Black Money, SIT on Black Money, Special Investigation Team for Black Money

Upload

dr-ambrish-sharmaCategory

view

222download

0

8/7/2019 budget and black money

http://slidepdf.com/reader/full/budget-and-black-money 1/26

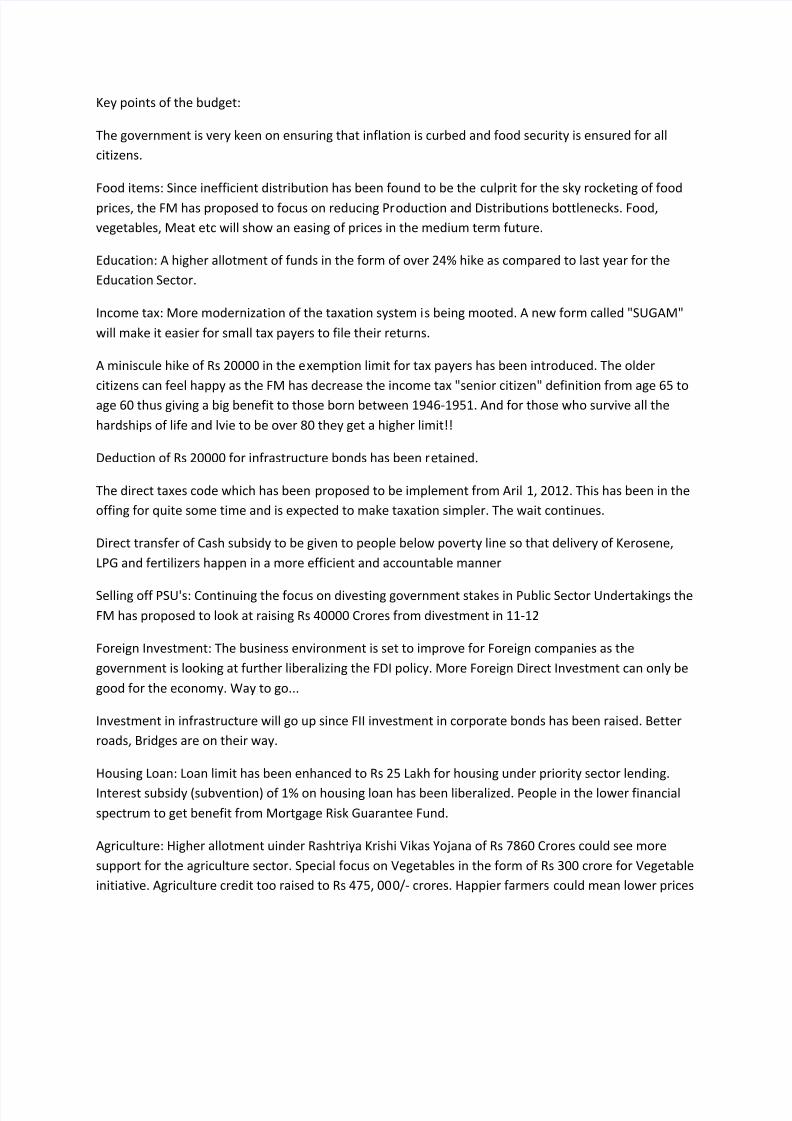

Key points of the budget:

The government is very keen on ensuring that inflation is curbed and food security is ensured for all

citizens.

Food items: Since inefficient distribution has been found to be the culprit for the sky rocketing of food

prices, the FM has proposed to focus on reducing Production and Distributions bottlenecks. Food,

vegetables, Meat etc will show an easing of prices in the medium term future.

Education: A higher allotment of funds in the form of over 24% hike as compared to last year for the

Education Sector.

Income tax: More modernization of the taxation system is being mooted. A new form called "SUGAM"

will make it easier for small tax payers to file their returns.

A miniscule hike of Rs 20000 in the exemption limit for tax payers has been introduced. The older

citizens can feel happy as the FM has decrease the income tax "senior citizen" definition from age 65 to

age 60 thus giving a big benefit to those born between 1946-1951. And for those who survive all the

hardships of life and lvie to be over 80 they get a higher limit!!

Deduction of Rs 20000 for infrastructure bonds has been retained.

The direct taxes code which has been proposed to be implement from Aril 1, 2012. This has been in the

offing for quite some time and is expected to make taxation simpler. The wait continues.

Direct transfer of Cash subsidy to be given to people below poverty line so that delivery of Kerosene,

LPG and fertilizers happen in a more efficient and accountable manner

Selling off PSU's: Continuing the focus on divesting government stakes in Public Sector Undertakings the

FM has proposed to look at raising Rs 40000 Crores from divestment in 11-12

Foreign Investment: The business environment is set to improve for Foreign companies as the

government is looking at further liberalizing the FDI policy. More Foreign Direct Investment can only be

good for the economy. Way to go...

Investment in infrastructure will go up since FII investment in corporate bonds has been raised. Better

roads, Bridges are on their way.

Housing Loan: Loan limit has been enhanced to Rs 25 Lakh for housing under priority sector lending.

Interest subsidy (subvention) of 1% on housing loan has been liberalized. People in the lower financial

spectrum to get benefit from Mortgage Risk Guarantee Fund.

Agriculture: Higher allotment uinder Rashtriya Krishi Vikas Yojana of Rs 7860 Crores could see more

support for the agriculture sector. Special focus on Vegetables in the form of Rs 300 crore for Vegetable

initiative. Agriculture credit too raised to Rs 475, 000/- crores. Happier farmers could mean lower prices

8/7/2019 budget and black money

http://slidepdf.com/reader/full/budget-and-black-money 2/26

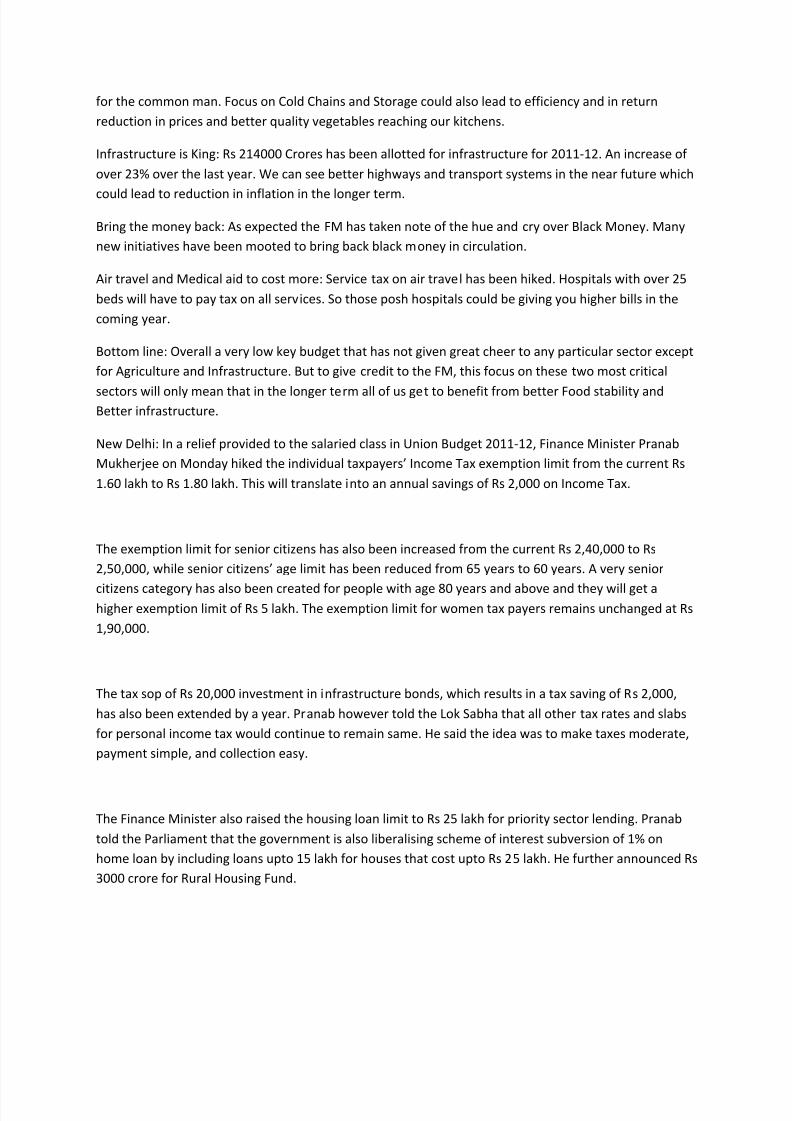

for the common man. Focus on Cold Chains and Storage could also lead to efficiency and in return

reduction in prices and better quality vegetables reaching our kitchens.

Infrastructure is King: Rs 214000 Crores has been allotted for infrastructure for 2011-12. An increase of

over 23% over the last year. We can see better highways and transport systems in the near future which

could lead to reduction in inflation in the longer term.

Bring the money back: As expected the FM has taken note of the hue and cry over Black Money. Many

new initiatives have been mooted to bring back black money in circulation.

