BOS Session 8-Revsd

40

Confidential Innovative Competitive Strategy: Blue Ocean Strategy Adapted from the work of BOS by Chan Kim Sept 04, 2012

-

Upload

ankush-rawat -

Category

Documents

-

view

213 -

download

0

Transcript of BOS Session 8-Revsd

8/22/2019 BOS Session 8-Revsd

http://slidepdf.com/reader/full/bos-session-8-revsd 1/40

Confidential

Innovative Competitive Strategy:Blue Ocean Strategy

Adapted from the work of BOS by Chan Kim

Sept 04, 2012

8/22/2019 BOS Session 8-Revsd

http://slidepdf.com/reader/full/bos-session-8-revsd 2/40

Confidential

Fundamental Premise

“Don’t Compete with Rivals – Make Them Irrelevant”

8/22/2019 BOS Session 8-Revsd

http://slidepdf.com/reader/full/bos-session-8-revsd 3/40

Confidential

Red Oceans

Represent all industries in existence today

Industry boundaries are defined and accepted

Companies try to outperform each other to gain

market share The market space becomes crowded and the

products become commoditized

Prospects for profit and growth are reduced

Competition turns the red ocean bloody

8/22/2019 BOS Session 8-Revsd

http://slidepdf.com/reader/full/bos-session-8-revsd 4/40

Confidential

Blue Oceans

Defined by untapped market space, demandcreation, and high-profit growth potential

Some are new industries, but most are created fromwithin red oceans by expanding existing industry

