BRAZILIAN AGRIBUSINESS -...

36

BRAZILIAN AGRIBUSINESS March, 2007

Transcript of BRAZILIAN AGRIBUSINESS -...

BRAZILIAN AGRIBUSINESS

March, 2007

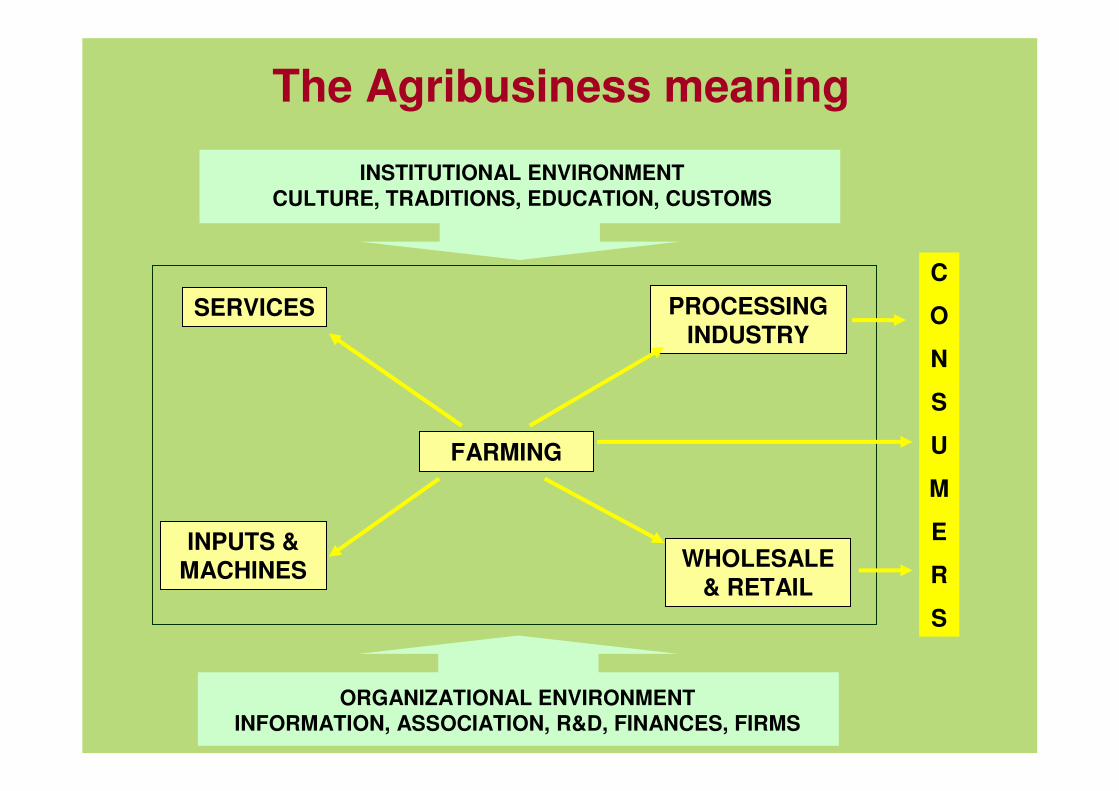

FARMING

WHOLESALE& RETAIL

PROCESSINGINDUSTRY

INPUTS &MACHINES

SERVICESC

O

N

S

U

M

E

R

S

INSTITUTIONAL ENVIRONMENTCULTURE, TRADITIONS, EDUCATION, CUSTOMS

ORGANIZATIONAL ENVIRONMENTINFORMATION, ASSOCIATION, R&D, FINANCES, FIRMS

The Agribusiness meaning

JOBS - 2005

37%

GDP - 2005

27.9%

Total: US$ 796 bi

Agribusiness: US$ 222.1 biAgriculture: US$ 156.1 bi (70.3%)Livestock: US$ 66.0 billion (29.7%)

Non-Agribusiness: US$ 573.9 bi

Agribusiness was responsible for:

