Building an Oncology Franchise: Lessons from the...

53

Therapeutic Alliances Series – Oncology June 6, 2006 - Pg. 1 © Defined Health, 2006 Building an Oncology Franchise: Lessons from the Past, View of the Present, and Speculation on the Future June 6, 2006 Jeffrey M. Bockman, PhD Vice President, Defined Health

Transcript of Building an Oncology Franchise: Lessons from the...

Therapeutic Alliances Series – OncologyJune 6, 2006 - Pg. 1

© Defined Health, 2006

Building an Oncology Franchise: Lessons from the Past, View of the Present, and Speculation on the Future

June 6, 2006Jeffrey M. Bockman, PhD

Vice President, Defined Health

Therapeutic Alliances Series – OncologyJune 6, 2006 - Pg. 2

© Defined Health, 2006

The information in this report has been obtained from what are believed to be reliable sources and has been verified whenever possible. Nevertheless, we cannot guarantee the information contained herein as to accuracy or completeness. All expressions of opinion are the responsibility of Defined Health, and though current as of the date of this report, are subject to change.

Therapeutic Alliances Series – OncologyJune 6, 2006 - Pg. 3

© Defined Health, 2006

From Slow Beginnings to Rapid Growth

Commercialization of penicillin Nature Reviews Cancer, January 2005

Therapeutic Alliances Series – OncologyJune 6, 2006 - Pg. 4

© Defined Health, 2006

Oncology Market

Therapeutic Alliances Series – OncologyJune 6, 2006 - Pg. 5

© Defined Health, 2006

Targeted Cytostatics Drive Growth

*excludes interferon sales

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

2005 2010

CytotoxicsCytostaticsImmunomodulators

Estimate Worldwide Market for Oncology Drugs ($MM)

Cytotoxics: Standard chemotherapeutics (i.e. Microtubule-targeting, DNA-targeting, DNA replication & antimetabolites), novel chemotherapies (i.e. HSP, KSP inhibitors, and aurora kinase inhibitors), and hormonal agents

Cytostatics:: Includes monoclonal antibodies, small molecule TKIs, multi-kinase inhibitors, but excludes blood cell factors.

Immunomodulators:: Revlimid and Cancer Vaccines

9% CAGR

27% CAGR

39 % CAGR

EvaluatePharma®, Defined Health analysis

Therapeutic Alliances Series – OncologyJune 6, 2006 - Pg. 6

© Defined Health, 2006

Therapeutic Oncology – Significant Growth

EvaluatePharma®, Defined Health analysis

Therapeutic Alliances Series – OncologyJune 6, 2006 - Pg. 7

© Defined Health, 2006

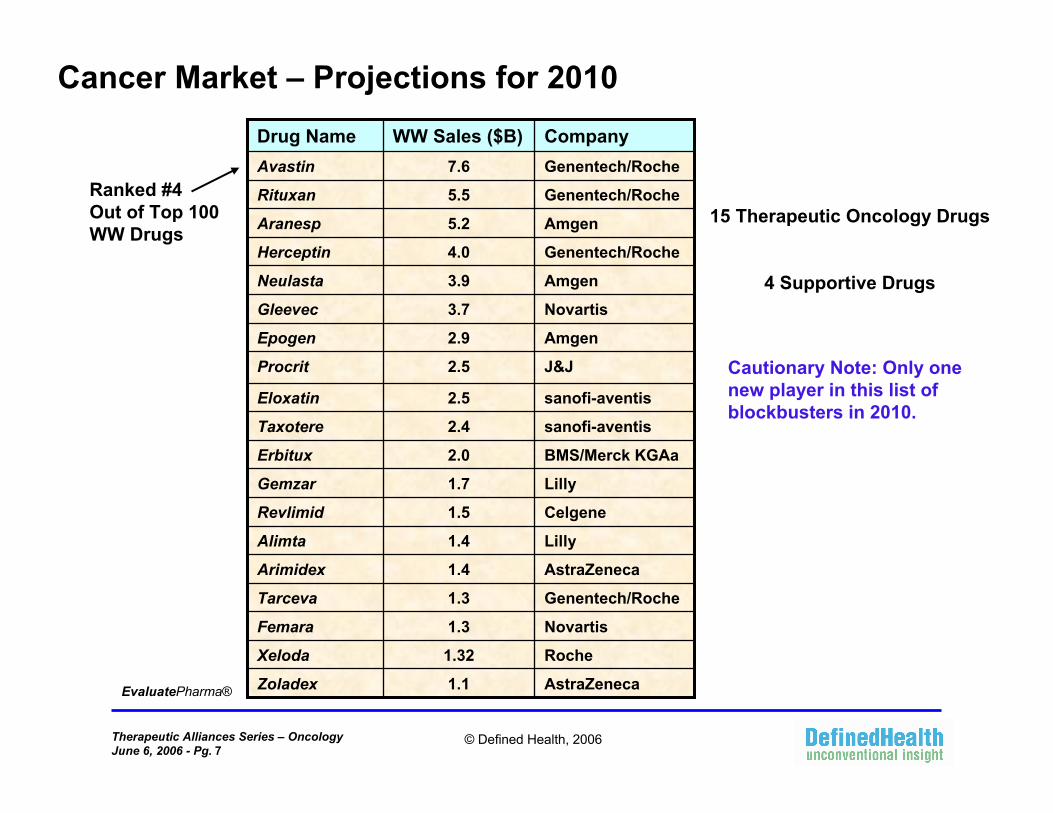

Cancer Market – Projections for 2010

EvaluatePharma®

Ranked #4 Out of Top 100 WW Drugs

Celgene1.5Revlimid

Lilly1.4Alimta

AstraZeneca1.4Arimidex

Genentech/Roche1.3Tarceva

Novartis1.3Femara

Lilly1.7Gemzar

Roche1.32Xeloda

Genentech/Roche7.6Avastin

AstraZeneca1.1Zoladex

BMS/Merck KGAa2.0Erbitux

sanofi-aventis2.4Taxotere

sanofi-aventis2.5Eloxatin

J&J2.5Procrit

Amgen2.9Epogen

Novartis3.7Gleevec

Amgen3.9Neulasta

Genentech/Roche4.0Herceptin

Amgen5.2Aranesp

Genentech/Roche5.5Rituxan

CompanyWW Sales ($B)Drug Name

15 Therapeutic Oncology Drugs

4 Supportive Drugs

Cautionary Note: Only one new player in this list of blockbusters in 2010.

Therapeutic Alliances Series – OncologyJune 6, 2006 - Pg. 8

© Defined Health, 2006

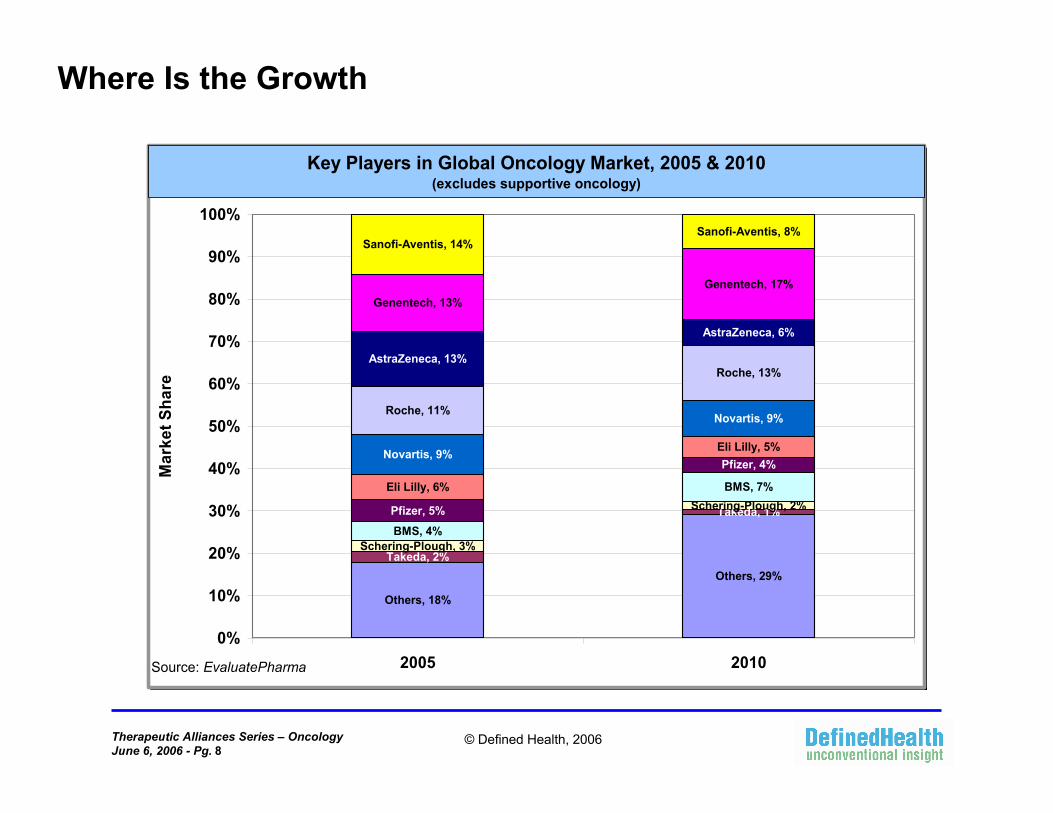

Where Is the Growth

Others, 18%

Others, 29%Takeda, 2%

Takeda, 1%

Schering-Plough, 3%

Schering-Plough, 2%

BMS, 4%

BMS, 7%

Pfizer, 5%

Pfizer, 4%

Eli Lilly, 6%

Eli Lilly, 5%Novartis, 9%

Novartis, 9%Roche, 11%

Roche, 13%AstraZeneca, 13%

AstraZeneca, 6%

Genentech, 13%Genentech, 17%

Sanofi-Aventis, 14%Sanofi-Aventis, 8%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2005 2010

Mar

ket S

hare

Key Players in Global Oncology Market, 2005 & 2010(excludes supportive oncology)

Source: EvaluatePharma

Therapeutic Alliances Series – OncologyJune 6, 2006 - Pg. 9

© Defined Health, 2006

Future Trends in Therapy

Therapeutic Alliances Series – OncologyJune 6, 2006 - Pg. 10

© Defined Health, 2006

MOAs – Expanding, Overlapping

Making decisions about the best targets is difficult, given the large number of them.

