Boost Your Business - slides

32

Company LOGO BOOST YOUR BUSINESS BOOST YOUR BUSINESS Colin Thompson Cavendish

Transcript of Boost Your Business - slides

Company

LOGO

BOOST YOUR BUSINESSBOOST YOUR BUSINESS

Colin Thompson

Cavendish

BOOST YOUR BUSINESSBOOST YOUR BUSINESS

1. We will be discussing `business`

2. Successful Implementation

3. Real Benefits

4. Success

5

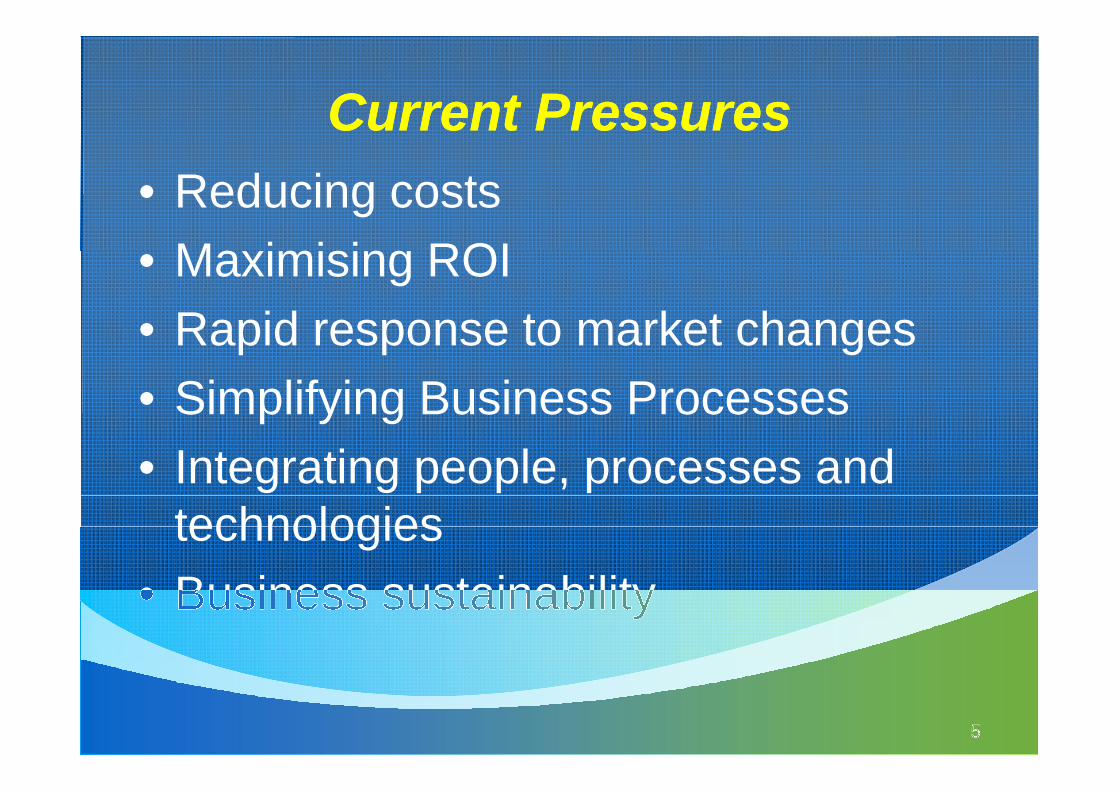

Current PressuresCurrent Pressures

• Reducing costs

• Maximising ROI

• Rapid response to market changes

• Simplifying Business Processes

• Integrating people, processes andtechnologies

• Business sustainability

NOTHING IN LIFE IS TO BE FEARED.IT IS ONLY TO BE UNDERSTOOD.

MADAME CURIE

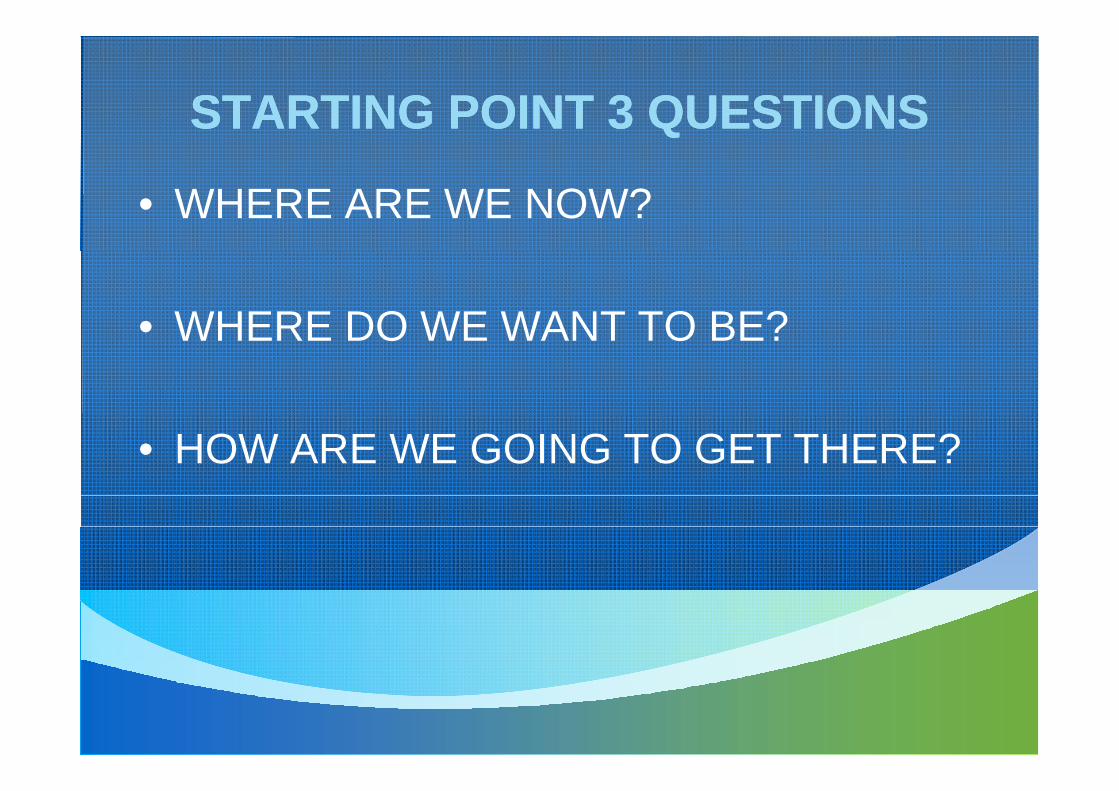

STARTING POINT 3 QUESTIONSSTARTING POINT 3 QUESTIONS

• WHERE ARE WE NOW?

