Bti thursday-luncheon-strand-as-of-11-2

53

Looking Back at the last 50 Years and Forward Toward the Next 50 Bank and Capital Markets Tax Institute November 5, 2015 Rob Strand Senior Economist American Bankers Association

-

Upload

summit-professional-networks -

Category

Business

-

view

495 -

download

0

Transcript of Bti thursday-luncheon-strand-as-of-11-2

Looking Back at the last 50 Years and Forward Toward the Next 50

Bank and Capital Markets Tax Institute

November 5, 2015

Rob StrandSenior EconomistAmerican Bankers Association

Rock ‘n Roll in 1965

Rock ‘n Roll is here to stay!

Source: National Bureau of Economic Research-40

0

40

80

120

Post World War II Business Cycles

Months Expansions

Recessions

Current77 months

Average

Source: U.S. Bureau of Economic Analysis

-1%

0%

1%

2%

3%

4%

1960s 1980s 2000s 2011 2013 2015

Net ExportsGovernmentBusiness InventoriesBusiness InvestmentConsumers

Contributions to Inflation-Adjusted GDP Growth

3 Qtrs

Consumer Spending

-3%

0%

3%

6%

9%

12%

1965 1975 1985 1995 2005 2015

Source: U.S. Bureau of Economic Analysis

throughAugust

Annual Growth

(2.5)

(2.0)

(1.5)

(1.0)

(0.5)

