Budgeting and Funding of United Nations Regular Budget

22

Budgeting and Funding of United Nations Regular Budget Mr. Johannes Huisman, Director Office of Programme Planning, Finance, and Budget (OPPFB) Programme Planning and Budget Division (PPBD) September 8 th , 2021

Transcript of Budgeting and Funding of United Nations Regular Budget

Budgeting and Funding of United Nations Regular Budget

Mr. Johannes Huisman, Director

Office of Programme Planning, Finance, and Budget (OPPFB)

Programme Planning and Budget Division (PPBD)

September 8th, 2021

Human resources

Scales of assessment Budgets

Other administrative matters

02

04

01

03

Fifth Committee (Administrative and Budgetary Committee)

Entrusted with administrative and budgetary matters such as:

1

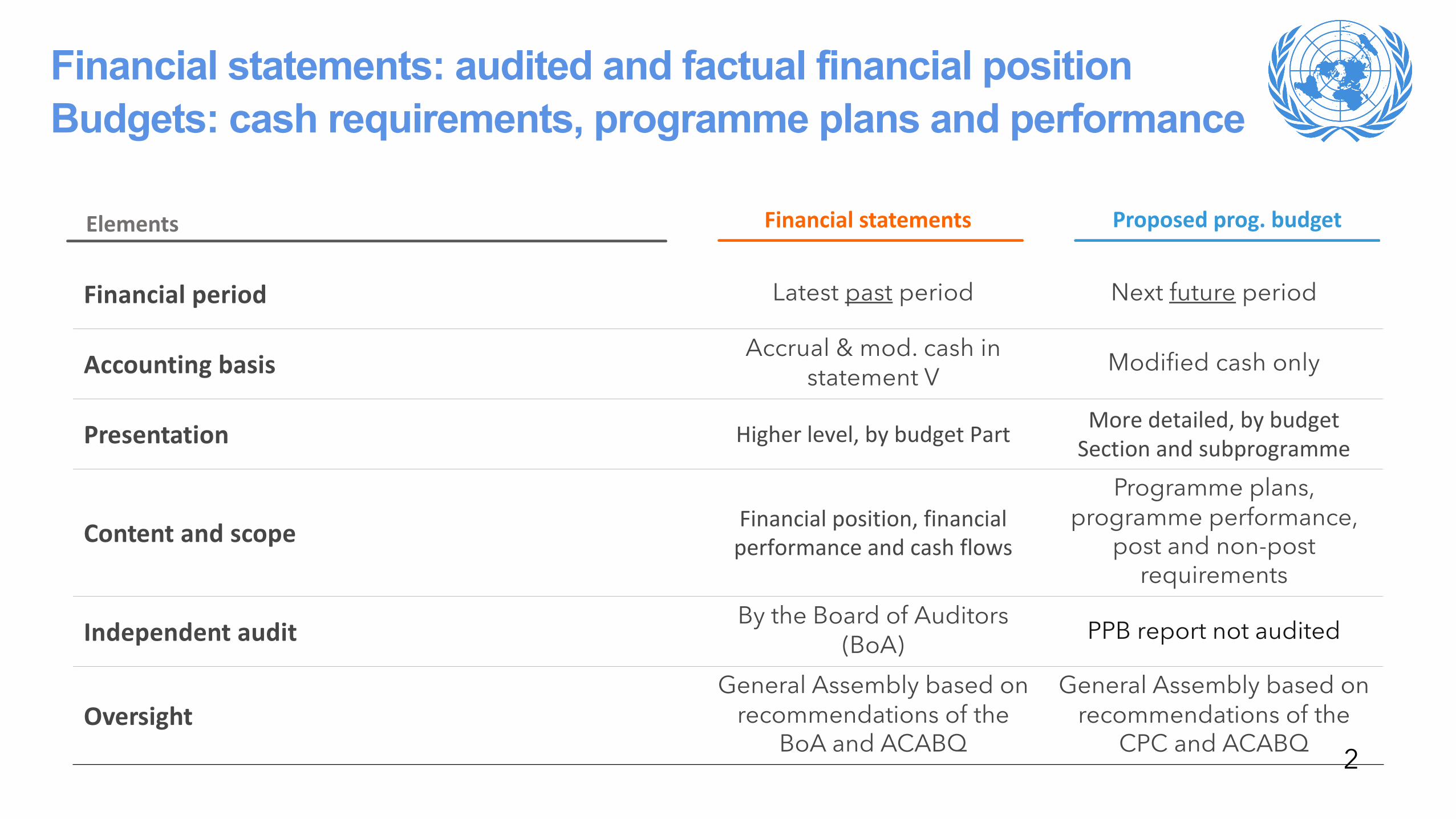

Financial statements: audited and factual financial positionBudgets: cash requirements, programme plans and performance

