Building Armenia’s - Proactiveinvestors UK€¦ · 3 NI 43-101 Disclosure Information concerning...

41

Building Armenia’s Largest Gold Mine Analysts Feasibility Study Presentation TSX:LYD September 2012 www.lydianinternational.co.uk

Transcript of Building Armenia’s - Proactiveinvestors UK€¦ · 3 NI 43-101 Disclosure Information concerning...

Building Armenia’s

Largest Gold Mine

Analysts Feasibility Study Presentation

TSX:LYD

September 2012 www.lydianinternational.co.uk

Forward Looking Statements

This presentation contains projections and forward looking information that

involve various risks and uncertainties regarding future events. Such

forward-looking information can include without limitation statements based

on current expectations involving a number of risks and uncertainties and

are not guarantees of future performance of the Company. These risks and

uncertainties could cause actual results and the Company’s plans and

objectives to differ materially from those expressed in the forward-looking

information. Actual results and future events could differ materially from

anticipated in such information. These and all subsequent written and oral

forward-looking information are based on estimates and opinions of

management on the dates they are made and expressly qualified in their

entirety by this notice.

The Company assumes no obligation to update forward-looking information

should circumstances or management’s estimates or opinions change. This

presentation does not constitute an offer to sell or a solicitation of an offer to

buy any securities of the Company within the United States or otherwise.

www.lydianinternational.co.uk 2

3

NI 43-101 Disclosure

www.lydianinternational.co.uk

Information concerning estimates of minerals reserves and resources

The mineral reserve and resource estimates reported in this presentation were prepared in accordance with Canadian National Instrument 43-101

standards of disclosure for mineral projects (‘NI 43-101’), as required by Canadian Securities Regulatory Authorities. For United States reporting

purposes, the United States Securities and Exchange Commission (‘SEC’) applies different standards in order to classify mineralization as a reserve. In

particular, while the terms ‘measured’, ‘indicated’ and ‘inferred’ mineral resources are required pursuant to NI 43-101, the SEC does not recognize such

terms. Canadian standards differ significantly from the requirements of the SEC. Investors are cautioned not to assume that any part or all of the

mineral deposits in these categories constitute or will ever be converted into reserves. In addition, ‘inferred’ mineral resources have a greater amount of

uncertainty as to their existence and great uncertainty as to their economic and legal feasibility. It cannot be assumed that all or any part of any inferred

mineral resource will ever be upgraded to a higher category. Under Canadian Securities laws, issuers must not make any disclosure of results of an

economic analysis that included inferred mineral resources, except in rare cases.

Under the guidelines of NI 43-101, the following qualified persons participated in a feasibility project for the Amulsar project.

The following individuals are Qualified Persons as defined by the CIM Definition Standards November 22, 2005 and Section 5.1 of National Instrument

43-101 Standards of Disclosure for Mineral Projects, Form 43-101F1 and Companion Policy 43-101CP.

Mr. Joseph M. Keane, P.E. of KD Engineering has responsibility for the report contents and preparation and all matters relating to the design and costs

of the processing facility. Mr. Keane visited the property May 2011. He has relied upon other experts for specific information in the Feasibility Study.

Mr. Richard Kiel, P.E. of Golder Associates, has responsibility for all matters relating to the HLF and WDF, the introduction, the geotechnical and the

update extracted from the NI-43-101 Preliminary Economic Assessment entitled “Development of Amulsar Heap Leach Facility”. Mr. Kiel visited the

property in June, September and October, 2011 and again in July, 2012.

Mr. Pete Lemke, P.E. of Golder Associates has responsibility for all matters relating to the Wastewater Treatment Plant design.

Mr. Herb Welhner, MMSA-QPM, of Independent Mining Consultants, has responsibility for all matters relating to geology, drilling, open pit and mine

design.

Mr. John Eyre, FRICS MIMMM MIQ Cenv of Wardell Armstrong International, has responsibility for all matters relating to the Environmental and Social

Impact Assessment and visited the property in June 2010 and 2011.

