Bot Regulations 2008

106

· .. THE GOVERNOR Cable:. 41024'"B·ENkUU" Tel. Gen: 255 22 22330000 Dlr: 25p 22 2233020/21 facsimile: 255 22 34085 · E-mall: [email protected] Ref. No. GA.302/389/01 All Commerclal Banks CIRCULAR NO. 1 (Issued on 28th November, ·2008} UNITED REPUBLIC OF TANZANIA BANK OF TANZANIA P.O. Box 2939 DAR ES SAlAAM November 28 1 2008 STATUTORY MINIMUM RESERVES AGAINST DEPOSITS AND BORR.OWINGS In accordance with Section 45 .of the Bank of Tanzania Act, 2006, and Sections 4 and 71 of .the Banking and Financial ltistltuttons Act. 2006, all banks In Tanzania - Mainland and Zanzibar. are reqolred to maintain statutory minimum reserves {SMR) on their total deposit liabilities and funds borrowed from the gene·ral public, pursuant to their authority to carry on banking buslr:tess. 1. GENERAL POLICY AND IMPLEMENTATION GUIDANCE The statu.tory reserve requirement remains an Important instrument of · monetary control and financial. prudence in ranzanla. However, lfs ' utilization Is determined by long term objectives of monetary policy given the current monetary conditions and Inflationary pressures, while the more flexible open market operations are adopted for Implementing short- qnd medium term objectives of monetary policy. The existing inflatlonar.y ,.pressl)res In ecqnomy. qmldst the on-going global financial crisis have necessitated the Bank of Tanzania to make some odjustments to the and composition of SMR. '

-

Upload

khadija-gogo -

Category

Documents

-

view

65 -

download

1

Transcript of Bot Regulations 2008

· ..

THE GOVERNOR Cable:. 41024'"B·ENkUU" Tel. Gen: 255 22 22330000

Dlr: 25p 22 2233020/21 facsimile: 255 22 34085

· E-mall: [email protected]

Ref. No. GA.302/389/01

All Commerclal Banks

CIRCULAR NO. 1 (Issued on 28th November, ·2008}

UNITED REPUBLIC OF TANZANIA

BANK OF TANZANIA P.O. Box 2939 DAR ES SAlAAM

November 281 2008

STATUTORY MINIMUM RESERVES AGAINST DEPOSITS AND BORR.OWINGS

In accordance with Section 45 .of the Bank of Tanzania Act, 2006, and Sections 4 and 71 of .the Banking and Financial ltistltuttons Act. 2006, all banks In Tanzania - Mainland and Zanzibar. are reqolred to maintain statutory minimum reserves {SMR) on their total deposit liabilities and funds borrowed from the gene·ral public, pursuant to their authority to carry on banking buslr:tess.

1. GENERAL POLICY AND IMPLEMENTATION GUIDANCE

The statu.tory reserve requirement remains an Important instrument of · monetary control and financial. prudence in ranzanla. However, lfs ' utilization Is determined by long term objectives of monetary policy given the current monetary conditions and Inflationary pressures, while the more flexible open market operations are adopted for Implementing short- qnd medium term objectives of monetary policy.

The existing inflatlonar.y ,.pressl)res In tb.~ ecqnomy. qmldst the on-going global financial crisis have necessitated the Bank of Tanzania to make some odjustments to the l~vel and composition of SMR.

'

christina.kongola

Sticky Note

Unmarked set by christina.kongola

J.

By this Circular, eaeh bank shall be required ·to maintain a statutory minimum reserves account with the Bank of Tanzania In the amount and manner In which the req'ulred cash reserves shall be calculated by banks as prescribed In this Circular. Henceforth, statutory minimum reserves requirement f.or each bank shall be:

1.1 Ten percen.t {1 0%) of the outstanding balance of Its total local and foreign currehcy deposit liabilities {of non-government entitles) and borrowings from the general public, all converted In local currency, and.

'. 1.2 Twenty percent (20%) of total government deposits also converted In

local currency.

1.3 Under the above arrangements, cash In vault shall not form part of t_be oyal!qble reserves. In the corr\putatlon of the required statutory minimum reserves.

1.4 Only balances In excess of SMR shall be available for clearing purposes. Any bank that wishes to withdraw the excess funds In Its SMR account shall.seek· and obtain approval from the. Director of Ban~ing Supervision.

1.5 No bank shall · be allowed to withdraw funds below Its· statutory minimum reserve requirement at the Bank of Tanztinla. Instead, banks are encouraged to make effective use of the Inter-bank cash market and other available liquidity bridging windows at the- Bank of Tanzania, namely: Intra-day, discount window and lombard facilities.

2. CALCULATION OF THE REQUIRED STATUTORY MINiMUM RESERV&S, SUBMISSION OF REPORT-5 AND PENALTY

2.1 Each bank shall calculate Its SM~ position dally, and shall. submit a weekly report to the Bank of Tanzania not lofer than the second Monday after the r~ference week. Such weekly reports shall be accomplished In the prescribed format In this Circular entitled 11Report on Required and Available Reserves", a copy of wh!ch Is attocned hereto as Annexure l.

2.2 In order to meet deadlines and avoid penalties for late reporting, each bank shall require Its head .office and all branches or units to record every ·transaction in their books of accounts on the same d9y,.

·.

.. to balance their accounts at the end of that day~ and submit the necessary data to the head office by the fastest means.

2.3 Any bank which. _violates the requirements of ·this Circular shall be Hable to penaltles·.as follows:

(a) For failure to submit the 11Report on Required .and Available Resery~s" on time - A fine of shillings one million (TZS J ,000,000) per day shall be_ Imposed for every day in which the failure continues.

(b) ; · For failure to maintain the minimum reserves required .under thls Circular - an Interest charge equlvah:mt to the weighted average yield of all Treasury bill maturities obtained In the most recent auction shall be applied on the amount of deficiency fot every day In which non"compllance continues.

(c) Misrepresentation or .submission of Incorrect Information In any of the returns by any bank shall attract the penalty charge amounting to shillings one million (TZS 1 ,000,000) per day of existence of such misrepresentation or submission of incorrect Information.

2.4 The penalty charges Imposed In section 2.3, subNsectlon (a), {b), and ·(c) above shall be recovered by the Bank of, Tanzania from any balances of or monies owed to .the bank concerned or as a civil debt.

3.0 REPEALING CLAUSE AND EfPEC.TIVE DATE

3.1. This Circular repeals Circular No.1 as amended on 12th November, 1999 and whlch became effective on 1Sih December, 1999.

3.2. This Circular also repeals the amendment on SMR requirement equivalent to ten percent on total government depo~its, which became effective on 9th June, 2008 ..

3.3. The Circular shall take effect on 15th January, 2009.

Sincerely,

~eWe'·· Prof. Benno Ndulu GOVERNOR

I.

,. .

-'i~AME OF INSTITUTION ........................................................... Ban.kCotfa ...........

BOT FOAM 16,3 (a) Submission: ·1. Dssdllns:Sacand Monday Ttllala a weakly report

after the reference week. 2. In trip/Jests to the Banking ·supervision Dlraotorate

REPORT ON GOVERNMENT DEPOSITS

FOR THE WEEK ENDING .......... ; ........... lin TShs Million}

PARTICULARS -MON TUE WED THU FRI WEEKLY

AVERAGE

CENTRAL GOVERNMENT A: DOMESTIC CURRENCY DEPOSITS (=1+2+3+4)

1. Demand daposlls 2; Time daooslls 3. Savln!ls depoe !Ia 4. Other deposits

B: FOREIGN CURRENCY DEPOSITS (converted Into Tshs> G: TOTAL CENTRAL GOVERNMENT_ (A plus Bl

LOCAL· GOVERNMENT D: DOMESTIC CURRENCY DEPOSITS (~1 +2+3+4)

1. Demand deposits 2. Tlina deposits 3. Savlnos deooslts 4. Olhsr daoostts -

E: FOREIGN CURRENCY DEPOSIT!;! (converted Into Tshs). F: TOTAL LOCAL GOVERNMENT CD plus E) G: GRAND T.OTAL GOVERNMENT (0 plus f) H: MINIMUM REQUIRED RESERVES {20% of G)

Signature ........................... Signature ........................ (Managing Dlreotor/Qeneral Manager) (Direotor of Finance)

Date ............................. Date ................................

Nl'..ME OP INSTITUTION ....................... : ...................................

a or Form 1 B-3 (b) Sank Coda ............

Thla fa 11 weekly report Bubmteafon: 1. Dlfltdllne:aeoond Monday after the reference week.

2. tn frfplfcs/e to tha Banking Supervision Directorate

REPORT ON REQUIRED SMR AND AVAILABLE RESERVES AGAINST TOTAL DEPOSITS AND BORROWINGS

I tin TSha Million) POR THE! WEEK ENOJNQ ......................

PARTICULARS MON rua WED THU FRS Wi!EKLY AVI!RAGE!

A: DOMESTIC CURRENCY DEPOSITS (Tshsl 1. Demand deposita 2. Tlma deposlfs '· ... 3, Sa\'lnoa deposita 4. Other di!QQ_alta 5; oEiP<iSiiB iiitiiirilia

B: BORROWINGS FROM THE PUBLIC (Tshs) C: TOTAL DOMESTIC OIJRI:NCY DEPOSITS AND BORROWING CA_!lfUa fh D: FOREIGN CURRENCY DEPOSITS (converted to Tshsl

1. Demand dePosita 2. Tlme deposita 3. Savings d~ls 4. Other deposlls 6. De~sfla of Banks

E: FOREIGN OURRENCY BORROWINGS FROM THE PUBLIC (converted Into Tsh~ F: TOTAl FOREIGN CURRENCY DEPOSITS AND BORROWING (D.JJius_El G:GRANDTOTAl(C~uaA

H: REQUJAEO SMA ON DEPOSITS AND BORROWING C10% OF Gl 1: REQUIRED SMA ON GOVERNMETIT_DEf>_OSITS tFORM1B-3talllne HI J:TOTAl STATUTORY MINIMUM ReQUIRED RESERVES (H+fl

Signature ............................ Slgnslurs ......................... (Managing IJirector/Qsnaral Manager) (Director of Flnan11a)

Oats ..... ""''"""'''""''' Data ................................

.. :;, .. ..:. ••• • ..... "::::.>;" •.••• ... :.' .. ·•-: ..... : .