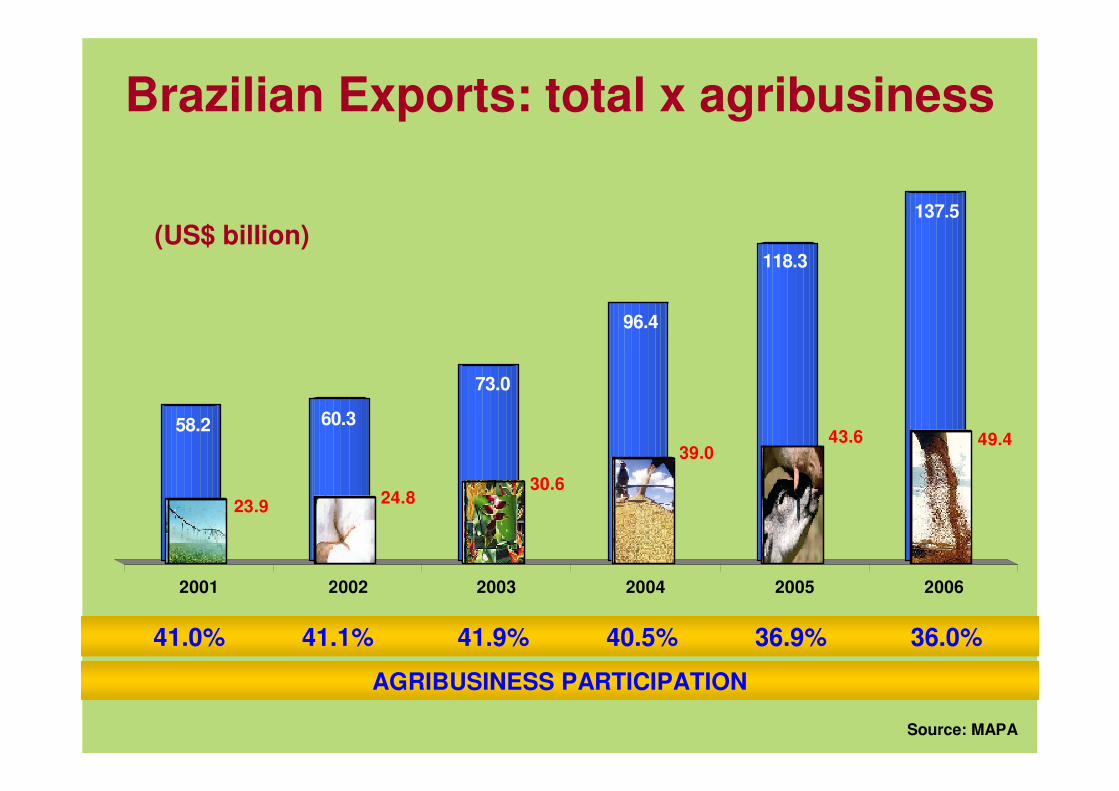

EXPORTS - 2006

Total: US$ 137.5 bi

Agribusiness US$ 49.4 bi

Non-Agribusiness US$ 88.1 bi

36%

Sources: CEPEA-USP/CNA, MAPA and IPEA

137.5

118.3

96.4

73.0

60.358.249.443.6

39.0

30.624.823.9

2001 2002 2003 2004 2005 2006

(US$ billion)