The NI 43-101 compliant Technical Report for the feasibility study of the Amulsar project will be filed on SEDAR within 45 days of September 5, 2012

press release announcing the results of the Feasibility Study.

www.lydianinternational.co.uk 4

Feasibility Study

Armenia and Amulsar

Armenia and Amulsar

www.lydianinternational.co.uk 5

• Armenia is a Democratic

presidential republic

• Member of WTO since

2003

• Mineral resources 60%

by value of exports

• New World Bank guided

Mining Law, effective

January 2012

• Located 170km from the

capital, Yerevan

• 4km from the nearest

town - Gorayk

Geology and Licence Outline

6 www.lydianinternational.co.uk

• High-Sulfidation

Epithermal Gold Deposit

• Volcaniclastic rocks of

dominantly dacitic

composition

• Entirely oxide

• Mineralization

dominantly fault and

fracture controlled with

some lithological/

stratbound control

• Two exploration licenses

• Mining license over main

Tigranes/Artavasdes pit

Drilling 2007 - 2011

www.lydianinternational.co.uk 7

Summary of Amulsar Geochemistry Samples

Project Year

Diamond Drilling RC Drilling Total

# of holes meters # of holes meters # of holes meters

Amulsar 2007 5 593 0 0 5 593

Amulsar 2008 18 2679.3 74 10363 92 13042.3

Amulsar 2009 8 1089.8 101 12446 109 13535.8

Amulsar 2010 52 7575.9 129 17036 181 24611.9

Amulsar 2011 198 16113.2 154 23099 352 39212.2

Total 2007-2011 281 28051.2 458 62944 739 90995.2

• A total of 739 holes have been drilled at Amulsar between 2007 and the end of 2011,

including, exploration, geotechnical, metallurgical, and sterilization holes

• Drilling continues in 2012 with exploration, step-out and infill

Drilling 2007-2011

8 www.lydianinternational.co.uk

Like many

development projects

drilling at Amulsar has

been focused by the

timeline on infill and

resource definition.

Limited exploration

drilling along the ridge

top has identified

other gold mineralized

zones that require

significant further

drilling and resource

definition work in the

coming years. These

zones include Orontes,

Erato North, Arshak

South and Tigranes

Northeast.

www.lydianinternational.co.uk 9

Feasibility Study

Mineral Resource Estimation

Mineral Resources January 2012

www.lydianinternational.co.uk

Resource Category Cut-off Grade Tonnes

(millions) Grade (g/t Au)

Gold Ounces

('000) Grade (g/t Ag)

Silver Ounces

('000)

Measured (M) 0.75 15.4 1.64 812 4.97 2459

0.5 27.7 1.18 1053 4.18 3720

0.4 36.5 1 1180 3.82 4489

0.3 50.2 0.83 1332 3.45 5574

0.2 70.7 0.66 1496 3.11 7065

Indicated (I) 0.75 13 1.57 655 4.78 1995

0.5 23.9 1.13 866 4.14 3178

0.4 32.2 0.95 986 3.84 3977

0.3 46.4 0.77 1143 3.48 5189

0.2 71.1 0.59 1339 3.13 7155

Total (M&I) 0.75 28.4 1.61 1467 4.88 4454

0.5 51.6 1.16 1919 4.16 6898

0.4 68.8 0.98 2166 3.83 8466

0.3 96.6 0.8 2475 3.47 10763

0.2 141.9 0.62 2835 3.12 14220

Inferred 0.75 15 1.45 696 4.56 2196

0.5 26.8 1.08 927 4.39 3779

0.4 35.5 0.92 1052 4.01 4580

0.3 48.1 0.77 1192 3.65 5645

0.2 73.9 0.59 1395 3.12 7410

10

The mineral resource is based on drilling completed through the 2011 drill season and includes a total of 665 core and reserve

circulation (RC) holes. The mineral resource was originally reported in the IMC report “2012 Mineral Resource Estimate, Amulsar

Gold Project, NI 43-101 Technical Report”, dated January 22, 2012. The mineral resource is summarized at several cut-off grades,

with the resource at a 0.40 g/t gold cut-off being the tonnage and grade that was selected to be reported.

Block Model and Floating Cone Resource

www.lydianinternational.co.uk 11

The mineral resource is based on drilling

completed up to and through the 2011 drill

season and includes a total of 665 core and

reserve circulation (RC) holes. Gold and silver

grades in the Amulsar model were estimated

using inverse distance to the eighth power

(ID8), spherical search ellipsoids of 50 meters

in Tigranes and Artavasdes and 100 meters in

Erato and no internal domain boundaries.