Air travel and Medical aid to cost more: Service tax on air travel has been hiked. Hospitals with over 25

beds will have to pay tax on all services. So those posh hospitals could be giving you higher bills in the

coming year.

Bottom line: Overall a very low key budget that has not given great cheer to any particular sector except

for Agriculture and Infrastructure. But to give credit to the FM, this focus on these two most critical

sectors will only mean that in the longer term all of us get to benefit from better Food stability andBetter infrastructure.

New Delhi: In a relief provided to the salaried class in Union Budget 2011-12, Finance Minister Pranab

Mukherjee on Monday hiked the individual taxpayers Income Tax exemption limit from the current Rs

1.60 lakh to Rs 1.80 lakh. This will translate into an annual savings of Rs 2,000 on Income Tax.

The exemption limit for senior citizens has also been increased from the current Rs 2,40,000 to Rs

2,50,000, while senior citizens age limit has been reduced from 65 years to 60 years. A very senior

citizens category has also been created for people with age 80 years and above and they will get ahigher exemption limit of Rs 5 lakh. The exemption limit for women tax payers remains unchanged at Rs

1,90,000.

The tax sop of Rs 20,000 investment in infrastructure bonds, which results in a tax saving of Rs 2,000,

has also been extended by a year. Pranab however told the Lok Sabha that all other tax rates and slabs

for personal income tax would continue to remain same. He said the idea was to make taxes moderate,

payment simple, and collection easy.

The Finance Minister also raised the housing loan limit to Rs 25 lakh for priority sector lending. Pranab

told the Parliament that the government is also liberalising scheme of interest subversion of 1% on

home loan by including loans upto 15 lakh for houses that cost upto Rs 25 lakh. He further announced Rs

3000 crore for Rural Housing Fund.

8/7/2019 budget and black money

http://slidepdf.com/reader/full/budget-and-black-money 3/26

For the corporate sector, the Finance Minister reduced surcharge of 7.5% to 5%. He however hiked

direct tax from 18% to 18.5% for corporate. Pranab said he was not proposing any roll back in either the

service tax or excise duty, which both currently stand at 10%.

Pranab hiked the service tax on each domestic air ticket by Rs 50 and on international ticket by Rs 250.

The Finance Minister also doled out sops for the agriculture sector and proposed Rs 7,860 crores for

Farmer Development Program. The minister further proposed to raise farm loan target to Rs 4.75 lakh

crores in the next fiscal year and said the government would also provide additional 3% interest benefit

on some farm loans.

Pranab said inflation has remained above the comfort level for most part of the current fiscal and is

another focus area. The overall inflation at 8.23% is higher than the comfort level of the Reserve Bank at

5-6%, he said. The minister added that food inflation had moderated to 9.3% in January this year from

20.2% in February 2010.

The Finance Minister further said that the new Companies Bill could be introduced in the current session

of Parliament. On the Direct Tax Code, Pranab said the Bill was likely to be passed by Parliament in the

next financial year after the Standing Committees report is received. GST, he assured, would roll out

from April 1, 2012.

On the disinvestment front, Pranab promised to maintain the tempo and said the government had set a

Rs 40,000 crore target this fiscal. The minister said discussions were on to further liberalise FDI Policy,

while announcing that FIIs would be allowed to invest in mutual funds while their investment limit in

corporate bonds to be hiked to USD 40 billion.

Budget Highlights

Income Tax Corporate Tax Black Money

Service Tax Indirect Tax Inflation

Growth Subsidies Infrastructure and Industry

8/7/2019 budget and black money

http://slidepdf.com/reader/full/budget-and-black-money 4/26

Agriculture Fiscal Health Fundamentals

Outlays Rural & Social Sector Education

Banking & Finance Green Initiatives

Income Tax

* Idea to make tax moderate, payment simple, collection easy

* Rs 1.80 lakh exemption for general tax payer; will accrue benefit Rs 2000

* Senior citizens age limit reduced from 65 years to 60 years

* Amount of exemption on senior citizens increased from Rs 2,40,000 to Rs 2,50,000

* Very senior citizens category created for 80 years and above

* Very senior citizens to get higher exemption limit of Rs 5 lakh

* To introduce simpler tax forms for presumptive tax

* Invest-linked deduction for housing linked products

* Tax sop of Rs 20,000 in infra bonds stays for one more year

* Low withholding tax of 5% for notified infra funds

* New revised income tax return form `Sugam` to be introduced for small tax papers

* Net loss from direct tax proposals estimated at Rs 11,500 crore

* Direct Taxes Code (DTC) to be effective from April 1, 2012

Corporate Tax

* Corporate surcharge reduced to 5% from current 7.5%

* Minimum Alternate Tax raised to 18.5%

* MAT introduced on developers of SEZ

* Foreign dividend rate tax cut to 15% for Indian companies

8/7/2019 budget and black money

http://slidepdf.com/reader/full/budget-and-black-money 5/26

Black Money

* Five-f old strategy to deal with black money

1. Discussions on double taxation avoidance agreements: India has comprehensive Double TaxationAvoidance Agreements (DTAA ) with 65 countries. This means that there are agreed rates of tax and

jurisdiction on specified types of income arising in a country to a tax resident of another country. Under

the Income Tax Act 1961 of India, there are two provisions, Section 90 and Section 91, which provide

specific relief to taxpayers to save them from DTAA. Section 90 is for taxpayers who have paid the tax to

a country with which India has signed DTAA, while Section 91 provides relief to tax payers who have

paid tax to a country with which India has not signed a DTAA. Thus, India gives relief to both kind of

taxpayers.

A large number of foreign institutional investors who trade on the Indian stock markets operate from

Mauritius. According to the tax treaty between India and Mauritius, capital gains arising from the sale of shares are taxable in the country of residence of the shareholder and not in the country of residence of

the company whose shares have been sold. Therefore, a company resident in Mauritius selling shares of

an Indian company will not pay tax in India. Since there is no capital gains tax in Mauritius, the gain will

escape tax altogether.

The Indian and Cypriot tax treaty is the only other such Indian treaty to provide for the same beneficial

treatment of capital gains.

It must be noted that India has and is making attempts to revise both the Mauritius and Cyprus tax

treaties to eliminate this favourable treatment of capital gains tax.

Double Taxation Avoidance Agreements A Brief Overview

Fiscal jurisdiction is often the most aggressively guarded jurisdiction of any nation. As a consequence,

even in times when economies are going global and borders fading, leading to liquid movement of

goods, services and capital, double taxation is still one of the major obstacles to the development of

inter-country economic relations. Nations are often forced to negotiate and accommodate the claims of

other nations within their heavily guarded fiscal jurisdiction by the means of double taxation avoidance

agreements, in order to bring down the barriers to international trade.

The Fiscal Committee of OECD in the Model Double Taxation Convention on Income and Capital, 1977,

defines the phenomenon of international juridical double taxation as the imposition of comparable

taxes in two or more states on the same tax payer in respect of the same subject matter and for

identical periods. Therefore, the basic cause of international multiple taxation is the exercise by

sovereign states of their inherent right to levy tax extra-territorially. Most of the countries subject their

residents to tax, on the basis of personal jurisdiction, on their global income including income arising or

having its source in foreign countries.

8/7/2019 budget and black money

http://slidepdf.com/reader/full/budget-and-black-money 6/26

8/7/2019 budget and black money

http://slidepdf.com/reader/full/budget-and-black-money 7/26

a) laying down rules for division of revenue between two countries;

b) exempting certain incomes from tax in either country ;

c) reducing the applicable rates of tax on certain incomes taxable in either countries

Secondly, and equally importantly tax treaties help a taxpayer of one country to know with greater

certainty the potential limits of his tax liabilities in the other country.

Still another benefit from the tax-payers point of view is that, to a substantial extent, a tax treaty

provides against non-discrimination of foreign tax payers or the permanent establishments in the source

countries vis-à-vis domestic tax payers.

Pattern of taxation

Double taxation agreements allocate jurisdiction with respect to the right to tax a particular kind of

income. The principle underlying tax treaties is to share the revenues between two countries. If each

country gets a reasonable share of tax revenues, the bilateral and multilateral trade prospers and the

overall tax collection also increases as a result of which both countries tend to benefit.[3] A double tax

avoidance agreement deals by and large with business income, income from moveable property and

from immovable property.

There are well established patterns of taxation of various types on income. The agreements provide of

allocation of taxing jurisdiction to different contracting parties in respect of different heads of income.

In general, the rules are to the following effect:

· Income from the business[4] is taxed

only in the resident country, if the business entity has no activity in the source state;

only on the source state, if there is a fixed place of business, i.e. Permanent Establishment and to the

extent it is attributable to that place

· Income form immovable property[5] arising to a non-resident is taxed primarily in the state of its

location, i.e. the source[6] state.

· Income from movable property such as dividends[7], interest[8] and royalties[9] are primarily taxed in

the resident state, but the source state may impose a reduced tax.