boundaries or competing with a fundamentallydifferent strategy

8/22/2019 BOS Session 8-Revsd

http://slidepdf.com/reader/full/bos-session-8-revsd 5/40

Confidential

Examples

CNN in 1980 with 24/7 news coverage

Starbucks with upscale coffee/beverages in a

pleasant environment

Southwest airlines with a “better than driving” sortof strategy

Some Indian companies are relentlessly trying to doa BO post recession

8/22/2019 BOS Session 8-Revsd

http://slidepdf.com/reader/full/bos-session-8-revsd 6/40

Confidential

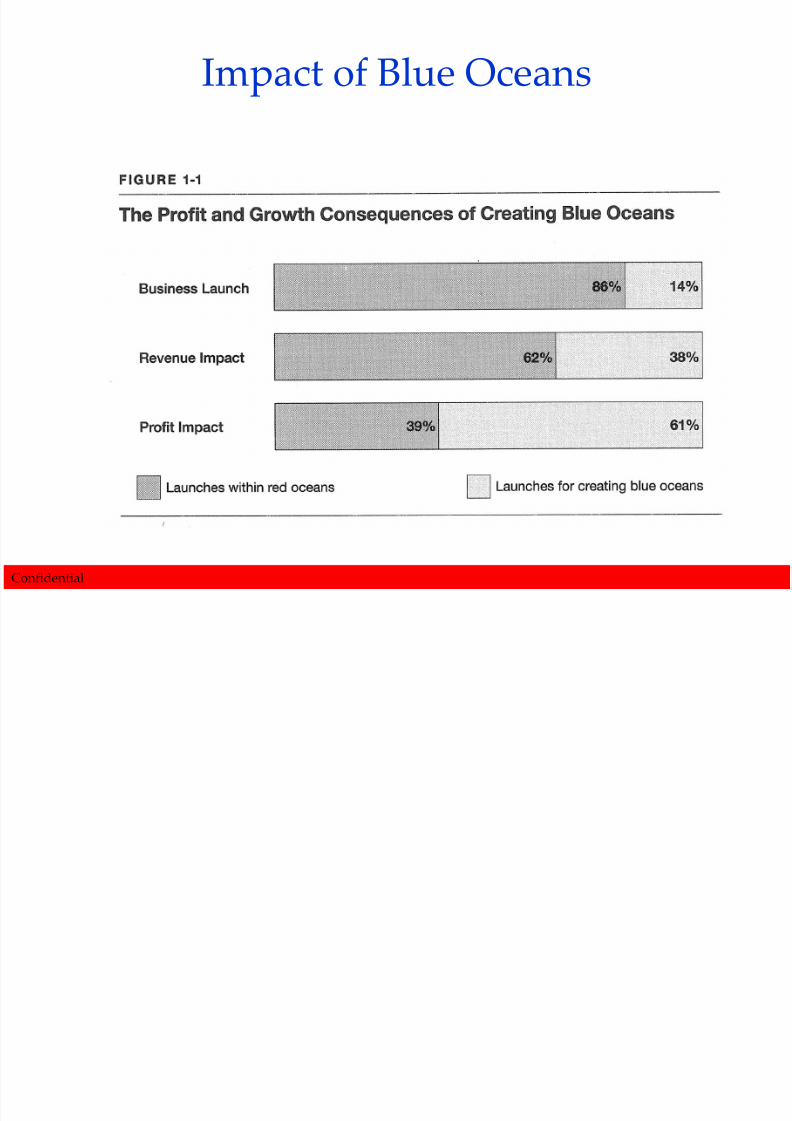

Impact of Blue Oceans

8/22/2019 BOS Session 8-Revsd

http://slidepdf.com/reader/full/bos-session-8-revsd 7/40Confidential

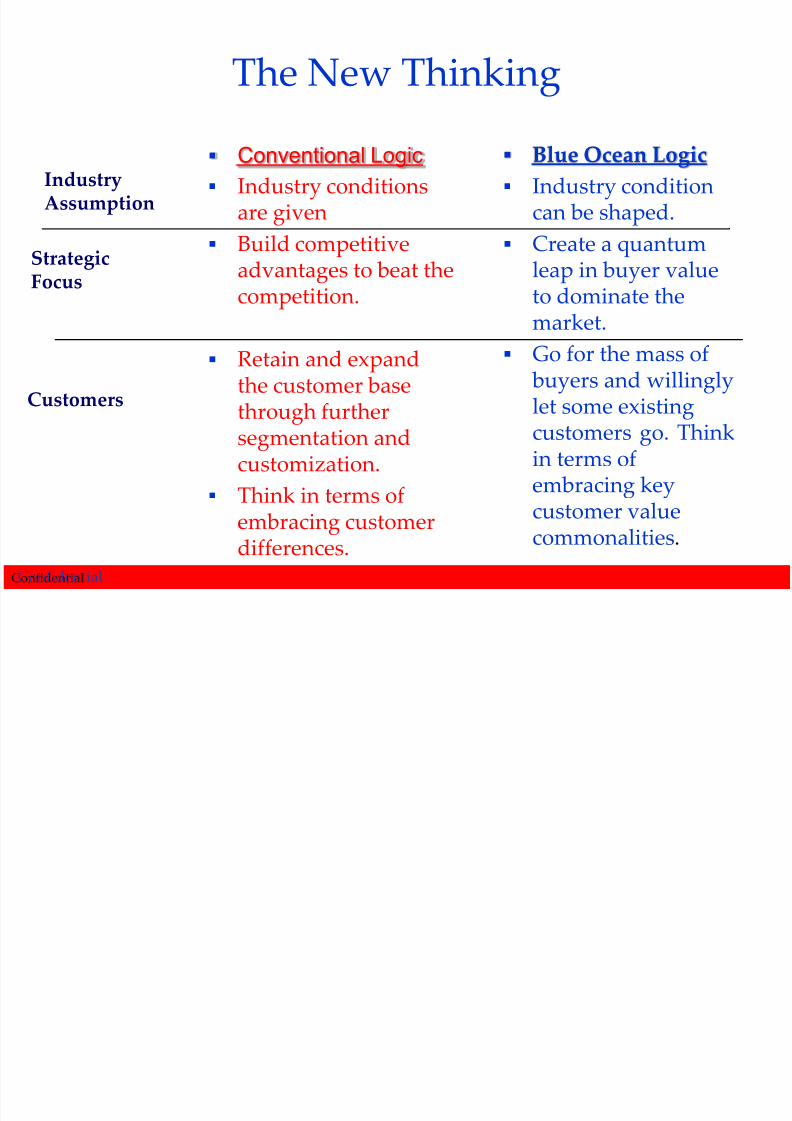

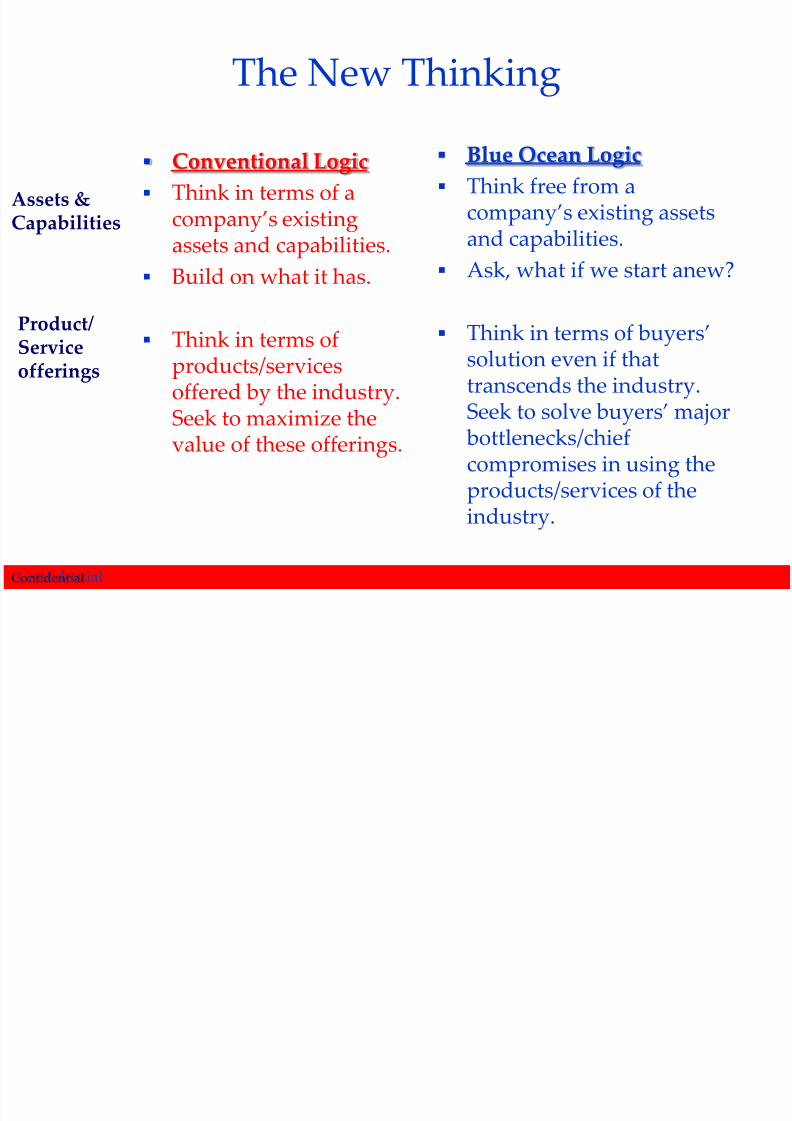

The New Thinking

Conventional Logic

Industry conditionsare given

Build competitive

advantages to beat thecompetition.

Retain and expandthe customer base

through furthersegmentation andcustomization.

Think in terms ofembracing customer

differences.

Blue Ocean Logic

Industry conditioncan be shaped.

Create a quantum

leap in buyer valueto dominate themarket.

Go for the mass of buyers and willingly

let some existingcustomers go. Thinkin terms ofembracing keycustomer valuecommonalities.

Confidential

IndustryAssumption

Strategic

Focus

Customers

8/22/2019 BOS Session 8-Revsd

http://slidepdf.com/reader/full/bos-session-8-revsd 8/40Confidential

The New Thinking

Conventional Logic

Think in terms of acompany’s existingassets and capabilities.

Build on what it has.

Think in terms ofproducts/servicesoffered by the industry.

Seek to maximize thevalue of these offerings.

Blue Ocean Logic

Think free from acompany’s existing assetsand capabilities.

Ask, what if we start anew?

Think in terms of buyers’solution even if thattranscends the industry.

Seek to solve buyers’ major bottlenecks/chiefcompromises in using theproducts/services of theindustry.