0.0

0.5

1.0

1.5

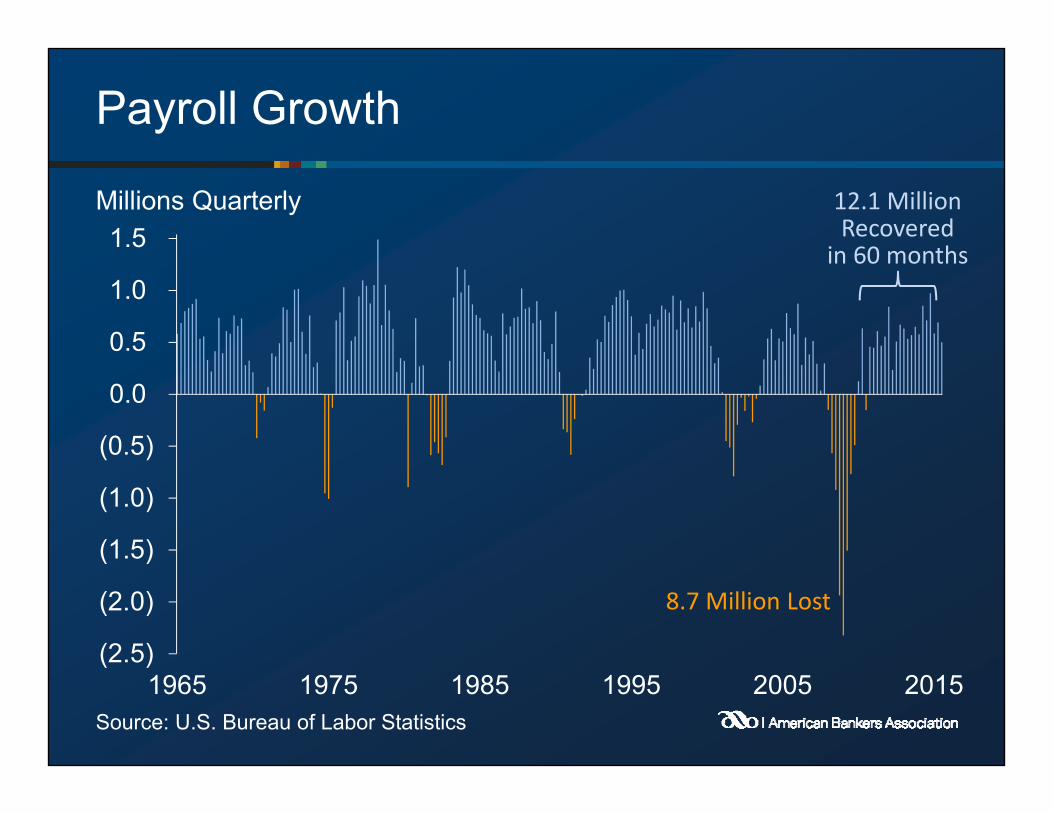

1965 1975 1985 1995 2005 2015Source: U.S. Bureau of Labor Statistics

8.7 Million Lost

12.1 Million Recovered

in 60 months

Payroll Growth

Millions Quarterly

0%

5%

10%

15%

1965 1975 1985 1995 2005 2015

Source: U.S. Bureau of Labor Statistics

Underemployed

10.0%

5.1%Unemployed

Unemployment Rate

10.8%

2¾%—4%

4%—5%

5%—6%

6%—7%

Unemployment Rate

Source: U.S. Bureau of Labor Statistics, September 2015

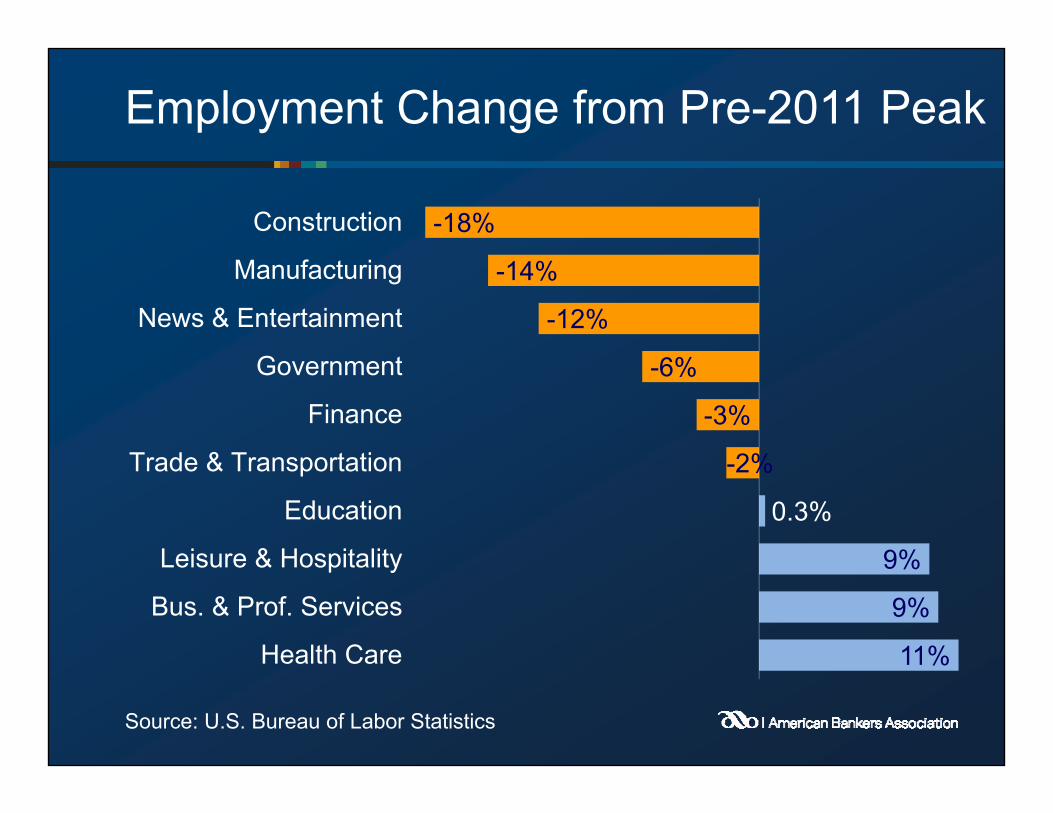

2.9%

2.8%

6.8%

6.7%

6.6%

5.9%

11%

9%

9%

0.3%

-2%

-3%

-6%

-12%

-14%

-18%

Health Care

Bus. & Prof. Services

Leisure & Hospitality

Education

Trade & Transportation

Finance

Government

News & Entertainment

Manufacturing

Construction

Employment Change from Pre-2011 Peak

Source: U.S. Bureau of Labor Statistics

Shifts in Employment Shares by Industry

GovernmentOther

TradeManufacturing

