brazil banking perf

73

Q3 2015 www.bmiresearch.com BRAZIL COMMERCIAL BANKING REPORT INCLUDES 5-YEAR FORECASTS TO 2019 ISSN 1747-8510 Published by:BMI Research

-

Upload

jitheshgopal -

Category

Documents

-

view

32 -

download

0

description

perf

Transcript of brazil banking perf

Q3 2015www.bmiresearch.com

BRAZILCOMMERCIAL BANKING REPORTINCLUDES 5-YEAR FORECASTS TO 2019

ISSN 1747-8510Published by:BMI Research

Brazil Commercial Banking Report Q3 2015INCLUDES 5-YEAR FORECASTS TO 2019

Part of BMI’s Industry Report & Forecasts Series

Published by: BMI Research

Copy deadline: April 2015

BMI ResearchSenator House85 Queen Victoria StreetLondonEC4V 4ABUnited KingdomTel: +44 (0) 20 7248 0468Fax: +44 (0) 20 7248 0467Email: [email protected]: http://www.bmiresearch.com

© 2015 Business Monitor International LtdAll rights reserved.

All information contained in this publication iscopyrighted in the name of Business MonitorInternational Ltd, and as such no part of thispublication may be reproduced, repackaged,redistributed, resold in whole or in any part, or usedin any form or by any means graphic, electronic ormechanical, including photocopying, recording,taping, or by information storage or retrieval, or byany other means, without the express written consentof the publisher.

DISCLAIMERAll information contained in this publication has been researched and compiled from sources believed to be accurate and reliable at the time ofpublishing. However, in view of the natural scope for human and/or mechanical error, either at source or during production, Business MonitorInternational Ltd accepts no liability whatsoever for any loss or damage resulting from errors, inaccuracies or omissions affecting any part of thepublication. All information is provided without warranty, and Business Monitor International Ltd makes no representation of warranty of any kindas to the accuracy or completeness of any information hereto contained.

CONTENTS

BMI Industry View ............................................................................................................... 7Table: Commercial Banking Sector Indicators . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

Table: Commercial Banking Sector Key Ratios, February 2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

Table: Annual Growth Rate Projections 2014-2019 (%) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

Table: Ranking Out Of 73 Countries Reviewed In 2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

Table: Commercial Banking Sector Indicators, 2012-2019 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

SWOT .................................................................................................................................... 9Commercial Banking .................................................................................................................................. 9

Political ................................................................................................................................................. 10

Economic ............................................................................................................................................... 11

Operational Risk ..................................................................................................................................... 12

Industry Forecast .............................................................................................................. 14Table: BRAZIL - BANKING SECTOR OVERVIEW . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

Industry Risk Reward Ratings .......................................................................................... 21Latin America Commercial Banking Risk/Reward Index .................................................................................. 21

Table: Latin America Commercial Banking Risk/Reward Index . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

Market Overview ............................................................................................................... 23Latin America Commercial Banking Outlook ................................................................................................ 23

Table: Banks' Bond Portfolios, 2013 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

Table: Comparison of Loan/Deposit & Loan/Asset & Loan/GDP ratios, 2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

Table: Comparison of Total Assets & Client Loans & Client Deposits (USDbn) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

Table: Comparison of USD Per Capita Deposits, 2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

Economic Analysis ................................................................................................................................... 25Table: GDP By Expenditure (Brazil 2012-2019) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

Competitive Landscape .................................................................................................... 31Market Structure ..................................................................................................................................... 31

Protagonists .......................................................................................................................................... 31Table: Protagonists In Brazil's Commercial Banking Sector . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

Definition Of The Commercial Banking Universe ......................................................................................... 31

List of Banks ......................................................................................................................................... 32Table: 50 Largest Banks In Brazil (by total assets) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32

Company Profile ................................................................................................................ 34Banco do Brasil ....................................................................................................................................... 34

Table: Stock Market Indicators . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36

Table: Balance Sheet (BRLmn) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36

Table: Balance Sheet (USDmn) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36

Table: Key Ratios (%) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37

Banco Safra ............................................................................................................................................ 38

Brazil Commercial Banking Report Q3 2015

© Business Monitor International Ltd Page 4

Table: Balance Sheet (BRLmn) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39

Table: Balance Sheet (USDmn) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39

Table: Key Ratios (%) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40

Bradesco ................................................................................................................................................ 41Table: Stock Market Indicators . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42

Table: Balance Sheet (BRLmn) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43

Table: Balance Sheet (USDmn) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43

Table: Key Ratios (%) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43

Caixa Economica Federal ......................................................................................................................... 44Table: Balance Sheet (BRLmn) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45

Table: Balance Sheet (USDmn) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46

Table: Key Ratios (%) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46

Santander .............................................................................................................................................. 47Table: Stock Market Indicators . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49

Table: Balance Sheet (BRLmn) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49

Table: Balance Sheet (USDmn) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49

Table: Key Ratios (%) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 50

Regional Overview ............................................................................................................ 51Latin America Overview ........................................................................................................................... 51

Table: Latin America Banking Sector Assets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 58

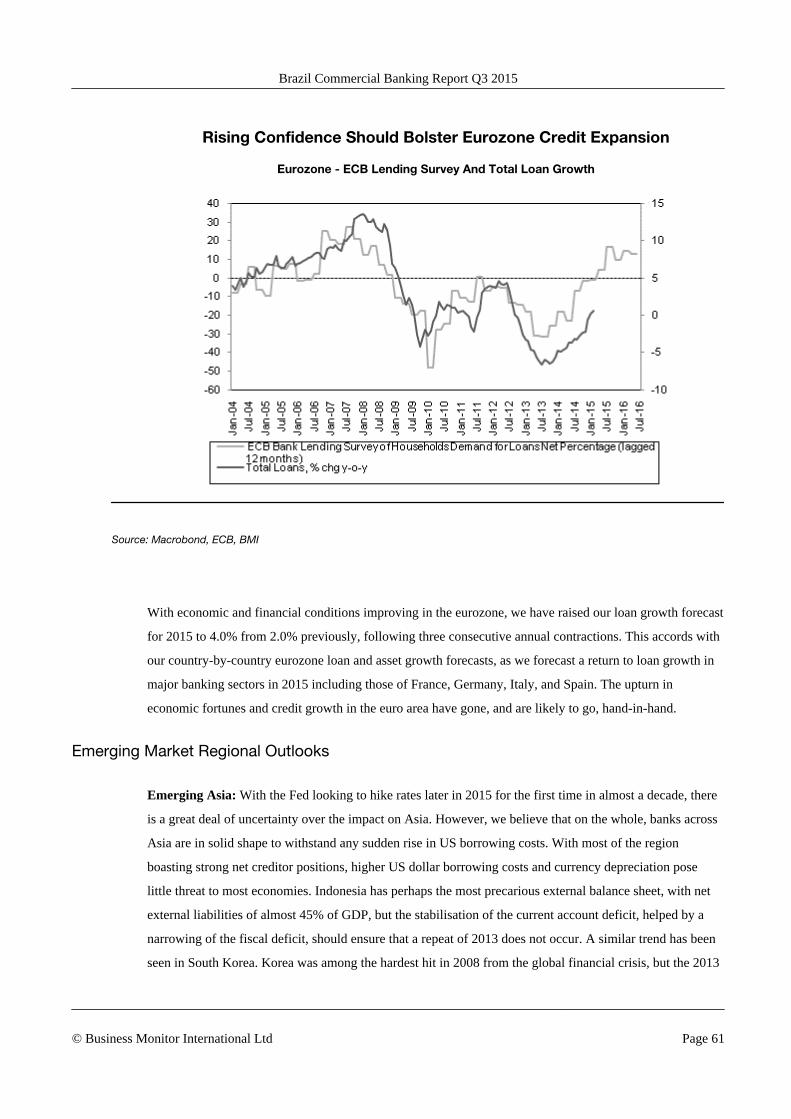

Global Industry Overview .................................................................................................. 60Global Commercial Banking Outlook .......................................................................................................... 60

US and Eurozone Banking Outlook ............................................................................................................ 60

Emerging Market Regional Outlooks ......................................................................................................... 61

Demographic Forecast ..................................................................................................... 65Table: Population Headline Indicators (Brazil 1990-2025) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 66

Table: Key Population Ratios (Brazil 1990-2025) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 66

Table: Urban/Rural Population & Life Expectancy (Brazil 1990-2025) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 67

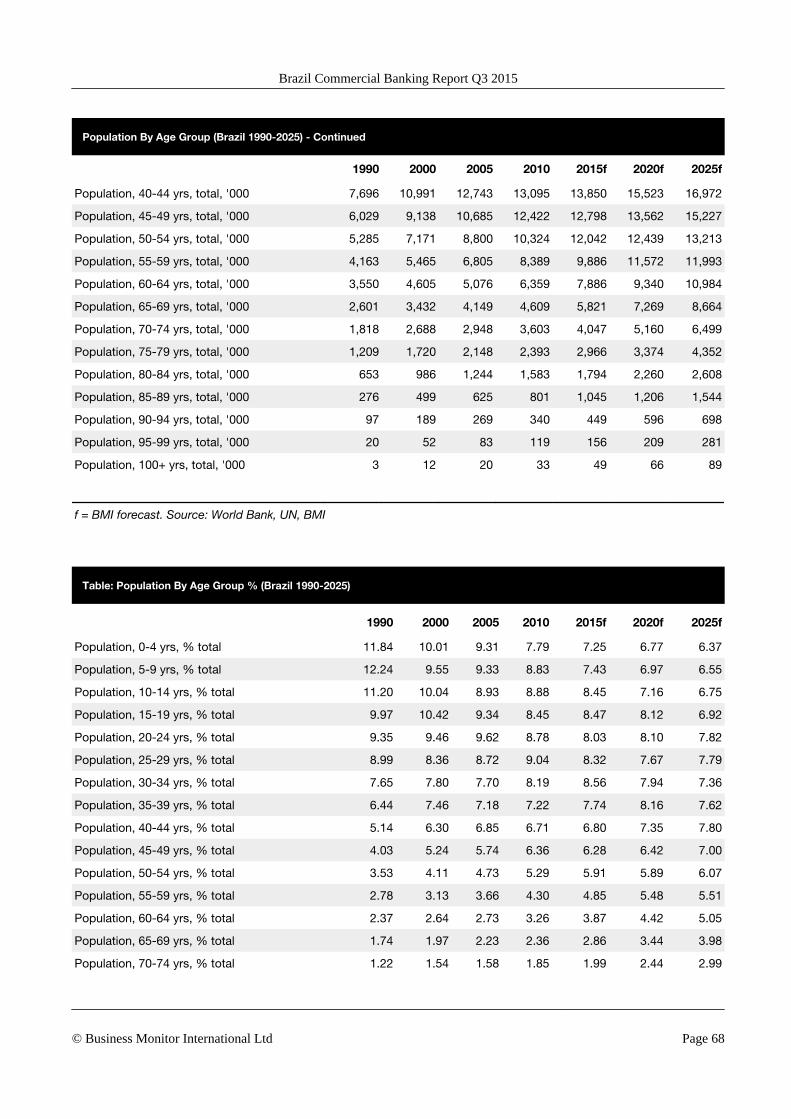

Table: Population By Age Group (Brazil 1990-2025) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 67

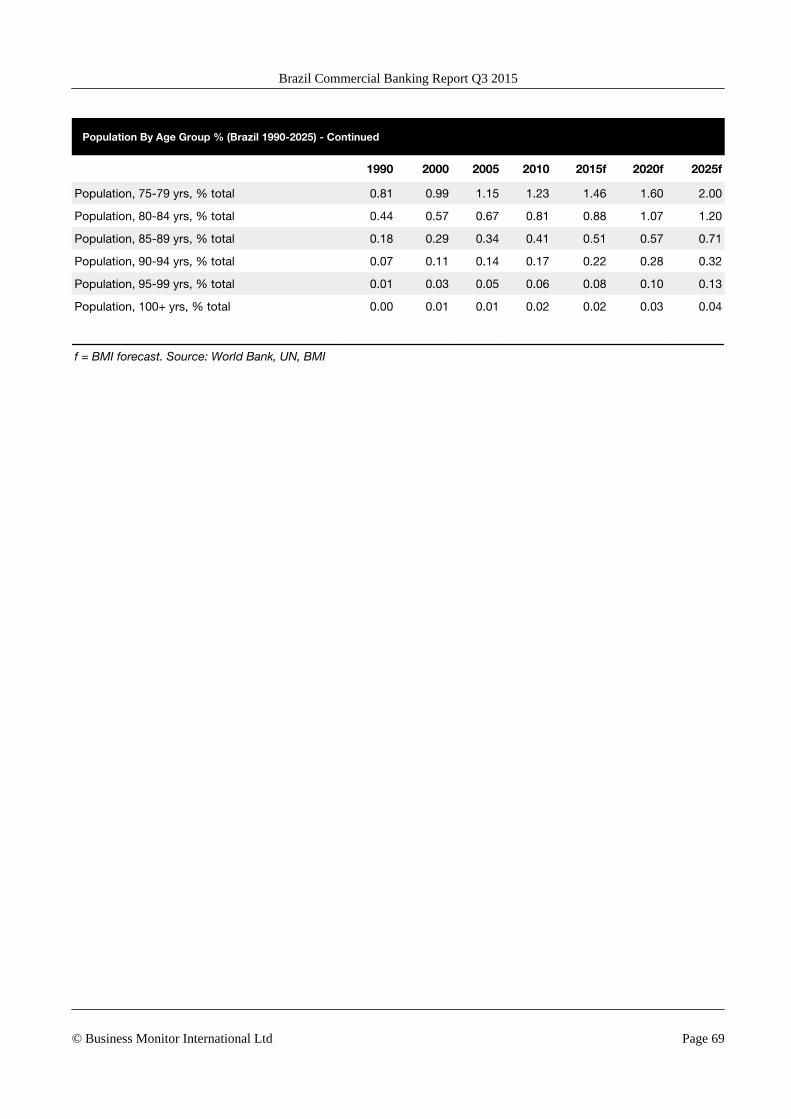

Table: Population By Age Group % (Brazil 1990-2025) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 68

Methodology ...................................................................................................................... 70Industry Forecast Methodology ................................................................................................................ 70

Sector-Specific Methodology .................................................................................................................... 71

Risk/Reward Ratings Methodology ............................................................................................................ 72Table: Commercial Banking Risk/Reward Rating Indicators . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 73