Methods of Eliminating Double Taxation

The objective of double taxation can be achieved Tax treaties employ various methods or a combination

of

(i) Exemption Method -

8/7/2019 budget and black money

http://slidepdf.com/reader/full/budget-and-black-money 8/26

One method of avoiding double taxation is for the residence country to altogether exclude foreign

income from its tax base. The country of source is then given exclusive right to tax such incomes. This is

known as complete exemption method and is sometimes followed in respect of profits attributable to

foreign permanent establishments or income from immovable property. Indian tax treaties with

Denmark, Norway and Sweden embody with respect to certain incomes.

(ii) Credit Method

This method reflects the underline concept that the resident remains liable in the country of residence

on its global income, however as far the quantum of tax liabilities is concerned credit for tax paid in the

source country is given by the residence country against its domestic tax as if the foreign tax were paid

to the country of residence itself.

(iii) Tax Sparing

One of the aims of the Indian Double Taxation Avoidance Agreements is to stimulate foreign investment

flows in India from foreign developed countries. One way to achieve this aim is to let the investor to

preserve to himself/itself benefits of tax incentives available in India for such investments. This is done

through Tax Sparing. Here the tax credit is allowed by the country of its residence, not only in respect

of taxes actually paid by it in India but also in respect of those taxes India forgoes due to its fiscal

incentive provisions under the Indian Income Tax Act.

Thus, tax sparing credit is an extension of the normal and regular tax credit to taxes that are spared by

the source country i.e. forgiven or reduced due to rebates with the intention of providing incentives for

investments.

The regular tax credit is a measure for prevention of double taxation, but the tax sparing credit extends

the relief granted by the source country to the investor in the residence country by the way of an

incentive to stimulate foreign investment flows and does not seek reciprocal arrangements by the

developing countries.

Applicability of Treaty benefits

In order to get the benefit of a tax treaty, it is necessary to have an access to it. For that purpose, a

person must qualify in terms of the treaty as a:

- person

8/7/2019 budget and black money

http://slidepdf.com/reader/full/budget-and-black-money 9/26

- resident of any of the Contracting states; and

- beneficial owner of the income by the way of dividends, interest or royalties for a lower rate of

withholding tax.

Residence of a Person/ Resident

The determination of the residential status is of great significance as the taxability of income under the

domestic laws depends upon it, and as also only the resident of a contracting state can seek relief from

double taxation.

The expression resident of contracting state is defined to mean any person who, under the laws of that

state, is

1. liable to tax therein by reason of

2. domicile, residence, place of management or

3. any other criterion of a similar nature.

The treaty provisions set forth rules for determination whether a person is a resident of a contracting

state for purposes of the treaty. The determination looks for first to a persons liability to tax as a

resident under the respective taxation laws of the contracting state. If a person is resident in both the

contracting states, there are provisions to assign a single state of residence to him for purposes of the

treaty through tie-breaking rules.

Business Income

The business income of a non-resident is taxable in India under section 9(1)(i) of the ITA only if it accrues

or arises, directly or indirectly, through or from any business connection in India, property in India, asset

or source of income in India, or through the transfer of an Indian capital asset. Explanation 2 of section

9(1) (i) contain an inclusive definition of business connection; as per which a business connection is said

to exist if any person carrying on a business activity acts on behalf of a non-resident and:

# has and habitually exercises an authority to conclude contracts on behalf of the non-resident

# has no such authority, but habitually maintains in India a stock of goods or merchandise from which he

regularly delivers goods or merchandise on behalf of the non-resident

# habitually secures orders in India, mainly or wholly for the non-resident or its affiliates.

8/7/2019 budget and black money

http://slidepdf.com/reader/full/budget-and-black-money 10/26

Permanent Establishment

Double taxation agreement restricts the jurisdiction of the contracting states to taxing business income

of a foreign enterprise only if such enterprise carries on business in India through a permanent

establishment.

The term permanent establishment as defined in Article 5 means a fixed place of business through

which business of an enterprise is carried on. The definition requires performance of business activity

through a fixed place of business in another country. The expression has been defined as:

a. fixed place of business through which the business of an

b. enterprise is

c. Wholly or partly carried on.

The first part of Article 5(1) postulates that the existence of a fixed place of business whereas the second

part postulates that the business is carried on through a fixed place. If the second part is not attracted,

there is no permanent establishment.[10] Thereby meaning that there should necessarily be a fixed

place of business through which the enterprise must conduct business activity and that activity must be

income generating.

Treating shopping

Treating shopping is an expression which refers to the act of a resident of a third country taking

advantage of a fiscal treaty between states. A person acts through a legal entity created in a state

essentially to obtain treaty benefits that would not be available directly to such person.

The basic feature of treaty shopping is the establishment of base companies in other states solely for the

purpose of enjoying the benefit of a particular treaty rules existing between the state involved and the

third state. An example of treaty shopping can be the India-Mauritius double Taxation agreement where

various companies have been incorporated in Mauritius to take advantage of the Indo-Mauritius DTAA

in which capital gains are to be assessed as per the law of the state of residence of the entity .However,

under the Mauritian law, tax is not levied on capital gains which means that the capital gains made by

the Mauritian entity on transfer of shares in an Indian company go unassessed.

8/7/2019 budget and black money

http://slidepdf.com/reader/full/budget-and-black-money 11/26

However, the last few tears have seen a change in the approach of the States in the wake of wide

reports of extensive money laundering and the tax evasion. As a consequences, a lot of countries are

adopting a Limitation of Benefits clause in the tax treaties so as o restrict third parties from taking

advantage of tax treaties between two other states.

Indian Tax Regime

The Income Tax Act, 1961 (ITA) governs taxation of income in India. According to section 5 of the ITA,

Indian residents[11] are taxable on their worldwide income, and nonresidents are taxed only on income

that has its source in India.[12]10 Section 6 of the ITA defines who may be a tax resident and contains

different residency criteria for companies, firms, and individuals. The scope of section 5 is expanded by

the legal fiction contained in section 9, which deems certain kinds of income to be of Indian source.

The ITA favors source-based taxation as compared to the OECD model conventions or treaties entered

into by many developed countries that favor residence based taxation. Indian courts have supported

source based taxation in several cases in the past.

Indian Policy With Respect To Double Taxation Avoidance Agreements

The policy adopted by the Indian government in regard to double taxation treaties may be worded as

follows:

Trading with India should be relieved of Indian taxes considerably so as to promote its economic and

industrial development.

There should be co-ordination of Indian taxation with foreign tax legislation for Indian as well as foreign

companies trading with India

The agreements are intended to permit the Indian authorities to co-operate with the foreign tax

administration.

Tax treaties are a good compromise between taxation at source and taxation in the country of residence

India primarily follows the UN model convention and one therefore finds the tax-sparing and credit

methods for elimination of double taxation in most Indian treaties as well as more source-based

taxation in respect of the articles on royalties and other income than in the OECD model convention.

Conclusion

8/7/2019 budget and black money

http://slidepdf.com/reader/full/budget-and-black-money 12/26

The regime of international taxation exists through bilateral tax treaties based upon model treaties,

developed by the OECD and the UN, between the Contracting States. India has entered into a wide

network of tax treaties with various countries all over the world to facilitate free flow of capital into and

from India. However, the international tax regime has to be restructured continuously so as to respond

to the current challenges and drawbacks.

2. 1200 cases have been filed under the Money Laundering Law:

3 National policy to curb narcotics trade as it also fuels black money

4 Money Laundering Legislations scope expanded

5 Strength of Enforcement Directorate increased three-fold

Service Tax

* Ambit of service tax increased

* No roll back in service tax, to stay at 10%

* Service tax widened to cover hotel accommodation above Rs 1,000 per day, A/C restaurants serving

liquor

* Service tax on some category of hospitals

* Service tax on diagnostic tests

* Some legal services to be brought under service tax net

* Service by an individual to another individual exempted

* Service tax to result in a revenue gain of Rs 4,000 crore

* To raise service tax on domestic air travel by Rs 50 per ticket

* To raise service tax on international air travel by Rs 250 per ticket

* A new scheme to be introduced for refund of service tax on lines of drawback of duties

* Service tax to be levied on investment services by insurance firms

* Service tax mop up pegged at Rs 820 billion in FY12

* Net revenue gain of Rs 40 bn from service tax changes

* GST decision have to be taken in consonance with states

* Areas of divergence have been narrowed on Goods and Services Tax (GST)

8/7/2019 budget and black money

http://slidepdf.com/reader/full/budget-and-black-money 13/26

* Working on model for GST roll out

* GTC, GST will improve governance

* Significant progress in establishing GST Network

Indirect Tax

* Central excise duty to be maintained at standard rate of 10%

* Reduction in number of exemptions in central excise rate structure

* Nominal central excise duty of 1% imposed on 130 items entering in the tax net

* Lower rate of central excise duty enhanced from 4% to 5%

* Optional levy on branded garments or made up to be converted into a mandatory levy at unified

rate of 10%

* Peak rate of customs duty held at its current level

* Excise duty exemptions enlarged to include agricultural storage and warehouse equipments

* Basic customs duty reduced for specified agricultural machinery from 5% to 2.5%