GovernmentOther

Trade

Manufacturing

1965 2015

Source: U.S. Bureau of Labor Statistics

Health Care

Median Annual U.S Household Income

$40,000

$45,000

$50,000

$55,000

$60,000

1965 1975 1985 1995 2005 2015

Source: U.S. Department of the Census

2014 $s

Quintiles of Annual Household Income

$0

$50,000

$100,000

$150,000

$200,000

1965 1975 1985 1995 2005 2015

Source: U.S. Department of the Census

2014 $sTop 5 Percent

Top Quintile

Fourth Quintile

Third QuintileSecond QuintileBottom Quintile

Price of a Gallon of Gas vs. Milk

$1

$2

$3

$4

1995 2000 2005 2010 2015

Premium Gas

Whole Milk

Source: Bureau of Labor Stats, Energy Information Administration

10%

15%

20%

1965 1975 1985 1995 2005 2015

Household Balance Sheets Strengthening

Source: Federal Reserve Flow of Funds

Debt / Assets

Financial Obligation Ratio

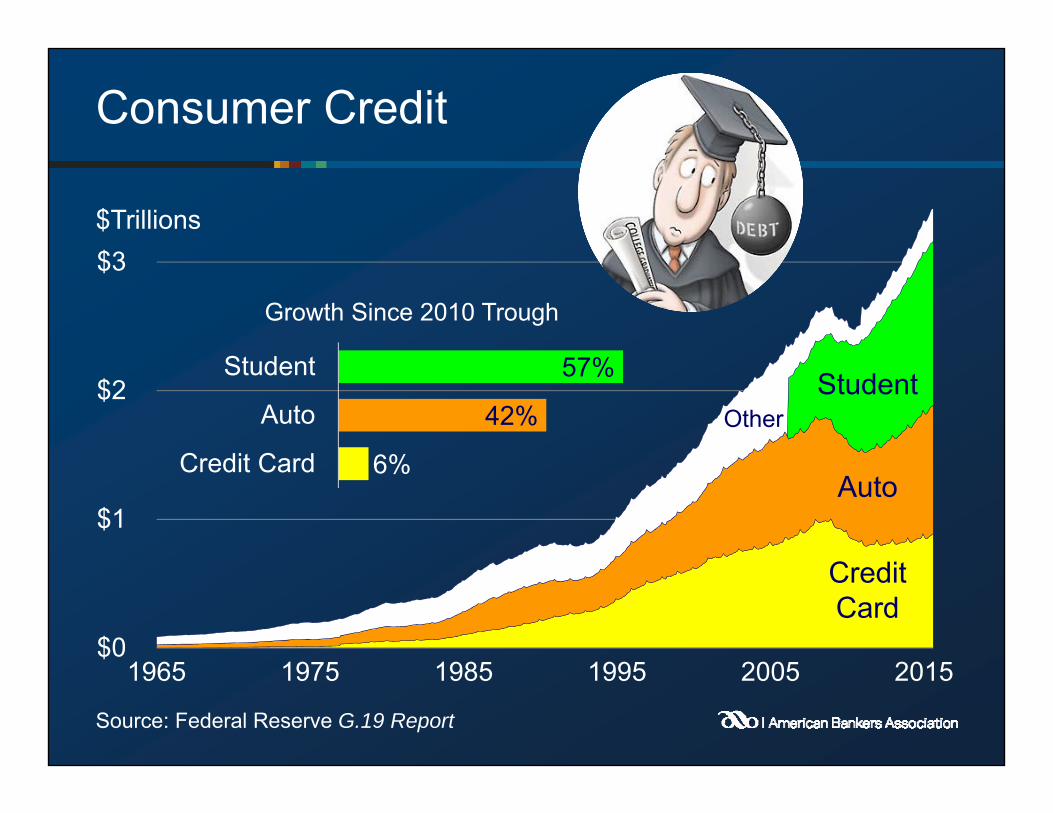

Consumer Credit

Source: Federal Reserve G.19 Report

$0

