Brazil Oil & Gas Growth prospects and new regulation José Luis Villanueva, Director Brazil Energy...

24

Brazil Oil & Gas Growth prospects and new regulation José Luis Villanueva, Director Brazil Energy Conference Brazilian-American Chamber of Commerce

-

Upload

kianna-gaskin -

Category

Documents

-

view

217 -

download

0

Transcript of Brazil Oil & Gas Growth prospects and new regulation José Luis Villanueva, Director Brazil Energy...

Brazil Oil & GasGrowth prospects and new regulation

José Luis Villanueva, Director

Brazil Energy ConferenceBrazilian-American Chamber of Commerce

Agenda

Global Oil Picture

Trends in Emerging Markets

Brazil’s Position within Latin America

Brazil: Growth Prospects and New Regulation

www.fitchratings.com 3

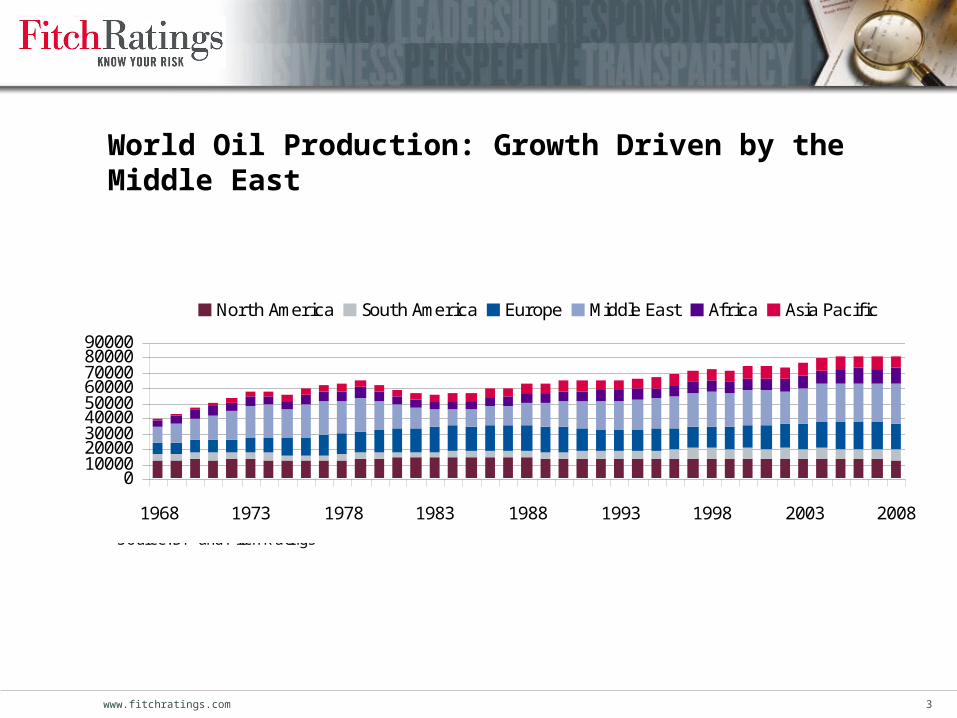

World Oil Production: Growth Driven by the Middle East

0100002000030000400005000060000700008000090000

1968 1973 1978 1983 1988 1993 1998 2003 2008

North America South America Europe Middle East Africa Asia Pacific

Source: BP and Fitch Ratings

(thousand barrels per day)

www.fitchratings.com 4

World Oil Consumption: Growth Driven by Asia Pacific

0100002000030000400005000060000700008000090000

1968 1973 1978 1983 1988 1993 1998 2003 2008

North America South America Europe Middle East Africa Asia Pacific

Source: BP and Fitch Ratings

(thousand barrels per day)

www.fitchratings.com 5

Oil Surplus in Middle East, Africa and South America

-20,000

-15,000

-10,000

-5,000

0

5,000

10,000

15,000

20,000

25,000

NorthAmerica

SouthAmerica

Europe Middle East Africa Asia Pacific

Tho

usan

d ba

rrel

s of

oil

per

day

1978 1988 1998 2008

Sources: BP and Fitch Ratings

www.fitchratings.com 6

World Oil Proved Reserves Concentrated in ME

0250500750

100012501500

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

North America South America Europe Middle East Africa Asia Pacific

Source: BP and Fitch

(billion barrels)