Brazilian Exports: total x agribusiness

Source: MAPA

AGRIBUSINESS PARTICIPATION

41.0% 41.1% 41.9% 40.5% 36.9% 36.0%

Brazil – Japan Trade Flow

�������������� ������� ���������

0

1

2

3

4

5

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

U S

$

b i

l l i

o n

TOTAL EXPORTS TOTAL IMPORTS AGRI EXPORTS AGRI IMPORTS

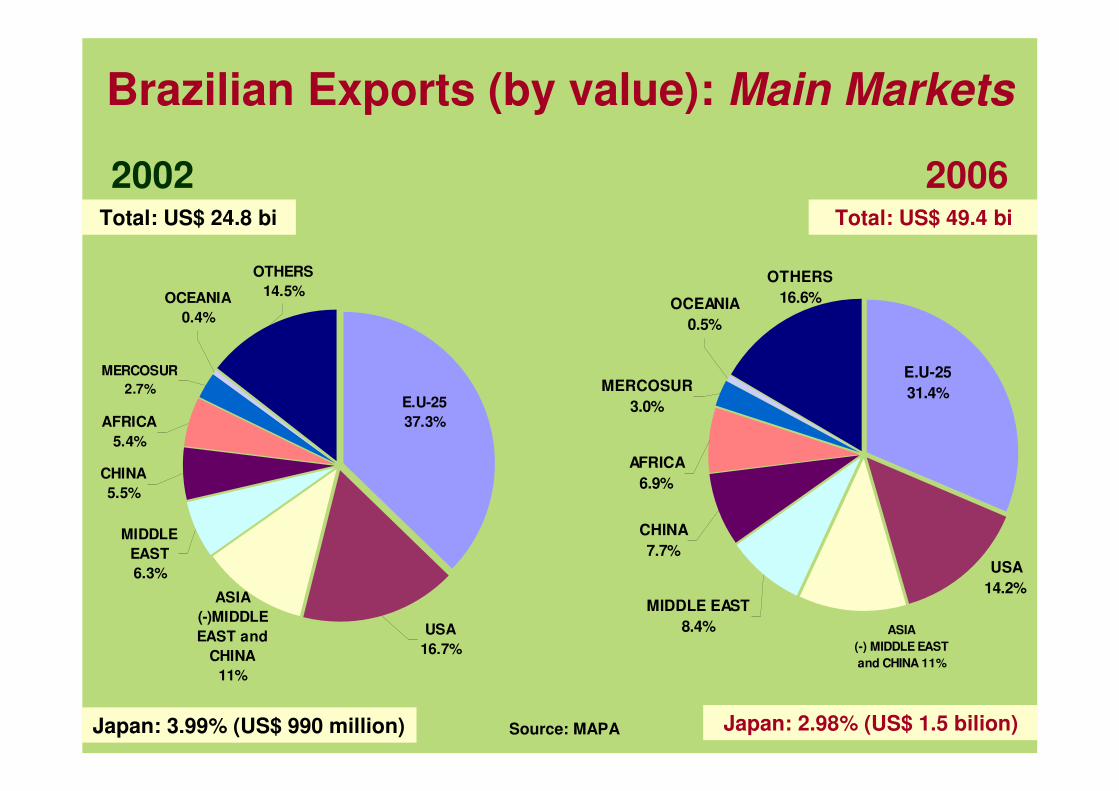

E.U-2537.3%

USA16.7%

ASIA(-)MIDDLE EAST and

CHINA11%

MIDDLE EAST6.3%

OCEANIA0.4%

OTHERS14.5%

CHINA5.5%

AFRICA5.4%

MERCOSUR2.7%

E.U-2531.4%

USA14.2%

ASIA(-) MIDDLE EAST and CHINA 11%

MIDDLE EAST8.4%

OCEANIA0.5%

OTHERS16.6%

CHINA7.7%

AFRICA6.9%

MERCOSUR3.0%

Brazilian Exports (by value): Main Markets

Source: MAPA

20062002

Japan: 3.99% (US$ 990 million) Japan: 2.98% (US$ 1.5 bilion)