$1

$2

$3

1965 1975 1985 1995 2005 2015

CreditCard

Auto

StudentOther

6%

42%

57%

Credit Card

Auto

Student

Growth Since 2010 Trough

$Trillions

1965 Pontiac GTO

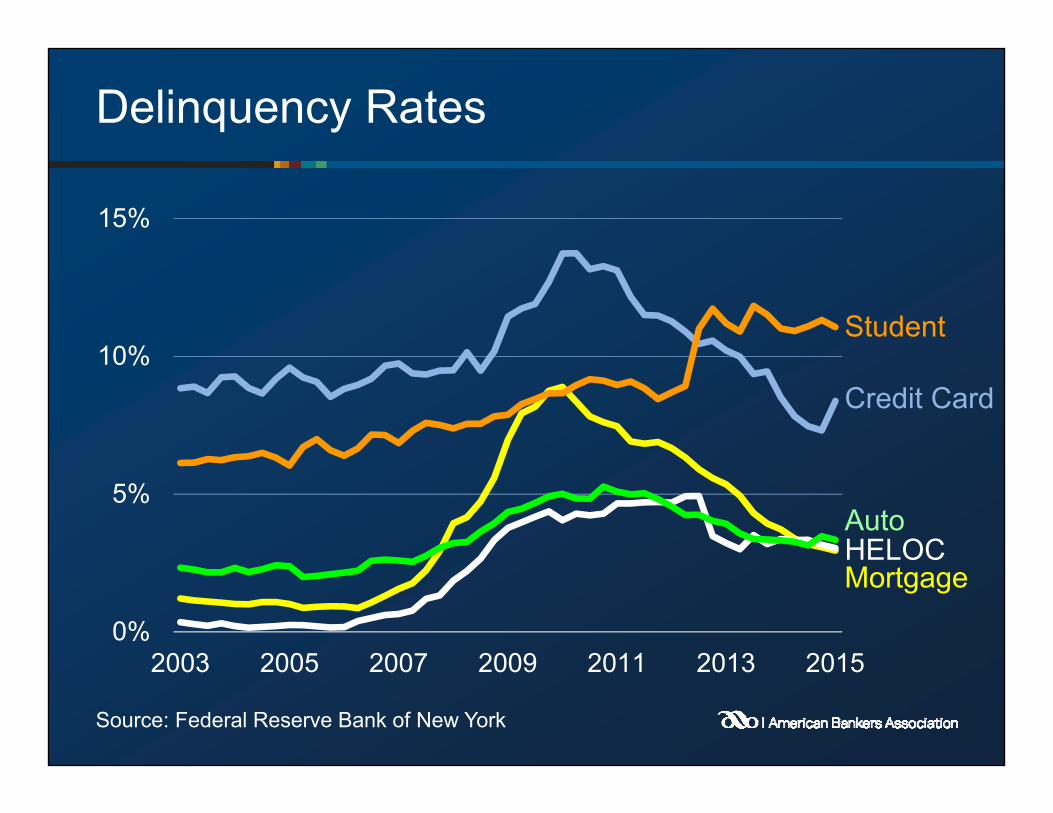

Delinquency Rates

0%

5%

10%

15%

2003 2005 2007 2009 2011 2013 2015

Source: Federal Reserve Bank of New York

Mortgage

Credit Card

HELOCAuto

Student

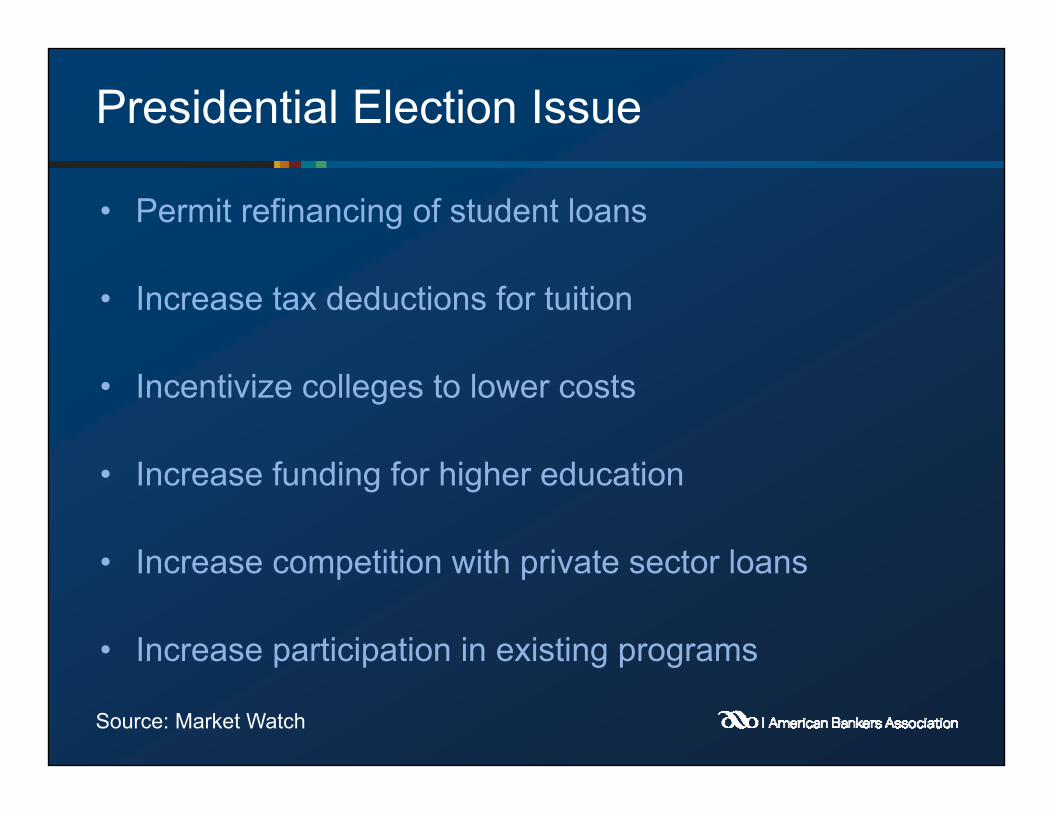

Presidential Election Issue

• Permit refinancing of student loans

• Increase tax deductions for tuition

• Incentivize colleges to lower costs

• Increase funding for higher education

• Increase competition with private sector loans

• Increase participation in existing programs

Source: Market Watch

-4%

0%

4%

8%

12%

16%

1965 1975 1985 1995 2005 2015

Target

Source: U.S. Bureau of Labor Statistics

Consumer Price Inflation

-1%

0%

1%

2%

3%

4%

2014 2015 2016 2017 2018

Federal Funds Rate Forecast (Year End)

