BOURBON Beyond BOURBON - bourbonoffshore.com · 3 BOURBON Presentation March 29, 2016 EXECUTIVE...

53

March 29, 2016 BOURBON Beyond BOURBON

-

Upload

nguyenxuyen -

Category

Documents

-

view

232 -

download

0

Transcript of BOURBON Beyond BOURBON - bourbonoffshore.com · 3 BOURBON Presentation March 29, 2016 EXECUTIVE...

March 29, 2016

BOURBON Beyond BOURBON

2010 - BOURBON 2015 LEADERSHIP STRATEGY

" 500 VESSELS "

2013 - TRANSFORMING FOR BEYOND

" FINANCIAL RESILIENCY "

2016 - BOURBON Beyond BOURBON

" NO GROWTH IS NOT AN OPTION "

BOURBON Presentation March 29, 2016 3

EXECUTIVE SUMMARY

BOURBON has decided to service customers’ shift towards energy transition by:

Investing in midstream gas export services with an initial focus on Ethane

Buying existing assets from JACCAR Holdings to speed up growth towards leadership

BOURBON Beyond BOURBON

Bourbon Offshore Anticipate how customers change their relationship to vessels offshore

Bourbon Gas Diversify into a fast growing segment of the gas market

Bourbon Invest Manage long term third parties’ investments in vessels for yield

1.BOURBON IS THE MOST RESILIENT OSV PLAYER IN TODAY ’S DOWN CYCLE

2. BOURBON AND THE NEW CUSTOMERS PARADIGM FOLLOWING THE DIGITAL REVOLUTIONS

3.MIDSTREAM GAS EXPORT SERVICES OFFER GROWTH POTENTIAL WELL WITHIN BOURBON DNA & TRACK RECORD

4. BUYING EXISTING ASSETS IN THE MIDSTREAM GAS EXPORT ACTIVITY AS A PLAFORM FOR LEADERSHIP

AGENDA

BOURBON Presentation March 29, 2016 5

1.