Total: US$ 24.8 bi Total: US$ 49.4 bi

Coffee6.8%

Leather and Products

7.0%

Sugar and Alcohol15.7%

Wood and Products

15.9%

Beef17.5%

Soy Complex18.8%

Others8.7%

Textile Products2.8%

Tobacco3.5%

Fruits Juice3.2%

Coffee5.6%

Leather and Products

9.4%

Sugar and Alcohol

9.1%

Wood and Products

17.2%

Beef12.9%

Soy Complex24.2%

Others9.7%

Textile Products

3.5%

Tobacco4.1%

Fruits Juice4.4%

Source: MAPA

Brazilian Exports (by value): Main Products

2002 2006

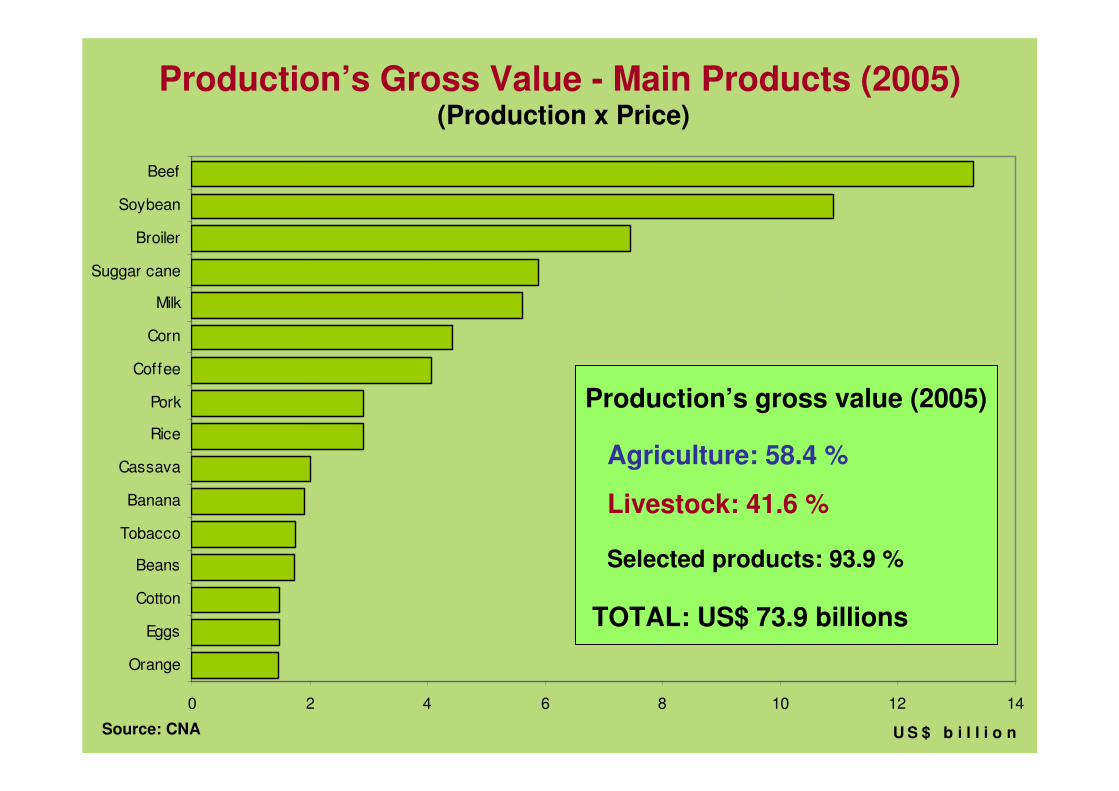

0 2 4 6 8 10 12 14

Orange

Eggs

Cotton

Beans

Tobacco

Banana

Cassava

Rice

Pork

Coffee

Corn

Milk

Suggar cane

Broiler

Soybean

Beef

U S $ b i l l i o n

Production’s Gross Value - Main Products (2005)

Production’s gross value (2005)

Agriculture: 58.4 %

Livestock: 41.6 %

TOTAL: US$ 73.9 billions

Selected products: 93.9 %

Source: CNA

(Production x Price)

Source: Conab / MAPA * Estimate (5th Grain Harvest Survey: February/2007)

Grain Production

GRAINS: cotton, peanut, rice, oats, rye, barley, beans, sunflowers, castor bean, corn, soy, sorgum, wheat and triticale.

45.547.349.047.443.9

40.237.837.836.935.036.637.038.539.135.638.537.9

126.5

57.9

68.4 68.376.0

81.173.6

78.4 76.682.4 83.0

100.3

96.7

123.2 119.1

113.9

120.7

90/91 91/92 92/93 93/94 94/95 95/96 96/97 97/98 98/99 99/00 00/01 01/02 02/03 03/04 04/05 05/06 06/07*

A r

e a

and

P r

o d

u c

t i o

n

( m i

l l i

o n

o f

h a

a n

d

t o n

)

AREA: + 20%

PRODUCTION: + 118.5%

PRODUTIVIDADE: + 86.7%

Meat Production

* Estimate

Sources: ABEF, ABIEC and ABIECS

8,900

5,200

9,200

3,411

2,830

1,330

1.000

2.000

3.000

4.000

5.000

6.000

7.000

8.000

9.000

10.000

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006*

P r

o d

u c

t i o

n

( t

h o

u s

a n

d

t o n

)

Beef: 71%

Pork: 113%

Broiler: 170%

0

2

4

6

8

10

12

14

16

18

20

22

24

26

28

30

32

90/91 91/92 92/93 93/94 94/95 95/96 96/97 97/98 98/99 99/00 00/01 01/02 02/03 03/04 04/05 05/06 06/07*

P r

o d

u c

t i o

n

( m i

l l i

o n

t o

n

a n

d m

³ )

