BUA321 CH13 Capital Structure - TMC Business -...

14

BUA321 CH13 Capital Structure Content Coordinator: Dr. Lawrence Byerly Chapter 13 Study Guide 1. What is the risk return value rule? If risk increases, investors want more returns, so new investors would pay a lower price. Risk up, required return up, value down 2. What is capital structure? Long-term financing 3. What is leverage? The magnification of risk that is realized when we add fixed cost operations and financing to the corporation. a. Describe business risk. The chance that you will be unable to meet the operating obligations of the firm. Created by fixed costs of operations b. Describe financial risk. The chance that you will not be able to meet the financing obligations of the firm. Borrowing and using preferred stock 4. What does break-even mean? Find the point where profits (primarily EBIT) are zero. Helps analyze risk levels of current choices. Can also see what future decisions will have on risk. a. How does this relate to risk? Sets the level of must do performance to get to zero profit. The higher the level the harder to make profit. b. What is contribution margin? P – VC The profit per unit that first covers fixed costs, then designates the profit per unit after FC are covered.

Transcript of BUA321 CH13 Capital Structure - TMC Business -...

BUA321 CH13 Capital Structure

Content Coordinator: Dr. Lawrence Byerly

Chapter 13 Study Guide

1. What is the risk return value rule?

If risk increases, investors want more returns, so new investors would pay a lower price. Risk up, required return up, value down

2. What is capital structure?

Long-term financing

3. What is leverage?

The magnification of risk that is realized when we add fixed cost operations and financing to the corporation.

a. Describe business risk.

The chance that you will be unable to meet the operating obligations of the firm. Created by fixed costs of operations

b. Describe financial risk.

The chance that you will not be able to meet the financing obligations of the firm. Borrowing and using preferred stock

4. What does break-even mean?

Find the point where profits (primarily EBIT) are zero. Helps analyze risk levels of current choices. Can also see what future decisions will have on risk.

a. How does this relate to risk?

Sets the level of must do performance to get to zero profit. The higher the level the harder to make profit.

b. What is contribution margin?

P – VC The profit per unit that first covers fixed costs, then designates the profit per unit after FC are covered.

BUA321 CH13 Capital Structure

Content Coordinator: Dr. Lawrence Byerly

5. The company currently sells the Widget Pro for $17. The variable costs are $12 per

unit. The company currently has modest fixed costs of $500. The managers are

proposing the purchase of a new piece of machinery that will reduce variable

costs to $9. The fixed costs will increase to $2,000.

i. What is the break-even point currently?

100 units 100 * 17 - 100 * 12 -500 = 0

ii. What is the proposed break-even?

250 units

6. What is DOL? DFL? DTL?

Degree of operating leverage – business risk Degree of financial leverage – financial leverage Degree of total leverage – combined effect

17.00$

12.00$

500.00$

100.00

-

Break-Even Units 100.00

Price per Unit

Variable Cost per Unit

Fixed Costs of Operation

Units of Production

Interest Expense

Preferred Dividends

Tax Rate

EBIT

BUA321 CH13 Capital Structure

Content Coordinator: Dr. Lawrence Byerly

Assume that Don Donuts utilizes a new donut hole machine to create edible wonders. This machine will

reduce variable costs to 25 cents per hole. The fixed costs of the new operation is $4,000. The donut

holes currently sell for 75 cents each. In the last year, Don sold 12,000 Donut holes. What is the new

break-even point for the company? What is the estimated EBIT if sales repeat themselves? What is the

DOL?

0.75$

0.25$

4,000.00$

12,000.00

2,000.00$

15.00%

4,999.81

Break-Even Units 8,000.00

Price per Unit

Variable Cost per Unit

Fixed Costs of Operation

Units of Production

Interest Expense

Preferred Dividends

Tax Rate

EBIT

3.00

1.67

5.00

Degree of Operating Leverage

Degree of Financial Leverage

Degree of Total leverage

BUA321 CH13 Capital Structure

Content Coordinator: Dr. Lawrence Byerly

Don’s current interest expense is $2,000. The company’s tax rate is 15%. What is the DFL

and DTL?

