Build Wealth, Not Debt Strategies for helping clients out of poverty.

30

Build Wealth, Not Debt Strategies for helping clients out of poverty

-

Upload

noel-oneal -

Category

Documents

-

view

215 -

download

0

Transcript of Build Wealth, Not Debt Strategies for helping clients out of poverty.

Build Wealth, Not Debt

Strategies for helping clients out of poverty

How wealthy are you?

Let’s calculate your net worth:

(Total the value of your assets)

- (Total your liabilities)

___________________________

= Your Net Worth

Asset Poverty

Asset poverty is defined as a household without a sufficient net worth to subsist at the poverty level for 3 months.

A crisis pushes these households into poverty or homelessness.

If your client’s income was disrupted, would your client be able to live at poverty

level for three months?

2008 Federal Poverty Guidelines (FPL)

Family Size Annual Income Monthly Income 3 months’ FPL income

One $10,400 $867 $2601

Two $14,000 $1167 $3501

Three $17,600 $1467 $4401

Four $21,200 $1767 $5301

Five $24,800 $2067 $6201

If your income was disrupted, would you be able to live at poverty level

for three months?

2008 Federal Poverty Guidelines (FPL)

Family Size Annual Income Monthly Income 3 months’ FPL income

One $10,400 $867 $2601

Two $14,000 $1167 $3501

Three $17,600 $1467 $4401

Four $21,200 $1767 $5301

Five $24,800 $2067 $6201

How do we build wealth?

Five steps:

1. Write down your goal.

2. Pay bills on time.

3. Pay necessary living expenses first.

4. Set aside money for emergencies.

5. Save for your goal.

How do we build wealth?

Five steps:

1. Write down your goal.

2. Pay bills on time.

3. Pay necessary living expenses first.

4. Set aside money for emergencies.

5. Save for your goal.

Write down your goal.

My goal is:

The cost will be:

I will complete my goal by:

I will save $______ each week (or month) to reach my goal.

Study of Harvard MBA students

Students were asked: “Have you set clear, written goals for the future and made plans to accomplish them?”

Only 3% had written goals and plans. Ten years later, the class members were interviewed again. The 3% that had clear, written goals were earning, on average, ten times as much as the other 97% put together.

From What They Don’t Teach You in the Harvard Business School by Mark McCormack.

How do we build wealth?

Five steps:

1. Write down your goal.

2. Pay bills on time.

3. Pay necessary living expenses first.

4. Set aside money for emergencies.

5. Save for your goal.

Pay bills on time.

One-third of your credit score is based on your bill payment history.

Your credit report affects your employment, housing, utilities, insurance, transportation, and loans.

Understand your credit report.

Ability to get utilities

Cost of loans and insurance

Homeownership

Job prospects and promotion

Credit report

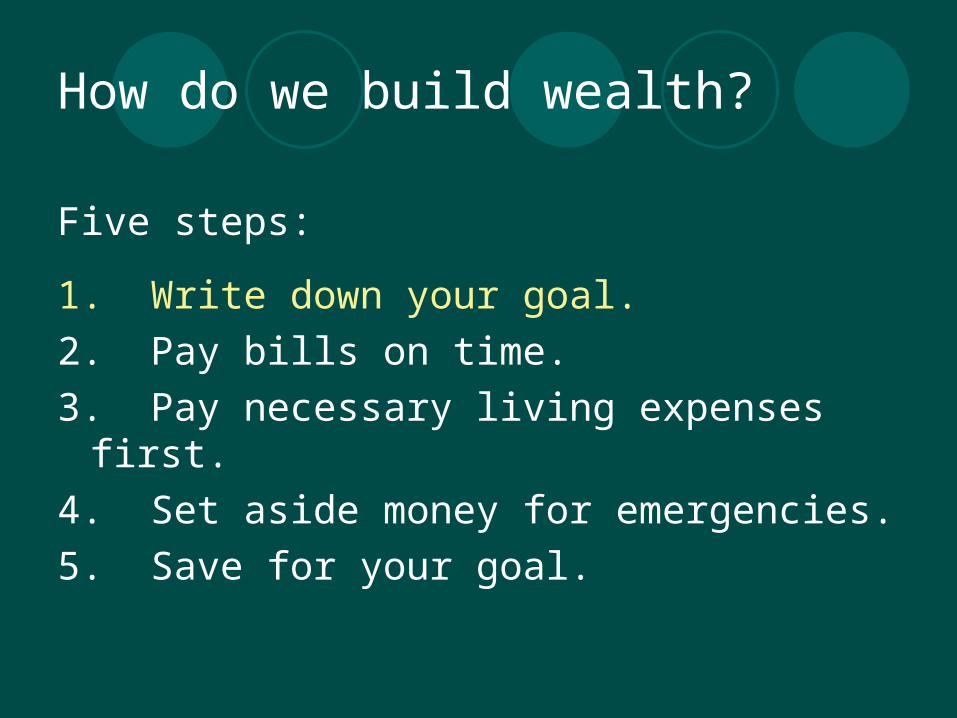

What happens if you fail to pay on time?