Sugar and Alcohol Production

Sources: SPAE / MAPA and Conab / MAPA * Estimate (3rd Sugar Cane Harvest Survey: November/2006)

SUGAR: + 328.6%

ALCOHOL: + 46.7%

0

10

20

30

40

50

90/9

1

91/9

2

92/9

3

93/9

4

94/9

5

95/9

6

96/9

7

97/9

8

98/9

9

99/0

0

00/0

1

01/0

2

02/0

3

03/0

4

04/0

5

05/0

6

06/0

7

07/0

8*

P R

O D

U C

T I

O N

m

i l l

i o

n s

a c

k s

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

A R

E A

m

i l l

i o

n h

a

Coffee Production

PRODUCTION: + 4.2%

Soures: USDA and EMBRAPA / Conab (after 1996) * Projection (1st Coffee Harvest Survey: December/2006)

AREA: - 38.2%

Ranking 2006: Production and Exports

Total Exports

US$ milhões

Suggar 1st 1st 113 6,167

Coffee 1st 1st 134 3,364

Orange Juice 1st 1st 82 1,469

Soy Complex 2nd 1st 74 9,308

Beef 2nd 1st 144 3,923

Tobacco 2nd 1st 114 1,752

Alcohol 2nd 1st 40 1,605

Broiler 3rd 1st 145 3,203

Corn 3rd 4th 34 460

Pork 4th 4th 72 1,036

ExportsNumber of

MarketsMain

ProductsProduction

Sources: USDA and F.O. Litch’s Preliminary data

AGROENERGY: THE NEW PARADIGM OF WORLD

AGRICULTURE

Coal

Oil

Natural Gas

Hydro Nuclear

Other

Modern Biomass

Biomass (firewood)

0

10

20

30

40

50

60

70

80

90

100

1850 1900 1950 2000 2050 2100

�����

21st Century: the beginning of a New Era

Sources: Nakícenovic, Grübler and MaConald, 1998

�

We are here

Challenge for mankind: TO DIVERSIFY ENERGY SOURCES

Why BIOFUELS?

Economic aspects- new component of the demand

- impacts on trade balance

Renewability- short production cycle

- man-controlled process

Social aspects- jobs creation

- income deconcentration

Environmental gains- carbon capture- lower emission levels in consumption

Brazilian energetic matrix - 2005

WORLD: Renewable Sources 13.3%

Petroleum andderivatives

38.7%

Natural Gas9.4%

Coal 6.3%

Uranium 1.2%

Other renewablesources

2.9%

Hydroelectricity14.8%

Wood 13.0%

Sugar cane13.8%

Source: BEN 2006100% = 218,6 million tep

BRAZIL: Renewable Sources 44.5%

Biomass: 26.8%

Brazilian Experience: nowadays…

1) Since 2003, models of Flex-Fuel Vehicles can use any mixture of gasoline and alcohol.

2) More than 2.7 million flex-fuel vehicles.

� economic viability� social justice

� environmental sustainability

Ministry of Agriculture, Livestockand Food Supply’s Mission:

to promote agribusiness’ sustainable development and competitiveness in benefit of the Brazilian society.

2% 3% 4% 5%8%

17%

21% 22%

30%

34%

58%

NewZeland

Brazil Australia Russia* China* USA Mexico Canada OCDE EuropeanUnion

Japan

Producer Subsidy Equivalent (PSE)Average (2002-2004)

* Average 2002-2003Source: OCDE

World:

� forced labour = 12,300,000 people (ILO)

Brazil:

� 4,273 rural workers in forced labour in 2005

� 17,700,000 people working in agribusiness

The ILO 2005 Report considered Brazil as an example on fight against forced labour

Forced labour exploitation is a crime in Brazil

Legal Amazon X Amazon Biome

Sources: IBGE / MMA / MAPA

: 5.2 million km2 (61%*)

: 4.2 million km2 (49%*)

* Percentage in relationto Brazilian territory

In 2005, 4.9% of the total soy plantingarea in Brazil were located within the

Amazon Biome. This arearepresented less than 0.3% of the

total Amazon Biome area.Amazon Biome

Legal Amazon

Soy Production - Amazon Biome (2005)