• WHERE DO WE WANT TO BE?

• HOW ARE WE GOING TO GET THERE?

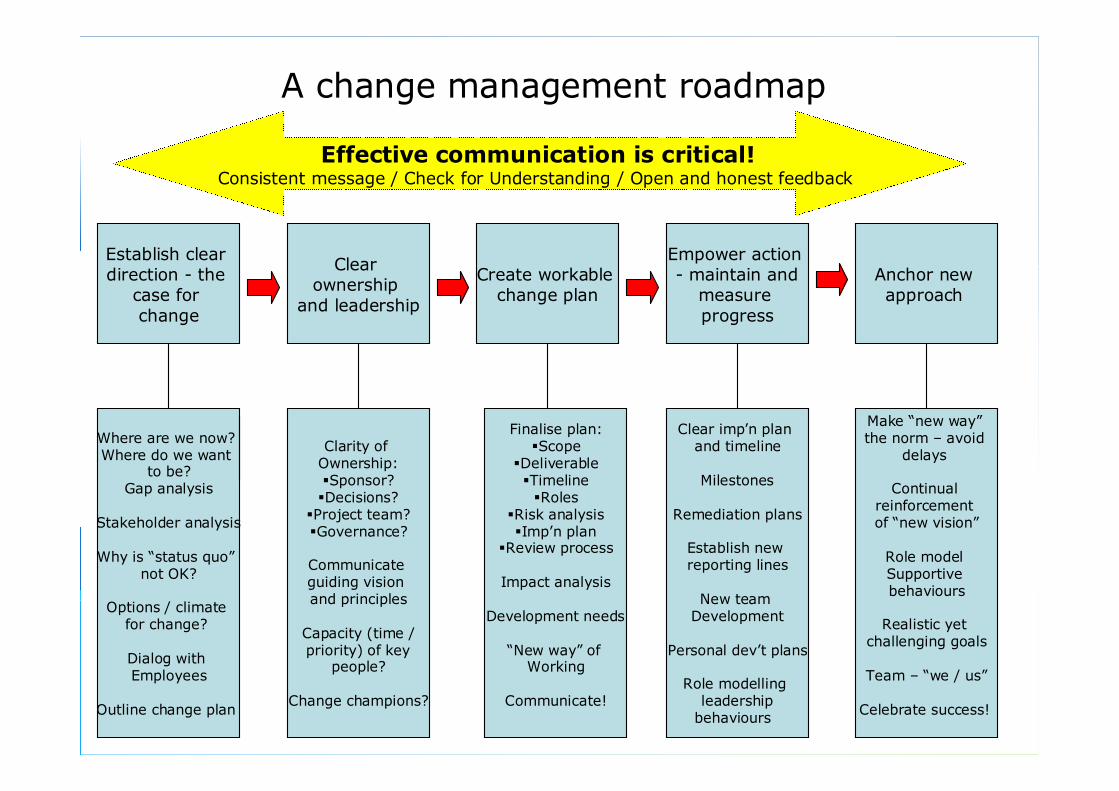

A change management roadmap

Clearownership

and leadership

Establish cleardirection - the

case forchange

Create workablechange plan

Empower action- maintain and

measureprogress

Anchor newapproach

Where are we now?Where do we want

to be?Gap analysis

Stakeholder analysis

Why is “status quo”not OK?

Options / climatefor change?

Dialog withEmployees

Outline change plan

Clarity ofOwnership:Sponsor?Decisions?Project team?Governance?

Communicateguiding visionand principles

Capacity (time /priority) of key

people?

Change champions?

Finalise plan:Scope

DeliverableTimelineRoles

Risk analysisImp’n plan

Review process

Impact analysis

Development needs

“New way” ofWorking

Communicate!

Clear imp’n planand timeline

Milestones

Remediation plans

Establish newreporting lines

New teamDevelopment

Personal dev’t plans

Role modellingleadership

behaviours

Make “new way”the norm – avoid

delays

Continualreinforcementof “new vision”

Role modelSupportivebehaviours

Realistic yetchallenging goals

Team – “we / us”

Celebrate success!

Effective communication is critical!Consistent message / Check for Understanding / Open and honest feedback

13

BOOST YOUR BUSINESSBOOST YOUR BUSINESS

STRATEGY

Setting a direction and objectives

for the business, based on an

understanding of the customers

it is targetting, and the

resources which will be needed

to accomplish them

TERMINOLOGY

STRATEGY

Setting a direction and objectives

for the business, based on an

understanding of the customers

it is targetting, and the

resources which will be needed

to accomplish them

OPERATIONS

The marketing, personnel and

other activities that need

to be planned and

implemented to put the

strategy into practice

TACTICS

The day to day decisions

involved in running the

business, such as

production planning

STRATEGY

Strategy provides you with a compass to steer your operational and tactical decisions in terms of a printing business

WHERE DO WE WANT TO BE ?

WHERE ARE WE NOW ?

WHAT HAVE WE TO DO TO GET THERE ?

WHAT IS THE PROCESS OF MAKING IT HAPPEN ?

WHY IS THE FUTURE BETTER THAN NOW ?

