Brighter opportunities beyond the shadow of the dollar Richard Adams – Client Portfolio Manager...

21

Brighter opportunities beyond the shadow of the dollar Richard Adams – Client Portfolio Manager For professional investors only September 2015

-

Upload

hope-marshall -

Category

Documents

-

view

217 -

download

0

Transcript of Brighter opportunities beyond the shadow of the dollar Richard Adams – Client Portfolio Manager...

Brighter opportunities beyond the shadow of the dollarRichard Adams – Client Portfolio ManagerFor professional investors only

September 2015

Learning objectives

Identify macroeconomic factors that can inform investment strategy choices

Understand how rising interest rates might impact the active vs passive debate

Identify areas of US market that may benefit despite dollar strength

2

Brighter opportunities beyond the shadow of the dollar

3

“So far every single person that’s bet against America has lost money, because we always come back.”Bill Clinton, Speech to the Democratic National Convention, 5 September 2012.

Near-term outlook

Strong dollar

Question mark over valuations

Improving consumer spending

Long-term outlook

Most dynamic and innovative economy

Positive demographics

Strong legal, regulatory and corporate governance framework

4

Dollar strength: threat or opportunity?

Impacts

Exporters > importers

Market > economy

Large > small companies

Opportunities

Consumers

Secular themes

Active managers

Overseas investorsSource: Columbia Threadneedle Investments.

Is the US market expensive?

5

Source: Bloomberg, as at 30 June 2015. Source: Bloomberg, as at 30 June 2015.

60 63 66 69 72 75 78 81 84 87 90 93 96 99 02 05 08 11 140

5

10

15

20

25

30

35

S&P 500 trailing 12 month P/E...

Average quarterly level

84 86 88 90 92 94 96 98 00 02 04 06 08 10 12 140%

2%

4%

6%

8%

10%

12%

14%

S&P 500 Earnings Yield US 10 Year Treasury Yield

S&P 500 trailing 12 month P/E ratio Earnings yield vs bond yield

6

Is the US market expensive?

Region Index 2015 P/E 2016 P/E 2015 P/CF 2016 P/CF

United Kingdom FTSE 100 15.1x 13.7x 9.3x 8.5x

Europe MSCI Europe 15.0x 13.7x 8.9x 8.2x

United States S&P 500 16.1x 14.7x 11.3x 10.2x

Japan TOPIX 13.5x 12.4x 7.6x 7.3x

Asia ex Japan MSCI AC Asia ex Japan 11.2x 10.1x 7.4x 6.7x

Source: Bloomberg, as at 8 Sep 2015.

7

Is the US market expensive?

Source: Bloomberg, as at 30 June 2015. Yellow line indicates current CPI vs S&P500 trailing P/E (at 30 June 15).

-2% 0% 2% 4% 6% 8% 10% 12% 14% 16%5

10

15

20

25

30

September 1987

March 1980

June 1971

March 2009

December 1999

CPI vs. S&P500 Trailing P/Es Quarterly data since 1960

CP

I

S&P P/E

8

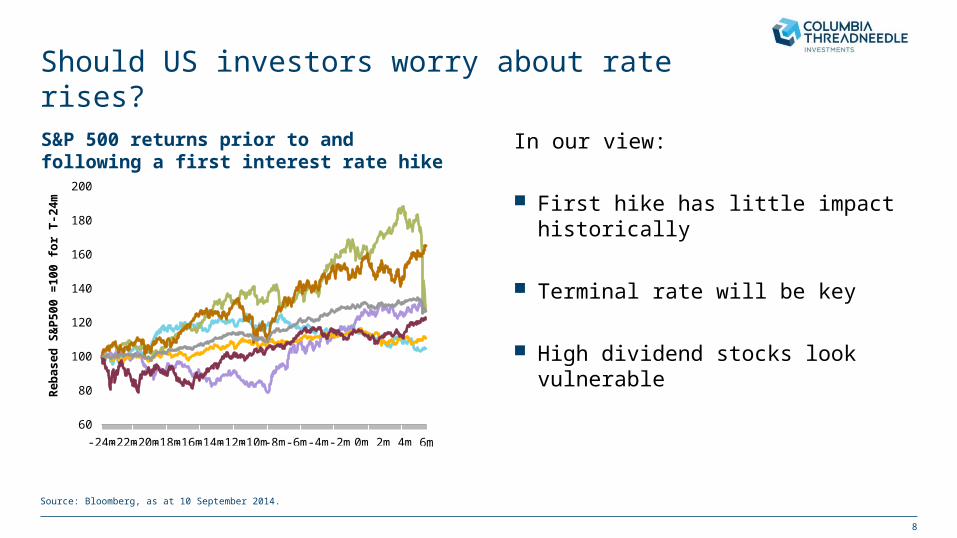

Should US investors worry about rate rises?

In our view:

First hike has little impact historically

Terminal rate will be key

High dividend stocks look vulnerable

Source: Bloomberg, as at 10 September 2014.