THE BANKING AND FINANCIAL INSTITUTIONS (PUBLICATION OF FINANCIAL STATEMENTS) REGULATIONS, 2008

ARRANGEMENT OF REGULATIONS

Regulation Title PART I

PRELIMINARY PROVISIONS

1. Short title 2. Application 3. Interpretation 4. Objectives

PART II PUBLICATION OF FINANCIAL STATEMENTS

5. Quarterly fmancial statements 6. Audited financiai statements 7. Exhibition of audited financial statements

PARTD;l MISCELLANEOUS PROVISIONS

8. Failure to publish ftnancial statements 9. Penalty charge recovery 10. Penalty for misrepresentation 11. Sanctions. and penalties 12. Revocation

1

GOVERNMENT NOTICE NO ................... published on ........... .

THE BANKING AND FINANCIAL INSTITUTIONS ACT

(CAP. 342)

REGULATIONS

(Made under section. 71)

THE BANKING AND FINANCIAL INSTITUTIONS (PUBLICATION OF FINANCIAL STATEMENTS) REGULATIONS, 2008

Short title

Appiication

Interpretation

Objectives

PART I PRELIMINARY

1. These Regulations may be cited as the Banking and .financial Institutions (Publication of Finan,cial Statements) Regulations, 2008 and shall come into operation on the date of publication in the Gazette.

2. These Regulations shall apply to all banks and financial institutions.

IIi these Regulations, unless the conteA.'i requires otherwise

"Act" means the Banking and Financial Institqtions Act; "Bank" means the Bank of Tanzania; bank" has the meaning ascribed to it in the Act; "director" has the meaning ascribed to it in the Act;

'"'financial institution" has the meaning ascribed to it in the Act; "officer" has the meaning ascribed to it in the Act;

4. The objectives of these Regulations are to-

(a) en~u.re that every bank or financial institution maintains a level transparency adequate to enable depositors and creditors and the public at large to make informed decisions;

2

Quarterly financial statements

Audited Financial statements

Exhibition of Audited Financial Statements.

(b) promote and maintain public confidence in the Tanzanian banking sector; and

(c) enhance market discipline by providing financial information to various stakeholders.

PART II

PUBLICAtiON OF FINANCIAL STATEMENTS

5.-(1) Every bank or financial institution shall publish its quarterly financial state:n1ents and any other information in the form to be prescribed by the Bank at least once in one newspaper of wide circulation in Tanzania.

(2) The quarterly financial statements under sub-regulation (I) shall be published within forty-five days after the end of the quarter.

(3) A community bank shall, in addition to the requirements prescribed in sub-regulation (1), display its quarterly financial statements in public places within the areas in which the bank operates.

( 4) A copy of quarterly and annual audited finanCial statements duly signed by the ·chl.ef Executive Officer, Head· of Finance, Head of Internal Audit arid attested by two non-executive board members and newspaper cuttings thereof shall be submitted to the Bank in three days time after publication.

6.-(1) Every bank or financial institution shail publish its annual audited financial statement~ as prescribed by .the Bank at least once every year.in the newspapers of wide circulation in Tanzania.

(2) The all.nuai audited finanCial statements shall be publi~hed within fifteen days after approval of the board of directors of the bank or financial institution but not later than one hundred and five days after the end of the financial year.

7. Every bank or financial institution shall at all times exhibit copies of its last audited fimmcial statements in a conspicuous position in the· public part of its principal place of business and in its branches and agencies.

PART III MISCELLANEOUS PROVISIONS

Failure to publish financial .statements

8. Any bank or fmancial institution which fails to publish its financial statements as required under these Regulations shall ·be liable to a penalty of one million shillings for each day during which such failure continues. ·

3

Penalty ~harge recovery

Penalty for misr~presentation

Sanctions and Penalties

Revocation GN. No. 103 of 2.00i

9. The penalty charge to be imposed under regulation·-8 may be recovered by deducting from any balance of, or moneys owing to the bank or financial institution concerned or collected by written notice.

10. Any bank or financial institution that makes a misrepresentation in its financial statements shall be liable to a penalty of one million shillings for each day until such misrepresentation is corrected.

11. Without prejudice to the other penalties and aCtions prescribed by the Act the Bank may impose on any· bank or financial institution any of the following sanctions for non~compliance-

(a) suspension from lending and investing activities; (b) prohibition from participating in the inter bank clearing

ej(changes; . (c) prohibition from isst1.ing letters of credit dr guarantee; (d) suspension of capital expenditure; (e) prohibition from establishing or opening new branches; (f) suspension from access to the credit facilities of

·the Bank; (g) suspension of the declaration or payment of

dividends; (h) prohibition from accepting deposits;

· . (i) · suspension or removal from office ofthe defaulting director, or employee;

G) .disqualification of defaulting director or employee from holding any_position or office in any bank or financial institution in· Tailza:nia;

(k) revocation or banking licence; or (1) such other sanctions or penalties as the Bank may deem

appropriate.

