Fordham Intellectual Property, Media ... - Fordham University

Upload

david-de-wolfCategory

view

146download

5

Identifying Commodity Price BubblesPotential Risk and Rewards of Holding Commodities for Retail Investor

Portfolios

David De Wolf

Fordham University

June, 17 2016

David De Wolf (Fordham University) Identifying Commodity Price Bubbles June, 17 2016 1 / 27

Table of Contents

1 Research question

2 Data

3 Econometric testsSADF (PWY)GSADF (PSY)

4 ResultsBubble testsPortfolio creation

5 Conclusion

David De Wolf (Fordham University) Identifying Commodity Price Bubbles June, 17 2016 2 / 27

Research question

Research Question

1 Can we detect bubbles in commodity markets based on the PWY andPSY test during the past 26 years?

2 If we can detect bubbles, can we build pro�table trading strategiesbased on historical information that we have obtained?

David De Wolf (Fordham University) Identifying Commodity Price Bubbles June, 17 2016 3 / 27

Data

Data Selection

Source: Thompson Reuters Datastream

Four commodities: Gold, Oil, Corn and Soybean

Data frame: 03/04/1990 - 29/04/2016

Frequency: daily observations (6544 full sample)

Continuous Futures prices

David De Wolf (Fordham University) Identifying Commodity Price Bubbles June, 17 2016 4 / 27

Econometric tests SADF (PWY)

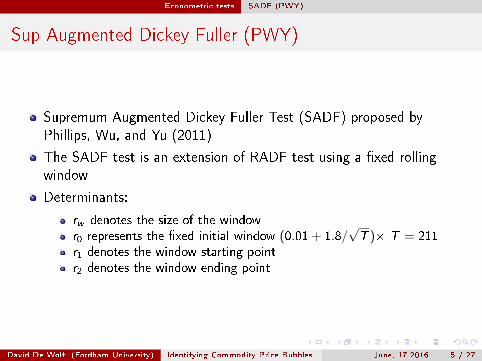

Sup Augmented Dickey Fuller (PWY)

Supremum Augmented Dickey Fuller Test (SADF) proposed byPhillips, Wu, and Yu (2011)

The SADF test is an extension of RADF test using a �xed rollingwindow

Determinants:

rw denotes the size of the windowr0 represents the �xed initial window (0.01 + 1.8/

√T )Ö T = 211

r1 denotes the window starting pointr2 denotes the window ending point

David De Wolf (Fordham University) Identifying Commodity Price Bubbles June, 17 2016 5 / 27

Econometric tests SADF (PWY)

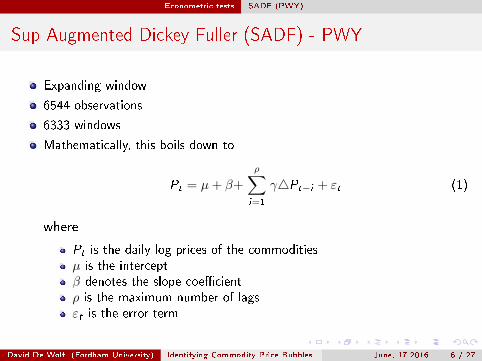

Sup Augmented Dickey Fuller (SADF) - PWY

Expanding window

6544 observations

6333 windows

Mathematically, this boils down to

Pt = µ+ β+

ρ∑i=1

γ4Pt−i + εt (1)

where

Pt is the daily log prices of the commoditiesµ is the interceptβ denotes the slope coe�cientρ is the maximum number of lagsεt is the error term

David De Wolf (Fordham University) Identifying Commodity Price Bubbles June, 17 2016 6 / 27

Econometric tests SADF (PWY)

Sup Augmented Dickey Fuller (SADF) - PWY

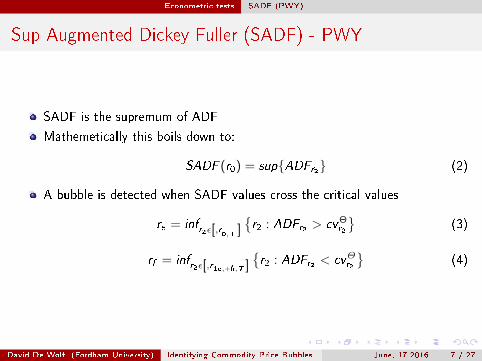

SADF is the supremum of ADF

Mathemetically this boils down to:

SADF (r0) = sup{ADFr2} (2)

A bubble is detected when SADF values cross the critical values

re = infr2ε[,r

0,T ]{r2 : ADFr2 > cvΘ

r2

}(3)

rf = infr2ε[,r1e,+h,T ]

{r2 : ADFr2 < cvΘr2

}(4)

David De Wolf (Fordham University) Identifying Commodity Price Bubbles June, 17 2016 7 / 27

Econometric tests GSADF (PSY)

Generalized Sup Augmented Dickey Fuller (GSADF) - PSY

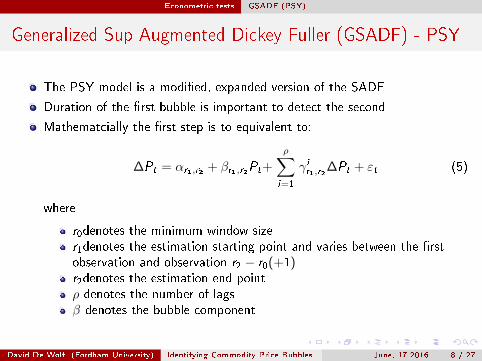

The PSY model is a modi�ed, expanded version of the SADF

Duration of the �rst bubble is important to detect the second

Mathematcially the �rst step is to equivalent to:

∆Pt = αr1,r2 + βr1,r2Pt+

ρ∑i=1

γ i

r1,r2∆Pt + εt (5)

where

r0denotes the minimum window sizer1denotes the estimation starting point and varies between the �rstobservation and observation r2 − r0(+1)r2denotes the estimation end pointρ denotes the number of lagsβ denotes the bubble component

David De Wolf (Fordham University) Identifying Commodity Price Bubbles June, 17 2016 8 / 27

Econometric tests GSADF (PSY)

Generalized Sup Augmented Dickey Fuller (GSADF) - PSY

Estimate an auto regressive model with a null hypothesis: βr1,r2 = 0(no bubble).

The alternative hypothesis is as follows: βr1,r2 > 0 (speculativebubble) in the time series

Test statistic is calculated as: ADF r1,r2 =βr1,r2

SE(βr1,r2)and is used to test

for signi�cance

David De Wolf (Fordham University) Identifying Commodity Price Bubbles June, 17 2016 9 / 27

Econometric tests GSADF (PSY)

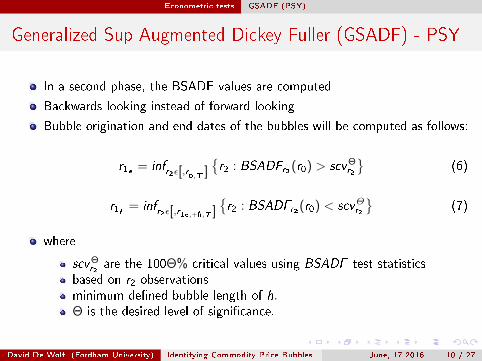

Generalized Sup Augmented Dickey Fuller (GSADF) - PSY

In a second phase, the BSADF values are computed

Backwards looking instead of forward looking

Bubble origination and end dates of the bubbles will be computed as follows:

r1e = infr2ε[,r

0,T ]{r2 : BSADFr2(r0) > scvΘ

r2

}(6)

r1f = infr2ε[,r1e,+h,T ]

{r2 : BSADFr2(r0) < scvΘr2

}(7)

where

scvΘr2

are the 100Θ% critical values using BSADF test statisticsbased on r2 observationsminimum de�ned bubble length of h.Θ is the desired level of signi�cance.

