Brazil Nuclear Power Generation and Equipments Market Report to 2030

2/1/2017cavanha.com 1

Brazil O&G @2030

Armando Cavanhacavanha.com

0

1. vision of oil ang gas industry in Brazil @ 20302. 10 key challenges

2030

1

cavanha.com

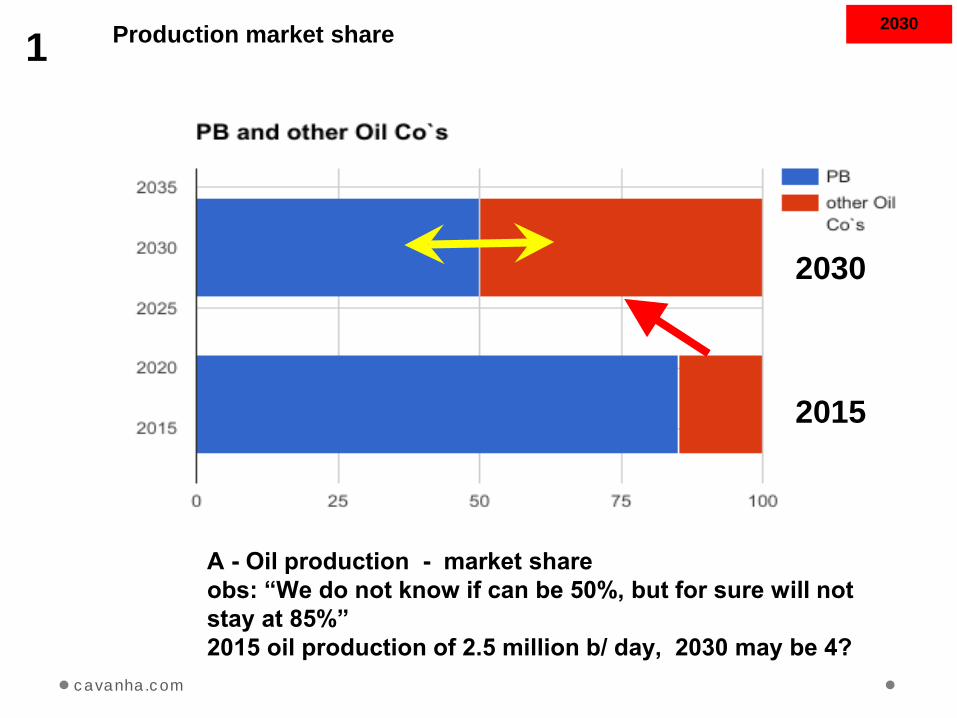

2015

2030

Production market share

2030

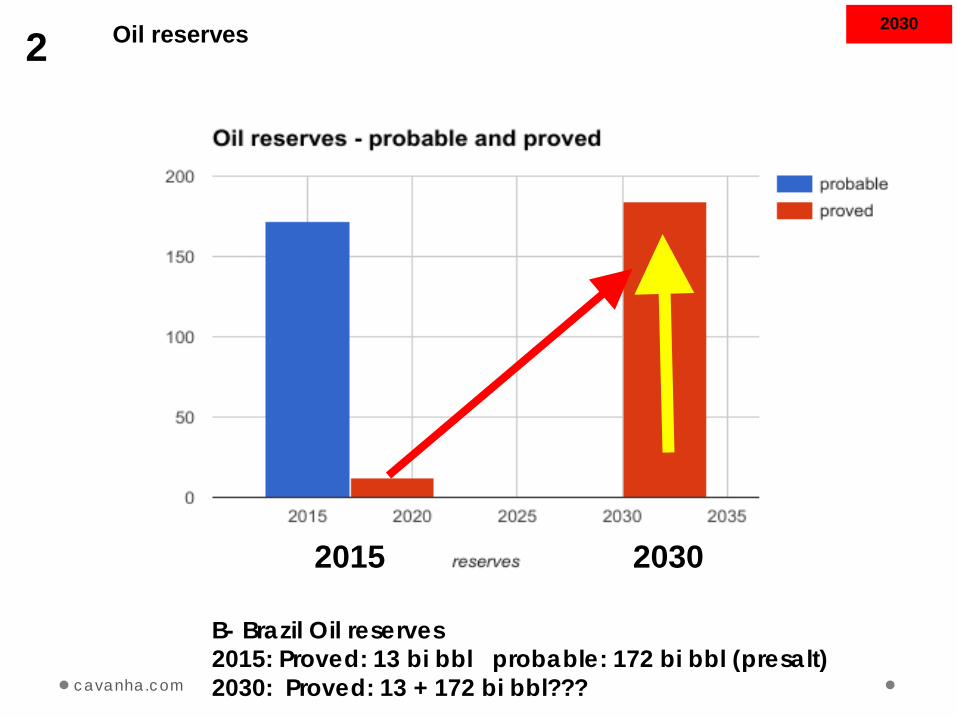

B- Brazil Oil reserves2015: Proved: 13 bi bbl probable: 172 bi bbl (presalt)2030: Proved: 13 + 172 bi bbl???

