Building a greener society Who are we and what do we do? Self-build mortgages Pricing for...

19

Building a greener society • Who are we and what do we do? • Self-build mortgages • Pricing for environmental excellence • A few tips Jon Lee, Business Development Manager

-

Upload

thomasine-dean -

Category

Documents

-

view

215 -

download

0

Transcript of Building a greener society Who are we and what do we do? Self-build mortgages Pricing for...

Building a greener society

• Who are we and what do we do?

• Self-build mortgages

• Pricing for environmental excellence

• A few tips

Jon Lee, Business Development Manager

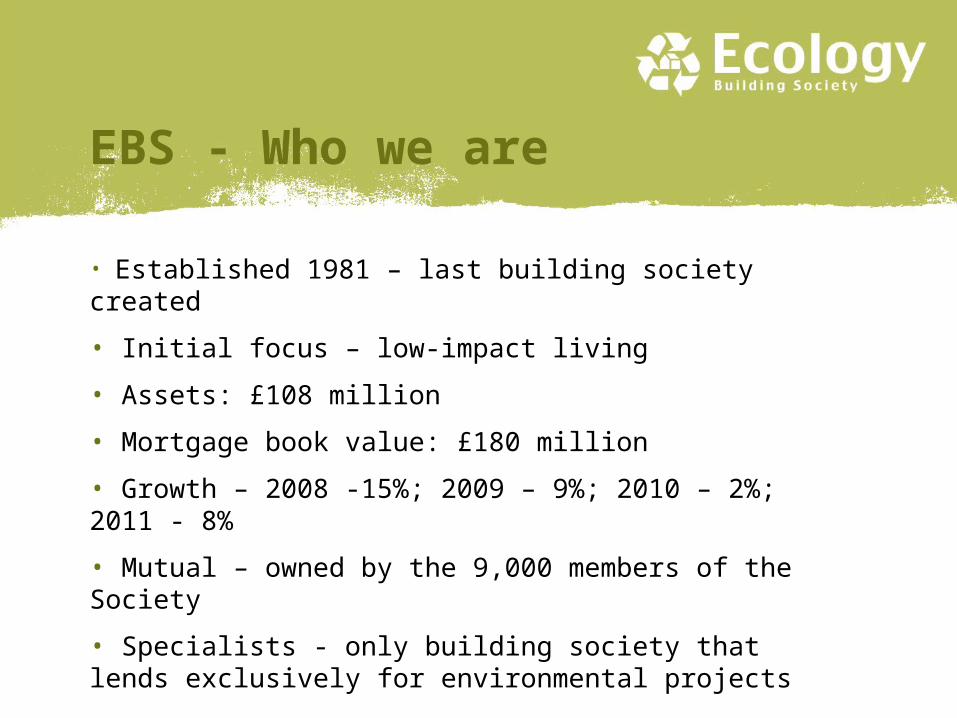

EBS - Who we are

• Established 1981 – last building society created

• Initial focus – low-impact living

• Assets: £108 million

• Mortgage book value: £180 million

• Growth – 2008 -15%; 2009 – 9%; 2010 – 2%; 2011 - 8%

• Mutual – owned by the 9,000 members of the Society

• Specialists - only building society that lends exclusively for environmental projects

The perception

The reality?

About our mortgages

• We fund eco new builds (including self-build), conversions, renovations and energy efficiency improvements

• We also support housing cooperatives, CLTs, Cohousing, community ownership, eco businesses, organic smallholdings and small woodlands

• Our C-Change mortgage discounts reward energy efficient properties and sustainable home improvements

• We offer long-term value through low fees, transparent pricing and customer service direct from our HQ

• Current Standard Variable Rate is 4.90%

Ecology view of self-build

• Tackling climate change and the environmental imperative through creation of sustainable housing stock