* Basic customs duty reduced on micro-irrigation equipment from 7.5% to 5%

* De-oiled rice bran cake to be fully exempted from basic customs duty

* Export duty of 10% to be levied on de-oiled rice bran cakes export

* Export duty for all types of iron ore enhanced and unified at 20% ad valorem

* Full exemption from export duty to iron ore pellets

* Rs 300 per 10 gram excise on gold bar from copper smelters

* Rs 150 per 10 gram CVD on gold dore bars of upto 80% purity

* Custom duty on specified gems, jewellery, machine cut to 5%

* Levies 1% excise duty on branded jewellery

* Extends 1% excise concession to water filters

* Cut customs duty on yarn to 5% from 7.5%

* 5% import duty on parts for DVD writers, combo drive

* Import duty of 5% on inkjet and laserjet printers

8/7/2019 budget and black money

http://slidepdf.com/reader/full/budget-and-black-money 14/26

* Customs duty on cement industry raw materials - petcoke and gypsum - to be reduced to 2.5%

* Cash dispensers fully exempt from basic customs duty

* Imported batteries for electrical vehicles fully exempt from basic customs duty, to attract

concessional rate of central excise duty

* Concessional excise duty of 10% to vehicles based on fuel cell technology

* Basic customs duty and special CVD exemption to critical parts/assemblies for Hybrid vehicles

* Reduction in excise duty on kits for conversion of vehicles into Hybrid vehicles

* Excise duty on LEDs reduced to 5% and special CVD being fully exempted

* Basic customs duty on solar lantern reduced from 10 to 5%

* Ship owners allowed duty free spare parts imports

* Crude palm oil used in soap fully exempted

* Pre-tanning chemicals, enzyme-based chemicals used in leather industry exempted

* Bio-waste road making machines exempted

* No excise duty on equipment for ultra mega power plants

* Concessions to newspaper establishments for high speed printing presses extended to mailroom

equipment

* Some imported film colour rolls exempted from excise duty

* No excise duty on select film rolls

* Out right concession to factory-built ambulances from excise duty

* Relief measures proposed for raw pistachio, bamboo for agarbatti, lactose for the manufacture of

homoeopathic medicines, sanitary napkins, baby and adult diapers

* Tax proposals to result in a net revenue gain of Rs 7,300 crore

* Net revenue loss on account of taxes and duties will be Rs 200 crore

* Net tax to Centre will be Rs 6,64,457 crore

* Non-tax receipts pegged at Rs 1,25,435 crore

* To retain factory tax rate at 10%

* Stainless steel scrap exempted from import tax

8/7/2019 budget and black money

http://slidepdf.com/reader/full/budget-and-black-money 15/26

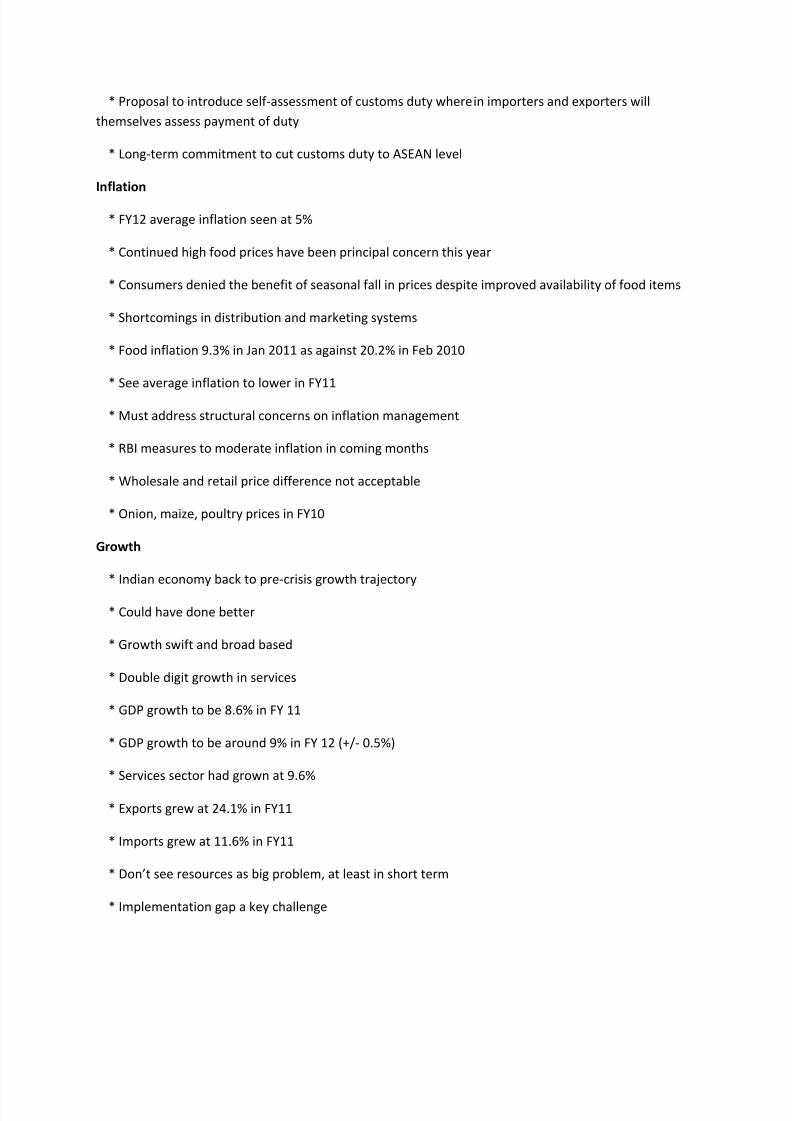

* Proposal to introduce self-assessment of customs duty wherein importers and exporters will

themselves assess payment of duty

* Long-term commitment to cut customs duty to ASEAN level

Inflation

* FY12 average inflation seen at 5%

* Continued high food prices have been principal concern this year

* Consumers denied the benefit of seasonal fall in prices despite improved availability of food items

* Shortcomings in distribution and marketing systems

* Food inflation 9.3% in Jan 2011 as against 20.2% in Feb 2010

* See average inflation to lower in FY11

* Must address structural concerns on inflation management

* RBI measures to moderate inflation in coming months

* Wholesale and retail price difference not acceptable

* Onion, maize, poultry prices in FY10

Growth

* Indian economy back to pre-crisis growth trajectory

* Could have done better

* Growth swift and broad based

* Double digit growth in services

* GDP growth to be 8.6% in FY 11

* GDP growth to be around 9% in FY 12 (+/- 0.5%)