2

cavanha.com

2015 2030

Oil reserves

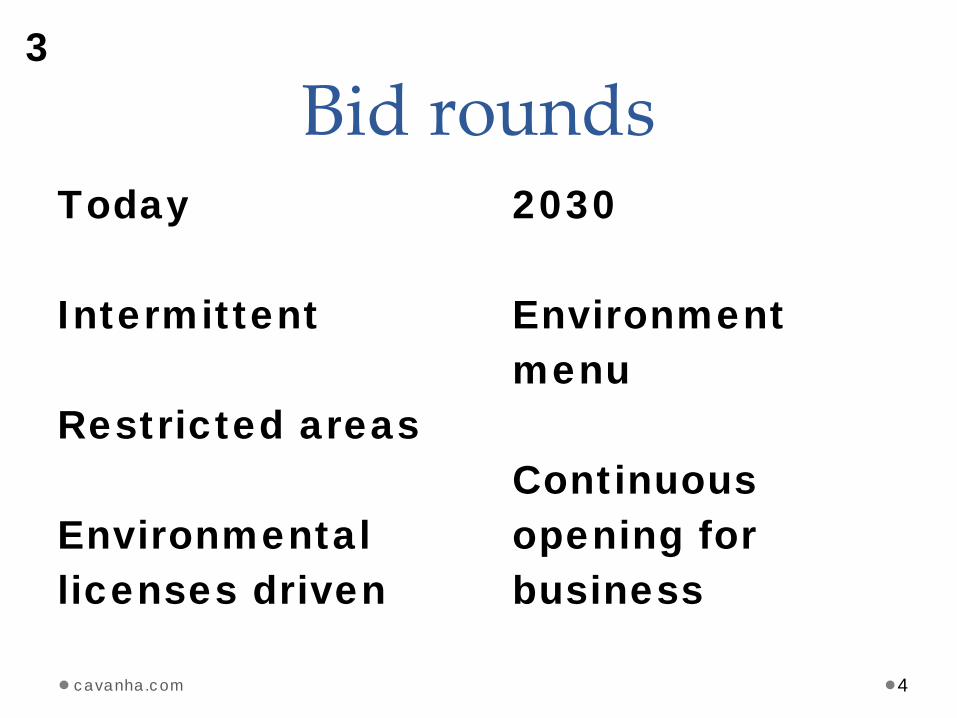

Bid roundsToday

Intermittent

Restricted areas

Environmental licenses driven

4

2030

Environment menu

Continuous opening for business

3

cavanha.com

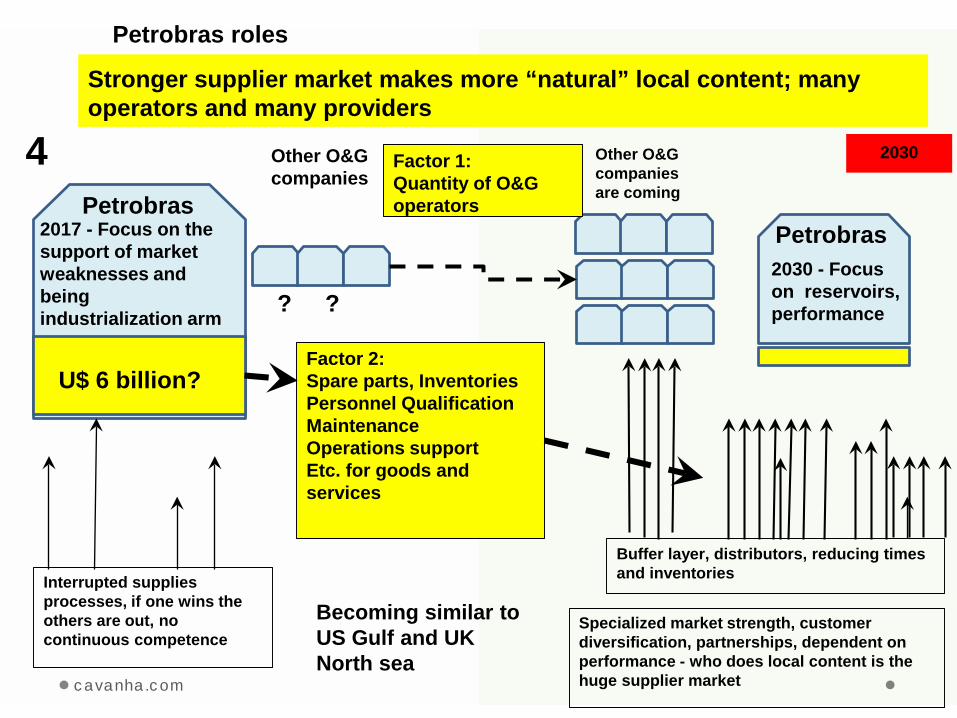

Factor 2:Spare parts, InventoriesPersonnel QualificationMaintenanceOperations supportEtc. for goods and services

PetrobrasPetrobras

Other O&G companies

Specialized market strength, customer diversification, partnerships, dependent on performance - who does local content is the huge supplier market

2030 - Focus on reservoirs, performance

2017 - Focus on the support of market weaknesses and being industrialization arm

Interrupted supplies processes, if one wins the others are out, no continuous competence

Other O&G companies are coming

Buffer layer, distributors, reducing times and inventories