Cell, January, 2000

Any given target is expanding into multiple, interconnected targets

Therapeutic Alliances Series – OncologyJune 6, 2006 - Pg. 11

© Defined Health, 2006

Future of Anticancer Therapy

Conventional Chemotherapy

Conventional Chemotherapy

TargetedTherapy

TargetedTherapy

Cancer Early Advanced

MolecularDiagnostics Molecular

Diagnostics

2005 2010

Cancer Early AdvancedAdvancedConventionalChemotherapy

TargetedTherapy

CombinationAdvancedCombination

ConventionalChemotherapy

TargetedTherapy

Targeted Therapy A

Targeted Therapy B

2 TargetedAgents

Defined Health analysis

Therapeutic Alliances Series – OncologyJune 6, 2006 - Pg. 12

© Defined Health, 2006

Anticancer Therapy Evolutionary Timeline

1990s 2000s 2010

Conventional Chemotherapy – Cytotoxics• Platinums• Taxanes• Topoisomerase

inhibitors• Alkylating agents

1st Generation Targeted

(ERBB, VEGF):• Herceptin• Gleevec• Erbitux• Iressa, Tarceva• Rituxan• Avastin

Multi-Targeted (kinases):

• Sunitinib• Sorafenib• Lapatinib• Combinations of

targeted agents (e.g., Anti-EGF plus Avastin)

1980sNovel Targetscytotoxic, cytostatic• Histone

deacetylaseinhibitors

• Heat shock protein inhibitors

• mTOR/Aktinhibitors

• Aurora kinase/Polo kinase inhibitors

Defined Health Analysis

Therapeutic Alliances Series – OncologyJune 6, 2006 - Pg. 13

© Defined Health, 2006

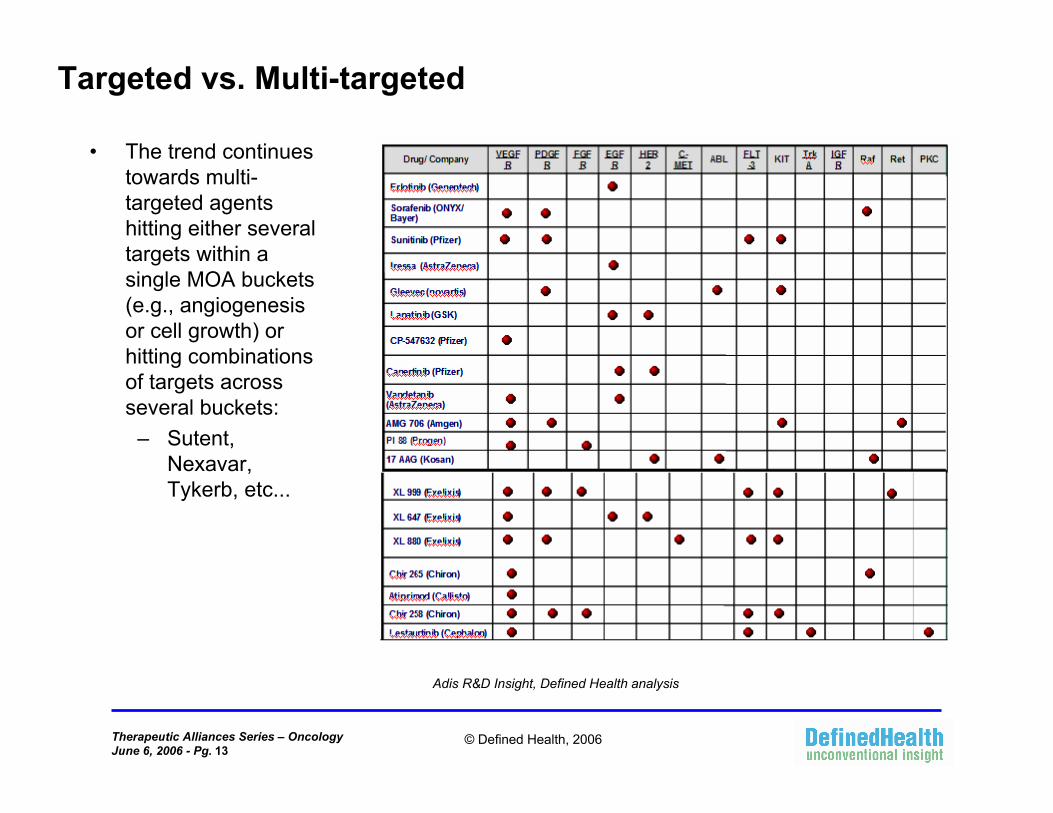

Targeted vs. Multi-targeted

• The trend continues towards multi-targeted agents hitting either several targets within a single MOA buckets (e.g., angiogenesis or cell growth) or hitting combinations of targets across several buckets:

– Sutent, Nexavar, Tykerb, etc...

Adis R&D Insight, Defined Health analysis

Therapeutic Alliances Series – OncologyJune 6, 2006 - Pg. 14

© Defined Health, 2006

Targeted vs. Multi-targeted

• But while smallmolecules, especially multi-targeted ones, constitute a majority of the drugs in the Phase I and higher pipeline for many tumors, largemolecules—including antibodies, oligonucleotides and vaccine approaches-lag behind, despite the significant contribution to sales in the category of the antibodies.

Adis R&D Insight, Defined Health analysis

NSCLC, Phase I and higher

SmallLarge

CRC, Phase I and higher

SmallLarge

BC, Phase I and higher

SmallLarge

Therapeutic Alliances Series – OncologyJune 6, 2006 - Pg. 15

© Defined Health, 2006

“Hit Hard, Hit Early” vs. “Sequential & Reserve”

• Oncologists are split between two related approaches to therapy:– Hit hard, hit early: does one use these agents together with current regimens to

suppress the tumor as quickly and completely as possible, or in doing so does one set up a situation for creating escape mutants, in which case one should reserve some of these for later lines of therapy (second through salvage). This is being debated hotly around use of the follow-ons developed for Gleevec-resistant mutants: should they be used instead of Gleevec, with Gleevec, or post Gleevec failures?

– Hit multiple pathways versus complete shutdown of a pathway: These are not mutually exclusive but some oncologists think combining TKIs and anti-receptor antibodies is a good idea, in which case one could add a SSKI to Erbitux or Avastin, others are more skeptical and would envision wanting to add oncompletely novel MOAs (Avastin plus HDAC inhibitor, for example).

Defined Health analysis

Therapeutic Alliances Series – OncologyJune 6, 2006 - Pg. 16

© Defined Health, 2006

Shutdown Single Pathway vs. Multiple Pathways

• Defined Health’s research suggests that while it would seem to be obvious to hit multiple pathways, given the heterogeneity and genetic instability of cancer cells, some oncologists favor shutting down a pathway completely over partially shutting down several pathways.

– For example: combining antibodies and TKIs to completely block cell growth signals through EGF.

– In this context, there is some relevance to the management of HIV, where multiple agents within a class and several classes are used to control the viral replication.

Defined Health analysis

Therapeutic Alliances Series – OncologyJune 6, 2006 - Pg. 17

© Defined Health, 2006

“Hit Hard, Hit Early” vs. “Sequential & Reserve”

• This is exemplified by the debate among hematologist oncologists regarding management of CML: On a theoretical level (that is, within the broader question of how to treat human cancer), there is disagreement as to whether combination therapy of Gleevec plus an agent hitting the Gleevec-resistant mutations or monotherapy with a more potent agent that hits wild type bcr-abl and the various mutations represents a logical first line approach. While many physicians believe that aggressive first line therapy makes sense since it theoretically can induce a long-lasting remission or perhaps eradicate disease, some believe that such an approach will only induce multi-drug resistant clones more rapidly.

– Clearly, as for HIV, clinical data will be needed to decide between these competing views.

Defined Health analysis

Sprycel (dasatinib), Nilotinib (AMN107)

Therapeutic Alliances Series – OncologyJune 6, 2006 - Pg. 18

© Defined Health, 2006

Pipeline Activity – Phase I and Higher

MBC

CRC

HRPC

NSCLC

Adis R&D Insight, Defined Health analysis

Therapeutic Alliances Series – OncologyJune 6, 2006 - Pg. 19

© Defined Health, 2006

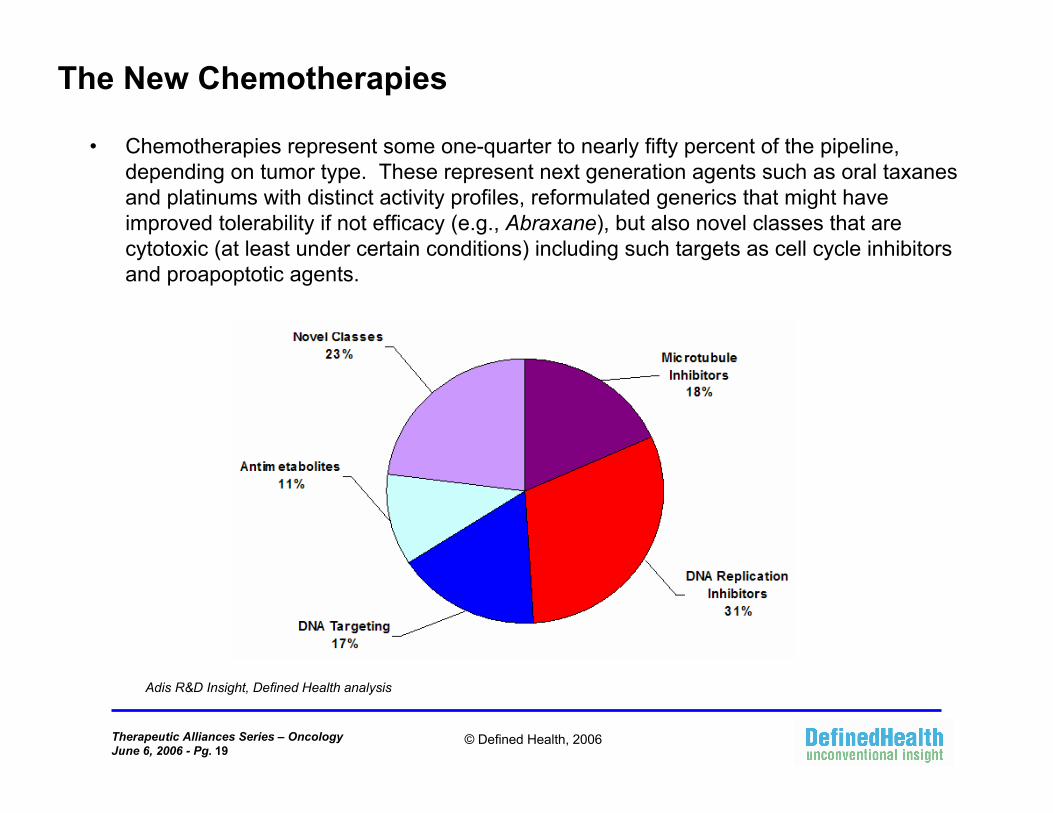

The New Chemotherapies

• Chemotherapies represent some one-quarter to nearly fifty percent of the pipeline, depending on tumor type. These represent next generation agents such as oral taxanes and platinums with distinct activity profiles, reformulated generics that might have improved tolerability if not efficacy (e.g., Abraxane), but also novel classes that are cytotoxic (at least under certain conditions) including such targets as cell cycle inhibitors and proapoptotic agents.