12. · The Publication of Financial Statements Regulations, 2000 are hereby revoked.

~~~X Dar ls Salaam, ; ~·; ·~··~btb~~hl'b'e;~~&:m

BENNO J. NDULU Governor

4

THE BANKING AND FINANCIAL INSTITUTIONS (INDEPENDENT AUDITORS) REGULATIONS, 2008

ARRANGEMENT OF REGULATIONS

Regulations Title

PART1 PRELIMINARY PROVISIONS

1. Short title 2. Applicatiqn 3. Interpretation 4. Objectives

PART II APPOINTMENT OF lNDEPENDENT AUDITORS

5. Appointment of independent auditors 6. Change ofindependentauditor

PART III DUTIES OF INDEPENDENT AUDITORS

7. Opinion of independent auditor 8. Additional duties 9. Special reports 1 0. Computation of capital position 11. Audit program

PART IV

APPLICATION BY INDEPENDENT AUDITORS

12. Application Letter 13. Assessment ofthe application

1

GOVERNMENT NOTICE NO .................. published on ........ .

THE BANKING AND FINANCIAL INSTITUTIONS ACT (CAP.342)

REGULATIONS

(Made under Section 71)

THE BANKING AND FINANCIAL INSTITUTIONS (INDEPENDENT AUDITORS)

Short title

Application

Interpretation

Cap.286

Cap. 212 Cap. 286

. REGULATIONS, 2008

PART I PRELIMINARY PROVISIONS

1. These regulations may be cited as the Banking and Financial Institutions (Independent Auditors) Regulations, 2008 and shall come into operation on the date of publication in the Gazette.

2. These regulations shall apply to all banks, financial institutions and approved independent auditors.

3. In these regulations, unless the context requires otherWise;

"Act" means the Banking and Financial Institutions Act; "Bank" means the Bank ofTanzania; "conflict of interest" means a situation in which someone in a position of trust,

has competing professional, business or personal interest, making it difficult to fulfil his duties impartially;

"independent auditor" means an accounting or auditing firm which is recognized by the National Board of Accountants and Auditors to be practicing in auditing and related activities and has been approved by the Bank to audit banks and financial institutions;

"officer" has the meaning ascribed to it in the Act; "statutory audit" means an audit performed in accordance with the requirements

of the Companies Act, and the National Board of Accountants and Auditors;

"undercapitalized" means a bank or financial institution whose capital does not meet the requirements of the Banking and Financial Institutions (Capital

3

Objectives

Appointment of independent auditors

Change of independent auditor

Opinion of Independent auditor

Additional duties

Adequacy) Regulations) 2008.

4. The objectives of these Regulations are to establish-(a) criteria for approving independent auditors of banks and financial

institutions; and (b) duties of banks, financial institutions and approved independent

auditors.

PART II APPOINTMENT OF INDEPENDENT AUDITORS

5.-(1) Every bank or financial institution shall appoint annually an independent auditor who has no conflict of interest and notify the Bank within seven days of such appointment.

(2) Where a bank or fmancial-institution fails to appoint an independent auditor under sub-regulation (1), or to fill any vacancy for an independent auditor which may arise, the Banlc may appoint, on behalf of the bank or financial institution, an independent auditor and fix his remuneration which shall be paid by the bank or_financial institution.

(3) A bank or financial institution shall not remain without an independent auditor for more than ninety days from the date when the position falls· vacant. ·

(4) An independent auditor shall not audit the same bank or financial institution for a continuous period exceeding four years.

6. A bank or financial institution shall not in the course of performance of the audit work, change its independent auditor except with the prior written approval of the Bank.

PART III DUTIES OF INDEPENDENT AUDITORS

7. A.n ·independent auditor shall provide ai1 opinion as to whether the financial statements of the bank or financial institution-

( a) represent true and fair view of the financial position and performance of the bank or financial institution; and

(b) have been prepared in accordance with International Financial · Reporting Standards.

8. Subject to section 22 of the Act, the Bank may require an independent auditor to-

( a) submit directly to the Bank such additional information in relation to his audit as the Bank may consider necessary;

(b) carry out any other special investigation and submit a report on any of the matters arising thereof and the bank or financial institution

4

Special reports

Cap. 197 Cap. 171

Computation of capital position

Audit pJ:ogram

Application Letter

Cap. 286

concerned shall-remunerate the auditor in respect of the discharge by him of all or any of such additional duties.

9. The independent auditor shall iminediately report to the Bank if he becomes aware of-

( a) any serious breach of or non-compliance with the provisions of the Act, the Bank of Tanzania Act, Foreign Exchange Act, or regulations, guidelines, circulars or·directives issued by the Bank or any other relevant legislations;

(b) any criminal offence involving fraud or other dishonesty committed by a bank or fmancial institution or any of its officers or employees;

( c} any losses incurred which have caused the bank or financial institution to be undercapitalized;

(d) any serious irregularities which may jeopardize the rights of a depositor or creditor of a bank or financial institution; or

(e) circumstances that make him unable to confirm ability ofthe bank or financial institution to settle claims of depositors or "creditors out of its assets. ·

10. The independent auditor s1J.all compute capital position of the bank or financial instiwtion as· at the end of each financial year taking irito account the requirements of the Act and all relevant prudential regulations issued by the Bank and provide a statement on its adequacy as part of the notes to· the accounts.

11. The audit program and reporting by an independent auditor shall, among other things, include computation of capital adequacy, related parties transactions, assessment of movement of loan provisions, liquidity ratios and profitability outlook, consistent with the requirements of the Act, regulations and circulars is.sued by the Bank.

PART IV APPLICATION BY INDEPENDENT AUDITORS

12. Any auditing firm seeking to be approved by the Bank as an independent auditor under these regulations shall submit an application letter together with- · ·

(a) a short history of the firm, details of its legal and National Board of Accountants and Auditors registration status;

(b) details of the structure and organization of the firm, its principal place of business and branches in Tanzania, and in the case of an international audit fi~, d~tails of the head office including legal and professional status of the parent firm;

(c) names, particulars and detailed curriculum vitae of partners and senior professional staff demonstrating previous experience in the audit of banks and financial institutions;

(d) list of major audit assignments that have been performed for the last

5

ASsessment of · the application Cap.286

Disqualification from appointment

three years and total fees received for the last year from each audit assignment that was performed.

(e) details of any existing relationship either directly or indirectly between the finn or partner and any bank or financial institution regulated by the Bank;

(f) any other information the Bank may require.

13. When assessing an application the Bank shall consider whether the firin has at least ten staff with education and experience in accountancy and auditing, and at least four of whom are registered with National Board of Accountants and Auditors ..

PARTV DISQUALIFICATION FROM APPOINTMENT

14. An audit firm shall not qualify for appointment as an ip.dependent auditor of a bank .or financial institution if any of its partner or member is-

( a) a director, officer or employee of any bank or financial institution; or

(b) a business partner of a director, officer or employee of that bank or financial institution; or

(c) an employee or employee of a director , officer or employee of that bank or financial institution; or

(d) a director, officer or employee of an associate of that bank or financial institution; or

(e) a person who, by himself or his business partner or his employee, . regularly P.erforms the duties of secretary or accounting for that bank or financial institution; or

(f) a firm or member of a firm of auditors of which any partner or employee falls within the above categories. or

(g) any other person whose appointment as an independent auditor may create conflict of interest.

Delisting approved auditors

of 15. An independent auditor shall be removed from office or from the list of approved independent auditors if he-

( a) fails to compiy with the requirements prescribed in the Act and these R~gulations, or

(b) fails to meet the requirements of International Standards of Auditing.

PART VI MISCELLANEOUS PROVISIONS

Notice 16. An independent auditor of a bank or financial institution shall forthwith give written notice to the Bank, of-

6

(a) his resignation from office and the reasons thereof; (b) his decision npt to seek re-appointment and the reasons thereof; or (c) any qualification ofhis opinion on the financial statements.

Notification 17. An independent auditor shall notify the Bank within 30 days of ~:~~!ange of changes in its organization structure involving the partners and staff specified

in regulation 12 and 13. ·

Notificati.on of relationship

Revocation GN. No. 102 of2001

18. An independent auditor shall· immediately notify the Bank if the finn or any partner ·establishes any relationship with a bank or finanCial institution.

19. The Independent Auditors Regulations, 2001 are hereby revoked.

7

£1~~ x BENNO J. NDULU

Governor

THE BANKING AND FINANCIAL INSTITUTIONS (PHYSICAL SECURITY MEASURES) REGULATIONS, 2008

ARRANGEMENT OF REGULATIONS

Reguiation Title PART I

PRELIMINARY PROVISIONS

1. Short title 2. Application 3. Interpretation 4~ Objectiv~s

PART II REQUlllliD MINIMUM SECURITY MEASURES.