• Alignment of pricing with climate change risk

• Ecology BS recognised as kick-starting the market for self-build

• Buildstore, Kevin McCloud, Green Building Store

• Our role has been to act to support self-build pioneers

• Self/custom-build has been a test-bed for new ideas in a conservative industry

• Self-build approaches tend to quality and enhance security

Self-build mortgages

• Ability to lend for purchase of land with planning consents

• Self-build does not necessarily mean DIY• Stage payments available benchmarked against the

increasing value of the plot / site• Discounts for ecological and energy efficient homes

on completion for the remainder of the mortgage• “Affinity” mortgage schemes available to members,

including bridging facilities where applicable• Development finance for groups available

Ecology lending model

• Individual approach – close dialogue with borrower

• Self-build, custom-build, co-housing, MHO model

• Loan to value – up to 90% at any stage of the project, including purchase of land

• No set stage payments – drawdown profile is agreed with borrower

• No Mortgage Indemnity Guarantee (MIG) required

• No differentiation on rates from our other lending

• C-Change discount options – for the life of the mortgage

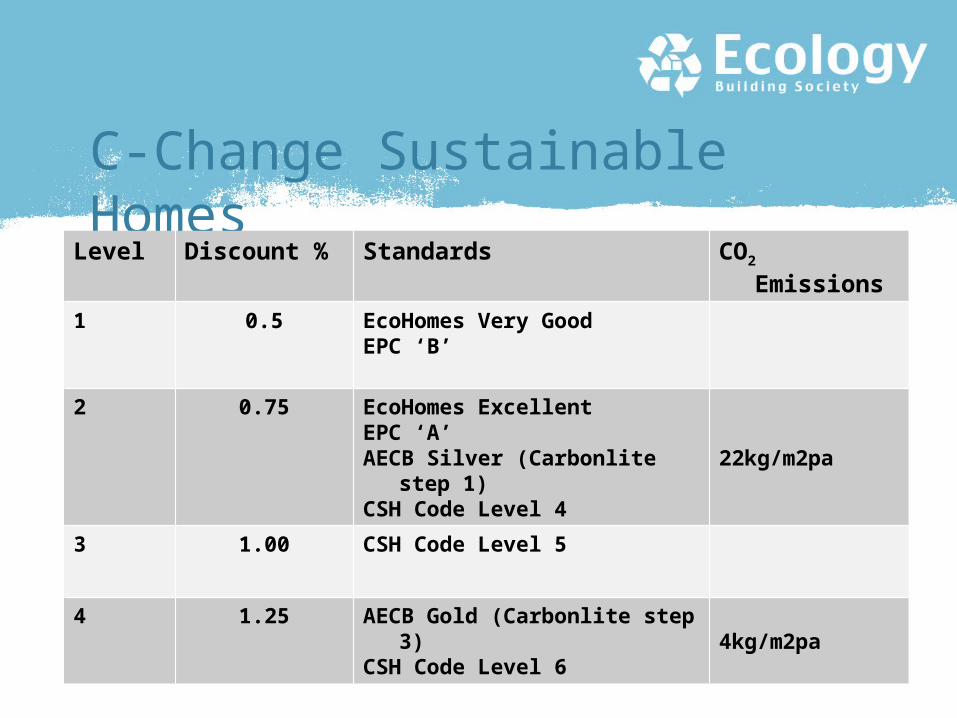

C-Change Sustainable Homes

Level Discount % Standards CO2 Emissions

1 0.5 EcoHomes Very GoodEPC ‘B’