RESILIENCY

FACTORS

SAFETY AND AVAILABILITY

SEGMENTS AND GEOGRAPHIES

LOCAL PARTNERSHIP, CUSTOMER BASE, FLEET STRUCTURE

CASH PRESERVATION STRATEGY AND PRO ACTIVE STACKING

BOURBON Presentation March 29, 2016 6

RESILIENCY FACTORS: OPERATIONS

BOURBON Presentation March 29, 2016 7

EXCELLENCE IN OPERATIONS: SAFETY

TRIR

4.56

1.14

0.55

2 26,3 47,6

2007 2015

TRIR: Total Recordable Incident per million hours worked, based on 24 hours/day

The single most

important factor of our

customers decision to

select OSV services

provider

BOURBON Presentation March 29, 2016 8

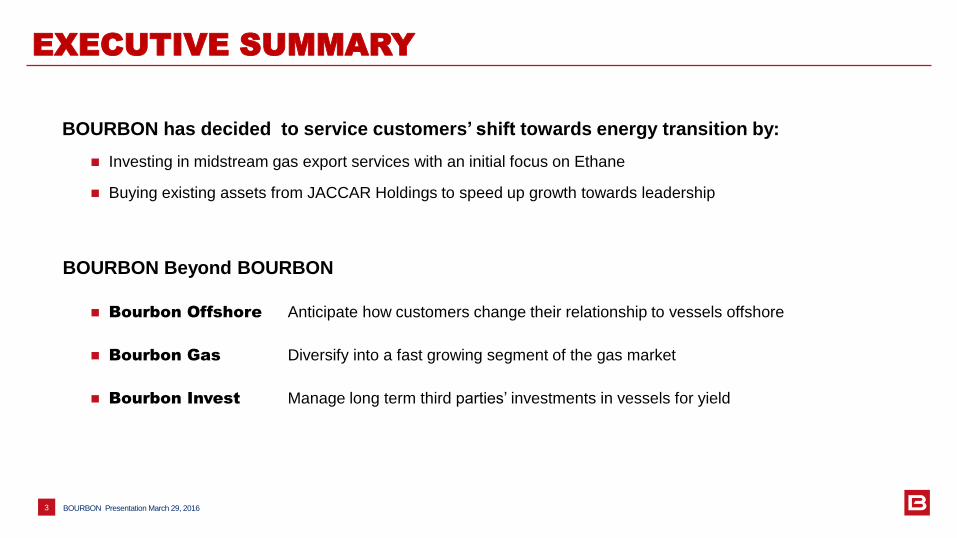

EXCELLENCE IN OPERATIONS: RELIABILITY

Excellence in operations

can be measured

BOURBON reached its

very high target since

2014

93.0%

94.3% 94.5%

95.5%

96.4%

95%

90%

91%

92%

93%

94%

95%

96%

97%

2011 2012 2013 2014 2015

Technical availability rate for BOURBON fleet

Technical availability rate objective

BOURBON Presentation March 29, 2016 9

EXCELLENCE IN OPERATIONS: BALANCED PORTFOLIO

Balanced diversification

of BOURBON revenues

by segment and market

for strong resilience

factor, specially in down

cycles

59%

4%

23%

14%

30%

32%

20%

18%

70%

19%

9% 2%

Africa

Europe/Mediterannea/Middle East

Americas

Asia

Deepwater offshore vessels

Shallow water offshore vessels

Crewboats

Subsea Services

57%

15%

18%

10%

2006

2015

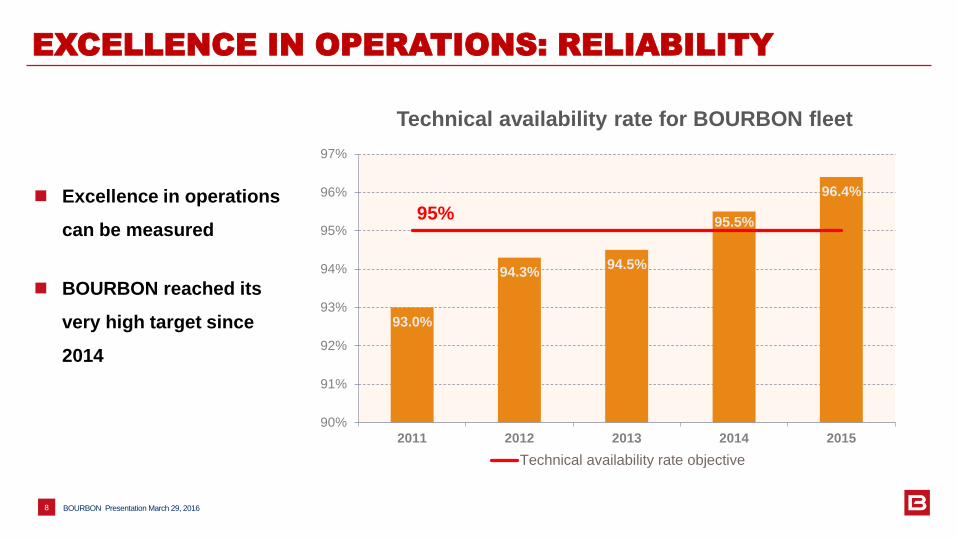

BOURBON Supply fleet

STRATEGICALLY conform* Average age

Shallow water

111 Bourbon Liberty 4.9

6 Seismic assistance vessels 2.1

Deep water

7 AHTS 13.1

47 PSV 5.2

Subsea

23 IMR vessels 5.0

Not conform to BOURBON standards Average age

50 Vessels 12.5

BOURBON Presentation March 29, 2016 10

EXCELLENCE IN OPERATIONS: FLEET PERFORMANCES

BOURBON innovative

fleet of series built

vessels provide real

saving to customers,

becoming their preferred

choice

* Refers to BOURBON’ standards criterias: Diesel Electric, DP capabilities, built in series