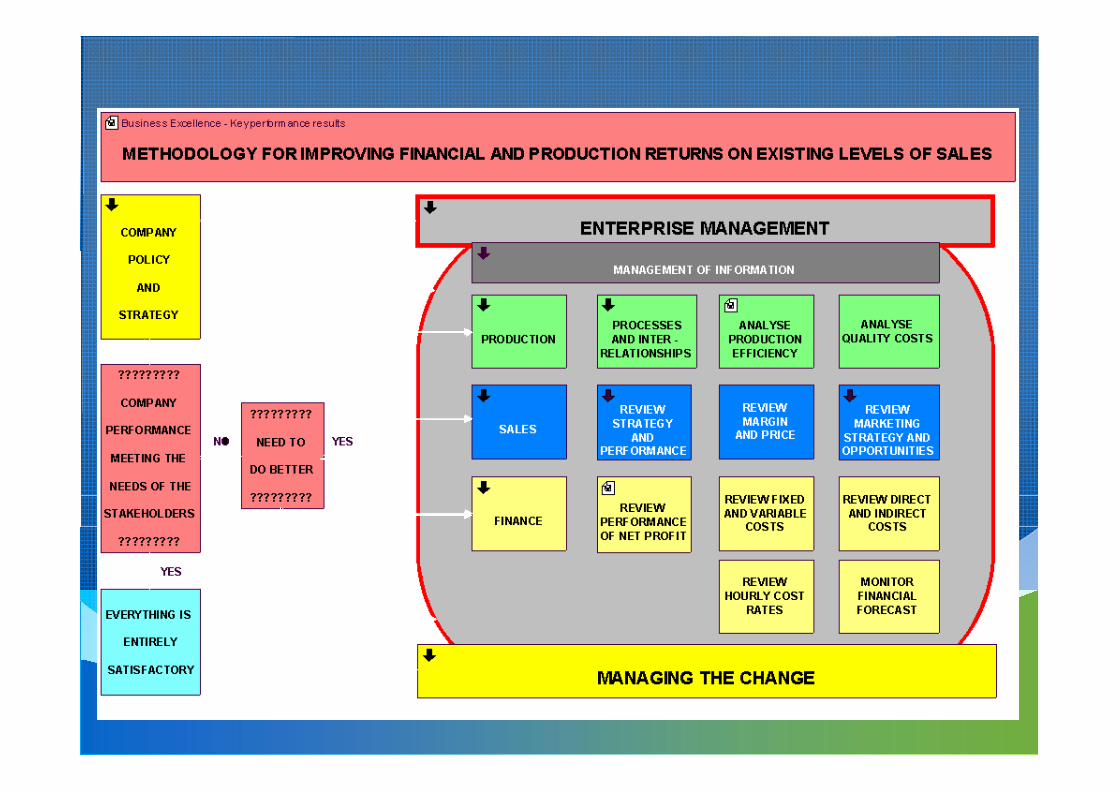

Business Excellence - Leadership / Policy and Strategy / Partnerships and Resources

The ChangeProcess

14

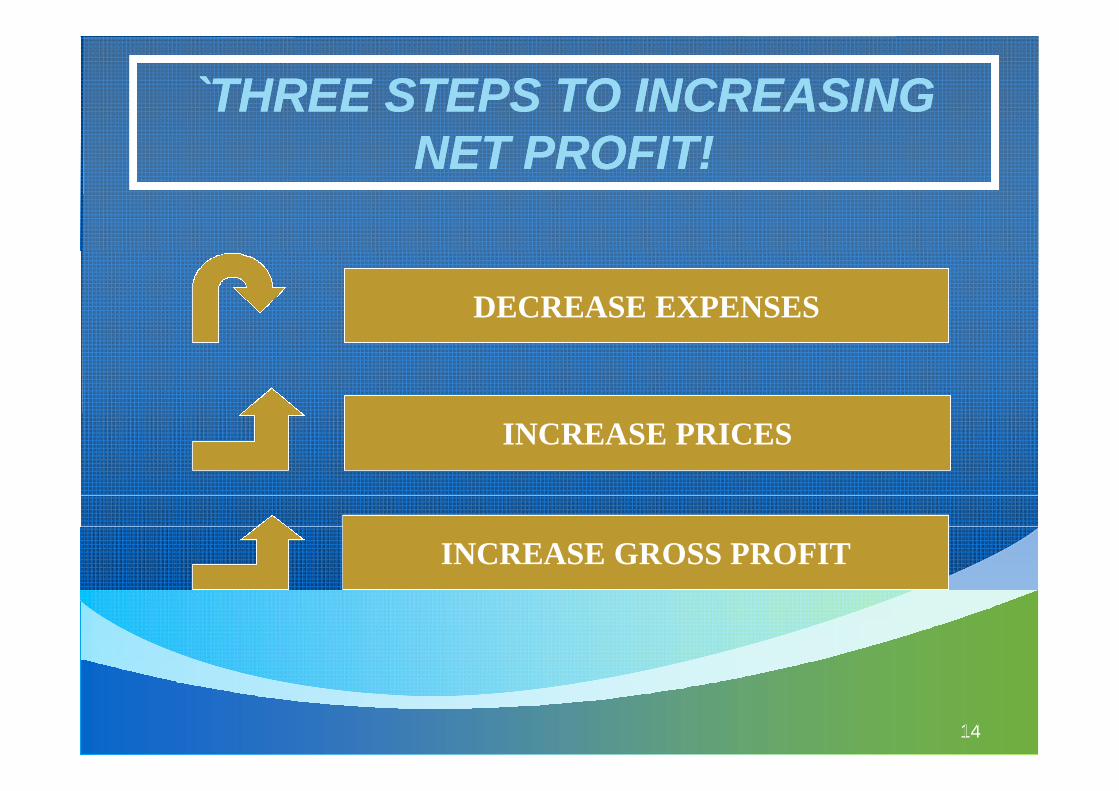

`THREE STEPS TO INCREASINGNET PROFIT!

`THREE STEPS TO INCREASINGNET PROFIT!