Credit score drops.

Loans becomemore expensive.

Late payment because payment is unaffordable.

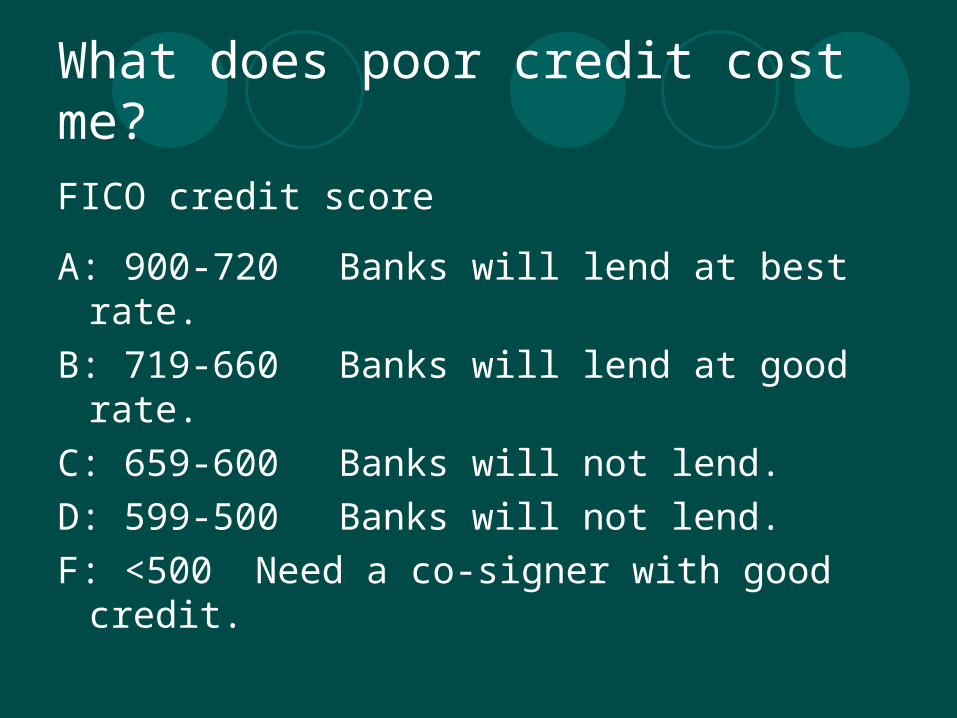

What does poor credit cost me?

FICO credit score

A: 900-720 Banks will lend at best rate.

B: 719-660 Banks will lend at good rate.

C: 659-600 Banks will not lend.

D: 599-500 Banks will not lend.

F: <500 Need a co-signer with good credit.