JV

Project JV

Affiliates

BOURBON Presentation March 29, 2016 11

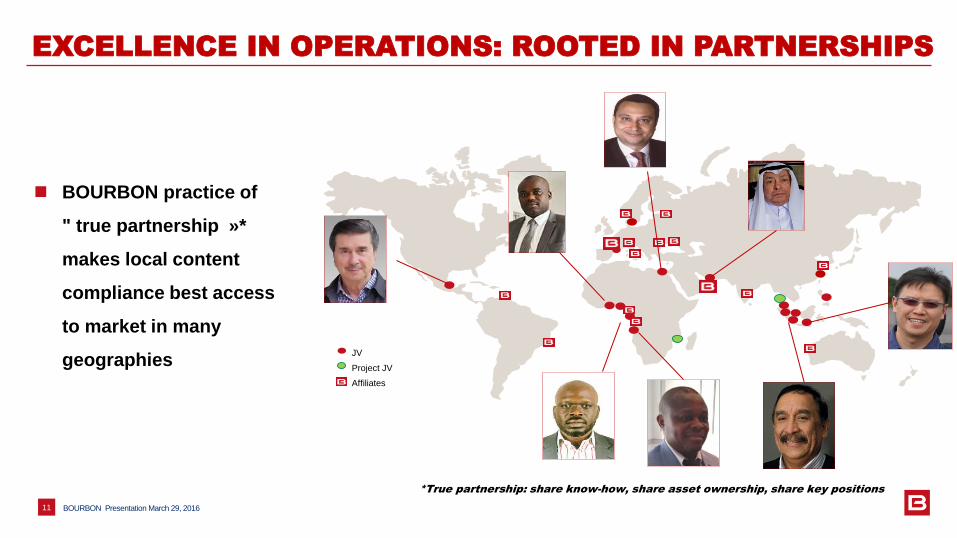

EXCELLENCE IN OPERATIONS: ROOTED IN PARTNERSHIPS

BOURBON practice of

" true partnership »*

makes local content

compliance best access

to market in many

geographies

*True partnership: share know-how, share asset ownership, share key positions

BOURBON Presentation March 29, 2016 12

EXCELLENCE IN OPERATIONS: BEING PROACTIVE

Proactive stacking of

vessels in an optimized

way is a strong cash

preservation tool and

adds to the other cost

control measures

Abidjan

Batam

RESILIENT REVENUES - UTILIZATION RATE – SHARE VALUE

TIMELY CAPEX

DELEVERAGE – ASSET SMART

FOREX AND INTEREST RATES

BOURBON Presentation March 29, 2016 13

RESILIENCY FACTORS: FINANCE

BOURBON Presentation March 29, 2016 14

FINANCIAL RESILIENCY: REVENUES

BOURBON

-

100

200

300

400

500

600

700

800

- 500 1 000 1 500 2 000 2 500

BOURBON

-

100

200

300

400

500

600

700

800

- 500 1 000 1 500 2 000 2 500

EB

ITD

AR

Revenues

In $m

Revenues

EB

ITD

AR

2014 2015

Source: Public information, BOURBON

In $m

15

FINANCIAL RESILIENCY: UTILIZATION RATE

Design and performance

of BOURBON fleet and

crews generate

consistently higher

utilization rates

0

10

20

30

40

50

60

70

80

90

100

Utiliz

atio

n %

Built in 1991 and earlier

Built in 2005 and later

Série2

Source: IHS, BOURBON

BOURBON Presentation March 29, 2016

BOURBON

OSV global utilization by build age compared to BOURBON fleet

76%

10

20

30

40

50

60

70

80

90

100

110

Bourbon Peer Average

BOURBON Presentation March 29, 2016 16

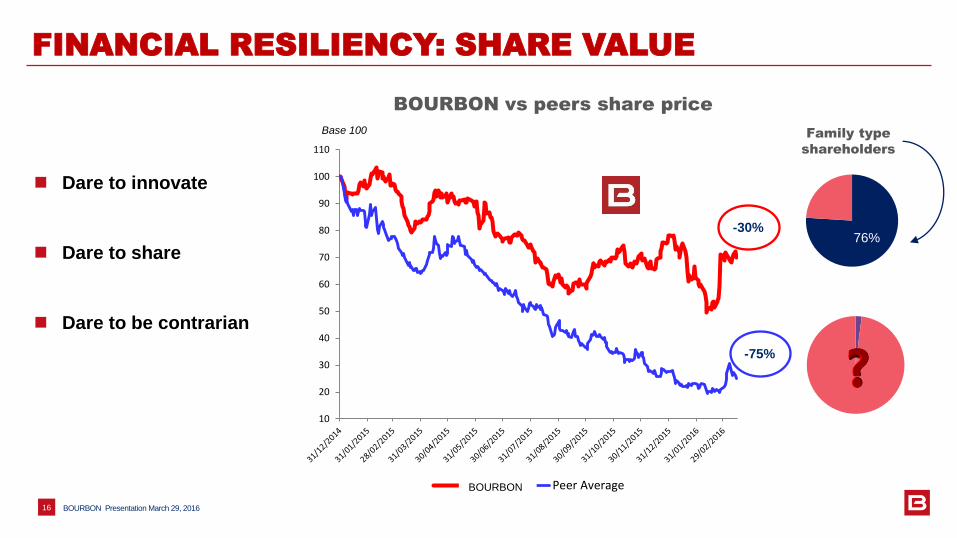

FINANCIAL RESILIENCY: SHARE VALUE

Dare to innovate

Dare to share

Dare to be contrarian

-30%

-75%

BOURBON vs peers share price

Family type

shareholders

Base 100

BOURBON

0

5

10

15

20

25

30

35

2010 2011 2012 2013 2014 2015 2016

900100011001200130014001500160017001800190020002100

2010 2011 2012 2013 2014 2015 E2016 E2017

BOURBON Presentation March 29, 2016 17

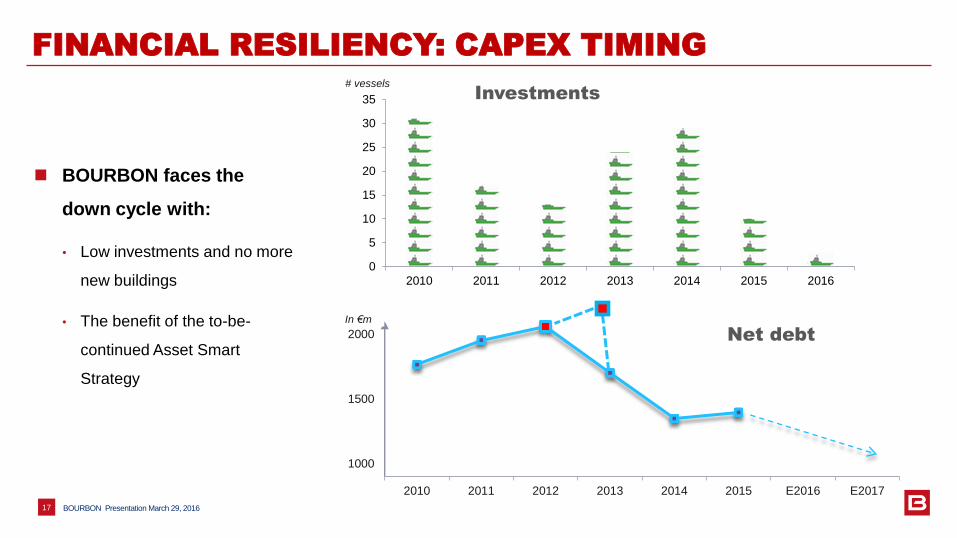

FINANCIAL RESILIENCY: CAPEX TIMING

BOURBON faces the

down cycle with:

• Low investments and no more

new buildings

• The benefit of the to-be-

continued Asset Smart

Strategy

In €m

Investments

Net debt

# vessels

BOURBON Presentation March 29, 2016 18

FINANCIAL RESILIENCY: FOREX AND INTEREST RATES

-1

0

1

2

3

4

5

6

1

1,2

1,4

1,6

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 e 2016

€/US$ Euribor 3M

EUR/US$ Euribor 3M

FINANCIAL RESILIENCY: ASSET SMART CONTRIBUTION

1,841

2,486

174

1,440 312

120

427

2,005

113

67

303

-

500

1 000

1 500

2 000

2 500

3 000

3 500

Sales of vessels

Cash generated by

operations

BOURBON dividends

Minority

Taxes

Interests

Cash net from activities Equity- like bond Net debt

changes

Net Investments

Working capital

FINANCING INVESTING

BOURBON Presentation March 29, 2016 19

2011-2015

Asset

smart

In $m

2.

NEW CUSTOMER

PARADIGM:

CHANGES IN

RELATION TO

VESSELS OFFSHORE

NEW CUSTOMER PARADIGM: BE THE PREFERRED

TRUST

ATTRACTION UNIQUENESS

AWARENESS

BECOME THE

PREFERRED COMPANY

BOURBON Presentation March 29, 2016 21

“World leadership”

“In people”

“We dare…” “Not only speed

but acceleration”

BOURBON Presentation March 29, 2016 22

NEW CUSTOMER PARADIGM: DIGITAL REVOLUTION

Connected vessels:

Follow the sun

Contractual:

Optional:

Apps for efficiency and

cost control

0

20

40

60

80

100

120

140

0

10

20

30

40

50

60

70

80

Tidewater Brent price

BOURBON Presentation March 29, 2016 23

BOURBON: WHAT ELSE?

For the leader in the

industry, growing in size

generates decreasing

returns and value reflects

changes in oil price

Waiting for the next tide is

not enough

Any growth potential not

linked to oil price cycle ?

Tid

ew

ate

r share

price

(U

S$)

Bre

nt o

il pric

e (U

S$)

Correlation between share price/oil price

Monthly data Data up to March 2016

3.

OPPORTUNITIES

IN MIDSTREAM

GAS EXPORT

SERVICES

BOURBON Presentation March 29, 2016 25

MAIN TAKE AWAY

Gas is a growing source of raw materials for downstream chemicals and power generation

Excess ethane from US Upstream producers has to be exported

Ethane is a competitive raw material for downstream activities

Midstream gas export services is a growing market backed by long term contracts from