Stronger supplier market makes more “natural” local content; many operators and many providers

2030

? ?

Becoming similar to US Gulf and UK North sea

Factor 1:Quantity of O&G operators

4

cavanha.com

U$ 6 billion?

Petrobras roles

oil industry100%

0%

RIS

K O

F TH

E A

CTI

VITY

+probabilistic/centralized + deterministic/decentralizedUpstream is Nomad, Associative,

Technological, OpportunityContracts follow Contingency,

Resilience

Downstream is Sedentary, Optimization, Chronogram, Planning

Contracts follow Redundancy, Robustness

2/1/2017cavanha.com 6

probabilisticvs

deterministic

2030

5 Upstream vs downstream

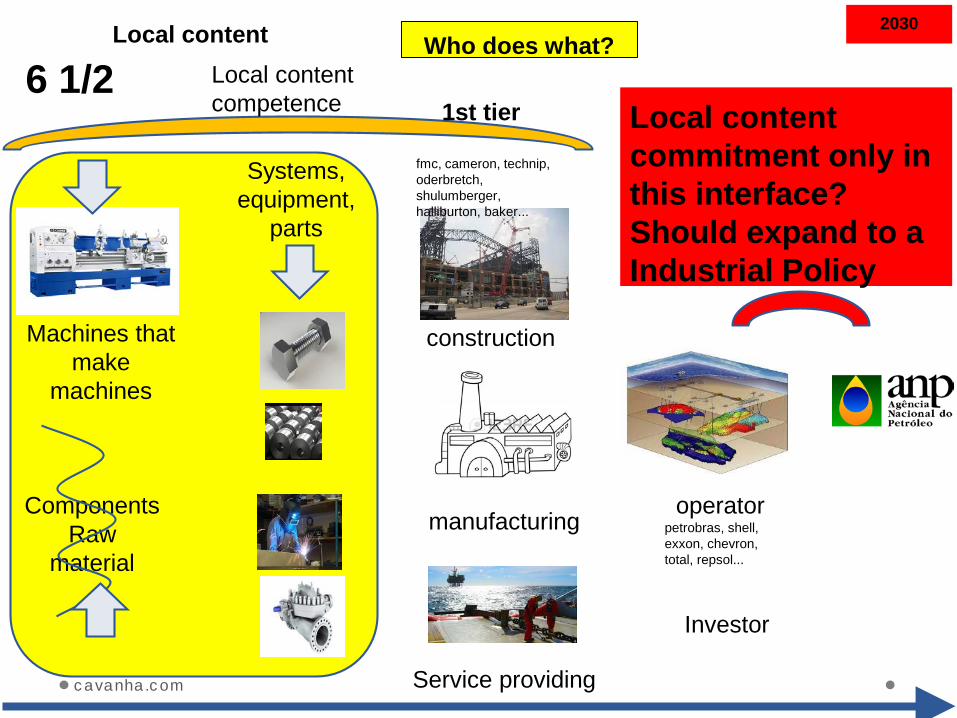

operator

Service providing

manufacturing

construction

Systems, equipment,

parts

ComponentsRaw

material

Machines that make

machines

Who does what?

fmc, cameron, technip, oderbretch, shulumberger, halliburton, baker...

petrobras, shell, exxon, chevron, total, repsol...