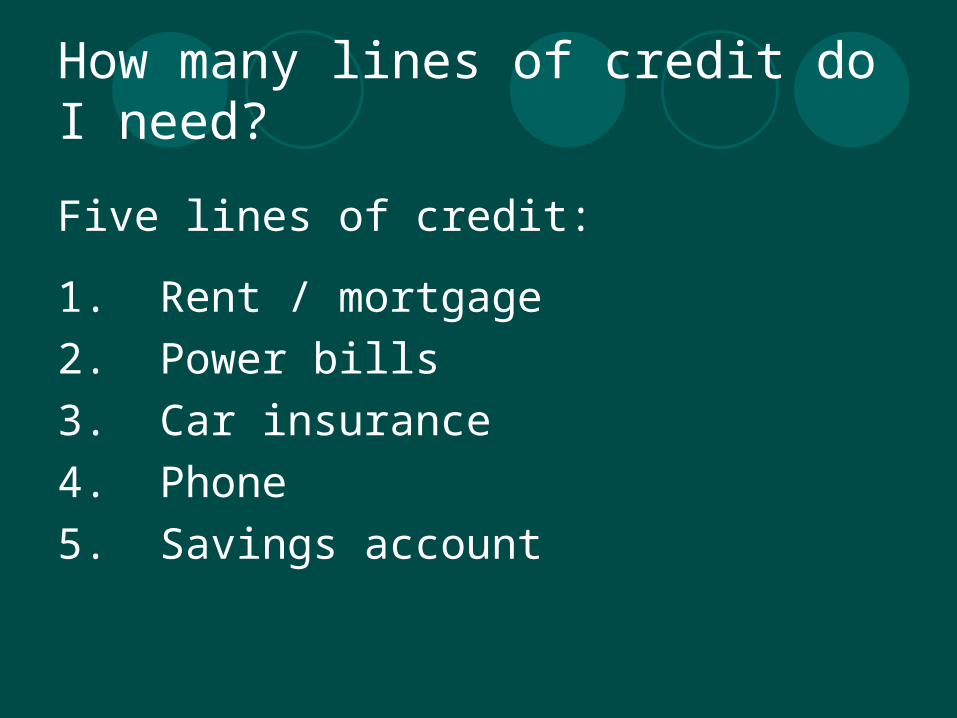

How many lines of credit do I need?

Five lines of credit:

1. Rent / mortgage

2. Power bills

3. Car insurance

4. Phone

5. Savings account

Should I open credit cards to improve my credit report?

No. Having more than two credit cards pulls down your credit score.

Pay off your credit card each month, if possible. If you have to pay over time, pay off the card within 2-4 months of a purchase.

How do we build wealth?

Five steps:

1. Write down your goal.

2. Pay bills on time.

3. Pay necessary living expenses first.

4. Set aside money for emergencies.

5. Save for your goal.

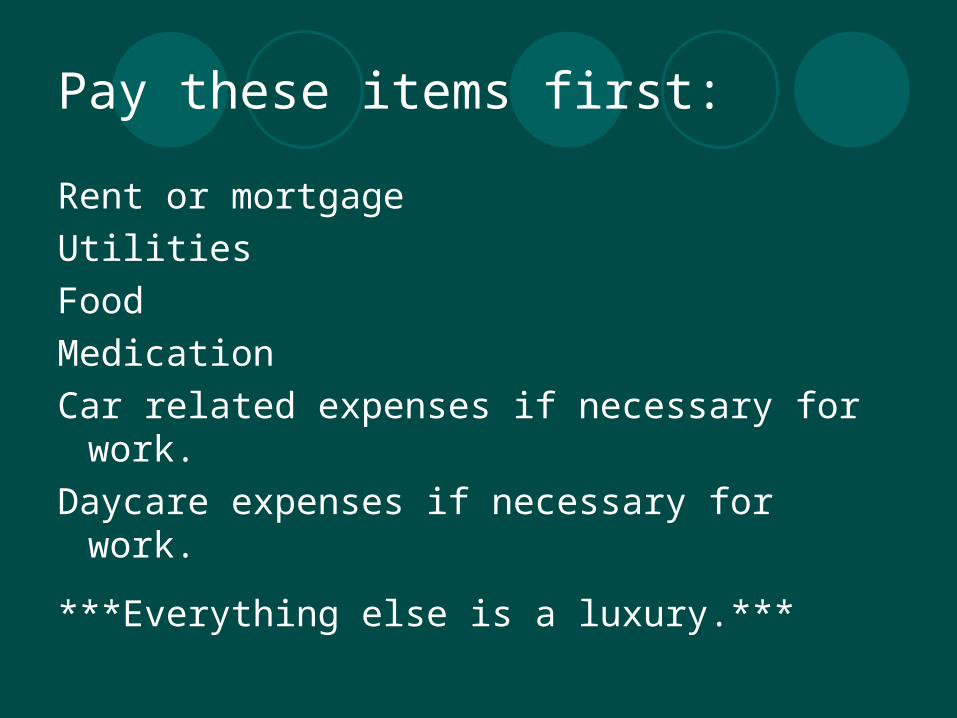

Pay these items first:

Rent or mortgage

Utilities

Food

Medication

Car related expenses if necessary for work.

Daycare expenses if necessary for work.