suppliers and end users

Semi refrigerated solution for large and multigas carriers is now available

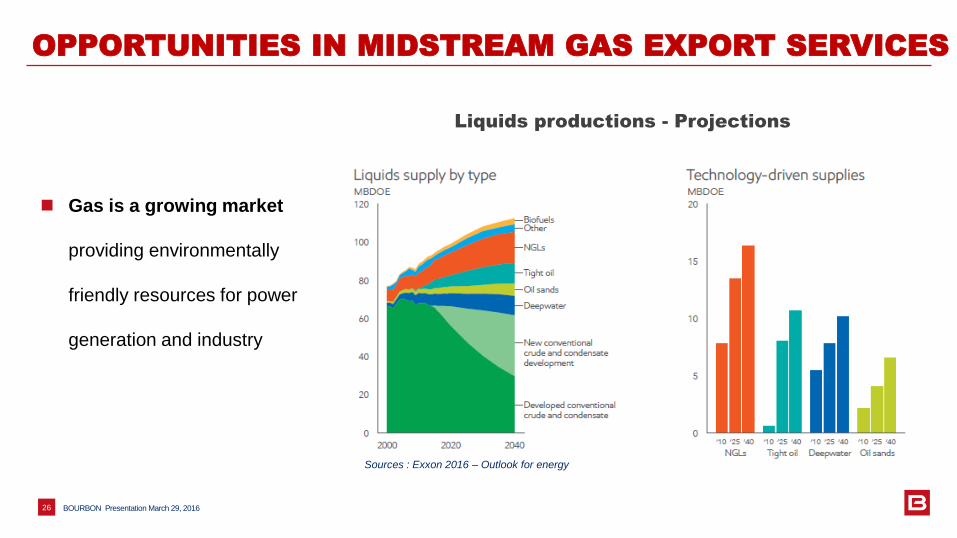

OPPORTUNITIES IN MIDSTREAM GAS EXPORT SERVICES

Gas is a growing market

providing environmentally

friendly resources for power

generation and industry

BOURBON Presentation March 29, 2016 26

Liquids productions - Projections

Sources : Exxon 2016 – Outlook for energy

BOURBON Presentation March 29, 2016 27

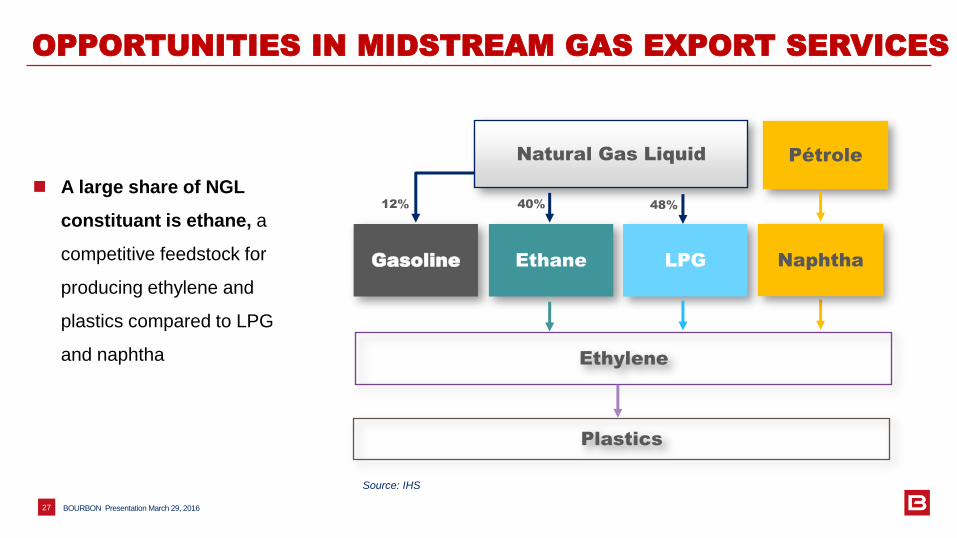

OPPORTUNITIES IN MIDSTREAM GAS EXPORT SERVICES

A large share of NGL

constituant is ethane, a

competitive feedstock for

producing ethylene and

plastics compared to LPG

and naphtha

48% 12% 40%

Natural Gas Liquid

Ethane LPG

Plastics

Ethylene

Gasoline

Pétrole

Naphtha

Source: IHS

BOURBON Presentation March 29, 2016 28

OPPORTUNITIES IN MIDSTREAM GAS EXPORT SERVICES

Ethane is the most

competitive raw material

for ethylene in Asia

Higher pure ethylene yield

Lower cost of production

Most new ethylene crackers

are ethane based

0 400 800 1200

30

50

75

100

Asia naphtha US ethane imports to Asia

Ethane cost savings

vs naphtha

$/barrel

80

45

30

13

28

26

2

15

13

5 12

31

Ethane Propane Naphtha

Ethylene Methane & Hydrogene Propylene Others

Ethylene

Yield by type of feedstock

Sources : EIA, Commodity Exchanges; Estin & Co estimates and analysis

100%

BOURBON Presentation March 29, 2016 29

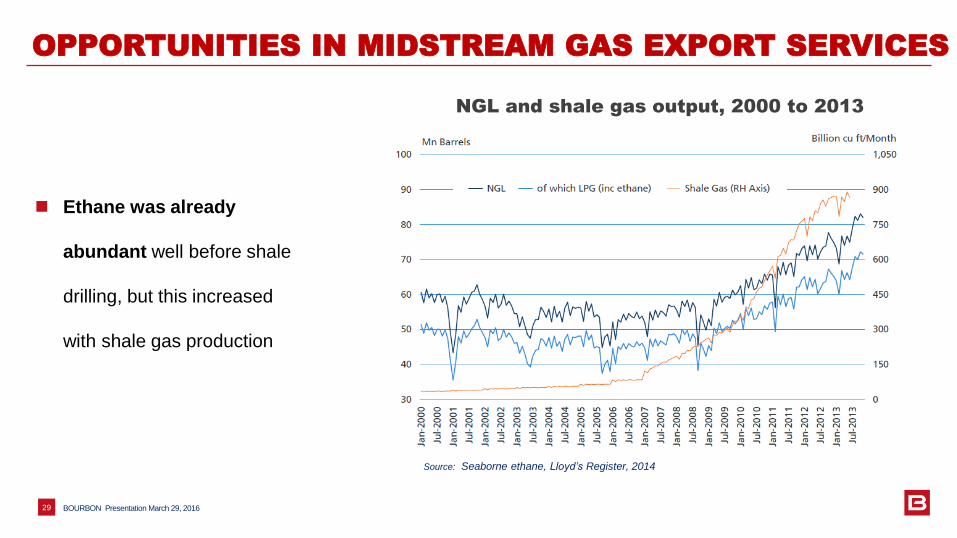

OPPORTUNITIES IN MIDSTREAM GAS EXPORT SERVICES

Ethane was already

abundant well before shale

drilling, but this increased

with shale gas production

Source: Seaborne ethane, Lloyd’s Register, 2014

NGL and shale gas output, 2000 to 2013

18 19 20 22 26 28 30 32 34 35 36 37 39

0

10

20

30

40

50

60

70

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Ethane US consumption Ethane available for export