* Services sector had grown at 9.6%

* Exports grew at 24.1% in FY11

* Imports grew at 11.6% in FY11

* Dont see resources as big problem, at least in short term

* Implementation gap a key challenge

8/7/2019 budget and black money

http://slidepdf.com/reader/full/budget-and-black-money 16/26

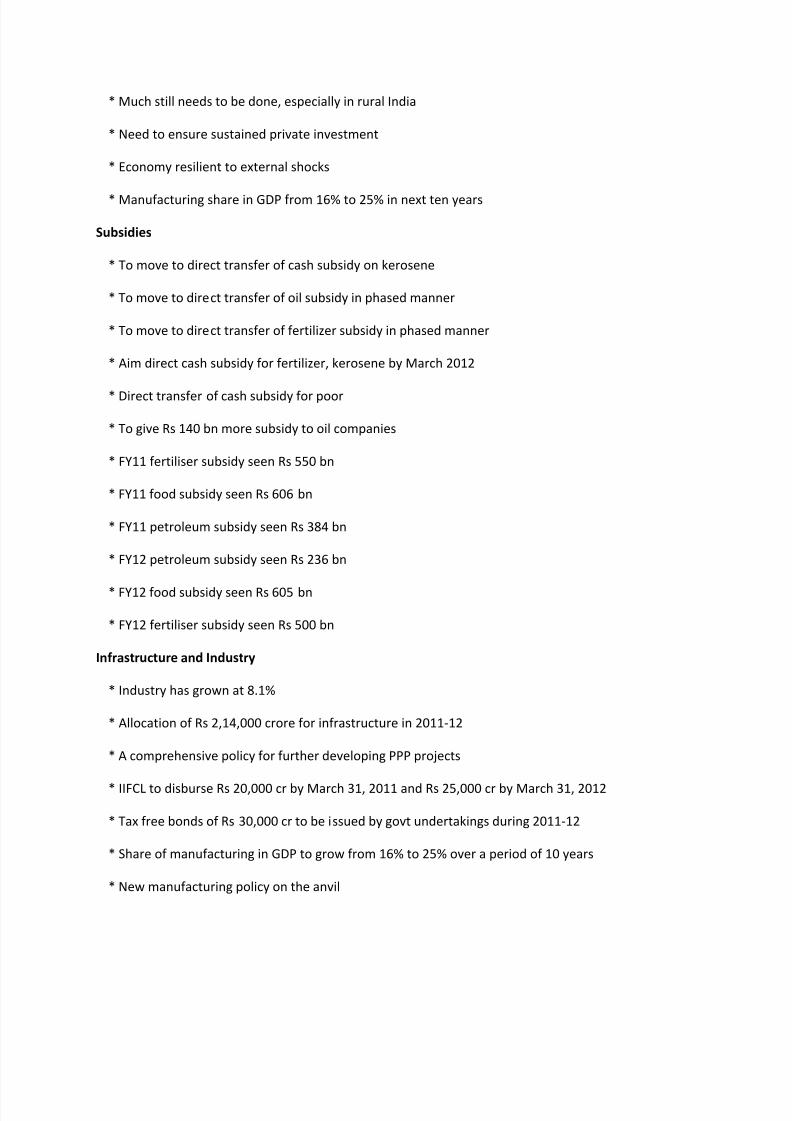

* Much still needs to be done, especially in rural India

* Need to ensure sustained private investment

* Economy resilient to external shocks

* Manufacturing share in GDP from 16% to 25% in next ten years

Subsidies

* To move to direct transfer of cash subsidy on kerosene

* To move to direct transfer of oil subsidy in phased manner

* To move to direct transfer of fertilizer subsidy in phased manner

* Aim direct cash subsidy for fertilizer, kerosene by March 2012

* Direct transfer of cash subsidy for poor

* To give Rs 140 bn more subsidy to oil companies

* FY11 fertiliser subsidy seen Rs 550 bn

* FY11 food subsidy seen Rs 606 bn

* FY11 petroleum subsidy seen Rs 384 bn

* FY12 petroleum subsidy seen Rs 236 bn

* FY12 food subsidy seen Rs 605 bn

* FY12 fertiliser subsidy seen Rs 500 bn

Inf rastructure and Industry

* Industry has grown at 8.1%

* Allocation of Rs 2,14,000 crore for infrastructure in 2011-12

* A comprehensive policy for further developing PPP projects

* IIFCL to disburse Rs 20,000 cr by March 31, 2011 and Rs 25,000 cr by March 31, 2012

* Tax free bonds of Rs 30,000 cr to be issued by govt undertakings during 2011-12

* Share of manufacturing in GDP to grow from 16% to 25% over a period of 10 years

* New manufacturing policy on the anvil

8/7/2019 budget and black money

http://slidepdf.com/reader/full/budget-and-black-money 17/26

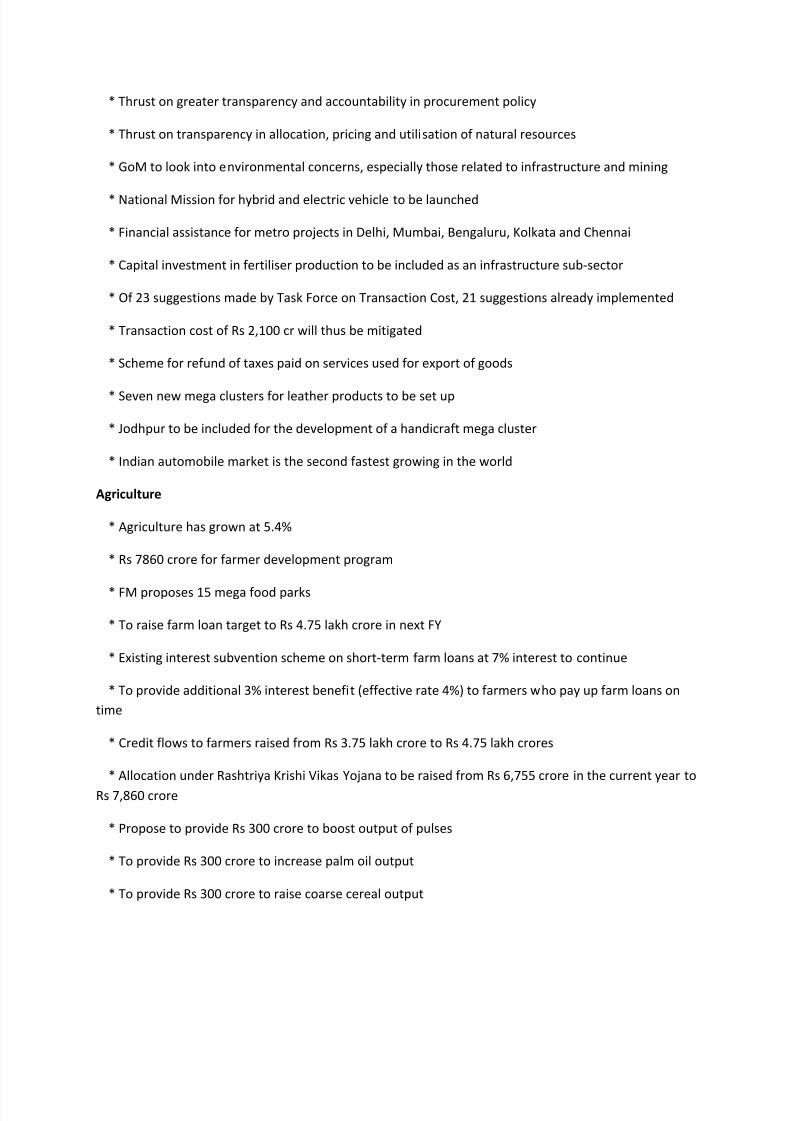

* Thrust on greater transparency and accountability in procurement policy

* Thrust on transparency in allocation, pricing and utilisation of natural resources

* GoM to look into environmental concerns, especially those related to infrastructure and mining

* National Mission for hybrid and electric vehicle to be launched

* Financial assistance for metro projects in Delhi, Mumbai, Bengaluru, Kolkata and Chennai

* Capital investment in fertiliser production to be included as an infrastructure sub-sector

* Of 23 suggestions made by Task Force on Transaction Cost, 21 suggestions already implemented

* Transaction cost of Rs 2,100 cr will thus be mitigated

* Scheme for refund of taxes paid on services used for export of goods

* Seven new mega clusters for leather products to be set up

* Jodhpur to be included for the development of a handicraft mega cluster

* Indian automobile market is the second fastest growing in the world

Agriculture

* Agriculture has grown at 5.4%

* Rs 7860 crore for farmer development program

* FM proposes 15 mega food parks

* To raise farm loan target to Rs 4.75 lakh crore in next FY

* Existing interest subvention scheme on short-term farm loans at 7% interest to continue

* To provide additional 3% interest benefit (effective rate 4%) to farmers who pay up farm loans on

time

* Credit flows to farmers raised from Rs 3.75 lakh crore to Rs 4.75 lakh crores

* Allocation under Rashtriya Krishi Vikas Yojana to be raised from Rs 6,755 crore in the current year to

Rs 7,860 crore

* Propose to provide Rs 300 crore to boost output of pulses

* To provide Rs 300 crore to increase palm oil output

* To provide Rs 300 crore to raise coarse cereal output

8/7/2019 budget and black money

http://slidepdf.com/reader/full/budget-and-black-money 18/26

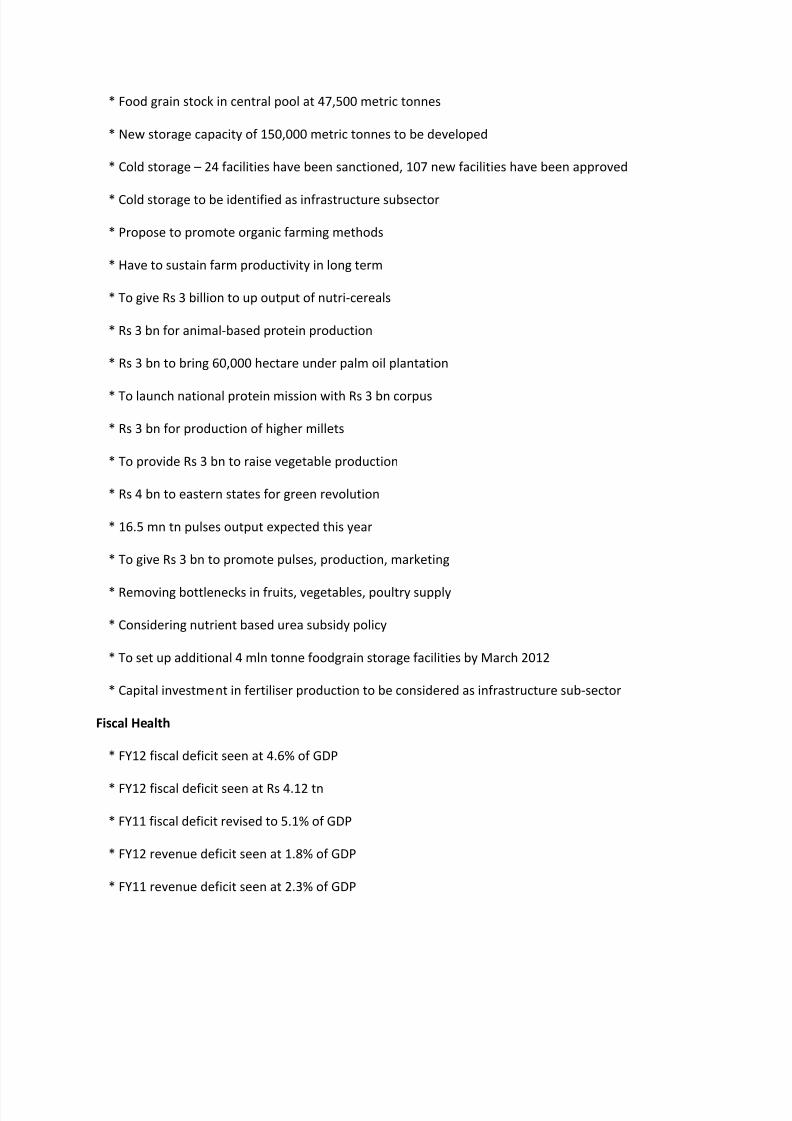

* Food grain stock in central pool at 47,500 metric tonnes

* New storage capacity of 150,000 metric tonnes to be developed

* Cold storage 24 facilities have been sanctioned, 107 new facilities have been approved