-24m-22m-20m-18m-16m-14m-12m-10m-8m-6m-4m-2m 0m 2m 4m 6m60

80

100

120

140

160

180

200

1977 1983 1987 1994 1999

Re

ba

se

d S

&P

50

0 =

10

0 f

or

T-2

4m

S&P 500 returns prior to and following a first interest rate hike

Implications of higher interest ratesVolatility

9

Jun 10 Jun 11 Jun 12 Jun 13 Jun 14 Jun 1550

60

70

80

90

100

110

120

130

140

150

VVIX Index Moving 200 day average

Expectations of rates rises have increased the frequency of market sell-offs

Market panics can create opportunities to invest in “superior” growth companies

Tactical shorting can add alpha

Source: Bloomberg, as at 10 July 2015.

VVIX Index June 2010 to July 2015

10

Implications of higher interest ratesExcess returns

1961 1968 1975 1982 1989 1996 2003 20100

2

4

6

8

10

12

14

16

-30

-20

-10

0

10

20

30

40

50

60

70

80

10-year treasury yieldActive fund excess return (median)

10-y

ear

trea

sury

yie

ld (

%)

Cu

mu

lative excess return

(%)

Treasury yields and cumulative excess returns are 0.91 correlated historically

Higher rates widen differences in corporate profitability

An active stock picking approach can profit

Source: Nomura Securities, as at 31 December 2014.

US active fund excess return vs. rate environment

11

How long will the recovery last?

Source: BEA, Haver Analytics, DB Global Markets Research, as at 30 June 2015.

-4 -3 -2 -1 0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 2390

95

100

105

110

115

120

125

Average of last 5 cycles Current business cycle

“0” represents the recession end date

Q2 2015

Real GDP (Q1 1958 to Q2 2015, pre-recession peak = 100)

12

A health check on the driver of global growth

90 92 94 96 98 00 02 04 06 08 10 12 1450%

60%

70%

80%

90%

100%

Ho

us

eh

old

de

bt:

GD

P

(%)

Source: Bloomberg, as at 30 June 2015.

Import costs

Energy costsLabour market

Household finances

Dec 13 Mar 14 Jun 14 Sep 14 Dec 14 Mar 15 Jun 155.0

5.5

6.0

6.5

7.0

Un

emp

loym

ent

rate

(%

)

Dec 13 Mar 14 Jul 14 Oct 14 Jan 15 Apr 1575

80

85

90

95

100

105

Do

llar

in

dex

Dec 13 Mar 14 Jul 14 Oct 14 Jan 15 Apr 1540

60

80

100

120

WT

I Cru

de

oil

fu-

ture

s (

$)

13

63 67 71 75 79 83 87 91 95 99 03 07 11 15200

400

600

800

1,000

1,200

1,400

Th

ou

san

ds

Averagemonthly level

US housingA question of supply and demand

Supply side

Stronger bank balance sheets

Relaxation of tight lending standards

Low new home inventories

Demand side

Household formation below trend

Good housing affordability

Improving wages and employment

Source: Lombard Street Research , as at 30 June 2015. The mention of specific stocks is not a recommendation to deal.

Annual US new homes sales

14

Disruptive innovationIdentifying winner and losers

The mention of specific stocks is not a recommendation to deal.

Investment optionsSecular growth of e-commerce

15

Biotechnology R&D renaissance

The mention of specific stocks is not a recommendation to deal.

Recent trends

Advances in statistical techniques

Large pharma less willing to bear R&D risk

Niche treatments offer good pricing power

Specialised stock research is key

16

Demographics are destiny

Source: US Census Bureau, December 2014.The mention of specific stocks is not a recommendation to deal.

Growing workforce

Positive birth rate

Better dependency ratio than most economies

US and China population pyramids for 2015 and 2050

Learning outcomes

Identify how macroeconomic factors can inform investment strategy choices Views on the dollar, volatility, and rates can influence the type of equity strategy investors may prefer

Understand how rising interest rates might impact the active vs passive debate Higher rates can create divergences for active stock pickers to explore

Identify areas of US market that may benefit despite dollar strength Rising consumer incomes Recovering housing market Disruptive innovators Biotechnology R&D renaissance Constructive demographics

17

18

Broad strategy palette with $11bn AuMUS Equities range, Columbia Threadneedle Investments (EMEA)

Source: Columbia Threadneedle Investments, as at 30 June 2015.1 The numbers indicated represent typical values under normal market conditions.