Adis R&D Insight, Defined Health analysis

Therapeutic Alliances Series – OncologyJune 6, 2006 - Pg. 20

© Defined Health, 2006

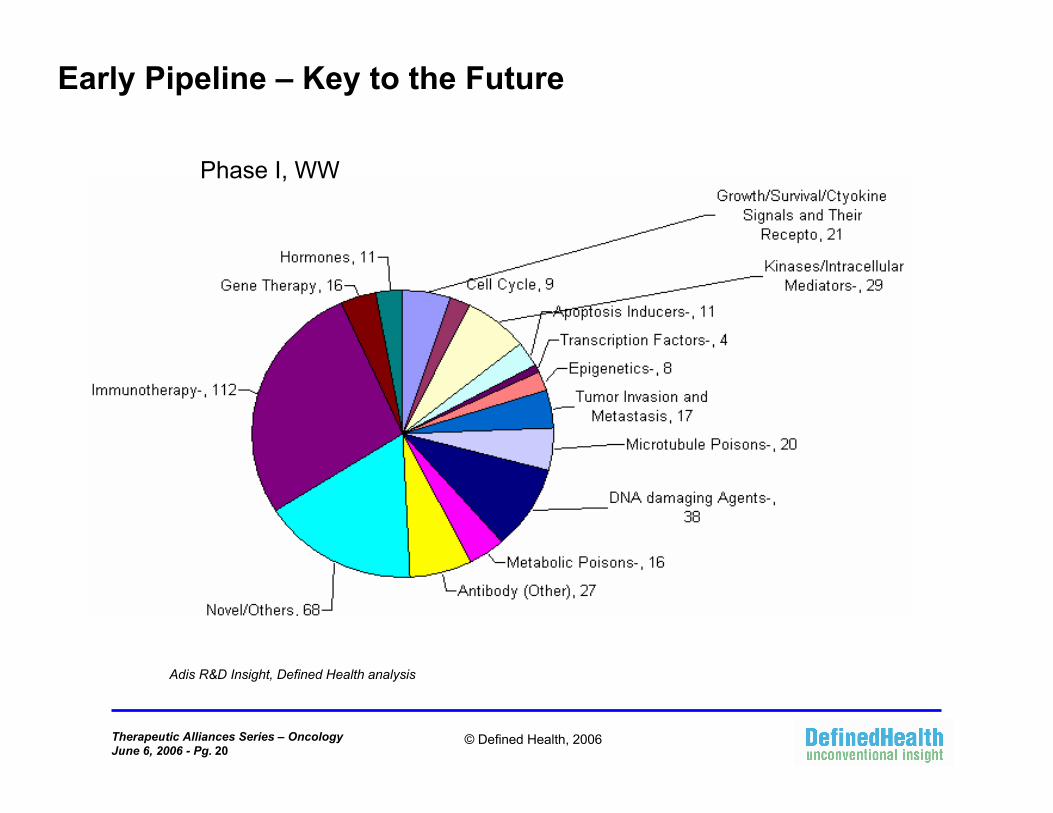

Early Pipeline – Key to the Future

Adis R&D Insight, Defined Health analysis

Phase I, WW

Therapeutic Alliances Series – OncologyJune 6, 2006 - Pg. 21

© Defined Health, 2006

Anti-CancerMOA’s –

Major Buckets

Anti-metabolites

Signal Transduction - Master Switches

Immunological Targets

Other InterestingMechanisms

Epigenetic Agents

Hormone Therapy Transcriptional

Regulation

Microtubule / Cytoskeletal

Inhibitors

Cell Cycling

DNA Targeting Agents

Cell and Gene Therapies

Other signal transduction

pathwaysPro-Apoptotic Mechanisms

Angiogenesis, cellular

Trafficking, Tumor Invasion

Growth Factor Receptors

Essential MOA Buckets

IDdb, Adis R&D Insight

Therapeutic Alliances Series – OncologyJune 6, 2006 - Pg. 22

© Defined Health, 2006

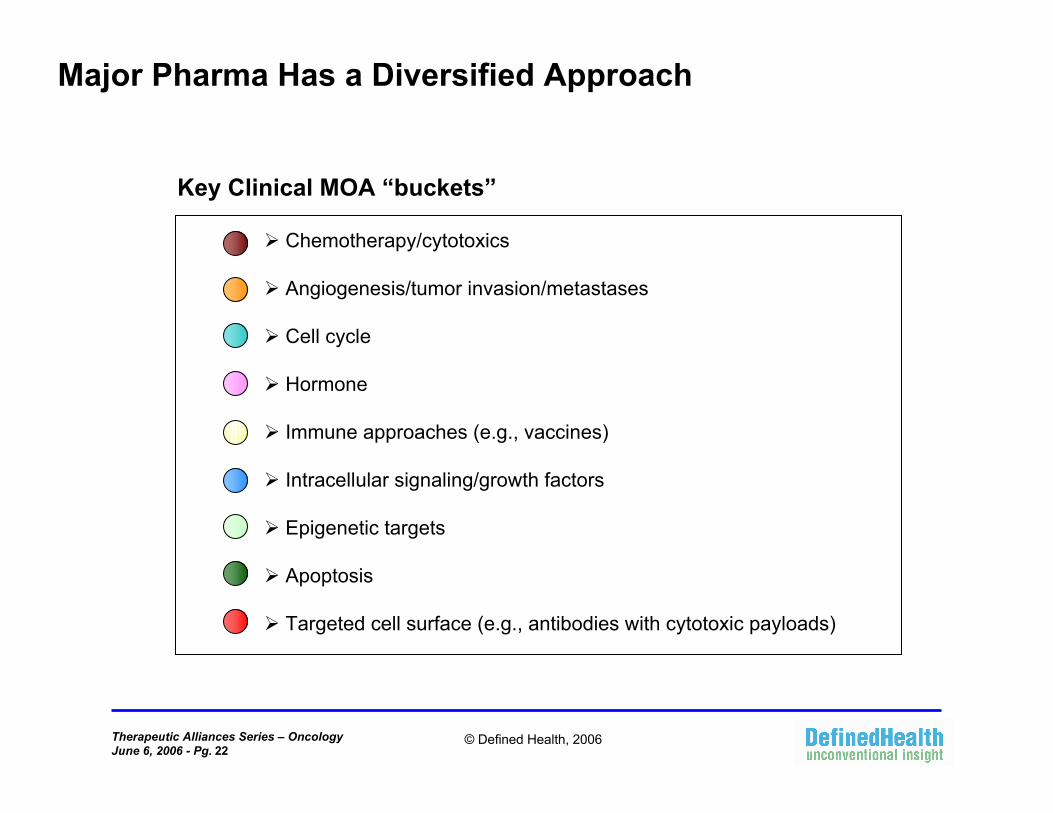

Major Pharma Has a Diversified Approach

Key Clinical MOA “buckets”

Chemotherapy/cytotoxics

Angiogenesis/tumor invasion/metastases

Cell cycle

Hormone

Immune approaches (e.g., vaccines)

Intracellular signaling/growth factors

Epigenetic targets

Apoptosis

Targeted cell surface (e.g., antibodies with cytotoxic payloads)

Therapeutic Alliances Series – OncologyJune 6, 2006 - Pg. 23

© Defined Health, 2006

Major Pharma Has a Diversified Approach

IDdb, Adis R&D Insight

Therapeutic Alliances Series – OncologyJune 6, 2006 - Pg. 24

© Defined Health, 2006

Major Pharma Has a Diversified Approach

PharmaProjects, Recap

Therapeutic Alliances Series – OncologyJune 6, 2006 - Pg. 25

© Defined Health, 2006

The Consequences of Complexity

Therapeutic Alliances Series – OncologyJune 6, 2006 - Pg. 26

© Defined Health, 2006

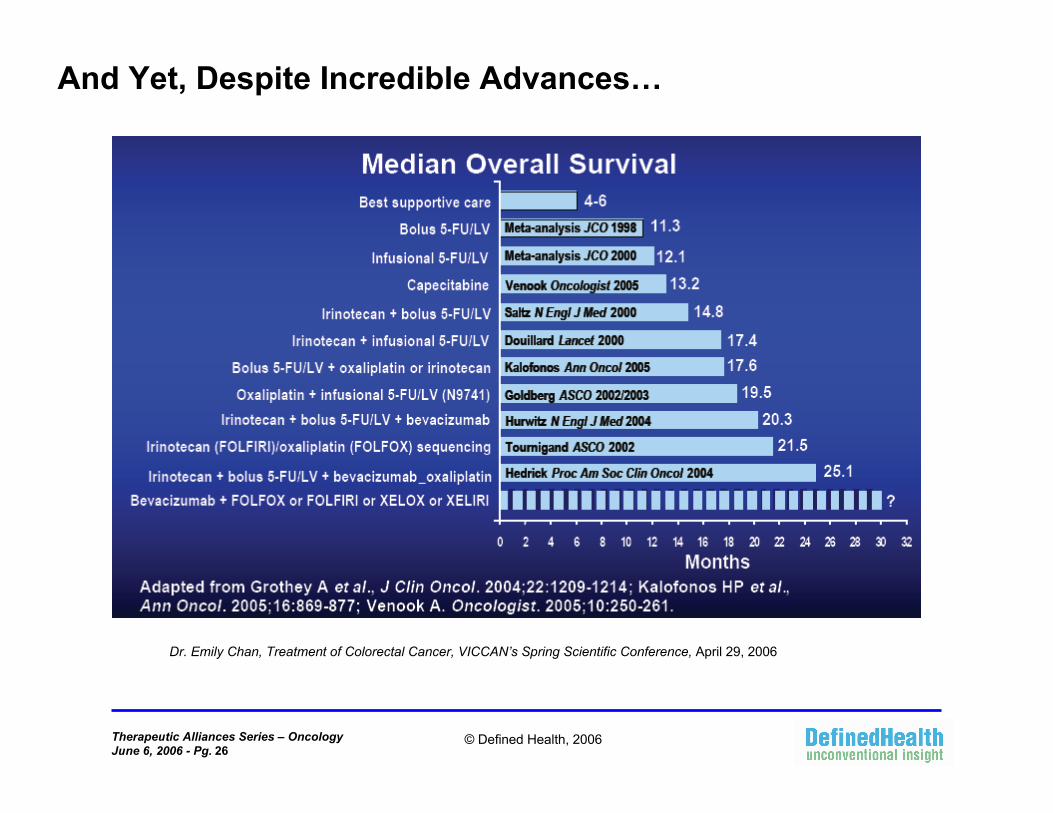

And Yet, Despite Incredible Advances…

Dr. Emily Chan, Treatment of Colorectal Cancer, VICCAN’s Spring Scientific Conference, April 29, 2006