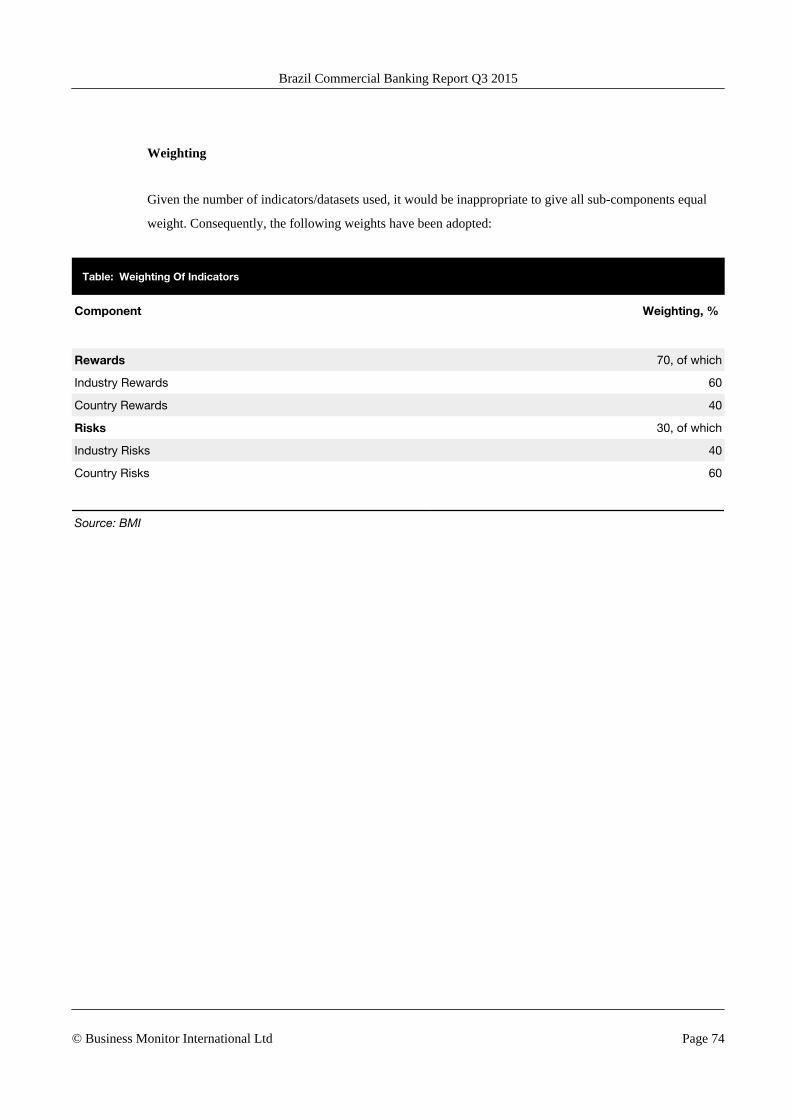

Table: Weighting Of Indicators . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 74

Brazil Commercial Banking Report Q3 2015

© Business Monitor International Ltd Page 5

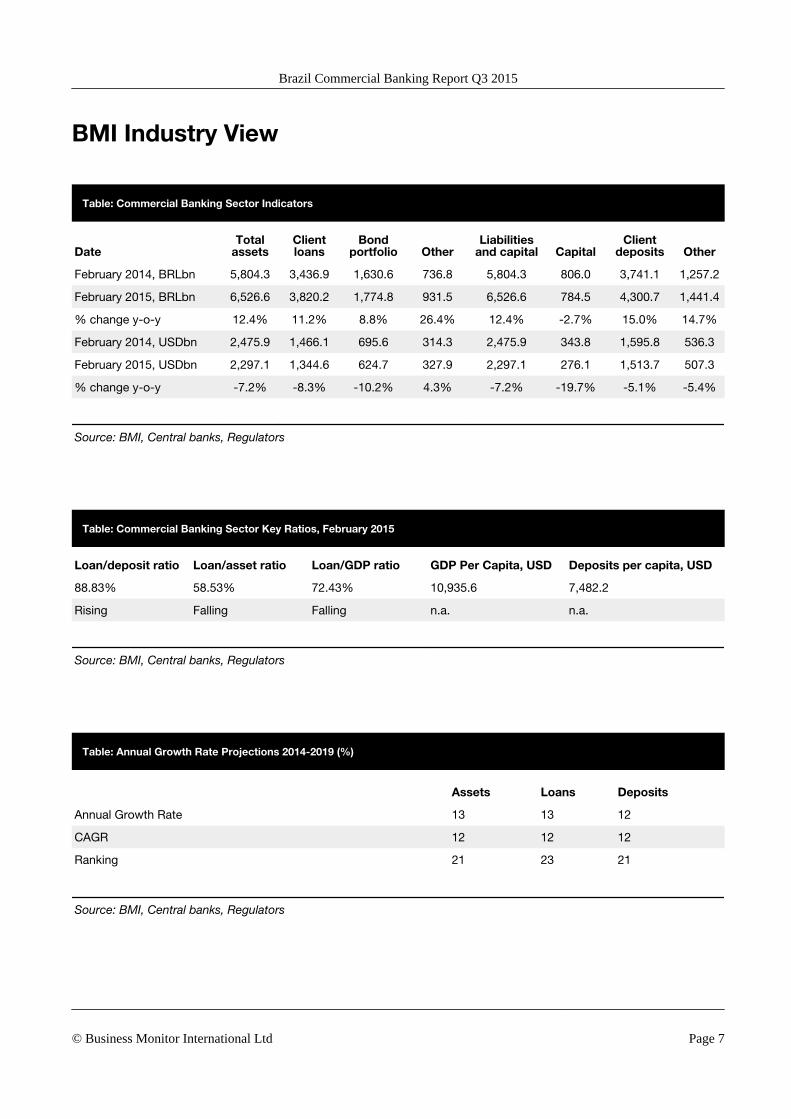

BMI Industry View

Table: Commercial Banking Sector Indicators

DateTotal

assetsClientloans

Bondportfolio Other

Liabilitiesand capital Capital

Clientdeposits Other

February 2014, BRLbn 5,804.3 3,436.9 1,630.6 736.8 5,804.3 806.0 3,741.1 1,257.2

February 2015, BRLbn 6,526.6 3,820.2 1,774.8 931.5 6,526.6 784.5 4,300.7 1,441.4

% change y-o-y 12.4% 11.2% 8.8% 26.4% 12.4% -2.7% 15.0% 14.7%

February 2014, USDbn 2,475.9 1,466.1 695.6 314.3 2,475.9 343.8 1,595.8 536.3

February 2015, USDbn 2,297.1 1,344.6 624.7 327.9 2,297.1 276.1 1,513.7 507.3

% change y-o-y -7.2% -8.3% -10.2% 4.3% -7.2% -19.7% -5.1% -5.4%

Source: BMI, Central banks, Regulators

Table: Commercial Banking Sector Key Ratios, February 2015

Loan/deposit ratio Loan/asset ratio Loan/GDP ratio GDP Per Capita, USD Deposits per capita, USD

88.83% 58.53% 72.43% 10,935.6 7,482.2

Rising Falling Falling n.a. n.a.

Source: BMI, Central banks, Regulators

Table: Annual Growth Rate Projections 2014-2019 (%)

Assets Loans Deposits

Annual Growth Rate 13 13 12

CAGR 12 12 12

Ranking 21 23 21

Source: BMI, Central banks, Regulators

Brazil Commercial Banking Report Q3 2015

© Business Monitor International Ltd Page 7

Table: Ranking Out Of 73 Countries Reviewed In 2015

Loan/deposit ratio Loan/asset ratio Loan/GDP ratio

36 36 29

Local currency asset growth Local currency loan growth Local currency deposit growth

28 30 24

Source: BMI, Central banks, Regulators

Table: Commercial Banking Sector Indicators, 2012-2019

2012 2013 2014 2015f 2016f 2017f 2018f 2019f

Total assets, BRLbn 5,277.1 5,779.3 6,457.8 7,103.6 7,956.0 8,950.6 10,069.4 11,378.4

Total assets, USDbn 2,572.2 2,446.7 2,429.9 2,059.0 2,241.1 2,594.4 3,098.3 3,670.4

Client loans, BRLbn 3,010.2 3,424.5 3,815.6 4,178.1 4,658.6 5,240.9 5,922.2 6,692.1

Client loans, USDbn 1,467.2 1,449.8 1,435.7 1,211.0 1,312.3 1,519.1 1,822.2 2,158.7

Client deposits, BRLbn 3,394.5 3,695.3 4,203.7 4,624.1 5,202.1 5,852.4 6,554.7 7,341.2

Client deposits, USDbn 1,654.6 1,564.4 1,581.8 1,340.3 1,465.4 1,696.3 2,016.8 2,368.1

e/f = estimate/forecast. Source: BMI, Central banks, Regulators

Brazil Commercial Banking Report Q3 2015

© Business Monitor International Ltd Page 8

SWOT

Commercial Banking

Brazil Commercial Banking SWOT

Strengths ■ Large absolute size.

■ Potential for further development in high-end financial services and company

financing.

Weaknesses ■ Strong state bank dominance of the sector puts artificial pressure on private and

public sector banks to lend at low rates, raising questions about asset quality.

Opportunities ■ Potential for consolidation over the long term, particularly if the government reduces

its intervention.

■ A growing middle class provides opportunity for sector growth.

Threats ■ Long-term corporate lending and some segments of consumer lending may remain

underdeveloped, given the past volatility of the economy and financial markets, as

well as the significant role of the state development bank.

■ Given strong household loan growth by public sector banks, any widespread

deterioration in asset quality is likely to end up on the government's balance sheet,

placing stress on the fiscal accounts.

Brazil Commercial Banking Report Q3 2015

© Business Monitor International Ltd Page 9

Political

SWOT Analysis

Strengths ■ President Dilma Rousseff has largely followed in the footsteps of her predecessor

former President Luiz Inácio Lula da Silva, maintaining relatively market-friendly

policies.

■ Although corruption scandals continue to plague the political landscape, President

Dilma Rousseff's attempts to crack down on corrupt officials has boosted confidence

in the executive's commitment to tackling the issue in recent years.

Weaknesses ■ Massive protests in June 2013, and intermittent demonstrations in the last several

quarters, indicate that Brazil's social fabric is beginning to fray. With the

demonstrations highlighting long-term issues including corruption, high living costs

and the sub-par quality of public services, we cannot rule out further social unrest in

the coming quarters.

Opportunities ■ Brazil's growing political influence in the region may pave the way for the country to

assume the role of a regional leader, pioneering closer integration among Latin

American states.

Threats ■ The smaller members of the ruling legislative coalition could stir up trouble for

Rousseff if they feel she has assigned too many cabinet posts to other parties or

disagree with her policy trajectory.

Brazil Commercial Banking Report Q3 2015

© Business Monitor International Ltd Page 10

Economic

SWOT Analysis

Strengths ■ A massive consumer base and significant hydrocarbons, mineral and agricultural

wealth will help to drive economic growth in the long term.

Weaknesses ■ Large-scale social spending programmes have seen the government's fiscal accounts

deteriorate at an alarming rate and prompted a sovereign credit rating downgrade in

March 2014.

■ High levels of labour market rigidity and an enormous public sector threaten to

jeopardise Brazil's economic growth.

Opportunities ■ Brazil's massive mineral and oil wealth will help ensure continued foreign investment

into the country.

Threats ■ A run-up in household debt levels in recent years, as well as an increase in public

sector banks lending to consumers, highlight important vulnerabilities in Brazil's

banking sector. Should we see a widespread deterioration in commercial banks'

asset quality, the authorities could be forced to step in to recapitalise the sector.

■ Rising lending by state development bank BNDES will become a growing government

liability, leaving the treasury to foot the bill for a number of bad loans. Our

Infrastructure team believes that several companies may not be able to pay back the

money borrowed for projects related to the government's ongoing transport

concessions programme.

■ The inability of successive governments to implement successful economic reforms,

such as an overhaul of the tax system and reform of the inflexible labour market, are

key threats to Brazil's economy.

Brazil Commercial Banking Report Q3 2015

© Business Monitor International Ltd Page 11

Operational Risk

SWOT Analysis

Strengths ■ There is a large working age population from which businesses can recruit, and Brazil

benefits from the highest rate of employment amongst working age people in Latin

America.

■ The country has the largest and best equipped military forces in the region, which

would be more than capable of repelling any potential aggressor.

■ Amongst the best developed financial markets in the emerging market world.

■ Investors benefit from good communication capabilities due to relatively widespread

internet coverage in the country, resulting in better access to clients/customers.

Weaknesses ■ Strict labour regulations with generous leave allowances and limited working hours.

Unions also exert a strong influence in the workplace.

■ Brazil suffers from some of the highest crime rates in the region and violent crime,

including sexual offences and homicide, are on the increase.

■ Significant red tape in all facets involved in operating a business acts as a deterrent to

foreign investors.

■ Lack of competition between freight modes and congestion at container terminals

means trading costs in Brazil are among the highest in the region.

Opportunities ■ Increasing female participation in the workforce which is being encouraged through

government policies.

■ Government anti corruption measures are strengthening, which will reduce the cost of

doing business.

■ Substantial potential for growth in railway, inland waterway and air cargo sectors,

providing greater diversification for supply chains over the longer term.

■ Continuing investment and privatisation on behalf of global logistics firms will improve

the efficiency of freight transport and port handling.

Brazil Commercial Banking Report Q3 2015

© Business Monitor International Ltd Page 12

SWOT Analysis - Continued

Threats ■ Tight labour market as demand for skilled labour is high, pushing up costs.

■ Due to the absence of terrorism, the security services are largely untested against

external terrorist threats, which could imply limited capability.

■ Despite continued investment, economic and population growth will continue to place

utilities and transport infrastructure under strain, posing a risk to business activity.

■ As the privatisation process continues, strikes across all sectors of the transport

network have the potential to cause delays and disruption to supply chains.

Brazil Commercial Banking Report Q3 2015

© Business Monitor International Ltd Page 13

Industry Forecast

BMI View: Asset and loan growth in Brazil is set for a further slowdown in the coming quarters. Poor

consumer confidence and an ongoing corruption scandal at national oil company Petrobras will weigh on

demand for credit, while a tightening of lending practices by state-owned banks will dampen the supply of

credit as well.

Rising interest rates and an economic recession will drive a further deceleration in Brazilian asset and loan

growth in the coming quarters (see 'Weak Demand And Limited Supply Drive Loan Growth Slowdown',

January 21). An ongoing corruption scandal at national oil company Petrobras will exacerbate these

dynamics, as a cessation of activity on a number of contracts in the oil and gas and construction sectors will

dampen demand for credit (see 'Corruption Scandal Could Prompt Market Restructure', March 6). The

trend of weaker asset and loan growth will continue over the course of our five-year forecast period in light

of slower real GDP growth, a highly-leveraged household sector, and a retrenchment in lending from state-

owned banks. Indeed, we forecast average annual loan growth of 11.9% over the course of our forecast

period to 2019, below 19.4% between 2010 and 2014. As a result, we see little upside for Brazil's score in

our Commercial Banking Risk/Reward Index, underpinning our view that the country will not regain the top

spot in Latin America in the coming quarters.