Sources: Federal Reserve, Chicago Mercantile Exchange (10/23)

FF Futures

Periods of Major Federal Reserve Tightening

0%

1%

2%

3%

4%

5%

6%

7%

-1 1 3 5 7 9 11 13 15 17 19 21 23 25

Fed

Fund

s Ta

rget

Rat

e

Months Since Tightening Began

1994 2004

2000

Source: Federal Reserve

Yield Spreads Shrink when the Fed Tightens

0%

3%

6%

9%

1990 1995 2000 2005 2010 2015

Tightening Began

Source: Federal Reserve

10-Year Bonds

3-Month Bills

Conventional 30-Year Mortgage Rate

0%

5%

10%

15%

20%

1965 1975 1985 1995 2005 2015

Source: Federal Reserve

3.8%

Home Sales

0

3

6

9

2000 2005 2010 2015

Millions of UnitsSAAR

Sources: U.S. Census Bureau, National Association of Realtors

New Homes

Existing Homes

Home Price Changes

-12%

-8%

-4%

0%

4%

8%

12%

16%

1975 1980 1985 1990 1995 2000 2005 2010 2015

Source: Case-Shiller National Index

Through August

0.0

0.5

1.0

1.5

1965 1975 1985 1995 2005 2015

Housing Starts

Source: U.S. Census Bureau

Millions of Units

Single Family

Multi-Unit

Home Flipping

Source: Albuquerque Journal

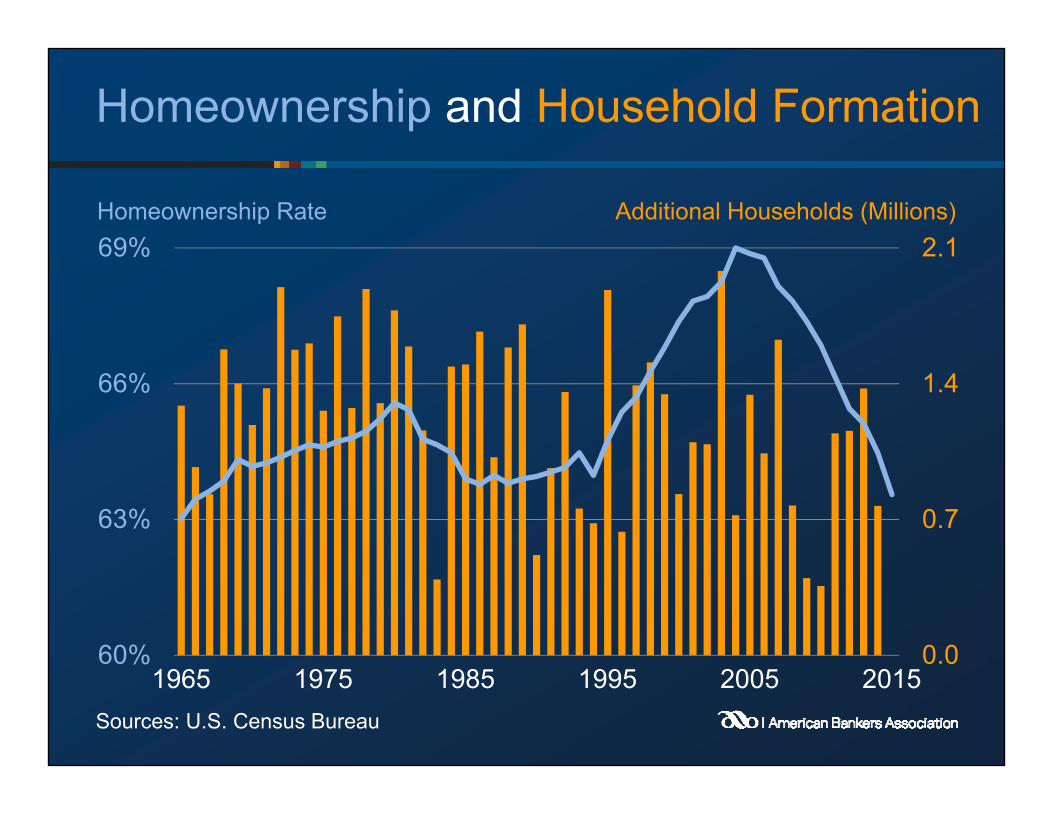

Homeownership and Household Formation

0.0

0.7

1.4

2.1

60%

63%

66%

69%

1965 1975 1985 1995 2005 2015Sources: U.S. Census Bureau