Amazon Biome

Others Biomes

Source: CONAB / IBGE / INPE / MMA / SIPAM / ADA

Ellaborated by: CONAB / DIGEM / SUINF / GEOTE

Areas that are responsible for approximately70% of soy production in the Legal Amazon

Gross tax of deforestation reduction in the Amazon

* Estimate

Source: Ministry of Environment

-

5.000

10.000

15.000

20.000

25.000

30.000

00\01 01\02 02\03 03\04 04\05 05\06*

km2/year

Years

- 31%

- 30%

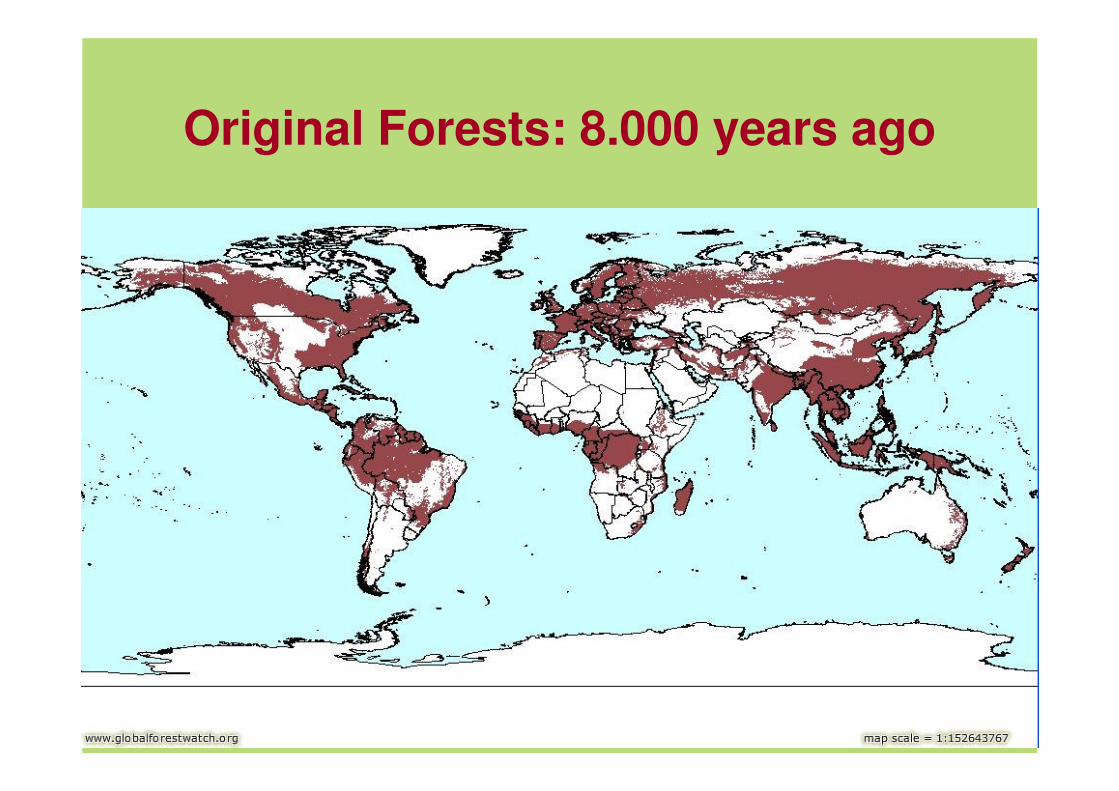

Original Forests: 8.000 years ago

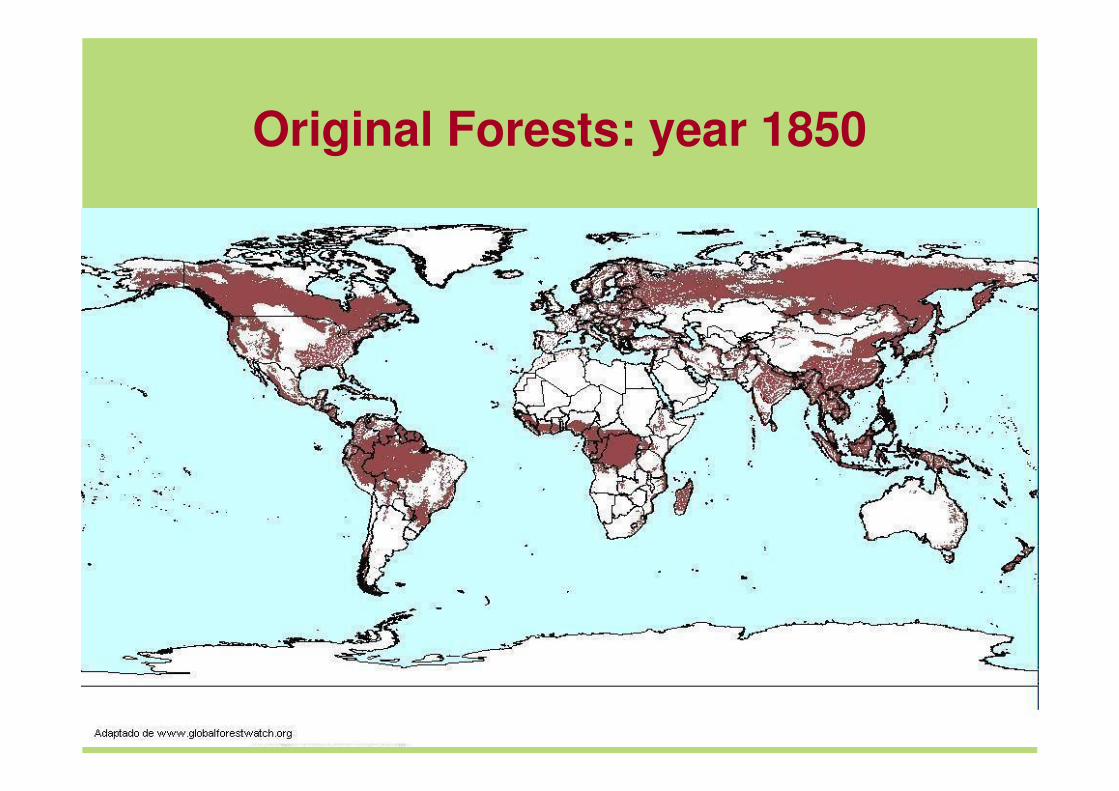

Original Forests: year 1850

Original Forests: year 1950

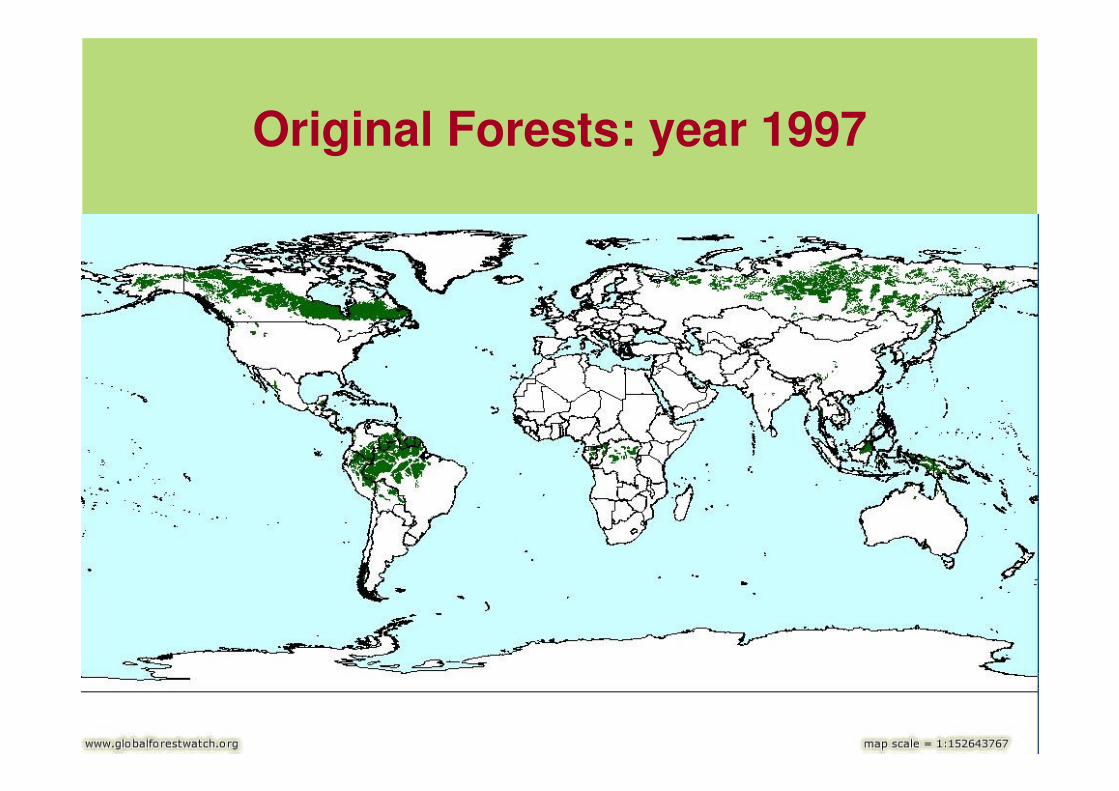

Original Forests: year 1997

Original Forests(1000 km²)

B.P.: Before Present

Original Forest

8000 B.P. % 1000 % 1650 % 1850 % 1950 % Currently %

African 6,799 100 6,459 95 5,779 85 5,099 75 2,380 35 527 7.8

Asia 15,132 100 13,619 90 11,349 75 8,323 55 3,783 25 844 5.6

North America 10,877 100 10,333 95 9,245 85 8,158 75 5,439 50 3,737 34.4

Central America 1,779 100 1,743 98 1,334 75 890 50 712 40 172 9.7

South America 11,709 100 11,592 99 11,475 98 11,124 95 8,196 70 6,412 54.8

Russian 11,759 100 10,583 90 9,407 80 7,055 60 5,880 50 3,448 29.3