Confidential

Assets &Capabilities

Product/ Serviceofferings

8/22/2019 BOS Session 8-Revsd

http://slidepdf.com/reader/full/bos-session-8-revsd 9/40ConfidentialConfidential

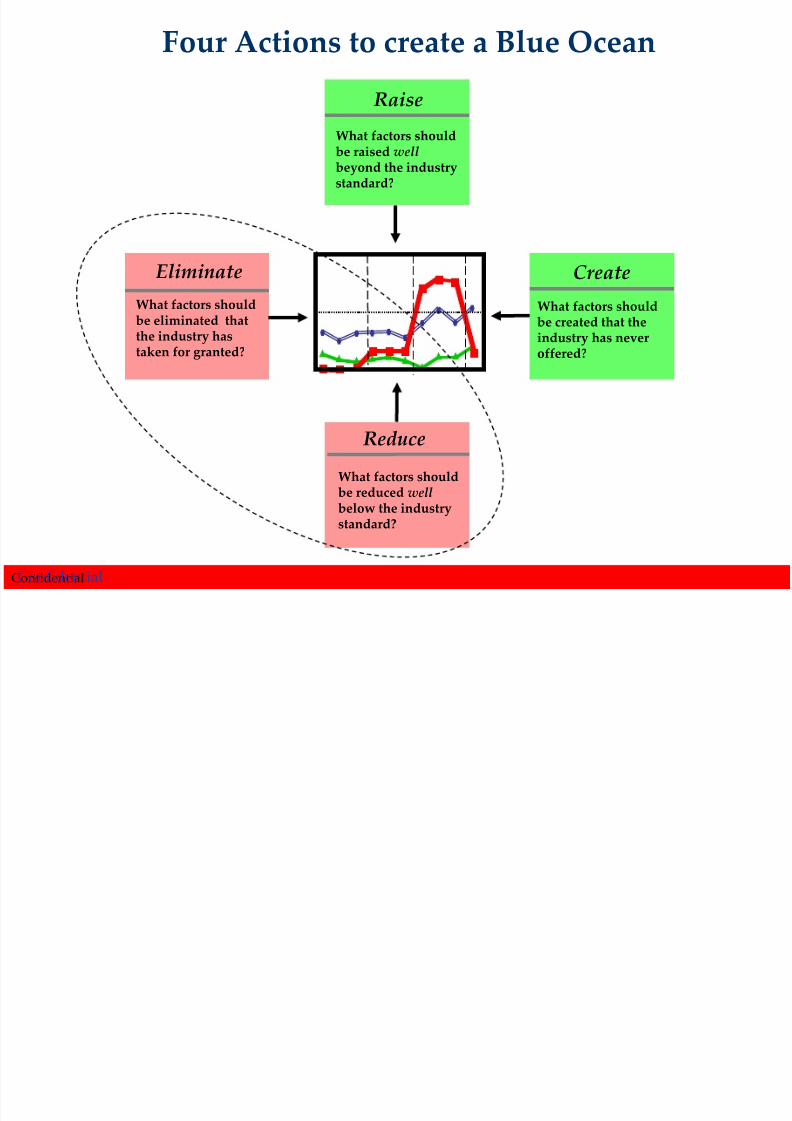

What factors shouldbe raised wellbeyond the industrystandard?

Raise

What factors shouldbe eliminated thatthe industry hastaken for granted?

EliminateWhat factors shouldbe created that theindustry has neveroffered?

Create

What factors shouldbe reduced wellbelow the industrystandard?