Additional Households (Millions)Homeownership Rate

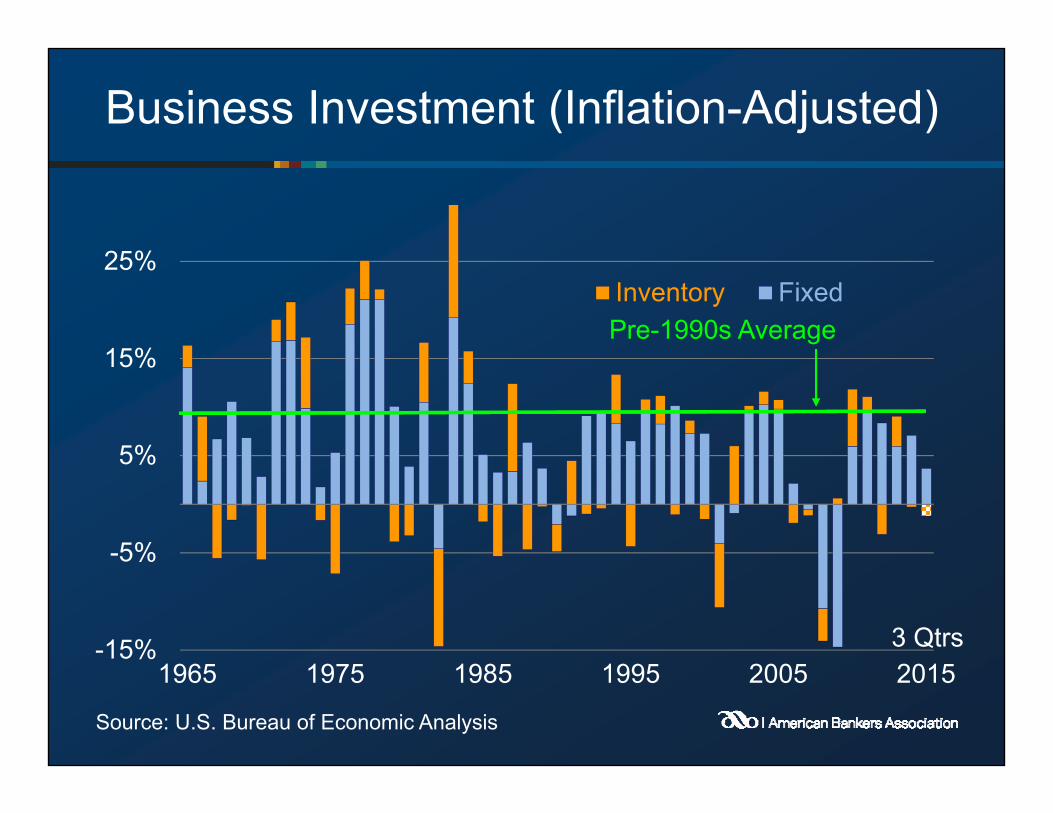

Business Investment (Inflation-Adjusted)

-15%

-5%

5%

15%

25%

1965 1975 1985 1995 2005 2015

Inventory Fixed

Source: U.S. Bureau of Economic Analysis

3 Qtrs

Pre-1990s Average

Labor Productivity Growth

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

1960s 1980s 2000s 2011 2013 2015

Source: Bureau of Labor Statistics

FirstHalf

Business Indexes

20

40

60

80

100

120

25

35

45

55

65

75

1965 1975 1985 1995 2005 2015

Industrial Production

Contraction Expansion

ISM Manufacturing

Sources: Federal Reserve, Institute for Supply Management

ISM Non-Manufacturing

50

Growth of Corporate Profits

Source: U.S. Bureau of Economic Analysis

$0.0

$0.6

$1.2

$1.8

1965 1975 1985 1995 2005 2015

Other TradeFinancial Manufacturing

With inventory valuation and capital consumption adjustments, SAAR, $Trillions

First Half

Small Business Sentiment

0

10

20

30

40

0

30

60

90

120

1985 1990 1995 2000 2005 2010 2015

Sources: National Federation of Independent Business

Index of Small Business Optimism (left axis)

– Outlook for Expansion Chief Concern: – Regulations – Labor Quality (right axis)