***Everything else is a luxury.***

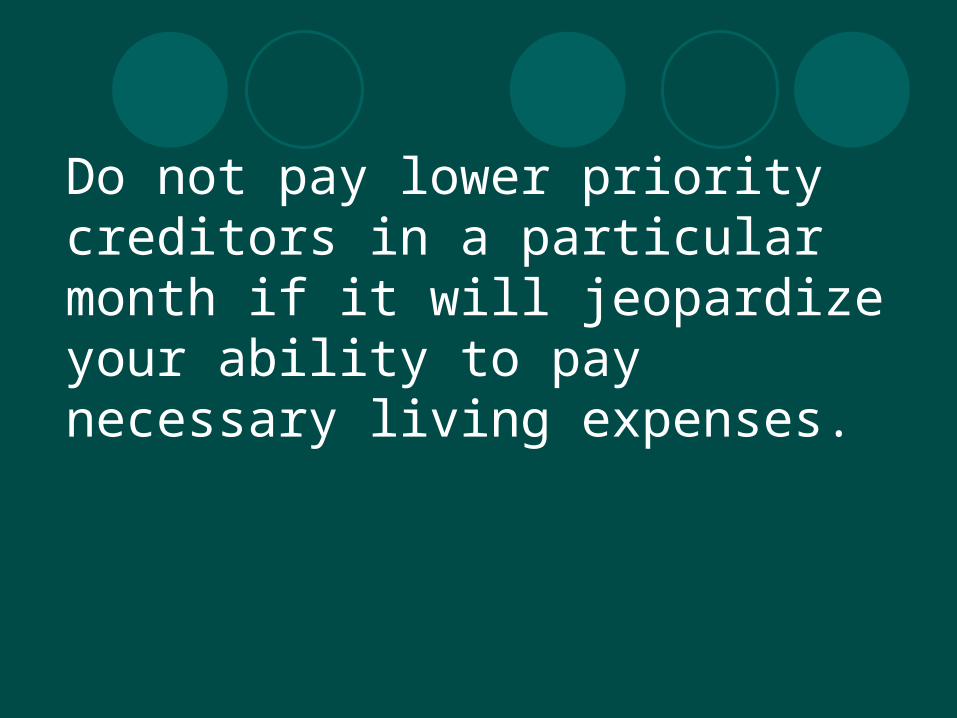

Do not pay lower priority creditors in a particular month if it will jeopardize your ability to pay necessary living expenses.

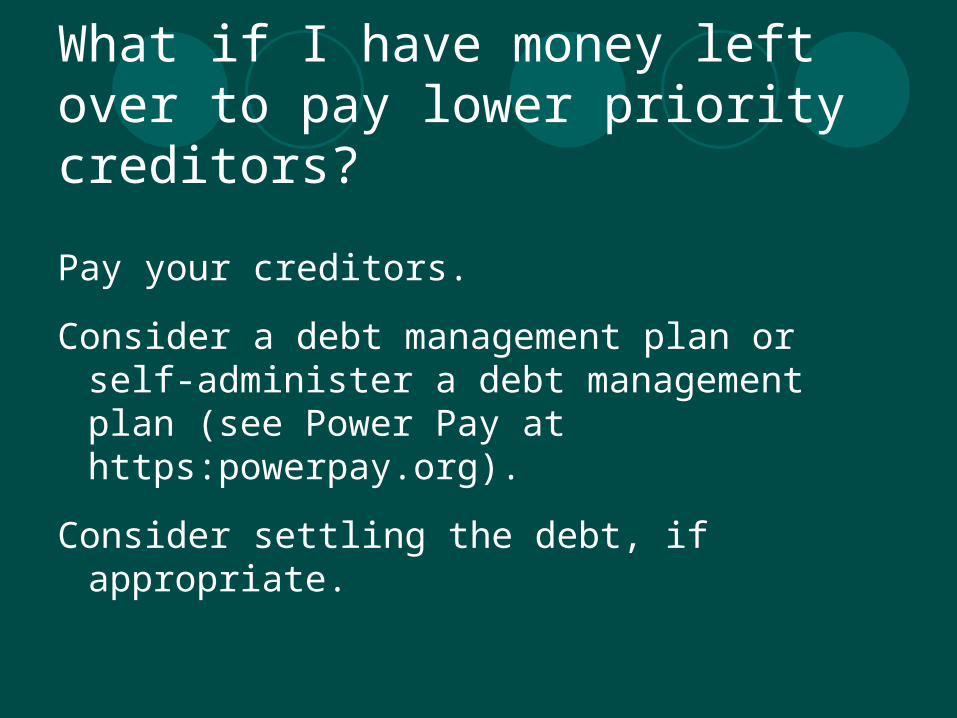

What if I have money left over to pay lower priority creditors?

Pay your creditors.