Strategy Strategy Focus Representative FundTracking error

target1 Stock holdings1 Benchmark Structure Strategy AuM Lead manager

Core and Core Plus

Diversified exposure to world’s largest

economy

Threadneedle American Fund

2-6% 60-80 S&P 500 OEIC & SICAV $7,595mNadia Grant/ Diane Sobin

Equity Income3% dividend yield with capital growth upside

potential

Threadneedle US Equity Income Fund

2-6% 50-70 S&P 500OEIC

(UK only)$124m

Diane Sobin/ Nadia Grant

High AlphaBest ideas from across

style & market cap ranges

Threadneedle American Select Fund

4-8% 50-60 S&P 500 OEIC & SICAV $1,797mDiane Sobin/ Nadia Grant

Small CapExploiting higher

growth, less efficient opportunities

Threadneedle American Smaller Companies Fund

4-8% 70-90 S&P 400 Midcap OEIC $948m Diane Sobin

Extended Alpha130/30 strategy with

60% extra gross investment power

Threadneedle American Extended

Alpha Fund4-8%

Long: 40-80 Short: 40-80

S&P 500 OEIC $359mNeil Robson/

Ashish Kochar

US Equities investment team

19

US Equities Team profile – Columbia Threadneedle Investments (EMEA)

Nine investment professionals within the with 18 years’ average industry experience

Diverse professional and academic backgrounds

Significant accumulated experience of living and working in the US

Additional resources

28 US industry specialists based in New York and Boston

Columbia Threadneedle Investments has over 450 investment professionals globally, covering all markets and asset classes

Source: Columbia Threadneedle Investments, as at 30 June 2015.1 Attached to the Global team. 2 Co-portfolio manager.

Long/Short strategies

Diane Sobin, CFA Head of US Equities Fund Manager Sectors: Energy 32 years’ experience

Nadia Grant, CFA Fund Manager Sectors: Healthcare 15 years’ experience

Neil Robson¹ Fund Manager 29 years’ experience

Ashish Kochar1,2

Fund Manager 10 years’ experience

Brad Colton Portfolio Analyst Sectors: Financials & Healthcare 18 years’ experience

Amit Kumar, CFA Portfolio Analyst Sectors: Consumer & Technology 8 years’ experience

Nicolas Janvier, CFA Fund Manager Sectors: Materials, Consumer & Utilities 15 years’ experience

Stéphane Jeannin, CFA Portfolio Analyst Sectors: Technology & Telecommunications 17 years’ experience

Benedikt Blomberg, CFA Portfolio Analyst Sectors: Industrials 19 years’ experience

Richard Adams Client Portfolio Manager 14 years’ experience

Learning outcomes

Identify how macroeconomic factors can inform investment strategy choices Views on the dollar, volatility, rates can influence the type of equity strategy investors may prefer

Understand how rising interest rates might impact the active vs passive debate Higher rates can create divergences for active stock pickers to explore

Identify areas of US market that may benefit despite dollar strength Rising consumer incomes Recovering housing market Disruptive innovators Biotechnology R&D renaissance Constructive demographics

20

21

Important notesFor internal use by Professional and/or Qualified Investors only (not to be used with or passed on to retail clients)

Past performance is not a guide to future performance. The value of investments and any income is not guaranteed and can go down as well as up and may be affected by exchange rate fluctuations. This means that an investor may not get back the amount invested.

This material is for information only and does not constitute an offer or solicitation of an order to buy or sell any securities or other financial instruments, or to provide investment advice or services.

Threadneedle Investment Funds ICVC (“TIF”), Threadneedle Investment Funds II ICVC (“TIF II”) and Threadneedle Specialist Investment Funds ICVC (“TSIF”) are open-ended investment companies structured as umbrella companies incorporated in England and Wales, authorised and regulated in the UK by the Financial Conduct Authority (FCA) as a UCITS scheme.

Subscriptions to a Fund may only be made on the basis of the current Prospectus and the Key Investor Information Document, as well as the latest annual or interim reports and the applicable terms & conditions. Please refer to the ‘Risk Factors’ section of the Prospectus for all risks applicable to investing in any fund. The above documents for TIF and TSIF are available in English, French, German, Portuguese, Italian, Spanish and Dutch (no Dutch Prospectus), Swedish (for the Key Investor Information Document only), for TIF II in English only, and may be obtained free of charge on request from Columbia Threadneedle Investments, Client Services department PO Box 10033, Chelmsford, Essex CM99 2AL.

The research and analysis included in this document has been produced by Columbia Threadneedle Investments for its own investment management activities, may have been acted upon prior to publication and is made available here incidentally. Any opinions expressed are made as at the date of publication but are subject to change without notice and should not be seen as investment advice. Information obtained from external sources is believed to be reliable but its accuracy or completeness cannot be guaranteed.

This presentation and its contents are confidential and proprietary. The information provided in this presentation is for the sole use of those attending the presentation. It may not be reproduced in any form or passed on to any third party without the express written permission of Columbia Threadneedle Investments. This presentation is the property of Columbia Threadneedle Investments and must be returned upon request.

Issued by Threadneedle Investment Services Limited. Registered in England and Wales, Registered No. 3701768, Cannon Place, 78 Cannon Street , London EC4N 6AG, United Kingdom. Authorised and regulated in the UK by the Financial Conduct Authority.

Columbia Threadneedle Investments is the global brand name of the Columbia and Threadneedle group of companies