Agenda

Global Oil Picture

Trends in Emerging Markets

Brazil’s Position within Latin America

Brazil: Growth Prospects and New Regulation

www.fitchratings.com 8

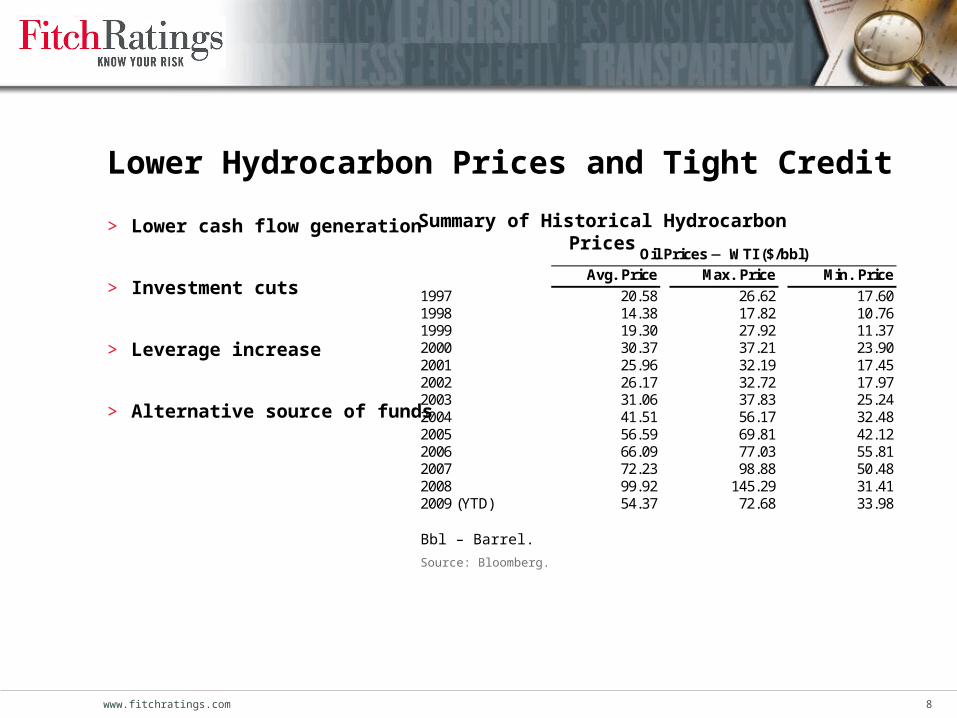

Lower Hydrocarbon Prices and Tight Credit

> Lower cash flow generation

> Investment cuts

> Leverage increase

> Alternative source of funds

Summary of Historical Hydrocarbon Prices

Oil Prices WTI ($/bbl)

Avg. Price Max. Price Min. Price 1997 20.58 26.62 17.60 1998 14.38 17.82 10.76 1999 19.30 27.92 11.37 2000 30.37 37.21 23.90 2001 25.96 32.19 17.45 2002 26.17 32.72 17.97 2003 31.06 37.83 25.24 2004 41.51 56.17 32.48 2005 56.59 69.81 42.12 2006 66.09 77.03 55.81 2007 72.23 98.88 50.48 2008 99.92 145.29 31.41 2009 (YTD) 54.37 72.68 33.98

Bbl – Barrel.