Commercial Real Estate Price Index

Source: Green Tree Advisors Commercial Property Price Index

0

30

60

90

120

1998 2000 2002 2004 2006 2008 2010 2012 2014

11.6% Annual Growth Since Mid-2009

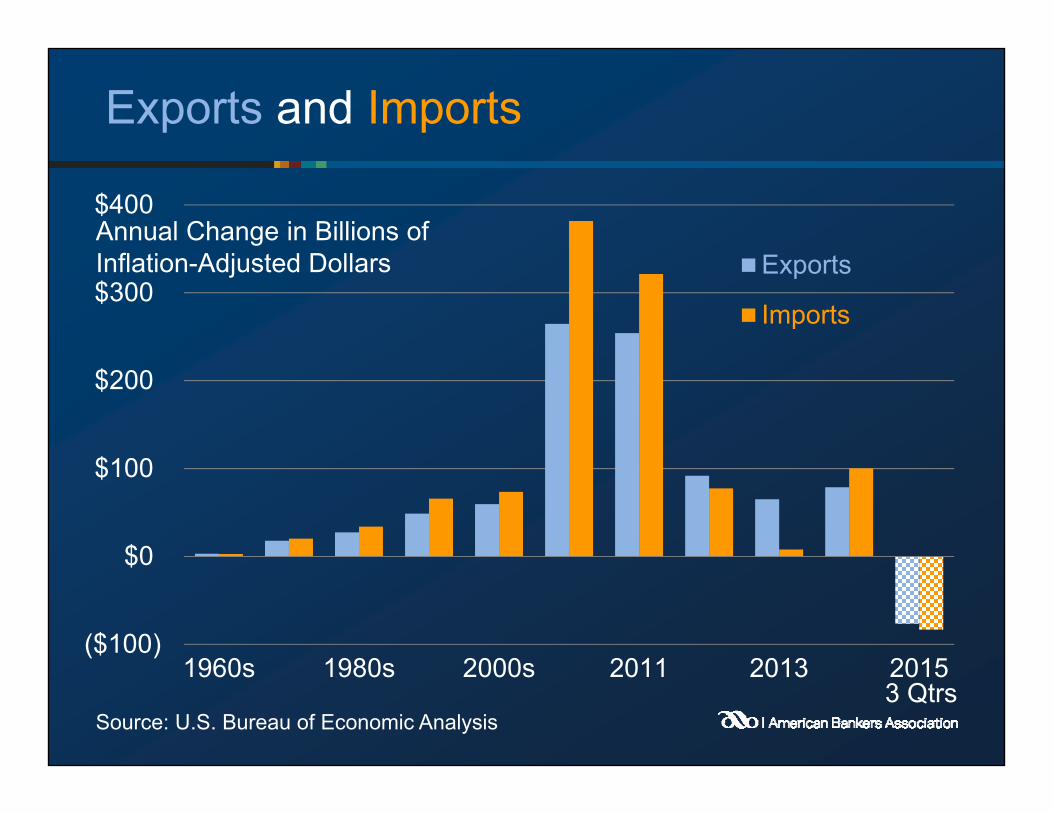

Exports and Imports

($100)

$0

$100

$200

$300

$400

1960s 1980s 2000s 2011 2013 2015

Exports

Imports

Source: U.S. Bureau of Economic Analysis3 Qtrs

Annual Change in Billions of Inflation-Adjusted Dollars

Crude Oil Exports

0

100

200

300

400

500

1965 1975 1985 1995 2005 2015

Source: U.S. Energy Information Administration

Thousands of Barrels per Day

Major Currency Trade-Weighted U.S. Dollar

60

90

120

150

1973 1979 1985 1991 1997 2003 2009 2015Source: Federal Reserve

1973=00

U.S. Exports

$248

$172

$134

$82

$56

$33

$32

$19

European Union

Canada

Mexico

China

Japan

South Korea

Brazil

India

All other

U.K. Germ Fra IT

$466

Source: U.S. Bureau of Economic Analysis

Billions of Dollars in the First Half of 2015

100

120

140

160

180

1995 2000 2005 2010 2015

Gross Domestic Product (Inflation-Adjusted)

Sources: U.S. Bureau of Economic Analysis and OECD

Index (1995=100)