Local content commitment only in this interface? Should expand to a Industrial Policy

2030

Investor

Local content competence

6 1/2

cavanha.com

1st tier

Local content

fases

O&G companies make free choices and partnerships among them and with providers to increase competitive local content, including export for foreign fields.Should be better with tax reductions and processes simplification at risk time.

The amount of local activities incorporated at the previous phases increases taxation, jobs, etc. As a consequence, Royalties and production taxation should be reduced proportionally.

$2030

6 2/2

cavanha.com

Local content

2/1/2017

cavanha.com

9

O&G companies

Exploration and reservoir delimitation

Conceptual engineering FEL1

Basic engineering FEL2

Detailing engineering

EPC – engineering procurement construction

geologygeophysics

reservoir

processes

systems

equipment

Operation of production (20 to 30 years)

“Basic Engineering”, R&D, Local Content

Engineering providers

reservoir

Syst

emic

kno

wle

dge

dom

ain

FEL 1 FEL 2 FEL 3

What market availability, technologies, suppliers an engineer working with basic engineering located in Singapore, Tokyo or Houston can see or select?Can he develop local suppliers?

selection of technologies,

systems, equipment, vendor list,

budgets, mass and energy

balances, etc.

Strong Local content depends on a consistent and competent Basic Engineering

2030

7Should be local, or in partnership with localsIts the time the company chooses tech options

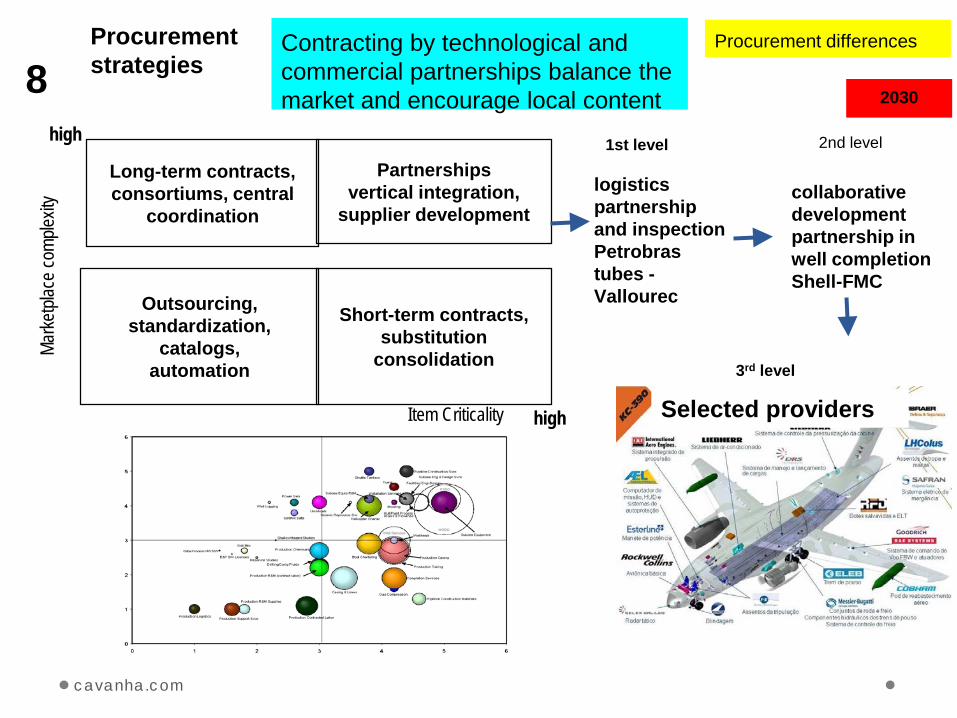

Basic engineering

Long-term contracts, consortiums, central

coordination

Partnershipsvertical integration,

supplier development

Outsourcing, standardization,

catalogs,automation

Short-term contracts,substitution

consolidation

high

Marke

tplac

e com

plexit

y

highItem Criticality

logistics partnership and inspection Petrobras tubes -Vallourec

collaborative development partnership in well completion Shell-FMC

1st level 2nd level

3rd level

Procurement differencesContracting by technological and commercial partnerships balance the market and encourage local content 2030

