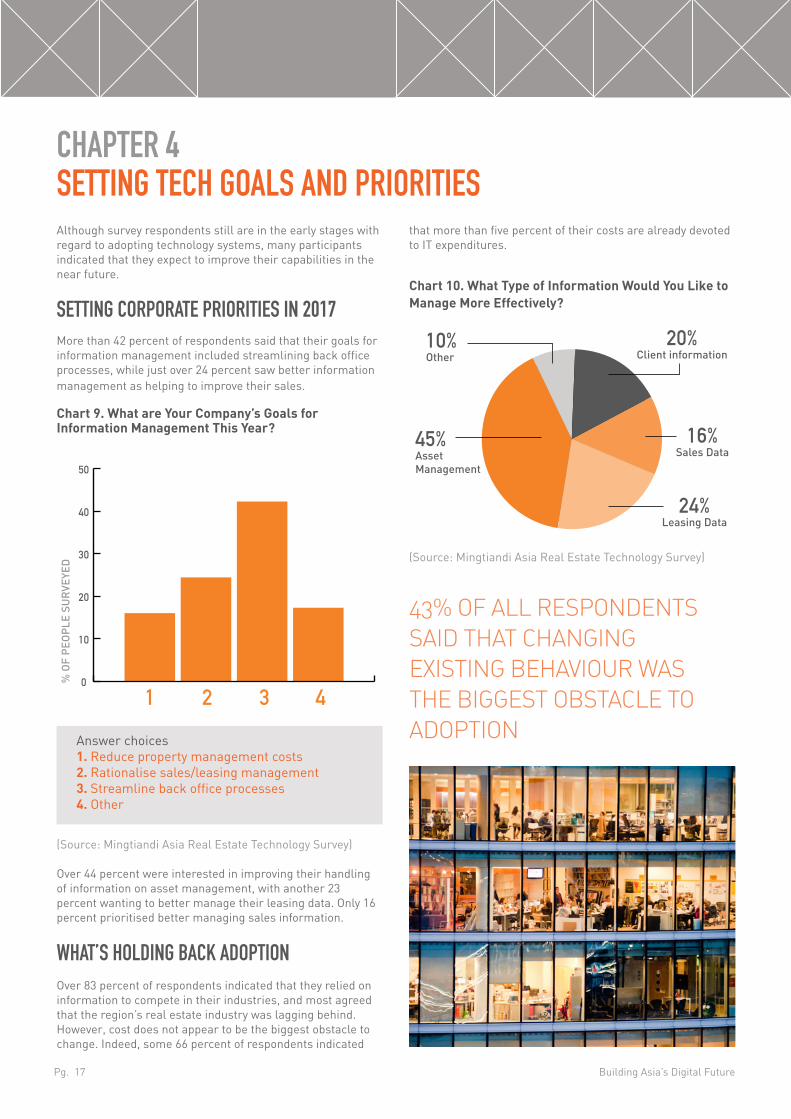

SETTING CORPORATE PRIORITIES IN 2017 More than 42 percent of respondents said that their goals for information management included streamlining back office processes, while just over 24 percent saw better information management as helping to improve their sales.

Chart 9. What are Your Company’s Goals for Information Management This Year?

% O

F P

EOP

LE S

UR

VEYE

D

0

10

20

30

40

50

1 2 3 4

(Source: Mingtiandi Asia Real Estate Technology Survey)

Over 44 percent were interested in improving their handling of information on asset management, with another 23 percent wanting to better manage their leasing data. Only 16 percent prioritised better managing sales information.

WHAT’S HOLDING BACK ADOPTIONOver 83 percent of respondents indicated that they relied on information to compete in their industries, and most agreed that the region’s real estate industry was lagging behind. However, cost does not appear to be the biggest obstacle to change. Indeed, some 66 percent of respondents indicated

CHAPTER 4SETTING TECH GOALS AND PRIORITIES

Answer choices1. Reduce property management costs2. Rationalise sales/leasing management3. Streamline back office processes4. Other

that more than five percent of their costs are already devoted to IT expenditures.

Chart 10. What Type of Information Would You Like to Manage More Effectively?

45%Asset Management

10%Other

24%Leasing Data

16%Sales Data

20%Client information

(Source: Mingtiandi Asia Real Estate Technology Survey)