Brazil Commercial Banking Report Q3 2015

© Business Monitor International Ltd Page 14

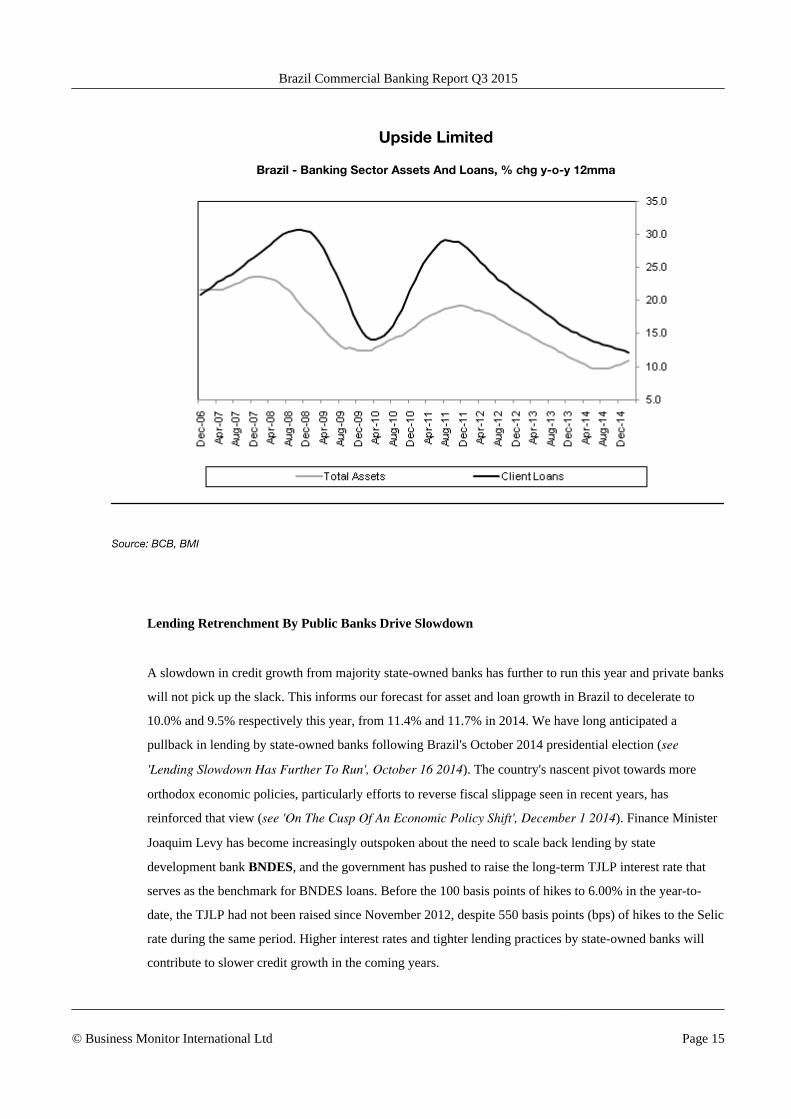

Upside Limited

Brazil - Banking Sector Assets And Loans, % chg y-o-y 12mma

Source: BCB, BMI

Lending Retrenchment By Public Banks Drive Slowdown

A slowdown in credit growth from majority state-owned banks has further to run this year and private banks

will not pick up the slack. This informs our forecast for asset and loan growth in Brazil to decelerate to

10.0% and 9.5% respectively this year, from 11.4% and 11.7% in 2014. We have long anticipated a

pullback in lending by state-owned banks following Brazil's October 2014 presidential election (see

'Lending Slowdown Has Further To Run', October 16 2014). The country's nascent pivot towards more

orthodox economic policies, particularly efforts to reverse fiscal slippage seen in recent years, has

reinforced that view (see 'On The Cusp Of An Economic Policy Shift', December 1 2014). Finance Minister

Joaquim Levy has become increasingly outspoken about the need to scale back lending by state

development bank BNDES, and the government has pushed to raise the long-term TJLP interest rate that

serves as the benchmark for BNDES loans. Before the 100 basis points of hikes to 6.00% in the year-to-

date, the TJLP had not been raised since November 2012, despite 550 basis points (bps) of hikes to the Selic

rate during the same period. Higher interest rates and tighter lending practices by state-owned banks will

contribute to slower credit growth in the coming years.

Brazil Commercial Banking Report Q3 2015

© Business Monitor International Ltd Page 15

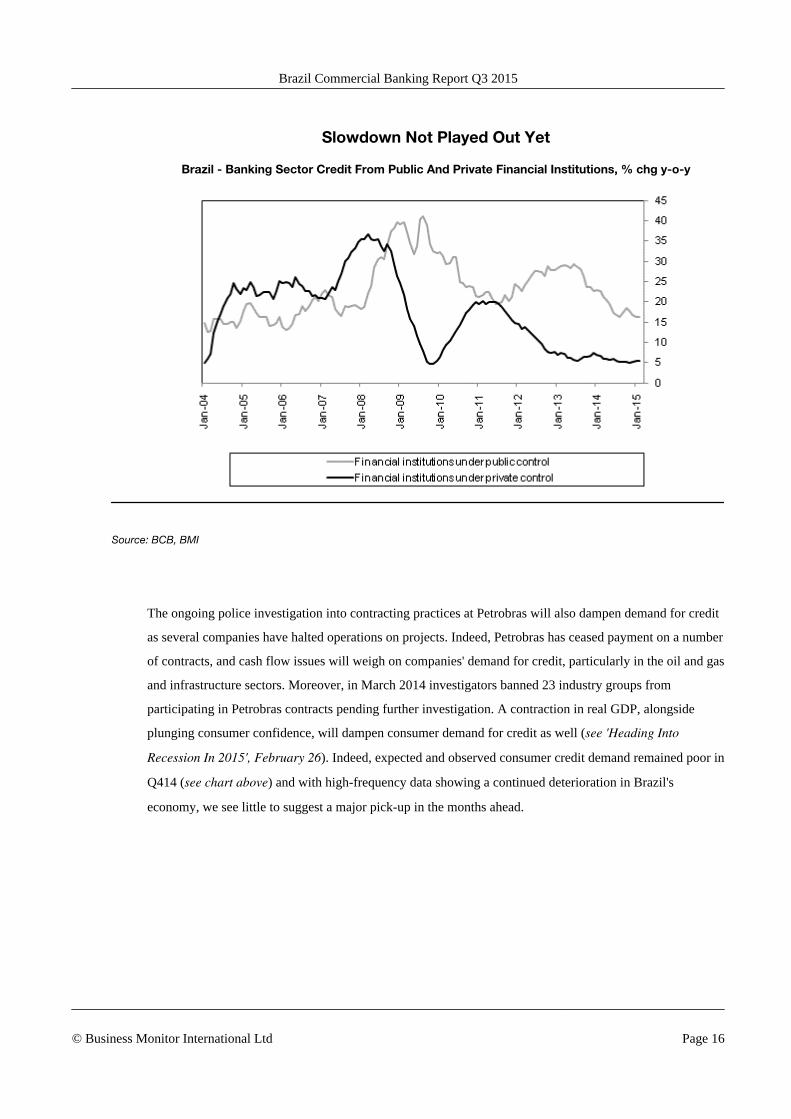

Slowdown Not Played Out Yet

Brazil - Banking Sector Credit From Public And Private Financial Institutions, % chg y-o-y

Source: BCB, BMI

The ongoing police investigation into contracting practices at Petrobras will also dampen demand for credit

as several companies have halted operations on projects. Indeed, Petrobras has ceased payment on a number

of contracts, and cash flow issues will weigh on companies' demand for credit, particularly in the oil and gas

and infrastructure sectors. Moreover, in March 2014 investigators banned 23 industry groups from

participating in Petrobras contracts pending further investigation. A contraction in real GDP, alongside

plunging consumer confidence, will dampen consumer demand for credit as well (see 'Heading Into

Recession In 2015', February 26). Indeed, expected and observed consumer credit demand remained poor in

Q414 (see chart above) and with high-frequency data showing a continued deterioration in Brazil's

economy, we see little to suggest a major pick-up in the months ahead.

Brazil Commercial Banking Report Q3 2015

© Business Monitor International Ltd Page 16

Significant Uptick Unlikely

Brazil - BCB Credit Demand Indicators

Note: Trend indicator of credit demand by financial institutions expressed in a point scale from 2 (best) to -2 (worst); Source: BCB

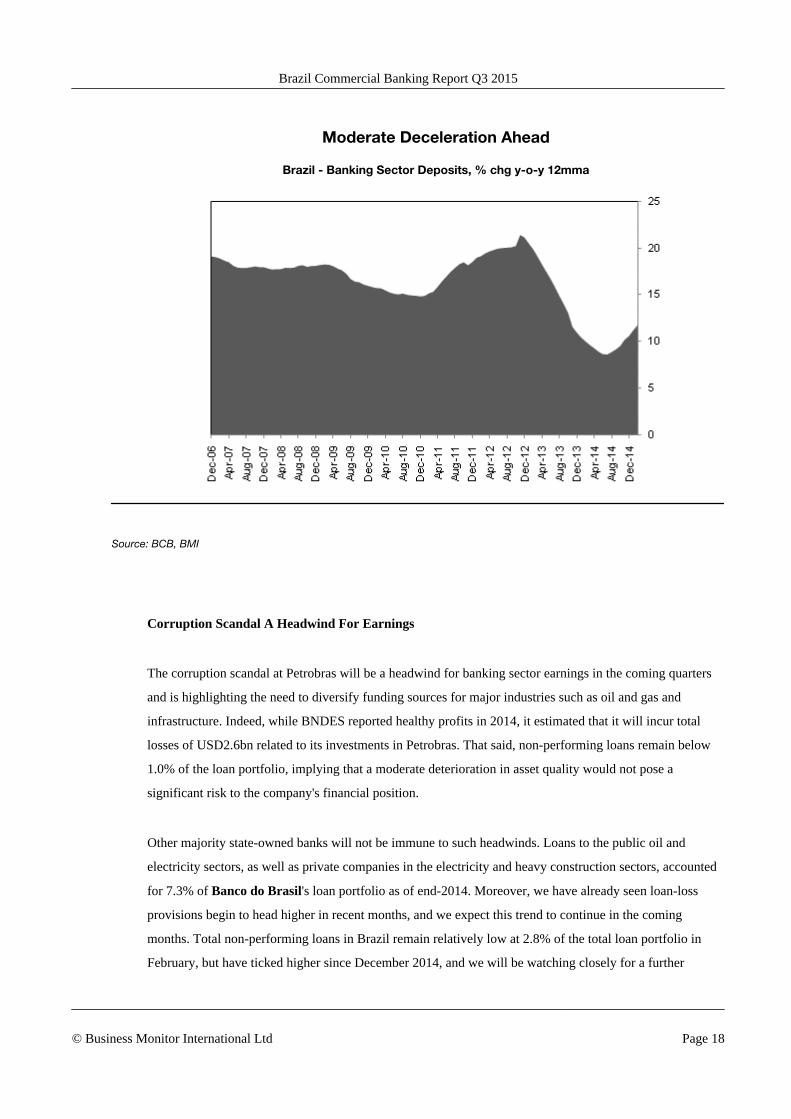

Weak Labour Market To Weigh On Deposit Growth

On the liabilities side of the balance sheet, deposit growth will slow in the coming months as a weakening

labour market weighs on income growth. Given an increase in the time it takes to find a job, a falling labour

participation rate, and rising reports that companies are looking to lay off workers due to poor economic

conditions, we expect deposit growth to decelerate in 2015. Nevertheless, rising deposit rates, which likely

contributed to a rebound in deposit growth in the latter half of 2014, will provide an incentive to save and

cushion the slowdown in deposits. Given these dynamics, we forecast deposits to increase by 10.0% this

year, down from 13.8% in 2014.

Brazil Commercial Banking Report Q3 2015

© Business Monitor International Ltd Page 17

Moderate Deceleration Ahead

Brazil - Banking Sector Deposits, % chg y-o-y 12mma

Source: BCB, BMI

Corruption Scandal A Headwind For Earnings

The corruption scandal at Petrobras will be a headwind for banking sector earnings in the coming quarters

and is highlighting the need to diversify funding sources for major industries such as oil and gas and

infrastructure. Indeed, while BNDES reported healthy profits in 2014, it estimated that it will incur total

losses of USD2.6bn related to its investments in Petrobras. That said, non-performing loans remain below

1.0% of the loan portfolio, implying that a moderate deterioration in asset quality would not pose a

significant risk to the company's financial position.

Other majority state-owned banks will not be immune to such headwinds. Loans to the public oil and

electricity sectors, as well as private companies in the electricity and heavy construction sectors, accounted

for 7.3% of Banco do Brasil's loan portfolio as of end-2014. Moreover, we have already seen loan-loss

provisions begin to head higher in recent months, and we expect this trend to continue in the coming

months. Total non-performing loans in Brazil remain relatively low at 2.8% of the total loan portfolio in

February, but have ticked higher since December 2014, and we will be watching closely for a further

Brazil Commercial Banking Report Q3 2015

© Business Monitor International Ltd Page 18

deterioration in asset quality in the coming months. Nevertheless, with most major banks remaining well

capitalised, we do not expect a significant increase in systemic risk in the banking sector in the next few

quarters.