DECREASE EXPENSES

INCREASE PRICES

INCREASE GROSS PROFIT

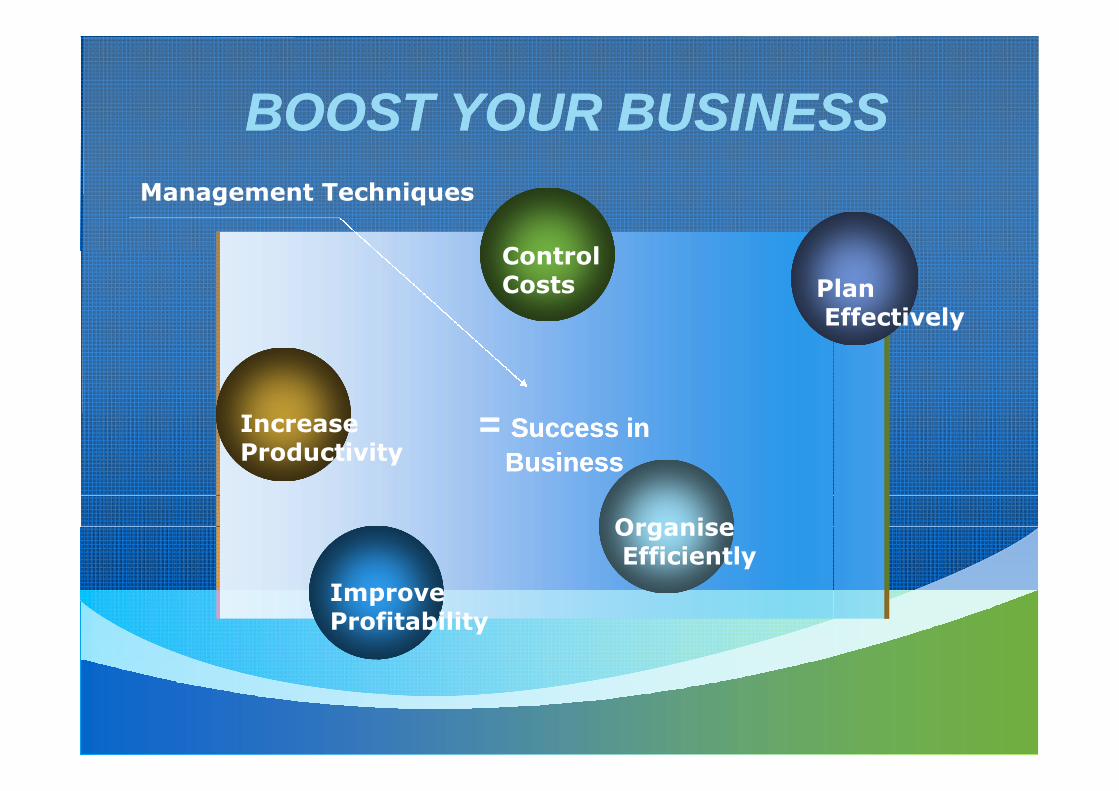

BOOST YOUR BUSINESSBOOST YOUR BUSINESS

IncreaseProductivity

ControlCosts Plan

Effectively

OrganiseEfficiently

ImproveProfitability

= Success in

Business

= Success in

Business

Management Techniques

16

The Print ArrowThe Print Arrow

Staff and Skills

ManagementInformation Systems

CUSTOMERS

TECHNOLOGY

Each contributes 20 % to the success of the business

Strategy

17

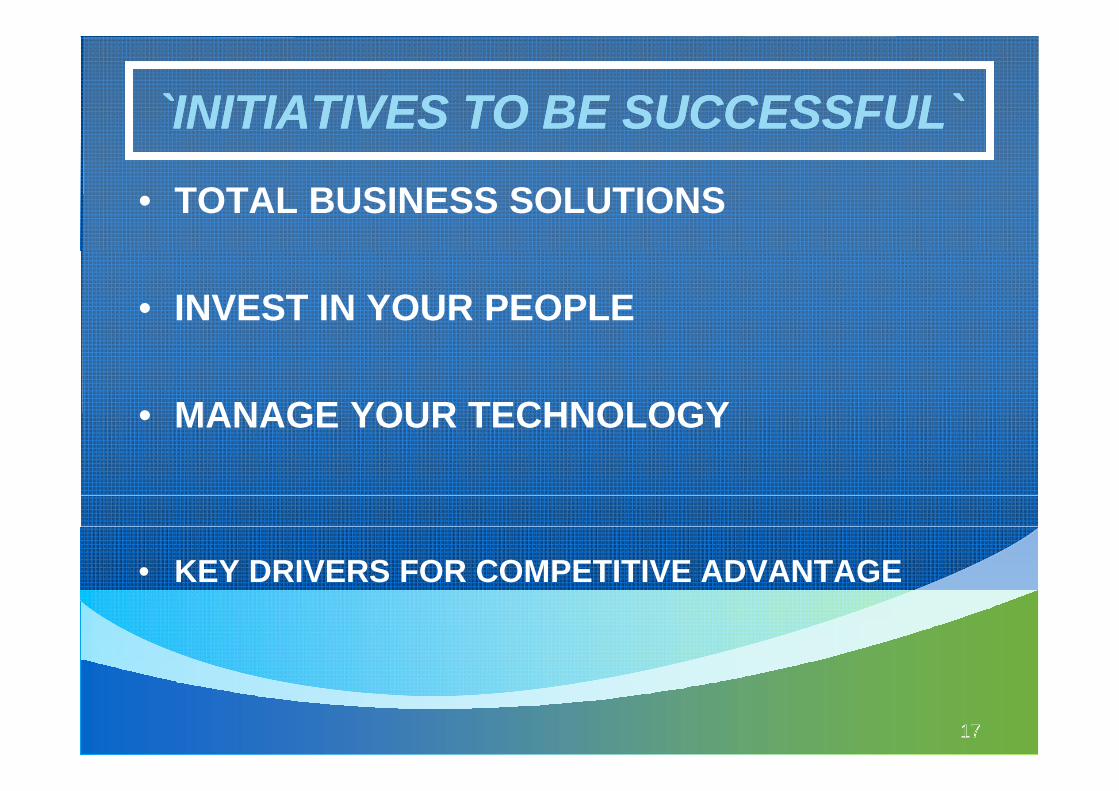

`INITIATIVES TO BE SUCCESSFUL``INITIATIVES TO BE SUCCESSFUL`

• TOTAL BUSINESS SOLUTIONS

• INVEST IN YOUR PEOPLE

• MANAGE YOUR TECHNOLOGY

• KEY DRIVERS FOR COMPETITIVE ADVANTAGE

18

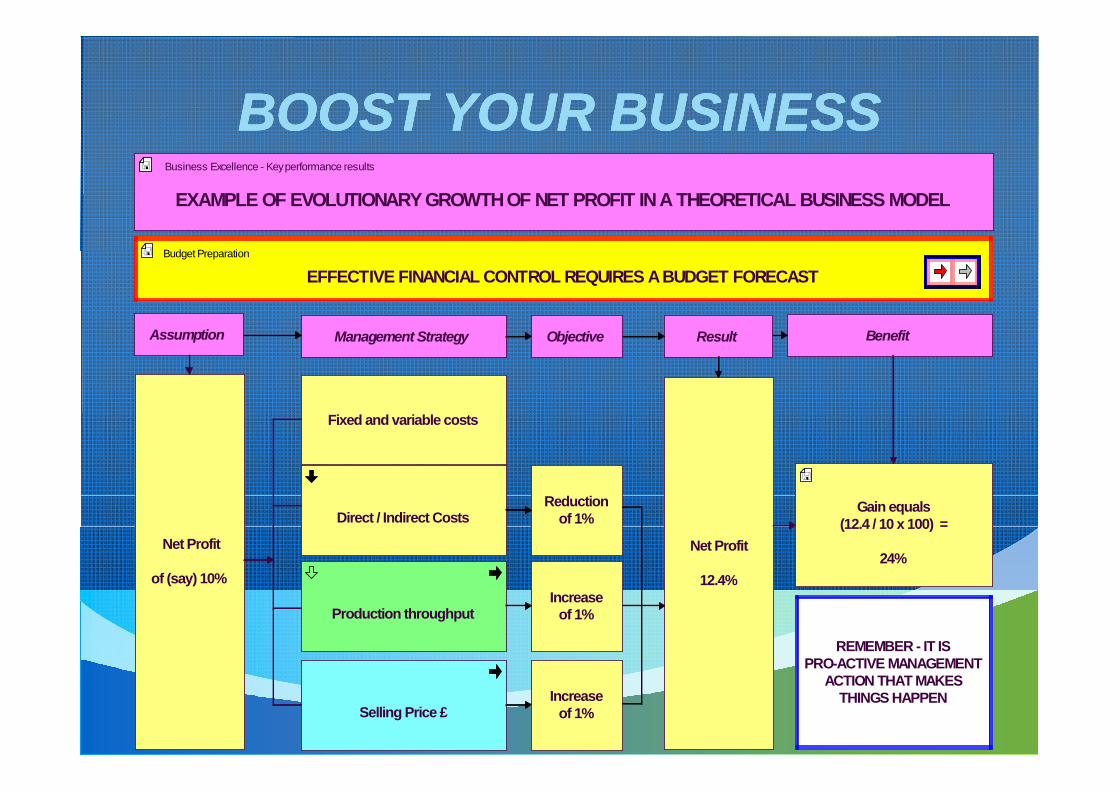