Source: Bloomberg.

www.fitchratings.com 9

Capital Expenditures to Decline in 2009 Declines in Russia and LatAm partially offset by increases in Asia

05,000

10,00015,00020,00025,00030,00035,00040,000

Pem

ex

PD

VS

A

Pet

robr

as

Eco

petr

ol

Luko

il

Ros

neft

TN

K-B

P

Gaz

prom

Nef

t

Kaz

Mun

aiG

asE

&P

Pet

roC

hina

Sin

opec

CN

OO

C

PT

T

Pet

rona

s

2003 2004 2005 2006 2007 2008 2009e

Source: Company reports, Fitch Ratings

Capex 2003-2009(USDbn)

www.fitchratings.com 10

Capex Efficiency Diverges Within RegionsMexico vs Brazil

Oil Production (’000 Bpd) Investments (USD bn)

Sources: Petrobras, Pemex, Fitch Ratings Sources: Petrobras, Pemex, Fitch Ratings

0

5

10

15

20

25

30

35

40

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

f

20

10

f

20

11

f

Petrobras Pemex

0

500

1000

1500

2000

2500

3000

3500

4000

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

f

20

10

f2

01

1f

Petrobras Pemex

www.fitchratings.com 11

China and State-Owned Banks Finance Sector

Expected Funding Sources in 2009a (USD Bil.)

Pemex ‘BBB’

Stable

PDVSA ‘B+’

Stable

Petrobras ‘BBB’

Stable

Ecopetrol ‘BB+’

Stable

Lukoil ‘BBB ’ Stable

Rosneft ‘BBB ’

Neg.

TNK-BP ‘BBB ’

Neg.

KMG E&P ‘BBB ’

Neg.

PetroChina ‘A+’

Stable

Sinopec ‘A ’

Stable

CNOOC ‘A’

Stable

PTT ‘BBB’

Stable

Petronas ‘A’

Stable Total % Government

Banks 12.5 5.0 3.0 6.6 5.0 3.5 35.6 33 China

Development Bank 4.0b 10.0 10.0 24.0 22

Exim Institutions 1.8 2.0 2.5 6.3 6 Domestic Capital

Markets 2.5 3.0 0.8 6.6 2.6 15.5 14 International

Capital Markets 2.5 2.8 1.5 1.0 1.0 4.5 13.3 12 Other 2.3 2.5 1.5 1.2 0.6 5.0 13.1 12 Total 9.0 9.0 30.3 3.0 8.0 13.0 1.6 0.0 13.2 10.0 3.5 2.6 4.5 106.7 100 aExpected funding sources include incremental debt and refinancing. bPDVSA funding sources includes a USD4 billion loan granted by CDB to Bandes (Venezuela’s Development Bank), which in turn grants loans to PDVSA. Source: Fitch Ratings and company reports.

www.fitchratings.com 12

Lower Oil Prices Not Likely to End Nationalism

> Hydrocarbon related revenues a significant revenue stream for the sovereign

– Close to 50% for Venezuela and Malaysia

– About 35% for Mexico, Russia and Kazakhstan

– Less than 20% for China, India, Thailand, Colombia and Brazil

> Need to attract capital and technical expertise from IOC to EM at risk

– Discouraged by higher royalties and taxes

– Nationalization or coerced sales in Venezuela, Bolivia, Russia and Kazakhstan

> Regulatory changes introduce marginal improvements or significant set-backs

– Mexico’s energy reform improves Pemex’s corporate governance & financial flexibility

– Brazil’s proposed pre-salt regulation increases government intervention in the industry

Agenda

Global Oil Picture

Trends in Emerging Markets

Brazil’s Position within Latin America

Brazil: Growth Prospects and New Regulation

www.fitchratings.com 14

Oil Production in Latin America: 10 mmbpd in 2008

0

20004000

6000

800010000

12000

1968 1973 1978 1983 1988 1993 1998 2003 2008

Brazil Mexico Venezuela Argentina Colombia Ecuador Other

Source: BP and Fitch Ratings

(thousand barrels per day)

www.fitchratings.com 15

Oil Production in Latin America Shifting to Brazil

Peru1%

T&T2%

Ecuador

5%Other

1%

Mexico33%

Brazil19%

Colombia6%

Argentina7%

Venezuela26%

2008 Oil Production in Latin America

(9.8 million barrels per day)