Therapeutic Alliances Series – OncologyJune 6, 2006 - Pg. 27

© Defined Health, 2006

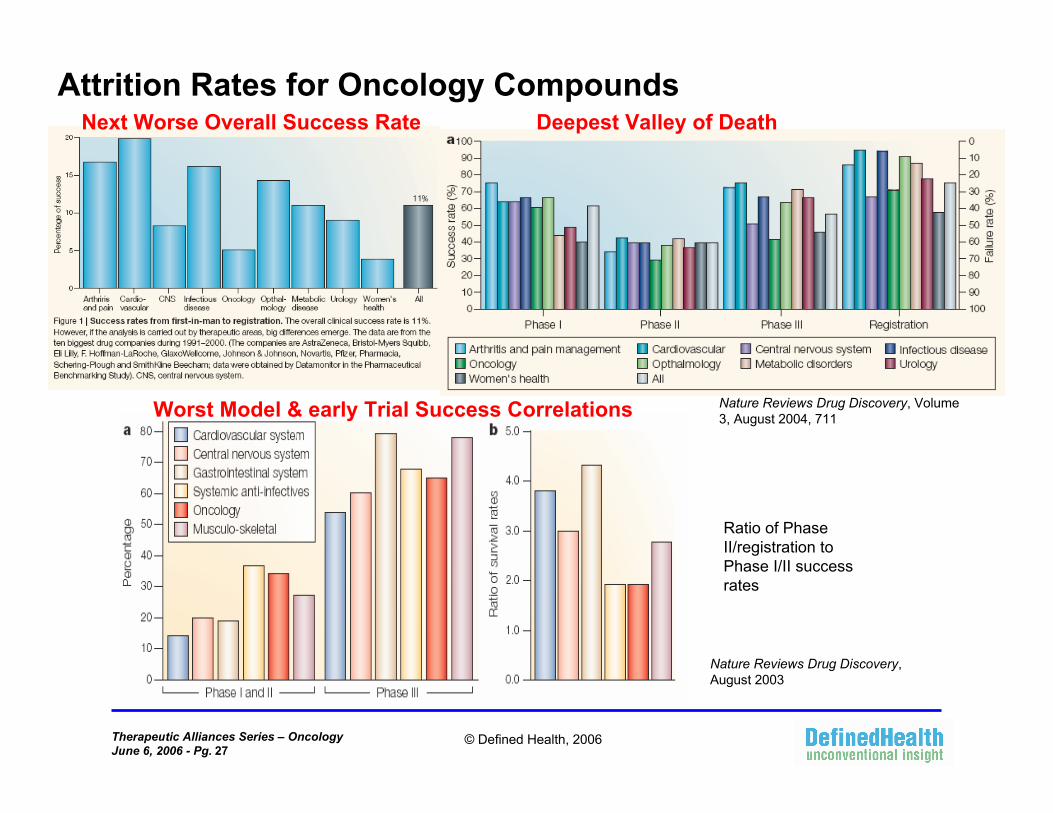

Attrition Rates for Oncology Compounds

Nature Reviews Drug Discovery, Volume 3, August 2004, 711

Nature Reviews Drug Discovery, August 2003

Ratio of Phase II/registration to Phase I/II success rates

Deepest Valley of DeathNext Worse Overall Success Rate

Worst Model & early Trial Success Correlations

Therapeutic Alliances Series – OncologyJune 6, 2006 - Pg. 28

© Defined Health, 2006

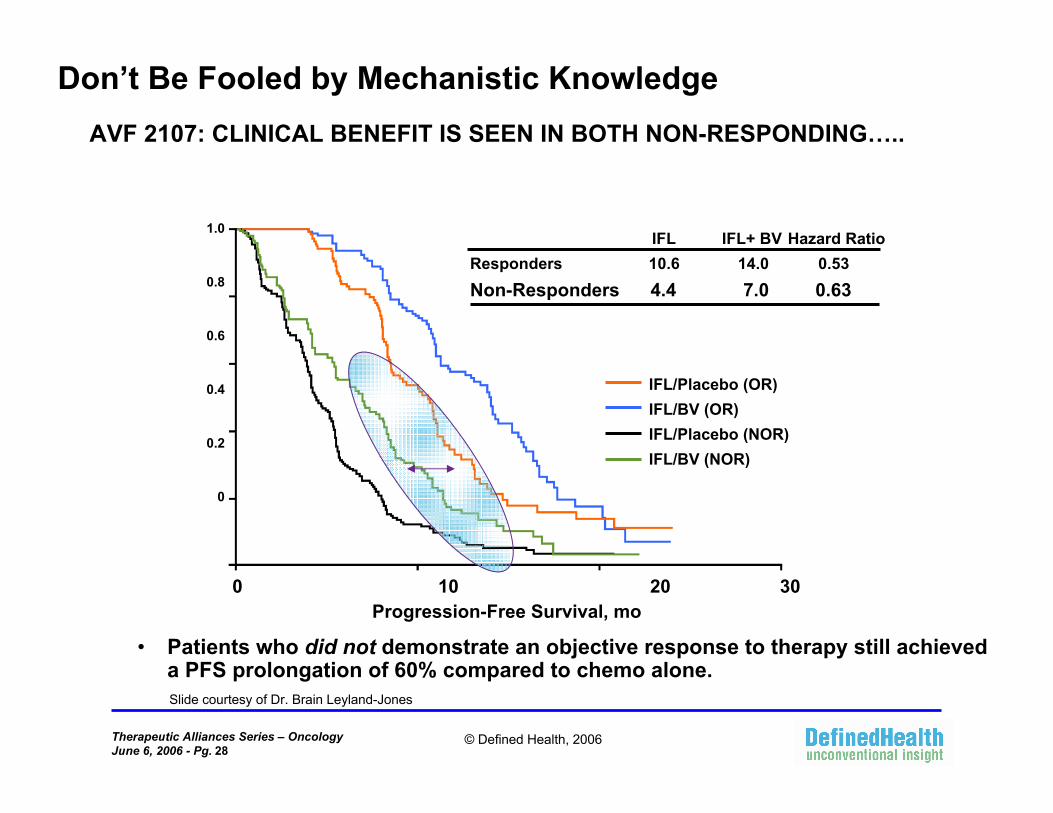

Don’t Be Fooled by Mechanistic Knowledge

IFL IFL+ BV Hazard RatioResponders 10.6 14.0 0.53 Non-Responders 4.4 7.0 0.63

1.0

0.8

0.6

0.4

0.2

0

0 10 20 30Progression-Free Survival, mo

IFL/Placebo (OR)IFL/BV (OR)IFL/Placebo (NOR)IFL/BV (NOR)

• Patients who did not demonstrate an objective response to therapy still achieved a PFS prolongation of 60% compared to chemo alone.

AVF 2107: CLINICAL BENEFIT IS SEEN IN BOTH NON-RESPONDING…..

Slide courtesy of Dr. Brain Leyland-Jones

Therapeutic Alliances Series – OncologyJune 6, 2006 - Pg. 29

© Defined Health, 2006

Deal-Making in Oncology

Therapeutic Alliances Series – OncologyJune 6, 2006 - Pg. 30

© Defined Health, 2006

Deal-making: Trends – 2005-Present

• At least twelve of the deals out of some 33 among major biotech and drug companies over the past year and half have

been for antibodies.

• Targets of interest include apoptosis, and many kinasesincluding PI3K, Akt, and MAPK.

• There have been only a few cytotoxic deals (e.g., Abraxane).

Recap

Therapeutic Alliances Series – OncologyJune 6, 2006 - Pg. 31

© Defined Health, 2006

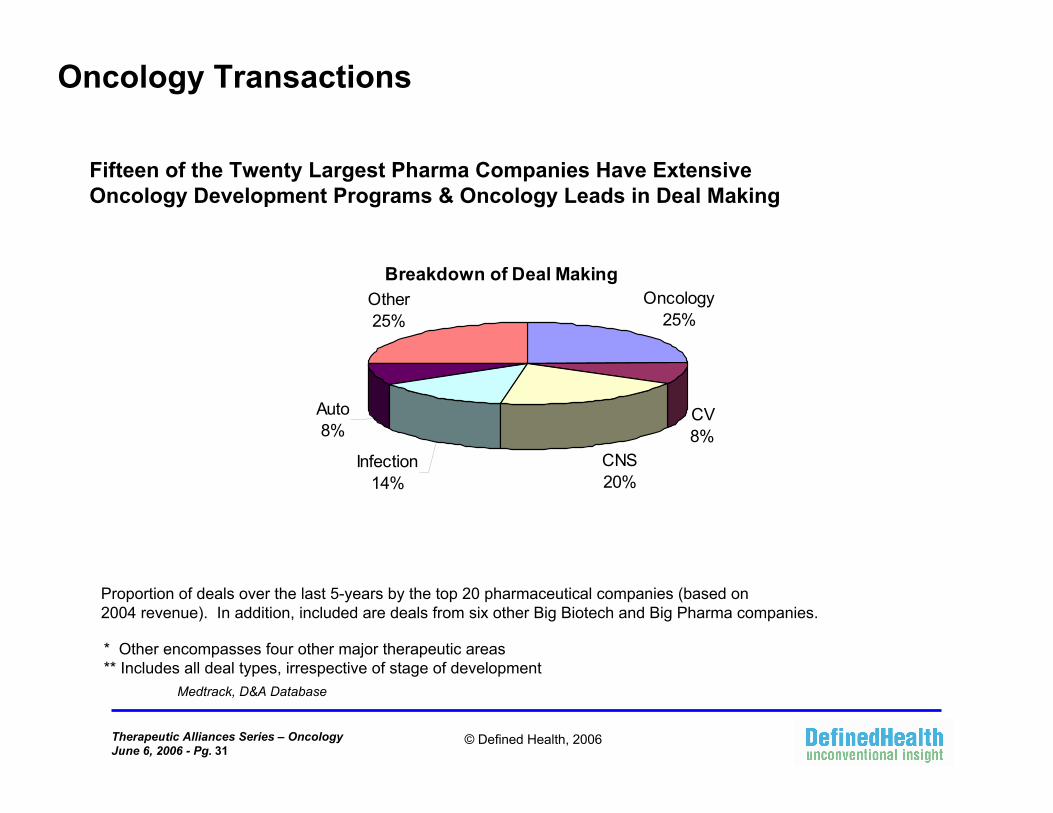

Oncology Transactions

Medtrack, D&A Database

* Other encompasses four other major therapeutic areas** Includes all deal types, irrespective of stage of development

Proportion of deals over the last 5-years by the top 20 pharmaceutical companies (based on2004 revenue). In addition, included are deals from six other Big Biotech and Big Pharma companies.