BOOST YOUR BUSINESSBOOST YOUR BUSINESSBOOST YOUR BUSINESSBOOST YOUR BUSINESS

Direct / Indirect Costs

Production throughput

Selling Price £

Reductionof 1%

Increaseof 1%

Increaseof 1%

Net Profit

of (say) 10%

Net Profit

12.4%

Gain equals(12.4 / 10 x 100) =

24%

EXAMPLE OF EVOLUTIONARYGROWTHOF NET PROFIT INA THEORETICAL BUSINESS MODEL

Assumption Management Strategy Objective Result Benefit

Fixed and variable costs

REMEMBER - IT ISPRO-ACTIVE MANAGEMENT

ACTION THAT MAKESTHINGS HAPPEN

Business Excellence - Keyperformance results

EFFECTIVE FINANCIAL CONTROL REQUIRES ABUDGET FORECAST

Budget Preparation

Reducing Costs and Driving ValueReducing Costs and Driving Value

Control

Improve

Analyse

MeasureDefine

DeliverROI

20

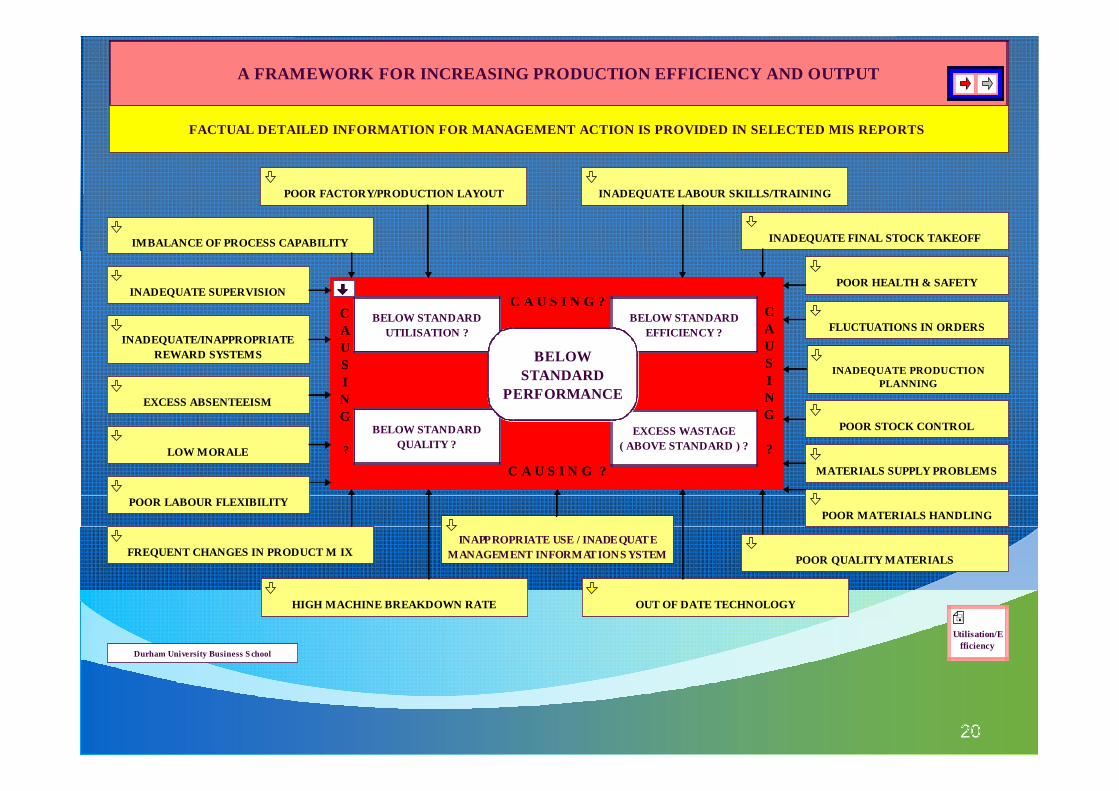

BELOW STANDARD

UTILISATION ?