Consider a debt management plan or self-administer a debt management plan (see Power Pay at https:powerpay.org).

Consider settling the debt, if appropriate.

How do we build wealth?

Five steps:

1. Write down your goal.

2. Pay bills on time.

3. Pay necessary living expenses first.

4. Set aside money for emergencies.

5. Save for your goal.

If you pay your bills on time and are on your way to building a good credit record, then what should you do?

Save money.

Reflect on your goal.

For example:

“My goal is to save 3 months’ living expenses in an emergency savings fund.”

or

“My goal is to save at least $500,000 for retirement.”

The Impact of Saving $20 a Week:

5% annual rate of return

10% annual rate of return

10 years $13,700 $18,200

20 years $36,100 $65,000

30 years $72,600 $188,000

40 years $131,900 $506,300

The Impact of Time of Money

Age Contributions Made Early

Contributions Made Later

22-30 (9 years) $2,000 annually $0

31-65 (35 years) $0 $2,000 annually

Total Saved $18,000 $70,000

Amount available at age 65, with a 9% rate of return

$579,471 $470,249

You can reach this goal by saving $40 a week.

Easy ways to save:

1. Pay yourself first.

2. Get your family on board with saving.

3. Use payroll deductions to automatically transfer money into savings.

4. When you finish paying off an installment loan, continue to make “payments” into your savings account.

5. Participate in an employer-sponsored retirement plan or a tax-deferred retirement plan.

How do we build wealth?

Five steps:

1. Write down your goal.

2. Pay bills on time.

3. Pay necessary living expenses first.

4. Set aside money for emergencies.

5. Save for your goal.

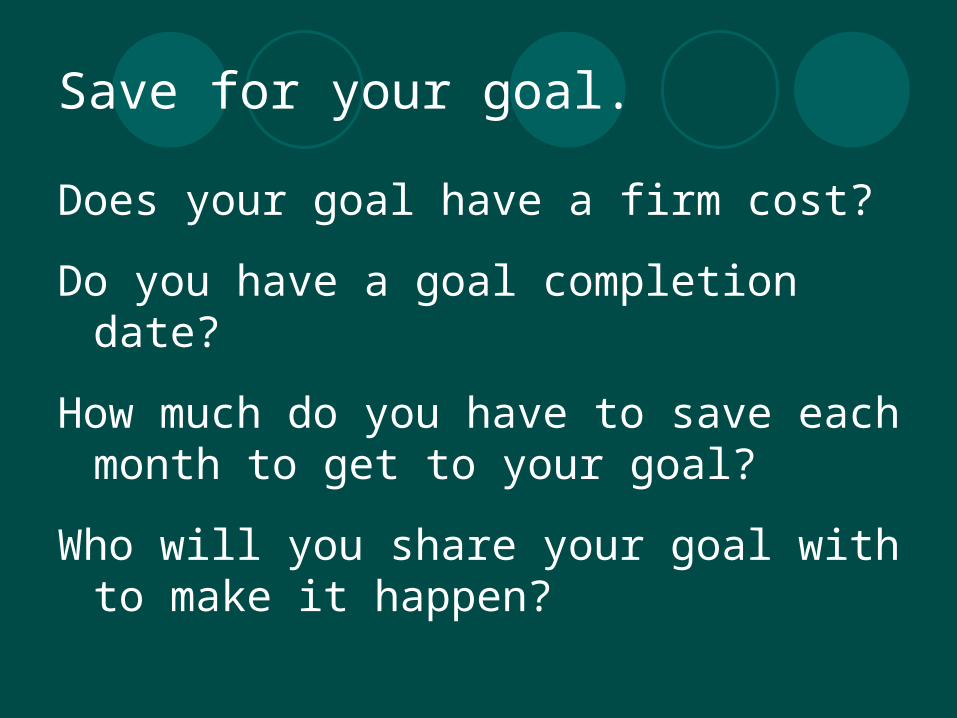

Save for your goal.

Does your goal have a firm cost?

Do you have a goal completion date?

How much do you have to save each month to get to your goal?

Who will you share your goal with to make it happen?