Breakdown of Deal MakingOncology

25%

CV8%

CNS20%

Infection14%

Auto8%

Other25%

Fifteen of the Twenty Largest Pharma Companies Have Extensive Oncology Development Programs & Oncology Leads in Deal Making

Therapeutic Alliances Series – OncologyJune 6, 2006 - Pg. 32

© Defined Health, 2006

2825 21

20

9

12

4

4

4

514

24

66

214

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2003 2004 2005 2006

Pre-clinical Phase I Phase II Phase III Filed

Comparing Early, Middle and Late-stage Oncology Deal Making(Sample Size = 73 deals)

2006 product deals projected out based on assumption that deal making activity in second half of year equals first half of year. For three of the past four years, early stage (Pre-clinical-Phase I) deals ranged from 70-80% of all deal making activity. Phase II deal making has fluctuated over the past few years and has shown no consistent trend. While Phase III deal making appears to reflect 10% of deal making between 2003-2005, the number of Phase III deals in 2006 appear to be on a downward trend, assuming our assumption for second half '06 holds true.

EvaluatePharma, Defined Health analysis

Trends in Oncology Deal Activity

Extrapolated deals to year end

Therapeutic Alliances Series – OncologyJune 6, 2006 - Pg. 33

© Defined Health, 2006

1317 18

55 6

0%

20%

40%

60%

80%

100%

2003 2004 2005

Phase IIIPhase I/II

Comparing Phase I/II Oncology Deals vs Phase III Deals(Sample Size = 73 deals)

EvaluatePharma, Defined Health analysis

Trends in Oncology Deal Activity

Extrapolated deals to year end

Therapeutic Alliances Series – OncologyJune 6, 2006 - Pg. 34

© Defined Health, 2006

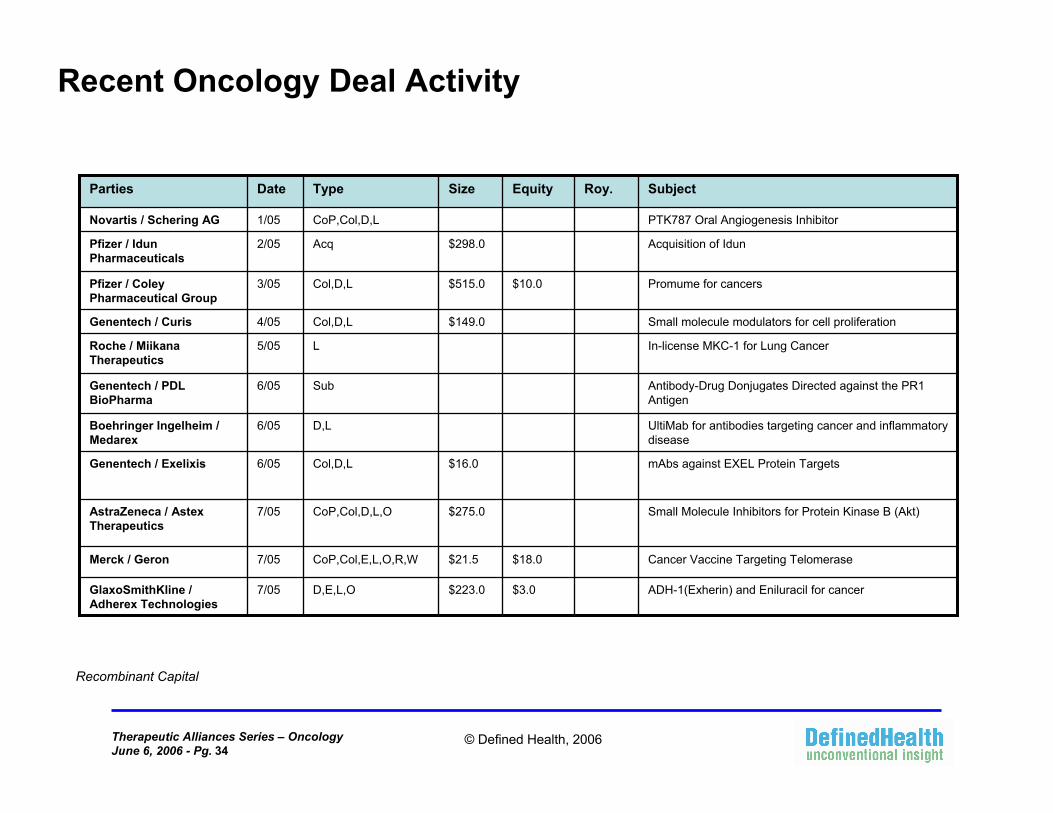

Recent Oncology Deal Activity

Promume for cancers$10.0$515.0Col,D,L3/05Pfizer / Coley Pharmaceutical Group

Cancer Vaccine Targeting Telomerase$18.0$21.5CoP,Col,E,L,O,R,W7/05Merck / Geron

ADH-1(Exherin) and Eniluracil for cancer$3.0$223.0D,E,L,O7/05GlaxoSmithKline / Adherex Technologies

Antibody-Drug Donjugates Directed against the PR1 Antigen

Sub6/05Genentech / PDL BioPharma

In-license MKC-1 for Lung CancerL5/05Roche / MiikanaTherapeutics

Small molecule modulators for cell proliferation$149.0Col,D,L4/05Genentech / Curis

Acquisition of Idun$298.0Acq2/05Pfizer / IdunPharmaceuticals

PTK787 Oral Angiogenesis InhibitorCoP,Col,D,L1/05Novartis / Schering AG

mAbs against EXEL Protein Targets$16.0Col,D,L6/05Genentech / Exelixis

Small Molecule Inhibitors for Protein Kinase B (Akt)$275.0CoP,Col,D,L,O7/05AstraZeneca / AstexTherapeutics

UltiMab for antibodies targeting cancer and inflammatory disease

D,L6/05Boehringer Ingelheim / Medarex

SubjectRoy.EquitySizeTypeDateParties

Recombinant Capital

Therapeutic Alliances Series – OncologyJune 6, 2006 - Pg. 35

© Defined Health, 2006

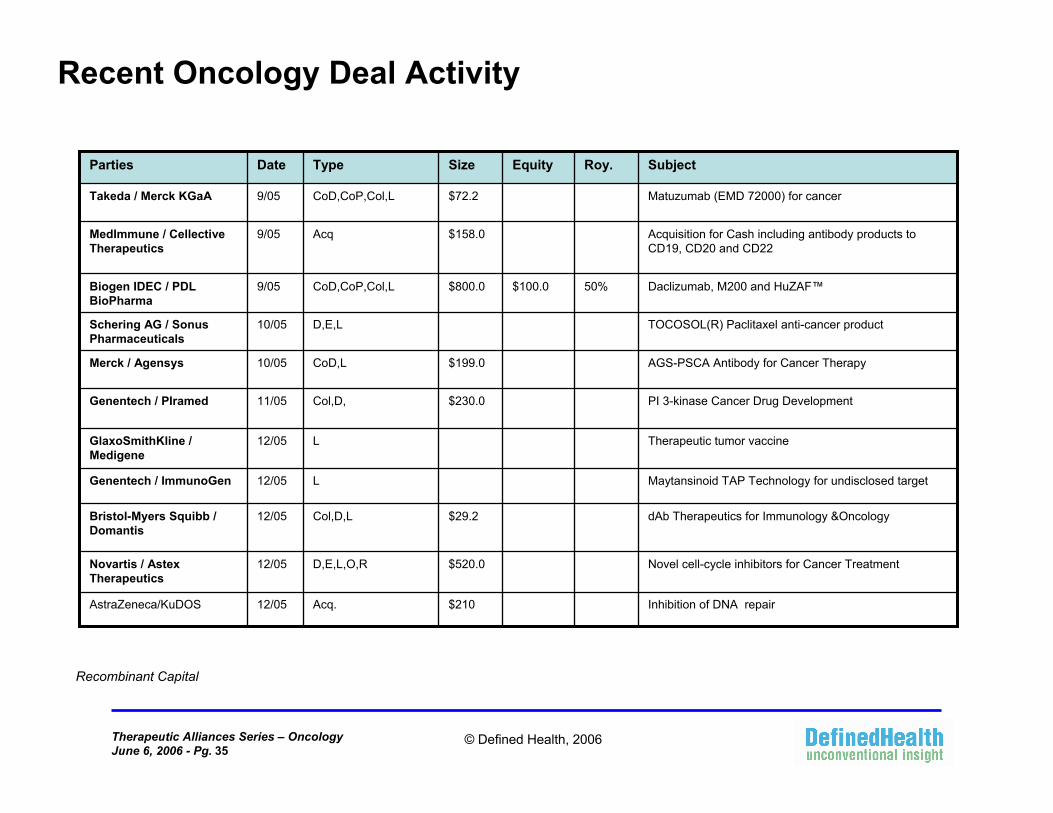

Recent Oncology Deal Activity

Matuzumab (EMD 72000) for cancer$72.2CoD,CoP,Col,L9/05Takeda / Merck KGaA

Acquisition for Cash including antibody products to CD19, CD20 and CD22

$158.0Acq9/05MedImmune / CellectiveTherapeutics

Inhibition of DNA repair$210Acq.12/05AstraZeneca/KuDOS

Novel cell-cycle inhibitors for Cancer Treatment$520.0D,E,L,O,R12/05Novartis / AstexTherapeutics

Therapeutic tumor vaccineL12/05GlaxoSmithKline / Medigene

PI 3-kinase Cancer Drug Development$230.0Col,D,11/05Genentech / PIramed

AGS-PSCA Antibody for Cancer Therapy$199.0CoD,L10/05Merck / Agensys

TOCOSOL(R) Paclitaxel anti-cancer productD,E,L10/05Schering AG / SonusPharmaceuticals

Daclizumab, M200 and HuZAF™50%$100.0$800.0CoD,CoP,Col,L9/05Biogen IDEC / PDL BioPharma

dAb Therapeutics for Immunology &Oncology$29.2Col,D,L12/05Bristol-Myers Squibb / Domantis