BELOW STANDARD

QUALITY ?

BELOW STANDARD

EFFICIENCY ?

EXCESS WASTAGE

( ABOVE STANDARD ) ?

C A U S I N G ?

C A U S I N G ?

C

A

U

S

I

N

G

?

C

A

U

S

I

N

G

?

A FRAMEWORK FOR INCREASING PRODUCTION EFFICIENCY AND OUTPUT

BELOW

STANDARD

PERFORMANCE

FACTUAL DETAILED INFORMATION FOR MANAGEMENT ACTION IS PROVIDED IN SELECTED MIS REPORTS

Durham University Business S chool

FREQUENT CHANGES IN PRODUCT M IX

IMBALANCE OF PROCESS CAPABILITY

POOR FACTORY/PRODUCTION LAYOUT

INADEQUATE FINAL STOCK TAKEOFF

INADEQUATE SUPERVISION

INADEQUATE/INAPPROPRIATE

REWARD SYSTEMS

EXCESS ABSENTEEISM

LOW MORALE

POOR LABOUR FLEXIBILITY

HIGH MACHINE BREAKDOWN RATE OUT OF DATE TECHNOLOGY

POOR QUALITY MATERIALS

INADEQUATE LABOUR SKILLS/TRAINING

POOR HEALTH & SAFETY

FLUCTUATIONS IN ORDERS

POOR STOCK CONTROL

MATERIALS SUPPLY PROBLEMS

POOR MATERIALS HANDLING

Utilisation/E

fficiency

INADEQUATE PRODUCTION

PLANNING

INAPPROPRIATE USE / INADEQUATE

MANAGEMENT INFORMATIONS YSTEM

21

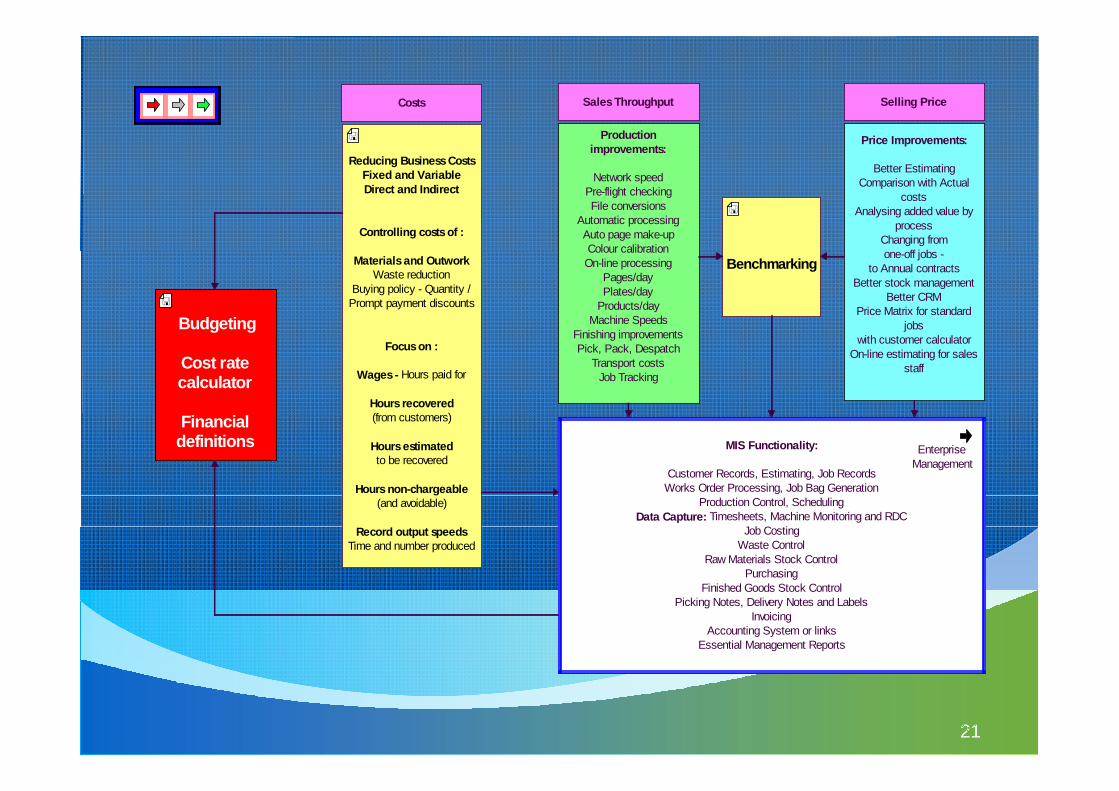

Productionimprovements:

Network speedPre-flight checkingFile conversions

Automatic processingAuto page make-upColour calibrationOn-line processing

Pages/dayPlates/day

Products/dayMachine Speeds

Finishing improvementsPick, Pack, Despatch

Transport costsJob Tracking

Price Improvements:

Better EstimatingComparison with Actual

costsAnalysing added value by

processChanging fromone-off jobs -

to Annual contractsBetter stock management

Better CRMPrice Matrix for standard

jobswith customer calculator

On-line estimating for salesstaff

MIS Functionality:

Customer Records, Estimating, Job RecordsWorks Order Processing, Job Bag Generation

Production Control, Scheduling

Data Capture: Timesheets, Machine Monitoring and RDCJob Costing

Waste ControlRaw Materials Stock Control

PurchasingFinished Goods Stock Control

Picking Notes, Delivery Notes and LabelsInvoicing

Accounting System or linksEssential Management Reports

Budgeting

Cost ratecalculator

Financialdefinitions

Costs Sales Throughput Selling Price

Benchmarking

Reducing BusinessCostsFixed and VariableDirect and Indirect

Controlling costsof :

Materialsand OutworkWaste reduction

Buying policy - Quantity /Prompt payment discounts

Focuson :