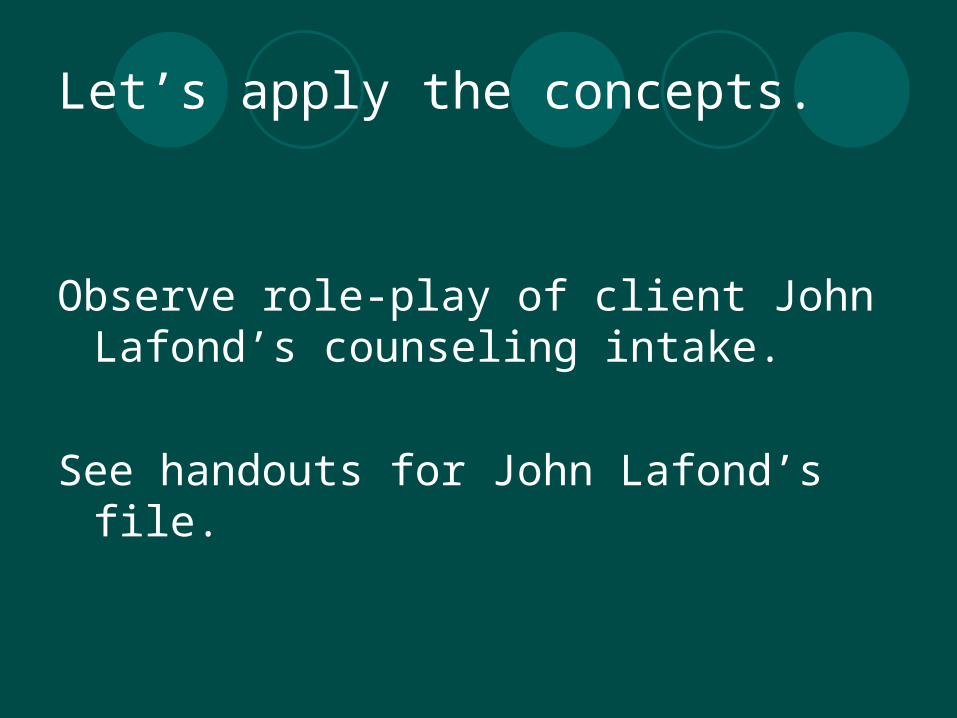

Let’s apply the concepts.

Observe role-play of client John Lafond’s counseling intake.

See handouts for John Lafond’s file.

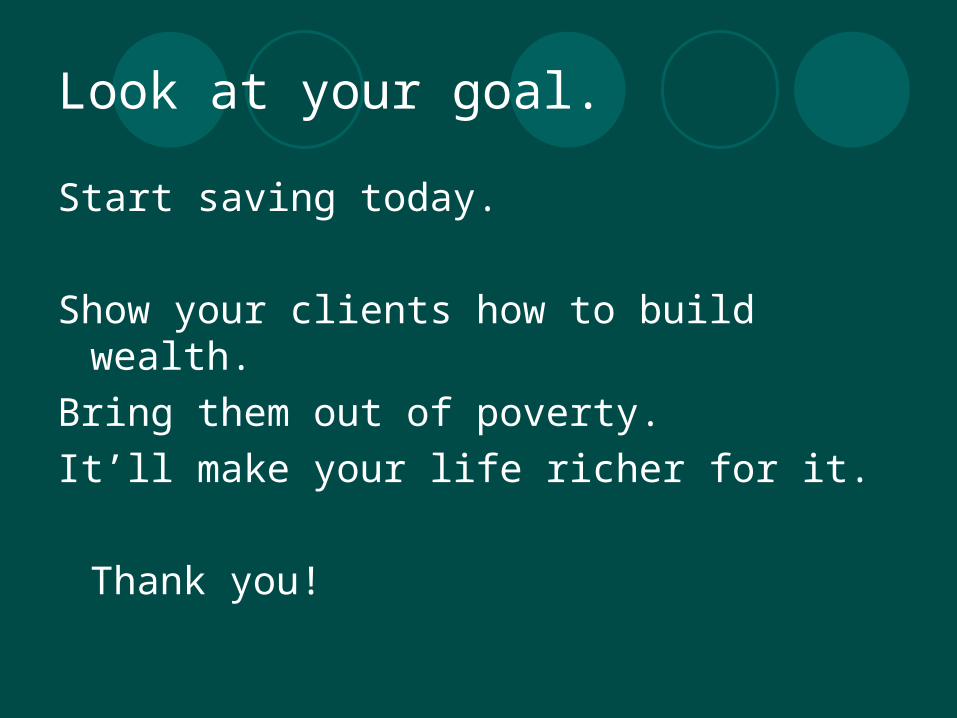

Look at your goal.

Start saving today.

Show your clients how to build wealth.

Bring them out of poverty.

It’ll make your life richer for it.

Thank you!