Maytansinoid TAP Technology for undisclosed targetL12/05Genentech / ImmunoGen

SubjectRoy.EquitySizeTypeDateParties

Recombinant Capital

Therapeutic Alliances Series – OncologyJune 6, 2006 - Pg. 36

© Defined Health, 2006

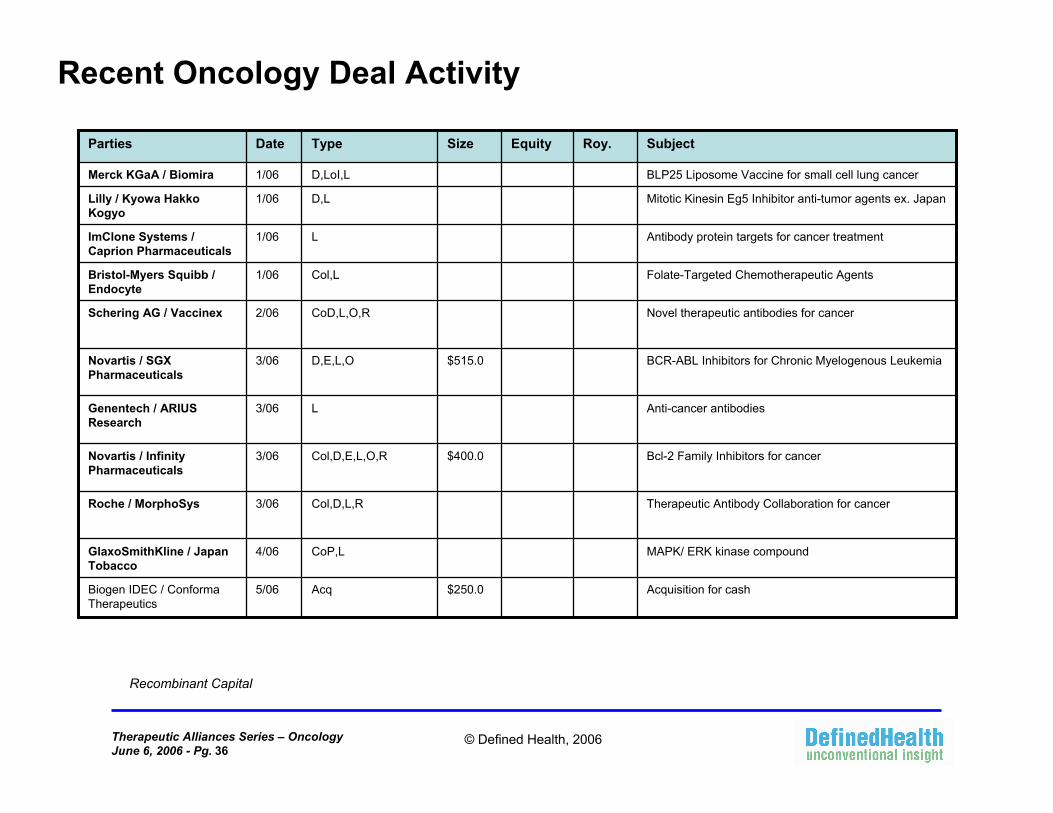

Recent Oncology Deal Activity

BLP25 Liposome Vaccine for small cell lung cancerD,LoI,L1/06Merck KGaA / Biomira

Mitotic Kinesin Eg5 Inhibitor anti-tumor agents ex. JapanD,L1/06Lilly / Kyowa Hakko Kogyo

Antibody protein targets for cancer treatmentL1/06ImClone Systems / Caprion Pharmaceuticals

Folate-Targeted Chemotherapeutic AgentsCol,L1/06Bristol-Myers Squibb / Endocyte

Novel therapeutic antibodies for cancerCoD,L,O,R2/06Schering AG / Vaccinex

BCR-ABL Inhibitors for Chronic Myelogenous Leukemia$515.0D,E,L,O3/06Novartis / SGX Pharmaceuticals

Anti-cancer antibodiesL3/06Genentech / ARIUS Research

Bcl-2 Family Inhibitors for cancer$400.0Col,D,E,L,O,R3/06Novartis / Infinity Pharmaceuticals

Therapeutic Antibody Collaboration for cancerCol,D,L,R3/06Roche / MorphoSys

Acquisition for cash$250.0Acq5/06Biogen IDEC / ConformaTherapeutics

MAPK/ ERK kinase compoundCoP,L4/06GlaxoSmithKline / Japan Tobacco

SubjectRoy.EquitySizeTypeDateParties

Recombinant Capital

Therapeutic Alliances Series – OncologyJune 6, 2006 - Pg. 37

© Defined Health, 2006

Portfolios, Franchises and the Idiosyncrasies of Risk-Reward

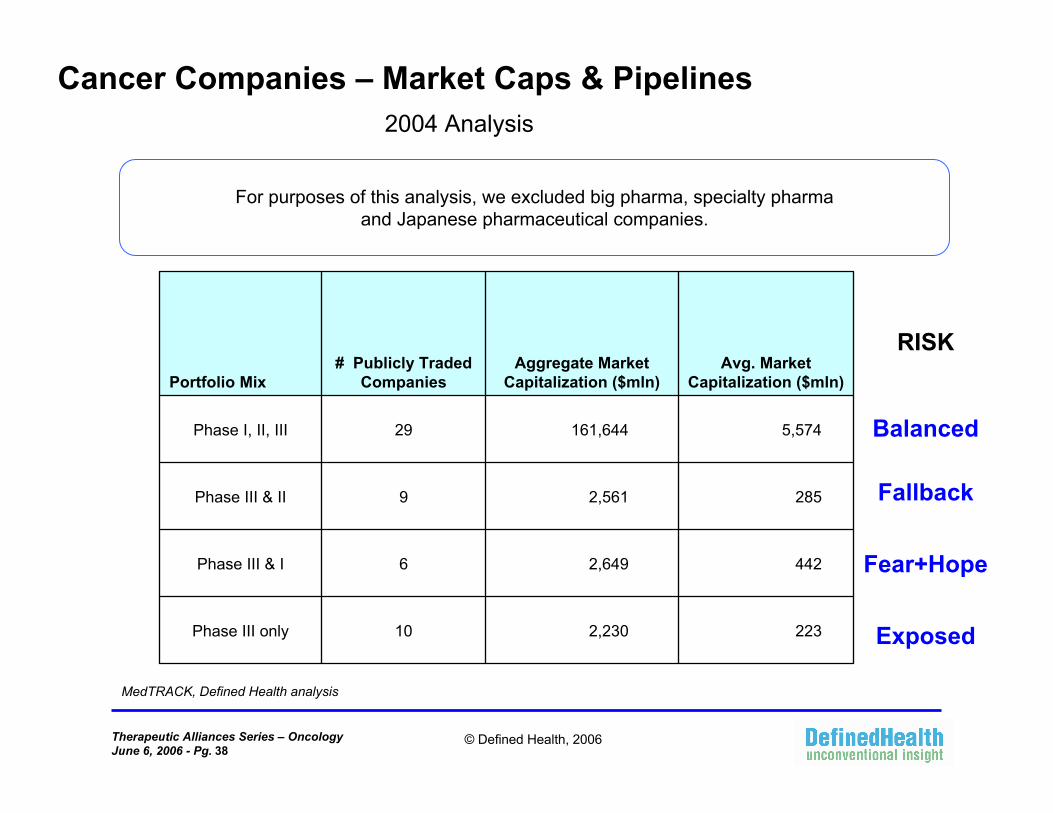

Therapeutic Alliances Series – OncologyJune 6, 2006 - Pg. 38

© Defined Health, 2006

Cancer Companies – Market Caps & Pipelines

223 2,230 10Phase III only

442 2,649 6Phase III & I

285 2,561 9Phase III & II

5,574 161,644 29Phase I, II, III

Avg. Market Capitalization ($mln)

Aggregate Market Capitalization ($mln)

# Publicly Traded CompaniesPortfolio Mix

MedTRACK, Defined Health analysis

For purposes of this analysis, we excluded big pharma, specialty pharma and Japanese pharmaceutical companies.

Balanced

RISK

Exposed

Fear+Hope

Fallback

2004 Analysis

Therapeutic Alliances Series – OncologyJune 6, 2006 - Pg. 39

© Defined Health, 2006

Cancer Companies – Market Caps & Pipelines

MedTRACK, Defined Health analysis

Balanced

RISK

Exposed

Fear+Hope

Fallback

For purposes of this analysis, we excluded big pharma and big biotech, specialty pharma and Japanese pharmaceutical companies.

223 2,230 10Phase III only

442 2,649 6Phase III & I

285 2,561 9Phase III & II

806 20,957 26Phase I, II, III

Avg. Market Capitalization ($mln)

Aggregate Market Capitalization ($mln)

# Publicly Traded

CompaniesPortfolio Mix

2004 Analysis

Therapeutic Alliances Series – OncologyJune 6, 2006 - Pg. 40

© Defined Health, 2006

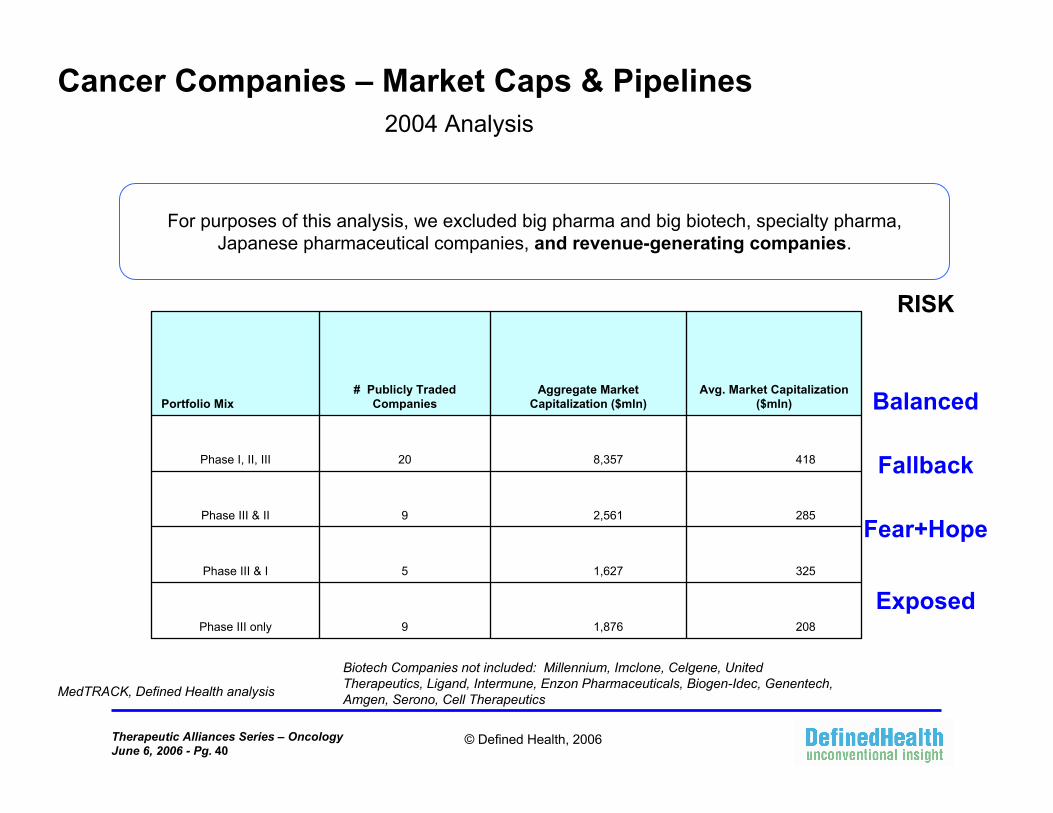

Cancer Companies – Market Caps & Pipelines

For purposes of this analysis, we excluded big pharma and big biotech, specialty pharma, Japanese pharmaceutical companies, and revenue-generating companies.