* Cold storage to be identified as infrastructure subsector

* Propose to promote organic farming methods

* Have to sustain farm productivity in long term

* To give Rs 3 billion to up output of nutri-cereals

* Rs 3 bn for animal-based protein production

* Rs 3 bn to bring 60,000 hectare under palm oil plantation

* To launch national protein mission with Rs 3 bn corpus

* Rs 3 bn for production of higher millets

* To provide Rs 3 bn to raise vegetable production

* Rs 4 bn to eastern states for green revolution

* 16.5 mn tn pulses output expected this year

* To give Rs 3 bn to promote pulses, production, marketing

* Removing bottlenecks in fruits, vegetables, poultry supply

* Considering nutrient based urea subsidy policy

* To set up additional 4 mln tonne foodgrain storage facilities by March 2012

* Capital investment in fertiliser production to be considered as infrastructure sub-sector

Fiscal Health

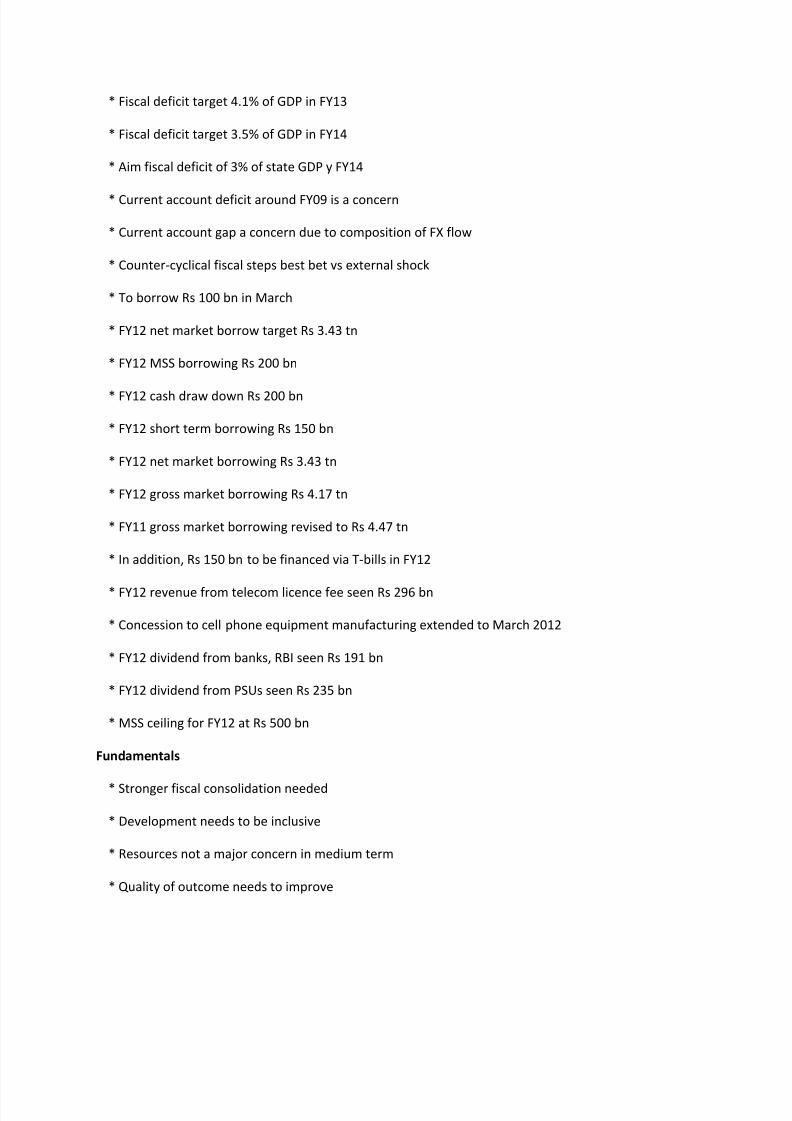

* FY12 fiscal deficit seen at 4.6% of GDP

* FY12 fiscal deficit seen at Rs 4.12 tn

* FY11 fiscal deficit revised to 5.1% of GDP

* FY12 revenue deficit seen at 1.8% of GDP

* FY11 revenue deficit seen at 2.3% of GDP

8/7/2019 budget and black money

http://slidepdf.com/reader/full/budget-and-black-money 19/26

* Fiscal deficit target 4.1% of GDP in FY13

* Fiscal deficit target 3.5% of GDP in FY14

* Aim fiscal deficit of 3% of state GDP y FY14

* Current account deficit around FY09 is a concern

* Current account gap a concern due to composition of FX flow

* Counter-cyclical fiscal steps best bet vs external shock

* To borrow Rs 100 bn in March

* FY12 net market borrow target Rs 3.43 tn

* FY12 MSS borrowing Rs 200 bn

* FY12 cash draw down Rs 200 bn

* FY12 short term borrowing Rs 150 bn

* FY12 net market borrowing Rs 3.43 tn

* FY12 gross market borrowing Rs 4.17 tn

* FY11 gross market borrowing revised to Rs 4.47 tn

* In addition, Rs 150 bn to be financed via T-bills in FY12

* FY12 revenue from telecom licence fee seen Rs 296 bn

* Concession to cell phone equipment manufacturing extended to March 2012

* FY12 dividend from banks, RBI seen Rs 191 bn

* FY12 dividend from PSUs seen Rs 235 bn

* MSS ceiling for FY12 at Rs 500 bn

Fundamentals

* Stronger fiscal consolidation needed

* Development needs to be inclusive

* Resources not a major concern in medium term

* Quality of outcome needs to improve

8/7/2019 budget and black money

http://slidepdf.com/reader/full/budget-and-black-money 20/26

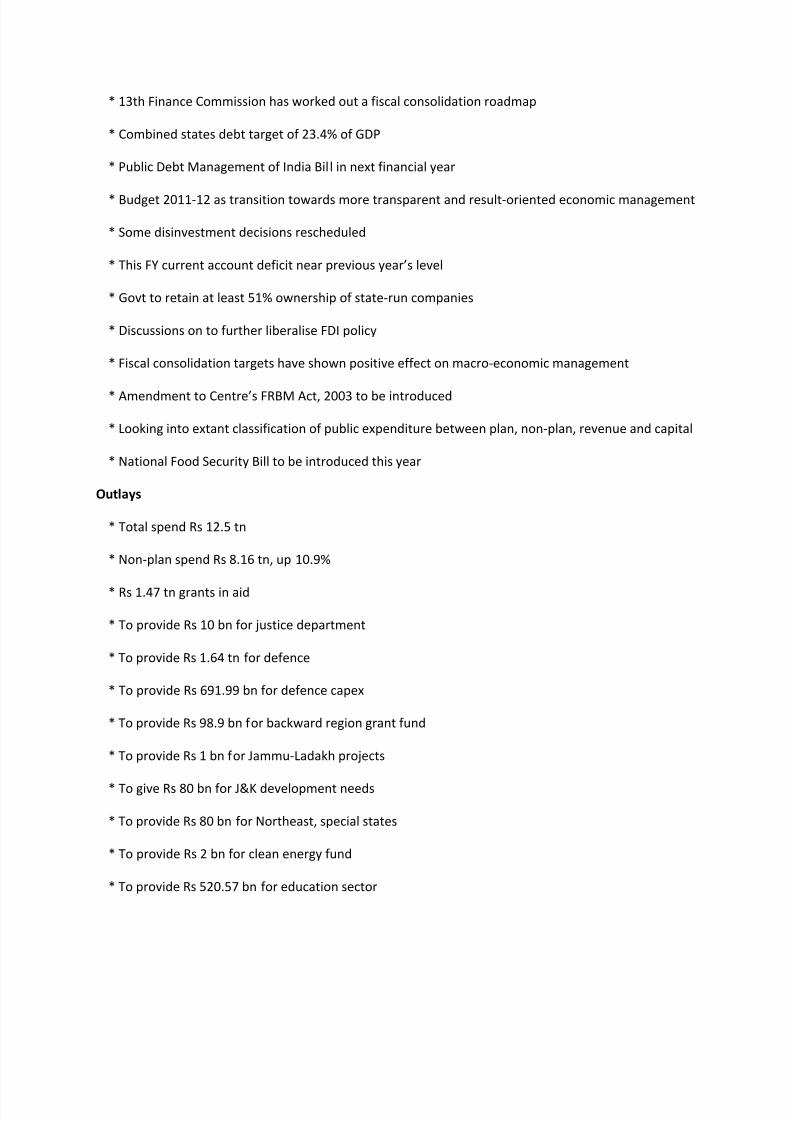

* 13th Finance Commission has worked out a fiscal consolidation roadmap

* Combined states debt target of 23.4% of GDP

* Public Debt Management of India Bil l in next financial year

* Budget 2011-12 as transition towards more transparent and result-oriented economic management