BOURBON Presentation March 29, 2016 30

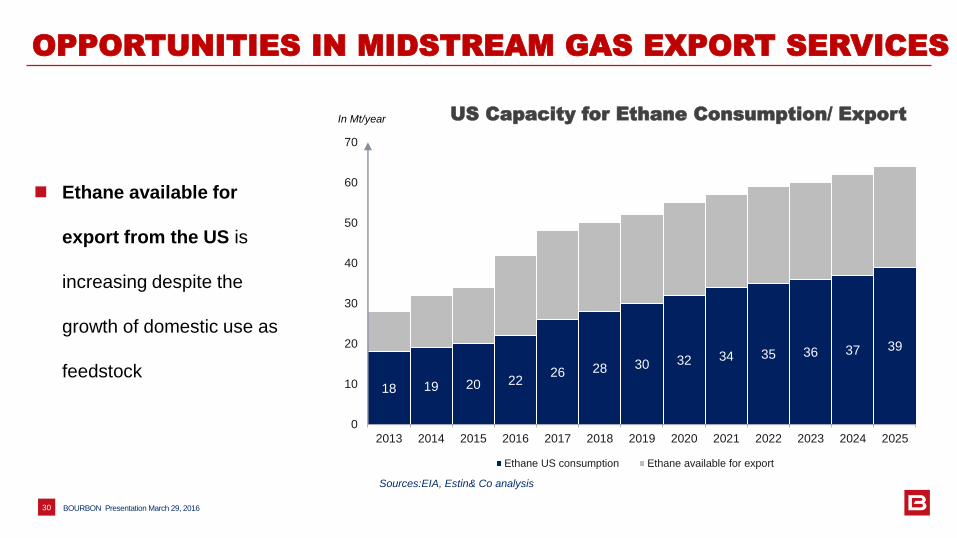

OPPORTUNITIES IN MIDSTREAM GAS EXPORT SERVICES

Ethane available for

export from the US is

increasing despite the

growth of domestic use as

feedstock

Sources:EIA, Estin& Co analysis

US Capacity for Ethane Consumption/ Export In Mt/year

BOURBON Presentation March 29, 2016 31

OPPORTUNITIES IN MIDSTREAM GAS EXPORT SERVICES

Ethane export flows

Source: CERI, Versen, Bloomberg, O&G Journal, ICIS, Estin & Co. analysis

1 Marcus Hook

Sunoco

Houston

US North East and

Houston areas are the

two natural gas export

hubs for Ethane outside

the US

BOURBON Presentation March 29, 2016 32

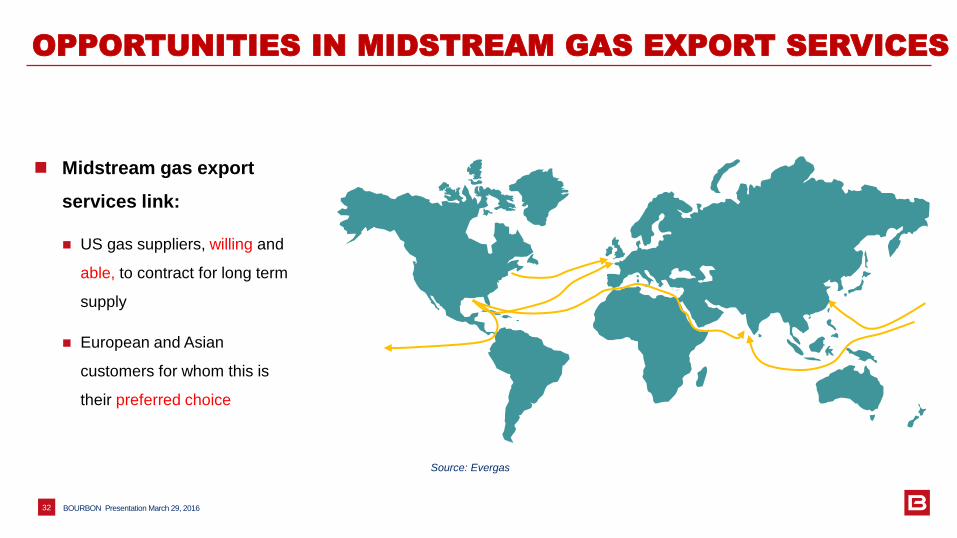

OPPORTUNITIES IN MIDSTREAM GAS EXPORT SERVICES

Midstream gas export

services link:

US gas suppliers, willing and

able, to contract for long term

supply

European and Asian

customers for whom this is

their preferred choice

Source: Evergas

BOURBON Presentation March 29, 2016 33

OPPORTUNITIES IN MIDSTREAM GAS EXPORT SERVICES

Midstream Gas export

services consist of:

Liquefaction and storage at

US export terminals

Dedicated fleet of mid and

large size vessels

BOURBON Presentation March 29, 2016 34

OPPORTUNITIES IN MIDSTREAM GAS EXPORT SERVICES

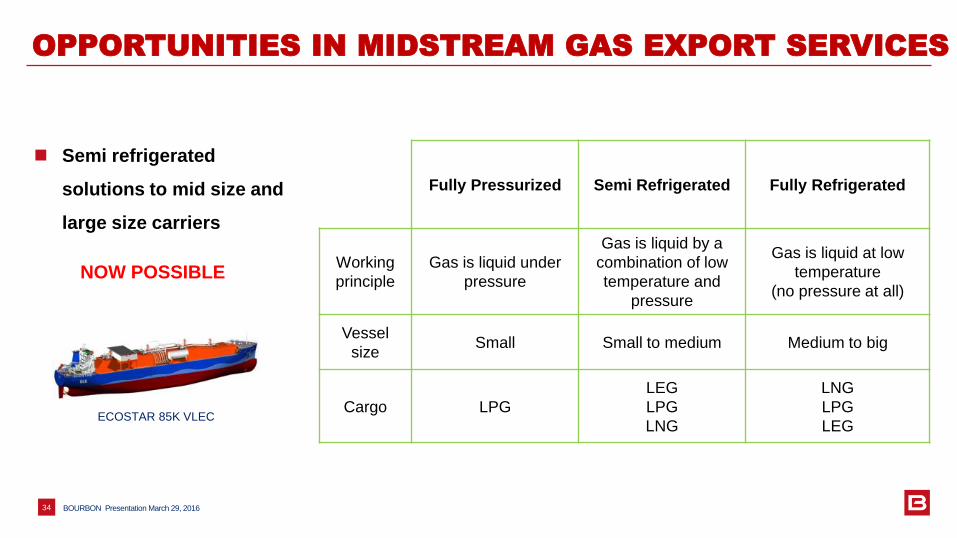

Semi refrigerated

solutions to mid size and

large size carriers

NOW POSSIBLE

Fully Pressurized Semi Refrigerated Fully Refrigerated

Working

principle

Gas is liquid under

pressure

Gas is liquid by a

combination of low

temperature and

pressure

Gas is liquid at low

temperature

(no pressure at all)