Wages- Hours paid for

Hours recovered(from customers)

Hoursestimatedto be recovered

Hours non-chargeable(and avoidable)

Record output speedsTime and number produced

EnterpriseManagement

3/31/2010 22

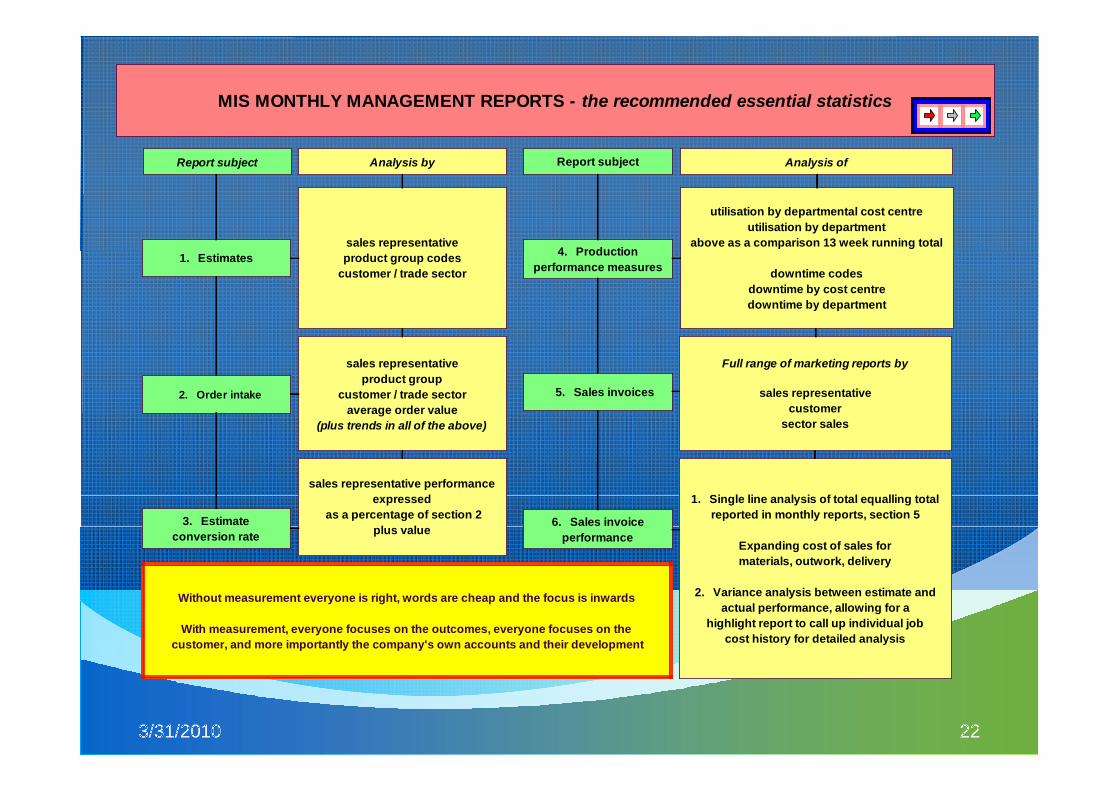

MIS MONTHLY MANAGEMENT REPORTS - the recommended essential statistics

Report subject Analysis by Report subject Analysis of

1. Estimates

2. Order intake

3. Estimate

conversion rate

4. Production

performance measures

5. Sales invoices

6. Sales invoice

performance

sales representative

product group codes

customer / trade sector

sales representative

product group

customer / trade sector

average order value

(plus trends in all of the above)