5. Minimum requirements in security policy 6. Burglary and robbery 7. Training on security measure!) 8. Appointment of security officer 9. Responsibility of Board of Directors 10. Minimum security devices 1 i: Exemption 12; Maintenance of records 13. Reporting to the BaTilc 14. Interrial audit ~anual 15. S~ong rooms 16. Attributes of a strong room

PART III MISCELLANEOUS PROVISIONS

17. Sanctions and penalties

1

financial institution; "robbery" means taking something of value from a person by means of force, violence or intimidation.

Objectives 4. The principal objective of these regulations is to prescribe

Minimum requirements in security policy

. minimum.:.security measures to be instituted by all banks and financial institutions for the purpose of-

( a) preventing acts of robbery and burglary; (b) assisting in identifying and apprehending persons who comniit

acts of robbery or bm:glary; (c) preventing injury and loss oflives to staff and customers; (d) ·preventing damage or loss of assets, which could result into

major los~es to individual in.Stitutions, the banking sector and the national economy, and;

(e). creating security awareness among management and staff in all banks and financial institutions thereby promoting a security conscious working environment.

PART II REQUIRED MINIMUM SECURITY MEASURES

5.-(1) Every bank or financial institution shall have a written physical security policy and procedure manual, which shall be submitted to the Bank for review and clearance.

(2) The physical security policy and procedure manual under subregulation (I) shall at least address the following-

( a) security measures for transporting of cash and other valuables; (b) measures for ensuring the safekeeping of all currency,

negotiable instruments, and other valuable items; (c) measures for ensuring security of strong rooms/vaults; (d) procedures for assisting in identification of persons committing

acts of robbery or burglary against the bank or financial institution;

(e) p~ocedures for preserving evidence that may aid identification and prosecution of persons committing acts of robbery or burglary against the bank or financial institution;

(f) provide for initial and periodic training of management and staff in their responsibilities under the .security program for proper employee conduct during and after a robbery or burglary;

(g) procedures for selecting, testing, operating and maintaining appropriate security devices as specified in regulation 1 0;

(h) criteria and procedures for selecting security company or.

3

Burglary and robbery

Training on security

measures

Appointment of Security Officer

Responsibility of Board of Directors

Minimum Security Devices

Exemption

Maintenance of records

(h) criteria and ·procedures for selecting security company or institution to provide security services to a bank or financial institution should such services be needed; and

(i) provide for need of having security program.

6. The physical security policy and procedure manual shall exhaustively address event~ of burglary and robbery.

7. Every bank or financial institution shall train its Management and staff on physical security measures and such training shall cover the importance of security measures, including at minimmn.

(a) how the secm:jty systems and devices work; (b) what to do in the event of robbery or burglary; (c) how to be a.good witness; (d) how to preserve evidence; (e) how to deal with t~eatening messages and kidnappings; and (f) what measures to take in the evt:?nt of fire o1,1tbreak.

8. Every bank or financial institution shall appoint or designate a suitable officer who shall be responsible fo.r day-to-day security matters of the bank or financial institution.

9. The Board of Directors of every bank or financial institution shall ensure effective implementation and administration of the security program and other security issues.

10. Every bank or fmancial institution shall install at minimum security devices as indicated in the First Schedule to these Regulations.

11. Upon prior written request from a bank or financial institution the Bank may grant exemption from complying with the provision of regulation 1 0.

12.-(1) Every bank or financial.institution shall maintain records on implementation, administration and effectiveness of the security policy, security program and other security issues.

(2) The records under sub-regulation (1) shall at least cover the information ·reflected in the Second Schedule to these Regulations.

4

Internal Audit Manual

Strong Rooms

Attributes of a strongroom

Sanctions and . penalties

14. Every bank or financial :institution shall include in its internal audit manual comprehensive procedures · for auditing its physical security measures.

15. Every bank or financial institution shall ensure that its banking halls are built in a manner that limits customer's visibility and access to cash vaults, safes or strong rooms. ·

16. Notwithstanding the location or set up of banks and financial institutions' strong rooms as prescribed under regulation 15, every bank or fmancial institution shall ensure its strong rooms are built in accordance to the best or international construction standards and should include-

( a) fire alarm security system; (b) intrusion detection Security Systems; (c) 24 hours monito~ed surveillance cameras (CCTVs); (d) secured locks and keys to avoid duplication; and (e) Secured safes and storage equipments, which are rust free,

water resistant and fire proof.

PART IV MISCELLANEOUS PROVISIONS

17. Without prejudice to other penalties and sanctions prescribed by the Act the violation of any of the provisions of these regulations shall attract one or more of the following sanctions and penalties-

( a) suspension of the right to establish or open new branches; (b) suspension of the right to accept deposits; (c) revocation ofbanking.license; (d) suspension from office of the defaulting director, officer or

employee; (e) perpetual disqualification from holding any position or office in

·any bank or financial institution under the supervision of the Bank; and

(f) imposition of other penalties on the bank or financial institutions in such amounts as may be determined by the Bank to be appropriate and reasonable;

5

FIRST SCHEDULE

(Made under Regulation 10)

MINIMUM SECURITY DEVICES

Every bank or financial institution shall install and appropriately maintain and operate in all its banking premises, the following security devices:- . .

I. A means of protecting cash and other liquid assets, such means may include vault, .safe or other secure space;

2. A combination lock for all safe and vault or strong room doors, with at least dual control;

3. Time locks or time delay locks for safe and strong.;.room doors, with special time for opening and closing; ·

4. An alarm system or other appropriate device for promptly notifying the nearest responsible law enforcement agency or a contracted security company or institution, of an attempted or perpetrated robbery, burglary

5. Intruder Alarm System;

6. Surveillance cameras or any other device for monitoring movements;

7. Panic buttons for all tellers;

8. Bullet proof glass for tellers' cubicles;

9. A means of controlling unauthorised persons to access various areas in a bank or financial institution.

6

SECOND SCHEDULE

(Made under Regulation 12)

RECORDS ON IMPLEMENTATION. ADMINISTRATION AND EFFECTIVENESS OF THE SECURITY PROGRAM AND OTHER SECURITY. ISSUES

Every bank or financial institution shall maintain records covering at least the following:-

I. Incidences of robbery or burglary the bank or financial institution experienced during the year. Please provide details; .

2. 1

Type of security devices the bank or-financial institution has installed. Please list;

3. Frequency during the year the bank or fin~ial institution tested each of its security devices to detennine its effectiveness and efficiency;

4. Frequency during the year the bank or financial institution canied. out maintenanc-e of its security devices;·

5. Plans the bank or financial institution has to improve testing and maintenance of security devices in the coming year; ·

6. Frequency during the year the bank or financial institution carried out training of its management and staff on security issues;

7. Type of training on security matters during the year the bank or financial institution ~onducted for its management and staff;

8. Members of management and staff who were trained during the year. Please list them by titles or positions; ·

9. Plans on training of security inatters the bank or financial institution has for next year; I 0. General annual security vulnerability assessment;

11. Any other security issues the bank or financial institution would wish to repOJ;t.

~a~-as. Sala~-' . . .. ,. _,_ · o:~;i. • -. ~December ~2000

7

GJN~-- X BENNO J. NDULU

(]overnor

./ l

Tiffi BANKING AND FINANCIAL INSTITUTIONS (PRO:MPT CORRECTIVE ACTION) RRGTJT.ATTONS, 2008

ARRANGEMENT OF REGULATIONS

Regulation Title

PART!

PRELIMINARY·PROVISIONS

I. Short title 2. Application 3. Interpretation 4. Objectives

PART II

CORRECTIVE ACTIONS

5. Mandatory actions for adequately capitalized institution

6. Discretionary actions for adequately capitalized institution

7. Mandatory actions for underc~pitaHzed institution

8. Discretionary actions for undercapitalized institution

9. Mandatory actions for significantly undercapitalized institution

I 0. Discretionary actions for significantly undercapitalized institution

11. Critically undercapitalized institutions

12. Submission ofrecapitaHzation plan

. 1

GOVERN1\.1ENTNOTICE.NO ... ; .............. published on ........ .

TIIE BANKING AND FINANCIAL INSTITUTIONS ACT (CAP. 342)

REGULATIONS

(Made under sections 34 and 71)

TH:E BANKING AND FINANCIAL INSTITUTIONS (PROMPT CoRRECTIVE ACTION) REGULATIONS~ 2008

PART I PRELIMINARY PROVISIONS

Short title 1. These regulations may be cited as the B~king ~d financial Institutions (Prompt Corrective Action) Regulations, 2008 and shall come into operations qri the date of publication in the Gaze tie.

Application 2. These regulations shall apply to all banks and financial institutions.