David De Wolf (Fordham University) Identifying Commodity Price Bubbles June, 17 2016 10 / 27

Econometric tests GSADF (PSY)

Generalized Sup Augmented Dickey Fuller (GSADF) - PSY

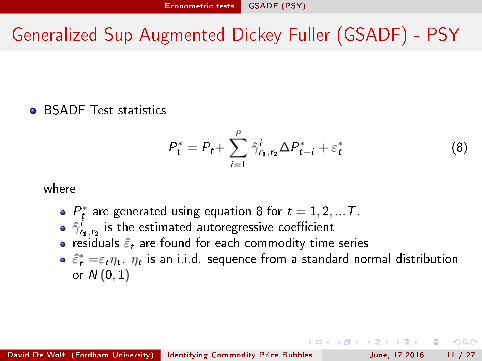

BSADF Test statistics

P∗t = Pt+

ρ∑i=1

γ̂ i

r1,r2∆P∗t−i + ε∗t (8)

where

P∗t are generated using equation 8 for t = 1, 2, ...T .γ̂ ir1,r2 is the estimated autoregressive coe�cientresiduals ε̂t are found for each commodity time seriesε̂∗t =εtηt . ηt is an i.i.d. sequence from a standard normal distributionor N (0, 1)

David De Wolf (Fordham University) Identifying Commodity Price Bubbles June, 17 2016 11 / 27

Econometric tests GSADF (PSY)

Overview SADF/BSADF/GSADF

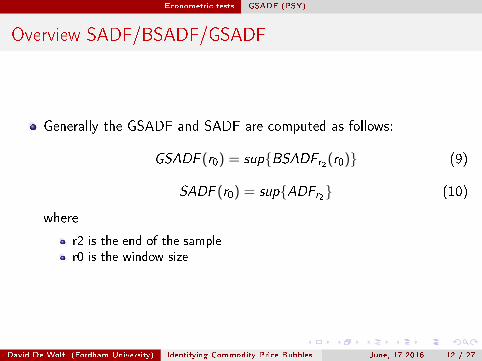

Generally the GSADF and SADF are computed as follows:

GSADF (r0) = sup{BSADFr2(r0)} (9)

SADF (r0) = sup{ADFr2} (10)

where

r2 is the end of the sampler0 is the window size

David De Wolf (Fordham University) Identifying Commodity Price Bubbles June, 17 2016 12 / 27

Results Bubble tests

Introduction to the SADF and GSADF

SADF/ GSADF test statistics and critical values

lagged order of 1

95 % con�dence levels

200 and 500 bootstrapping iterations

Trade o� between daily and weekly observations

David De Wolf (Fordham University) Identifying Commodity Price Bubbles June, 17 2016 13 / 27

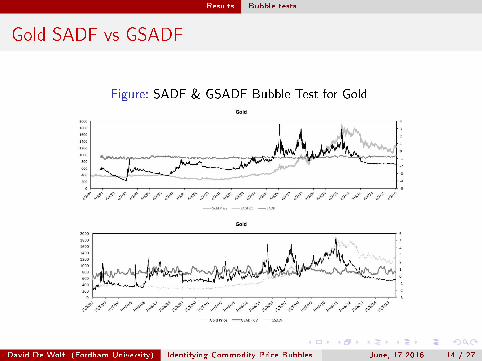

Results Bubble tests

Gold SADF vs GSADF

Figure: SADF & GSADF Bubble Test for Gold

David De Wolf (Fordham University) Identifying Commodity Price Bubbles June, 17 2016 14 / 27

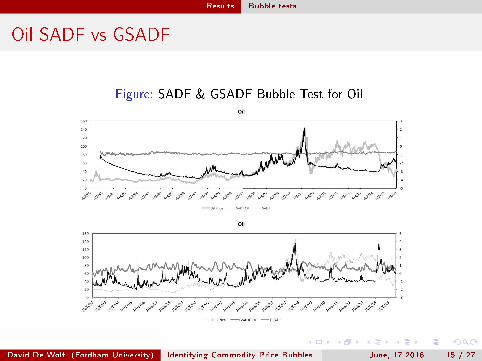

Results Bubble tests

Oil SADF vs GSADF

Figure: SADF & GSADF Bubble Test for Oil

David De Wolf (Fordham University) Identifying Commodity Price Bubbles June, 17 2016 15 / 27

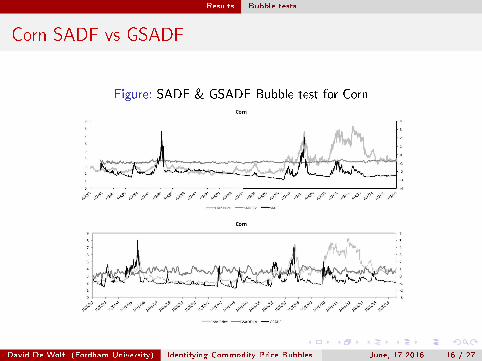

Results Bubble tests

Corn SADF vs GSADF

Figure: SADF & GSADF Bubble test for Corn

David De Wolf (Fordham University) Identifying Commodity Price Bubbles June, 17 2016 16 / 27