Reduce

Four Actions to create a Blue Ocean

8/22/2019 BOS Session 8-Revsd

http://slidepdf.com/reader/full/bos-session-8-revsd 10/40Confidential10

Example: A highly competitive Industry

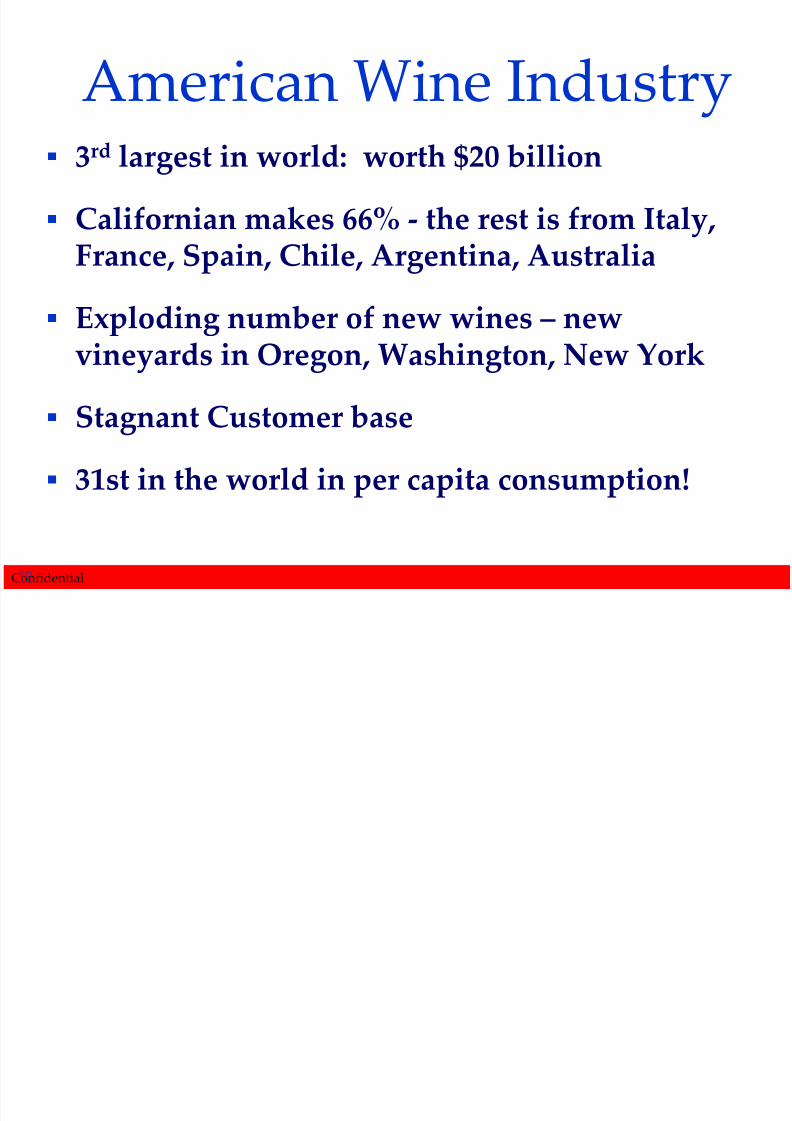

The American Wine Industry

8/22/2019 BOS Session 8-Revsd

http://slidepdf.com/reader/full/bos-session-8-revsd 11/40Confidential11

What the industry offers

Premium Wines Budget Wines

Massive Choice

8/22/2019 BOS Session 8-Revsd

http://slidepdf.com/reader/full/bos-session-8-revsd 12/40Confidential12

American Wine Industry 3rd largest in world: worth $20 billion

Californian makes 66% - the rest is from Italy,France, Spain, Chile, Argentina, Australia

Exploding number of new wines – newvineyards in Oregon, Washington, New York

Stagnant Customer base

31st in the world in per capita consumption!

8/22/2019 BOS Session 8-Revsd

http://slidepdf.com/reader/full/bos-session-8-revsd 13/40Confidential13

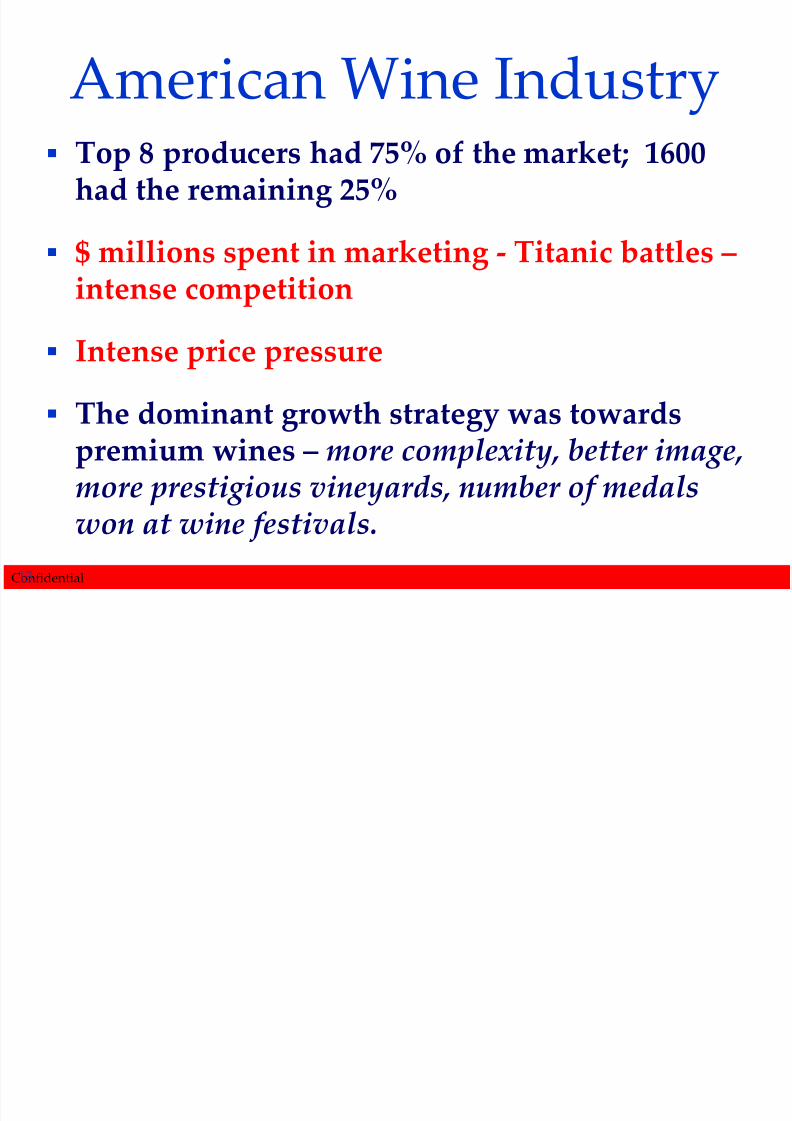

American Wine Industry Top 8 producers had 75% of the market; 1600

had the remaining 25%

$ millions spent in marketing - Titanic battles – intense competition

Intense price pressure

The dominant growth strategy was towardspremium wines – more complexity, better image,more prestigious vineyards, number of medalswon at wine festivals.

8/22/2019 BOS Session 8-Revsd

http://slidepdf.com/reader/full/bos-session-8-revsd 14/40Confidential14

Very high

O f f e r i n g L e v e l v e r s u

s W i n e

D r

i n k e r s ’ E x p e c t a t i o

n s

High

Normal

Low

Very low

Non-

existent

Premium and Budget Wines

8/22/2019 BOS Session 8-Revsd

http://slidepdf.com/reader/full/bos-session-8-revsd 15/40Confidential15

What people said … ‚It is too confusing and complex‛

Wine descriptions and terminology

The shopping experience

The lack of clear guidance on what to buy anddrink

Thus, massively intimidating for‘noncustomers’ (the large majority of the USpopulation who were not wine drinkers)

8/22/2019 BOS Session 8-Revsd

http://slidepdf.com/reader/full/bos-session-8-revsd 16/40Confidential

16

Yellow Tail created a BlueOcean

Premium Budget

Creatinga Blue Ocean

Australia, a major wine exporter was making bid toenter the US market

8/22/2019 BOS Session 8-Revsd

http://slidepdf.com/reader/full/bos-session-8-revsd 17/40Confidential17

Yellow Tail Only 2 types initially – Chardonnay and Shiraz

Fruity, soft on palette, sweet-ish – great for those who hadnot drunk wine before

Same bottle for red and white – low logistics costs Simple vibrant packaging – lower case letters/kangaroo

Un-intimidating

They were selling ‚The essence of a great land …

Australia‛ – ie they were not selling the wine

Retail staff – they enthusiastically promoted a wine theycould understand.