43% OF ALL RESPONDENTS SAID THAT CHANGING EXISTING BEHAVIOUR WAS THE BIGGEST OBSTACLE TO ADOPTION

Building Asia’s Digital FuturePg. 17

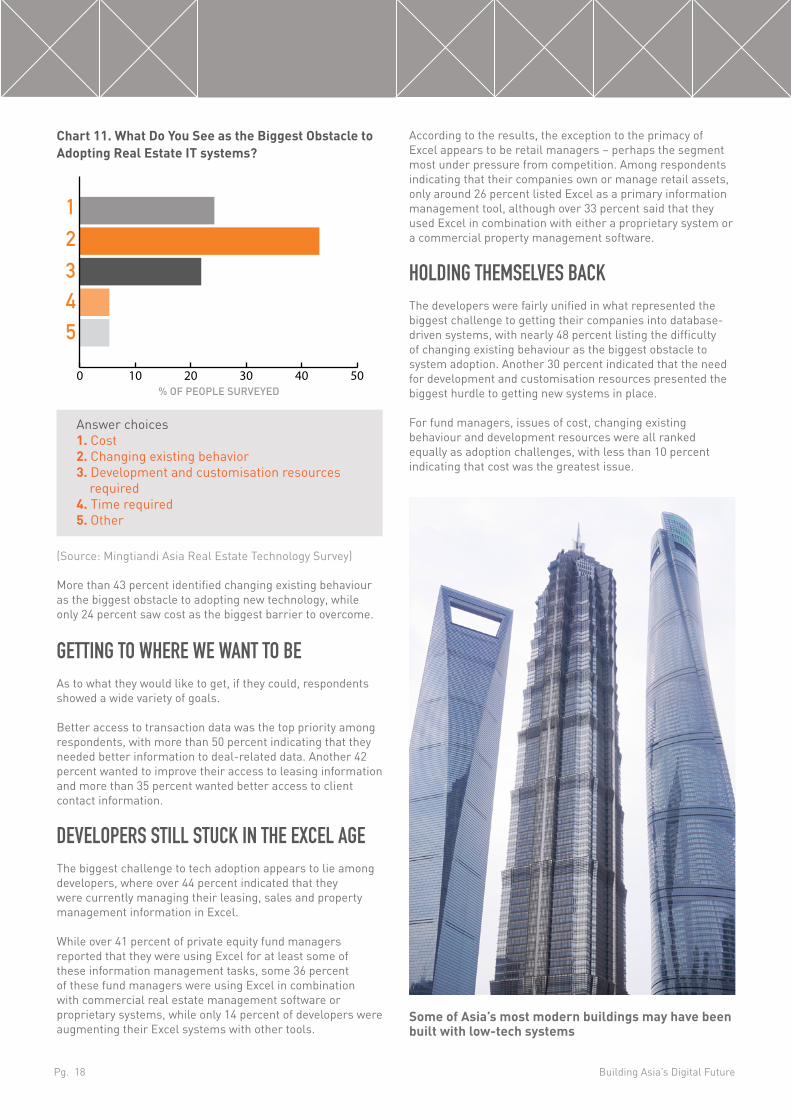

Chart 11. What Do You See as the Biggest Obstacle to Adopting Real Estate IT systems?

% OF PEOPLE SURVEYED

12345

0 10 20 30 40 50

Answer choices1. Cost2. Changing existing behavior3. Development and customisation resources required4. Time required5. Other

(Source: Mingtiandi Asia Real Estate Technology Survey) More than 43 percent identified changing existing behaviour as the biggest obstacle to adopting new technology, while only 24 percent saw cost as the biggest barrier to overcome.

GETTING TO WHERE WE WANT TO BEAs to what they would like to get, if they could, respondents showed a wide variety of goals.

Better access to transaction data was the top priority among respondents, with more than 50 percent indicating that they needed better information to deal-related data. Another 42 percent wanted to improve their access to leasing information and more than 35 percent wanted better access to client contact information.

DEVELOPERS STILL STUCK IN THE EXCEL AGEThe biggest challenge to tech adoption appears to lie among developers, where over 44 percent indicated that they were currently managing their leasing, sales and property management information in Excel.

While over 41 percent of private equity fund managers reported that they were using Excel for at least some of these information management tasks, some 36 percent of these fund managers were using Excel in combination with commercial real estate management software or proprietary systems, while only 14 percent of developers were augmenting their Excel systems with other tools.

According to the results, the exception to the primacy of Excel appears to be retail managers – perhaps the segment most under pressure from competition. Among respondents indicating that their companies own or manage retail assets, only around 26 percent listed Excel as a primary information management tool, although over 33 percent said that they used Excel in combination with either a proprietary system or a commercial property management software.

HOLDING THEMSELVES BACK The developers were fairly unified in what represented the biggest challenge to getting their companies into database-driven systems, with nearly 48 percent listing the difficulty of changing existing behaviour as the biggest obstacle to system adoption. Another 30 percent indicated that the need for development and customisation resources presented the biggest hurdle to getting new systems in place.

For fund managers, issues of cost, changing existing behaviour and development resources were all ranked equally as adoption challenges, with less than 10 percent indicating that cost was the greatest issue.

Some of Asia’s most modern buildings may have been built with low-tech systems

Building Asia’s Digital FuturePg. 18

With respondents having indicated that they see the industry, and the region, lagging global standards, while simultaneously continuing to work with simple information management tools such as spreadsheets, it appears that many real estate professionals in Asia have only just begun to improve information management at their companies.

As in many industries, the real estate professionals answering this survey point to internal resistance as holding back change. However, the more advanced adoption of systems by retail managers indicate that external threats, such as pressure from ecommerce, may be what drives industry players to upgrade their information management approaches.

In future surveys, it will be useful to investigate to what degree respondents see their industries as threatened by technological changes, and to look into potential origins for these perceived threats.

Where ecommerce has created pressure on shopping centre managers, will co-working operators be perceived as a threat by office developers? (To help answer that question,

CHAPTER 4CONCLUSIONS AND RECOMMENDATIONS

Mingtiandi will begin providing quarterly updates on that market segment beginning in early 2018.)

FUTURE SURVEYS WILL EXAMINE PERCEIVED THREATS AND THEIR ORIGINRising costs, such as salaries for analysts, are liable to increase the appeal of technology-based solutions, at the same time that a broader variety of options become available for users. Changes in employee behaviour, such as greater familiarity with database solutions, could also lower barriers to system adoption.

Given these rising incentives for adoption, combined with ever-lower barriers, future editions of this survey will track whether these conditions lead to changes in how Asia’s real estate industry manages information, and what form these shifts take.

Building Asia’s Digital FuturePg. 19

CONTACT Mingtiandi.comShanghai | Bangkok | Hong Kong For more information, contact [email protected]