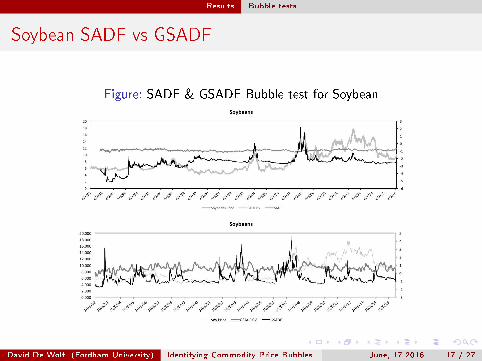

Results Bubble tests

Soybean SADF vs GSADF

Figure: SADF & GSADF Bubble test for Soybean

David De Wolf (Fordham University) Identifying Commodity Price Bubbles June, 17 2016 17 / 27

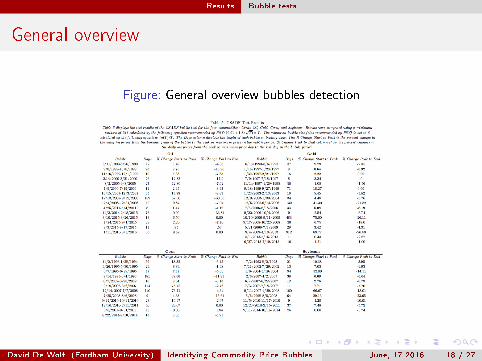

Results Bubble tests

General overview

Figure: General overview bubbles detection

David De Wolf (Fordham University) Identifying Commodity Price Bubbles June, 17 2016 18 / 27

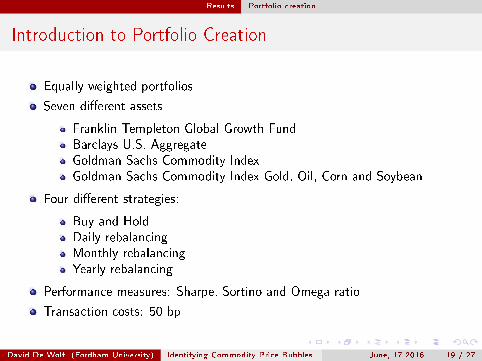

Results Portfolio creation

Introduction to Portfolio Creation

Equally weighted portfolios

Seven di�erent assets

Franklin Templeton Global Growth FundBarclays U.S. AggregateGoldman Sachs Commodity IndexGoldman Sachs Commodity Index Gold, Oil, Corn and Soybean

Four di�erent strategies:

Buy and HoldDaily rebalancingMonthly rebalancingYearly rebalancing

Performance measures: Sharpe, Sortino and Omega ratio

Transaction costs: 50 bp

David De Wolf (Fordham University) Identifying Commodity Price Bubbles June, 17 2016 19 / 27

Results Portfolio creation

Portfolio Description

Portfolio 1: only global equities via the Templeton Global Growth Fund

Portfolio 2: equally weighted portfolio of Global Equities and U.S. FixedIncome securities

Portfolio 3: equally weighted portfolio of Gobal Equities, U.S. Fixed incomeand the Broad Commodity Index

Portfolio 4: equally weighted portfolio of Global Equities, U.S. Fixed incomeand the Gold Commodity Index

Portfolio 5: Equally weighted portfolio of Global Equities, U.S. Fixed incomeand the Gold - , Oil - , Corn - and Soybeans Commodity Index.