* Some disinvestment decisions rescheduled

* This FY current account deficit near previous years level

* Govt to retain at least 51% ownership of state-run companies

* Discussions on to further liberalise FDI policy

* Fiscal consolidation targets have shown positive effect on macro-economic management

* Amendment to Centres FRBM Act, 2003 to be introduced

* Looking into extant classification of public expenditure between plan, non-plan, revenue and capital

* National Food Security Bill to be introduced this year

Outlays

* Total spend Rs 12.5 tn

* Non-plan spend Rs 8.16 tn, up 10.9%

* Rs 1.47 tn grants in aid

* To provide Rs 10 bn for justice department

* To provide Rs 1.64 tn for defence

* To provide Rs 691.99 bn for defence capex

* To provide Rs 98.9 bn for backward region grant fund

* To provide Rs 1 bn for Jammu-Ladakh projects

* To give Rs 80 bn for J&K development needs

* To provide Rs 80 bn for Northeast, special states

* To provide Rs 2 bn for clean energy fund

* To provide Rs 520.57 bn for education sector

8/7/2019 budget and black money

http://slidepdf.com/reader/full/budget-and-black-money 21/26

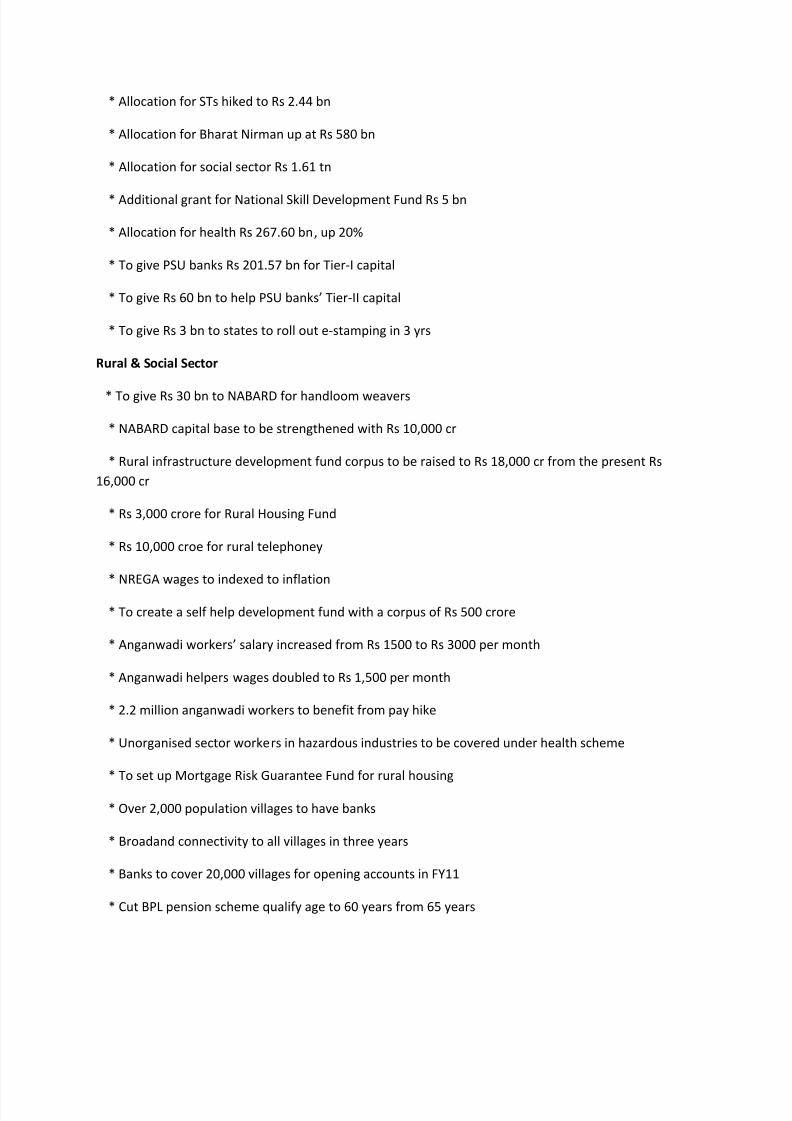

* Allocation for STs hiked to Rs 2.44 bn

* Allocation for Bharat Nirman up at Rs 580 bn

* Allocation for social sector Rs 1.61 tn

* Additional grant for National Skill Development Fund Rs 5 bn

* Allocation for health Rs 267.60 bn, up 20%

* To give PSU banks Rs 201.57 bn for Tier-I capital

* To give Rs 60 bn to help PSU banks Tier-II capital

* To give Rs 3 bn to states to roll out e-stamping in 3 yrs

Rural & Social Sector

* To give Rs 30 bn to NABARD for handloom weavers

* NABARD capital base to be strengthened with Rs 10,000 cr

* Rural infrastructure development fund corpus to be raised to Rs 18,000 cr from the present Rs

16,000 cr

* Rs 3,000 crore for Rural Housing Fund

* Rs 10,000 croe for rural telephoney

* NREGA wages to indexed to inflation

* To create a self help development fund with a corpus of Rs 500 crore

* Anganwadi workers salary increased from Rs 1500 to Rs 3000 per month

* Anganwadi helpers wages doubled to Rs 1,500 per month

* 2.2 million anganwadi workers to benefit from pay hike

* Unorganised sector workers in hazardous industries to be covered under health scheme

* To set up Mortgage Risk Guarantee Fund for rural housing

* Over 2,000 population villages to have banks

* Broadand connectivity to all villages in three years

* Banks to cover 20,000 villages for opening accounts in FY11

* Cut BPL pension scheme qualify age to 60 years from 65 years

8/7/2019 budget and black money

http://slidepdf.com/reader/full/budget-and-black-money 22/26

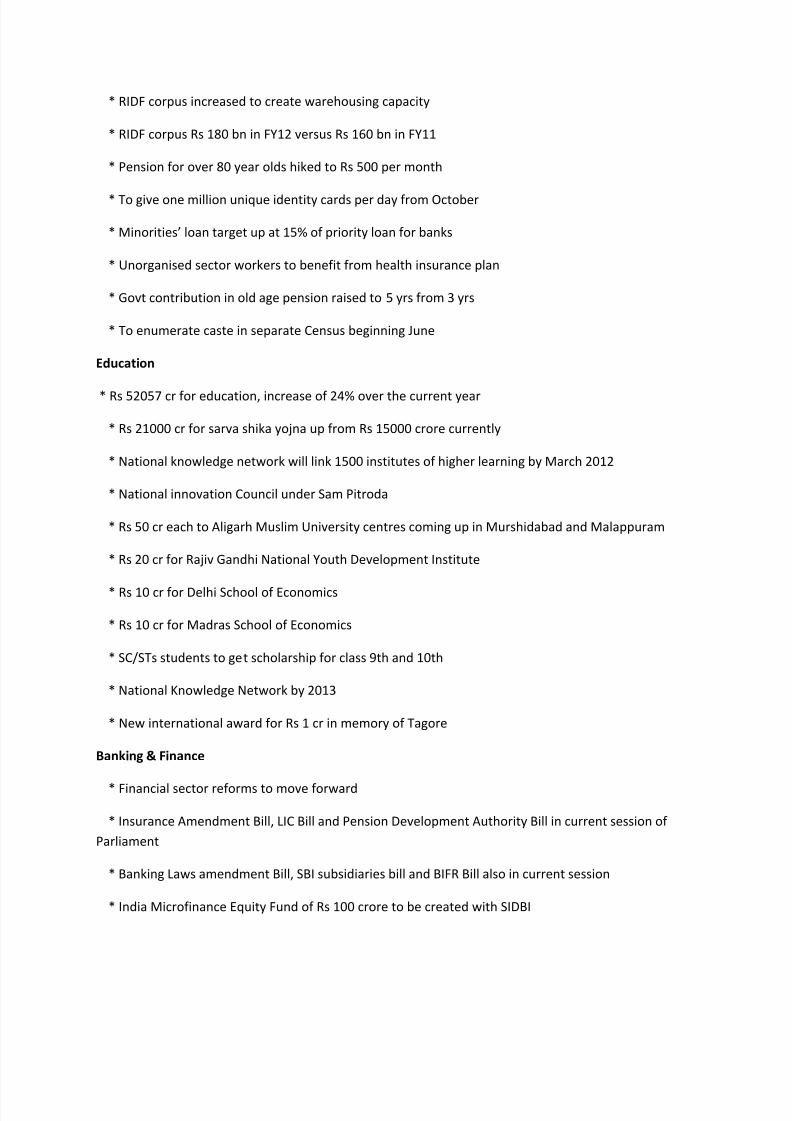

* RIDF corpus increased to create warehousing capacity

* RIDF corpus Rs 180 bn in FY12 versus Rs 160 bn in FY11

* Pension for over 80 year olds hiked to Rs 500 per month

* To give one million unique identity cards per day from October

* Minorities loan target up at 15% of priority loan for banks

* Unorganised sector workers to benefit from health insurance plan

* Govt contribution in old age pension raised to 5 yrs from 3 yrs

* To enumerate caste in separate Census beginning June

Education

* Rs 52057 cr for education, increase of 24% over the current year

* Rs 21000 cr for sarva shika yojna up from Rs 15000 crore currently

* National knowledge network will link 1500 institutes of higher learning by March 2012