The mineral resource is summarized in slide

10 at several cutoff grades, with the resource

at a 0.40 g/t gold cutoff being the tonnage and

grade that was selected to be reported. Higher

and lower cutoff grades are presented to show

the distribution of tonnage and grades. The

mineral resource is within a floating cone

geometry based on US$ 1300/oz gold price (no

credit for silver) and preliminary estimates of

gold recovery and operating costs provided in

January 2012. Additional definition of these

estimates were subsequently done and used

for the definition of the mineral reserve. The

reported mineral resource represents about 98

percent of the model contained mineralization.

www.lydianinternational.co.uk 12

Measured and Indicated Mineral Resource

0.20-0.75 g/t cut-off

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

0

20

40

60

80

100

120

140

160

0.75 0.5 0.4 0.3 0.2

Au

(g

/t)

To

nn

ag

e (

Mt)

Tonnes

Gold g/t

Cut-off Grade (g/t)

13 www.lydianinternational.co.uk

Feasibility Study

Mineral Reserve and

Mine Plan

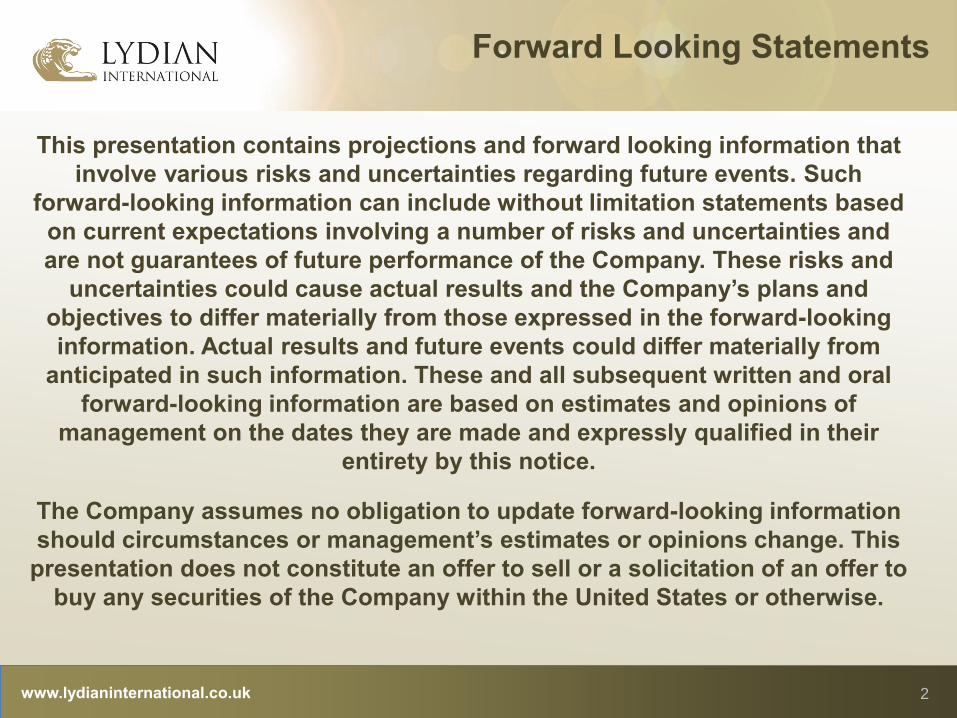

Project Assumptions and Parameters

14 www.lydianinternational.co.uk

Steady State Annual

Gold Production

First 3 Years

= 118,341 oz

Average LOM Cash

Cost = S$468.5/oz

Assumptions

Gold price (US$/oz) 1,200

Foreign Exchange Rate (AMD/US$) 389:1

Electricity (US$/kWh) 0.06

Tax Deductible Royalty ‘Top Line’ Charge (%) 4.0

Tax Deductible Royalty ‘Bottom Line’ Charge (%) 12.5

Corporate Tax (%) 20.0

Mine Parameters (LOM)

Average Strip ratio (waste:ore) 2.23

Average Gold Grade (g/t) 0.75

Average Silver Grade (g/t) 3.27

Total Contained Gold (M oz) 2.26

Total Contained Silver (M oz) 9.63

Estimated Gold Recovery (%) 88.6

Estimated Silver Recovery (%) 36.9

Total Recovered Gold (M oz) 2.03

Total recovered Silver (M oz) 3.68

Mine life (years) 12

Average Annual Silver Production (oz) 306,706

Steady State Average Annual Gold Production Yrs 1 to 3 (oz) 118,341

Steady State Average Annual Gold Production Yrs 4 to 12 (oz) 186,047

Note: Please see www.lydianinternational.co.uk for a detailed explanation on the Mining taxes

www.lydianinternational.co.uk

Mineral Reserves

Mineral Reserves at US$1200/oz and a variable cut-off grade by year

Reserve

category

Ore

(‘000s)