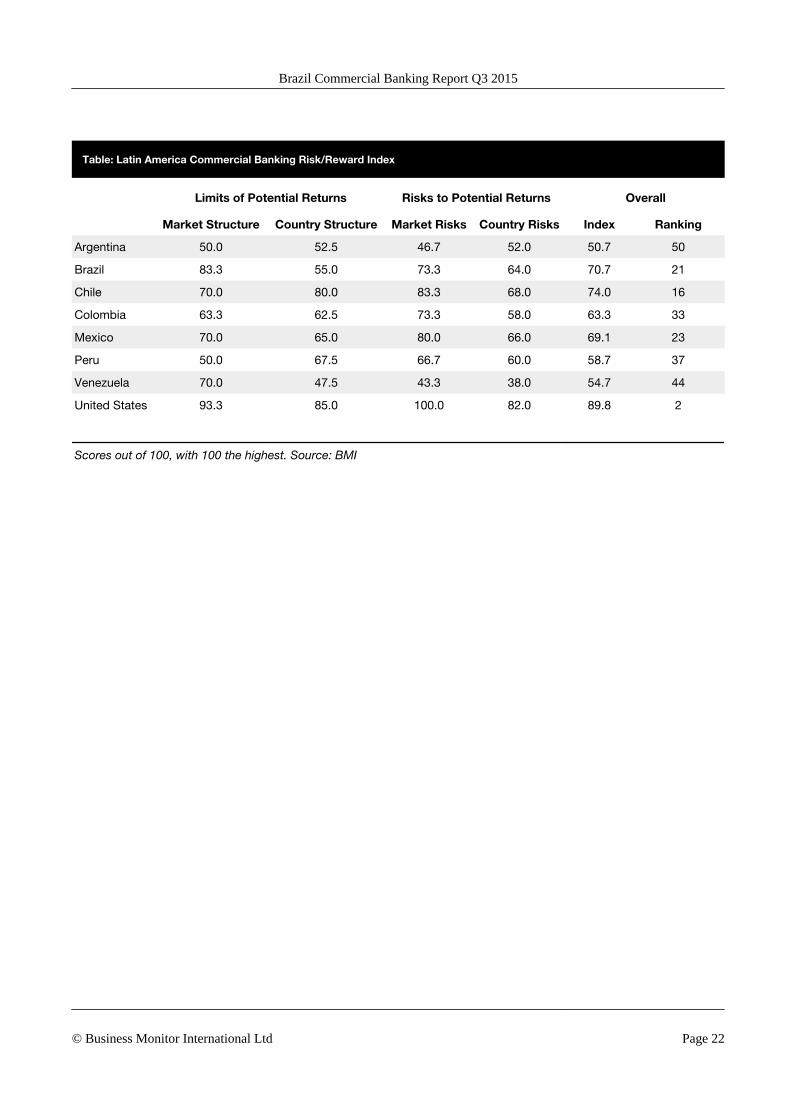

Risk/Reward Index Affirms Lacklustre Outlook

Given our view for notably slower asset and loan growth in the coming years, Brazil is highly unlikely to

re-take the top spot in our Commercial Banking Risk/Reward Index in the foreseeable future. Indeed, the

country's score dropped from 70.7 this quarter, from 71.4 previously, due to a decline in the 'country

rewards' sub-component. This came on the back of a weakening macroeconomic outlook for Brazil, in line

with our view that real GDP will contract in 2015 and see only a modest return to growth thereafter. With

the risks to our growth forecasts for the next few years lying primarily to the downside, with knock-on

effects for the banking sector, we see little to suggest a rebound in Brazil's Commercial Banking Risk/

Reward Index score in the next several months.

Brazil No Longer The Outperformer

Latin America - Commercial Banking Risk/Reward Index, Out Of 100

Brazil Chile Colombia Mexico Peru

2010 2011 2012 2013 2014 2015f

50

55

60

65

70

75

Source: BMI

Brazil Commercial Banking Report Q3 2015

© Business Monitor International Ltd Page 19

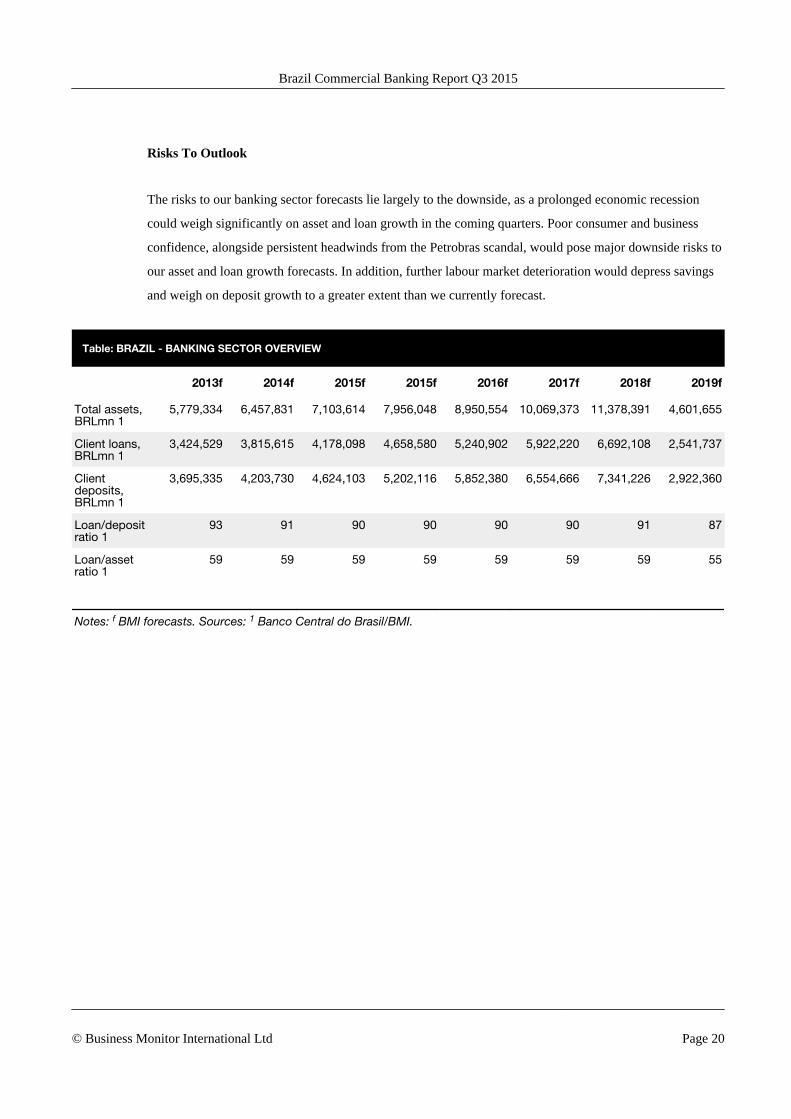

Risks To Outlook

The risks to our banking sector forecasts lie largely to the downside, as a prolonged economic recession

could weigh significantly on asset and loan growth in the coming quarters. Poor consumer and business

confidence, alongside persistent headwinds from the Petrobras scandal, would pose major downside risks to

our asset and loan growth forecasts. In addition, further labour market deterioration would depress savings

and weigh on deposit growth to a greater extent than we currently forecast.

Table: BRAZIL - BANKING SECTOR OVERVIEW

2013f 2014f 2015f 2015f 2016f 2017f 2018f 2019f

Total assets,BRLmn 1

5,779,334 6,457,831 7,103,614 7,956,048 8,950,554 10,069,373 11,378,391 4,601,655

Client loans,BRLmn 1

3,424,529 3,815,615 4,178,098 4,658,580 5,240,902 5,922,220 6,692,108 2,541,737

Clientdeposits,BRLmn 1

3,695,335 4,203,730 4,624,103 5,202,116 5,852,380 6,554,666 7,341,226 2,922,360

Loan/depositratio 1

93 91 90 90 90 90 91 87

Loan/assetratio 1

59 59 59 59 59 59 59 55

Notes: f BMI forecasts. Sources: 1 Banco Central do Brasil/BMI.

Brazil Commercial Banking Report Q3 2015

© Business Monitor International Ltd Page 20

Industry Risk Reward Ratings

Latin America Commercial Banking Risk/Reward Index

Commercial Banking Risk/Reward Index Methodology

Since Q108, we have described numerically the banking business environment for each of the countries

analysed by BMI. We do this through our Commercial Banking Industry Risk/Reward Index (RRI), a

measure that ensures we capture the latest quantitative information available. It also ensures consistency

across all countries. Like all of BMI's Industry Risk/Reward Indices, its takes into account the Rewards on

offer within the banking sector in a given country, but also the Risks to investors being able to realise those

opportunities. The overall index is weighted 70% towards Rewards and 30% towards Risks.

Within the Rewards category, we look at factors that are specific to the banking industry (accounting for

60% of the score within this category), and elements that relate to that country in general (accounting for

40% of the weighting). These include, but are not limited to, total assets, asset and loan growth, GDP and

taxation. Likewise on the Risks side, we look at industry-specific Risks (weighted 40% of the Risks total)

and country-specific Risks (weighted 60%). These include, but are not limited to, the regulatory framework

and environment, the competitive environment, financial risk, legal risk and policy continuity.

In general three aspects need to be borne in mind when interpreting the RRIs. The first is that the Industry

Rewards element is the most heavily weighted of the four elements, accounting for 42% (60% of 70%) of

the overall Index. Second, if the Industry Rewards score is significantly higher than the Country Rewards

score, within the Rewards category, it usually implies that the banking sector is (very) large and/or

developed relative to the general wealth, stability and financial infrastructure in the country. Conversely, if

the industry score is significantly lower, it usually means that the banking sector is small and/or

underdeveloped relative to the general wealth, stability and financial infrastructure in the country. Third,

within the Risks category, the industry-specific elements (i.e. how regulations affect the development of the

sector, how regulations affect competition within it, and Moody's Investor Services' Ratings for local

currency deposits) can be markedly different from BMI's long-term Country Risk Index for a given market.

Brazil Commercial Banking Report Q3 2015

© Business Monitor International Ltd Page 21

Table: Latin America Commercial Banking Risk/Reward Index

Limits of Potential Returns Risks to Potential Returns Overall

Market Structure Country Structure Market Risks Country Risks Index Ranking

Argentina 50.0 52.5 46.7 52.0 50.7 50

Brazil 83.3 55.0 73.3 64.0 70.7 21

Chile 70.0 80.0 83.3 68.0 74.0 16

Colombia 63.3 62.5 73.3 58.0 63.3 33

Mexico 70.0 65.0 80.0 66.0 69.1 23

Peru 50.0 67.5 66.7 60.0 58.7 37

Venezuela 70.0 47.5 43.3 38.0 54.7 44

United States 93.3 85.0 100.0 82.0 89.8 2

Scores out of 100, with 100 the highest. Source: BMI

Brazil Commercial Banking Report Q3 2015

© Business Monitor International Ltd Page 22

Market Overview

Latin America Commercial Banking Outlook

Table: Banks' Bond Portfolios, 2013

Bond Portfolio, USDbn Bond as % total assets Year-on-year growth %

Argentina 19.2 12.4 7.2

Brazil 725.5 29.7 1.5

Chile 35.0 11.6 9.0

Colombia 43.4 19.7 15.5

Mexico 46.7 9.3 2.6

Peru 6.1 6.5 9.3

Venezuela 70.8 29.2 78.2

United States 486.5 3.5 -8.5

Source: Central banks, regulators, BMI.

Table: Comparison of Loan/Deposit & Loan/Asset & Loan/GDP ratios, 2015

Loan/Deposit

ratio % Rank TrendLoan/Asset

ratio % Rank TrendLoan/GDP

ratio % Rank Trend

Argentina 61.7 69 Falling 42.4 63 Falling 12.1 73 Falling

Brazil 90.4 35 Falling 58.8 35 Falling 74.1 30 Rising

Chile 125.6 6 Rising 69.4 9 Falling 91.5 24 Rising

Colombia 107.5 22 Rising 65.3 19 Rising 43.4 53 Rising

Mexico 91.7 33 Falling 48.2 55 Rising 20.0 67 Rising

Peru 112.0 17 Rising 65.6 21 Rising 34.7 59 Rising

Venezuela 56.5 70 Rising 48.0 58 Rising 37.7 56 Rising

United States 104.8 20 Rising 73.1 7 Rising 64.5 37 Rising

Source: Central banks, regulators, BMI.

Brazil Commercial Banking Report Q3 2015

© Business Monitor International Ltd Page 23

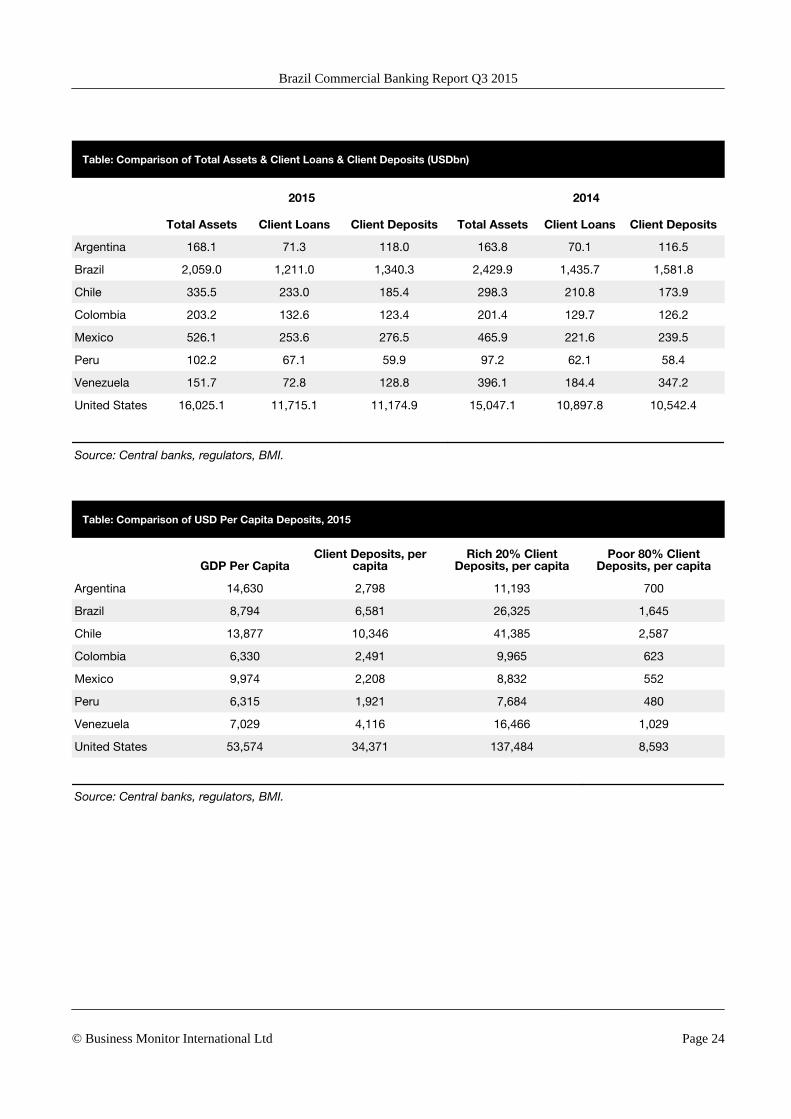

Table: Comparison of Total Assets & Client Loans & Client Deposits (USDbn)

2015 2014

Total Assets Client Loans Client Deposits Total Assets Client Loans Client Deposits

Argentina 168.1 71.3 118.0 163.8 70.1 116.5

Brazil 2,059.0 1,211.0 1,340.3 2,429.9 1,435.7 1,581.8

Chile 335.5 233.0 185.4 298.3 210.8 173.9

Colombia 203.2 132.6 123.4 201.4 129.7 126.2

Mexico 526.1 253.6 276.5 465.9 221.6 239.5

Peru 102.2 67.1 59.9 97.2 62.1 58.4

Venezuela 151.7 72.8 128.8 396.1 184.4 347.2

United States 16,025.1 11,715.1 11,174.9 15,047.1 10,897.8 10,542.4

Source: Central banks, regulators, BMI.