US

France

Japan

CanadaMexico

UK

Germany

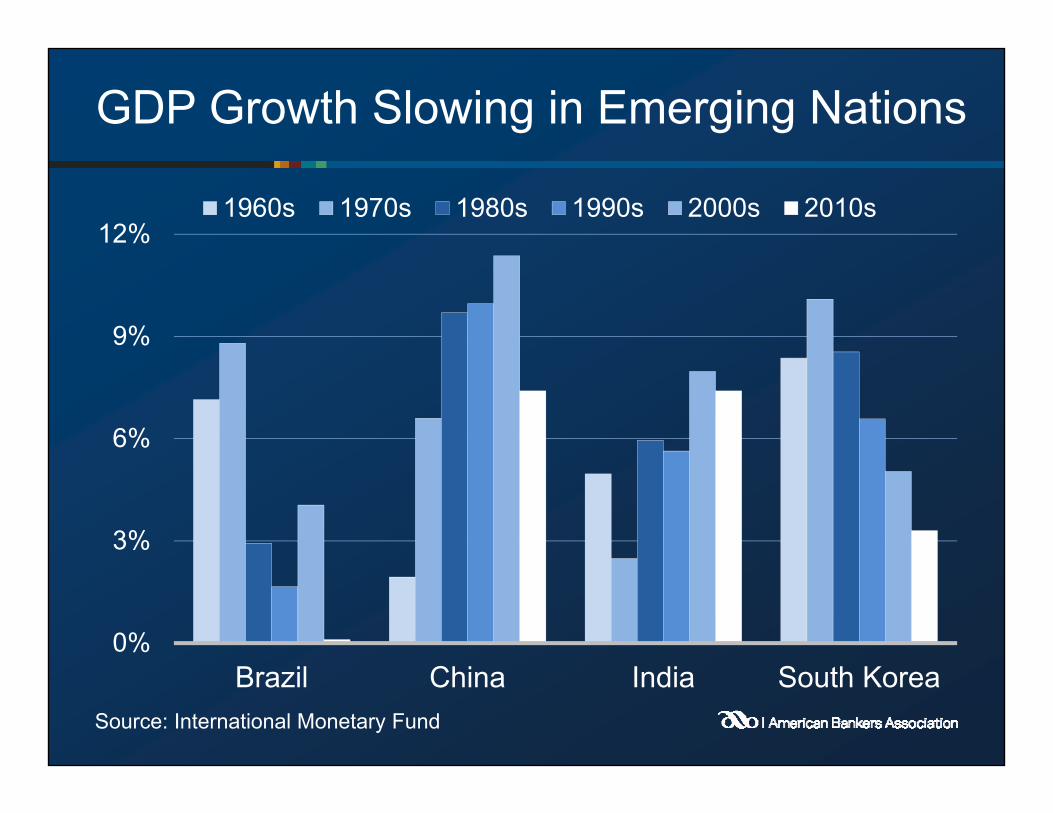

GDP Growth Slowing in Emerging Nations

0%

3%

6%

9%

12%

Brazil China India South Korea

1960s 1970s 1980s 1990s 2000s 2010s

Source: International Monetary Fund

Government Spending (Inflation-Adjusted)

-5%

0%

5%

10%

15%

1965 1975 1985 1995 2005 2015

State and Local Federal

Source: U.S. Bureau of Economic Analysis

3 Qtrs

Growth Rate

Federal Receipts, Outlays and Deficit

0%

20%

40%

60%

80%

1965 1975 1985 1995 2005 2015 2025

Receipts

Outlays

Forecast

Percent of GDP

Source: CBO Long-Term Budget Outlook (August 2015)

FederalDeficit

Medicare and Medicaid were chartered in 1965

Long-Term Structural Imbalance

The long-term fiscal problem cannot be solved by:

• a growing economy,

• eradicating fraud, waste and abuse,

• pulling U.S. troops out of the Middle East and cutting defense,

• restraining discretionary spending, and

• eliminating Congressional earmarks.

Source: U.S. Congressional Budget Office

Conclusion: Stress Points

• Concentration of Income and Wealth• Fed Lift-off and Interest Rates• Housing Recovery• Student Debt• Business Capital Formation• Foreign Economies• Government Finances

U.S. Inflation-Adjusted GDP Growth

‐3%

0%

3%

6%

9%

1965 1975 1985 1995 2005 2015

Source: U.S. Bureau of Economic Analysis

FirstHalf

0

500

1000

1500

2000

2005 2007 2009 2011 2013 2015

S&P 500 Index

Source: Standard & Poor’s

Up 167%in 6½ years

U.S. Traditional Advantages

• Highly diverse economy

• Robust entrepreneurial culture

• Flexible capital and labor markets

→ Technological leader

→ Strong global competitor

Patent Applications

0

200,000

400,000

600,000

1965 1975 1985 1995 2005

Source: U.S. Patent and Trademark Office

2015

![bti[1]- huka](https://static.fdocuments.us/doc/165x107/577d26f41a28ab4e1ea2a579/bti1-huka.jpg)