2

Financial statements Proposed prog. budgetElements

Financial period Latest past period Next future period

Accounting basis Accrual & mod. cash in statement V Modified cash only

Presentation Higher level, by budget Part More detailed, by budget Section and subprogramme

Content and scope Financial position, financial performance and cash flows

Programme plans, programme performance,

post and non-post requirements

Independent audit By the Board of Auditors (BoA) PPB report not audited

OversightGeneral Assembly based on

recommendations of the BoA and ACABQ

General Assembly based on recommendations of the

CPC and ACABQ

Nine thousand pages of budgetary information

2500 pages of responses to

ACABQ

4500 pages ofbudget reports

500 pages of supplementary

reports

Budget Information Portal

https://results.un.org/

500 pages of ACABQ reports 150 pages of

CPC report

Update in Q4 of 2021

General Assembly

30 pages ofGA resolution

Live

3

Improved accessibility through online tools to facilitate GA deliberations

Nominal growth between 2014 & 2022 of $440m or 15%

2,2292,386 2,246 2,207 2,281 2,403 2,362 2,478 2,389

598596 561 669 635 656 712 730 731

0

1,000

2,000

3,000

4,000

2014 2015 2016 2017 2018 2019 2020 2021 2022

In m

illio

ns o

f US

dolla

rs

Regular Budget SPMs

4

3,0743,0592,9162,8762,8072,982

2,827

(21%)(20%)

(20%) (23%) (22%)(21%) (23%)

3,208

(23%)

3,120

(23%)

No real growth; Recosting totals $430m

150?3,270?

Total posts approved for 2014-2015: 10,118Total posts proposed for 2022: 10,005

Recosting parameters subject to technical revision

* If actual expenditures for staff exceed appropriation additional resources will be sought

Inflation Updated Consumer Price Index from the Economist

Rates of Exchange Adjustments due to currency fluctuations

Projected Staff Cost*Actual payroll and allowancesPost adjustment/cost of living

adjustmentsActual vacancy rates

RecostingParameters

5

Recosting remains technical process. Changes to the methodology require approval by the GA

2020 2021

PPB 2021 approved by GA

• Forward RoE for 2021

Updated projection for 2021 of:• Post adjustment multiplier• Cost-of-living adjustment• Consumer-price Index

Projections based on prior expenditure experience for:• Standard salaries• Vacancy rates

Formulation of PPB 2022

• Use of same forward RoE for 2021

Preliminary projection for 2022 of:• Post adjustment multiplier• Cost-of-living adjustment• Consumer-price Index

Use of same:• Standard salaries• Vacancy rates

Revised estimates PPB 2022

• Forward RoE for 2022

Updated projection for 2022 of:• Post adjustment multiplier• Cost-of-living adjustment• Consumer-price Index

Projections based on prior expenditure experience for:• Standard salaries• Vacancy rates

6

Assessment to Member States reduced by income estimates, mainly staff assessment

More than $250m in staff assessment

contributes to lower assessments

7

Appropriations under

expenditure sections

Approved income

estimatesOther

Decreasing trend in overall assessment

196 190 66 109 93 90 80 82

2,612 2,771 2,549 2,578 2,487 2,849 2,867 2,955

6,783 6,377

10,631

6,866

4,981

9,406

6,593

3,615

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

2014 2015 2016 2017 2018 2019 2020 2021

In m

illio

ns o

f US

dolla

rs

Peacekeeping Regular Budget Tribunals

9,591

13,246

9,553

7,561

12,345

9,540

6,652

8

Annual average 9,7289,338

PPB, includes regular budget and estimates for XB & support account• RB estimates proposed for approval. Programme plans enabled by resources from all funding sources.• Extrabudgetary (XB) estimates & support account resources for information purposes• 75% of XB estimates are for Refugees (under UNHCR and UNRWA)