8/22/2019 BOS Session 8-Revsd

http://slidepdf.com/reader/full/bos-session-8-revsd 18/40Confidential18

Yellow Tail Strategy Eliminated: Diffiult terminology and distinctions, Aging

qualities, Above the line marketing

Reduced: Wine complexity, Wine range, Vineyardprestige

Raised: Price versus Budget Wines, Simplicity of retailstore environment, Enthusiasm of Sales People

Created: Easy drinking, Ease of selection, Sense of funand adventure

8/22/2019 BOS Session 8-Revsd

http://slidepdf.com/reader/full/bos-session-8-revsd 19/40Confidential19

Very high

High

Normal

Low

Very low

Non-existent

Yellow Tail Value Curve‚The Essence of a Great Land‛

8/22/2019 BOS Session 8-Revsd

http://slidepdf.com/reader/full/bos-session-8-revsd 20/40Confidential20

Results No 1 imported wine in the US (outsells France and Italy)

Fastest growing imported wine in the history of the USAindustry

New consumers of wine

Jug drinkers trade up (Low cost drinkers)

Premium wine drinkers trade down

Industry criticizes them mercilessly at first

Now wine press blurb gives it a ‚best buy‛ for value;winning wine awards.

8/22/2019 BOS Session 8-Revsd

http://slidepdf.com/reader/full/bos-session-8-revsd 21/40Confidential

BO creates a new world...

Red Ocean Strategy Blue Ocean Strategy

Compete in existing market

space.

Create uncontested market

space.

Beat the competition. Make the competition irrelevant.

Exploit existing demand. Create and capture new demand.

Make the value-cost trade-off. Break the value-cost trade-off.

Align the whole system of a

strategic firm's activities with its

choice of differentiation or lowcost.

Align the whole system of a firm's

activities in pursuit of

differentiation and low cost.

VALUE INNOVATION

8/22/2019 BOS Session 8-Revsd

http://slidepdf.com/reader/full/bos-session-8-revsd 22/40

Confidential

How to Create Blue Oceans

• Most academia focuses on competing in the bloodyred oceans

•

The real thing is value innovation – Leap in value for buyers leading to uncontested market space

– Pursue differentiation and low cost simultaneously (a HybridStrategy of Porter)

• STRATEGY that is key

8/22/2019 BOS Session 8-Revsd

http://slidepdf.com/reader/full/bos-session-8-revsd 23/40

Confidential

Some Indian Examples who havemoved into uncontested spaces

Symphony Air Coolers

MOOV

Bausch & Lomb Color Lenses

Nano?? Bacardi – Breezers

Ramoji Film City

Online Discounted Luxury Stores

Confidential

8/22/2019 BOS Session 8-Revsd

http://slidepdf.com/reader/full/bos-session-8-revsd 24/40

Confidential

An Unlikely ExampleNYPD – New York Police Dept.

80’s NY the crime capital

Demoralized police force

Political interference

Meager resources

Disgusted citizens

New chief makes 180° turn on the state of affairs

Changes the face of NYP

Within 3 years makes NY the safest city in the US

– An extreme example of Blue Ocean Strategy at work

Confidential

8/22/2019 BOS Session 8-Revsd

http://slidepdf.com/reader/full/bos-session-8-revsd 25/40

Confidential

BOS Logic: The Core Principles

Reconstruct Market Boundaries… overcome beliefs.

Reach beyond existing Demand… go for uncontested

space.

Get the strategic sequence right … value

[innovation] first.

Focus on the Big Picture, Not the Numbers … be

creative

Overcome Key Organizational Hurdle Build Execution into Strategy

Confidential

8/22/2019 BOS Session 8-Revsd

http://slidepdf.com/reader/full/bos-session-8-revsd 26/40

Confidential

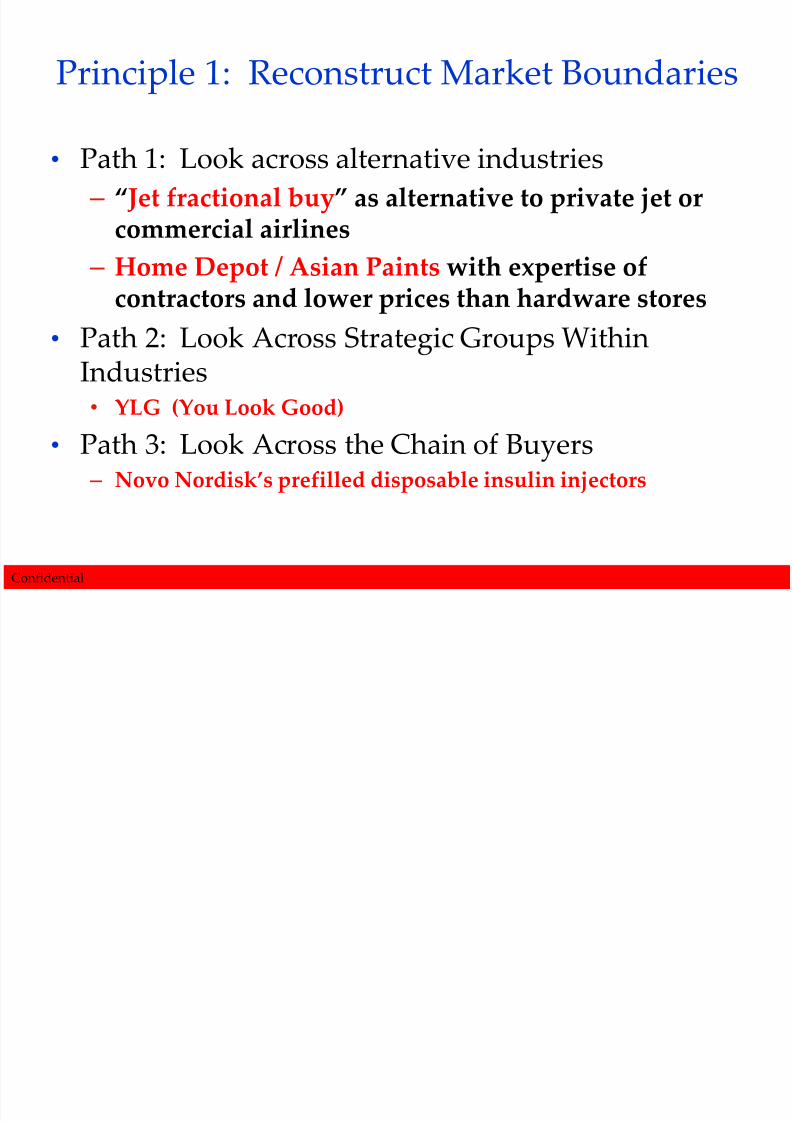

Principle 1: Reconstruct Market Boundaries

• Path 1: Look across alternative industries

– ‚Jet fractional buy‛ as alternative to private jet orcommercial airlines

–

Home Depot / Asian Paints with expertise ofcontractors and lower prices than hardware stores