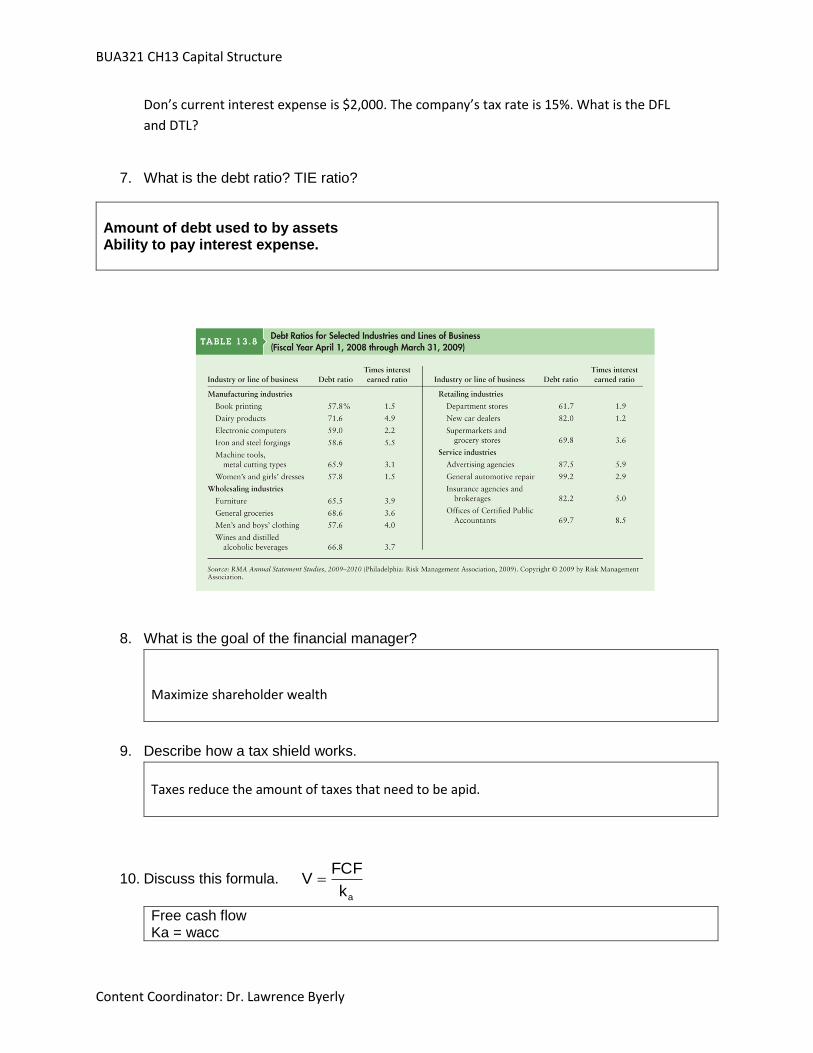

7. What is the debt ratio? TIE ratio?

Amount of debt used to by assets Ability to pay interest expense.

8. What is the goal of the financial manager?

Maximize shareholder wealth

9. Describe how a tax shield works.

Taxes reduce the amount of taxes that need to be apid.

10. Discuss this formula. ak

FCFV

Free cash flow Ka = wacc

BUA321 CH13 Capital Structure

Content Coordinator: Dr. Lawrence Byerly

How can you increase the stock price?

11. Scenario

a. World with NO taxes

i. Who cares?

ii. What happens if we change the capital structure?

No one cares. No taxes. If a company pays you $100, do you care if they call it a dividend payment or an interest payment? What about the company? As we switch to less expensive debt, the cost of equity keeps pace and the WACC dos not change.

b. World with Corporate Taxes

i. Who cares?

ii. What happens if we change the capital structure?

Corporate taxes. If a company pays you $100, do you care if they call it a dividend payment or an interest payment? What about the company? The tax shield provides a benefit to the company.

12. How does the chance of bankruptcy change the amount of debt a company will take?

This adds a cost to borrowing. It increases as we borrow more.

BUA321 CH13 Capital Structure

Content Coordinator: Dr. Lawrence Byerly

13. Capital Structure problem

a. The Sunshine Vacation Company, is preparing to make a capital structure

decision. It has obtained estimates of sales and the associated levels of

earnings before interest and taxes (EBIT) from its forecasting group: There

is a 30% chance that sales will total $600,000, a 40% chance that sales will

total $900,000, and a 30% chance that sales will total $1,200,000. Fixed

operating costs total $300,000, and variable operating costs equal 40% of

sales. These data are summarized, and the resulting EBIT calculated, in the

following table:

b. Currently the company has no debt and $1,000,000 in common stock. There

are 40,000 shares selling at $25. Taxes are currently 40% at the margin.