Europe 4,690 100 3,752 80 1,407 30 469 10 235 5 14 0.3

Oceania 1,431 100 1,402 98 1,288 90 1,073 75 716 50 319 22.3

World 64,176 100 59,484 92.7 51,285 79,9 42,190 65.7 27,339 42.6 15,473 24.1

Brazil 6,304 100 6,241 99 6,178 98 5,989 95 5,043 80 4,378 69.4

������������ ������

��������

� Land availability: Pasture area = 220 million ha

� Appropriate climate:Up to three harvests during thesame season

� Technology for tropical agriculture

� Qualified human resources

� Public Policies

Potential

Territorial distribution - estimate

(million ha)

851TOTAL

91Non exploited areas stillavailable for agriculture

38Other types of usage

722Subtotal

5Cultivated forests

20Cities, lakes and roads

15Perennial crops

47Yearly crops

55Protect areas

220Pasture

360Amazon Forest

Sustainable Production

Sources: IBGE and ConabAdaptation: MAPA

Potential of Production

Brazilian Livestock

Potential area - 72 million ha

Livestock Area Productivity Livestock Area Productivity

(million heads) (million ha) (head/ha) (million heads) (million ha) (head/ha)

207 220 0.94 207 148 1.4*

2005 Estimate

* Average SP

Sources: IBGE and IEA / SP

�������������

���

AMAZONREGION

TOTAL AREA WITHOUT ENVIRONMENTALRESTRICTIONS . . . . . . . . . . . .

437,2 MM hectares

AREA WITH SLOPEABOVE 12% . . . . . . . . . . . . . . 75,6 MM hectares

TOTAL AVAILABLE ANDSUITABLE LAND . . . . . . . . . . 361,6MM hectares

PANTANAL

How to expand sustainable sugar-cane production?

Current number: 360 units

Estimate for 2010: 77 new units

Plants / distilleries:

POTENTIAL AREAS

2

4

6

8

10

12

14

16

2001 2002 2003 2004 2005

m i

l l i

o n

BOVINE (heads) PASTURE (ha) SUGAR-CANE (ha)

Fonte: Instituto de Economia Agrícola / SP

7,0%

-2,5%

22,1%

São Paulo State: The expansion of sugar-cane

(Head/ha) -(2001)1.27

(2005)1.4

Source: Instituto de Economia Agrícola / SP

7%

- 2.5%

22.1%

Challenges

� Liberalization of world agricultural trade.

Agricultural protectionism: it hampers the growth and the diversification of agricultural activities.

With a greater trade liberalization Brazil would be able to develop a more diversified agribusiness.

� Infrastructure: agribusiness expansion implies bulkyinvestments.

Lucky chances for private investments

Ministry of Agriculture, Livestockand Food Supply

www.agricultura.gov.br