Table: Comparison of USD Per Capita Deposits, 2015

GDP Per CapitaClient Deposits, per

capitaRich 20% Client

Deposits, per capitaPoor 80% Client

Deposits, per capita

Argentina 14,630 2,798 11,193 700

Brazil 8,794 6,581 26,325 1,645

Chile 13,877 10,346 41,385 2,587

Colombia 6,330 2,491 9,965 623

Mexico 9,974 2,208 8,832 552

Peru 6,315 1,921 7,684 480

Venezuela 7,029 4,116 16,466 1,029

United States 53,574 34,371 137,484 8,593

Source: Central banks, regulators, BMI.

Brazil Commercial Banking Report Q3 2015

© Business Monitor International Ltd Page 24

Economic Analysis

BMI View: In light of a poor business environment, weak consumer confidence and a lacklustre external

environment, there is little upside for Brazilian real GDP growth in the next several years. A nascent policy

shift will gradually regain investor confidence following years of unorthodox economic policies, but will be

slow to translate into a significant uptick in growth.

Brazilian real GDP growth will remain anaemic in the coming years. A less favourable external

environment in light of an ongoing slowdown in Chinese growth, a poor domestic business environment

and lack of export competitiveness pose significant headwinds to growth. Brazil is in the early stages of an

economic policy shift with new Finance Minister Joaquim Levy set to reverse the fiscal deterioration of

recent years, and a central bank that is more committed to reining in inflation (see 'On The Cusp Of An

Economic Policy Shift', December 1 2014). However, consumer and business confidence will be slow to

recover given the unorthodox economic policies in place during President Dilma Rousseff's first term. In

addition, interest rates will continue heading higher in the coming months, constraining consumers' take-up

of credit and weighing on household spending. A reduction in government expenditures will also remove

support for growth. As a result, we have downgraded our 2015 real GDP growth forecast to 0.6% from

1.0% previously, implying a more moderate uptick from an estimated 0.2% expansion in 2014.

Brazil Commercial Banking Report Q3 2015

© Business Monitor International Ltd Page 25

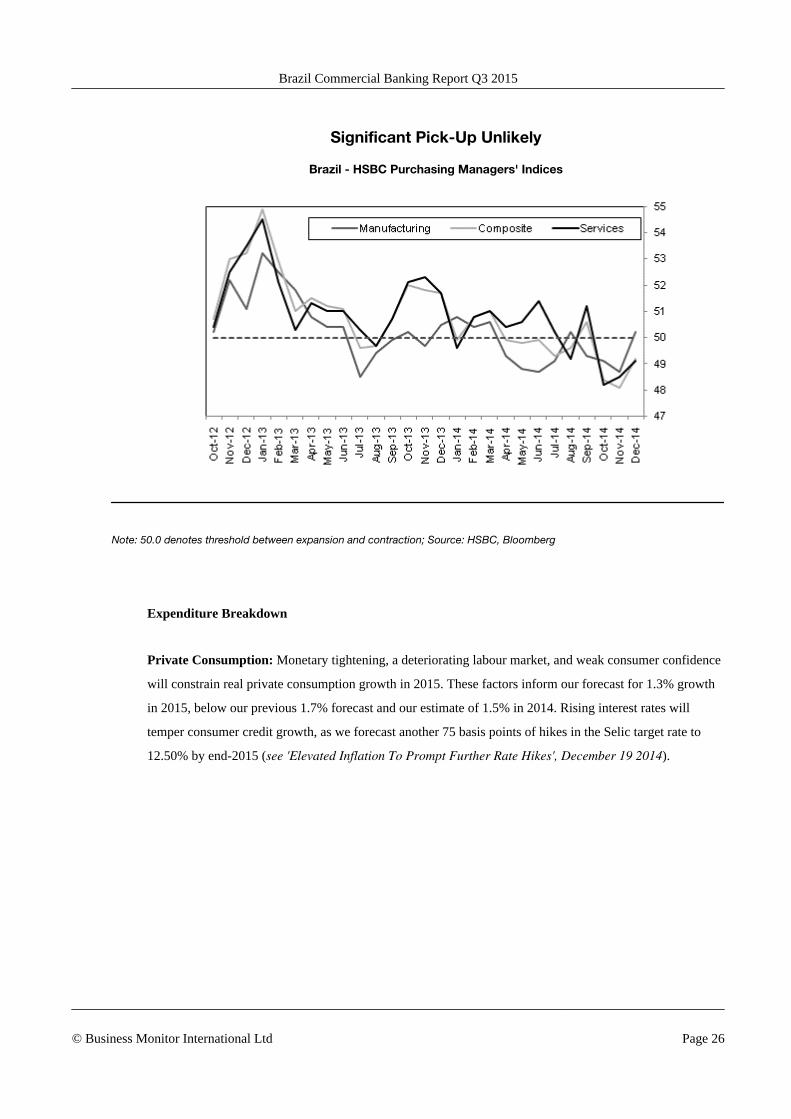

Significant Pick-Up Unlikely

Brazil - HSBC Purchasing Managers' Indices

Note: 50.0 denotes threshold between expansion and contraction; Source: HSBC, Bloomberg

Expenditure Breakdown

Private Consumption: Monetary tightening, a deteriorating labour market, and weak consumer confidence

will constrain real private consumption growth in 2015. These factors inform our forecast for 1.3% growth

in 2015, below our previous 1.7% forecast and our estimate of 1.5% in 2014. Rising interest rates will

temper consumer credit growth, as we forecast another 75 basis points of hikes in the Selic target rate to

12.50% by end-2015 (see 'Elevated Inflation To Prompt Further Rate Hikes', December 19 2014).

Brazil Commercial Banking Report Q3 2015

© Business Monitor International Ltd Page 26

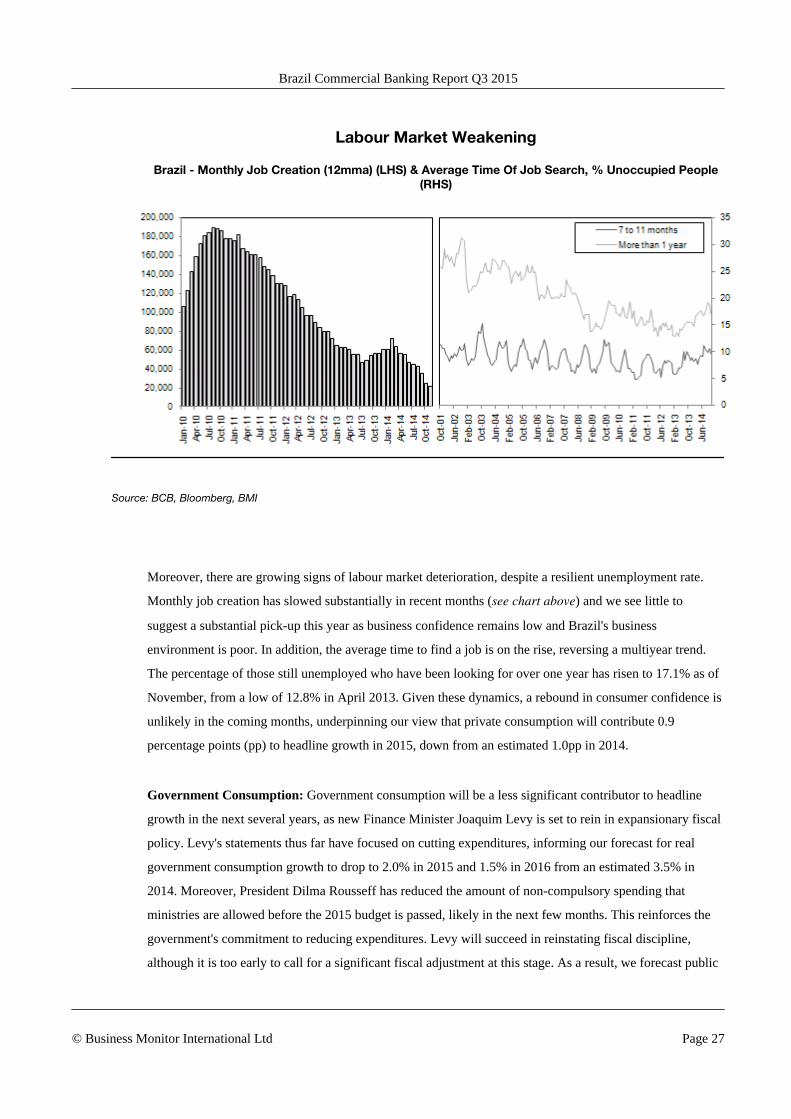

Labour Market Weakening

Brazil - Monthly Job Creation (12mma) (LHS) & Average Time Of Job Search, % Unoccupied People(RHS)

Source: BCB, Bloomberg, BMI

Moreover, there are growing signs of labour market deterioration, despite a resilient unemployment rate.

Monthly job creation has slowed substantially in recent months (see chart above) and we see little to

suggest a substantial pick-up this year as business confidence remains low and Brazil's business

environment is poor. In addition, the average time to find a job is on the rise, reversing a multiyear trend.

The percentage of those still unemployed who have been looking for over one year has risen to 17.1% as of

November, from a low of 12.8% in April 2013. Given these dynamics, a rebound in consumer confidence is

unlikely in the coming months, underpinning our view that private consumption will contribute 0.9

percentage points (pp) to headline growth in 2015, down from an estimated 1.0pp in 2014.

Government Consumption: Government consumption will be a less significant contributor to headline

growth in the next several years, as new Finance Minister Joaquim Levy is set to rein in expansionary fiscal

policy. Levy's statements thus far have focused on cutting expenditures, informing our forecast for real

government consumption growth to drop to 2.0% in 2015 and 1.5% in 2016 from an estimated 3.5% in

2014. Moreover, President Dilma Rousseff has reduced the amount of non-compulsory spending that

ministries are allowed before the 2015 budget is passed, likely in the next few months. This reinforces the

government's commitment to reducing expenditures. Levy will succeed in reinstating fiscal discipline,

although it is too early to call for a significant fiscal adjustment at this stage. As a result, we forecast public

Brazil Commercial Banking Report Q3 2015

© Business Monitor International Ltd Page 27

consumption to contribute 0.4pp and 0.3pp to headline growth in 2015 and 2016 respectively, down from an

estimated 0.7pp in 2014.

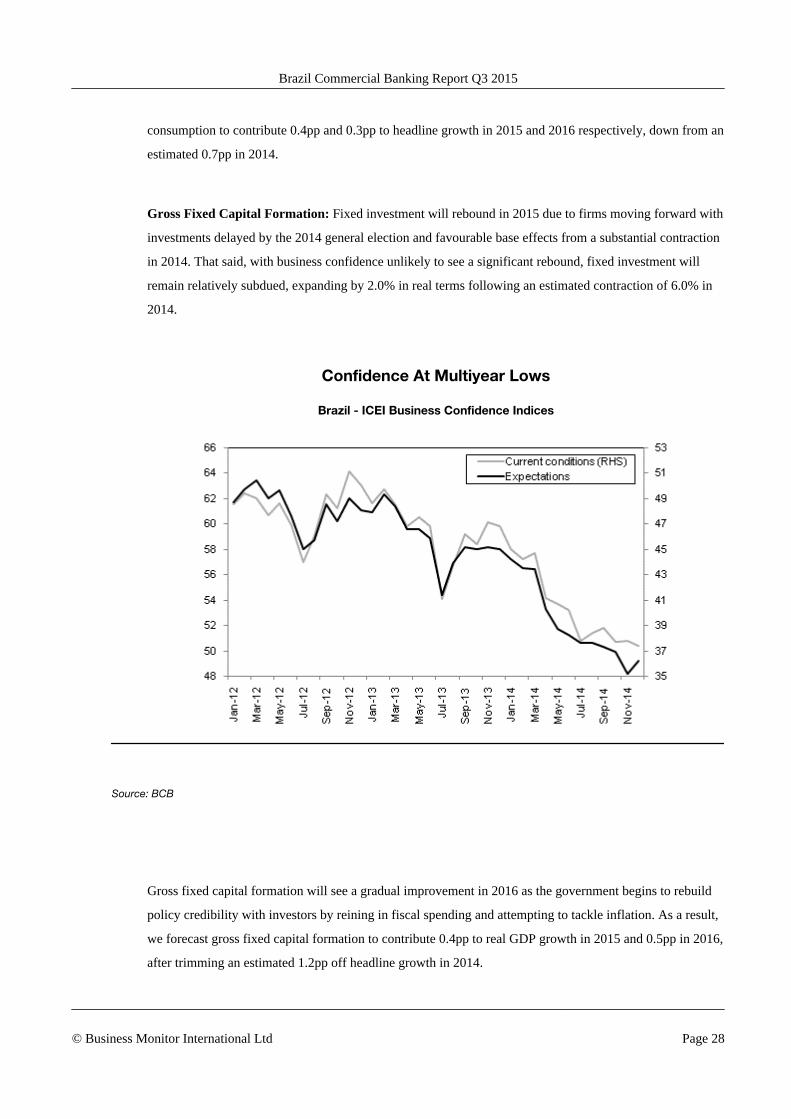

Gross Fixed Capital Formation: Fixed investment will rebound in 2015 due to firms moving forward with

investments delayed by the 2014 general election and favourable base effects from a substantial contraction

in 2014. That said, with business confidence unlikely to see a significant rebound, fixed investment will

remain relatively subdued, expanding by 2.0% in real terms following an estimated contraction of 6.0% in

2014.

Confidence At Multiyear Lows

Brazil - ICEI Business Confidence Indices

Source: BCB

Gross fixed capital formation will see a gradual improvement in 2016 as the government begins to rebuild

policy credibility with investors by reining in fiscal spending and attempting to tackle inflation. As a result,

we forecast gross fixed capital formation to contribute 0.4pp to real GDP growth in 2015 and 0.5pp in 2016,

after trimming an estimated 1.2pp off headline growth in 2014.