Interpreta- 3. In these Regulations, unless the context requires otherwise-tion

"Act" means the Banking and Financial Institutions Act; ·"adequately capitalized" in rel~tion to a ·bank or financial institution,

means core capital of not less than ten percent of total riskweighted assets, and off balance sheet exposur-es determined in accordance with the Banking and Financial Institutions {Capital Adequacy) Regulations, 2008;

''Bank" means the Ban:k ofTanzania; "bank" has the meaning ascribed to it in the Act; "critically undercapitalized" in relation to a bank or financial institution,

means core capital of less than four percent of risk wei-ghted assets and off balance sheet exposure determined in accordance with the Banking and Financial Institutions '(Capital Adequacy) Regulations, 2008;

"core capital" has the meaning ascribed to it in the Act; "financial institution" has the meaning ascribed to it in the Act;

2

Objectives .

Mandatoxy actions for adequa~ely

capitalized institution

"signific?IJ.tly undercapitalized" in relation to a bank· or financial institution, means core capital of.less than six percent of total "riskweighted assets, off balance sheet exposure and capital charges for market risk determined in accordance with the Capital Adequacy Regulations, 2008;

"undercapitali7;ed'-; in: relation to· a bank or. financial instilulion, means . core capital of less than ten percent of total risk weighted assets and off balance she.et exposures determined in acc.ordance with the Banking and Financial fustitutions (Capital Adequacy) Regulations, 2008.

4. The objectives of these Regulations are to-( a) ensure timely and effective actions to deal with a weakening

bank or fmancial institution; (b) enhance transparency by establishing the minimum actions

the Bank shall take in addressing identified weaknesses in banks and financial institutions; and

(c) maintain confid~nce in the Tanzanian banking sector.

PART II <::;ORRECTIVE ACTIONS

5. Where in the opinion of the Bank, an adequately capitalized bank or financial institution is likely to incur a loss which may result in it bec_oming·undercapitalized, or is otherwise conducting its business in an unsound manner, the Bank shall-

(a) notify and require the bank or financial institution to submit to the Bank, within such period as it may spedfy, a written plan of corrective action which- ·

(i) identifies ~ the existing weaknesses in the administration or operations of the bank or financial institution;

(iii)

(iv)

(v)

(vi)

determines in detail the corrective required to remedy such weaknesses; and offers a realistic time-table for taking such measures. identifies the existing weaknesses administration or operations of the financial institution; determines in deta:il the corrective required to remedy such weaknesses; and offers a realistic time-table for taking such measures.

meas_ures

in the bank or

measures

(b) prohibit the bank or financial institution from declaring and paying any dividends which would, iri the opinion of the :Sank, likely cause the bank or financial institution fail to comply with the requirements prescribed under the Banking

Discretii:·nar y actions for adequately capitalized institution

Mandatory actions for undercapitali zed institution

Discretionar y actions for undercapitali zed institution

Mandatory actions for · significantly undercapitali zed institution

may-

and Financial Institutions (Capital Adequacy) Regulations, 1008;and .

(c) inteirsify its oversight and monitoring of the bank or financial institution in accordance with the principles of risk-based supervision.

6. In addition to actions prescribed in regulation S, the Bank

(a) .impose :civil money penalties; (b) issue cease and desist orders; or (c)· initiate suspension or removal of any director, officer or other

person or persons in the position of management;

7. Where· a bank or financial institution is undercapitalized, the Bank shall-

(a) take the measures prescribed in regulation 5, and (b) require the bank or financial institution to submit to the Bank

within forty five days of such notification a capital restoration plan which:

(i) specifies steps to be taken by the bank or financial institution to become adequately capitalized; and

(ii) specifies the levels of capital to be at:tained during each quarter in which the plan will be in effect.

8.-(1) Irt addition to actions prescribed in regulation 7, the Bank may appoint a suitably qualified person who shaH-

(a) advise-and assist the bank or financial institution in designing and fulfilling the capital restoration plan; and

(b) regtilarly submit to the Bank a progress report of the plan. (2) The Bank shall fix remuneration of the person appointed in

sub-regulation (l) ·and the bank or financial institution shall pay such remuneration.

9. · · Where a bank or financial institution is significantly undercapitalized, the Bank shall-

(a) take the measures prescribed in regulation 7; (b }- prohibit all transactions with connected parties except

repaym~nt to the bank or financial institution of any outstanding -credit accommodation or any transaction specifically permitted by the Bank to facilitate recap i taliza ti on.

(c) prohibit the bank or financial institution from awarding any bonuses or .increments in the salary, emoluments and other

4

Discretionar y actions for significantly undcrCllpitali zed institution

Critically undercapitali zed institution

Submission of recapitalization plan

benefits of its directors and officers; and (d) prohibinhe bank or financial institution from opening any

.branches or other expansion of operations.

10. In addition to any other actions prescribed in regulation 9~ the Bank may-

(a) impose restrictions on the growth of assets~ liabilities or l?oth ofthe bank or financial institution;

(b) restricfthe rate of interest on deposits; or. (c) require the l;:>arik or financial institution to cease lending or

any other business activity.

ll.-(1) Where a bank or financial institution is cr:iticalJy 1.1ndercapitalized, the Bank shal1-

(a) take the actions prescribed in regulation 9; (b) assist the institution in handling the crisis. (2) Not later than ninety days after a bank or financial institution

is determined by the Bank to be critically undercapitalized, the Bank shall appoint a statutory manager or liquidator unless-

( a) core ·capital is greater than two percent of its total riskweighted assets and off.:balance sheet exposure; and

(b) the bank or financial institution is operating in compliance with a capital restorati6n plan accepted by the Bank.

12. Where an und_ercapitalized or significantly undercapitalized bapk or financial institution fails to submit a recapitalization plan, or such plan is not accepted by the Bank~ the Bank shall, not later than ninety days from the date of the original notification, deem the bank or financial institution to be critically undercapitalizt?d and take the actions prescribed in regulation 11. ·

~-= ~ D~~ .. ~ala~, __ <?> .· .. - .. .

BENNO J. NDULU Governor

·~·'•~ •. ; ~ .necember,2008

5

I

7

/

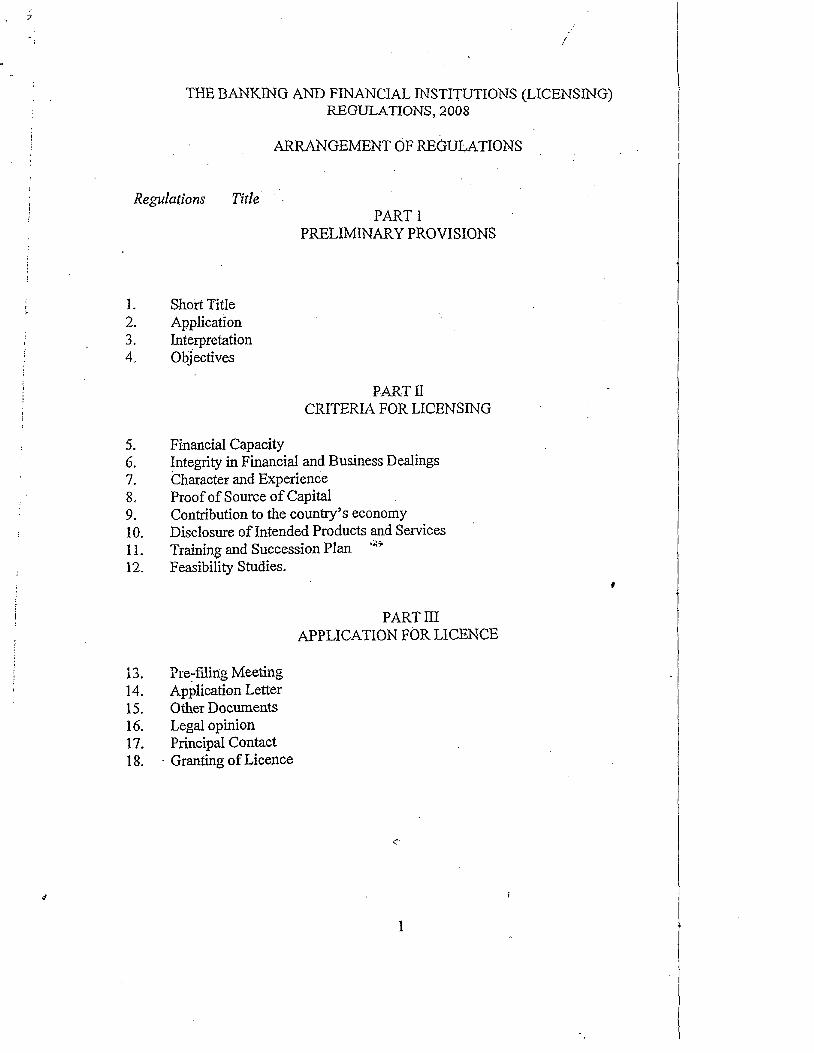

THE BANKING AND FINANCIAL INSTITUTIONS (LICENSING) REGULATIONS, 2008

ARRANGEMENT OF REGULATIONS

Regulations Title

1. Sheri Title 2. Application 3. Interpretation 4. Objectives

5. Financial Capacity

PART l PRELIMINARY PROVISIONS

PART II CRITERIA FOR LICENSING

6. Integrity in Financial and Business Dealings 7. Character and Experience 8. Proof of Source of Capital 9. Contribution to the country,s economy 10. Disclosure of Intended Products and Services 11. Training and Succ.ession Plan •:>is-

12. Feasibiiity Studies.

13. Pre-flling Meeting 14. Application Letter 15. Other Documents 16. Legal opinion 17. Principal Contact 18. · Granting of Licence

PART III APPLICATION FOR LICENCE

-;;:·

1

I

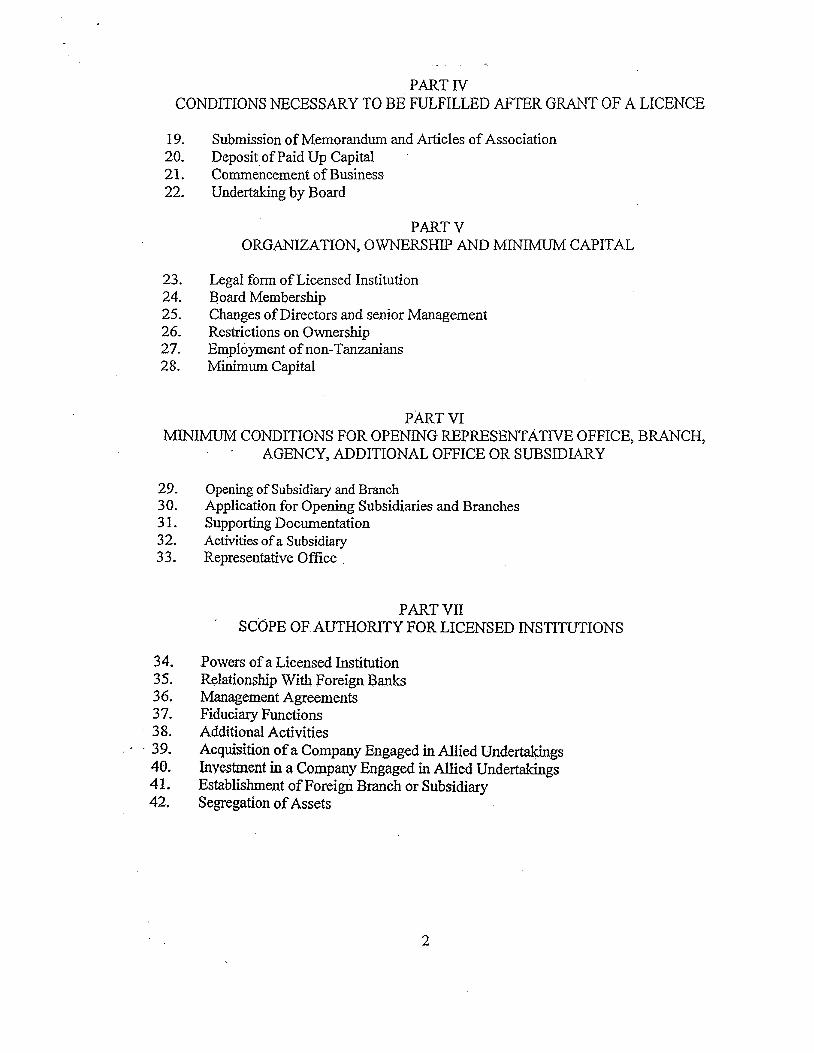

PART IV CONDITIONS NECESSARY TO BE FULFILLED AFTER GRANT OF A LICENCE

19. Submission of Memorandum and Articles of Association 20. Deposit of Paid Up Capital 21. Commencement of Business 22. Undertaking by Board

PARTV ORGANIZATION, OWNERSHIP AND MINIMUM CAPITAL

23. Legal form of Licensed Institution 24. Board Membership 25. Changes ofDirectors and senior Management 26. Restrictions on Ownership 27. Employment of non-Tanzanians 28. Minimmn Capital

PART VI MINIMUM CONDITIONS FOR OPENING REPRESENTATIVE OFFICE, BRANCH,

AGENCY, ADDITIONAL OFFICE OR SUBSIDIARY

29. OpeningofSubsidiary and Branch 30. Application for Opening Subsidiaries and Branches 31. Supporting Documentation 32. Activities of a Subsidiary 33. Representative Office _

34. 35. 36. 37. 38.

- - 39. 40. 41. 42.

PART VII SCOPE OF. AUTHORITY FOR LICENSED INSTITUTIONS

Powers of a Licensed Institution Relationship With Foreign Banks Management Agreements Fiduciary Functions Additional Actjvities Acquisition of a Company Engaged in Allied Undertakings Investment in a Company Engaged in Allied Undertakings Establishment of Foreign Branch or Subsidiary Segregation of Assets

2

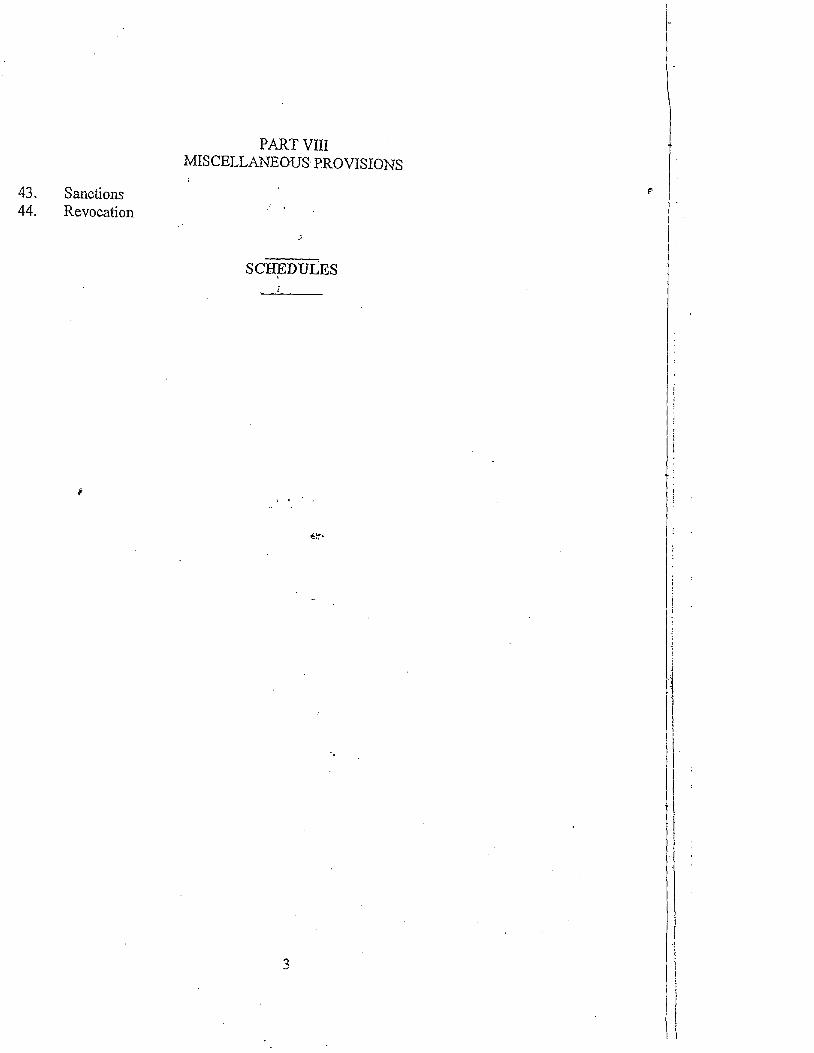

43. Sanctions 44. Revocation

PART VIII MISCELLANEOUS· PROVISIONS

~·

SCHEDULES

3

,1

I I I I

I :

GOVERNMENT NOTICE NO ........................ published on .................... .

f

Short title

Application

Interpretation

_,

THE BANKING AND FINANCIAL INSTITUTIONS ACT [CAP 342]

REGULATIONS

(Made under section 71)

THE BANKING AND FINANCIAL INSTITUTIONS (LICENSING) REGULATIONS, 2008

PART 1 PRELIMINAR ?-PROVISIONS

1. These Regulations may be cited as the Banking and Financial Institutions (Licensing) Regulations, 2008 and shall come into operation on the date of publication in the Gazette;

2. These regulations shall apply to all banks and financial institutions.

3. In these regulations unless the context requires otherwise: "Act" means the Banking and Financial Institutions Act; "allied undertakings" include such activities as may be specified by the

Bank to be allied or related to the business of banking; · "Bank" means the Bank of Tanzania; "bank" and "banking business" have the meaning ascribed to them inthe Act; "conflict of interest" means a situation in which someone in a position of