Selected providers

8

cavanha.com

Procurement strategies

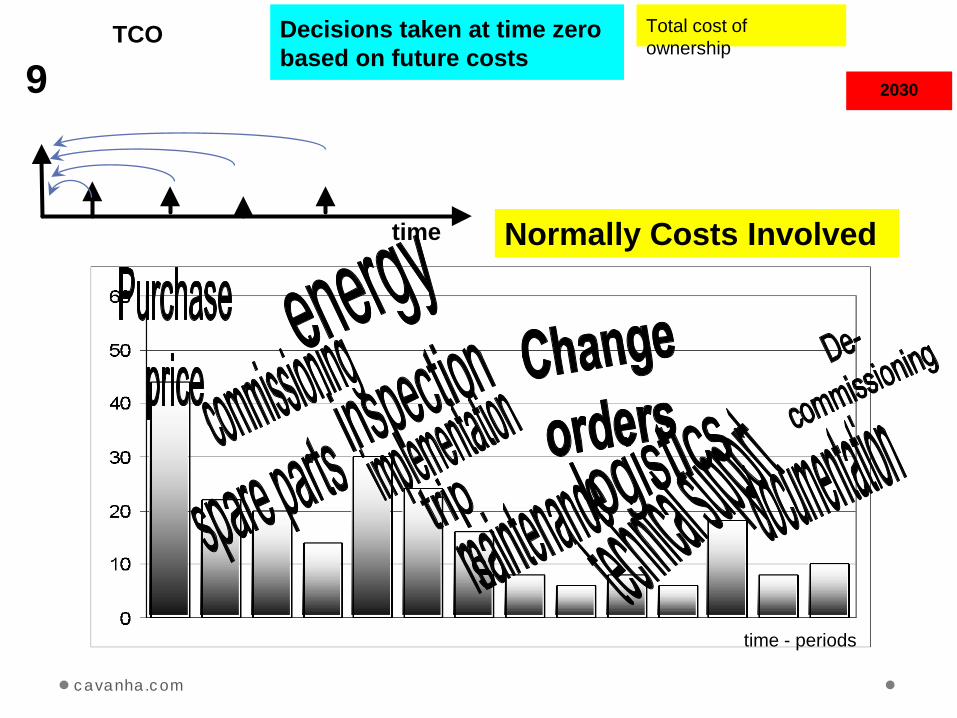

time

Total cost of ownership

Decisions taken at time zero based on future costs

2030

Normally Costs Involved

time - periods

9

cavanha.com

TCO

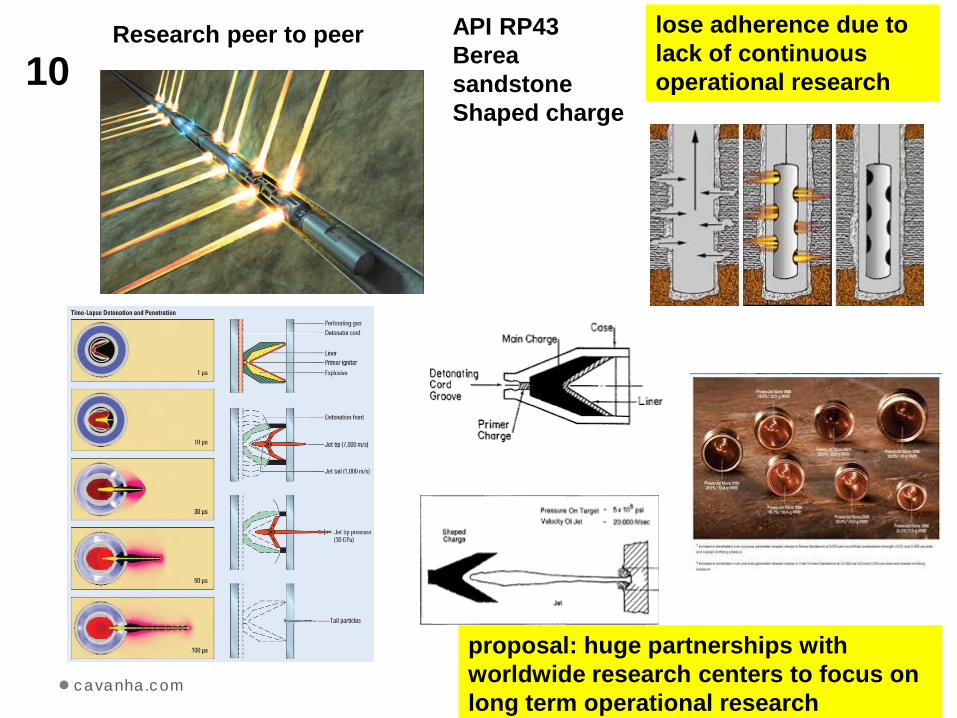

API RP43Berea sandstoneShaped charge

lose adherence due to lack of continuous operational research10

cavanha.com

proposal: huge partnerships with worldwide research centers to focus on long term operational research

Research peer to peer