Source: BP and Fitch

Peru1%

T&T1%

Ecuador

5%Other

1%

Mexico34%

Brazil10%

Colombia7%

Argentina9%

Venezuela33%

1998 Oil Production in Latin America

(10.4 million barrels per day)

Source: BP and Fitch

www.fitchratings.com 16

Consistent Production Increases in Brazil

-2000

-1500

-1000

-500

0

500

1000

1500

2000

Brazil Mexico Venezuela Argentina Colombia Ecuador Other

Tho

usan

d ba

rrel

s of

oil

per

day

1970-1980 1980-1990 1990-2000 2000-2008

Sources: BP and Fitch Ratings

www.fitchratings.com 17

Reserves shifting to Venezuela and Brazil

Peru1%

T&T1%

Ecuador

5%

Other1%

Mexico9%

Brazil9%

Colombia1%

Argentina2%

Venezuela73%

2008 Proved Oil Reserves in Latin America

(135 billion barrels)

Source: BP and Fitch Ratings

Venezuela65%

Argentina2%

Colombia2%

Brazil6%

Mexico18%

Other1%

Ecuador

5%

T&T1%Peru

1%

1998 Proved Oil Reserves in Latin America

(117 billion barrels)

Source: BP and Fitch Ratings

Agenda

Global Oil Picture

Trends in Emerging Markets

Brazil’s Position within Latin America

Brazil: Growth Prospects and New Regulation

www.fitchratings.com 19

Brazil: Internal Demand is Robust

Sources: BP and Fitch

0.00

0.50

1.00

1.50

2.00

2.50

19

80

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

Mil

lio

n b

arre

ls p

er d

ay

Oil Production Oil Consumption

www.fitchratings.com 20

Strong Production, Reserves and Reserve Life Trends in Brazil

Reserve Life (years)

0

5

10

15

20

25

19

80

19

84

19

88

19

92

19

96

20

00

20

04

20

08

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

-

0.200

0.400

0.600

0.800

1.000

1.200

1.400

1.600

1.800

2.000

Reserves P roduction

Reserves and Production in Brazil(million barrels)

Source: BP and Fitch Ratings

www.fitchratings.com 21

Discoveries Increase Production and ReserveGrowth Prospects

> With the pre-salt areas reserves are expected to more than double in Brazil

– 5 billion boe to 8 billion boe in Tupi

– 3 billion boe to 4 billlion boe in Iara

– 1 billion boe to 2 billion boe in Guara

> Production also could double by 2020 (excluding PSA)

– 2015E production of 582 mboe

– 2020E production of 1,815 mboe

> Significant investments are required for developing pre-salt (excluding PSA)

– USD29 billion from 2009 to 2013

– USD111 billion from 2009 to 2020

www.fitchratings.com 22

Proposed Regulation Increases Government Intervention

> Creation of Petrosal – Participates in PSA’s operating committees

– Has veto power

> Increased attribution of the CNPE

– Determines areas considered strategic

– Defines the oil profit paid to the government in areas directly assigned to Petrobras

> Government may increase stake in the industry

– “Profit oil” vs royalties and special taxes

– If minority shareholders do not exercise their pre-emptive rights

– By buying Petrobras’ shares with treasury notes

www.fitchratings.com 23

Petrobras to Take a More Active Role in the Industry

> Benefits from proposed regulation:

– Operator in all blocks

– 30% minimum participation in PSAs

– Government contribution of up to 5 billion boe

– Likely to raise more than USD15 billion from minority shareholders

> Burdens from proposed regulation:– Significant investment requirements to develop pre-salt

– Could end up participating in non-economical fields

– Technical and economic challenges

– Resource overextension

Fitch Ratingswww.fitchratings.com

Singapore6 Temasek Blvd.#35-03/04/05Suntec Tower FourSingapore 038986+65 6336 6801

New YorkOne State Street PlazaNew York, NY 10004+1 212 908 0500+1 800 75 FITCH

Fitch Group Fitch Ratings Fitch Solutions Algorithmics

London101 Finsbury PavementLondonEC2A 1RS44 20 7417 4222