Portfolio 6: Equally weighted portfolio made up of the Gold, Oil, Corn, andSoybeans Commodity Indexes

David De Wolf (Fordham University) Identifying Commodity Price Bubbles June, 17 2016 20 / 27

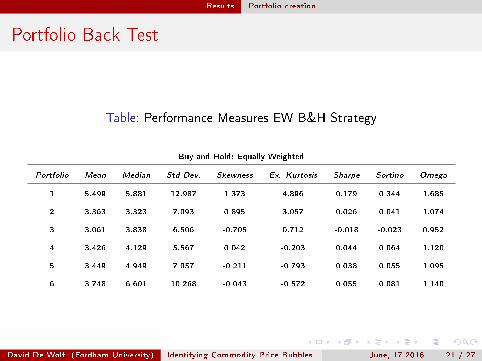

Results Portfolio creation

Portfolio Back Test

Table: Performance Measures EW B&H Strategy

Buy and Hold: Equally Weighted

Portfolio Mean Median Std Dev. Skewness Ex. Kurtosis Sharpe Sortino Omega

1 5.499 5.881 12.987 1.373 4.896 0.179 0.344 1.685

2 3.363 3.323 7.093 0.895 3.057 0.026 0.041 1.074

3 3.061 3.838 6.506 -0.705 0.712 -0.018 -0.023 0.952

4 3.426 4.129 5.567 0.042 -0.203 0.044 0.064 1.120

5 3.449 4.949 7.057 -0.211 -0.793 0.038 0.055 1.095

6 3.748 6.601 10.268 -0.043 -0.572 0.055 0.081 1.140

David De Wolf (Fordham University) Identifying Commodity Price Bubbles June, 17 2016 21 / 27

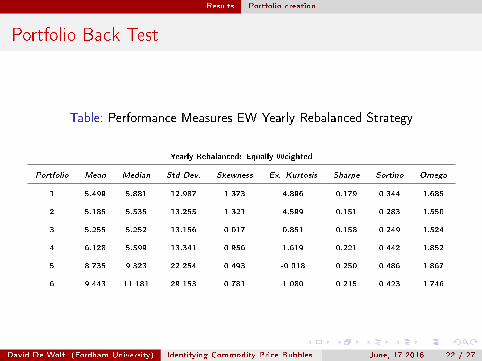

Results Portfolio creation

Portfolio Back Test

Table: Performance Measures EW Yearly Rebalanced Strategy

Yearly Rebalanced: Equally Weighted

Portfolio Mean Median Std Dev. Skewness Ex. Kurtosis Sharpe Sortino Omega

1 5.499 5.881 12.987 1.373 4.896 0.179 0.344 1.685

2 5.185 5.535 13.255 1.321 4.599 0.151 0.283 1.550

3 5.255 5.252 13.156 0.017 0.851 0.158 0.249 1.524

4 6.128 5.599 13.341 0.956 1.619 0.221 0.442 1.852

5 8.735 9.323 22.254 0.493 -0.018 0.250 0.486 1.867

6 9.443 11.181 29.153 0.781 1.080 0.215 0.423 1.746

David De Wolf (Fordham University) Identifying Commodity Price Bubbles June, 17 2016 22 / 27

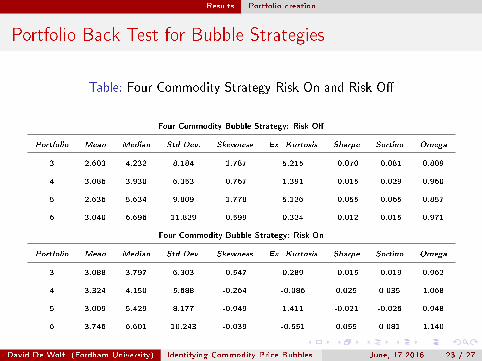

Results Portfolio creation

Portfolio Back Test for Bubble Strategies

Table: Four Commodity Strategy Risk On and Risk O�

Four Commodity Bubble Strategy: Risk O�

Portfolio Mean Median Std Dev. Skewness Ex. Kurtosis Sharpe Sortino Omega

3 2.603 4.232 8.184 -1.787 5.215 -0.070 -0.081 0.809

4 3.086 3.930 6.353 -0.767 1.391 -0.015 -0.029 0.960

5 2.636 5.634 9.809 -1.778 5.126 -0.055 -0.065 0.857

6 3.040 6.696 11.829 -0.599 0.324 -0.012 -0.015 0.971

Four Commodity Bubble Strategy: Risk On

Portfolio Mean Median Std Dev. Skewness Ex. Kurtosis Sharpe Sortino Omega

3 3.088 3.797 6.303 -0.547 0.289 -0.015 -0.019 0.962

4 3.324 4.150 5.688 -0.264 -0.086 0.025 0.035 1.068

5 3.009 5.429 8.177 -0.949 1.411 -0.021 -0.026 0.948

6 3.746 6.601 10.243 -0.039 -0.551 0.055 0.081 1.140

David De Wolf (Fordham University) Identifying Commodity Price Bubbles June, 17 2016 23 / 27