Vessel

size Small Small to medium Medium to big

Cargo LPG

LEG

LPG

LNG

LNG

LPG

LEG ECOSTAR 85K VLEC

BOURBON Presentation March 29, 2016 35

OPPORTUNITIES IN MIDSTREAM GAS EXPORT SERVICES

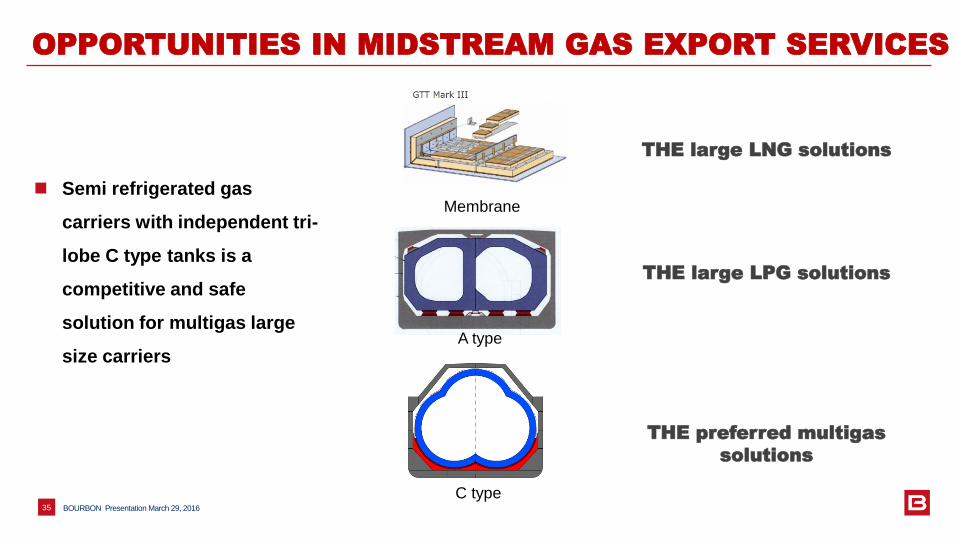

Semi refrigerated gas

carriers with independent tri-

lobe C type tanks is a

competitive and safe

solution for multigas large

size carriers

THE large LNG solutions

THE large LPG solutions

THE preferred multigas

solutions

Membrane

A type

C type

BOURBON Presentation March 29, 2016 36

OPPORTUNITIES IN MIDSTREAM GAS EXPORT SERVICES

Innovation in containment

systems for carrying gas

Tri-lobe C type tanks up to

23,000 m3 per unit

Semi-refrigerated technology

for large vessels

41m Width – 33m Depth – 31m Height

Mega tank size

• Gas producing country

• Excess ethane – Shale gas

• Can commit to long term

export supply contract

BOURBON Presentation March 29, 2016 37

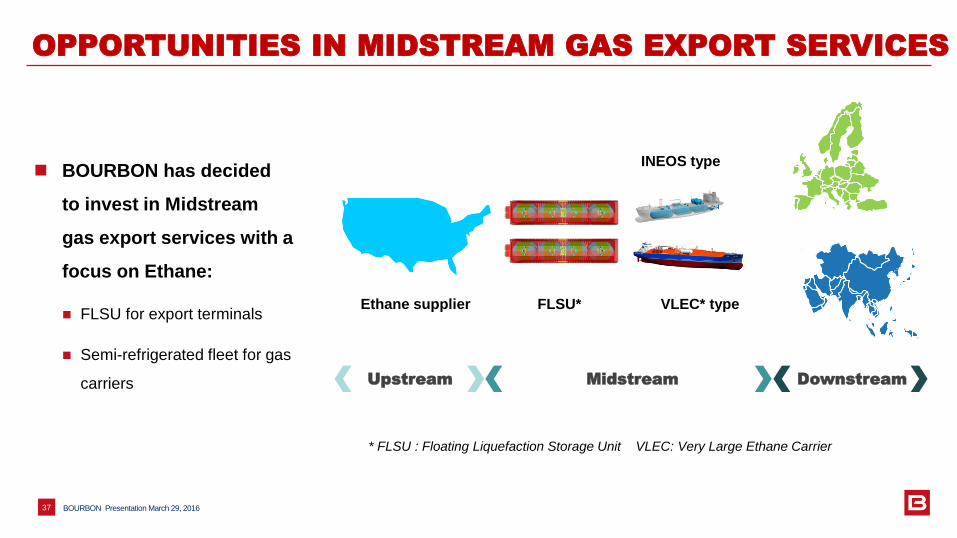

OPPORTUNITIES IN MIDSTREAM GAS EXPORT SERVICES

BOURBON has decided

to invest in Midstream

gas export services with a

focus on Ethane:

FLSU for export terminals

Semi-refrigerated fleet for gas

carriers Upstream Midstream Downstream

Ethane supplier FLSU* VLEC* type

INEOS type

* FLSU : Floating Liquefaction Storage Unit VLEC: Very Large Ethane Carrier

3 7

12 17

21 25

29 31 33 35 35

3

11

20

28

35

39 41

45 46 46

3

10

23

37

49

60

68

72

78

81 81

0

10

20

30

40

50

60

70

80

90

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Mid sized VLEC TOTAL

BOURBON Presentation March 29, 2016 38

OPPORTUNITIES IN MIDSTREAM GAS EXPORT SERVICES

Market expected to need

around 80 mid and large

size vessels

JACCAR has today 19 out

of 32 vessels already

ordered for Ethane

transportation, i.e 60%

market share

18%

13%

9%

60%

JACCAR Reliance

Hartmann

Navigator

Sources: Estin& Co analysis

Number of units

4.