• Path 2: Look Across Strategic Groups WithinIndustries•

YLG (You Look Good)• Path 3: Look Across the Chain of Buyers

– Novo Nordisk’s prefilled disposable insulin injectors

8/22/2019 BOS Session 8-Revsd

http://slidepdf.com/reader/full/bos-session-8-revsd 27/40

Confidential

Principle 1: Reconstruct Market Boundaries(Cont.)

• Path 4: Look Across Complementary Productand Service Offerings – Toyota (competing on lifecycle cost, not purchase price)

•

Path 5: Look Across Functional or EmotionalAppeal to Buyers – Swatch transformed functionally driven budget watch

industry into an emotionally driven fashion statement

•

Path 6: Look Across Time (finding actionableinsights on observable trends) – iTunes leaping past pirated downloads

8/22/2019 BOS Session 8-Revsd

http://slidepdf.com/reader/full/bos-session-8-revsd 28/40

Confidential

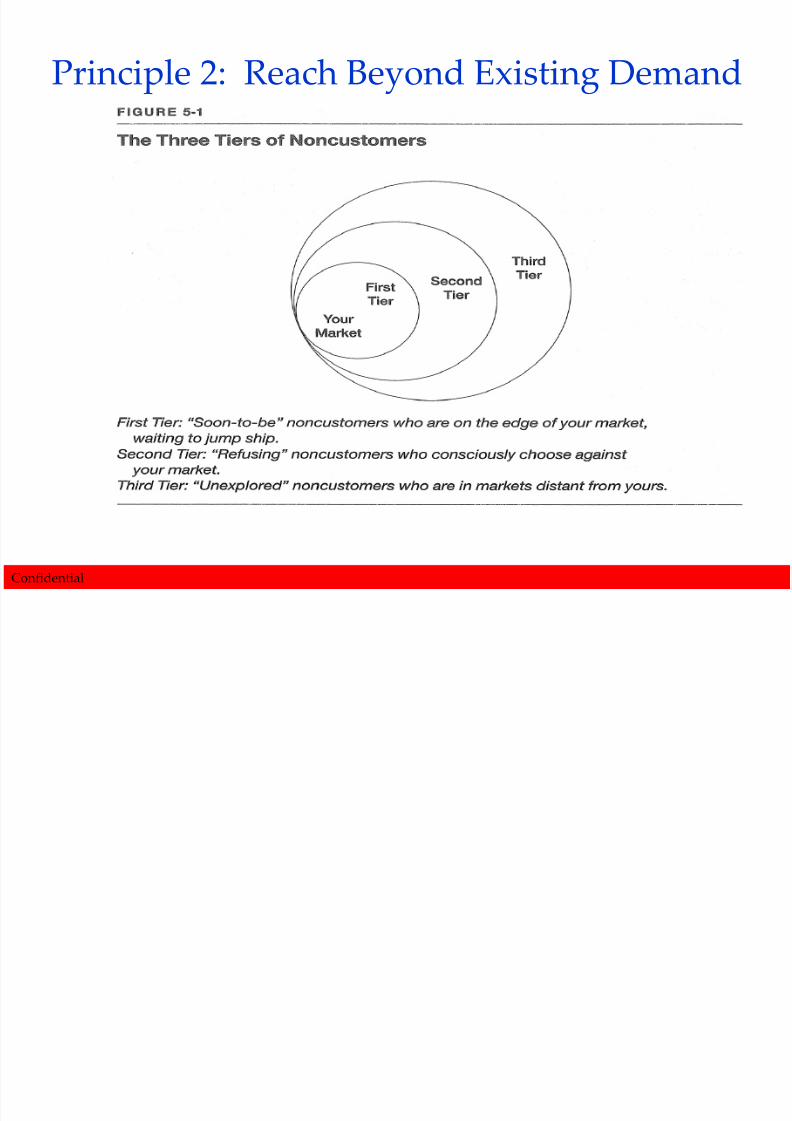

Principle 2: Reach Beyond Existing Demand

P i i l 3 G t th St t i S i ht

8/22/2019 BOS Session 8-Revsd

http://slidepdf.com/reader/full/bos-session-8-revsd 29/40

Confidential

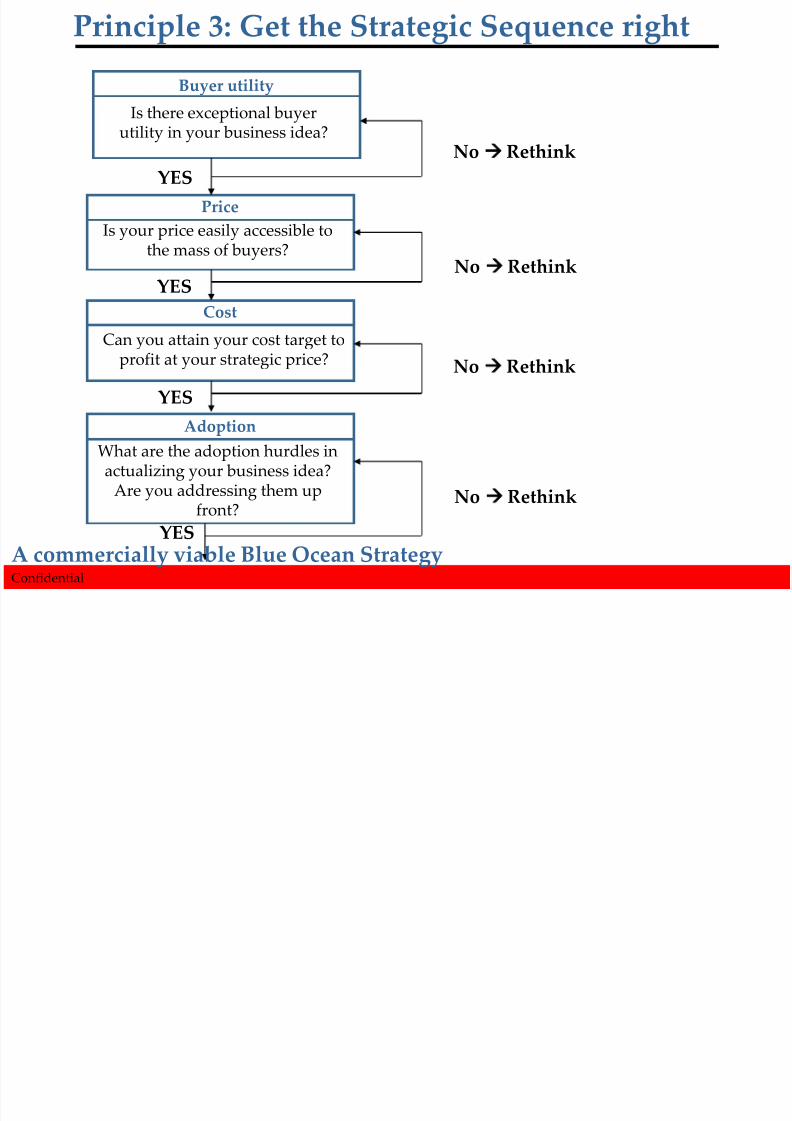

Principle 3: Get the Strategic Sequence right

Buyer utility