Brazil Commercial Banking Report Q3 2015

© Business Monitor International Ltd Page 28

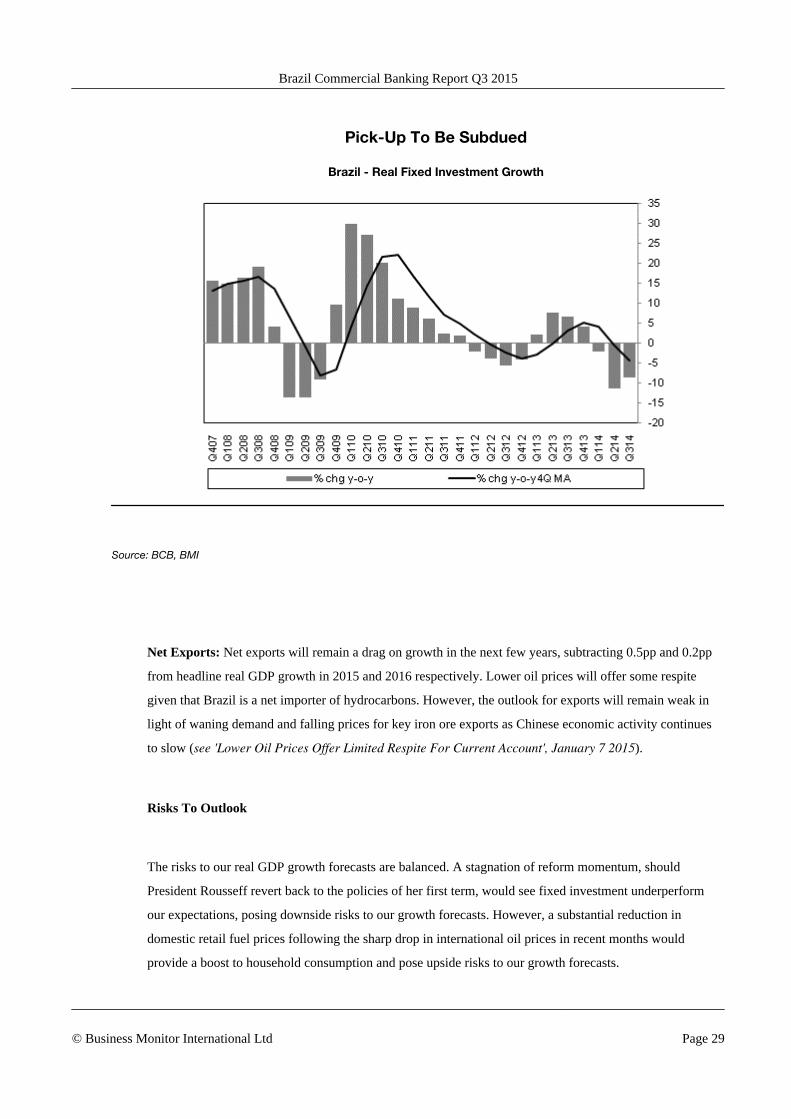

Pick-Up To Be Subdued

Brazil - Real Fixed Investment Growth

Source: BCB, BMI

Net Exports: Net exports will remain a drag on growth in the next few years, subtracting 0.5pp and 0.2pp

from headline real GDP growth in 2015 and 2016 respectively. Lower oil prices will offer some respite

given that Brazil is a net importer of hydrocarbons. However, the outlook for exports will remain weak in

light of waning demand and falling prices for key iron ore exports as Chinese economic activity continues

to slow (see 'Lower Oil Prices Offer Limited Respite For Current Account', January 7 2015).

Risks To Outlook

The risks to our real GDP growth forecasts are balanced. A stagnation of reform momentum, should

President Rousseff revert back to the policies of her first term, would see fixed investment underperform

our expectations, posing downside risks to our growth forecasts. However, a substantial reduction in

domestic retail fuel prices following the sharp drop in international oil prices in recent months would

provide a boost to household consumption and pose upside risks to our growth forecasts.

Brazil Commercial Banking Report Q3 2015

© Business Monitor International Ltd Page 29

Table: GDP By Expenditure (Brazil 2012-2019)

2012 2013 2014e 2015f 2016f 2017f 2018f 2019f

Private final consumption,BRLbn 2,750.2 3,033.7 3,273.2 3,518.0 3,778.0 4,061.8 4,367.0 4,711.2

Private final consumption,USDbn 1,406.9 1,405.6 1,389.7 1,379.6 1,453.1 1,544.4 1,699.2 1,884.5

Private final consumption, realgrowth % y-o-y 3.2 2.6 1.5 1.3 1.6 2.1 2.2 2.5

Government finalconsumption, BRLbn 935.8 1,064.5 1,171.2 1,267.5 1,359.8 1,454.8 1,558.0 1,672.6

Government finalconsumption, USDbn 478.7 493.2 497.3 497.1 523.0 553.2 606.2 669.0

Government finalconsumption, real growth %y-o-y

3.3 2.0 3.5 2.0 1.5 1.6 1.8 2.0

Fixed capital formation,BRLbn 798.1 880.9 891.0 977.9 1,078.5 1,195.3 1,337.6 1,489.6

Fixed capital formation,USDbn 408.3 408.2 378.3 383.5 414.8 454.5 520.5 595.9

Fixed capital formation, realgrowth % y-o-y -4.0 5.2 -6.0 2.0 2.5 3.0 4.0 3.5

Exports of goods andservices, BRLbn 552.8 608.2 632.4 687.2 717.6 754.8 768.4 782.5

Exports of goods andservices, USDbn 282.8 281.8 268.5 269.5 276.0 287.0 299.0 313.0

Exports of goods andservices, real growth % y-o-y 0.5 2.5 -3.5 0.9 -3.0 -2.3 -5.5 -5.4

Imports of goods andservices, BRLbn 616.4 728.5 756.3 831.3 871.0 912.6 925.2 927.5

Imports of goods andservices, USDbn 315.3 337.5 321.1 326.0 335.0 347.0 360.0 371.0

Imports of goods andservices, real growth % y-o-y 0.2 8.3 -2.2 3.6 -1.2 -1.2 -4.4 -5.5

Net exports of goods andservices, BRLbn -63.5 -120.3 -123.9 -144.1 -153.4 -157.8 -156.8 -145.0

Net exports of goods andservices, USDbn -32.5 -55.7 -52.6 -56.5 -59.0 -60.0 -61.0 -58.0

Net exports of goods andservices, real growth % y-o-y -0.9 32.6 2.0 11.8 3.7 1.6 -1.9 -5.7

e/f=BMI estimate/forecast; Source: IBGE/IMF

Brazil Commercial Banking Report Q3 2015

© Business Monitor International Ltd Page 30

Competitive Landscape

Market Structure

Protagonists

Table: Protagonists In Brazil's Commercial Banking Sector

Central bank: Banco Central do Brasil (BCB)

www.bcb.gov.br

Established in 1964, BCB supersedes the previous monetary authorities Banco do Brasil, the National Treasury and theSuperintendency of Currency and Credit. The central bank is governed by the Complementary Law of the NationalFinancial System that describes its activities and structure. BCB is responsible for monetary policy and foreign exchangepolicy. It is also issues notes and is the manager of the national payments system. It regulates the banks and some otherfinancial institutions and is banker to the banks. However, Banco do Brasil remains banker to the government to asignificant extent.

Principal banking regulator: Banco Central do Brasil (BCB)

www.bcb.gov.br

Alongside its other functions, BCB is the principal regulator of the banks.

Banking trade association: Federação Brasileira de Bancos (Febraban)

www.febraban.org.br

Febraban, established in 1967, is the main trade association of the Brazilian commercial banking sector. Its membershipincludes 121 financial institutions, representing 97% of total banking system assets at end-2013. It lobbies to thegovernment on behalf of its members and seeks to improve the efficiency and reach of the Brazilian financial system.

Banking trade association: Associação Brasileira de Bancos Internacionais (ABBI)

www.abbi.com.br

ABBI's aim is to bring together and represent the international banks in Brazil. Its membership also includes major lawfirms and other service providers.

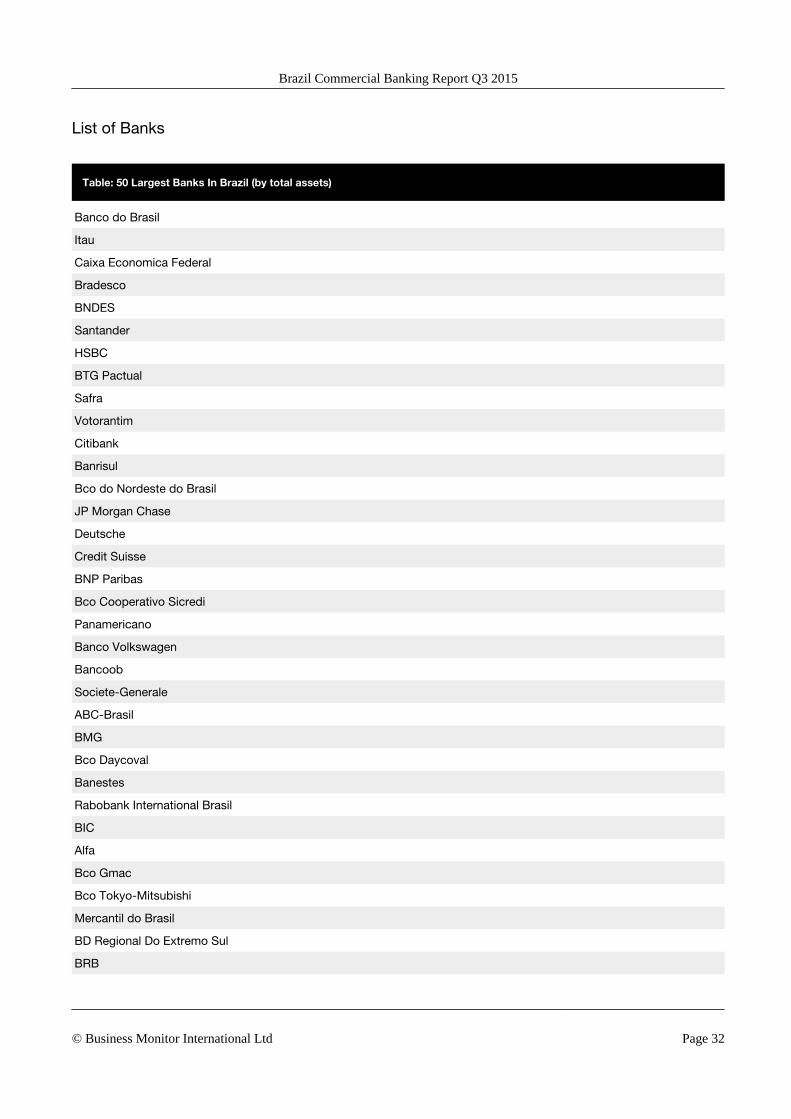

Definition Of The Commercial Banking Universe

According to the Banco Central do Brasil (BCB), there were 132 multiple banks and 22 commercial banks

(including full branches of foreign banks) operating in Brazil as of November 2014. The central bank

currently lists the 50 largest banks as of September 2014.

Brazil Commercial Banking Report Q3 2015

© Business Monitor International Ltd Page 31

List of Banks

Table: 50 Largest Banks In Brazil (by total assets)

Banco do Brasil

Itau

Caixa Economica Federal

Bradesco

BNDES

Santander

HSBC

BTG Pactual

Safra

Votorantim

Citibank

Banrisul

Bco do Nordeste do Brasil

JP Morgan Chase

Deutsche

Credit Suisse

BNP Paribas

Bco Cooperativo Sicredi

Panamericano

Banco Volkswagen

Bancoob

Societe-Generale

ABC-Brasil

BMG

Bco Daycoval

Banestes

Rabobank International Brasil

BIC

Alfa

Bco Gmac

Bco Tokyo-Mitsubishi

Mercantil do Brasil

BD Regional Do Extremo Sul

BRB

Brazil Commercial Banking Report Q3 2015

© Business Monitor International Ltd Page 32

50 Largest Banks In Brazil (by total assets) - Continued

Morgan Stanley

Bco Da Amazonia

BOFA Merrill Lynch

Mercedez-Benz

Pine

Barclays

Bco Fibra

BES

Banco IBM

Banco CNH Industrial Capital

Credit Agricole

Bco Classico

Bco Des. De MG

Bco de Lage Landen Brasil

J Malucelli

Banco Fidis

Source: BCB, September 2014

Brazil Commercial Banking Report Q3 2015

© Business Monitor International Ltd Page 33

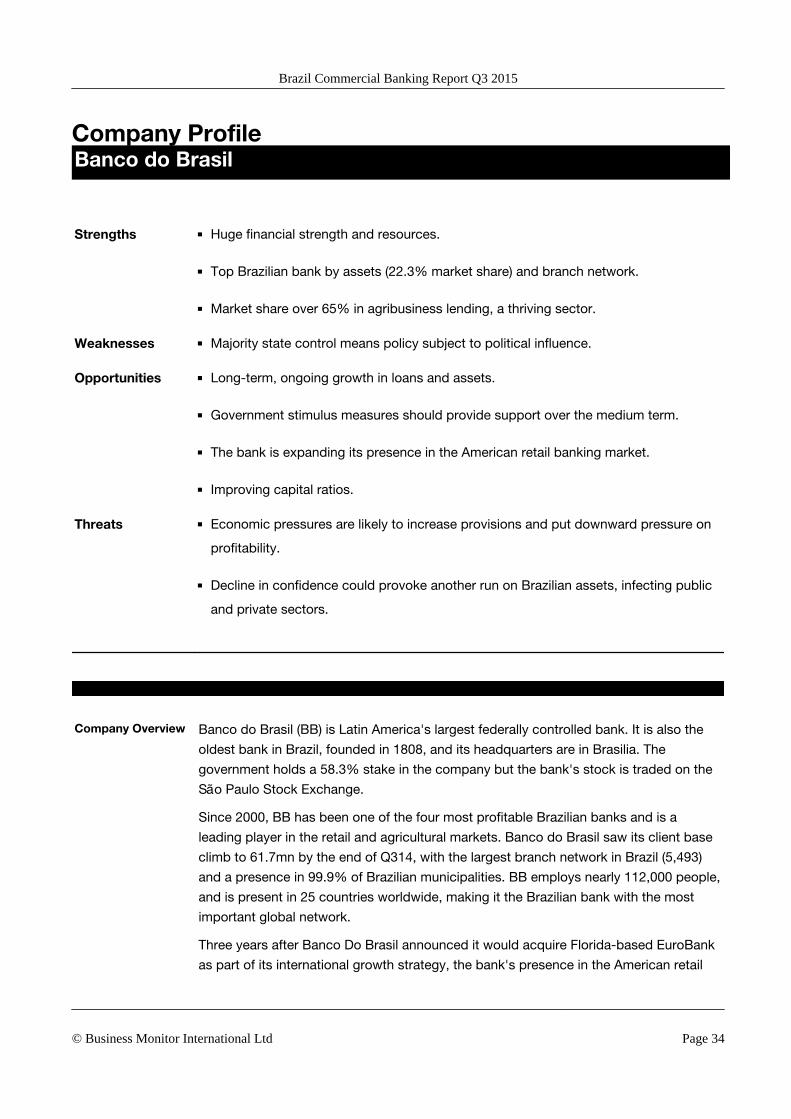

Company ProfileBanco do Brasil

SWOT Analysis

Strengths ■ Huge financial strength and resources.