2 0.75 EcoHomes Excellent EPC ‘A’AECB Silver (Carbonlite step 1)CSH Code Level 4

22kg/m2pa

3 1.00 CSH Code Level 5

4 1.25 AECB Gold (Carbonlite step 3)CSH Code Level 6 4kg/m2pa

CSH Level 6 – shared ownership

Community Land Trust

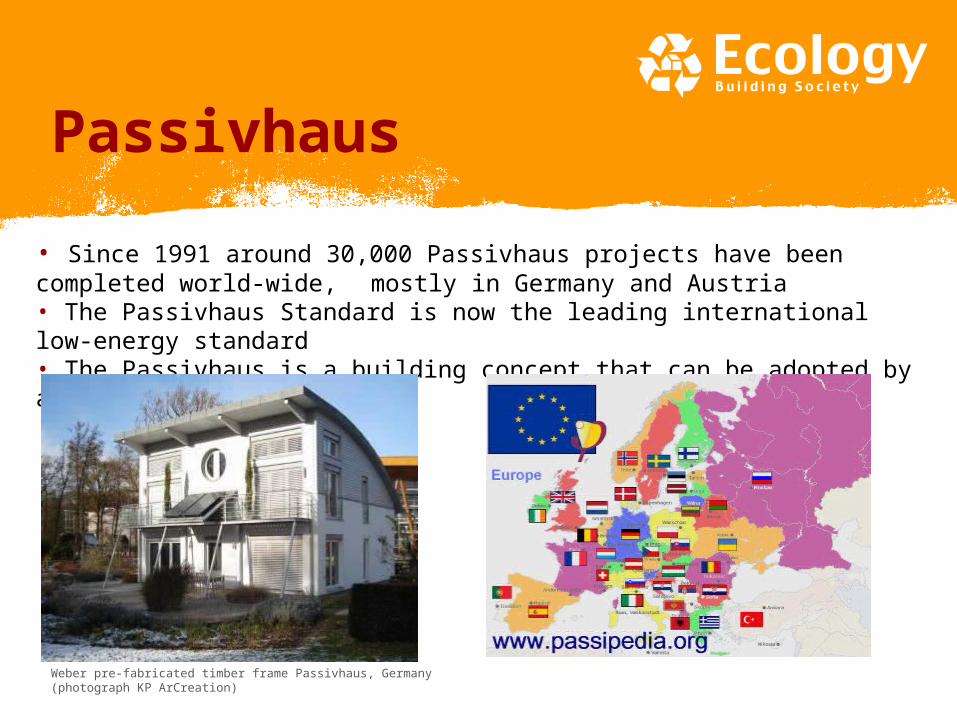

• Since 1991 around 30,000 Passivhaus projects have been completed world-wide, mostly in Germany and Austria

• The Passivhaus Standard is now the leading international low-energy standard• The Passivhaus is a building concept that can be adopted by anyone!

Weber pre-fabricated timber frame Passivhaus, Germany (photograph KP ArCreation)