INVESTING FOR

LEADERSHIP

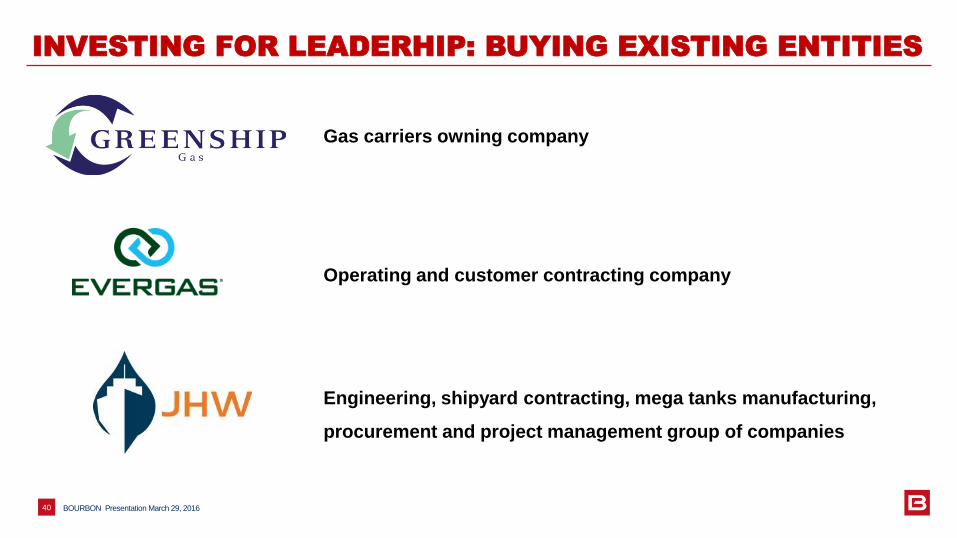

INVESTING FOR LEADERHIP: BUYING EXISTING ENTITIES

Gas carriers owning company

Operating and customer contracting company

Engineering, shipyard contracting, mega tanks manufacturing,

procurement and project management group of companies

BOURBON Presentation March 29, 2016 40

BOURBON Presentation March 29, 2016 41

INVESTING FOR LEADERSHIP: INNOVATIVE VESSELS

Semi refrigerated multigas

vessels with a focus on

Ethane long term contracts

8 x 27,500 m3 vessels for

INEOS with 10 and 15 years

contract

5 x 85,000 m3 VLEC for

ORIENTAL Energy with 10

years contract

All in services by 2019

8 vessels

- 12,000 m3

8 vessels*

-Dragon Ineos

- 27,500 m3

[6 vessels]

- 32,000 m3

[5 vessels]

- 85,000 m3

*- 4 already in services, 4 by mid 2017, all LNG capable

- [on order]