Gold Grade

(g/t)

Silver Grade

(g/t) Gold oz Silver oz

Proven 51,143 0.801 3.37 1,317,000 5,541,000

Probable 37,106 0.789 3.43 941,000 4,092,000

Total (P&P) 88,249 0.796 3.40 2,258,000 9,633,000

• Some material in year two above 0.3g/t recoverable gold stockpiled

• The gold and silver recoveries vary by deposit area based on the metallurgical test

work. A recoverable grade for gold and silver is assigned in the block model and

used for tabulations

15

Mine Schedule

16 www.lydianinternational.co.uk

Waste tonnes mined, ore tonnes sent to the crusher and

recoverable ounces of gold put on to the heap leach.

0

50,000

100,000

150,000

200,000

250,000

300,000

0

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

Yr1 Yr2 Yr3 Yr4 Yr5 Yr6 Yr7 Yr8 Yr9 Yr10 Yr11 Yr12

Dilu

ted

Rec

ove

rab

le O

un

ce

s p

ut

on

Hea

p o

z.

To

nn

es

Mo

ve

d i

n P

eri

od

Waste Mined

Ore to Crusher

OZ. Au to Heap

. The drop in ounce

production in Years 7 to 10

is a result of the

commencement of mining in

the early stages at Erato. As

the drill density at Erato is

less, a larger proportion of

the material inside the

ultimate pit shell is in the

inferred category and hence

cannot be included in this

study. It is expected that as

exploration activities

continue in 2012 and 2013,

more material will be

upgraded from inferred and

this drop in ounces

produced can be reduced.

Increased understanding of

the Erato ore body will also

lead to more optimized stage

designs which will also

improve the production

schedule in the later years.

Pit Reserve

17 www.lydianinternational.co.uk

Erato

Tigranes/ Artavasdes

Au Grade g/t

Green 0.1 - 0.5

Yellow 0.5 - 1.0

Red >1.0

www.lydianinternational.co.uk 18

Feasibility Study

Infrastructure and

Process Plant

Mine Layout Plan

19 www.lydianinternational.co.uk

Waste Dump

Truck Shop

Maintenance

Shop

Waste Water Treatment Plant

Open

Pit

Crushing

Plant

Hydro Plant

Rom

Stockpile

Heap

Leach

Pad

Mine Access Road

Solution

Ponds

Mine

Camp

ADR Plant

Water Tank

ERATO

TIGRANES

ARTAVASDES

ARSHAK

Topsoil Stockpile

Mine

Offices

GORAYK

Phase 4 – Allows

expansion from

90Mt to 120 Mt

(not costed in FS)