Regular Budget(19%)

XB - Refugees(59%)

Support account(3%)

9

XB – All other*(17%)

*Mostly RC System, UNEP, HABITAT, UNODC, UN Women & Human Rights

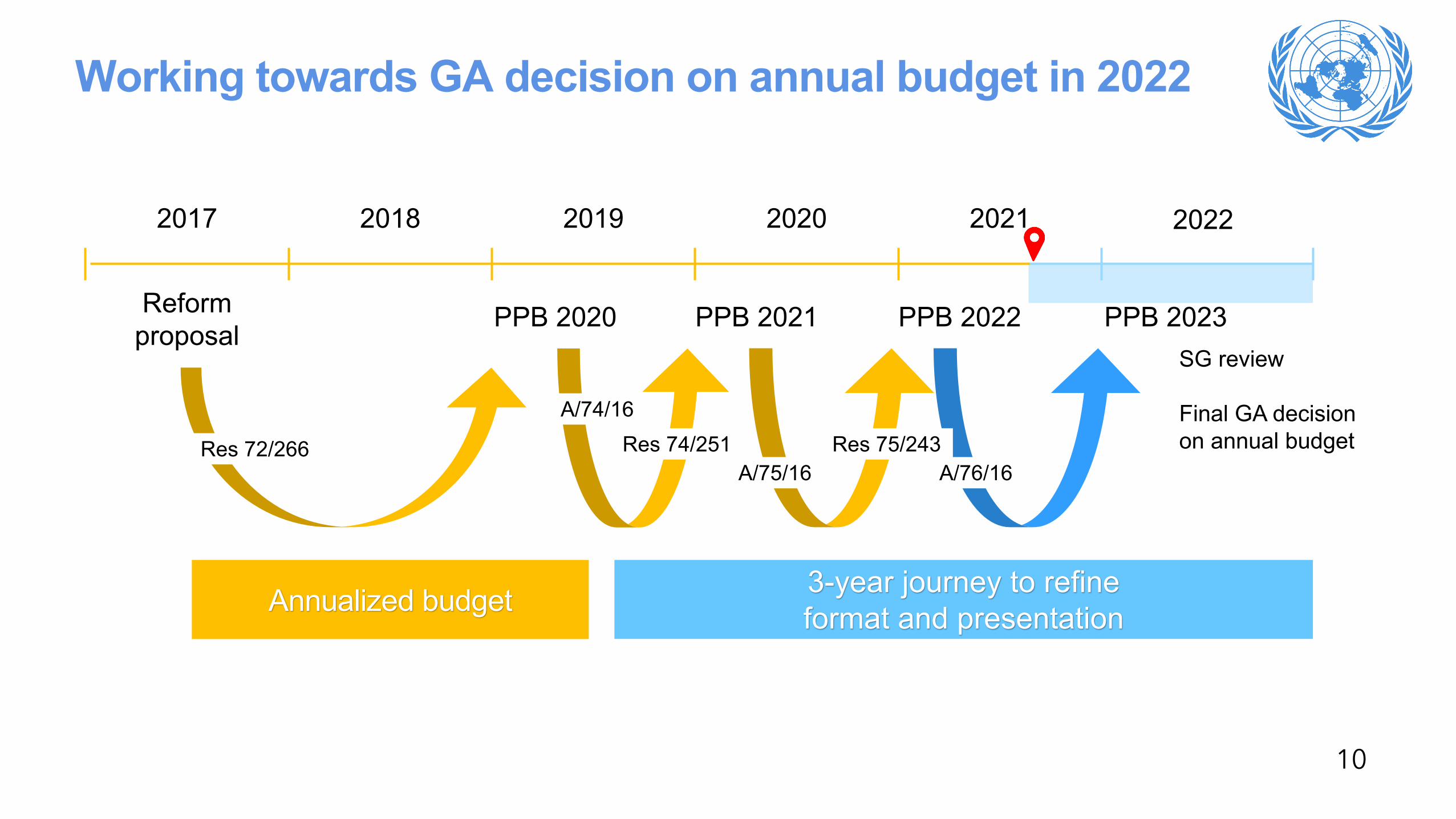

Working towards GA decision on annual budget in 2022

10

2017 2018 2019 2020 2021 2022

Reform proposal

Annualized budget 3-year journey to refine format and presentation

PPB 2020SG review

Final GA decision on annual budgetRes 72/266 Res 74/251

A/74/16

PPB 2021 PPB 2022 PPB 2023

A/75/16 A/76/16Res 75/243

Budget reform: to earn trust by demonstrating added-value

Demonstration of more concrete results

Enhanced accountability

by performance &lesson learned

More responsive to

emerging needs

Deeper trust in the Organization

11

Strategy

Result-based budgeting in the UN driven by resolutionsSequential nature preserved by starting w/ programme planning and target results