Passivhaus

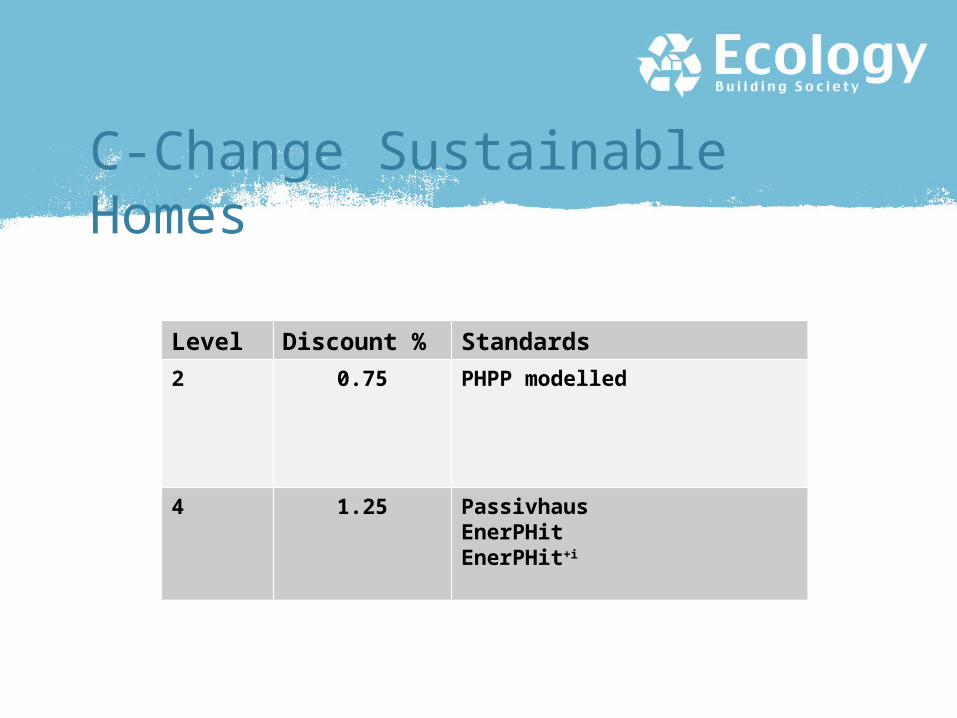

C-Change Sustainable Homes

Level Discount % Standards

2 0.75 PHPP modelled

4 1.25 PassivhausEnerPHitEnerPHit+i

Passivhaus Cohousing - Lancaster

The evidence….

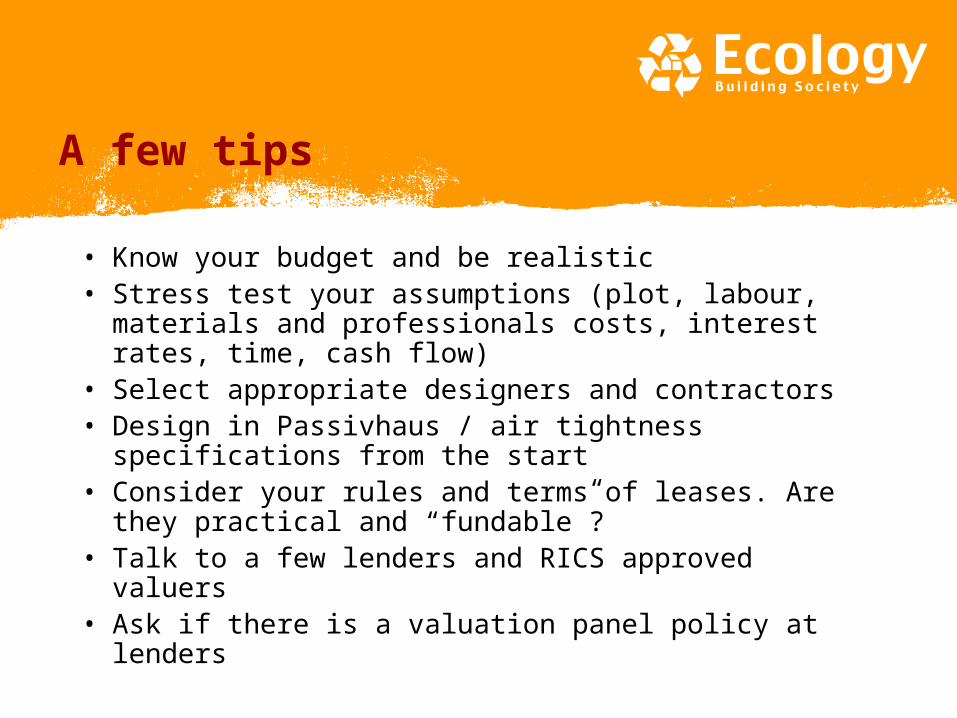

A few tips

• Know your budget and be realistic• Stress test your assumptions (plot, labour, materials

and professionals costs, interest rates, time, cash flow)

• Select appropriate designers and contractors• Design in Passivhaus / air tightness specifications

from the start• Consider your rules and terms of leases. Are they

practical and “fundable”?• Talk to a few lenders and RICS approved valuers• Ask if there is a valuation panel policy at lenders

A few tips

•Check Loan to Value ratios and how draw downs are signed off

•Have a robust project cash flow model including contingencies

•If a self build for your own residence, be aware of income multiples and do not assume any projected income will be included by your lender

•Be aware that project spend and sweat equity does not equate to increases in interim values on the project

•Above all, choose partners that understand what you are trying to achieve and don’t look at you like you have three heads!

Thanks for listening!

• Any questions?

• Jon Lee, 01535 650774

• www.ecology.co.uk