sales representative performance

expressed

as a percentage of section 2

plus value

utilisation by departmental cost centre

utilisation by department

above as a comparison 13 week running total

downtime codes

downtime by cost centre

downtime by department

Full range of marketing reports by

sales representative

customer

sector sales

1. Single line analysis of total equalling total

reported in monthly reports, section 5

Expanding cost of sales for

materials, outwork, delivery

2. Variance analysis between estimate and

actual performance, allowing for a

highlight report to call up individual job

cost history for detailed analysis

Without measurement everyone is right, words are cheap and the focus is inwards

With measurement, everyone focuses on the outcomes, everyone focuses on the

customer, and more importantly the company's own accounts and their development

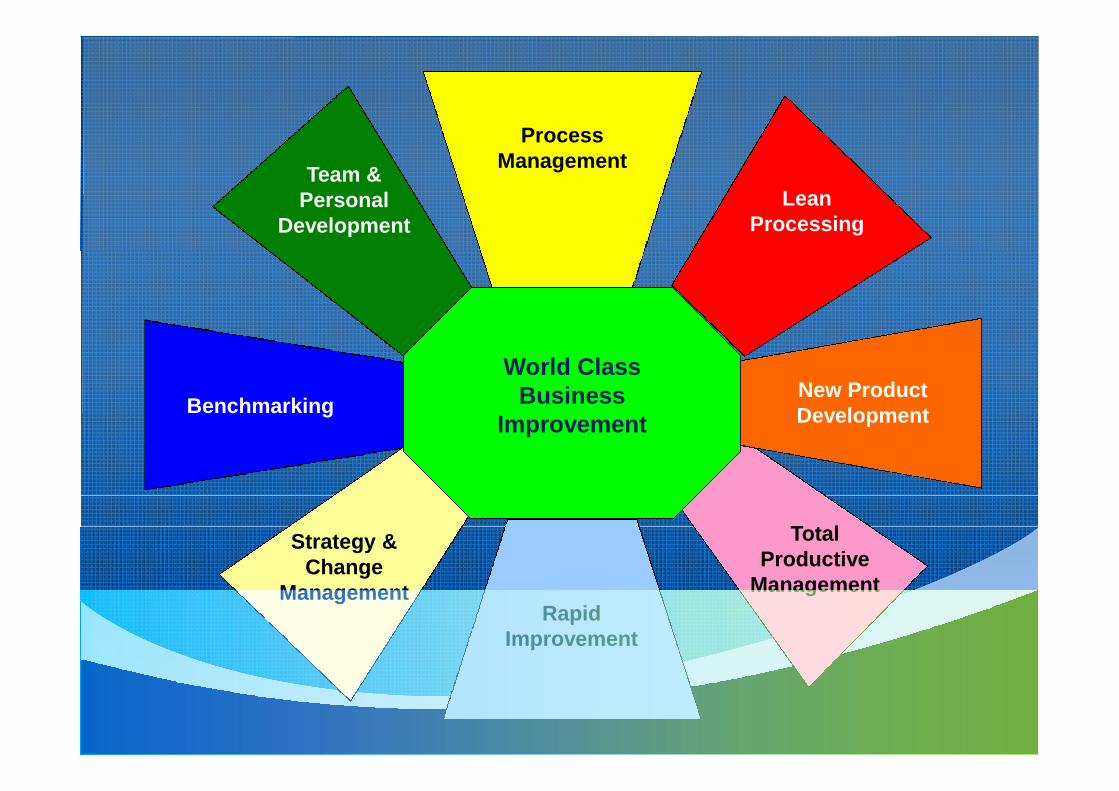

ProcessManagement

World ClassBusiness

Improvement

RapidImprovement

Strategy &Change

Management

TotalProductive

Management

BenchmarkingNew ProductDevelopment

Team &Personal

Development

LeanProcessing

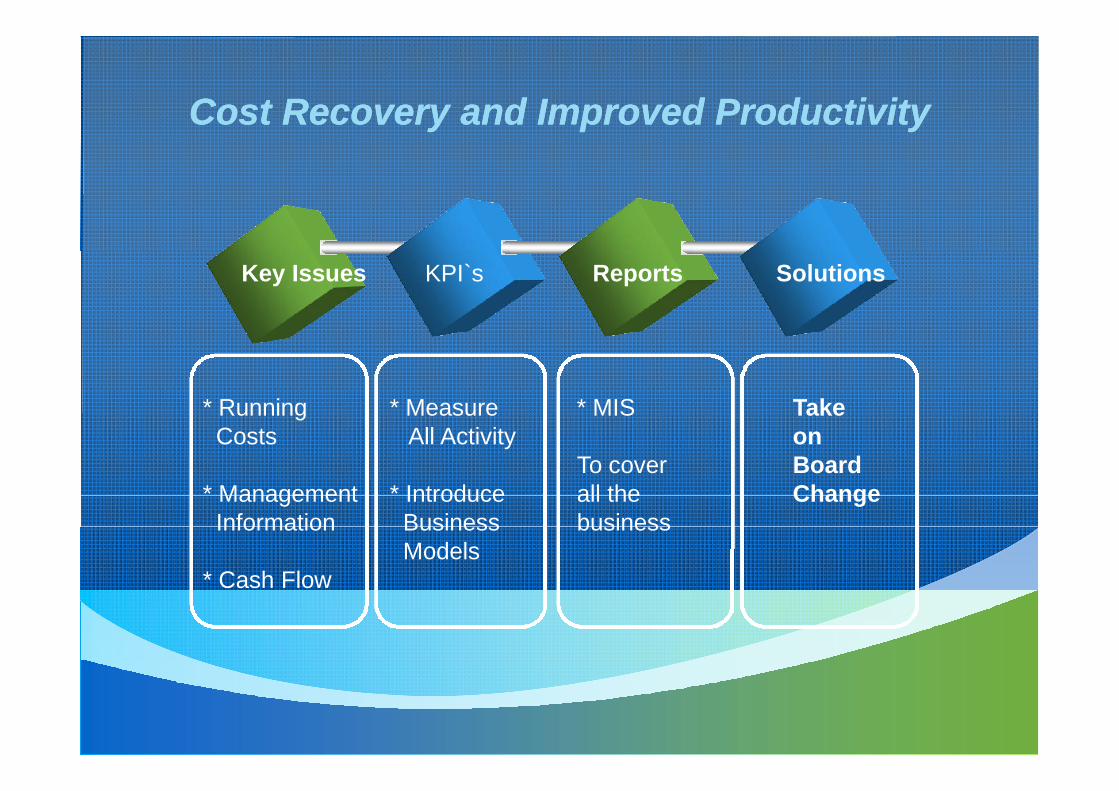

Cost Recovery and Improved ProductivityCost Recovery and Improved Productivity

Key Issues KPI`s Reports Solutions

* RunningCosts

* ManagementInformation

* Cash Flow

* MeasureAll Activity

* IntroduceBusinessModels

* MIS

To coverall thebusiness

TakeonBoardChange

BOOST YOUR BUSINESSBOOST YOUR BUSINESS

Successful Business

People ProductivityPerformance Profit

COMING TOGETHER IS A BEGINNING;

KEEPING TOGETHER IS PROCESS;

WORKING TOGETHER IS SUCCESS

HENRY FORD

28

WE ALL NEED A HELPING HAND TOBE SUCCESSFUL!

WE ALL NEED A HELPING HAND TOBE SUCCESSFUL!

• SUCCESS IS A JOURNEY,NOT A DESTINATION

Who

has

the

first question?

`TO THE SUCCESSFUL FUTURE``TO THE SUCCESSFUL FUTURE`

• THANK YOU FOR THE OPPORTUNITY TODAY

• COLIN THOMPSON

• www.cavendish-mr.org.uk

COPYRIGHTCOLIN THOMPSON

COPYRIGHTCOLIN THOMPSON

• THIS WORK IS PROTECTED BY COPYRIGHT. THE RIGHTS COVEREDBY THIS ARE RESERVED, IN PARTICULAR THOSE OF TRANSLATING,REPRINTING, RADIO BROADCASTING, REPRODUCTION BY PHOTO-MECHANICAL OR SIMILAR MEANS AS WELL AS THE STORAGE ANDEVALUATION IN DATA PROCESSING INSTALLATIONS EVEN IF ONLYEXTRACTS ARE USED. SHOULD INDIVIDUAL COPIES FORCOMMERCIAL PURPOSES BE MADE WITH WRITTEN CONSENT OFTHE PUBLISHERS THEN A REMITTANCE SHALL BE GIVEN TO THEPUBLISHERS IN ACCORDANCE WITH SECTION 54,PARA.2 OF THECOPYRIGHT LAW. THE PUBLISHERS WILL PROVIDE INFORMATIONON THE AMOUNT OF THIS REMITTANCE.