Is there exceptional buyerutility in your business idea?

Adoption

What are the adoption hurdles inactualizing your business idea?

Are you addressing them upfront?

Price

Is your price easily accessible tothe mass of buyers?

Cost

Can you attain your cost target toprofit at your strategic price?

A commercially viable Blue Ocean Strategy

YES

YES

YES

YES

No Rethink

No Rethink

No Rethink

No Rethink

8/22/2019 BOS Session 8-Revsd

http://slidepdf.com/reader/full/bos-session-8-revsd 30/40

Confidential

Principle 4: Focus on the Big Picture, Notthe Numbers

8/22/2019 BOS Session 8-Revsd

http://slidepdf.com/reader/full/bos-session-8-revsd 31/40

Confidential

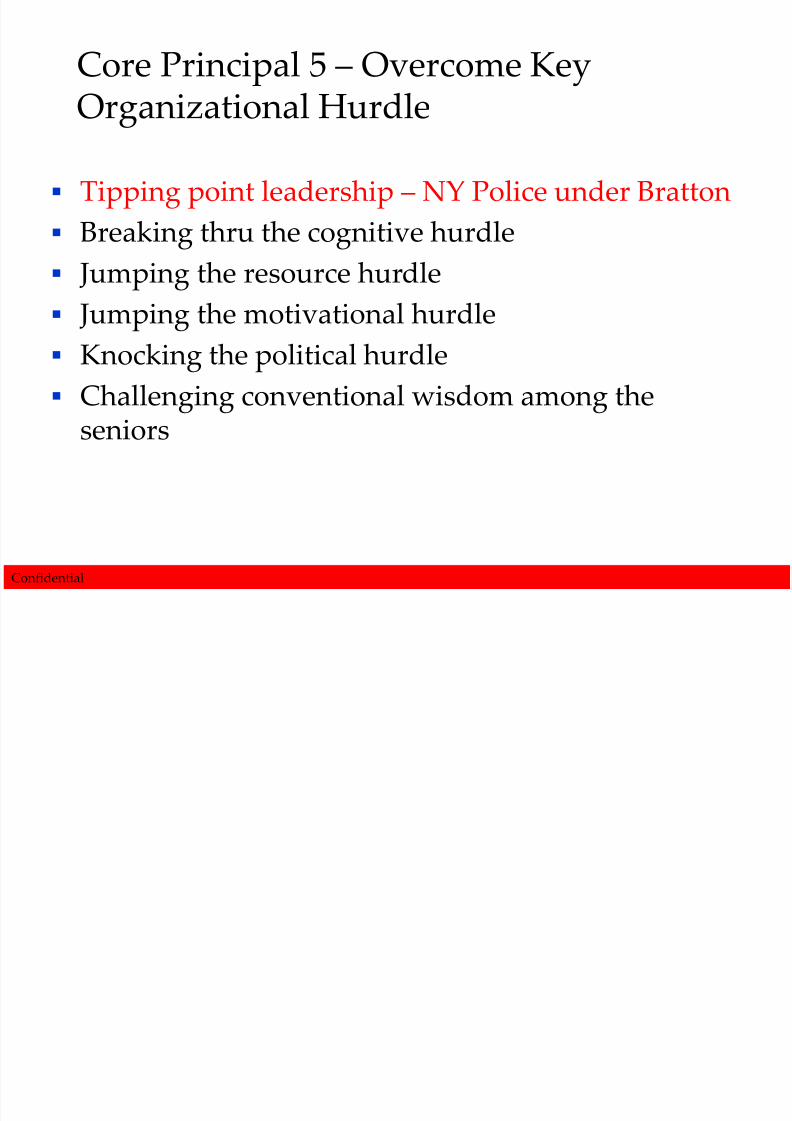

Core Principal 5 – Overcome KeyOrganizational Hurdle

Tipping point leadership – NY Police under Bratton

Breaking thru the cognitive hurdle

Jumping the resource hurdle Jumping the motivational hurdle

Knocking the political hurdle

Challenging conventional wisdom among theseniors

8/22/2019 BOS Session 8-Revsd

http://slidepdf.com/reader/full/bos-session-8-revsd 32/40

Confidential

Principle 6 - Build Execution intoStrategy

Poor processes can ruin a brilliant strategy (RFC)