Haulage Road

Crushing Plant Flow Diagram

www.lydianinternational.co.uk 20

www.lydianinternational.co.uk

ADR Plant and Heap Leach

21

Pad Capacity

Process water sourced from river

CELL 1 + CELL 2 = +/- 17.8Mt

CELL 3 + CELL 4 = +/- 27.8Mt

CELL 5 + CELL 6 = +/- 49.4Mt

TOTAL CAPACITY = 95.1Mt

• Total Capacity of Cells 1 - 6 = 95.1Mt as per the

FS mine schedule

• Construction of Cells is staged to optimise

capital spend

• Extra Capacity of 30Mt (+/- 3 yrs production) to

give total heap capacity of 125Mt as pits increase

• Leach ponds designed for a 1 in 100 year event

• ADR Plant standard design, carbon columns,

gold room etc

• Water sourced from Vorotan River

• Potential for water to be sourced from Waste

Dump reducing requirement for Waste Water

Treatment Plant

• Heap Leach Height 72m, lifts of 8m at a time

• Stacking completed with portable stacker

conveyors

• No agglomeration required

• Low lime and cyanide consumption

• Short recovery time

Overall Flowsheet

www.lydianinternational.co.uk 22

www.lydianinternational.co.uk

MINE MANAGER Tim Richards

HR MANAGER

LOGISTICS &

SUPPORT

MANAGER

FINANCE

MANAGER

PRODUCTION

MANAGER PROCESS

MANAGER ENGINEERING

MANAGER SECURITY

MANAGER

ENVIRONMENTAL

MANAGER CONSTRUCTION

MANAGER OH&S

MANAGER Tony Nicotra Murray Wright Stephen Ainsworth

CONSTRUCTION

MANAGER CHIEF

ACCOUNTANT

MAINTENANCE

SUPERINTENDENT

TECHNICAL

SERVICES

SUPERINTENDENT

PRODUCTION

SUPERINTENDENT

CRUSHER &

CONVEYOR

SUPERINTENDENT

ADR & HEAP

SUPERINTENDENT

METALLURGIST

ELECTRICAL

SUPERINTENDENT

MECHANICAL

SUPERINTENDENT

CAMP

SUPERINTENDENT

WAREHOUSE

SUPERINTENDENT

I.T

SUPERINTENDENT

TRAINING

SUPERINTENDENT

DOCTOR

SECURITY

CONTRACTOR

COMMUNITY

LIAISON

Carl Nicholas

ENVIRONMENTAL

OFFICER

EPCM

FIRM

HLF & WASTE

DUMP

CONSULTANTS

ARMENIAN

CIVILS

CONTRACTOR

CONSTRUCTION &

OPERATIONS

CONSTRUCTION

ONLY

OPERATIONS ONLY

KEY

Construction and Production

Senior Team

The total workforce during operation is

estimated at around 550 employees. The

total workforce during construction is

estimated at 600.

23

www.lydianinternational.co.uk

Upcoming Engineering and Construction

Events

24

• Construction due to start end of 2012

• Engineering contract to be awarded Q4 2012

• Detailed Engineering Studies to be

completed by the end of Q2 2013

• PCM contract to be awarded H1 2013

www.lydianinternational.co.uk 25

Feasibility Study

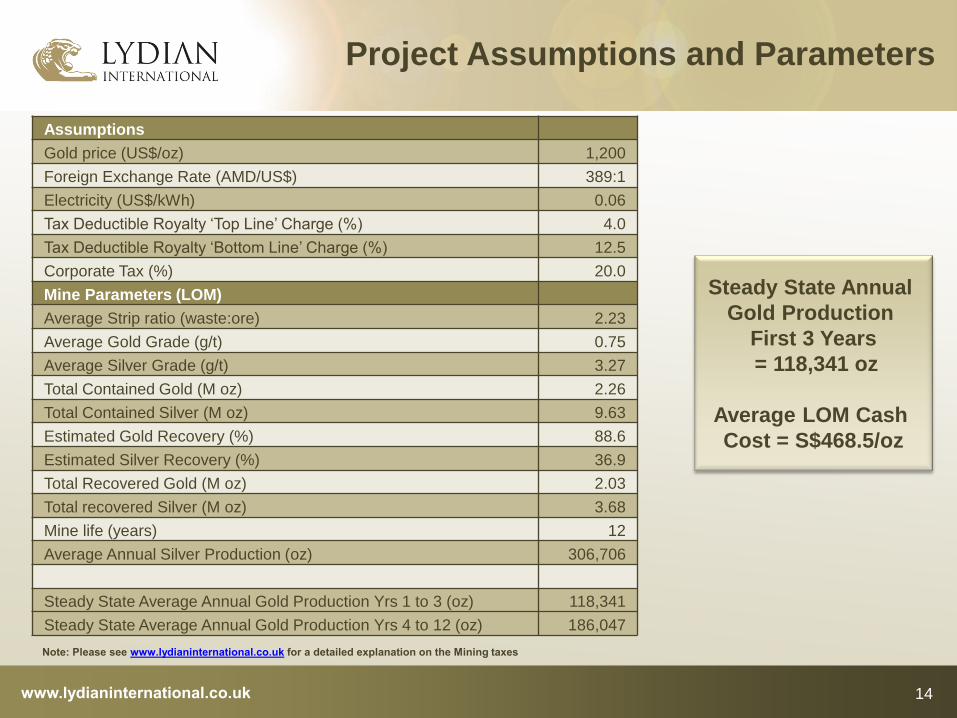

Capital Expenditures

Capital Expenditures

Note: The level of accuracy of the capital costs estimates is within ±15% for feasibility studies. Sustaining costs include the majority of the capital costs associated with the Phase II expansion.