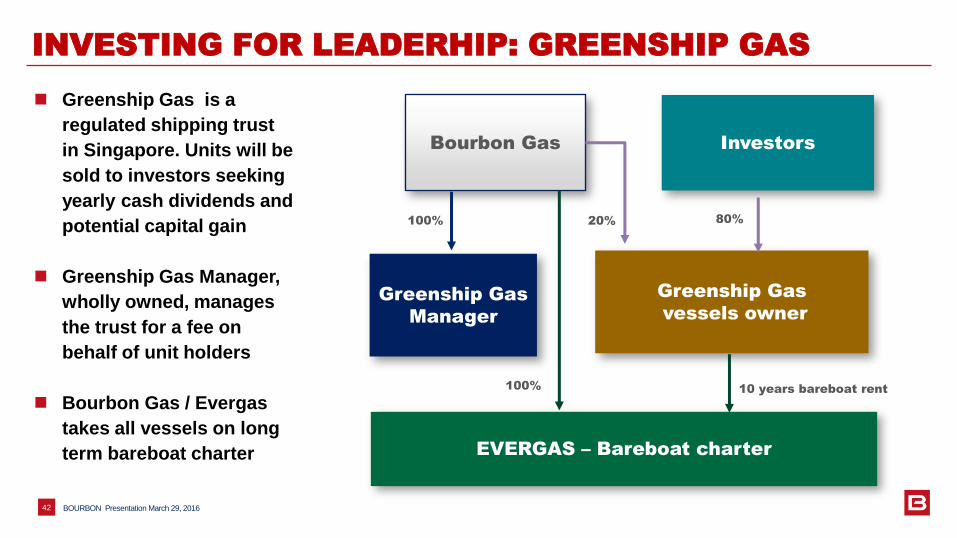

INVESTING FOR LEADERHIP: GREENSHIP GAS

Greenship Gas is a

regulated shipping trust

in Singapore. Units will be

sold to investors seeking

yearly cash dividends and

potential capital gain

Greenship Gas Manager,

wholly owned, manages

the trust for a fee on

behalf of unit holders

Bourbon Gas / Evergas

takes all vessels on long

term bareboat charter

BOURBON Presentation March 29, 2016 42

20% 100%

Bourbon Gas

Greenship Gas

vessels owner

EVERGAS – Bareboat charter

Greenship Gas

Manager

Investors

80%

100% 10 years bareboat rent

BOURBON Presentation March 29, 2016 43

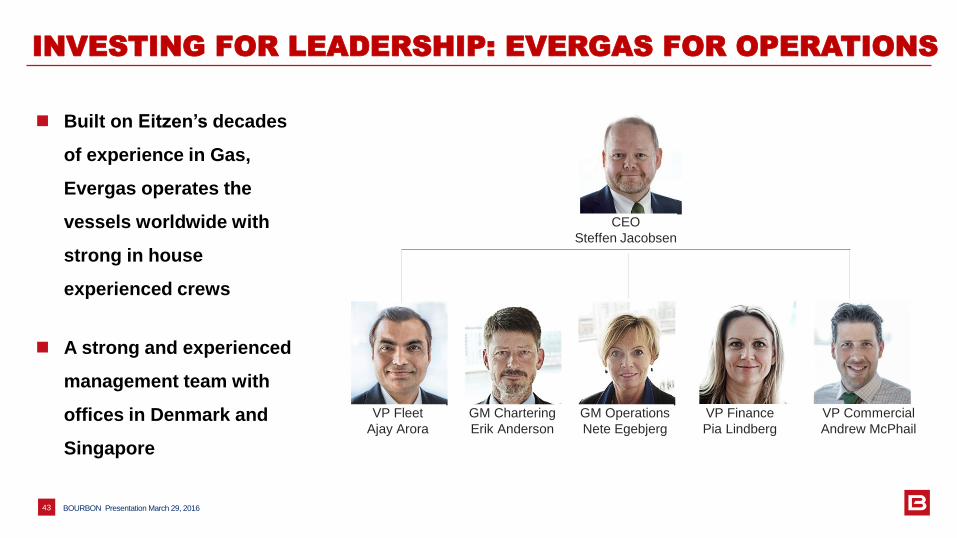

INVESTING FOR LEADERSHIP: EVERGAS FOR OPERATIONS

Built on Eitzen’s decades

of experience in Gas,

Evergas operates the

vessels worldwide with

strong in house

experienced crews

A strong and experienced

management team with

offices in Denmark and

Singapore

CEO

Steffen Jacobsen

VP Fleet

Ajay Arora

GM Chartering

Erik Anderson

GM Operations

Nete Egebjerg

VP Finance

Pia Lindberg

VP Commercial

Andrew McPhail

BOURBON Presentation March 29, 2016 44

INVESTING FOR LEADERSHIP: STRONG CUSTOMER BASE

Evergas manages spot,

contract of affreightment

and long term contracts

with industrial customers

and gas exporters

BOURBON Presentation March 29, 2016 45

INVESTING FOR LEADERSHIP: JHW E&C

JHW controls the

differents steps in the

value chain:

Design and engineering

Procurement

Manufacturing of mega tanks

Contracting to shipyards

Project management

Bourbon GAS

(E&C)

• JHW Trading

• EXEN Trading

Management team

80% 20%

Design Manufacturing Procurement and

Project management

25% 100% 51%

BOURBON Presentation March 29, 2016 46

INVESTING FOR LEADERSHIP: JHW E&C

BOURBON Presentation March 29, 2016 47

INVESTING FOR LEADERSHIP: WOE FOR MEGA TANKS

CONCLUSION

BOURBON Presentation March 29, 2016 49

CONCLUSION

BOURBON has decided to service customers’ shift towards energy transition by:

Investing in midstream gas export services with an initial focus on Ethane

Buying existing assets from JACCAR Holdings to speed up growth towards leadership

Strong synergies between divisions will lower execution risk:

Customers and Brand

Know-how (high tech vessels operations)

Reduced financial and execution risk

BOURBON Presentation March 29, 2016 50

CONCLUSION

BOURBON SA will become

BOURBON CORPORATION

pending AGM’ approval on May

26, 2016

Jacques de Chateauvieux will

become Chairman and CEO of

BOURBON CORPORATION

with Christian Lefèvre as

Deputy CEO and Gaël

Bodénès as COO

BOURBON CORPORATION

CEO: Philippe Rochet CEO: Christian Lefèvre

Deputy CEO: Gaël Bodénès

Chairman and CEO: Jacques de Chateauvieux Deputy CEO: Christian Lefèvre

COO: Gaël Bodénès

CEO: Jacques de Chateauvieux

Deputy CEO: Philippe Rochet

CEO: Steffen Jacobsen CEO: Kevin Zhu

CONCLUSION

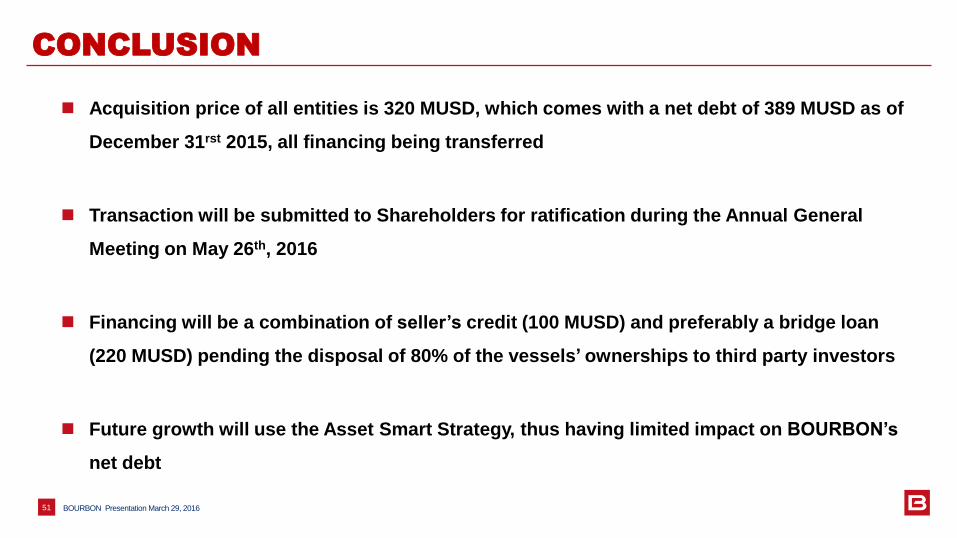

Acquisition price of all entities is 320 MUSD, which comes with a net debt of 389 MUSD as of

December 31rst 2015, all financing being transferred

Transaction will be submitted to Shareholders for ratification during the Annual General

Meeting on May 26th, 2016

Financing will be a combination of seller’s credit (100 MUSD) and preferably a bridge loan

(220 MUSD) pending the disposal of 80% of the vessels’ ownerships to third party investors

Future growth will use the Asset Smart Strategy, thus having limited impact on BOURBON’s

net debt

BOURBON Presentation March 29, 2016 51

BOURBON Presentation March 29, 201654

BOURBON Presentation March 29, 2016 53

This document may contain information other than historical information, which constitutes expectations, estimated, provisional data concerning the financial position, results, plans, other trend information and strategy of BOURBON. These projections are based on assumptions that could differ materially from those anticipated, may prove to be incorrect and/or depend on risk factors including, but not limited to: foreign exchange fluctuations, fluctuations in oil and natural gas prices, changes in oil companies investment policies in the exploration and production sector, the growth in competing fleets, which saturates the market, the impossibility of predicting specific client demands, political instability in certain activity zones, ecological considerations and general economic conditions.

All written or oral statements attributable to BOURBON and its employees or representatives acting on the BOURBON’s behalf are expressly qualified in their entirety by the factors referred to above.

BOURBON assumes no liability for updating, revising or correcting the provisional information or forward-looking statements based on new information in light of future events or any other reason, and these statements speak only to the date of today’s presentation.