Biotech Companies not included: Millennium, Imclone, Celgene, United Therapeutics, Ligand, Intermune, Enzon Pharmaceuticals, Biogen-Idec, Genentech, Amgen, Serono, Cell Therapeutics

208 1,876 9Phase III only

325 1,627 5Phase III & I

285 2,561 9Phase III & II

418 8,357 20Phase I, II, III

Avg. Market Capitalization ($mln)

Aggregate Market Capitalization ($mln)

# Publicly Traded CompaniesPortfolio Mix Balanced

RISK

Exposed

Fear+Hope

Fallback

MedTRACK, Defined Health analysis

2004 Analysis

Therapeutic Alliances Series – OncologyJune 6, 2006 - Pg. 41

© Defined Health, 2006

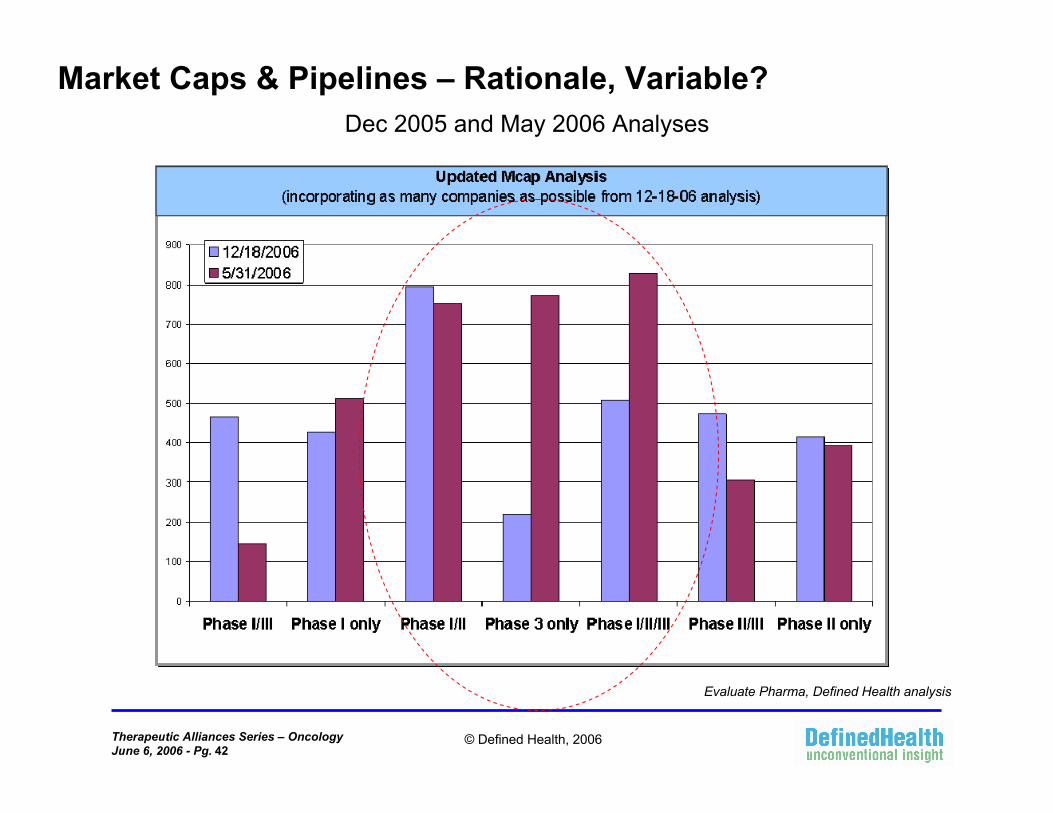

Market Caps & Pipelines – Rationale, Variable?

May 2006 Criteria:<$50M in 2005 Revenue (all sources)67% of R&D projects in Oncology

Initial Criteria 2005: <$100M in 2005 Revenue (all sources)50% of R&D projects in Oncology

Dec 2005 and May 2006 Analyses

Evaluate Pharma, Defined Health analysis

Therapeutic Alliances Series – OncologyJune 6, 2006 - Pg. 42

© Defined Health, 2006

Market Caps & Pipelines – Rationale, Variable?Dec 2005 and May 2006 Analyses

Evaluate Pharma, Defined Health analysis

Therapeutic Alliances Series – OncologyJune 6, 2006 - Pg. 43

© Defined Health, 2006

Market Caps & Pipelines – Rationale, Variable?

Evaluate Pharma, Defined Health analysis

Therapeutic Alliances Series – OncologyJune 6, 2006 - Pg. 44

© Defined Health, 2006

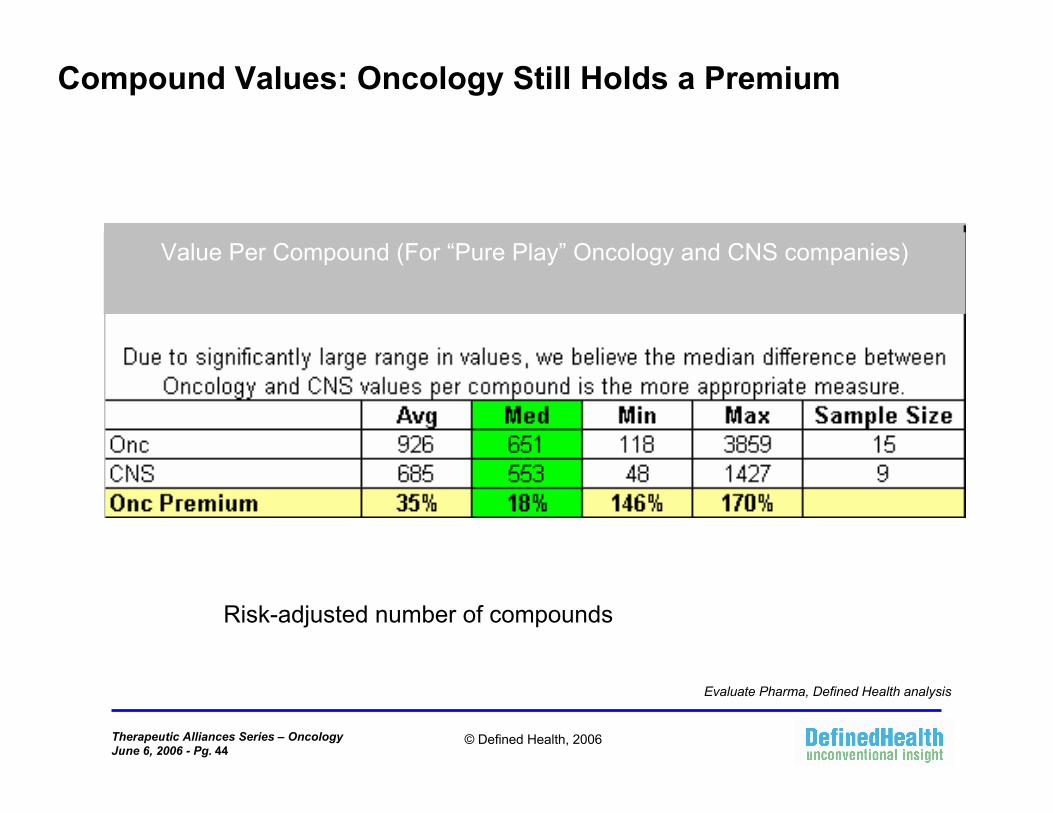

Compound Values: Oncology Still Holds a Premium

Value Per Compound (For “Pure Play” Oncology and CNS companies)

Risk-adjusted number of compounds

Evaluate Pharma, Defined Health analysis

Therapeutic Alliances Series – OncologyJune 6, 2006 - Pg. 45

© Defined Health, 2006

Franchise Building - Merck

Merck

Rigel– (Nov. 2004)•Investigate ubiquitin ligasesto find treatments for cancer

•Rigel to receive initial cash payment and funding for Rigel

research scientists for 2.5 years

Pierre Fabre Medicament (August 2004)•License for antibody in preclinical development, which targets insulin like

growth factor (IGF-1)•Financial terms not

disclosedVertex– (June 2004)•Collaboration -- VX-680, Vertex's

lead Aurora kinase inhibitor•$20 million up-front payment;

$14M R&D funding; $130M milestone for successful

development in first oncology indication; $220M follow-on or

development in other indications

Aton Pharma (Feb. 2004)•Acquisition of oncology

focused Biotech•Target’s pipeline includes

HDAC inhibitors; lead product candidate in phase

II•Financial terms not

disclosed

Recap

Agensys (October 2005)•PSCA antibody for prostate,

pancreatic and bladder cancers•Global alliance to jointly

develop and commercialize AGS-PSCA, Agensys' fully

human monoclonal antibody (MAb) to Prostate Stem Cell

Antigen (PSCA)•$199M

Geron– (July 2005)•Jointly potential vaccine against

telomerase using Merck's platform.