www.lydianinternational.co.uk

Item Initial

Capital US$

Sustaining

Capital US$ Total US$

Mining Cost 8,791,700 17,189,800 25,981,500

Process Plant Direct Cost 228,568,063 26,872,254 255,440,318

Waste Water Treatment Plant 19,078,412 19,078,412

Leach Pads 15,687,450 31,814,488 47,501,938

Waste Dump 16,575,893 14,302,181 30,878,074

Closure and Reclamation 37,221,477 37,221,477

Total Initial and Future

Sustaining Project Capital 269,623,106 146,478,612 416,101,718

Total Initial and Future Sustaining Project Costs

26

www.lydianinternational.co.uk 27

Feasibility Study

Operating Costs

Cash Operating Expenses

LOM Average First 3yrs

Item US$/Tonne Ore Mined US$/oz US$/oz

Mining 5.50 257.11 241.18

Mining Equipment Lease Cost 0.79 37.04 91.18

Processing 2.92 136.55 140.59

Waste Water Treatment Plant 0.13 6.05 9.43

G & A 0.47 21.88 31.37

Cash Operating Costs 9.81 458.63 513.75

Newmont Payment 0.21 9.85 33.80

Total Cash Operating Costs 10.02 468.48 547.55

www.lydianinternational.co.uk

Note: Mining and Mine Lease costs also fall in Year -2 and Year -1. See table 22.3 in the Feasibility Study report. First 3 years are years 1, 2 and 3.

28

www.lydianinternational.co.uk

Mine Operating Cost Profile

29

Note: Mine Operating costs also fall in Year -1. See table 22.3 in the Feasibility Study report.

The average stripping ratio in the first 3 years of mining is 1.8:1 waste:ore. Beginning in

year 4, the stripping ratio increases to 2.35:1 and continues at that ratio to year 10. Average

Mining Cost per tonne mined is US$1.66 and average Leasing Cost per tonne mined is

US$0.29

0

0.5

1

1.5

2

2.5

3

$0

$1

$2

$3

Yr1 Yr2 Yr3 Yr4 Yr5 Yr6 Yr7 Yr8 Yr9 Yr10 Yr11 Yr12

Stri

p R

atio

Co

st p

er

ton

ne

Min

ed

(U

S$)

Mining Cost per tonne Mined (US$)

Strip Ratio

LOM Strip Ratio 2.23

Leasing Cost per tonne Mined (US$)

www.lydianinternational.co.uk

Major Mining Fleet

Equipment type Yr -1 Yr 1 Yr 2 Yr 3 Yr 4 Yr 5 Yr 6 Yr 7 Yr 8 Yr 9 Yr 10 Yr 11 Yr 12