trust has competing professional, business or personal interest, making it difficult to fulfil his duties impartially;

"core capital" or "tier 1 capital" has the meaning ascribed to it in the Act; "director" has the meaning ascribed to it in the Act; "disclosed reserves" has the meaning ascribed to it in the Act; "financial institution" has the meaning ascribed to it in the Act; "financial intermediation" has the meaning ascribed to it in the Act; "fit and proper person" means a person with th~ attributes required of a

member of the board of directors and management of a bank or financial institution as per the criteria set out in the First Schedule to these Regulations;

,.

Objectives

Financial capacity

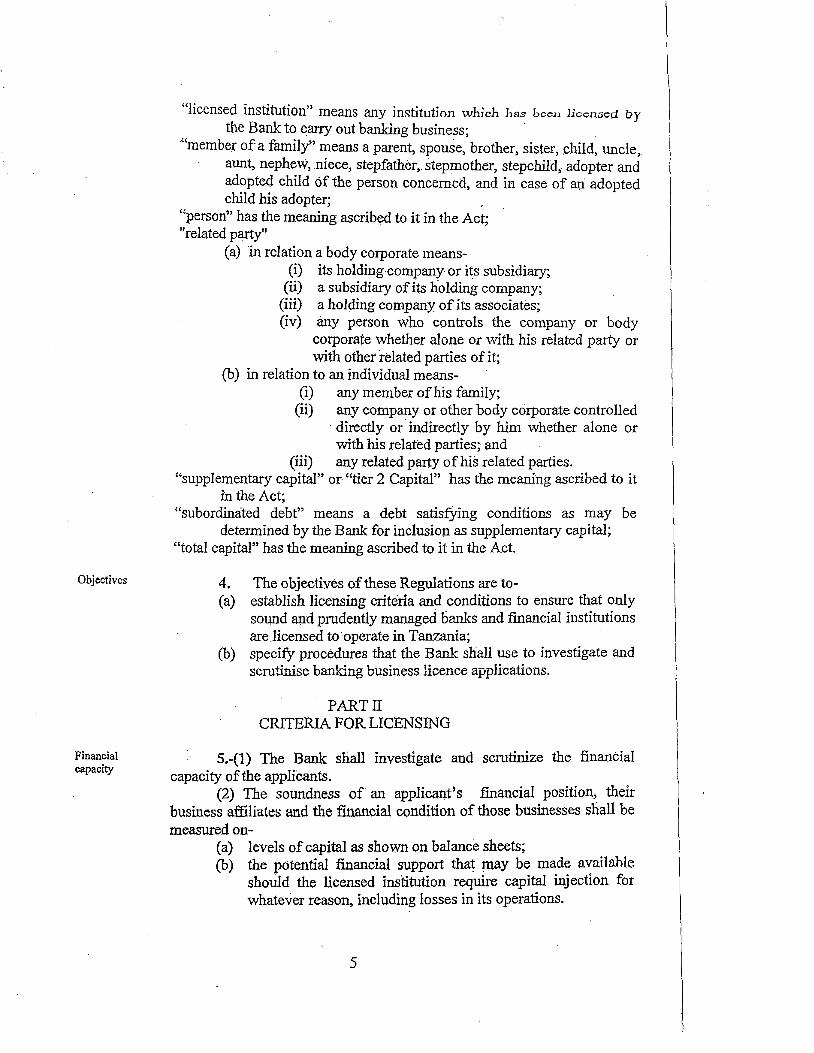

"licensed institution" means any institution which has been licensed by the Bank to carry out banking business; · .

·"member of a family" means a parent, spouse, brother, sister, .child, uncle,. aunt, nephew, niece, stepfather,. stepmother? stepchild,. adopter and adopted child of the person concerned, and in case of an· adopted child his adopter; .

"person" has the meaning ascribed to it in the Act; . "related party"

(a) in relation a body corporate means-(i) its holding company or its subsidiary;

(ii) a subsidiary of its holding company; (iii) a holding co~ party of its associates; (iv) any person who controls the company or body

corporate whether alone or with his related party or with other related parties of it;

(b) in relation to an individual means-(i) any member of his family;

(ii) any company or other body corporate controlled · directly or· indirectly by him whether alone or with his related parties; and

(iii) any related party of his related parties. "supplementary capital" or "tier 2 Capital" has the meaning ascribed to it

in the Act; "subordimited debt" means a debt satisfYing conditions as may be

determined by the Bank for inclusion as supplementary capital; "total capital" has the meaning ascribed to it in the Act.

4. The objectives of these Regulations are to-( a) establish licensing criteria and conditions to ensure that only

soqnd and prudently managed banks and financial institutions are.Iicensed to·operate in Tanzania;

(b) specify procedures that the Bank shall use to investigate and scrutinise banking business licence applications.

PART II CRITERIA FOR LICENSING

5.-(1) The Bank shall investigate and scrutinize the financial capacity of the applicants.

(2) The soundness of an applica11-fs financial position, their business affiliatm; and the financial condition of those businesses shall be measured on-

( a) levels of capital as shown on balance sheets; (b) the potential financial support tha~ t1laY be made availahl.c

shoUld the licensed institution require capital injection for whatever reason, including losses in its operations.

5

Integrity financial business d~~iings

Ch;'lf8.cter ~xperjenc«

(3) The Bank, shall asse~s th~ ability of the appli~ap.t and their bu~jn(;?s~ ·l;!ffili~t~s to pay their ·CU.rt~.Q.t obligatiou~ from their income, reasonabillty.of~alu~tion they as.sign to tp,e1r ~ssets, and their net:-worthin relation to other liapilities. .

.... (4) +t sh~U b~ jn the interest of the Bank to e.stablish that shares in a licem>ed in~~itV-tio.n are not purchaseQ. with borrowed money.

(5) Sl.lb~regulation (4) shall not apply to licensed bank or financial instit:tJtio4 going .PJJP,lic, provided that shan~s t9 be purchased at the Initial :Publio Ofter sta.ge shall P.ot be pledged as collateral.

(6).The applic::$t shall indicate and declare to the Bank sources of fun4s f()r b11ying ~h8{es.

·in 6. The J3a,nk shall review the history of the applicant to determ.ine and their reputation, exp~Jjence in banking operations, financial so~dness

arid integrity in past and present business practices. ·

a,nd 7.-(1) The Bank shall make an assessment, in ac~ordance with the criteria set out in the First Schedule to these Regulations as to whether the propos¢ members of the board of directors or senior management of a proposed il.lstitution are fit and proper persons. · (2) The ~~ shall evaluate the proposed members of the board of directors or senior management team with' respect to their experience l;l,nd apility to manage fun4s, institute proper credit e.valJJatio~, collection procedures~ accounting sy~t~ms, eff'1c~ve i11temal ~qptrql, audit progrru,nmes a.rld manag_ement infonnation syst~rns.

(3) The Bank may interview the prppos~d boqrd or senior management team members and enquire as to past performance, reputation. and skills.

·· ( 4) The Bank shall make an assessment of proposed board or senior management team members regarding their fortrl.al education, professional qualifications, work experience, reputation, crirp.inal record and conflict of intereSt.

(5) The Bank shall requiry board or senior management team members to comprise people of Sl)fficiently strong ch~acter who are able to oversee the licensed institution's operations effectively by having the requisite ballking busin~ss experience.

(6) The Bank ~hall further assess whether individuals proposed as · h<;>l;ll'q or s~.plor ll1anagement team memb~rs hav~ tl;te necessary adrn~nistrative, organizational and decision-making skills, and ability to demonstrate reliability and sound char~cter.

Proof of source · ofcapi~I 8. Every shareholder of a proposed institution shall provide to the

Bank assurance that the proposed paid up capital shall be fully paid up prior to the Bank's issuance of a permit or an authority to commence banking operations.

6

Contribution to the country's economy

9.-(1) Every application shall convey to the Bank intentions of the proposed institution with regard to contributions towards the country's economic development.

(2) The Bank shall take into account the extent· to which lending policies and internal controls of the applicant are designed to promote directly or indirectly the financial or economic activities in the rural sector including rural-based industries, mining and tourism.

Disclosure intended products services

of 10. Each applicant shall indicate the financial products and and services to be offered and how ·such. products and services shall be of

benefit to the country.

Training and su_ccession plan

Feasibility studies

11.-.(1) Every applicant shall submit a training plan for imparting banking skills and expertise to staff indicating specific time frame.

(2) The applicant shall submit a clear plan and strategies on mode, time and contents of the extent to whi~h Tanzanian staff shall occupy senior management positions in the licensed institution.

12.-(1) Every applicant shall provide details of feasibility studies, business plans and projected balance sheets, income statements and cashflow statements for four years.

(2) At minimum each applicant shall provide-( a) draft policies and procedural manuals establishing how the

licensed fmancial institution shall operate in a manner consistent With the principles established in Risk Management Guidelines issued by the Bank;

(b) description of accounting system ~d information and communication technology to be used in the operations of the institution and proposed future investment;

(c) number of employees, job descriptions of senior management positions and an organization ch.art; ·

(d) des~ripuon of internal control procedures that the licensed institution shall implement;

(e) narrative description of shareholders, board and senior management and strategy for the successful operation of the licensed institution;

(f) plans and strategy on supporting rural based activities; (g) Sources.offunds of shareholders and subscribers; (3) Every applic~t shail submit ·business plan and financial

projections prepared in accordanc_e with the guidelines provided in the Fourth Schedule to these Regulations.

7

Pre-filing meeting

Application letter ·

Other documents

Legal opinion

Principal contact

PART III APPLlCATION FC>It LICENCE

l3.-(1) A pre-filing meeting between promoters and the Bank sh~ll be held prior to formal submis::;ion of the application.

. (2). An application shall not by considered until such a meeting is held or a waiver is granted. ·

14. A pt!f$On int~nqing tp carry on b:'!.nking busine$.S ·in Tanzania shall submit to t4e B~- a l~tter of application as prescribed in the Second Schedule to tb.eseRegula.tions.

l5. An a,pplication shall be signed by the directors of the applicant or a person authorized by the appilcant and submitted together with-

( a) authe11ticat.ed legal documents or board rysolution authorizing the signatory; .

(b) .one copy of each of the d9cllinents listed in the Third Sdledule to these Regulaticms;

(c) banker's cheque for three million shillings or any other amop.p.t as may be determined by the Bank from time to time, pay~ble to the Bank as'non-refinlciable application fee; :md

(d) evidence regarding sotirce and availability of funds to subscribe to the capital. of the bank or financial institution.

16. The Banl:c may require the applicant to provide legal opinion on any issue related to the a,pplic~J.tion of the licen-se as it may determine.

17. An applicant shall designate and inform the Bank its principal contact and spoke~person of the proposed institution.

Granting licence · of 18.-(1) The Ba.nlc shC!J-1, within ninety days aft-er receipt of a

complete application or where further information has been required, after receipt of such iiUQnnation, grant a licence or reject the application.

Submission of MEMARTS

· (2) In case of rejection,, the Bank shall in writing provide the applic:ap.t an .~xplanation of the .ground upon which the rejection is based. · · (3) A licence once i~~ueu ~hall remain in force unle~-os suspended

or revoked as provided in th~ Act.

PART IV CONDITIONS NECESSARY TO BE FULFILLED AFTER

GRANT OF A LICENCE

19.-(1) An applicant shall obtain the Bank's approval before filing and registering its Memorandum and Articles of Association with the Registrar of Companies.

8

Oeposit of .paid up tapital

Commencement ofbusin~ss .

Undertaking by . board

. , .,·;/(: );\;'i<¥~~f;;¥~~:;i:.;~