Resolution

Concerns

DeliverablesObjective

Inputs

Mandates

Preambular Paragraphs Operating Paragraphs

PerformanceMeasures MS Intergovernmental

UN Programme Plans UN Resources

12

UN and MS Intergovernmental

PPB 2022, Financial performance report for 2020 &additional reports to be considered during main session

13

2021

PPB 2022

2020 Fin. Statem. 2020 Transfers 2020 FPR

GA Main session

PBIs and Rev. Est.

Construction

Recosting

Cont. Fund

Subventions

Tribunals

Preliminary estimates of $150m expected in additional resources above PPB 2022

14

Reports based on resolutions Amount in

millions of USD

Human Rights Council $35-40*

Resolutions and decisions bythe GA > $4*

Countering use of ICT $3.5Law of the Sea $0.6Counter-terrorism TBD*African Descent $0.1

Resolutions and decisions ofthe Economic and Social Council $0.5

Resolutions and decisions bythe Security Council TBD*

Colombia, Libya, UNITAMS

Total: >$40

Constructions $21.2

ECA -ECLAC $6.6ESCAP $7.0UNON $7.6

Strategic Heritage Plan (presented outside RB) $71.7

Subventions $18.6

ECCC $7.5RSCSL $2.8STL $8*

Recosting TBD*

Total: >$110

Other reportsAmount in

millions of USD

* Preliminary estimates

Discussion on CPC increasingly on substantive issues and less on format

15

OHRLLS

DPPA

ESCWA

UNCTAD

And many others

ACABQ recommends $15 million reduction. 16 fewer posts. More information in future proposals.

16

Various funding mechanisms; not all with immediate appropriation

17

Description AppropriationFunding mechanisms

Proposed programme budget Requirements known until April ü

Unforeseen and extraordinary expenses (UEE)

$10m with the concurrence of ACABQ (if >10m GA) û

$8m under SG authority to quickly respond to events that threat

maintenance of peace and securityû

ICJ: 362.5k Security: 500k û

Subventions Complement XB funding and honor obligations and mandates ü û

PBIs and Rev. EstimatesFollowing resolutions deciding

on new / expanded mandates or SG initiatives as per Fin. Reg.

ü

û Presented post-facto in the financial performance report for possible appropriation

Programme budget implications (PBIs)

Mandates not provided for in the programme budget

18

Contingency fund is not a funding mechanismIt’s a presentation mechanism

• Political margin set at 0.75% of the appropriation to accommodate mandates not in the programme budget.

• Depending on the magnitude of new and expanded mandates with budgetary implications, level of the contingency fund may be exceeded.

• Appropriation outside of contingency fund will be sought when PBIs and revised estimates exceed level set for the contingency fund.

• General Assembly regularly approves RE and PBIs that exceed level set for the contingency fund.

19

Prop. Programme

budget

PBIs, Revised Estimates and Construction Up to 0.75% of

previous appropriation

Appropriation and charge against

contingency fund

Appropriation

ü

û

Budgetary implications influenced by nuances in language

Condition 1Binding request for action

Decides…

Mandates…

Requests…

Condition 2New/expanded activities

A new report of…

New consultations…

Additional meetings…

or ➔ No PBIs

and ➔ PBI triggered

Illustrative examples• Invites to explore… N

(no conditions met)

• Decides to maintain… N

(only condition 1 met)

• Invites a new report N(only condition 2 met)

• Request a new report Y (both

conditions met; hence, budget

implications)In contrast to: encourage, call upon, invites, etc. In contrast to: maintain, continue to, etc.

Condition 1 Condition 2

Condition 1 Condition 2 20

Case by case assessment continues to be required

Thank You!