•Geron will continue development of its dendritic cell-based vaccine

product, which is currently in Phase I/II clinical trials and is the

subject of the exclusive option obtained by Merck

•$21.5M upfront, $18M equity

Therapeutic Alliances Series – OncologyJune 6, 2006 - Pg. 46

© Defined Health, 2006

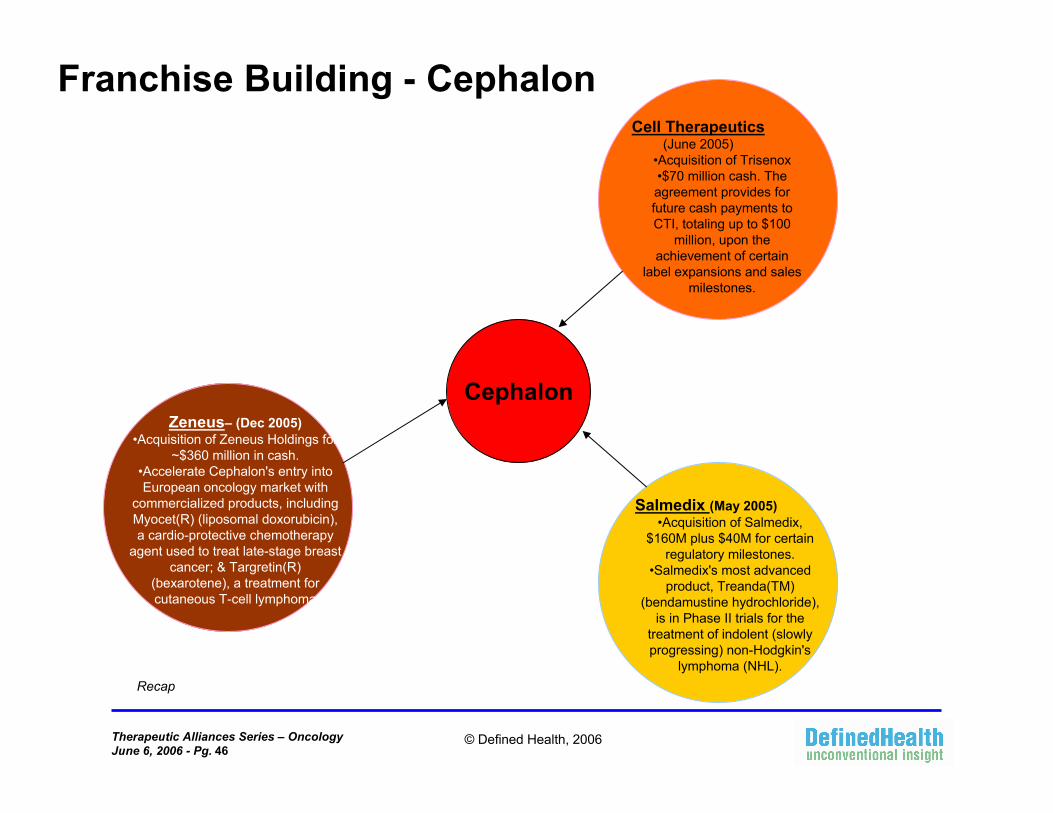

Franchise Building - Cephalon

Cephalon

Salmedix (May 2005)•Acquisition of Salmedix,

$160M plus $40M for certain regulatory milestones.

•Salmedix's most advanced product, Treanda(TM)

(bendamustine hydrochloride), is in Phase II trials for the

treatment of indolent (slowly progressing) non-Hodgkin's

lymphoma (NHL).

Zeneus– (Dec 2005)•Acquisition of Zeneus Holdings for

~$360 million in cash. •Accelerate Cephalon's entry into European oncology market with

commercialized products, including Myocet(R) (liposomal doxorubicin), a cardio-protective chemotherapy

agent used to treat late-stage breast cancer; & Targretin(R)

(bexarotene), a treatment for cutaneous T-cell lymphoma

Cell Therapeutics (June 2005)

•Acquisition of Trisenox•$70 million cash. The agreement provides for future cash payments to CTI, totaling up to $100

million, upon the achievement of certain

label expansions and sales milestones.

Recap

Therapeutic Alliances Series – OncologyJune 6, 2006 - Pg. 47

© Defined Health, 2006

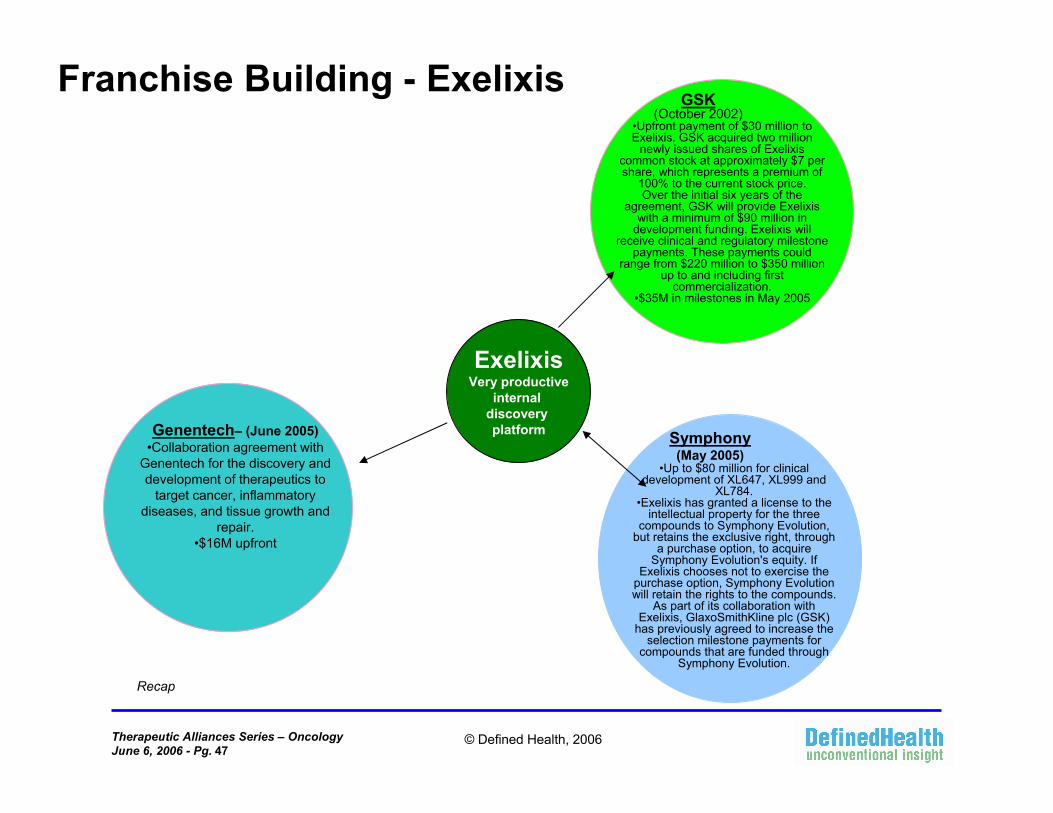

Franchise Building - Exelixis

ExelixisVery productive

internal discovery platform Symphony

(May 2005)•Up to $80 million for clinical

development of XL647, XL999 and XL784.

•Exelixis has granted a license to the intellectual property for the three

compounds to Symphony Evolution, but retains the exclusive right, through

a purchase option, to acquire Symphony Evolution's equity. If

Exelixis chooses not to exercise the purchase option, Symphony Evolution will retain the rights to the compounds.

As part of its collaboration with Exelixis, GlaxoSmithKline plc (GSK)

has previously agreed to increase the selection milestone payments for

compounds that are funded through Symphony Evolution.

Genentech– (June 2005)•Collaboration agreement with

Genentech for the discovery and development of therapeutics to

target cancer, inflammatory diseases, and tissue growth and

repair. •$16M upfront

GSK (October 2002)

•Upfront payment of $30 million to Exelixis. GSK acquired two million

newly issued shares of Exelixiscommon stock at approximately $7 per share, which represents a premium of

100% to the current stock price. Over the initial six years of the

agreement, GSK will provide Exelixiswith a minimum of $90 million in

development funding. Exelixis will receive clinical and regulatory milestone

payments. These payments could range from $220 million to $350 million

up to and including first commercialization.

•$35M in milestones in May 2005

Recap

Therapeutic Alliances Series – OncologyJune 6, 2006 - Pg. 48

© Defined Health, 2006

Franchises In Oncology• Except for Genentech, no

company appears more than twice in the 2010 consensus analyst blockbuster list of billion dollar plus therapeuticoncology drugs.

Celgene1.5Revlimid

Lilly1.4Alimta

AstraZeneca1.4Arimidex

Genentech/Roche1.3Tarceva

Novartis1.3Femara

Lilly1.7Gemzar

Roche*1.32Xeloda

Genentech/Roche7.6Avastin

AstraZeneca1.1Zoladex

BMS/Merck KGAa2.0Erbitux

sanofi-aventis2.4Taxotere

sanofi-aventis2.5Eloxatin

J&J2.5Procrit

Amgen2.9Epogen

Novartis3.7Gleevec

Amgen3.9Neulasta

Genentech/Roche4.0Herceptin

Amgen5.2Aranesp

Genentech/Roche5.5Rituxan

CompanyWW Sales ($B)Drug Name

Evaluate Pharma

Therapeutic Alliances Series – OncologyJune 6, 2006 - Pg. 49

© Defined Health, 2006

Distribution of Past and Projected Peak SalesPeak sales by type of product - Products launched as of 2004 - Data from 1986 to 2009.

0

2

4

6

8

10

12

14

16

18

0-10

0

100-

200

200-

300

300-

400

400-

500

500-

600

600-

700

700-

800

800-

900

900-

1000

Mor

e th

an 1

000

Peak sales in $m

# of

pro

duct

s

Organic

External

Evaluate Pharma, Defined Health analysis

Therapeutic Alliances Series – OncologyJune 6, 2006 - Pg. 50

© Defined Health, 2006

Final Thoughts, Questions Remaining

Therapeutic Alliances Series – OncologyJune 6, 2006 - Pg. 51

© Defined Health, 2006

The Oft Asked Question: Is Cancer Different?

• One of the few, if not only, therapeutic categories that will experience not simply incremental growth but exponential, innovative growth in the next ten years.

• A category in which to date a limited number of drugs have obtained significant blockbuster status (therapeutic oncology) compared to many other TAs.

• A therapeutic category in which significant clinical benefit has been made but in which the standard of care remains suboptimal in nearly all settings.

• Oncology is perhaps unique in having the most detailed molecular data available and yet still having only incremental insight into the proper usage of regimens containing available and development stage agents.

• Oncology is one of the most difficult categories for design of clinical trials and endpoints.

• One of the therapeutic categories with the highest clinical development stage risk (failure rates at Phase II and Phase III).

• Cancer will therefore be one of the leading categories to be impacted by pharmacogenomics/personalized medicine.

• Oncology is a key area where portfolio diversity has never really been translated into commensurate commercial value and yet the potential for franchise synergies is enormous (with some notable exceptions, such as Genentech).

• Cancer is where everyone, large and small companies alike, biotech, pharma and specialty, want to play.

Therapeutic Alliances Series – OncologyJune 6, 2006 - Pg. 52

© Defined Health, 2006

Questions/Issues Going Forward

• Some questions just don’t reduce to a simplistic formula, like those pertaining to partnering and diversifying a portfolio:

– What?– When?– How?– How much?

• But this much is certain: – Be open, be creative, be proactive, be informed– And, while a level of passion and commitment to the programs are essential to

move them forward in a small company, don’t drink the:

Therapeutic Alliances Series – OncologyJune 6, 2006 - Pg. 53

© Defined Health, 2006

Acknowledgements

• Jason Gerberry, JD, MBA, Consultant, Defined Health