■ Top Brazilian bank by assets (22.3% market share) and branch network.

■ Market share over 65% in agribusiness lending, a thriving sector.

Weaknesses ■ Majority state control means policy subject to political influence.

Opportunities ■ Long-term, ongoing growth in loans and assets.

■ Government stimulus measures should provide support over the medium term.

■ The bank is expanding its presence in the American retail banking market.

■ Improving capital ratios.

Threats ■ Economic pressures are likely to increase provisions and put downward pressure on

profitability.

■ Decline in confidence could provoke another run on Brazilian assets, infecting public

and private sectors.

Company Overview Banco do Brasil (BB) is Latin America's largest federally controlled bank. It is also the

oldest bank in Brazil, founded in 1808, and its headquarters are in Brasilia. The

government holds a 58.3% stake in the company but the bank's stock is traded on the

São Paulo Stock Exchange.

Since 2000, BB has been one of the four most profitable Brazilian banks and is a

leading player in the retail and agricultural markets. Banco do Brasil saw its client base

climb to 61.7mn by the end of Q314, with the largest branch network in Brazil (5,493)

and a presence in 99.9% of Brazilian municipalities. BB employs nearly 112,000 people,

and is present in 25 countries worldwide, making it the Brazilian bank with the most

important global network.

Three years after Banco Do Brasil announced it would acquire Florida-based EuroBank

as part of its international growth strategy, the bank's presence in the American retail

Brazil Commercial Banking Report Q3 2015

© Business Monitor International Ltd Page 34

banking market continues to grow. The takeover was completed with the launch of

Banco do Brasil Americas in October 2012, and now has five branches in Florida.

The bank's key goals through to 2018 include increasing efficiency and productivity and

producing sustainable results, while also continuing to expand internationally. In

November 2013, the bank issued its first bond denominated in Swiss francs, as part of

an effort to diversify its customer base.

In November 2014, Banco do Brasil announced that it will form a US$4.5bn joint

venture with Cielo, the country's largest card-payment processor, to manage debit and

credit card transactions. BB will hold a 30% share of capital in the new company, but

counting its holdings in Cielo, it will indirectly hold a 50% stake in it overall.

Corporate

HighlightsThe bank was hit hard by the global financial crisis and resulting provisions, though

recovered strongly. According to the latest available data from the company's quarterly

financial statements, Banco do Brasil recorded net income of BRL8.3bn in the first three

quarters of 2014, an increase of 5.0% compared to the profit reported in the same

period of the previous year. The increase in profit was supported by a 7.3% hike in net

interest income to BRL36.7bn.

In keeping with its strategic plan of maintaining its position as the leading Brazilian

bank, the loan portfolio expanded by 12.3% y-o-y to reach BRL732.7bn as of

September 30 2014. Over the same period the bank also saw its total assets rise by

13.7% to BRL1.43trn, up from BRL1.26trn a year earlier.

Banco do Brasil's Core Tier 1 capital ratio stood at 9.3% at end-September 2014, up for

8.4% a year earlier. The Capital Adequacy Ratio also improved from 15.3% to 16.0%

over the same period.

As of end September 2014, BB had a long-term credit rating of 'BBB' at Fitch, 'Baa2' at

Moody's, and 'BBB-' at Standard & Poor's.

Company Data ■ Website: www.bb.com.br

Brazil Commercial Banking Report Q3 2015

© Business Monitor International Ltd Page 35

Table: Stock Market Indicators

2008 2009 2010 2011 2012 2013 2014 17-Apr-2015

Market Capitalisation BRL 37,319 76,275 89,884 67,910 73,355 69,916 68,111 72,610

Market Capitalisation USD 15,977 43,786 54,101 36,405 35,888 29,619 25,725 23,823

Share Price BRL 14.68 29.70 31.42 23.70 25.60 24.40 23.77 25.34

Share Price USD 6.28 17.05 18.91 12.71 12.52 10.34 8.98 8.31

Share Price USD, % change (eop) -63.3 171.3 10.9 -32.8 -1.4 -17.5 -13.1 n.a.

Change, year-to-date n.a. n.a. n.a. n.a. n.a. n.a. n.a. -7.4

Shares Outstanding (mn) 2,568 2,569 2,861 2,865 2,845 2,809 2,797 n.a.

Source: BB (Banco du Brazil), Bloomberg

Table: Balance Sheet (BRLmn)

2008 2009 2010 2011 2012 2013 2014

Total Assets 521,273 702,572 802,820 966,823 1,136,007 1,303,915 1,278,137

Loans & Mortgages 193,849 286,001 338,388 399,032 498,071 561,494 631,633

Total Deposits 256,776 327,102 359,301 429,177 455,515 491,013 437,822

Total Shareholders' Equity 29,937 40,521 54,419 63,269 69,898 72,225 85,440

Earnings per share (BRL) 3.43 5.24 4.17 4.43 3.93 5.58 4.23

Source: BB (Banco du Brazil), Bloomberg

Table: Balance Sheet (USDmn)

2008 2009 2010 2011 2012 2013 2014

Total Assets 225,220 403,313 483,626 518,877 554,556 551,945 482,899

Loans & Mortgages 83,754 164,180 203,848 214,154 243,139 237,680 238,640

Total Deposits 110,942 187,774 216,447 230,332 222,365 207,845 165,416

Total Shareholders' Equity 12,935 23,261 32,782 33,955 34,122 30,573 32,281

Earnings per share (USD) 1.90 2.66 2.37 2.65 2.02 2.60 1.80

Source: BB (Banco du Brazil), Bloomberg

Brazil Commercial Banking Report Q3 2015

© Business Monitor International Ltd Page 36

Table: Key Ratios (%)

2008 2009 2010 2011 2012 2013 2014

Return on Assets 2.0 2.2 1.5 1.4 1.1 1.3 0.9

Return on Equities 32.5 38.2 23.8 21.7 17.1 22.7 15.7

Loan Deposit Ratio 80.7 91.1 97.2 95.8 112.9 119.0 148.6

Loan Asset Ratio 39.7 42.4 43.5 42.5 45.3 44.8 50.9

Equity Asset Ratio 5.7 5.8 6.8 6.5 6.1 5.3 6.4

Total Risk Based Capital Ratio 15.6 13.8 14.1 14.0 14.8 14.5 16.1

Tier 1 Capital Ratio 15.2 10.6 11.0 10.5 10.6 10.5 11.4

Source: BB (Banco du Brazil), Bloomberg

Brazil Commercial Banking Report Q3 2015

© Business Monitor International Ltd Page 37

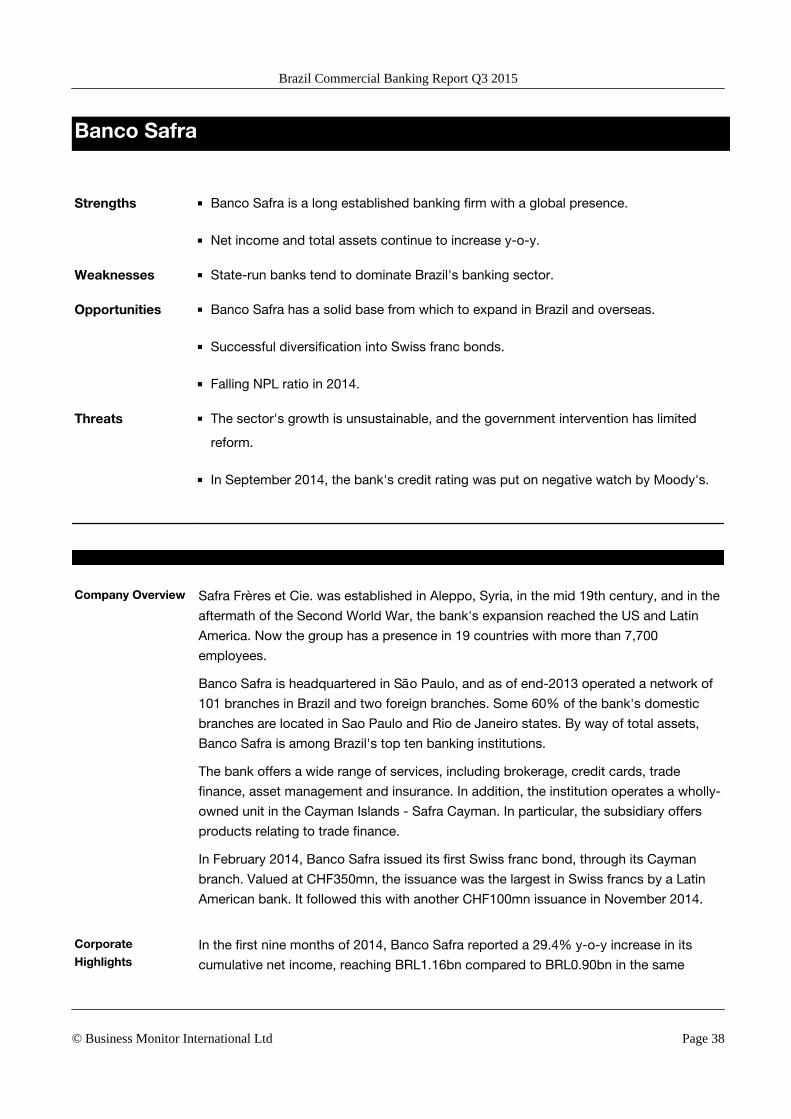

Banco Safra

SWOT Analysis

Strengths ■ Banco Safra is a long established banking firm with a global presence.

■ Net income and total assets continue to increase y-o-y.

Weaknesses ■ State-run banks tend to dominate Brazil's banking sector.

Opportunities ■ Banco Safra has a solid base from which to expand in Brazil and overseas.

■ Successful diversification into Swiss franc bonds.

■ Falling NPL ratio in 2014.

Threats ■ The sector's growth is unsustainable, and the government intervention has limited

reform.

■ In September 2014, the bank's credit rating was put on negative watch by Moody's.

Company Overview Safra Frères et Cie. was established in Aleppo, Syria, in the mid 19th century, and in the

aftermath of the Second World War, the bank's expansion reached the US and Latin

America. Now the group has a presence in 19 countries with more than 7,700

employees.

Banco Safra is headquartered in São Paulo, and as of end-2013 operated a network of

101 branches in Brazil and two foreign branches. Some 60% of the bank's domestic

branches are located in Sao Paulo and Rio de Janeiro states. By way of total assets,

Banco Safra is among Brazil's top ten banking institutions.

The bank offers a wide range of services, including brokerage, credit cards, trade

finance, asset management and insurance. In addition, the institution operates a wholly-

owned unit in the Cayman Islands - Safra Cayman. In particular, the subsidiary offers

products relating to trade finance.

In February 2014, Banco Safra issued its first Swiss franc bond, through its Cayman

branch. Valued at CHF350mn, the issuance was the largest in Swiss francs by a Latin

American bank. It followed this with another CHF100mn issuance in November 2014.

Corporate

HighlightsIn the first nine months of 2014, Banco Safra reported a 29.4% y-o-y increase in its

cumulative net income, reaching BRL1.16bn compared to BRL0.90bn in the same

Brazil Commercial Banking Report Q3 2015

© Business Monitor International Ltd Page 38

period of 2013. This came despite a 6.9% y-o-y increase in administrative expenses

during the same period.

The bank also saw its total assets rise to BRL137.6bn by September 30 2014, up 4.2%

y-o-y from BRL132.0bn in September 2013.

In September 2014, Moody's Investors Service downgraded the credit rating outlook for

several Brazilian banks, including Banco Safra, to negative from stable, in line with the

outlook for the country's sovereign debt. Banco Safra has been rated Baa2 by Moody's

since October 2012. Its equivalent long-term credit rating at Fitch is 'BBB' (stable

outlook) and at Standard & Poor's it is 'BBB-' (stable outlook).

The bank's non-performing loan ration fell to 0.99% in September 2014, from 1.70% a

year earlier.

Table: Balance Sheet (BRLmn)

2008 2009 2010 2011 2012

Total Assets 61,940 65,863 73,313 86,867 111,452

Loans & Mortgages 22,421 25,196 36,478 46,824 47,169

Total Deposits 14,695 13,679 14,567 16,501 11,959

Total Shareholders' Equity 4,126 4,907 5,614 6,016 7,247

Earnings per share (BRL) 776.64 839.15 925.42 0.86 0.85

Source: Bank Safra, Bloomberg

Table: Balance Sheet (USDmn)

2008 2009 2010 2011 2012

Total Assets 26,762 37,809 44,165 46,620 54,407

Loans & Mortgages 9,687 14,464 21,975 25,129 23,026

Total Deposits 6,349 7,853 8,775 8,856 5,838

Total Shareholders' Equity 1,783 2,817 3,382 3,228 3,538

Earnings per share (USD) 431.05 425.51 526.43 0.52 0.44

Source: Bank Safra, Bloomberg

Brazil Commercial Banking Report Q3 2015

© Business Monitor International Ltd Page 39

Table: Key Ratios (%)

2008 2009 2010 2011 2012

Return on Assets n.a. 1.4 1.5 1.6 1.3

Return on Equities n.a. 20.2 19.9 21.6 19.3

Equity Asset Ratio 6.7 7.4 7.7 6.9 6.5

Source: Bank Safra, Bloomberg

Brazil Commercial Banking Report Q3 2015

© Business Monitor International Ltd Page 40

BradescoSWOT Analysis

Strengths ■ Strong brand and revenue growth in recent years.

■ Wide spread of lending to a range of businesses and organisations in Brazil and

worldwide.

■ Successfully raising capital internationally.

Weaknesses ■ Government measures to curb credit growth are impacting lending.

Opportunities ■ Long-term growth in lending and deposits.

■ A slowdown in the expansion of lending by state banks could create room for private

lenders.

■ Strong growth in net income in first nine months of 2014.

Threats ■ Bradesco may experience increases in its level of past due loans as its loans and

advances portfolio becomes more seasoned.

Company Overview Bradesco, based in Osasco, São Paulo, was the largest private bank in Brazil until the

merger of Banco Itaú and Unibanco. It remains a giant institution, with reported assets

of BRL879bn at end-2012, and it ranks as one of Brazil's biggest private-sector

employers with 98,849 staff. It has 74,028 service points around Brazil, including 4,659

branches and over 48,000 ATMs. It lends to individuals, major local and international

corporations and organisations, and to small and medium-sized businesses.