What does the current capital structure look like?

c. Show the range of capital structures that are possible.

d. The company has been given the following interest rate structure for

borrowing. Prepare an interest expense schedule.

Debt ratio

Cost of debt

0 0%

10 6%

15 8%

30 10%

45 13%

50 15%

60 17%

Debt Ratio Total Assets Debt Equity Shares

0.00% $1,000,000 $0 $1,000,000 40000.00

10.00% $1,000,000 $100,000 $900,000 36000.00

15.00% $1,000,000 $150,000 $850,000 34000.00

30.00% $1,000,000 $300,000 $700,000 28000.00

45.00% $1,000,000 $450,000 $550,000 22000.00

50.00% $1,000,000 $500,000 $500,000 20000.00

60.00% $1,000,000 $600,000 $400,000 16000.00

Est Capital Structure (000's)

BUA321 CH13 Capital Structure

Content Coordinator: Dr. Lawrence Byerly

e. What is the worst-case scenario for EPS? Average? Best?

Interest Rates

Debt Ratio Debt Rate Interest Expense

0.00% $0 0.00% 0.000

10.00% $100,000 6.00% 6,000.000

15.00% $150,000 8.00% 12,000.000

30.00% $300,000 13.00% 39,000.000

45.00% $450,000 13.00% 58,500.000

50.00% $500,000 15.00% 75,000.000

60.00% $600,000 17.00% 102,000.000

Worst

Debt Ratio Interest Expense EBT Taxes NI EPS

0.00% $0 $60,000.00 $24,000.00 $36,000.00 $0.9000

10.00% $6,000 $54,000.00 $21,600.00 $32,400.00 $0.9000

15.00% $12,000 $48,000.00 $19,200.00 $28,800.00 $0.8471

30.00% $39,000 $21,000.00 $8,400.00 $12,600.00 $0.4500

45.00% $58,500 $1,500.00 $600.00 $900.00 $0.0409

50.00% $75,000 -$15,000.00 -$6,000.00 -$9,000.00 -$0.4500

60.00% $102,000 -$42,000.00 -$16,800.00 -$25,200.00 -$1.5750

Lawrence Byerly PhD © 2013 CTRL+SHIFT+B = MAIN MENU

Average

Debt Ratio Interest Expense EBT Taxes NI EPS

0.00% $0 $240,000.00 $96,000.00 $144,000.00 $3.60

10.00% $6,000 $234,000.00 $93,600.00 $140,400.00 $3.90

15.00% $12,000 $228,000.00 $91,200.00 $136,800.00 $4.02

30.00% $39,000 $201,000.00 $80,400.00 $120,600.00 $4.31

45.00% $58,500 $181,500.00 $72,600.00 $108,900.00 $4.95

50.00% $75,000 $165,000.00 $66,000.00 $99,000.00 $4.95

60.00% $102,000 $138,000.00 $55,200.00 $82,800.00 $5.18

Best

Debt Ratio Interest Expense EBT Taxes NI EPS

0.00% $0 $420,000.00 $168,000.00 $252,000.00 $6.30

10.00% $6,000 $414,000.00 $165,600.00 $248,400.00 $6.90

15.00% $12,000 $408,000.00 $163,200.00 $244,800.00 $7.20

30.00% $39,000 $381,000.00 $152,400.00 $228,600.00 $8.16

45.00% $58,500 $361,500.00 $144,600.00 $216,900.00 $9.86

50.00% $75,000 $345,000.00 $138,000.00 $207,000.00 $10.35

60.00% $102,000 $318,000.00 $127,200.00 $190,800.00 $11.93

BUA321 CH13 Capital Structure

Content Coordinator: Dr. Lawrence Byerly

f. Utilize the following table of costs of equity to complete the capital

structure question. The company has a steady cost of equity until a

breaking point at 30%.

g. What is the optimal capital structure for the firm? Is that level also the

maximum EPS? What is the risk level at that point?