* National innovation Council under Sam Pitroda

* Rs 50 cr each to Aligarh Muslim University centres coming up in Murshidabad and Malappuram

* Rs 20 cr for Rajiv Gandhi National Youth Development Institute

* Rs 10 cr for Delhi School of Economics

* Rs 10 cr for Madras School of Economics

* SC/STs students to get scholarship for class 9th and 10th

* National Knowledge Network by 2013

* New international award for Rs 1 cr in memory of Tagore

Banking & Finance

* Financial sector reforms to move forward

* Insurance Amendment Bill, LIC Bill and Pension Development Authority Bill in current session of

Parliament

* Banking Laws amendment Bill, SBI subsidiaries bill and BIFR Bill also in current session

* India Microfinance Equity Fund of Rs 100 crore to be created with SIDBI

8/7/2019 budget and black money

http://slidepdf.com/reader/full/budget-and-black-money 23/26

* Appropriate regulatory framework to protect interest of small borrowers

* Rs 5,000 cr to SIDBI for refinancing incremental lending

Green Initiatives

* Rs 200 cr for Green India Mission from National Clean Energy Fund

* Rs 200 cr to be allocated for Environmental Remediation Programmes

* To provide Rs 200 cr for clean-up of important lakes and rivers other than Ganga

Budget explains government strategy on black money

Press trust of India, February 28, 2011 (New Delhi)

Expressing "serious concern" over the generation and circulation of black money, Finance Minister

Pranab Mukherjee today said the government has adopted a five-fold strategy to deal with the menace.

"The generation and circulation of black money is an area of serious concern. To deal with this problem

effectively, the government has put into operation a five-fold strategy which consists of joining the

global crusade against black money," Mukherjee said in his Budget speech.

The Finance Minister also said trafficking in narcotic drugs also contributes to the generation of black

money and the government proposes to announce a national policy in this regard.

"To strengthen controls over prevention of trafficking and improve the management of narcotic drugs

and psychotropic substances, I propose to announce a comprehensive national policy in the near

future," he added.

During the year, the government has concluded discussions on 11 Tax Information Exchange

Agreements (TIEAs) and 13 new Double Taxation Avoidance Agreements (DTAAs), along with revision of

provisions of 10 existing DTAAs.

"To effectively handle the increase in tax information exchange and transfer pricing issues, Foreign Tax

Division of CBDT has been strengthened. A dedicated cell for exchange of information is being set up to

work on this agenda," he added.

He also said the Finance Ministry has commissioned a study on unaccounted income and wealth held

within and outside the country to suggest methods to tax and repatriate the illicit money.

Mukherjee added that the amendment in the Money Laundering Legislation in 2009 has significantly

increased its scope and application.

"The number of cases registered under this law have increased from 50 between 2005 to 2008 to over

1200 by January this year. The strength of the enforcement directorate has been increased three-fold to

deal effectively with the increased workload," he added.

8/7/2019 budget and black money

http://slidepdf.com/reader/full/budget-and-black-money 24/26

The Finance Minister said that India secured the membership of the Financial Action Task Force (FATF) in

June last year.

"This is an important initiative of G-20 for anti-money laundering. We have also joined the Task Force on

Financial Integrity and Economic Development, Eurasian Group (EAG) and Global Forum on

Transparency and Exchange of Information for Tax Purposes," he added.

Read more at: http://profit.ndtv.com/news/show/budget-explains-govt-strategy-on-black-money-

142932?cp

What is Financial Inclusion

What is Financial Inclusionchillibreeze writer Sreela Manoj

Financial inclusion is the availability of banking services at an affordable cost to disadvantaged and low-

income groups. In India the basic concept of financial inclusion is having a saving or current account with

any bank. In reality it includes loans, insurance services and much more.

The first-ever Index of Financial Inclusion to find out the extent of reach of banking services among 100

countries, India has been ranked 50. Only 34% of Indian individuals have access to or receive banking

services. In order to increase this number the Reserve Bank of India had the Government of India take

innovative steps. One of the reasons for opening new branches of Regional Rural Banks was to make

sure that the banking service is accessible to the poor. With the directive from RBI, our banks are now

offering No Frill Accounts to low income groups. These accounts either have a low minimum or nil

balance with some restriction in transactions. The individual bank has the authority to decide whether

the account should have zero or minimum balance. With the combined effort of financial institutions, six

million new No Frill accounts were opened in the period between March 2006-2007. Banks are now

considering FI as a business opportunity in an overall environment that facilitates growth.

The main reason for financial exclusion is the lack of a regular or substantial income. In most of the

cases people with low income do not qualify for a loan. The proximity of the financial service is another

fact. The loss is not only the transportation cost but also the loss of daily wages for a low income

individual. Most of the excluded consumers are not aware of the banks products, which are beneficial

8/7/2019 budget and black money

http://slidepdf.com/reader/full/budget-and-black-money 25/26

for them. Getting money for their financial requirements from a local money lender is easier than

getting a loan from the bank. Most of the banks need collateral for their loans. It is very difficult for a

low income individual to find collateral for a bank loan. Moreover, banks give more importance to

meeting their financial targets. So they focus on larger accounts. It is not profitable for banks to provide

small loans and make a profit.

Financial inclusion mainly focuses on the poor who do not have formal financial institutional support

and getting them out of the clutches of local money lenders. As a first step towards this, some of our

banks have now come forward with general purpose credit cards and artisan credit cards which offer

collateral-free small loans. The RBI has simplified the KYC (Know your customer) norms for opening a

No frill account. This will help the low income individual to open a No Frill account without identity

proof and address proof.

In such cases banks can take the individuals introduction from an existing customer whose full KYC

norm procedure has been completed. And the introducer must have a satisfactory transaction with the

bank for at least 6 months. This simplified procedure is available to those who intend to keep a balance

not exceeding Rs.50,000 in all accounts taken together. With this facility we can channel the untapped,

considerable amount of money from the low income group to the formal economy. Banks are now

permitted to utilize the service of NGOs, SHGs and other civil society organizations as intermediaries in

providing financial and banking services through the use of business facilitator and business

correspondent models.

Self Help Groups are playing a very important role in the process of financial inclusion. SHGs are usually

groups of women who get together and pool money from their savings and lend money among them.

Usually they are working with the support of an NGO. The SHG is given loans against the group

members guarantee. Peer pressure within the group helps in improving recoveries. Through SHGs

nearly 40 million households are linking with the banks. Micro finance is another tool which links low

income groups to the banks.

Yet, banks are fighting to fulfill the Financial Inclusion dream. The main reason is that the productsdesigned by the banks are not satisfying the low income families. The provision of uncomplicated, small,

affordable products will help to bring the low income families into the formal financial sector. Banks

have limitations to reach directly to the low income consumers. Correspondents can be considered to be

an excellent channel which banks can use to distribute their product information. Educating the

consumers about the financial benefits and products of banks which are beneficial to low income groups

will be a great step to tap their potential.

8/7/2019 budget and black money

http://slidepdf.com/reader/full/budget-and-black-money 26/26

Banks are now using new technologies like mobile phones to reach low income consumers. It is possible

that the telephone providers themselves will start basic banking services like savings and payments.

Indian telecom consumers have few links to financial institutions. So without much difficulty telecom

providers can win the battle with banks. Banks should therefore be proactive about transferring thistechnology into an opportunity.

The Indian Government has a long history of working to expand financial inclusion. Nationalization of

the major private sector banks in 1969 was a big step. In 1975 GOI established RRBs with the same aim.

It encouraged branch expansion of bank branches especially in rural areas. The RBI guidelines to banks

shows that 40% of their net bank credit should be lent to the priority sector. This mainly consists of

agriculture, small scale industries, retail trade etc. More than 80% of our population depends directly or

indirectly on agriculture. So 18% of net bank credit should go to agriculture lending. Recent

simplification of KYC norms are another milestone.

Financial inclusion is a great step to alleviate poverty in India. But to achieve this, the government

should provide a less perspective environment in which banks are free to pursue the innovations

necessary to reach low income consumers and still make a profit. Financial service providers should

learn more about the consumers and new business models to reach them.

In India Financial inclusion will be good business ground in which the majority of her people will decidethe winners and losers.

Chillibreeze's disclaimer: The views and opinions expressed in this article are those of the author(s) and

do not reflect the views of Chillibreeze as a company. Chillibreeze has a strict anti-plagiarism policy.

Please contact us to report any copyright issues related to this article.

![4028774 Black Money or Defaced Money[1]](https://static.fdocuments.us/doc/165x107/55cf9ba2550346d033a6cc8d/4028774-black-money-or-defaced-money1.jpg)