In 2011, the bank opened over 1,000 new branches in a major expansion drive, and

strengthened its position in Brazil via the acquisition of Banco do Estado do Rio de

Janeiro (BANERJ) from the local government, which gave Bradesco responsibility for

handling the state's civil service payroll. In 2012, it launched Bradesco Next, a hi-tech

'branch of the future' offering personalised financial services via digital avatars,

continuing a strategy of being a regional pioneer in internet and digital banking.

It now has offices in New York, London, Buenos Aires, Mexico City, Grand Cayman,

Hong Kong, London, Luxembourg and Tokyo, and an extended network of

correspondent banks.

In November 2014 the head of Bradesco's Asset Management Unit, Joaquim Levy, was

named Finance Minister in the new cabinet following the re-election of President Dilma

Brazil Commercial Banking Report Q3 2015

© Business Monitor International Ltd Page 41

Rousseff in October. He was replaced by Reinaldo Le Grazie, former head of fixed

income and hedge funds.

Corporate

HighlightsFor the first three quarters of 2014 (latest available figures), Bradesco reported an

impressive 28.2% y-o-y increase in cumulative net income to reach BRL3.95bn, up

from BRL3.08bn in the same period of 2013. This was supported by a 14.5% y-o-y

increase in net interest income over the same nine-month period.

At the end of September 2014, total assets stood at BRL987.4bn, up 8.8% y-o-y from

BRL907.7bn reported in September 2013. Over the same period loans to customers

increased by 7.7% y-o-y to BRL444.2bn, while total deposits were down 2.3% to

BRL211.9bn.

The bank's non-performing loan ratio remained steady at 4.4% as of end-September

2014, while Tier 1 and total capital ratios stood at 12.6% and 16.3%, respectively, at

the same period.

Bradesco has a long-term credit rating of BBB+ at Fitch, Baa1 at Moody's, and BBB- at

Standard & Poor's.

Company Data ■ Website: www.bradesco.com.br■ Status: Private Sector Bank

Table: Stock Market Indicators

2008 2009 2010 2011 2012 2013 2014 17-Apr-2015

Market Capitalisation BRL 65,358 103,389 111,588 107,171 132,166 128,406 145,950 156,157

Market Capitalisation USD 27,981 59,351 67,165 57,452 64,660 54,398 55,123 51,238

Share Price BRL 14.03 22.59 24.63 23.26 26.64 24.24 29.22 31.15

Share Price USD 6.00 12.97 14.83 12.47 13.04 10.27 11.03 10.22

Share Price USD, % change (eop) -53.8 115.9 14.3 -15.9 4.5 -21.2 7.4 n.a.

Change, year-to-date n.a. n.a. n.a. n.a. n.a. n.a. n.a. -7.3

Shares Outstanding (mn) 4,923 5,486 4,966 5,040 5,543 5,036 5,034 n.a.

Source: Bradesco, Bloomberg

Brazil Commercial Banking Report Q3 2015

© Business Monitor International Ltd Page 42

Table: Balance Sheet (BRLmn)

2008 2009 2010 2011 2012 2013 2014

Total Assets 435,290 496,815 621,612 722,087 799,541 838,302 930,451

Loans & Mortgages 164,517 165,362 204,160 245,875 269,021 304,121 328,064

Total Deposits 164,501 171,115 193,203 216,321 210,774 216,218 210,032

Total Shareholders' Equity 37,262 46,110 52,832 59,382 71,346 72,103 82,292

Earnings per share (BRL) 1.43 1.70 1.94 2.18 2.04 2.46 3.04

Source: Bradesco, Bloomberg

Table: Balance Sheet (USDmn)

2008 2009 2010 2011 2012 2013 2014

Total Assets 188,071 285,198 374,465 387,531 390,305 354,852 351,538

Loans & Mortgages 71,081 94,927 122,988 131,957 131,326 128,734 123,947

Total Deposits 71,074 98,229 116,387 116,096 102,892 91,525 79,353

Total Shareholders' Equity 16,099 26,470 31,827 31,869 34,829 30,521 31,091

Earnings per share (USD) 0.79 0.86 1.10 1.30 1.05 1.14 1.30

Source: Bradesco, Bloomberg

Table: Key Ratios (%)

2008 2009 2010 2011 2012 2013 2014

Return on Assets 1.8 2.0 1.7 1.6 1.5 1.5 1.7

Return on Equities 20.9 22.3 19.6 19.6 17.3 17.3 19.9

Loan Deposit Ratio 106.3 105.2 113.5 121.8 137.1 149.8 166.3

Loan Asset Ratio 40.2 36.2 35.3 36.5 36.1 38.6 37.5

Equity Asset Ratio 8.5 9.2 8.5 8.2 8.9 8.6 8.8

Total Risk Based Capital Ratio 16.1 17.8 n.a. 15.1 16.2 16.6 16.6

Tier 1 Capital Ratio 12.9 14.8 n.a. 12.4 11.0 12.3 12.9

Source: Bradesco, Bloomberg

Brazil Commercial Banking Report Q3 2015

© Business Monitor International Ltd Page 43

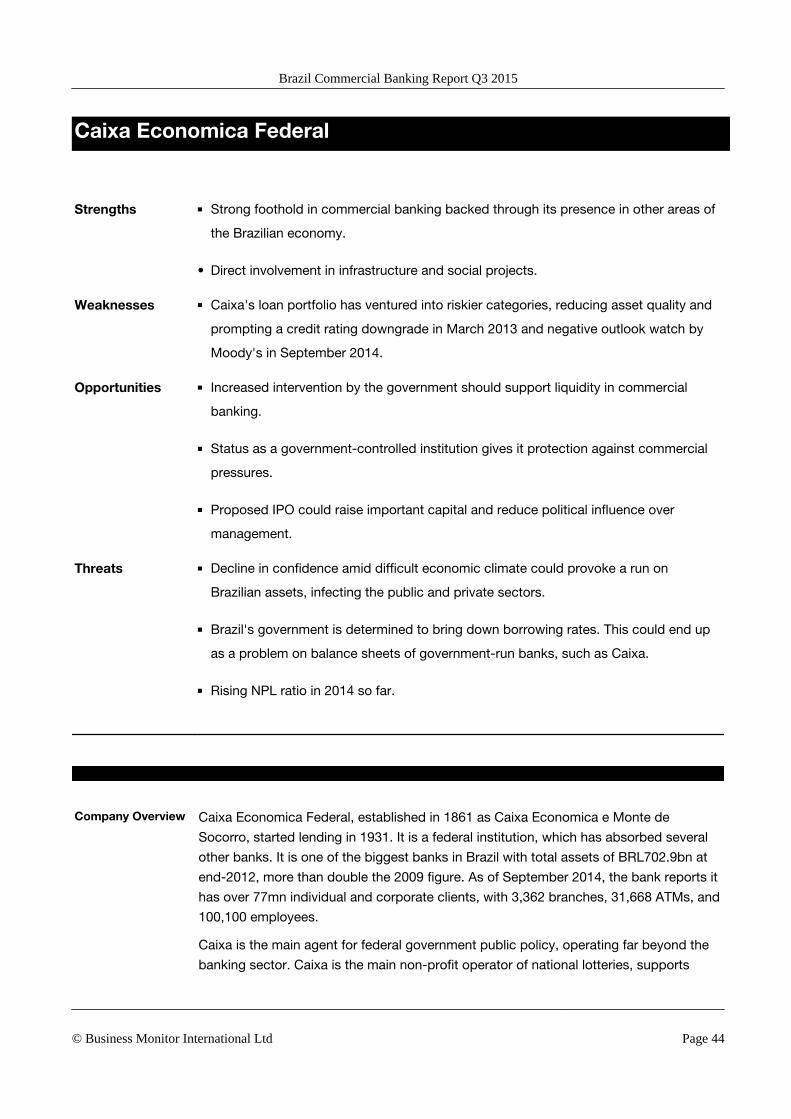

Caixa Economica Federal

SWOT Analysis

Strengths ■ Strong foothold in commercial banking backed through its presence in other areas of

the Brazilian economy.

• Direct involvement in infrastructure and social projects.

Weaknesses ■ Caixa's loan portfolio has ventured into riskier categories, reducing asset quality and

prompting a credit rating downgrade in March 2013 and negative outlook watch by

Moody's in September 2014.

Opportunities ■ Increased intervention by the government should support liquidity in commercial

banking.

■ Status as a government-controlled institution gives it protection against commercial

pressures.

■ Proposed IPO could raise important capital and reduce political influence over

management.

Threats ■ Decline in confidence amid difficult economic climate could provoke a run on

Brazilian assets, infecting the public and private sectors.

■ Brazil's government is determined to bring down borrowing rates. This could end up

as a problem on balance sheets of government-run banks, such as Caixa.

■ Rising NPL ratio in 2014 so far.

Company Overview Caixa Economica Federal, established in 1861 as Caixa Economica e Monte de

Socorro, started lending in 1931. It is a federal institution, which has absorbed several

other banks. It is one of the biggest banks in Brazil with total assets of BRL702.9bn at

end-2012, more than double the 2009 figure. As of September 2014, the bank reports it

has over 77mn individual and corporate clients, with 3,362 branches, 31,668 ATMs, and

100,100 employees.

Caixa is the main agent for federal government public policy, operating far beyond the

banking sector. Caixa is the main non-profit operator of national lotteries, supports

Brazil Commercial Banking Report Q3 2015

© Business Monitor International Ltd Page 44

urban infrastructure projects and manages social programmes such as state benefit

payments. The bank is dominant in the housing sector, with a 67.6% market share.

In December 2014 Brazilian President Dilma Rousseff said Caixa would hold an IPO,

reported Reuters, though she did not indicate when this would occur.

Corporate

HighlightsCaixa posted cumulative net profit of BRL5.3bn in the nine months ending September

2014, up 5.6% compared the same period of 2013. This was supported by a 35.9% y-

o-y increase in revenues over the same period, while operating expenses were up

16.7% y-o-y

The bank held BRL1,019bn in assets at the end of Q314, up 18.6% y-o-y on the

BRL859bn recorded at the same point of 2013. The bank's loan portfolio expanded

24.4% y-o-y over the same period to reach BRL576bn, with strong growth in mortgage

lending (26.1% y-o-y) and credit for infrastructure projects (52.8%).

The non-performing loan ratio inched up to 2.7% by end-September 2014, compared to

2.4% a year earlier. The capital adequacy ratio stood at 15.3%, down from 17.0% a

year earlier, with the Tier 1 capital ratio standing at 12.9%.

At the government's instigation, however, it has ventured into riskier categories, such as

short-term consumer loans, to help kick start the economic recovery. The bank is rated

'BBB' by Fitch and S&P, and 'Baa2' by Moody's, which changed its outlook from stable

to negative in September 2014.

Company Data ■ Website: www.caixa.gov.br■ Status: Public Sector Bank

Table: Balance Sheet (BRLmn)

2008 2009 2010 2011 2012 2013

Total Assets 295,920 341,832 401,412 510,214 703,208 858,325

Loans & Mortgages 21,299 115,516 164,638 233,848 334,022 461,845

Total Deposits 165,528 180,670 215,189 259,829 319,780 360,770

Total Shareholders' Equity 12,705 13,144 15,437 19,561 24,046 35,373

Source: CEF, Bloomberg

Brazil Commercial Banking Report Q3 2015

© Business Monitor International Ltd Page 45

Table: Balance Sheet (USDmn)

2008 2009 2010 2011 2012 2013

Total Assets 127,855 196,230 241,815 273,823 343,279 363,328

Loans & Mortgages 9,203 66,312 99,179 125,502 163,057 195,498

Total Deposits 71,518 103,714 129,632 139,446 156,104 152,713

Total Shareholders' Equity 5,489 7,545 9,299 10,498 11,738 14,973

Source: CEF, Bloomberg

Table: Key Ratios (%)

2008 2009 2010 2011 2012 2013

Return on Assets n.a. 0.9 1.0 1.1 0.9 0.9

Return on Equities n.a. 23.2 26.3 29.6 25.9 22.6

Loan Deposit Ratio n.a. 63.9 n.a. n.a. 110.6 134.6

Loan Asset Ratio n.a. 33.8 n.a. n.a. 50.3 56.6

Equity Asset Ratio 4.3 3.8 3.8 3.8 3.4 4.1

Source: CEF, Bloomberg

Brazil Commercial Banking Report Q3 2015

© Business Monitor International Ltd Page 46

Santander

SWOT Analysis

Strengths ■ Continued expansion is likely to boost income and profit in the medium-to-long term

as it focuses on targeting its services towards Brazil's upper and middle classes.

■ Strong backing of international parent, which has held up well in the financial crisis.

■ The Brazilian economy, the world's sixth largest, continues to provide strong potential

for the Group's business.

Weaknesses ■ Net profit down in 2014.

Opportunities ■ Long-term growth in lending and deposits.

■ Increased lending to small and medium-sized companies (SMEs).

■ In 2011, technology integration and brand unification was completed with Banco

Real. This should help the bank narrow the profitability gap with its local competitors.

■ The currently relatively low penetration of banking products and services in Brazil

represents a major opportunity for commercial banks willing to diversify.

Threats ■ Economic pressures in Brazil could continue to increase provisions and writedowns,

putting downward pressure on profitability.

■ Credit rating placed on negative watch by Moody's due to weakening outlook for

Brazilian economy.

Company Overview Banco Santander Brasil (BSB) established its first commercial office in São Paulo in

1970. In 1982, the bank opened its first office for clients. Since then it has become one

of the largest financial institutions in Brazil through a series of acquisitions. It is the

country's third largest private bank and the largest foreign bank. Within Brazil,

Santander has over 3,400 branches, 17,774 ATMs, 49,481 employees, and 30.8mn

customers. As the largest overseas contributor to profits, Santander Brazil remains

central to the parent group's growth strategy.

Santander's main business areas are retail banking, wholesale banking, asset

management and insurance. It also provides crediting, financing, real estate crediting,

Brazil Commercial Banking Report Q3 2015

© Business Monitor International Ltd Page 47

exchange, insurance and commercial savings services to a range of individual,

commercial and government institutions and agencies.

Technology integration and brand unification with Banco Real was completed

successfully in 2011 and with an optimum commercial banking platform and a wider

range of products and services, left Santander Brazil well placed to carry out its

business. In September 2014, BSB confirmed that it was seeking to acquire 50% of

Superbank, a general use prepaid-card company. Earlier in the year, the bank

purchased card payment processor GetNet Tecnologia for BRL1.1bn.

Corporate

HighlightsIn the first nine months of 2014, Banco Santander Brasil posted net profit of

BRL4.28bn, down slightly from the BRL4.41bn reported in the same period of 2013.