This is an important table. What is the debt ratio for maximized profit? Maximized value? Shows that maximizing profit does not necessarily maximize stock price.

Debt ratio

Cost of equity

0 12%

10 12%

20 12%

30 13%

40 14%

50 16.5%

60 19%

EPS

Debt Ratio Worst Average Best

0.00% $0.90 $3.60 $6.30

10.00% $0.90 $3.90 $6.90

15.00% $0.85 $4.02 $7.20

30.00% $0.45 $4.31 $8.16

45.00% $0.04 $4.95 $9.86

50.00% -$0.45 $4.95 $10.35

60.00% -$1.58 $5.18 $11.93

Probability 0.30 0.40 0.30

Debt Ratio Expected EPS Standard Deviation Coefficient of Var. Est. Share Price

0.00% $3.60 2.091$ 0.581$ $30.000

10.00% $3.90 2.324$ 0.596$ $32.500

15.00% $4.02 2.460$ 0.612$ $33.529

30.00% $4.31 2.988$ 0.694$ $33.132

45.00% $4.95 3.803$ 0.768$ $35.357

50.00% $4.95 4.183$ 0.845$ $30.000

60.00% $5.18 5.229$ 1.010$ $27.237

BUA321 CH13 Capital Structure

Content Coordinator: Dr. Lawrence Byerly

14. Describe asymmetric information.

Unequal information. Who should know most about what goes on in the corporation. What things would we like to know but do not want to know??

15. How do managers send signals?

What does borrowing say about the future? What does issuing stock say?

BUA321 CH13 Capital Structure

Content Coordinator: Dr. Lawrence Byerly

BUA321 CH13 exercise HW (47 points) _______ Internet (15 points) ______

Use the EPS – EBIT worksheet to complete the information below:

VC is 40% of sales; fixed costs are $15,000

a. (3)

Interest Rates

Debt Ratio Rate

0.00% 0.00%

10.00% 6.00%

15.00% 8.00%

30.00% 10.00%

45.00% 13.00%

50.00% 15.00%

60.00% 17.00%

Worst Average Best

Probability 0.15 0.5 0.35

Sales $70,000 $100,000 $150,000

Long Term Debt $0

Common Stock $450,000

Book Value of Stock $5.50

Taxes 35.00%

Current Capital Structure (000's)

Debt Ratio (weight) Cost of Equity

0.00% 10.00%

10.00% 10.00%

15.00% 10.00%

30.00% 12.00%

45.00% 14.00%

50.00% 16.00%

60.00% 19.00%

BUA321 CH13 Capital Structure

Content Coordinator: Dr. Lawrence Byerly

Probability

0.30 0.40 0.30

EBIT

b. (5)

Debt Ratio

Amount

of Debt

Amount

of Equity

Number of Shares of

Common Stock*

0%

15%

30%

45%

60%

c (5)

Debt Ratio

Amount

of Debt

Before Tax

Cost of Debt

Annual Interest

0%

15%

30%

45%

60%

d. (9)

Cut and paste table from Excel

Worst Scenario

Average Scenario

Best Scenario

BUA321 CH13 Capital Structure

Content Coordinator: Dr. Lawrence Byerly

e. statistics and share price (5)

cut and paste from excel

Debt ratio Expected EPS Standard

deviation

CV Price

0

15

30

45

60

f. (10)

(1) copy and paste graph with EBIT and EPS

(2) create a graph showing the relationship between the debt ratio and the EPS. Copy and

paste here.

g) (10)

describe what the 2 graphs are illustrating.

BUA321 CH13 Capital Structure

Content Coordinator: Dr. Lawrence Byerly

BUA321 CH13 Research

1) Debt in companies. (15)

Go to www.smartmoney.com

Enter your company’s ticker symbol and go to key statistics.

IN the table below record the data.

Then repeat the exercise for the other companies listed>

Name Ticker symbol ROE LT Debt to Equity

Your company

DIS

AIT

MRK

LG

LUV

TAP

GE

BUD

PFE

What conclusions do reach about the amount of debt for these companies and the return

to the shareholders?

BUA321 CH13 Capital Structure

Content Coordinator: Dr. Lawrence Byerly

2) Using the financial statements you gathered in Chapter 1. (6)

Company name Ticker Symbol

Calculate the company’s

DOL,

DFL

DTL