(2) ){'· c&py' of:iY.I:grnofkndbtn and ArtiCles qf Association registered shall be submitted to the Bank. after being registered by the Registrar of companies.

20. A licensed institution, not later than thirty days after grant of · t:heJ~cence shall deposit if4 paid up capital either in Tanzanian shilHngs or ih foreign currency, in a Tanzanian. registered barik or financial institution, in Treasury Bills or other· Government securitie,s of not more than 364 d~ys held with the Bank.

21. A licensed institution shall not .commence business untU all senior management staff have been vetted and the business premises, security facilities, communication facilities, processing equipments, accounting. and internal control systems are. in place arid ·have been inspected or reviewed by the-.Bank.

22.-(1) Every memtJer of the board of directors of a licensed institution shall execute a ·legally binding undertaking to fulfil his obligations towards maintaiq,ing a safe, sound and profitable institution .

.: (2) Without prejudice to sub-regulation (1) a member shall also undertake to comply with the provisiorts of the Act, Bank of Tanzania Act, other laws, Regulations, policies,' circulars, orders and instructions made there under.

PARTV ORGANISATION, OWNERSHIP AND MINIMUM CAPITAL

Legal form of licensed institUtion

Board mem.~ership ·

Z3. A licensed. institution shall be organized in the foim of a ·company lllp.ited by shares and incorporated tinder the laws ofTanzania ..

24.-.(1) The bo~rd of directors of a 11~ensed insti~tion shall have a membership of not less than five, tWo of whom shall have banJdng or related experi~nce and, majoritY ofwlJ.om shall be non-executive. · (2) ~'The chairperson of the licensed institution)ihall be a non-exec').ltive member ofth~ board~

Change of . .. 25.-(1) A licensed institution shall not appoint any per$on to the ~~r:o~ . and·. post of sen..ior mamtgement 6r board of qirectors without obtaining .prior manatom~uL approval of the<Bank,

Restrictions on ownership

(2) A licensed in~titution Shall, within seven days of the departure of any meJ:I?.l:>er,of the sehior" ~anagement or board of directors, notify the Bank ·of such departure together with rea:Sons thereof.

26: ... (1) A person ·shrui·:not own or control directly or indirectly a beneficial interest of more than twenty percent of the voting shares of any

9

Ero.ployment

bank or financialinstituti_on, ~~cept as provided undyr s~ction 15 of th Act. . ., ' . . . I

· . (2) For th~ ptlrpps~; bf ~U.b,r"¢suUi~f9~· (i) indirect. OW11er$hip d1 control shall mean ownersh.iji or .Control through relaJec;l parties. . !

. ~·· .· . . . . . I

of non., ' 27. A licensed ihstit1,1tio~ $.hali not employ a non-Tanz~an o:

ren~w any cqntr~ct of such p<1ison unless it seeks and obtains prio1 ~ro~~~a~ · . Tani:ifli<l.!lS

. Minimum ca~ital

' (2) Tq!( n4mber · o:f non-Taw;anians in the in~titution shall nq1 · exceed. fiv~ at aily ti1U~·

. 28.-(l).Every licensed institution shall com~ence operations with a core, c.apjt?l $p~pified i_p. the B~n,king and Finaridal t~~titutions (Capital Adeq~a~y) Regulatiqns, 2608 or such higher .amount as· the Bank may prescribe~· · (2) Where c~pital is remitted in foreign currency, it shall be

. reflected in the books of the licensed institution in Tanzahian shilling .. using eX.chang~ rate prevmli~g on the date of rell.1ittance. ' .

PART VI MINIMUM CONI)JTIONS FOR OPENING REPRESENTATNE OFFICE, BRANCH,

. . ... AGE;NCY,. ·. ' ; ..

Opening of sub"sidiaries and branches .

Appli~~tion for opening

:subsidiaries and brail_ches

S~ppQr$g documentation

·· . .ADI)ITIONAL OFFICE OR SUBSIDIARY

z~. A lipensed. institutioi1 shall not invest in capital expenditUre for the ·purpose of open.ip.g a representative office, subsidiary, branch, .agency or additional office in or outside TmlZallia. without the prior a:pprqyaJ of ¢e a~.

30.. The · B.ank may apprqve an application for opening a subsidiary,, l:Jranch, a.gency or additional office only . after proven successful,· sound and profit~ble operation· ?Jid it may, aS a condition of approval require additional capital.

·31. - An a,ppliqati()n- for establislun~rit of a subsidiary, branch, ~gency or an additional offi.cc sh~l b¢·suppor.t.ed by-. . (a) projepted b~anc~. sheet ancf income · statetnt;nt for the next

· ihree yea,rs; · (b )-Pcinsolic;Iated .projected bahmce sheet and income statement fo:r

the next three years; "(c) proposed organiza,tion stn,Icture; (d) d~taiied . bu.dget . and programme for the

establishment; · (e) names and particulars, including cuniculwn vi~e for persons

proposed to take up s~nior positions; and (f) any other information 'the Bank may require.

Activities of a subsidiary.

32. A subsidiary of licensed institution shall not activities other than those'permitted by Section 24 ofthe Act.

Representative office

Powers.ofa licensed institution

Cap. 212

Relationship with foreign banks

Management igreements ·

FiducilU)' fimctions

Additionai activities

33.:-(l) A foreign bank or fmancial institution shall not op n . representative office in Tanzania without prior approval of the Bank d= where approval has been granted; such representative office shall no· conduct banking b~iness or finaiicial intermediation. · . '

(2) .An application for establishment of a representative offic ir.: Tanzania shall include a detailed budget for.the office,_ ·curriculum itae: for the· pr9posed officers and staff and other information as may "f?e' required.by the Bank.

PART VII SCOPE OF AUTHOIUTY FOR LICENSED INSTITUTIONS

34. A licensed institution shall have all such powers necessary to carry out the permitted activities specified in section 24 of the . Act, in additiop. to the general powers vested in companies incorporated under t e Companies Act.

. 35. A _licensed institution shall not establish a relationship wifh any correspondent bank or financial institution abroad without pri~r approval of the Bank.

. 36. A management or technical assistance agreement involving licensed institution shall be. subject to prior approval of the Bank an go-yerned by the laws ofTanzania.

37. A licence institution with a core capital of not tess than twen two billion five ·hundred million shillings may be authorized by the· B to. perform· duties and · functi~ns of a trustee and such other fiduci functions as the Bank may authorize.

38 .• -(1) A licensed institution with a core capital of not less than thirty bimo~ shillings may be authorized by the Bank to-

( a} acquire up to one hundred per yent of the equity ofa company organized primarily for the purpose of underwriting debt or equity secUrities of other companies;

(b) acquire majority or all of the equity of a bank or 'financial institution; ·

(c) inves~ in .the equity of a company which is engaged in activities that are not allied o.r not related to bankirig; Provided ~t the equity investment of the bank shall not ex~eed five percent of the total subscribed share . capital of the investee company

11

Acquisition of a company . . engage<! in allkd undertakings

lnvestm,e11t in ~ com,pany · engaged in a!Jied undertal,<ings

Establishment of foreign b11\llch or subsidiary

Segregation of assets

(2) Wh~x:e a licensed institution intends to deal in securities, it· shaH fo.rm a subsidiary for such purpose.

39 .. A licensed institution with a core capital. between fifteen billion $billings and thirty billion shillings may, with the prior approval of the Bank acquire up to one hundred per· cent ofthe total subscribed share capital of the company engaged in activities classified as allied undertC!.kings.

_,

40. A lic~nsed Institutions with a core capit~ ranging fr<~m ten · billion shillings to iess thm fifteen· billion shillfugs may, w.lth the priQJ,". approval of the Bank, invest in the eq~ity of co[Ilpanies engaged in activities classified as allied unde.rtakings sU:l;>ject to the limits provided in the Banking and Financial Institutions (Credit Concentration a,nd Other Exposure Limits) Regulations, 2008. ·

41. A licensed institutions with '!. core capital of not less than fifty billion shillings may be authorized by the Bal;l,k to establish a l;)rqn,ch or a subsidiary ~broad.

42. A licerised institution author.ized by the Bank to act as an agent shall account .for and keep money, se~urities and other valliables, which it has received in such capacity d:uly separated from it~ own. assets and liabilities. ·

PAA'TVIII MISCELLANEOUS.PROVISIONS

Sanctions penalties·

~d 43. Without prejudice to the other penalties and actions prescribed by the Act, the Bank mcty impose one or more of the following sanctions where any ofth¢se provisions are contravened- ·

(a) penaltY 6n the licepsed institution or directors, officers or

(b) (c)

. (d) (e). (f) (g) {h)

(i)

(j)

employees responsible for non-:compliance in such amounts as ma_y be determ1ned by .the :$~; prohibition from declaring or paying dividends; ~uspension of the priviiege to issue letters of credit or guar~Wtee;

suspenSion of access to the c1-edit facilities of the Bank; suspension oflellding and investment operations; suspension of capital expenditur-e; susp~nsion of the privil~e to accept new deposits; suspension from office of the defaulting drrector, officer. or employee; di$qua1ification from holding any position or office in any licen.S,ed or financ#l institution in Tanzania; and. revocation of banking liccnct;:.

12

Revocation GN. No. I !8 ofl997

G) revocation of banking licence.

44. The Banking and Financial Institutions Regulations, 1997 are hereby revoked.

FIRST SCHEDULE

(Made under Regulation 7)

CRITERIA FOR DETERMINING THE CHARACTER AND EXPERIENCE REQUIRED FOR. A MEMBER OF THE BOARD OF DIRECTORS AND SENIOR MANAGEME}l"T OF BANK OR

FINANCIAL INSTITUTION

1. In order to determine, for the purpose of these Regulations, the character and moral suitability of persons proposed to be members of the Board or senior management, the B<_tnk shall have regard to the following qualities, in so far as they are. reasonably determinable, ofthe person concerned-

( a) adequate education background; (b) general character; (c) professional skills, competence and soundness of judgment for the