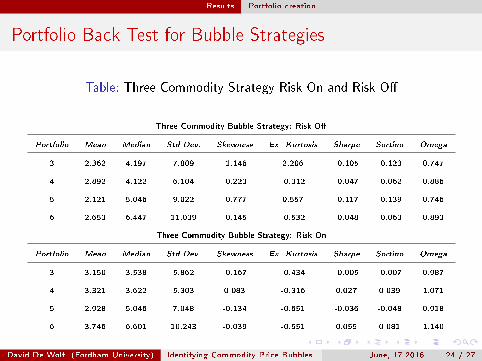

Results Portfolio creation

Portfolio Back Test for Bubble Strategies

Table: Three Commodity Strategy Risk On and Risk O�

Three Commodity Bubble Strategy: Risk O�

Portfolio Mean Median Std Dev. Skewness Ex. Kurtosis Sharpe Sortino Omega

3 2.362 4.197 7.809 -1.146 2.206 -0.105 -0.123 0.747

4 2.892 4.122 6.104 -0.223 -0.312 -0.047 -0.062 0.886

5 2.121 5.046 9.022 -0.777 0.557 -0.117 -0.139 0.746

6 2.653 6.447 11.039 -0.145 -0.532 -0.048 -0.063 0.893

Three Commodity Bubble Strategy: Risk On

Portfolio Mean Median Std Dev. Skewness Ex. Kurtosis Sharpe Sortino Omega

3 3.150 3.538 5.862 -0.167 -0.434 -0.005 -0.007 0.987

4 3.321 3.622 5.303 0.083 -0.316 0.027 0.039 1.071

5 2.928 5.046 7.048 -0.134 -0.651 -0.036 -0.048 0.918

6 3.746 6.601 10.243 -0.039 -0.551 0.055 0.081 1.140

David De Wolf (Fordham University) Identifying Commodity Price Bubbles June, 17 2016 24 / 27

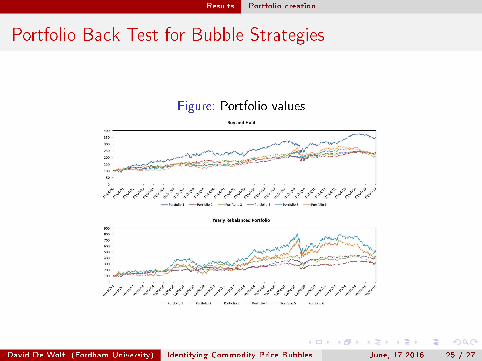

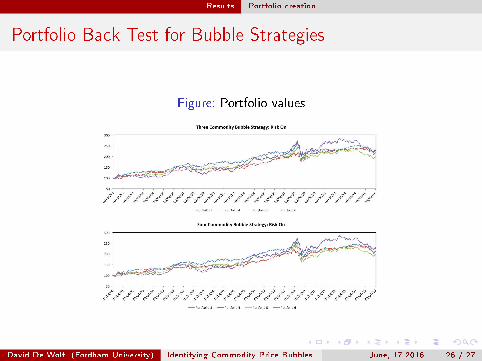

Results Portfolio creation

Portfolio Back Test for Bubble Strategies

Figure: Portfolio values

David De Wolf (Fordham University) Identifying Commodity Price Bubbles June, 17 2016 25 / 27

Results Portfolio creation

Portfolio Back Test for Bubble Strategies

Figure: Portfolio values

David De Wolf (Fordham University) Identifying Commodity Price Bubbles June, 17 2016 26 / 27

Conclusion

Conclusion

Based on the GSADF (PSY Test) we �nd:

17 bubbles in Gold15 bubbles in Oil12 bubbles in Corn11 bubbles in Soybeans

Longest bubble in Gold and lasted for 912 days

Shortest bubble in both Oil as Gold and lasted for 8 days

TC's play an improtant role in portfolio rebalancing

Yearly rebalanced and EW portfolios deliver the best result

Bubble strategies in EW portfolios fail to deliver satisfying results

David De Wolf (Fordham University) Identifying Commodity Price Bubbles June, 17 2016 27 / 27