Sandvik DP1500 Drill 0 3 2 3 7 7 7 7 7 7 7 6 1

10 cu m Excavator 0 1 1 1 2 2 2 2 2 2 2 2 2

17 cu m Excavator 0 1 1 1 2 2 2 2 2 2 2 2 2

Cat 777 Haul Truck 0 19 19 20 37 37 37 37 34 25 24 24 18

Cat D10 Tractor Dozer 1 3 3 3 3 3 3 3 3 3 3 2 2

Cat 824G Wheel Dozer 1 1 1 1 1 1 1 1 1 1 1 1 1

Cat 16M Motor Grader 1 1 1 1 1 1 1 1 1 1 1 1 1

Cat 777 Water Truck 1 1 1 1 1 1 1 1 1 1 1 1 1

Cat 992G Wheel Loader 1 1 1 1 1 1 1 1 1 1 1 1 1

Cat 336DL Excavator 1 1 1 1 1 1 1 1 1 1 1 1 1

Total 6 32 31 33 56 56 56 56 53 44 43 41 30

30

www.lydianinternational.co.uk 31

Feasibility Study

Project Economics

www.lydianinternational.co.uk

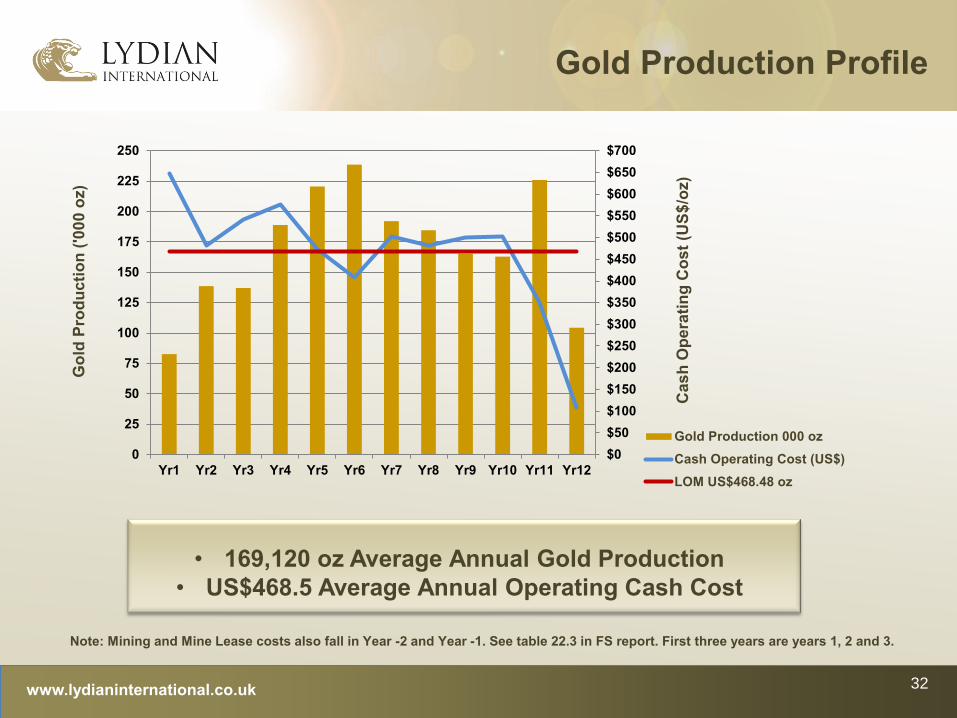

Gold Production Profile

32

Note: Mining and Mine Lease costs also fall in Year -2 and Year -1. See table 22.3 in FS report. First three years are years 1, 2 and 3.

$0

$50

$100

$150

$200

$250

$300

$350

$400

$450

$500

$550

$600

$650

$700

0

25

50

75

100

125

150

175

200

225

250

Yr1 Yr2 Yr3 Yr4 Yr5 Yr6 Yr7 Yr8 Yr9 Yr10 Yr11 Yr12

Cas

h O

pe

rati

ng

Co

st

(US

$/o

z)

Go

ld P

rod

ucti

on

('0

00

oz)

Gold Production 000 oz

Cash Operating Cost (US$)

LOM US$468.48 oz

• 169,120 oz Average Annual Gold Production

• US$468.5 Average Annual Operating Cash Cost

www.lydianinternational.co.uk

Financial Analysis

33

Base Case

Discount Rate Undiscounted 5% 10%

NPV pre-tax (US$M) 1121.6 646.0 366.8

Payback (yrs) 4

Net Cash Flow (US$B) 1.17

Gold Price, US$/oz US$1100 US$1200 US$1300 US$1400 US$1500

NPV @5% (US$M) 513 646 779 913 1,046

IRR (%) 23.8 27.7 31.3 34.8 38.1

Payback (yrs) 4.5 4.0 3.7 3.4 3.1

At a gold price of $1,500, pre-tax NPV is in excess of $1.05 billion, the IRR is

robust at 38.1% and the pre-tax operating cash flow is expected to be

around $1.73 billion.

www.lydianinternational.co.uk

Financial Analysis - Sensitivities

34

Capex change +10% Base Case -10%

NPV @ 5% ($M) 611 646 681

IRR (%) 25.2 27.7 30.5

Operating Cost change +10% -10%

NPV @ 5% ($M) 582 646 681

IRR (%) 25.7 27.7 29.7

Gold Recovery change +10% -10%

NPV @ 5% ($M) 806 646 486

IRR (%) 32.0 27.7 23.0

The Project is not very sensitive to changes in capital costs nor operating

costs. A 10% improvement in gold recovery can improve IRR to 32% (an

increase of nearly 16%).

www.lydianinternational.co.uk 35

Feasibility Study

Permitting

www.lydianinternational.co.uk

Current ML,

CA & RAA

(2009)

New

Resources

& ML

EIA Approved

HLF

& Processing

EIA Approval

Pit and

Waste

Mining License

Concession

Agreement and

RAA

Plant EIA after

Detailed Engineering

and EIA on

new resources

March 2009 Nov 2011 Feb 2012 Estimated Date H1 2013

Pit approved over

approximately

600k oz gold.

Rock Allocation

Area (RAA, or

mine footprint)

over pit and

prospect areas.