fulfilment of the responsibilities ofthe office in question; and (d) the diligence with which the person concerned is likely to fulfil those

responsibilities. 2. For the purpose of and without prejudice to the generality of the provisions of

paragraph (1), the Bank may have regard to the previous conduct and activities of the person concerned in the business or financial matters and, in particular to evidence that such person-

( a) (b)

(c)

(d)

(e)

has committed any act ofb~ptcy; was a director or in a senior management position of a bank or financial

institution that has been liquidated or is und~r liquidation or statutory management; has COIJJ.mitted or been convicted of the offence of fraud or any other

offence of which dishonesty is an element; has contravened the provision of any law designated for the protection of

members of the public against financial loss due to the dishonesty or incompetence of, or malpractices by, persons engaged in the provision of banking, insurance, investment or other fmancial services; any other criteria, which the Ba.nl< may prescribe; from time to time.

4. The following documents shall be submitted to the Bank with respect to each proposed director and senior management team, together with other documents the Bank may require

( a) (b) (c)

(d) (e)

detailed curriculum vitae; certified copies of academic and professional certificates; photocopy of the pages of the pru1sport which contain personal information including photograph, nationality, date and place of birth and issuer of the passport; two certified passport size photographs; and references from two persons who are not relatives, vouching for good moral character, integrity and performance.

13

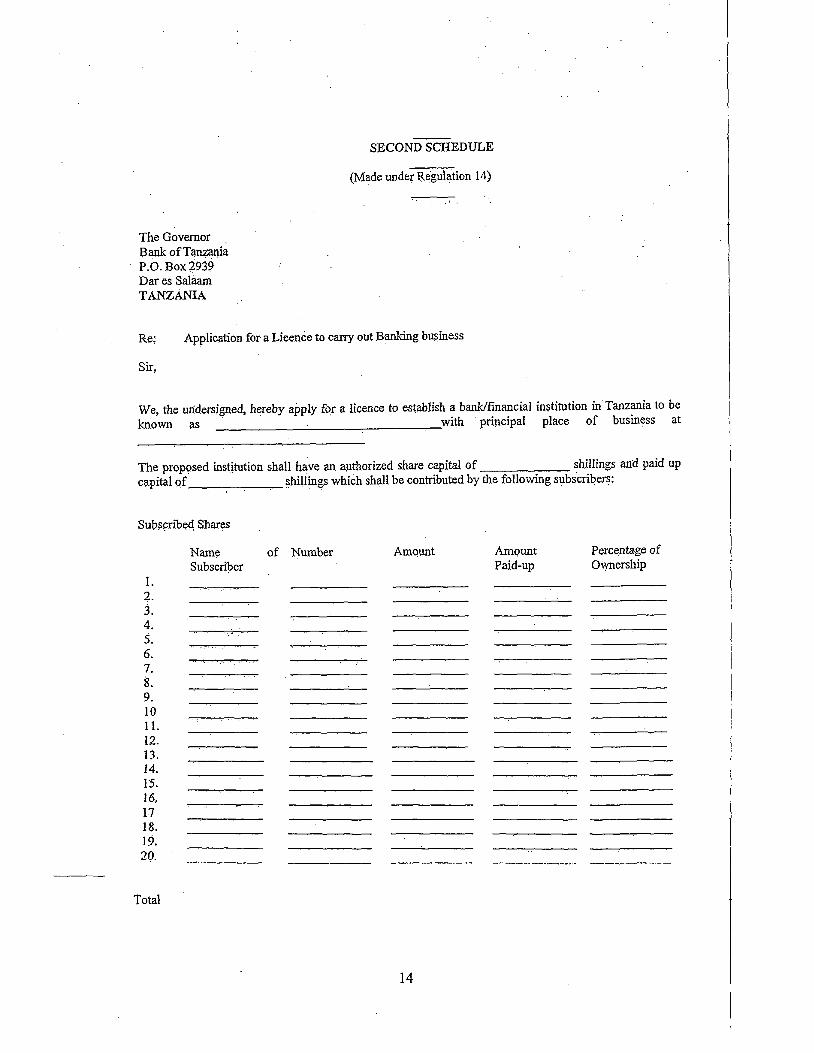

The Governor Bank ofTa~ania P.O. Box ~939 Dar es Salaam TANZANIA

SECOND SCHEDULE

(Made under Regulation 14)

Re: Application for a Licence to carry out Banking business

Sir,

We, the undersigned, hereby apply for a licence to establish a bank/financial in~titution in Tanzania to be known as · with principal place of business at

The proposed institution shall have an a~thorized share capital of shillings and paid up capital ()f ~hili~~ which shall be contributed by the following subscribers:

Subs~ribeq Shares

1. 4. 3. 4; 5. 6. 7. 8. 9. 10 11. 12. 13. 14. 15. 16.. 17 18. 19. 20.

Total

Name Subscriber

of Number Amount

14

Amount Paid-up

Percentage of Ownership.

We jointly and severally make a fmn conunitment to deposit a total amount of paid up capital for the

proposed institution with any bank registered in Tanzania such deposit to be made n.ot later than thirty da)IS after grant of this ap~lication.

In support ofthis application, we submit herewith the documents listed in the accompanying checklist. We certify the correctness of all the information indicated in such documents to the best of our knowledge and belief.

We hereby authorize the Bank of Tanzania and any of its authorized ag~nts or staff members to make an enquiry or obtain any information from any source for the purpose or' determining the correctness of all the representations made in connection.with this application or of assessing its merits.

To facilitate communication between us, we have authorized ................. ;. to represent all ofus in: regard to this application. It is understood th~t any notice to him shall constitute sufficient notice to all of us.

Enclosed is a cheque for three million shillings being payment of our application fee.

Yours faithfully,

15

THIRD SCH]!;DULE

(Made underRegulatiop. 15)

Checkiist of Documents

I. Letter of appli~ation in the pr~scribed form.

2. Proposed Memorandum and Articles of Association.

3. Proof of source and availability of funds for inves.tment as capital of the proposed institution.

4. List of subscripers and proposed members of board of directors and Chief Executive Officer.

5. Proof of citi~ep,ship of every. ~ubscriber an<;! every proposed director and senior management officer. This includes.detaiied currk:uhim vita,e, photocopy of the pag~~ of the passport which contain personal information and two recent passport ~iz~ photographs. · ·

6. Audited balance sheet, inc;:ome stitement and cash flpw for the last three years, of every subscriber who owns five per ~ent or rp.qre of the share capital of the proposed institution engaged in business

7. Certified copies of annual returns of every subscriber who owns five per cent or more of the share capital of the proposed institution and every proposed member <;>f the board of directors and Chief Executive Officer together with accompanying·schedules or fmancial statements filed duri,ng the last three years with relevant Authority.

8. Certified copies of tax returns cif every subscriber who owns five per cent or more of the share capital of the proposed institution and every proposed member of the board of directors and Chief Executive Officer together with accompanying schedules or financial statements filed di.rring the last three years with relevant Tax authorities iogether with respective Tax clearance -c~rtificates.

9. Statements J;Tom two persons who are not relatives vouching for the good moral character and financial responsibility of the subscribers who owns five per cent or more of the share capital of the propo.sed iruititution anc:l the proposed directors and Chief Executive Officer.

10. Home Col.llltry Regulator Certification if the applicant is a foreign bank or financial institution.

11. Declaration that the fu11cis to be invested have not been obtained criminally or associated with any criminal activity:·

12. Business plans for the first four years qf operations including the strategy for growth, branch expansion plans, dividend payout policy, career development progranune for the staff and budget for the first year. . · .

13. Projected annual balance sheets, projected annual income statements and projected annual cash flow statements for the first four years of operation,

14~ Brief description of economic benefits to be derived by Tanzania and the community from the proposed banl<: or fmancial institution.

16

FOURTH SCHEDULE

(Made under Regulation 12)

General guidelines ~or preparation of Business plan

l. The business plan should be prepared by the promoters and will be reviewed by the Bank to determine whether approval should be given to ·operate a bank or fmancial institution. The plan should identify the institution's markets, its proposed services, management capabilities, growth plan, and strategies for profitability. ·

2. The business plan should present data, which accurately reflect the economic condition of the delineated market and address statutory and regulatory changes, which may affect the operations of the proposed bank or financial institution. Proposal should reflect the realities of the market place.

3. A business plan should contain sufficient information to demonstrate that the proposed bank or financial institution has reasonable likelihood of success. In this regard a detailed listing of all assumptions such as used in preparing the· business plan should be attached to the submission (e.g. a margin analysis and cost of funds). Therefore, organizers must ensure that the business plan projections are well supported and goals and objectives are properly defmed -on initial submission.

Market Analysis

4. Analyse the market to be served. Describ.e the market in which you expect to provide services in terms of economic characteristics for example size, income and industry patterns. Include anticipated changes in the market, the factors influencing those changes, and the effect they will have on the proposed institution. to the extent necessary for making business decision, describe differences in the product market to be served for example, differences in the depository and credit market. Analysis will be base.d on use of the most current economic data available. Sources of information used are reviewed for credibility and are important in reviewing the data.

5. Ana,lyse the competition. List the competitors inside the market to be served, those outSide who might affect the markets served and any potential competition. Give your perception and analysis ofthe market st:r;ategies and expected results in terms of relative strength, market shares and prices.

6. Explain. the strategies you wiii foiiow to capture a share of each product market and the results ~ou expect to achieve. Use a sample format to present a summary ofyoqr expectations.

Plans and Objectives

7. Review major planning assumptions used in the analysis and in setting the plans and objectives for a new institution. Tndudt' at least the following mC~rket growth, intere::~l ruLe::~, co~l of funds and

competition.

8. Projections should show the expected asset and liahilily mix, volume for each type of services, fixed asset investments and officer and staff remuneration. Projections must be based on the planning assumptions which must be submitted as part of the application, m!U'ket analysis, aud strategies discussed above. Discuss the advantages and disadvantages of the proposed asset/liabilities mix, including a net interest margin analysis, and any actions whiCh will be taken to reduce major risks through appropriate finids management techniques and systems.

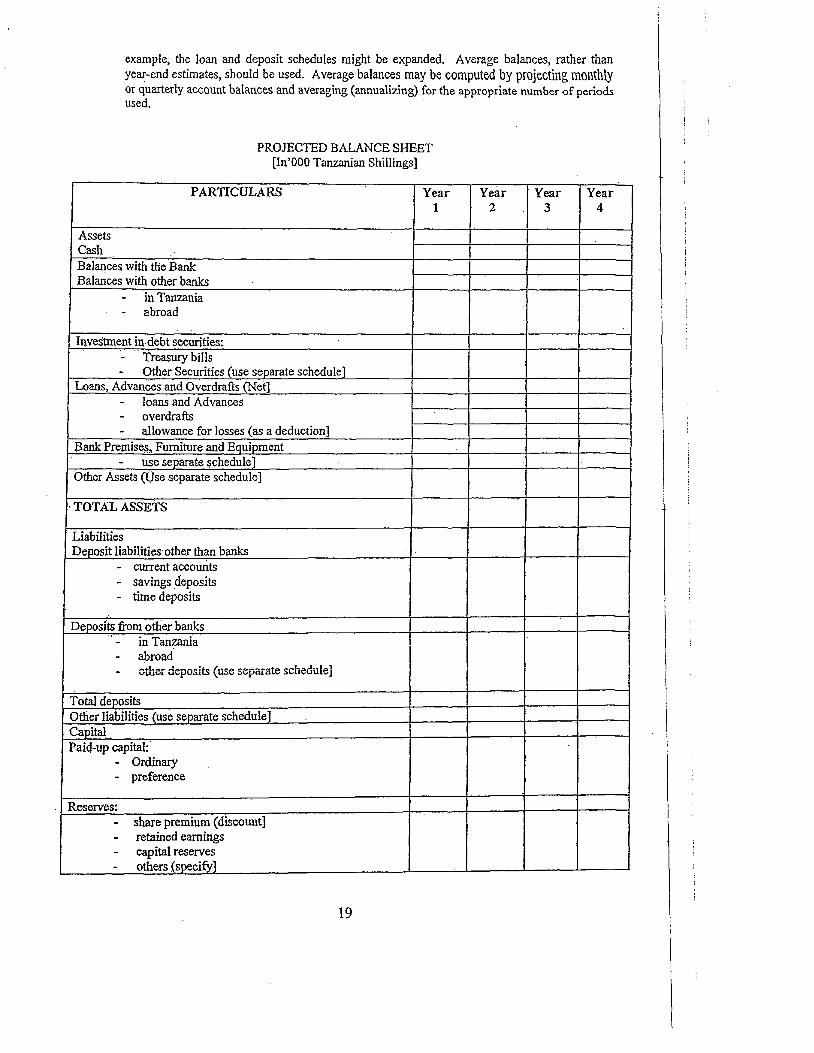

17

9. Discuss the fonnula or basis used to arrive at the proposed capital structure and an explanation of why the promoters believe the proposed <miOUnt is sufficient in light of given market factors, strategies, and expenses. Promoters are expected to raise an amount sufficient to effectively compete in the market are and adequately support planned operations ~n addition to all organizational expenses. The Bank may require a higher amoljnt to maintain capital adequacy to support operations projected through the end ofthe institution's fourth year.

10. Discuss ·pl;;tns for raisipg capital initially e;md to financ\? groWI:h wiFl;lin th~ first four yea,rs. Explain how the plans willk~ep the institution in cqnfor$ity wjth th~ Bank's C;:tpit~l Adequacy Regulations, 2001 specifically addressing compliance with the r~sk-bas~d capital guidelines.

. . . '. . . . '

Credit Policy apd Procequres