Execution is key by Dr. Ramacharan

8/22/2019 BOS Session 8-Revsd

http://slidepdf.com/reader/full/bos-session-8-revsd 33/40

Confidential

How innovative companies break freefrom the pack to a new market space

Value Innovation approach vs. Conventionalapproach to strategy

Price corridor of the mass

Confidential

8/22/2019 BOS Session 8-Revsd

http://slidepdf.com/reader/full/bos-session-8-revsd 34/40

Confidential

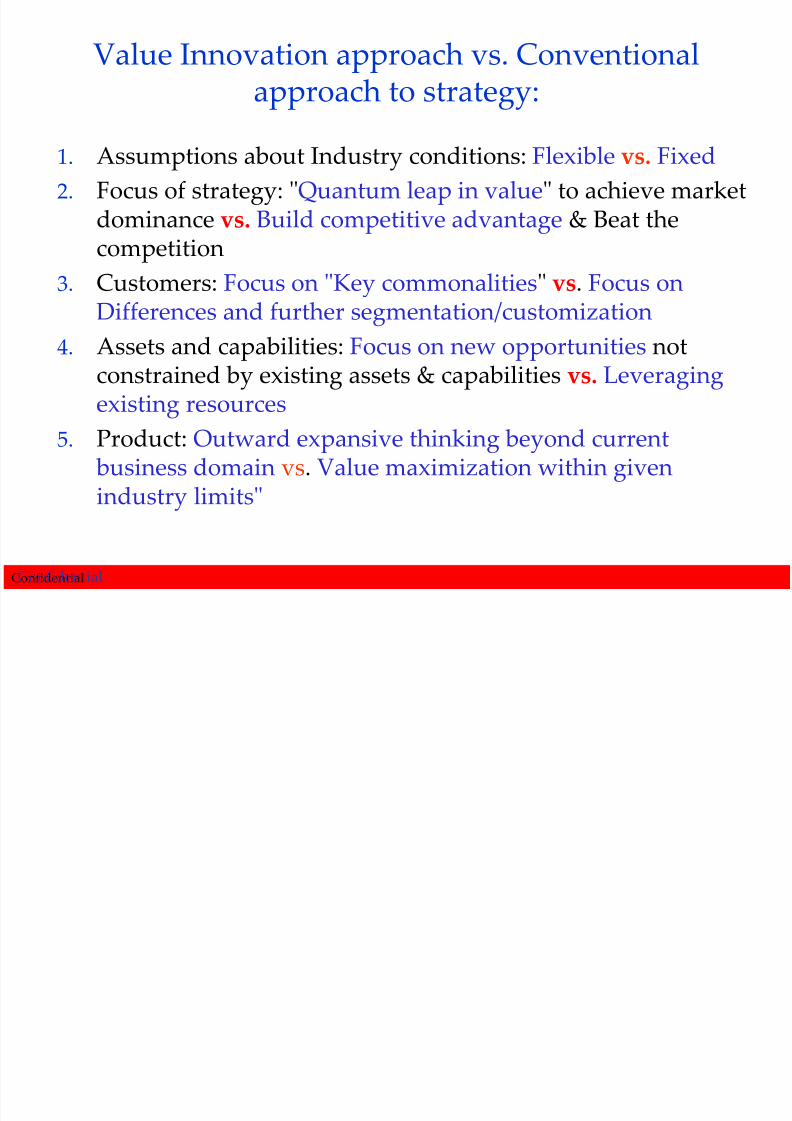

Value Innovation approach vs. Conventionalapproach to strategy:

1. Assumptions about Industry conditions: Flexible vs. Fixed

2. Focus of strategy: "Quantum leap in value" to achieve marketdominance vs. Build competitive advantage & Beat thecompetition

3. Customers: Focus on "Key commonalities" vs. Focus onDifferences and further segmentation/customization

4. Assets and capabilities: Focus on new opportunities notconstrained by existing assets & capabilities vs. Leveragingexisting resources

5. Product: Outward expansive thinking beyond current business domain vs. Value maximization within givenindustry limits"

Confidential

8/22/2019 BOS Session 8-Revsd

http://slidepdf.com/reader/full/bos-session-8-revsd 35/40

Confidential

Price corridor of the mass

Step 1 Identifying the price corridor of the mass. Understand the price

sensitivities of the consumers.

Look at products/services, which are offered outside the group oftraditional competitors. Identify the mass of target customers andwhat prices they are willing to pay.

The price corridor that captures the largest group of target customersis the price corridor of the mass.

Step 2: Specifying a level within the price corridor.

Determine how high a price can be set without inviting competition

from imitation products/services.

look at the degree to which the product/service is protected throughpatents or copyrights

look at the degree to which the company owns exclusive assets or corecapabilities, which can block imitation."

Confidential

8/22/2019 BOS Session 8-Revsd

http://slidepdf.com/reader/full/bos-session-8-revsd 36/40

Confidential

Some Comparisons of Different Models

Confidential

8/22/2019 BOS Session 8-Revsd

http://slidepdf.com/reader/full/bos-session-8-revsd 37/40

Confidential

BOS & Porter’s 5 Forces

Cost leadership

Operating within the industry structure and within theindustry definition; operate within a defined cluster orStrategic Groups.

• Focus & differentiation

• Draw Strategic Group Map and show how in BOS youneed to break free from the SG and look beyond thecurrent industry structures, how you need to make all

the competitors in the SG irrelevant by redefining youroperating parameters or evolving into a bundle of arecalibrated parameters that might result into a new

business design or a new product category altogether

Confidential

8/22/2019 BOS Session 8-Revsd

http://slidepdf.com/reader/full/bos-session-8-revsd 38/40

Confidential

BOS and Core Competencies

Does BOS challenge your existing corecompetencies, resources and capabilities?

Confidential

8/22/2019 BOS Session 8-Revsd

http://slidepdf.com/reader/full/bos-session-8-revsd 39/40

Confidential

BOS and Value Migration

When the value migrates from an established business to another business or company in theperiphery, what might be happening is that thatcompany might be creating a new business designthru a BOS strategy, that might be giving a bettervalue to your existing customers. Ex. (yellow tail) inthe US wine industry

Confidential

8/22/2019 BOS Session 8-Revsd

http://slidepdf.com/reader/full/bos-session-8-revsd 40/40

Wrap Up on Blue Ocean Strategy

Don’t bleed – stay out of Red Oceans and CreateYourself a Blue One!