Under Concession

Agreement (CA)

must mine at least

2.25Mt ore before

March 2015.

New

resources,

pit-outline

and

Mining

License

approved.

EIA

approved

for Heap

Leach Facility,

crushing,

conveying

and ADR

Plant

EIA approval

for open-pit

mining and

location of

waste dump

facility

Outline new Rock Allocation Area (RAA) to cover complete mine layout Execute new Mining License Concession Agreement

EIA approval once all

detailed engineering is

submitted and new

resources EIA for areas

that warrant pit

extensions e.g. Erato.

Mine Closure Plan

EIA to be submitted

minimum of two years

before mine closure

Independent

Review of

International

ESIA

July 2012 Sept 2012

Independent

review of the

International

ESIA

requested by

the Ministry

of Nature

Protection

Q4 2012

Permits and Licenses

36

www.lydianinternational.co.uk 37

Feasibility Study

Opportunities

www.lydianinternational.co.uk

Opportunities – Expansion

38

• 25,000 metre drill programme on-going in

2012

• Approx. 28% exploration, 36% infill and

36% step out

• Key objective of the programme is to link

up Erato with Tigranes/ Artavasdes

• Expected to add to reserves in 2013

• Even with the extensive 2011 drill

campaign, the Amulsar deposit remains

open at depth. The Artavasdes area

remains open along strike and to the

south. The area to northeast of Tigranes

has untested potential on the extensions

of the main northeast trending

mineralized faults. The Erato area

remains open in all directions and limited

drilling has occurred at the Erato North

target

www.lydianinternational.co.uk

Opportunities – Increasing Resource

at Erato

www.lydianinternational.co.uk

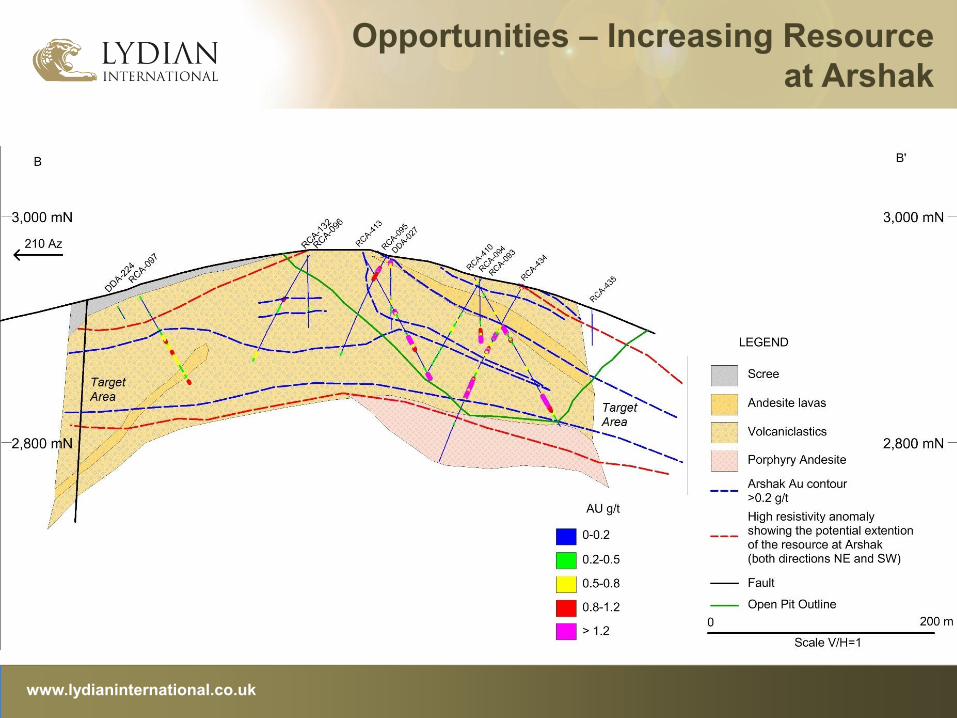

Opportunities – Increasing Resource

at Arshak

www.lydianinternational.co.uk

Opportunities

41

The Company intends to carry out additional studies with a view

to further optimising project economics, including:

• Adding new reserve ounces

• Eliminating the Phase II ramp up and commencing initial

production at 10 Mtpa

• Comparing the installation of a single gyratory versus two

jaw crushers

• Reviewing key infrastructure layout and configuration